12/12/2024 - CedarOwl – Will Cryptocurrencies Address the Unsustainable U.S. Debt Crisis?

12/12/2024 - CedarOwl – Will Cryptocurrencies Address the Unsustainable U.S. Debt Crisis?

Transitioning the global USD-based economy and the rapidly rising use of cryptocurrencies results in USD cryptos backed by/with a demand for U.S. Treasuries

Link Here to the CedarOwl Article

Key Messages:

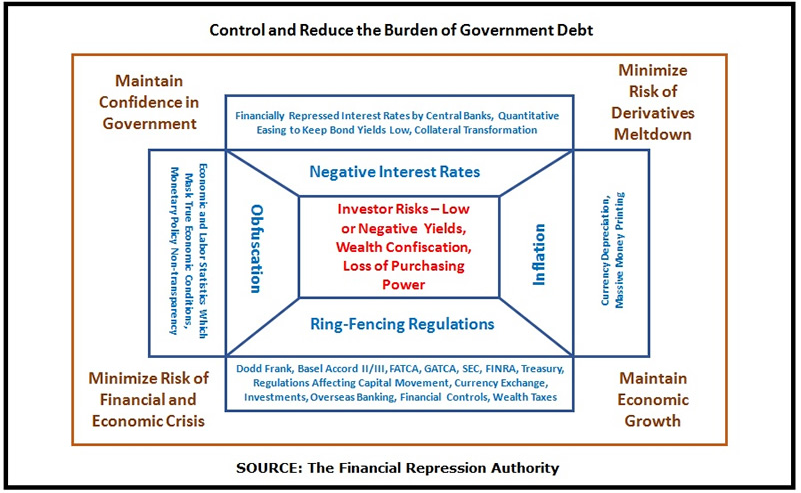

- Given falling demand for U.S. Treasuries by many foreign central banks, the U.S. appears to be planning to put a bid on U.S. Treasuries through promoting the rise and interest in cryptocurrencies, some of which require purchases of U.S. Treasuries as collateral backing;

- The rise and interest in cryptocurrencies is funneling a considerable level of money into cryptocurrencies as an asset class, instead of into the real economy, commodities and hard assets – this is serving as an inflation “honey-pot” or “heat-sink”, thereby diverting money from excessive money printing in recent years away from commodities and hard assets;

- The rise and interest in cryptocurrencies is generating momentum and buy-in to the eventual use of permissioned (controlled) cryptocurrencies that are software-programmable and government-controlled, which will likely be implemented by commercial banks not central banks as a Central Bank Digital Currency (CBDC); without a Digital Bill of Rights in place, these permissioned cryptocurrencies will severely control and limit personal and human freedoms and liberties, even whether or not your cryptocurrency account can accessed or used outside of your home country;

- Most cryptocurrencies are not backed by anything like a commodity or the full faith and credit of a government, and can be “printed” ad-infinitum in a manner similar to government fiat money, bringing the usual loss of currency purchasing power and currency dilution results.