Blog

05/23/2024 - Commodity Culture – Commodities Have ‘Never, Ever’ Been More Undervalued Than Today: Leigh Goehring

05/23/2024 - Commodity Culture – Commodities Have ‘Never, Ever’ Been More Undervalued Than Today: Leigh Goehring

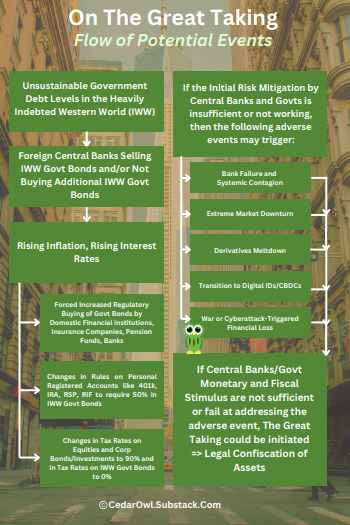

05/23/2024 - CedarOwl – The Great Taking: How Could It Happen & What Can We Do to Slow The Momentum of Becoming At-Risk?

Become a free subscriber by entering your email address in the form below:

05/17/2024 - The Roundtable Insight Vision Series – Charles Hugh Smith on Gold and What Currency Systems Make Sense

05/16/2024 - The Roundtable Insight – Sam Perry, Tobias Harris and Yra Harris on Japan at the Crossroads

05/03/2024 - Adam Rozencwajg on The Impact of New Copper Technologies

“Nearly all copper demand growth came from the non-OECD world … Given its population of 275 mm, even if it takes another 15 years, assuming 5% economic growth, we expect Indonesia will consume over 1 mm tonnes annually – five times the current rate .. ”

04/25/2024 - CedarOwl – How We are Investing in Artificial Intelligence (AI) – “Picks and Shovels”

Enter your email to become a free subscriber below:

04/22/2024 - FamilyOffice Podcast with Leon Cooperman

04/22/2024 - CedarOwl – Full Special Report on Dr. Marc Faber

Link here to the Full Report on Dr. Marc Faber for free

Become a free subscriber by entering your email address in the form below:

04/18/2024 - Get to Know the CedarOwl

Check out our latest posting – Get to Know the CedarOwl … .. learn about how and why we take an approach based on the Principles of the Austrian School of Economics .. also learn the 4 Principles of Market Environmentalism – what these principles are and how they can be used to identify Positive Ideas to help the environment that make not only environmental sense but also financial sense and economic sense! .. also be sure to read the latest views and thoughts of one of our top 10 Most Admired Advisors (MAA) – Dr. Marc Faber – posting will be published tomorrow Friday Apr 19 at 3pm ET and be available fully free to all subscribers!

04/17/2024 - Louis-Vincent Gave and David Hay on the Coming Rebound of Inflation and Market Implications

04/17/2024 - CedarOwl – Russell Napier. Twenty One Lessons from Financial History for the Way We Live Now.

April 15, 2024

This is a timeless lecture by Russell Napier. It is also applicable to the current economic and investing environment. Russell goes through twenty-one lessons from financial history. Download all the slides – link here.

- Spend as much time analyzing supply as you spend analyzing demand – the China impact.

- There is no relationship between GDP growth and the return from equities – price is what you pay and value is what you get.

- Pepper’s law – estimate how long the unsustainable can be sustained – double it and take off a month.

- ‘Never, ever think about anything else when you should be thinking about incentives’- Charlie Munger.

- Governments like markets only when they deliver the prices they want governments do suspend market prices.

- The ratio of corporate profits to GDP ratio must mean revert in a free society- one way to do this is inflation.

- In assessing the appropriateness of monetary policy assess both the price of money and the quantity of money – banks make money.

- The most dangerous form of speculation is the search for yield- ‘John Bull can stand many things but he cannot stand 2%’ Walter Bagehot.

- The real danger for investors from populism depends upon the strength of the constitution and the rule of law.

- The countries most likely to default on their debt are those that have defaulted on their debt- institutions count.

- High equity valuations fall slowly when the surprise is inflation and quickly when it is deflation – our current repression creates a slow decline.

- Never buy emerging market equities if the exchange rate is overvalued- an exchange rate policy is a monetary policy.

- Tourism is the best guide to whether an exchange rate is over-valued or under-valued always visit to Rockefeller Center at Christmas.

- Always buy equites below 10X CAPE unless the future holds – communism, war or a surrender of monetary independence with an overvalued exchange rate.

- Democracy is more suited to the operation of capital controls than the free movement of capital.

- When private savings are exhausted monetization of government debt and high inflation/hyperinflation follow – savings are not yet exhausted if conscripted.

- Technology never ultimately defeats inflation.

- Monetary systems fail about every 30 years – the rules of the old system leave a legacy of bad habits for those in a new system.

- Money is almost always in disequilibrium.

- Never trust a forecast with a decimal point-especially your own.

- Extrapolation is the opiate of the people.

- CedarOwl Commentary – Some interesting points and observations:

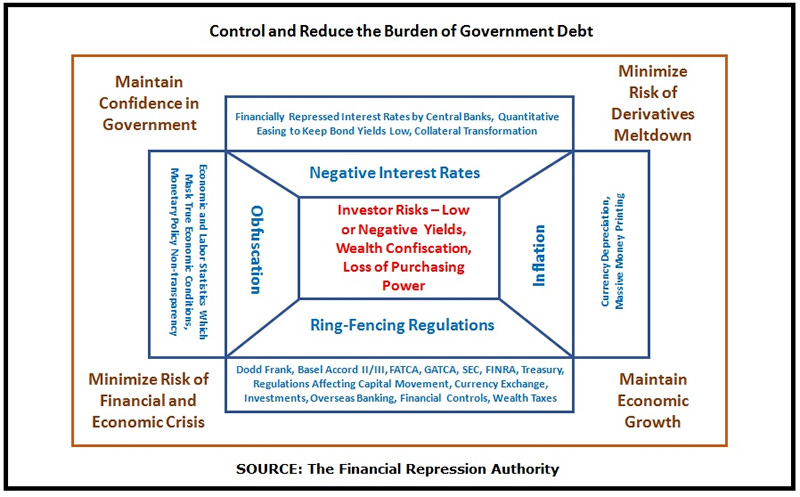

- Russell’s biggest theme is on the risks of financial repression – in many of the lessons he discusses in this presentation, he provides ideas to minimize these risks – jurisdictional-focused investing, diversification in asset classes, holding some gold and certain equities to preserve purchasing power, investing in jurisdictions where the rule of law and respect for property rights is strong and maintained, emphasizing equities versus bonds to minimize capital being forced to fund unsustainable reckless-spending governments.

- Thinks best to look for undervalued equities in emerging markets where currencies are not overvalued, instead of holding stagnant developed-world overvalued equities likely to go no where (or even losing purchasing power in real terms) in a manner similar to what happened to equities between 1966 to 1982.

- Sees a massive disequilibrium, a result of the monetary change in the world today – will likely result in liquidity going to emerging markets, driving emerging market currencies stronger in general. Advises to look for value-based equities in emerging markets instead of growth equities in the indebted western world.

- Observes on the variation of the famous Karl Marx quote of “Religion is the opiate of the people” that extrapolation is really the danger as the opiate of the people. Also known as recent bias. Just because the western world countries have led economic growth and enhancement in the standard of living over the past several decades since World War II – does not mean that this trend will go on forever. The western world countries are now heavily indebted, finding it increasingly difficult to even make the minimum payments on servicing their existing unsustainable government debt levels.

Become a free subscriber by entering your email address in the form below:

04/11/2024 - CedarOwl – Dividend-Paying Companies We Invest In – April 2024 Edition

Become a free subscriber by entering your email address in the form below.

Here are just a few of the crowning qualifications that gave us the green-light to feature today’s pick on the first of our monthly series:

- This company currently pays about 15% dividend yields.(from stockcharts.com and investing.com)

- In addition to dividend distributions, this company shows a potential for capital appreciation, making them potentially promising for both short and long-term strategies.

- This company’s business model is currently based on assets in an underinvested, undervalued jurisdiction.

- This company deploys great sustainability programs and initiatives.

- This company strives towards international-based environmental certification on their assets.

- This company is currently leveraging digitalization technologies for growth and operational efficiencies, supportive of UN SDGs 8, 9 & 16.

- This company has over 20 years of proven, stable growth since it started in 1991.

- This company is publicly listed on two exchanges for ease of access.

Next up, let’s introduce today’s company pick and explore an up-to-date fundamental and technical analysis on its equity share price. Introducing …

Become a free subscriber by entering your email address in the form below:

04/08/2024 - The Roundtable Insight – Legendary Investors Chris Wood and Yra Harris on Gold, Geo-Political Risks, and the Global Financial Markets

Download the podcast in voice format MP3 here

04/05/2024 - Larry McDonald on MacroVoices – How To Listen When Markets Speak

04/05/2024 - The Roundtable Insight – Charles Hugh Smith on Four Thematic Challenges Causing Economic and Social Dysfunction – and Solutions

04/05/2024 - CedarOwl: Most Admired Advisors (MAA) Views and Perspective on Finance, the Economy & Global Markets – April 2024

04/04/2024 - Adam Rozencwajg – $15,000 Gold, $125 Uranium, $0 Lithium – on Resource Talks

04/04/2024 - CedarOwl – Introducing the Most Admired Advisors (MAA) – views and perspective of our Top 10 financial advisors, fund and asset managers

If you’ve been searching for a trustworthy monthly pocketbook of trends and insights on the economy and financial markets, this new, recurring segment is for you.

Introducing ‘Most Admired Advisors’ (MAA) by CedarOwl – a monthly report featuring a global top-10 roster of financial advisors, fund and asset managers. We source and cite a distillation of their current, relevant sentiments on trends in the economy and financial markets as a reliable source of insights for our readers.

Our MAA roster is reassessed monthly and stacked against our values and analysis models so you can enjoy an ever-fresh perspective on our category’s thought leadership.

For each economist or manager, look forward to fulsome summary points and observations on their views and perspective on the economy, the financial markets, and their investment ideas.

All taken from publicly linked sources across the open web, including our partners at FRA Roundtable Insight Podcast.

We do the assessment, research and compilation work as a service to you.

Sign up below to become a free subscriber to CedarOwl:

04/01/2024 - CedarOwl – Bloomberg Article: How the Nuclear Fusion Market Could Achieve at $40 Trillion Valuation

“Nuclear Fusion as a solution towards the sustainable, green vision that the world has been striving towards has been severely downplayed and relatively unknown. Yet, key players in the energy sector are advancing nuclear fusion technologies, preparing the world for its commercialization as an energy source, presenting potentially enormous investment opportunities. Does this make your hair stand on end? It should.

Read How nuclear fusion market could achieve a $40 trillion valuation, a Bloomberg report. ..

In today’s posting, we explore the current opportunity presented by the advancements in nuclear fusion as an energy source.

- What is nuclear fusion, and why has it been downplayed?

- Does nuclear fusion make environmental, financial and economic sense?

- What are our nuclear fusion investment strategies that leverage key players advancing the technologies, that can help us attain outperforming return on investment (ROI)?”

Link Here to the CedarOwl substack posting on nuclear fusion

03/30/2024 - Frank Giustra & Pierre Lassonde on Gold, Macroeconomics, Geopolitical Threats, and Why Canada is Failing