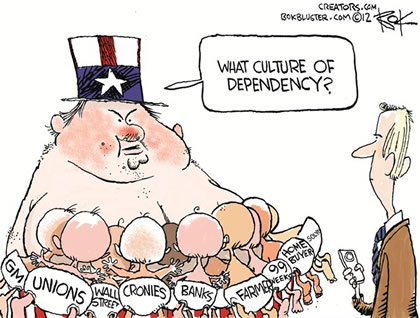

BUT DESTROYED THE US MIDDLE CLASS

FINANCIAL REPRESSION

Accelerated the Decline of America

AMERICA Now A Two Class Society

“Haves & Have Nots”

& Maybe More Concerning

A Culture of

“SOCIAL DEPENDENCY”

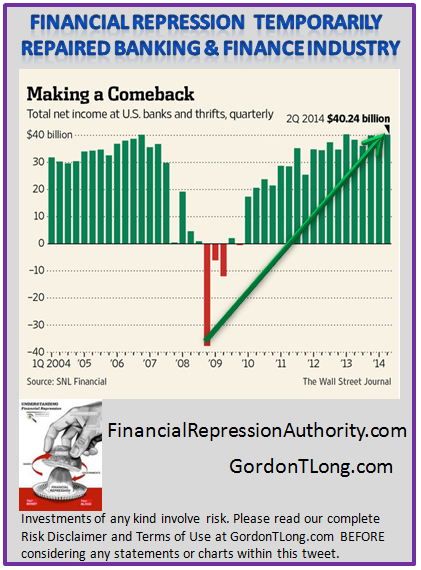

08/16/2014 - FINANCIAL REPRESSION SAVED THE BANKS

08/16/2014 - FINANCIAL REPRESSION SAVED THE BANKS

BUT DESTROYED THE US MIDDLE CLASS

FINANCIAL REPRESSION

Accelerated the Decline of America

AMERICA Now A Two Class Society

“Haves & Have Nots”

& Maybe More Concerning

A Culture of

“SOCIAL DEPENDENCY”

08/11/2014 - Federal Reserve & Congress Talk “ENHANCED PRUDENTIAL STANDARDS”

CENTRAL PLANNING & CONTROL

Moving towards Control of YOUR Pensions

through Control of Insurance Industry

Other non-banks to face ‘designation’ as “systemic risks to the financial system”

The Fed has insisted that the Dodd-Frank financial reform bill forced it to apply bank capital standards to non-banks. In response, the Senate recently passed a bill that would give the Fed the room to apply capital standards that are tailored for the insurance industry

Life insurer MetLife is waiting to see if it will be designated this year, while its smaller rival

Prudential Financial was deemed a systemic risk last September.

LARGEST ASSET MANAGERS: On July 31, FSOC decided for now to lift the threat of systemic risk designations for the largest asset managers, but said it would focus on the industry’s products and activities.

PRIVATE EQUITY & HEDGE FUNDS: The review of asset managers came after an FSOC-commissioned report on the industry, which also said it was reviewing private equity and hedge funds, prompting predictions that those sectors could be next on the council’s agenda.

Fed gives preview of future non-bank scrutiny 08-11-14 FT

08/10/2014 - DON’T EXPECT SOCIAL SECURITY TO BE THERE TO SAVE YOU!

THERE ARE

$84T OF UNFUNDED RETIREMENT ENTITLEMENTS

US is Bankrupt: $89.5 Trillion in US Liabilities vs. $82 Trillion in Household Net Worth & The Gap is Growing. We Now Await the Nature of the Cramdown 08-04-14 Chris Hamilton via Charles Biderman TrimTabs’ blog, via ZH

America’s Hidden Credit Card Bill Laurence Kotlikoff: The Government Should Report Its ‘Fiscal Gap,’ Not Just Official Debts LAURENCE J. KOTLIKOFF

08/09/2014 - THE GOVERNMENT’S GAME OF “ENTRAPMENT” via FINANCIAL REPRESSION

FINANCIAL REPRESSION

Initially Forced Fund Managers Into

Junk Bond Yields

THE SET-UP

STEP 1: EXCESSIVE LIQUIDITY

STEP 2: EXCESSIVE RISK TAKING

STEP 3: BAD MONEY FORCES OUT GOOD MONEY

NOW THE SQUEEZE

STEP 4: THE PANIC

THE FLIGHT TO PERCEIVED SAFETY

STEP 5: ACHIEVE GOAL -> CHEAPER GOVERNMENT FINANCING COSTS

“Wolf Richter’s essay posted on Stockman’s Contra Corner sees junk bond investors running for the hills, “But there no hills” .. In the latest week, investors yanked $7.1 billion out of junk bond funds, a record amount, according to Lipper – this exodus has been going on since early July, junk bond prices have dropped, yields have jumped from all-time lows, yield spreads have suddenly widened .. “After having been inflated to dizzying proportions, the junk-bond bubble has been pricked. And the hot air is hissing out of it .. Neither glorious economic fundamentals nor corporate financial engineering caused investors to pile helter-skelter, eyes-closed into this high-yield junk. The Fed’s financial repression did .. The Fed has made it impossible for yield investors to earn a noticeable return above the rate of inflation with low-risk paper. So they chased after whatever yield they could get and they held their noses and ventured deeper and deeper into a swamp they normally wouldn’t want to be in. They did that in unison. The demand they created for junk drove up valuations and repressed yields further into low-yield purgatory, where potential losses are huge and potential gains very meager. Exactly as the Fed had wanted them to .. But the Fed has changed its mind”CliffKule.com

08/08/2014 - We have reached the point where Keynesian Central Planning manipulations are now stifling Innovation & Growth

“.. we have moved far away from free markets. The authorities have established endless ‘detours’ (via policies such as Financial Repression) that restrict free market capitalism. We have reached the point that all the manipulations interfere with the innovations & growth that free markets would produce. We are living through ‘Capitulation of all the Manipulation’ (the ‘Keynesian Endpoint’). The manipulations of the last 5 or 6 decades have stifled the ‘invisible hand’ that makes free markets superior to centrally planned economies. In other words, Adam Smith has been defeated. Our system is more like Karl Marx’s, but not in the way that most people think. A small group of wealthy ‘capitalists’ ended free markets when they were awarded monopoly control over the creation & distribution of the money. They called their group ‘Federal’ even though it is no more Federal & just as private as Federal Express. They used the word ‘Reserve’ even though they create money from no reserves at all. Their government contract to control America’s money was the beginning of a long slippery slope away from free market capitalism to a centrally planned economy. Think about it: Free Markets When Money Is Privately Controlled? That is an OXYMORONIC. That is our system & it is OXYMORONIC.” CliffKule.com

FINANCIAL REPRESSION’S REGULATORY DETOURS ARE INCREASINGLY TAKING US AWAY FROM THE ‘SELF CORRECTING” POWER OF FREE MARKETS

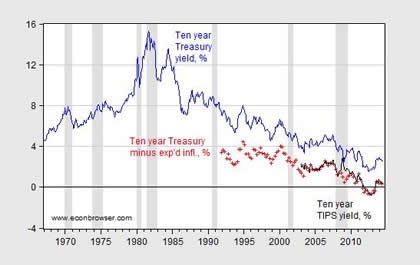

08/07/2014 - REAL GOVERNMENT BORROWING COSTS CLOSE TO ZERO

FINANCIAL REPRESSION

STRIPS SAVERS, PENSIONERS,

PRUDENTIAL INVESTING &

REAL DISPOSABLE INCOME

TO FINANCE GOVERNMENT SPENDING

Ten year constant maturity Treasury yields (blue), ten year constant maturity yields minus ten year (median) expected inflation (red +), and ten year constant maturity TIPS (black). NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, Survey of Professional Forecasters, and author’s calculations.

08/06/2014 - Central-Planners Herd Money Market Funds Into Government Financing

“We’re definitely worried about breaking the buck,” Verett Mims, assistant treasurer at Chicago-based Boeing, said in a telephone interview on July 30. “That’s our biggest problem, the notion of principal preservation.”

“one of the biggest winners in the push to make money-market funds safer for investors is turning out to be none other than the U.S. Government.” (no surprise to the Financial Repression Authority!!!)

Rules adopted by regulators last month will require money funds that invest in riskier assets to abandon their traditional $1 share-price floor and disclose daily changes in value. For companies that use the funds like bank accounts, the prospect of prices falling below $1 may prompt them to shift their cash into the shortest-term Treasuries, creating as much as $500 billion of demand in two years, according to Bank of America Corp.

“Whether investors move into government institutional money-market funds or just buy securities themselves, there will be a large demand” for short-dated debt, Jim Lee, head of U.S. derivatives strategy at Royal Bank of Scotland Group Plc’s capital markets unit in Stamford, Connecticut, said in a telephone interview on July 28. “That will lower yields.”

He predicts investors may shift as much as $350 billion to money-market funds that invest only in government debt.

Bank of America, which also has hated Treasurys as an asset class since mid-2013, also chimes in:

Investors using prime funds to manage their idle cash may find floating prices an unnecessary risk when differences in fund rates are so minimal, said Brian Smedley, an interest-rate strategist at Bank of America in New York. He estimates about half the $964 billion held in institutional prime funds will flow into those that only invest in government debt and yield about 0.013 percentage point less, before the new rules become fully effective in 2016.

The Fed will continue herding investors as long as it takes: first out of the money market funds, then out of bond funds, until the only possible investment product remains triple digit P/E stocks, and everyone is all the biggest market ponzi bubble of all time.

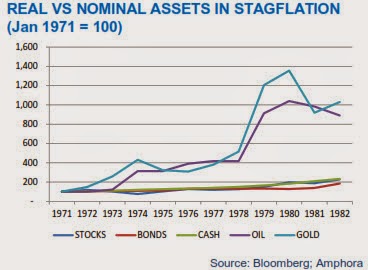

08/04/2014 - The Amphora Report Investing In Financial Repression

READ: Amphora Report

In his latest report, John Butler sees a long-term stagflationary environment similar to the 1970s but it could be worse .. sees stagflation as the inevitable result of the aggressive, neo-Keynesian policy responses to the global financial crisis .. this report discusses the causes, symptoms & financial market consequences of the new stagflation .. “Stagflation is a hostile environment for investors .. Keynesian policies require that the public sector siphon off resources from the private sector, thereby reducing the ability of private agents to generate economic profits. So-called ‘financial repression’, a more overt seizure of private resources by the public sector, is by design and intent hostile for investors.”

He recommends avoiding financial assets & cash altogether – instead accumulating real assets like gold & oil .. “Some readers might be skeptical that, from their current starting point, gold, oil or other commodity prices could rise tenfold in price from here. Oil at $100/bbl sounds expensive to those who remember the many years when oil fluctuated around $20. Gold at $1,300 also seems expensive compared to the sub-$300 price fetched by UK Chancellor Brown in the early 2000s. In both cases, prices have risen by a factor of 4-5x. Note that this is the rough order of magnitude that gold and oil rose into the mid1970s .. But it was not until the late 1970s that both really took off, leaving financial assets far behind .. If anything, a persuasive case can be made that the potential for gold, oil and other commodity prices to outperform stocks and bonds is higher today than it was in the mid-1970s.”

Stagflation Is A Keynesian Phenomenon

08/04/2014 - Why the Fed Has Declared War on Your Money America’s Roots WERE In Sound (Honest) Money

Daily Reckoning essay explores the roots of sound (also referred to as ‘honest’) money in the U.S

Alexander Hamilton, America’s first Secretary of the U.S. Treasury under U.S. President George Washington faced the challenge of restoring the U.S. economy that had been devastated by the U.S. Revolutionary War

.. “When money serves as a stable measure of value, it most clearly expresses the value of everything in terms of everything else.”

.. “When money serves as a stable measure of value, it most clearly expresses the value of everything in terms of everything else.”

.. Hamilton boosted the U.S. economy with legislation for the U.S. federal government to assume & pay off all the debts of the states, establishing the foundation for U.S. creditworthiness

.. the essay describes the historical success with the gold standard:

“Fixing a nation’s currency to gold assures that the currency maintains astable long term value, without inflation, or deflation. That enables a nation’s money to serve as a measure of value, like a ruler measures inches, or a clock measures time. Such a stable measure of value, in turn, means money can best perform its most essential function in facilitating transactions .. The termination of any link between the dollar and gold immediately inaugurated worsening boom and bust cycles of inflation and recession in the 1970s, with inflation soaring into double digits for several years. Inflation peaked at 25% over just two years in 1979 and 1980.”

Campaign poster showing William McKinley holding U.S. flag and standing on gold coin “sound money”, held up by group of men, in front of ships “commerce” and factories “civilization”. (Photo credit: Wikipedia)

08/03/2014 - U.S. & China Financial Repression Is Preventing Their Economic Recovery China’s Risky Play in the U.S. Debt Market READ: China’s Risky Play in the U.S. Deb t Market Caixin Online 07-31-14

CATO Institute Senior Fellow James Dorn explains how & why China has been picking up the pace of its purchases of U.S.Treasury Bonds recently, but “both it & the U.S. would be better off if China relied less on the accompanying investment & export-led model”

CATO Institute Senior Fellow James Dorn explains how & why China has been picking up the pace of its purchases of U.S.Treasury Bonds recently, but “both it & the U.S. would be better off if China relied less on the accompanying investment & export-led model”

.. China is supporting U.S. Treasury bond prices from a desire to stimulate its export growth & to protect its state-owned enterprises, not out of the goodness of its heart to help the U.S. to finance debt & deficits

.. “Financial Repression in China and in the United States (with negative real interest rates) distorts the global allocation of capital. China, as a capital-poor country, should not be a net exporter of capital. By controlling capital flows, suppressing interest rates and pegging the exchange rate, China continues to rely on investment and export-led development. That model of development, with the central role of state-owned banks and enterprises, is not sustainable, as China’s leaders have noted

.. It is in China’s long-run interest to downsize its holding of U.S. debt by ending financial repression and allowing a greater play of market forces. A virtuous outcome would be to deny the U.S. government the means to over-leverage and overspend, while invigorating China’s non-state sector by releasing scarce capital for private investment.”

08/02/2014 - More Financial Repression To Pay Down Debt

READ: Asset Forfeiture – How Cops Continue to Steal Americans’ Hard Earned Cash with Zero Repercussions libertyblitzkrieg.com 07-28-14

There is a growing trend among U.S. local city & state municipalities to use asset forfeiture to help finance their budgets & pay down debt

.. In a nutshell, civil forfeiture is the practice of confiscating items from people, ranging from cash, cars, even homes based on no criminal conviction or charges, merely suspicion

.. lots of this going on in especially Texas, Tennessee, Michigan

.. “A town of 150 people called Estelline Texas earns more than 89% of its gross revenues from traffic fines and forfeitures

.. If you think that example is just a one-off, think again. One of the most horrific instances of non-lethal police abuse last year was the story of David Eckert, the New Mexico man for whom a routine traffic stop turned into a nightmare of torture, including multiple involuntary anal probes. The police dog that ‘sniffed drugs’ and kicked off the entire episode wasn’t even certified to sniff for drugs in the state of New Mexico at the time. His certification expired two years earlier, but that didn’t stop local police from using it to harass and torture state residents.”

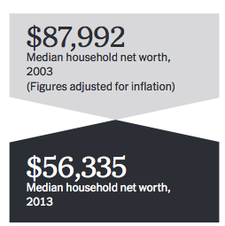

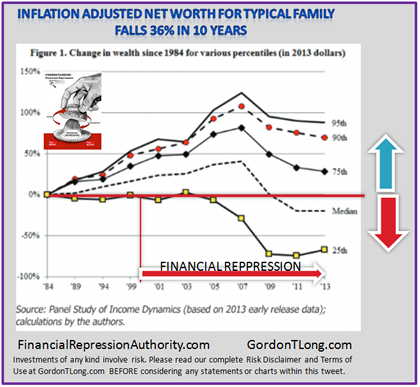

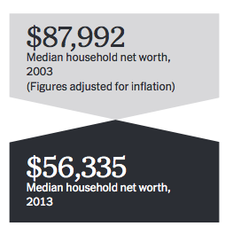

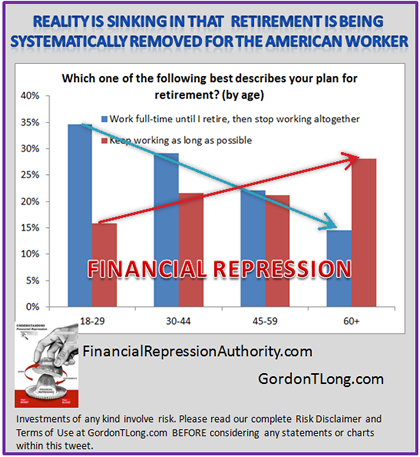

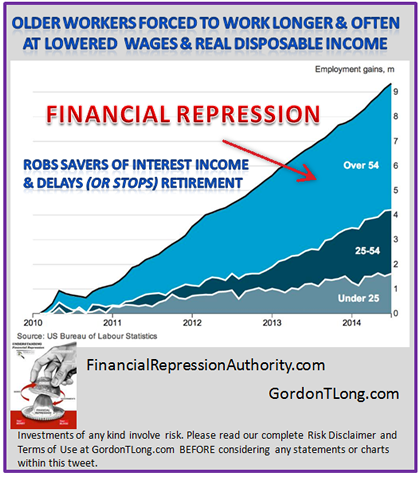

08/01/2014 - The Typical Household During Era of FINANCIAL REPRESSION Now Worth a Third Less

New money is being re-directed to pay increasing debt loads as corporate profits come primarily at the expense of reduced income growth while inflation crushes real disposable income.

A study financed by the Russell Sage Foundation.

DECLINING FINANCIAL WEALTH FOR MOST AMERICANS SINCE 2001

“The housing bubble basically hid a trend of declining financial wealth at the median that began in 2001” — Fabian T. Pfeffer, the University of Michigan professor who is lead author of the Russell Sage Foundation study.

“For households at the median level of net worth, much of the damage has occurred since the start of the last recession in 2007. Until then, net worth had been rising for the typical household, although at a slower pace than for households in higher wealth brackets. But much of the gain for many typical households came from the rising value of their homes. Exclude that housing wealth and the picture is worse: Median net worth began to decline even earlier.”

“For households at the median level of net worth, much of the damage has occurred since the start of the last recession in 2007. Until then, net worth had been rising for the typical household, although at a slower pace than for households in higher wealth brackets. But much of the gain for many typical households came from the rising value of their homes. Exclude that housing wealth and the picture is worse: Median net worth began to decline even earlier.”

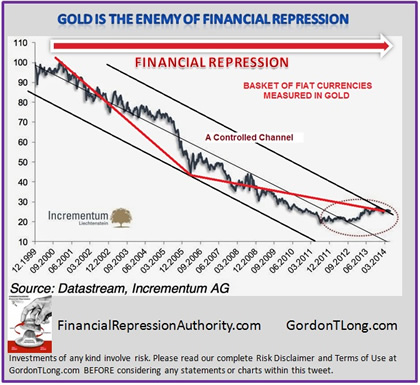

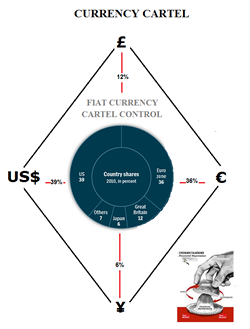

07/30/2014 - FINANCIAL REPRESSION HAS BEEN AGGRESSIVELY PURSUED SINCE THE DOTCOM BUBBLE IMPLOSION

FIAT CURRENCIES ARE BEING DEVALUED IN A COORDINATED MANNER AS PART OF THIS MACROPRUDENTIAL POLICY

This is only evident by measuring a basket of Fiat Currencies in Hard Assets

THE CURRENCY CARTEL

Controls +90% of the $5T in currencies traded daily.

07/29/2014 - Fund managers now have the Legal Right to ‘suspend redemptions’ by the you on your Money Market Funds

SEC Approves Tighter Money Fund Rules – Plan Allows Money Funds to Temporarily Block Investors from Withdrawing Money in Times of StressWSJ

SEC Votes Through Money Market Exit Gates Zero Hedge

HIDDEN TAX INCENTIVES

In conjunction with Wednesday’s release, the U.S. Treasury department is expected to relax certain accounting burdens on the reporting of gains and losses “to ease the transition to a floating share price”.

CREDIT RATINGS REMOVED

Separately, the SEC voted unanimously to re-propose a plan, originally floated in 2011, to purge references to credit-rating firms embedded in the SEC’s money-fund rule. The change is a requirement of the 2010 Dodd-Frank financial law that requires federal agencies to scrub their rule books of references to credit ratings, forcing them to find new measures to help investors assess creditworthiness.

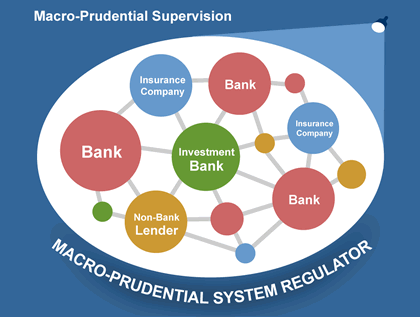

07/27/2014 - “Relying upon Macroprudential Supervision to prevent financial instability provides an artificial sense of confidence!?”

READ: The Danger of Too Loose, Too Long With an improving labor market and an uptick in inflation, the danger now is to wait too long to tightenRichard W Fisher 07-27-14 WSJ

“I have grown increasingly co. ncerned about the risks posed by current monetary policy. First, we are experiencing financial excess that is of our own making. There is a lot of talk about “macroprudential supervision” as a way to prevent financial excess from creating financial instability. But macroprudential supervision is something of a Maginot Line: It can be circumvented. Relying upon it to prevent financial instability provides an artificial sense of confidence”.

“There are some who believe that “macroprudential supervision” will safeguard us from financial instability. I am more skeptical. Such supervision entails the vigilant monitoring of capital and liquidity ratios, tighter restrictions on bank practices and subjecting banks to stress tests. All to the good. But whereas the Federal Reserve and banking supervisory authorities used to oversee the majority of the credit system by regulating depository institutions, depository institutions now account for no more than 20% of the credit markets”.

Mr. Fisher is president of the Federal Reserve Bank of Dallas. This article is excerpted from his speech on July 16 at the University of Southern California’s Annenberg School for Communication & Journalism.

Low interest rates and abundant availability of credit in the nondepository market, the bond markets and other trading markets have spawned an abundance of speculative activity

“The Fed has been running a hyper-accommodative monetary policy to lift the economy out of the doldrums and counteract a possible deflationary spiral. Much of what we have paid out to purchase Treasurys and mortgage-backed securities has been put back to the Fed in the form of excess reserves deposited at the Federal Reserve banks. As of July 9, $2.517 trillion of excess reserves were parked on the 12 Fed banks’ balance sheets, while depository institutions wait to find eager and worthy borrowers to lend to. But with low interest rates and abundant availability of credit in the nondepository market, the bond markets and other trading markets have spawned an abundance of speculative activity. ” — Fabian T. Pfeffer, the University of Michigan professor who is lead author of the Russell Sage Foundation study.

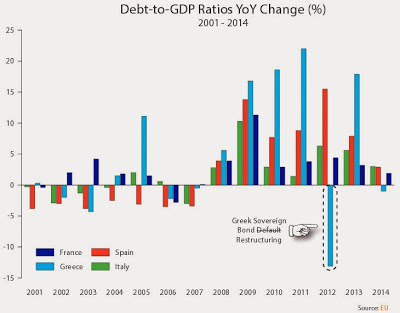

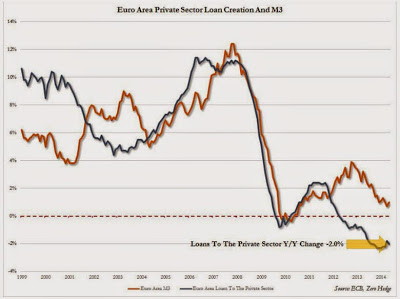

07/24/2014 - Which Is Better For Getting People To Understand The Economy’s Problems?

A Classic Comedic Metaphor? from

Or Graphic Statistical Analysis?

In his latest Hmmm, Grant Williams* makes the analogy of an episode from Monty Python’s Flying Circus, to the ‘line’ we are being fed by the Fed & other central banks .. highlights the example of Europe where the central bank has encouraged the buying of bond of bankrupt countries – “we’ll make sure you don’t lose money” – financial repression European-style .. “European banks loaded themselves to the gills with peripheral European debt as part of the quid pro quo with Draghi, but making free carry off the desperate central bank is hardly what used to pass for banking. Remember when banking used to be about things like making loans?” This is a thoughtful piece with graphs to substantiate the commentary. Don’t miss it.

Click on “Hmmm July 28” to download the report (may have to provide your email address), or hit “View Fullscreen” far below next to the ‘S’ icon to enlarge the viewing .. John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore .. permission granted by Grant Williams to us to post the below, courtesy of www.vulpesinvest.com funds.

Grant Williams Does An Admirable Job Of Bringing Both Together

Get a load of the first one that shows European banks are not lending to people anymore. On the second one, understand that above 0 means the math of it all is getting worse, even with austerity.

07/22/2014 - Opinion – Macropru is credit rationing by another name

The Bank of England has been flashing an amber light for months about the complacency shown by low market volatility, but in house-price obsessed Britain, mortgage excess is the focus of its worry. Last month it became the first of the major central banks to set out to try to control credit using non-monetary tools: in the jargon, “macroprudential measures”. Ms Yellen has been highlighting macropru as the first line of defence against bubbles for a while.

The problem SEEMS simple central bankers. Central bankers want money to lubricate the real economy, not to flow into pointless leverage of existing assets. Higher rates could reduce the incentives to leverage, but at the cost of damage to the real economy. Their solution is to set up barriers inside the banks to direct the flow.

If central bankers ever get serious about using macropru to control bubbles, it will mean limits on more than just mortgages. The obvious place to start is with the froth in junk bonds and the leveraged loans used by private equity houses. It is interesting, therefore, that the Fed’s monetary policy report last week emphasised that the central bank is “working to enhance compliance” with leveraged loan underwriting and pricing standards. If it becomes harder for private equity groups to gear up, they can afford to pay less to buy companies, cutting back one source of demand for shares. READ MORE

The real danger comes if central banks try to use macropru as a semi-permanent way to keep interest rates lower than normal, as Mr Napier fears. In this case investors will face a double setback: they will not be treated as part of the “real economy” deserving of funds, while state-directed allocation of assets has a terrible history of supporting duds, hurting growth.

The real danger comes if central banks try to use macropru as a semi-permanent way to keep interest rates lower than normal, as Mr Napier fears. In this case investors will face a double setback: they will not be treated as part of the “real economy” deserving of funds, while state-directed allocation of assets has a terrible history of supporting duds, hurting growth.

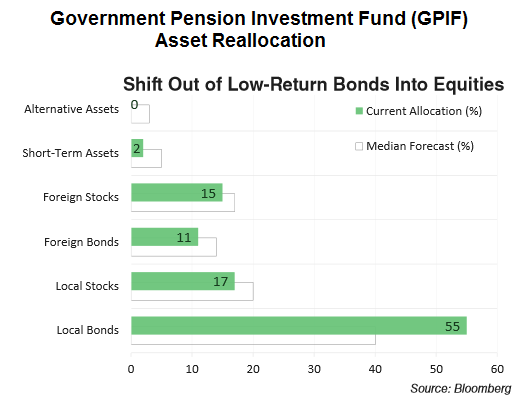

07/22/2014 - Government Pension Investment Fund (GPIF) Asset Reallocation

It is no secret that unlike other banks who, while directly intervening in the bond market only manipulate equity prices in relative secrecy (usually via HFT-transacting intermediaries such as Citadel), the Bank of Japan has historically had no problem with buying equities outright, traditionally in the form of REITs and equity-tracking ETFs. Which explains why overnight it was revealed that in order to boost the stock market, pardon, economy, the Bank of Japan is preparing to purchase exchange-traded funds based on the JPX-Nikkei Index 400 as an “option to boost the impact of unprecedented easing,” according to people familiar with BOJ discussions.

Bloomberg reports that including funds that track the index would broaden the range of shares in the BOJ’s ETF purchases, and encourage companies to deploy cash for investment. That is the official storyline. It goes without saying that what the BOJ is really after is to generate further upside in the Nikkei225 which unlike other stock markets, is still notably in the red, because not only will the primary impetus behind QE – the wealth effect of the 1% – suffer, but also all those new billions in Japanese pension funds reallocated away from bonds and into stocks will continue to lose money. And the last thing the Abe cabinet, its popularity already flailing needs, is the realization that it has gambled the retirement funds of the locals on the biggest Ponzi scheme in Japanese history. READ MORE

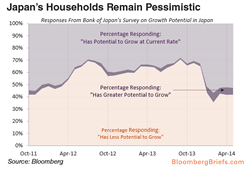

07/21/2014 - Japan’s Plan By Its Central Planners For Financial ‘Repression’ Of The People: Central Bank To Buy Bonds, Pension Funds To Buy Stocks

Japan is moving to get its pension funds to sell Japanese government bonds (JGB) to its central bank, then use corporate governance & regulatory changes to force the pension funds to buy stocks

.. “A return to more normal JGB interest rates of above 3% – which will prove loss-making for present holders such as the BoJ – is not likely for at least two years. Part of the Bank of Japan (BoJ)/Ministry of Finance (MoF) strategy of encouraging Japanese private sector portfolio shifts away from JGBs into equity-type assets is that the BoJ can bear such losses far more easily than other investing institutions. One of the most important moves concerns redeployment of assets held by the $1.2tn government pension investment fund (GPIF), where decisions are imminent on investing more in domestic equities rather than government bonds.”

READ MORE: Japanese QE to continue as inflation rise slows Abe’s impatience spurs reform drive

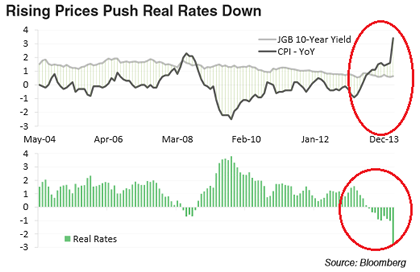

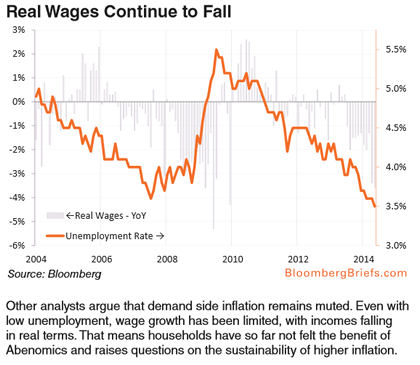

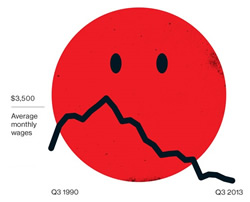

07/20/2014 - WHAT FINANCIAL REPRESSION LOOKS LIKE IN JAPAN

GREAT FOR GOVERNMENT AS DEBT FINANCING GETS CHEAPER

A DISASTER FOR THE PEOPLE HAS REAL WAGES PLUMMET

THE JAPANESE PEOPLE HAVEN’T FULLY WOKEN UP TO THE FACT THEY HAVE BEEN ‘CONNED’

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority

{kind=link}