Professor and CEO of Create-Research Amin Rajan shares his knowledge with an in depth interview on Risk Mitigation and how European Pension Plans are Coping with Financial Repression with FRA Co-Founder Gordon T Long .

Amin Rajan worked as an economic forecaster in the UK treasury for over 8 years, and since then has been focusing on investment matters driven by macro investment behaviors catering to pension funds, insurance companies and wealth managers.

What Structural Solutions Are Being Adopted to Cope With Financial Repression.

Risk focus has shifted from the past to the future

Structural solutions are being adopted

The resulting personalization of risk is an Everest of a task

Personalization of Risk

Amin Rajan thinks that there are two leading principles that must be noted when looking to mitigate risk in the future, since the risk in the past is much different from today with a huge emphasis on macro risk.

Firstly, the sources of risk in the future will be different from the past, referring to the debt crisis and the threat to the Chinese markets.

Secondly, he believes that a portfolio investment should be looked at as a whole and protected as a whole, instead of looking at individual positions of your investments.

“The next crisis will be caused by systemic forces and will not be your usual crisis”

Currently pension funds are facing a very difficult situation where they are experiencing negative cash flows, due to the changing demographics in the United States. They are using up all their money on current retirees and not leaving enough behind for the later generations. The non investment approach would be to change your retirement age, you can reduce your liability by 3-5% each year of increase in retirement age. But it is not very easy to change benefits because these funds come fixed and are for the most part impossible to change.

“These pension funds are turning themselves into a ponzi scheme.”

Lately most employers are changing their employment plans and membership requirements, the new employees are no longer open to the retirement benefit plans. They are freezing the future accruals for existing employees; meaning your benefits are fixed today and your benefits are not a result of your future retirement level. Furthermore, they are moving away from employee’s final salary towards career average salary to further decrease the amount of benefits provided upon retirement. However even with all these new policies being taken place there is still not enough cash for them to sustain because the level of debts are too big for pension funds to solve on their own, and Amin expects Washington to step in soon.

“We are transferring risk from people who couldn’t manage it (governments and employees) to people who don’t even understand it”

Retirement Taxation

Europe always had high taxation; retirees were always paying taxes on top of their social security income. In Australia however once the individual retires they take out all their money and spend it. Storing it away, buying property for their children instead of keeping it with the banks. This personalization of risk is nobody’s first choice it is their only choice because of their situation. Employers do not have the money to put into equity; governments are facing imperishable levels of deficits. So individuals are now facing more responsibility when they do not have the right degree of financial knowledge to do so, putting us all in a downwards spiral where no one can help anyone else when everyone is faced with ultimatums.

Amin thinks that there is a fourth leg coming up in the new generation of retirees, which is working a part time job after retiring because they are not able to sustain their lives on just their retirement benefits.

Amin Rajan tells us that we should question everything; we live in an environment where we must approach everything with an open mind. Do not assume things are automatically going to get worse in the future nor should we take anything for granted so always weigh your options before making crucial financial decisions.

All of Amin Rajan’s research journals and papers are available for free and online to contact him and inquire about Amin’s research please visit www.create-research-UK.com.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/30/2016 - Martin Armstrong: ” A COLLAPSE IN GOVERNMENT IS INCOMING, MARKETS ARE GOING TO START RESPONDING!”

FRA Co-founder Gordon T. Long delineates political developments and their consequences on the global economy with Martin Armstrong, founder of Armstrong Economics.

Martin Armstrong began his studies into market behavior when first becoming fascinated by the events during the Crash of 1966. He pursued his studies of economics searching for answers behind the cycle of boom and busts that plagued society both in Princeton and in London. He began to do forecasting as a service to institutional cash market players in gold that included Swiss banks.Armstronghad the unusual background in computer science in hardware and software and was perhaps the first to begin to apply his diverse knowledge from two fields together. He began creating a global model in the mid-70s and was publishing the results from about 1972.

Armstrong began providing forecasts for clients generally three times during the course of each trading day, it began on a closed-circuit telex system – a forerunner to the internet among professional dealers. As a consequence Princeton Economics International, Ltdwas born. Armstrong became the chairman focusing on the research while the partners became the managing directors around the globe. By 1985, Armstrong was certainly one of the top premier Foreign Exchange analysts in the world. He stepped up in 1985 when James Baker was convincing President Ronald Reagan to create the G5 (Group of 5 now G20) nations to manipulate the currency values to affect the trade deficit, which became known as the Plaza Accord.

Armstrong’s work has become world renown. This model has successfully pinpointed not merely major specific days who events well in advance, but it has provided one of the most consistent guides for understanding the turning points in the global economy and thus the business cycle not merely within a domestic economy, but within the global economy on a collective basis. This has been demonstrated by numerous articles.

CHINA AND CURRENCY DEVELOPMENTS

“Pegs do not work and they always break because of politicians setting the value of something for private agendas.”

The Chinese are trying to maintain a controlled economy but they are losing the grip of it. Many people misunderstood the economic statistics because they do not understand what is happening. You had many companies in Hong Kong borrowing in dollars, converting it back in and paying 1% then funneling it into China and collecting 5%-8%. People perceived this as the Chinese getting lots of capital inflow, and the economy doing good, but it had nothing to do with the economy. Following this, shadow banking was shut down and then it was perceived that the economy was going down, but it’s been going down since 2007. We have China in trouble, Japan’s currency is really a closed economy and these pegs are starting to go because the dollar is the only viable currency. You can’t park in China, they don’t trust the bonds yet, can’t go into Russia, and essentially all of Europe; therefore it’s been dollar by default.

“The dollar is the most liquid and the least ugly. It is the prettiest of the 3 ugly sisters. It is the rise in the dollar which will create the change in the monetary systems.”

A change will occur sometime around 2020, the whole thing with negative interest rates and quantitative easing just does not work. Economies are just much more fluid today. Emerging markets began expanding debt to more than 50% of US debt and they did this because they issued their debt in dollars because of low interest rates, and pension funds needed high yields so they went and bought all this emerging market debt. The money supply that supposedly the Fed increased did not stay here. If you look at real estate, the Chinese are the #1 buyer of real estate in the US, and the IRS is also buying lots of real estate in New York and Miami. It has been all foreign money coming in and it’s shown in the US stock markets. When the Japanese came in what did they do? They bought the high profile stuff, Rockefeller Center etc. Foreign money goes into the Dow, so the Dow lead the market all the way up, the other markets only began to overtake only when foreign capital began to subside.

“International capital flows are really what drives everything, but unfortunately it is something they don’t teach in school and not many pay attention to it.”

ECONOMIC CONFIDENCE MODEL

The economy peaked in September of last year on a global scale. Everyone is pretty much in recession, the US rallied a bit but you drive down a street and you see every office building has ‘space for rent.’ The business cycles do a good job in showing you where things are developing. The last peak was in real estate in 2007, but what is important about that is many of these markets peaked back then, and to this day markets have not surpassed that peak throughout the world.

The US is realizing that there is a problem here. The Fed has been lobbied by the IMF not to raise interest rates because of international concerns and not domestic concerns. They realize that with the dollar as a reserve currency, they are losing the power to control their own economy.

“International interest has taken priority over domestic, keep this going and the Fed won’t be able to do anything to help the US economy.”

Eventually the market is going to raise the interest rate, because we are in a phase now where governments are all in trouble. They are all chasing money, going bankrupt and keep raising taxes; just another reason why quantitative easing is failing. Disposable income is consequently shrinking rather than expanding. This is largely why Trump is doing so well, many people don’t understand it but the middle class has been completely devastated so it is more of a protest vote. The American people are starting to wake up to this problem, and even if Trump does not win we are projecting a congress turnover by 2018 which is similar to what happened in Scotland. This is not a domestic issue, it is happening everywhere.

Younger generations don’t understand the core facts either. The Clinton White House was bought and paid for by Wall Street. The press will never say this because they are afraid it might hurt Hillary, but who basically made all student loans non deschargeable in bankruptcy? None other than the Clintons. In other words all the student loans that are hurting all our youth, it is Hillary that did it.

PRECIOUS METALS AND HARD CURRENCIES

“You can go back and forth in arguments about gold but to the average person it means absolutely nothing.”

Things will only change when these people lose confidence in their government. For example, Republicans are tremendously against Trump, and they rigged the rules in the last convention to sabotage Ron Paul. They made rules that if you did not have enough votes your name couldn’t even be put in to be nominated, but under these rules the only viable person is Donald Trump.

The primary reason why Republicans do not want Trump in is because he is an outsider, he is not owned by the banks or by anyone for that matter; he has funded himself and they do not know what he is going to do. One thing from studying law that I carry with me is, you never ask a question that you do not already know the answer to. Politicians are mostly lawyers and they do not know what he will do.

MAJOR CONCERNS

“A collapse in the confidence of government is incoming, and that is when your markets are going to start responding.”

We are entering a political year from hell. Europe desperately needs Britain and if Britain votes to get out you will see other countries voting for the same thing. They are very much afraid of a contagion developing and the EU collapsing. Everybody criticized Trump for saying he wants to block Muslims from coming in, and what does Cruz say? He is going to implement a bill that all Europeans have to have a visa.

“They are looking at collapsing the global economy and they are destroying it with every breath they take.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/26/2016 - Michael Pento: “Price discovery is essential, it is the nucleus of capitalism and we haven’t had it in decades!”

FRA Co-founder Gordon T. Long is joined by Michael Pento in discussing topics from the government debt problem, the current boom in gold and the outlook of the dollar.

Mr. Pento is the President and Founder of Pento Portfolio Strategies (PPS). PPS is a Registered Investment Advisory Firm that provides money management services and research for individual and institutional clients. Mr. Pento is a well-established specialist in the Austrian School of economics and a regular guest on CNBC, Bloomberg, FOX Business News and other national media outlets. His market analysis can also be read in most major financial publications, including the Wall Street Journal. He also acts as a Financial Columnist for Forbes, Contributor to thestreet.com and is a blogger at the Huffington Post.

Prior to starting PPS, Mr. Pento served as a senior economist and vice president of the managed products division of another financial firm. There, he also led an external sales division that marketed their managed products to outside broker-dealers and registered investment advisors. Additionally, Mr. Pento has worked for an investment advisory firm where he helped create ETFs and UITs that were sold throughout Wall Street. Earlier in his career Mr. Pento spent two years on the floor of the New York Stock Exchange. He has carried series 7, 63, 65, 55 and Life and Health Insurance Licenses. Mr. Pento graduated from Rowan University in 1991.

KEYNESIAN INTEREST RATE MANIPULATION

“You cannot take interest rates down to zero percent and then into the negative territory, constantly increase the amount of something I like to call ‘quantitative counterfeiting’ and ultimately hope for a good ending. It’s just not possible.”

They’re constantly pushing interest rates lower and lower and now to the point where if you’re going to loan money to somebody, you’re going to pay them to do it. The reason their doing this as a method to make their debt serviceable; they need to make ends-meat so they borrow at lower cost. We know there is going to be a collapse because markets have been aggravated and not allowed to function for years.

“30% of all the worlds sovereign debt now has a negative sign in front of it, that’s $7 trillion.”

Here’s the main issue, let’s consider Japan: There is -0.1% for the Japanese 10yr note, an all-time record low. You’re loaning money to Japan, a nation that has 250% debt-GDP and you’re loaning this money going out for 10 years. All for the deal that you’re going to lose money each and every year in nominal terms, and then they have an inflation target and assuming they meet it, Japanese authorities will eventually step in and all of a sudden begin fighting inflation. The only thing this can lead to is an enormous implosion.

“Price discovery is essential, it is the nucleus of capitalism and we haven’t had it in decades.”

SUSTAINING GOVERNMENT DEBT

“As debt has increased, interest rates have gone lower; it is all that they can do.”

When you base a nation’s growth, not on productivity and the size of the labour force, rather on market bubbles, furthermore when you consider there is 19-20 trillion in the US of outstanding debt; there is just no tax base that can finance this.

Look what Draghi had to do, it was not enough to buy $60 billion euros a month, they went to 80 billion, and why just buy government debt when you can buy corporate debt? These practise make no sense, seemingly there is no rationally thinking individual that enforces decisions.

We are stuck until we are hit with an inevitable implosion. The trigger will be when they reach their inflation targets and then become inflation fighters. There will be a period of time following this where you will see bond yield completely unravel, they will soar, and consequently stock prices and economic growth will plummet.

CENTRAL BANK PATTERNS

Local banks have their excess reserves at the central bank, and now the central banks rather than paying to keep the reserves, they are charging for the reserves. They are doing this so banks can go out looking for someone who cannot pay back in taking out a loan, else they will simply go buy more sovereign debt.

“Have we become such children in this world where grown men and women cannot just come forth and admit they have made a mistake and admit there will be a year or two of a recession or depression followed by prosperity?”

If you have so much debt which you cannot pay back, something has to change; the debt needs to be restructured. Debt is not fixed by artificially taking out interest rates and forcing individuals to take out more debt. We are not adjusting we just keep rolling the debt over and over.

“Capitalist systems do not work unless you have a cleansing at some point of excess debt. It is a healthy and necessary part of growth.”

THE GOLD BOOM

Well now in a time where if you stick your money in a sovereign note in a bank, you either get nothing from it or even charged for doing so, gold is definitely lucrative now more than ever. Additionally the ratio between gold miners and gold has never been lower than it is now. As interest rates go more and more negative across the globe, more and more money will be put into gold because for every ounce of gold you’ll pull out just that, an ounce of gold.

“The only escape is a deflationary depression on a global scale from the likes of which the world has never seen.”

ADVICE FOR INVESTORS

“Gold is going to be a winner no matter what happens, there is no losing scenario for gold.”

To have 20-25% of my portfolio in mining shares which is high as far as Wall Street is concerned. So have gold, short in the market, and the only place being long is with energy. being long with energy as of late has proven to show great results. Forget base metals and in terms of energy it’s a great hedge in being short in the market.

THE FUTURE OF THE DOLLAR

“As I predicted, I have been on record in December of 2015 in saying the dollar will fall hard and it did. I knew it was going to happen because I knew the economic data wasn’t supportive of floor rate hikes and this is what the dollar was priced in. It is important to question not what the dollar is going to do against the Yen and Euro, but moreover intrinsically against gold. I believe all the currencies out there are going to lose their value, the reason being that the real money out there and it has been for thousands of years, is none other than gold. “

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/18/2016 - Ty Andros: “ITS A CURRENCY & FINANCIAL EXTINCTION EVENT!”

The Financial Repression Authority is pleasured to be revisited by Ty Andros, Chief Investment Officer of the Sanctuary Fund. FRA Co-Founder Gordon T. Long has has a stirring conversation with Mr. Andros on a number of current economic developments and consequently, the things to unfold.

Ty began his commodity career in the early 1980’s and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Diego, and the University of Miami, majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView of which he is the CEO. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis. Ty prides himself on his personal preparation for the markets as they unfold. Ty is an expert in applying the indirect exchange method as a principle of the Austrian School of Economics in his investing approach.

THE AUSTRIAN SCHOOL OF ECONOMICS

It consists of 3 major components.

Sound money and private property

Free market capitalism

Human behavior

The cycle we are going through now has happened hundreds of times in history and has led to the rise and falls of empires. It’s because of people forgetting the past and repeating the same mistakes. If you don’t have sound money, you really don’t have protection against the government. They can confiscate your money and they have been doing so since Bretton Woods.

“The money that we hold in banks is a worthless junk bond. The government has essentially become the mafia; they are scheming and transferring property to themselves.”

SOUND MONEY

The figure below outlines the specific functions of money:

If it doesn’t have these components then you’re not holding money. Until 1971 it had all those features, and it has been replaced with an I.O.U of fiscally and morally bankrupt politicians and banks. It is worth no more than the paper it is printed on.

“In my opinion, the gold and silver bear market is over so it is a prime time to start accumulating now.”

MARKET CAPITALISM AND WEALTH CREATION

Capitalism is about getting more for less and three groups of people being rewarded for it: The consumer because he is able to give his family a better life, the company which supplied it, and the employees within the company.

Socialism eats everything. Real wealth and income creation are in freefall. There will be no recovering. The confiscation of wealth is also known as runaway regulations, runaway debt creation, more taxes and currency debasement.

“Its pure confiscation, cannibalism, and slavery. It is eating the golden goose. It’s the people that aren’t self-reliant and don’t produce anything eating those that do.”

It’s pure confiscation, cannibalism, and slavery. It is eating the golden goose. It’s the people that aren’t self-reliant and don’t produce anything eating those that do. Nobody owns their homes, it’s simply a record that’s held in a database and all they have to do is misplace it. Nobody owns their stocks in their name and if you look at your banking agreement you don’t even have title to your money, the bank does. Slowly but surely they have removed everything. They don’t let you hold money because they can’t steal from it; real money has been outlawed.

“Gold is the currency of kings, silver is the currency of merchants, and debt is the currency of slaves.”

CURRENCY EXTINCTION EVENT

GDP is nothing of the sort, it’s just debt disguised as GDP. It is spending future wealth rather than creating future wealth for proper allocation to productive enterprises.

“We have nothing; we are just a bunch of debt slaves living in an illusion until we wake up.”

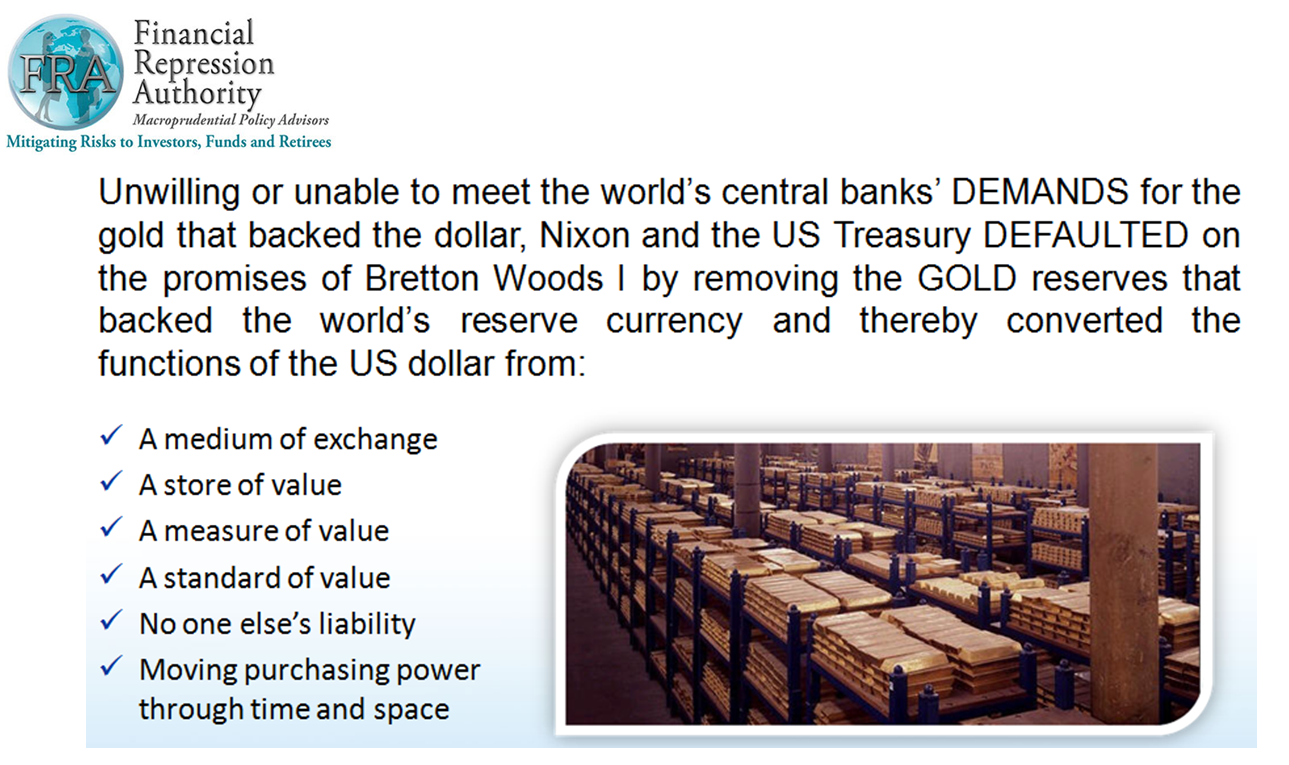

THE EVENTS OF 1971

President Nixon changed from a reserve backed system where the dollar was semi redeemable in gold and silver to a system that has no backing.

“It was the greatest heist in history. It was the greatest transfer of wealth from the public to the ‘bankseters’.”

He did this so that he wouldn’t have to operate in a prudent manner. Prudent manner means have to pass laws and have taxes which gives people a reason to get up in the morning and have the ability to do the capitalism which was discussed earlier. When you have bad laws and bad regulations, the economy will either collapse or they have to print the money to fill the whole; unfortunately they chose the latter.

“History has shown what happens to people who try to fix this system.”

Kennedy was taking the central bank back and creating silver backed money, 90 days later he was dead. Of course we will never truly know, everything is so covered up now and the government is incapable of telling the truth.

THE INDIRECT EXCHANGE

“This is how you go through a currency and financial extinction event. Exchange something of uncertain value, fiat money, for something of certain value, real wealth. This is the indirect exchange in simplest terms.”

So much of the ‘financialization’ of the economy is an illusion because it is not the real things going up; it’s the paper that they’re priced in losing its purchasing power

“The greatest applied Austrian economist in the world is none other than Warren Buffet. “

What Warren does is he sells paper which means liabilities are being debased by central bank’s printing presses and credit creation. If he writes an insurance policy for someone for $10 million, he now has a liability of 10 million, if he did this in 2000 that liability may be 5 million and simultaneously he took that money and bought the Burlington Northern Railroad, which is something that will just reprice to reflect the lower purchasing power it is denominated in. If we are in a depression or a boom, regardless the railroads will run. Half of his great track record is inflation that isn’t properly disclosed. He has been doing this since, coincidently 1971. He has been selling paper and buying real things with cash flow ever since.

Gold doesn’t cash flow but it is about to. Because of negative interest rates you’re paying somebody to borrow money from you. If you are able to hold your money without having to pay someone to hold it.The gold and silver bear market is over. As these destructive negative interest rates go deeper and deeper, people will eventually wake up. They’ve already woken up, this is what’s going on with the presidential race and particularly Donald Trump.

“This is the greatest insanity ever. It will be studied and written about for centuries. It is a much bigger example of stupidity and failing to learn the lessons of history. It is much larger in scale than the Great Depression because of the nature of globalization and the nature of man.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/16/2016 - Egon von Greyerz: “THE WAR ON CASH IS REAL!”

Gordon T Long, Co-Founder of FRA interviewed Egon von Greyerz in Zurick. Egon Von Greherz is the founder of Matterhorn Asset Management who has worked as a financial director for over 17 years in Geneva, and has been advocating for wealth preservation through Gold for over 13 years. MAM now has plans in over 40 countries for investors to place their savings into physical Gold storage for preservation in the world’s largest Gold vault in Switzerland.

Wealth Preservation

Egon says that approximately less than half a percent of assets are invested in Gold today by the people and that most of them do not own any Gold whatsoever. Even with the risky stock market in recent months we have not seen a significant increase in the purchase of Gold as an investment itself. However the increase in Gold purchases is linked more closely to the retail market for public use. Von Greyerz expects the market stocks to drop further down below their current value and is viewing the current spike in stocks as a mere bear trap, insisting that following this we may see a rise in purchases for gold.

“Less than half a percent of world financial assets are of gold today and that’s absolutely nothing!”

It is necessary to understand that gold is not to be viewed as an investment but for insurance purposes against all the property investments and bonds that you may have currently. For over 5000 years the price of gold has only gone up and the value of money has been decreasing ever since. With the expectation of the stock market dropping by at least 50% in its current state, having even 10% of your assets in gold will ensure the safety of your portfolio. The reason being that with the drop in stocks the price of gold compared to the dollar could be at a 1:1 ratio like the 1980’s meaning Gold will outperform all the other assets.

With only a .5% of current assets invested in Gold there is no current risk of a shortage of physical Gold. However, in the near future with the price of Gold expected to rise rapidly there is a certainly a risk of there being a shortage. If institutions, governments and pension funds begin to hedge their assets in gold there will never be enough Gold to satisfy their needs. Alongside rapid printing of money there will be no way to control the rapid increase other than to increase the price of gold itself to purchase smaller amounts of physical gold but for much larger prices to ensure that there is no shortage of real Gold.

“In the next few years it will be hard to get a hold of gold, as there will be a time when there will be no price offered in the market for gold due to its shortage”

Thoughts on NIRP and the cashless society

There are no positive consequences for this situation, Japan had other options but chose this disease which again will make no difference to either economy in the world. The negative interest rate will however stop withdrawals and place cash limits in Europe since people would rather take the money out and hold on to it rather than pay interest on it. But we should still expect more countries to go into negative interest rates even though it is hard to imagine this central bank policy to solve our economic problems.

Unfortunately there are not many other options for investors at the moment to encourage them to place their money elsewhere outside of the collapsing banking system. To avoid possible ‘bailins’ people can invest in property, fine art, and precious metals but not much else to be safe from this risk. Gold on the other hand has not seen a significant price increase and shows just how powerful it can be in the future. It is like holding real money it has the equivalent purchasing power to any currency in its history for the past 5000 years and does not devalue over time.

Even in the event that a bank does not have money to exchange for your gold you may still use it as barter, it has had this function throughout its history and will remain this way. It is an excellent opportunity for insuring your wealth and having liquidity at the same time. This is away from the banking regime and does not need to be declared to the IRS either for further taxation.

Furthermore, there is no safe spot currently to store your wealth other than a select few countries with good law and politics to ensure you get to keep what you’ve earned. Switzerland currently holds 70% of all the gold bars in the world and is by far the most secure location for storing wealth in long term.

Egon does not think that the current primary elections going on in the United States will have any effect on the current economic situation of the world. Referring to the fact that there is simply too much debt at this point and no difference will come from the selection of a new president. He suggests that there needs to be a complete systemic overhaul of the way the economic system works. Egon von Greherz publishes several articles weekly and you can find his research and upcoming investment opportunities online at www.matterhorn.gold or at www.goldswitzerland.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/11/2016 - Jeffrey Snider: US$ STRENGTH IS A MANIFESTATION OF A US$ SHORTAGE

FRA Co-Founder Gordon T.Long and Jeffrey Snider, Head of Global Investment Research at Alhambra Investment Partners discuss a broad array of Global Macro subjects in this 48 minute video discussion with supporting slides.

As Head of Global Investment Research for Alhambra Investment Partners, Jeff spearheads the investment research efforts while providing close contact to Alhambra’s client base. Jeff joined Atlantic Capital Management, Inc., in Buffalo, NY, as an intern while completing studies at Canisius College. After graduating in 1996 with a Bachelor’s degree in Finance, Jeff took over the operations of that firm while adding to the portfolio management and stock research process.

In 2000, Jeff moved to West Palm Beach to join Tom Nolan with Atlantic Capital Management of Florida, Inc. During the early part of the 2000′s he began to develop the research capability that ACM is known for. As part of the portfolio management team, Jeff was an integral part in growing ACM and building the comprehensive research/management services, and then turning that investment research into outstanding investment performance. As part of that research effort, Jeff authored and published numerous in-depth investment reports that ran contrary to established opinion. In the nearly year and a half run-up to the panic in 2008, Jeff analyzed and reported on the deteriorating state of the economy and markets. In early 2009, while conventional wisdom focused on near-perpetual gloom, his next series of reports provided insight into the formative ending process of the economic contraction and a comprehensive review of factors that were leading to the market’s resurrection. In 2012, after the merger between ACM and Alhambra Investment Partners, Jeff came on board Alhambra as Head of Global Investment Research.

Jeff holds a FINRA Series 65 Investment Advisor License.

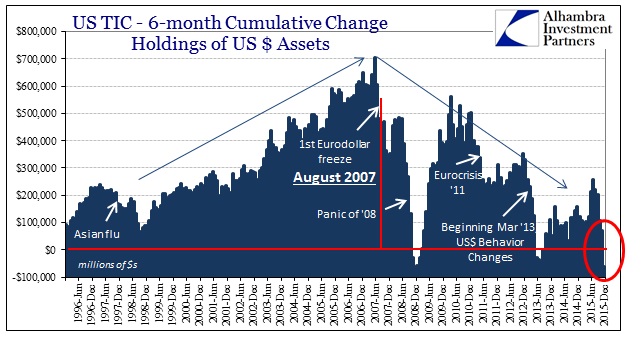

US TIC REPORT, TREASURY SALES

TIC is a compilation done by the US Treasury based on their access to data on foreign accounts and holdings of Dollar accounts and securities, and estimates the foreign Dollar market. Over the last decade or so, it is clear that the Eurodollar market grew steadily at a rapid rate until about August 2007, at which point it pivots and comes back down. The TIC data shows the tendency of dollar markets to essentially be stable, usually addressed through selling Treasury. However, the private dollar markets offshore are in disarray to the extent that central banks around the world are forced to fill the dollar deficiency with their own holdings. Of especial note is China’s reduction of their US Treasuries and foreign currency reserves, and OPEC countries incurring serious Current Account deficits in an attempt to maintain their pegs with the US dollar. In addition are the emerging markets who borrowed about $7-9T in USD, who now have difficulty paying back debts due to slowing trade and falling currencies.

This all leads to the US dollar strengthening, which is the manifestation of the dollar shortage. In recent days, Japan using NIRP will further disrupt the dollar system.

“US Dollar Strength is a manifestation of a US Dollar Shortage!”

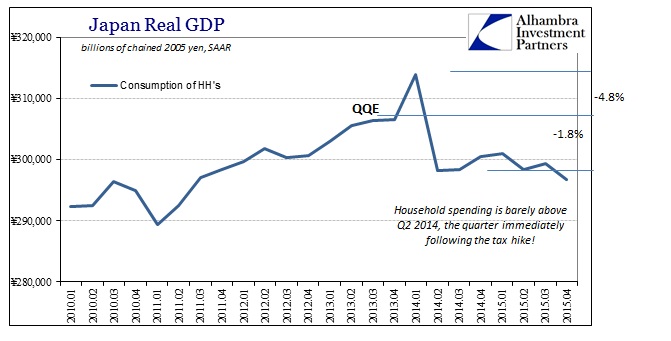

JAPAN: QE FAILURE AND WHAT NIRP MEANS

Under QE, Japan obtained a burst of inflation around 2014. Instead of leading to sustained economic activity, household income and spending dropped about 7%, which was also not offset by growth in GDP and demand. The surge in expansion, due to cheaper money, increases supply which then demolishes pricing power. In addition to the reduced value of savings, large companies have also shifted production offshore, thus increasing the effect and emphasizing the failure of QE/QQE to stimulate the economy.

NIRP also carries with it the threat of failing like QE, along with numerous other particle effects that cannot be currently measured or predicted, mostly as this type of system has not existed for over a hundred years. This is an indicator of the lack of power central banks have over the economy, but can be put down to overemphasizing the value of monetary policy over fiscal policy in the developed world. The dollar system has been artificially expanded past any control by banks and monetary policy, globally, over the last decade. The only way to stop it is to focus on other fiscal factors that would allow economic potential to be realized again and to refrain from following Keynesian economics once it has been proven to be ineffective.

“Japan is a test case in almost clinical conditions for QE and QQE, and it failed on every count.”

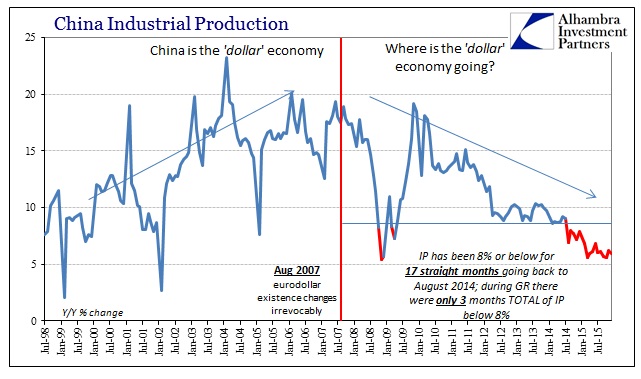

CHINA: COLLAPSING TRADE AND CREDIT

China is both an impediment to growth and a casualty of the rest of the world, but recently more of a reflection of the global dollar economy as they are most sensitive to changes there. The lack of growth over several years forces a fundamental shift toward a Keynesian response of fiscal and monetary stimulation that creates asset buffers at odds with overcapacity. Meanwhile, China still lacks any real method for economic growth and is forced to react to outside influences while juggling the problem of overcapacity with the falling export industry. This then leads to capital flight, which furthers the struggle to grow GDP.

China is clearly attempting to manage the Yuan by selling dollars to strengthen it, but will eventually falter like any pegged currency. Many currencies pegged to the US dollar, Eurodollar, and Petro dollar will likely collapse. Keynesian economists believed that 2007 was the beginning of a temporary deviation from sustainable global growth, but was in fact the structural revaluation of higher economics of the financial system. We are likely headed for a systemic reset and reorientation, which will be disruptive with significant risk but can be adapted to.

“I think we are headed for a systemic reset.”

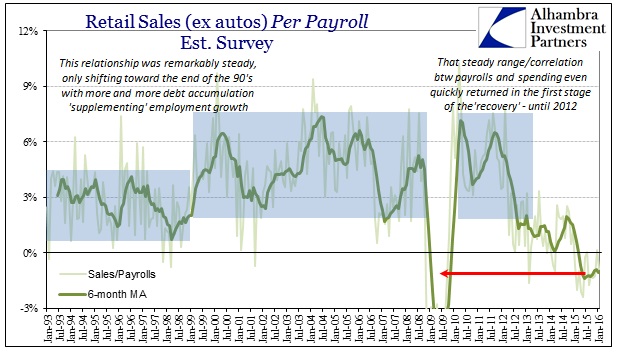

RETAIL: JANUARY SALES AND CONTINUING TREND

Retail sales have been near recession levels of low, indicating that consumers are under pressure, but inventories are still rising despite manufacturers cutting back. Retail slowing is a fixed trend starting from 2012, amplified in 2014-2015 with the disappearance of the manufacturing industry and loss of export goods. This is likely due to lack of real recovery that slowly eroded US consumers’ ability to continuously expand their activity. The middle class has no savings, so thus the capitalist system that relies on savings to reinvest into productivity.

Over the last several years, companies have been spending on buybacks instead of investing in productive capacity. 1900 of the S&P companies spent more on buybacks and dividends than they were earning, thus creating more debt.

“Recession is a necessary process, like anything else. It’s creative destruction.”

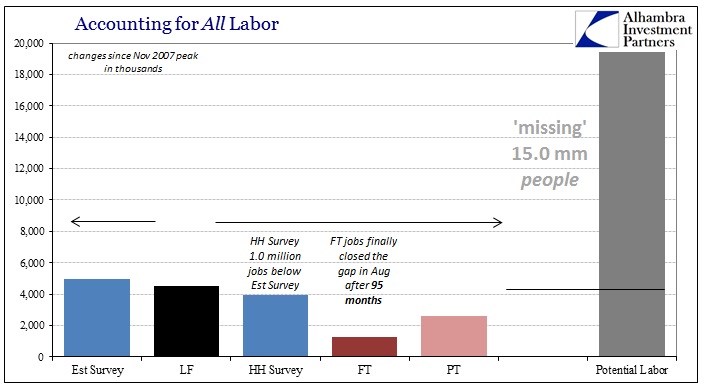

LABOR: FULL EMPLOYMENT – NOT REALLY!

There is a major disconnect between major unemployment statistics and the rest of the economy, where even having a job is not necessarily enough to support the expected standard of living. There are low prospects for growth in the job market, and people sense that there is a need for a restructuring of the system. Job growth is mostly in low income occupations, which results in potential workers entering college with a loan but failing to actually enter the labour force.

The current economic state is similar to the suppressed state of the 1930’s and 1940’s, and once the systemic reset is allowed to occur, the economic potential released will be tremendous. Recessions are necessary to allow risk to be properly priced, which in turn creates confidence in investment. The resulting reset should shift away from one centered around banks and the value of credit toward a capitalist system that prioritizes “money is money” over “money is credit”.

“Monetary policy is designed for companies to borrow more; it’s just that economists expected they’d borrow more for productive capacity rather than financial capacity.”

Abstract by: Annie Zhoua: zhou108@gmail.com

Video Editing by: Minjung Kim: minjung.kim@ryerson.ca

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/04/2016 - Dan Amerman: MARGIN RULE CHANGES FORCE NEW PRIVATE FUNDING OF PUBLIC DEBT

FRA Co-Founder Gordon T.Long and Dan Amerman have an in-depth conversation covering various topics such as financial repression, quantitative easing, devious actions of the Fed and much more. Daniel R. Amerman is a Chartered Financial Analyst, author, and speaker, with BSBA and MBA degrees in Finance, and over 30 years of professional financial experience. As an investment banking vice president in the 1980s he did groundbreaking work in the security originations and asset/liability management areas, including CMO/REMIC originations as part of portfolio restructurings for financial institutions, as well as the creation of synthetic securities for institutional clients. As an independent quantitative analyst in the 1990s and 2000s, he structured mortgage-backed bond financings and provided analytical services for real estate acquisitions by multifamily and commercial real estate owners, investment banks, and tax-exempt issuers.

Mr. Amerman is the creator of a number of DVDs and books on finance, including two books published by McGraw-Hill (and subsidiary): Mortgage Securities, and Collateralized Mortgage Obligations: Unlock The Secrets Of Mortgage Derivatives. He has been a speaker and workshop leader for sponsors including The Institute for International Research, New York University, and many banking groups.

Mr. Amerman has spent a number of years in researching alternatives. Drawing upon his background outside the individual investor industry, he has developed an interrelated group of non-traditional solutions – including asset/liability management strategies – for such concerns as financial crisis, inflation, inflation taxes, low economic growth rates, and pervasive low yield markets.

REVISiTING THE EXPANSION OF FIAT CURRENCY

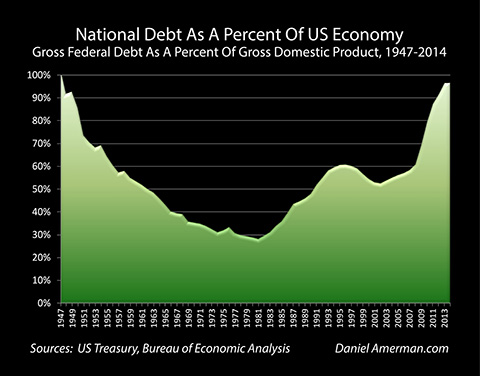

The bigger issue is that we had a change in the national debt super cycle. As of 1947 due to the expense of WWII, the outstanding US debt was approximately equal to the size of the total economy. This is as toxic for a country back in 1947 as it is today.

Historically the growth rate of heavily indebted countries is much slower. It is a slow economic growth and a high interest rate risk environment. This was not just the US alone, this was most definitely global. What world leaders did as a result was get together, and yes Bretton Woods was part of this and they agreed to put rigid financial controls on the population. Effectively the size of national debt was held down for approximately 25 years while the economies experiences periods of substantial growth. Eventually these national debts as a percent of the economy had dropped down to below 30%.

This decline promoted a rapid growth environment, free market interest rate, removal of capital controls, and lifted the limitations on private ownership which we have had since 1973; individuals in the US could not hold gold for investment purposes.

RING FENCING

“You’re not going to keep up with inflation and there is not much you can do about it. That’s the point of ring fencing.”

I split it into two ways. The first is capital controls and second, forcing intermediaries to participate in financial repression. Another component as well is repressing the ownership of precious metals so people do not have an alternative protection from inflation. What’s surprising is that the term financial repression has a conspiracy theory connotation associated with it, when in fact financial repression is an integral part of macroeconomics. It has been a core part of managing financial systems over a long period of time. What’s surprising is that the term financial repression has a conspiracy theory connotation associated with it, when in fact financial repression is an integral part of macroeconomics. It has been a core part of managing financial systems over a long period of time.

In the US in a relatively short period of time, particularly in 2010 all these elements were released for the first time since the 1970s. Interest rates were forced down below inflation by massive government intervention, quantitative easing and forms of capital controls all came out together and as a result dominated the markets ever since. The fascinating part is that there has been a series of developments over the last few months which may be the biggest round of financial repression that we have seen since 2010.

“Ring fencing which I consider as the third pillar is the forced participation of financial intermediaries in the name of public safety. Two key developments were what came out in 2015 was that the Fed has a part of the financial stability board. This board is the G20, the IMF, World Bank combined and all simultaneously agreed to change their money fund policy as well as their margin rules.”

Ring fencing which I consider as the third pillar is the forced participation of financial intermediaries in the name of public safety. Two key developments that came out in 2015 was that the Fed has a part of the financial stability board. This board is the G20, the IMF, World Bank combined and all simultaneously agreed to change their money fund policy as well as their margin rules. They changed regulation on money funds which are apparently done in the name of public safety such that it was an expensive burden for any funds to use anything other than federal debt for their money funds. Effectively creating an enormous financial advantage.

“This is a classic scenario. Take a financial intermediary and in the name of public safety make them hold US government debt.”

This is a classic scenario. Take a financial intermediary and in the name of public safety make them hold US government debt. In doing this you have expanded the market for government debt by whatever the net change is. Essentially locking in an additional trillion dollars of funding for the debt.

“A key thing to make note of is that these are all financial intermediaries, so when people ask who is funding the debt, the answer is all of us are.”

We are essentially financing the government through an intermediary. By changing regulations they are both increasing the relationship and locking into it. At this short term end of the yield curve we are doing this for virtually no yield whatsoever. We are providing the money to the federal government through an intermediary whose participation is forced.

FORCED MACROPRUDENTIAL POLICIES

“They are forcing ever lower interest rates on more of the population. This is providing larger low-cost funds to the government in an ever more constrained manner where it becomes harder for people to escape.”

On Nov 12, 2015 the financial stability board agreed to implement margin rule changes. They were talking about it being a blast from the past, it was what central banks used to do in the 1970s. This is now brought back out, but in this case it is also an expansion of the mandate of the Fed. Where we are with these changes is that the Fed will be without active congress and expanding their control over the US markets to all investment firms to participate in some sort of secured lending.

Financial firms often need cheap money on a short term basis. They can sell a treasury security to someone else at a given price and agree to buy it back at a higher price; in effect it becomes a short term loan. The difference in price is the interest rate that they are paying, this can be done without an actual sale and instead with the pledge of the securities as collateral.

“Central banks are concerned that these low quality collateral loans are now considered to be at risk for triggering a new financial crisis. That’s why they’re changing the regulations where they have the ability to change margin rules at will.”

The best known forms of margin deal with stock ownership where your borrowings become limited. If this was raised to 60% or 70% to bring down stock values, people will have to scramble to sell these securities or they will have to come up with the additional cash through some other means, otherwise there will be a forced liquidation.

What has been created is a major incentive to use US treasuries securities as collateral for repurchase agreements. Once everyone does this then you get a situation where the Fed is no longer in control of leverage in the market.

PREPARING FOR THE FUTURE

Funding for US national debt has just increased by $2.5 trillion. This is very similar to something that is far controversial and that is quantitative easing. Total US treasuries securities held by the Fed are between 2.4 to 2.5 trillion. They are holding this approximate level because they say they are not doing quantitative easing and rather doing purchases every time they take principal to keep at that level. This was major news and made headlines throughout the world, yet something just as big happened and nobody noticed; this is a forced funding of the federal debt that is just as large as what happened with QE.

“The Fed is in the process of deploying two massive stabilizers. Why are they doing this in 2016 when they hadn’t done so in 2010?”

The logical interpretation would be they are very concerned of what’s to unfold in the future. They are pre-emptively moving major stabilizers in place.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

FRA Co-Founder Gordon T. Long has an in-depth discussion on the future of Bitcoins and Block Chain technology with serial entrepreneur, Reggie Middleton. Middleton’s experience has given him the ability to recognize value, or the lack thereof, well before much of the professional populace. His ability to identify opportunity and his “out-the-box” mind-set are due to years of entrepreneurial pursuits in insurance, financial valuation/modeling, technology, media, and real estate. He is the founder of Veritaseum and the finance and technology blog, Boom Bust Blog. Until 2011, he wrote about financial evaluation and the global financial crisis at the Huffington Post.

After graduation with a degree in business management from Howard University, he worked for Prudential Insurance and trained in the sale of financial products. Since then, he worked in the fields of financial securities and risk management. He was also a significant investor in residential real estate.

Middleton is known for making predictions about the crash of markets and large financial institutions long before they occur. Aaron Elstein of Crain’s New York Business said “Mr. Middleton has been startlingly accurate in the past. He forecast the collapse of the housing market in 2007, and in early 2008 warned of the demise of Bear Stearns weeks before it happened. Earlier this year, he said that Ireland’s finances were in terrible shape long before Standard & Poor’s got around to downgrading that nation’s credit rating.”

In 2007, he founded Boom Bust Blog, a commercial financial advisory reported to have over 3000 subscribers. In February 2013, he won CNBC’s first-ever stock draft competition, beating out six other professional traders. He then went on to win the second CNBC stock draft in 2014 by an even larger margin, beating out all other professional participants.In 2014, he founded his current venture, Veritaseum, the progenitor of UltraCoin technology. According to Mr. Middleton, UltraCoin exploits modern cryptography in the fields of finance, economics and value transfer to disintermediate legacy financial institutions such as Wall Street banks.

THE EUROPEAN BANKING SYSTEM

“The problems from 2006-2009 are the same problems we have now.”

I call it the great global macro experiment. Authorities attempted to do things they have never done before. Things such as negative interest rates and particularly QE which was a practise adopted from the Japanese. It is important to note that Japan began QE within their economy 30 years ago and still to this day the desired results from it have not been achieved; Japan is still fighting inflation.

“Central bankers believe that if they prolong the problem long enough they can export their economic problems to other countries, not realizing that it is a global economy.”

The way it works is, we have a bubble; and a bubble is defined as an instance when prices shoot above the fundamental value of the good or service. Once this bubble pops and instead of allowing a natural reset of prices and value, instead people try to further push prices up.

Blockchain Technology

“It is essentially bitcoin revamped with a different name.”

Bitcoins underlying foundation is essentially a new way of dealing with databases. It is a database that is distributed amongst many individuals. In essence it is a database run by 3 million machines which each shares a full copy of the database and each having full functionality of the database.

With this much territory, you get a system which cannot be taken down by a single or even multiple authorities. In addition it solves something called the “double spending problem” which is the risk that a digital currency can be spent twice.

Double-spending is a problem unique to digital currencies because digital information can be reproduced relatively easily. Physical currencies do not have this issue because they cannot be easily replicated, and the parties involved in a transaction can immediately verify the bona fides of the physical currency. With digital currency, there is a risk that the holder could make a copy of the digital token and send it to a merchant or another party while retaining the original.

This was a concern initially with Bitcoin, since it is a decentralized currency with no central agency to verify that it is spent only once. However, Bitcoin has a mechanism based on transaction logs to verify the authenticity of each transaction and prevent double-counting. Bitcoin requires that all transactions, without exception, be included in a shared public transaction log known as a “block chain.” This mechanism ensures that the party spending the bitcoins really owns them, and also prevents double-counting and other fraud. The block chain of verified transactions is built up over time as more and more transactions are added to it.

“The bitcoin and block chain technology now parallels what the internet was in 1993. Most people didn’t get it and if they did get it they strictly thought of the internet as email; fast forward and look where we are now with the internet. Bitcoins and digital currencies are a way of transferring value.”

INDEPENDENT GLOBAL BANKING

Certain strong regimes such as the US, Germany and Britain have attempted to impose their limitations. An example would be the US with peer-to-peer file sharing halting the activities of The PirateBay. This was possible because it was a centralized server which was easy to target. But now we are in an environment that has similar things with millions of hubs and files are transferred in a huge web. This is near impossible to take down therefore the law was broken and governments and authorities resorted to illegal means to halt these new developments, it is unclear still as to how successful they were.

“It is about adapting to paradigm shifts. History shows that entities that fight or prevent these shifts will not be successful and eventually be forgotten. Microsoft is a good example of a top tier company which sustained two paradigm shifts and this was because of all their patents and so much of the world using their services.”

The banks are taking bitcoin technology and trying to incorporate it into their business models. It will make many processes faster but at the same time, you do not need banks to make transactions anymore. Therefore no matter how much more efficient banks become, if they become obsolete than the increased efficiency is of no good.

“The banks are following the same route with banking as AOL did with the internet. Ultimately the end result will be no different as well.”

If you charge a correct risk payment for capital, a bank could never get big enough to take down the world because it wouldn’t be able to afford to take that risk. If I can get money at 75 basis points then I would take all the risk in the world and if I mess up I only have to pay 75 basis points; there is no reason not to take risk. But if I paid 18-25% for that money I would become far less risk averse.

“Bring back true fundamental market analysis, natural market economics and the system solves itself.”

FUTURE OF BITCOIN AND BLOCKCHAIN

At the end of the quarter we are launching an HTML client which allows you to hold assets in your device on a webpage. It is like having a bank account on a webpage that sits on your device and it cannot be stolen unless it is stolen from you directly.

Additionally we will be launching applications of block chain technology to capital markets. We plan to have applications for credit, peer-to-peer swaps and for real estate transactions in beta of md-year but definitely by year end.

There are legal issues but we can get passed these issues by putting actual cash within the block chains. It will increase the efficiency to facilitate cash flows from various kinds of investments. It is a way of eliminating banks from the equation.

Abstract written by, Karan Singh

Karan1.singh@ryerson.ca

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/22/2016 - Graham Summers: 2008 was just a warm up for what is ahead!

Graham Summers is the Chief Market Strategist with Phoenix Capital Research in Washington, DC. Phoenix capital research is an investment research firm, that has clients in 56 countries around the world, specializing in investment research on a subscription basis.

Japan‘s NIRP announcement & the US$

Japan is at the forefront of the Keynesian central planning that has been in the markets for the past few decades. The federal reserve first went to ZIRP and launched quantitative easing in 2008. The European central bank went to ZIRP and they launched QE in 2015. The bank of Japan first went to ZIRP in 1999, in which they then launched quantitative easing in 2000. They’re much more experienced in seeing what these sorts of policies can accomplish.

A week or two before NIRP was announced, Kuroda, the head of the Bank of Japan announced that Japan’s potential GDP growth was 0.5% or lower, which is an astounding admission, implicitly admitting that no matter how much money is printed or what monetary policy will be used, Japan’s GDP will not and cannot break above 0.5%.

Graham states, “From a psychological perspective, this is like a central banker saying, ‘we don’t have the tools required to generate economic growth’ – Similar to a doctor saying, ‘no matter how much medicine you take you won’t possibly get better’.”

That was the beginning of the end. “It wasn’t too surprising for me that shortly thereafter when the Bank of Japan went to NIRP, the market reaction was terrible. When you reach the end game for central banking omnipotence, there are no longer positive results from central bank policy.”

“Anytime you cut interest rates, or launch quantitative easing, there will always be negative as well as unintended consequences. The one positive consequence since 2008 is that when these policies are launched, stocks go up” “None of these policies really generate economic growth, they’re all about the bond bubble”

Graham mentions that when Kuroda launched NIRP, the positive consequences of that policy which is the Japanese stocks rising, only lasted one day. The negative aspects exist, and Japan has since had to cancel a bond auction due to a lack of interest, which in Japanese history, has never happened. Meaning that Japan was not able to sell it’s debt on the markets because investors did not want to buy bonds at a negative yield. “When the crisis hit in 2008, all central banks coordinated their responses, however, this was in a fiat world, where everything was relative. All the policies consisted of currency debasement, with the idea of inflating away debt payments.” The problem with this is that when any one country launches any policy, it has an adverse effect on the currency against which their currency trades. The most obvious example being the euro vis-à-vis US federal reserve and the dollar. The euro represents 56% of the value against which the dollar trades, if the ECB does anything to push the euro down, the dollar would naturally go up. The bank of Japan and the European Central Bank employing NIRP, should be very dollar positive. However, for years hedge funds have been betting very large leveraged sums that are shortening the yen and going long on the Nikkei, when the Bank of Japan implemented NIRP and the negative consequences occurred, that trade began to surge, as did the yen, and the Nikkei collapsed. What this has done is forced very many institutions and hedge funds to liquidate their positions.

“We are seeing the yen soaring and the dollar is falling as a result. That is not based on any fundamentals, that is just liquidity sloshing around the system. From a global perspective, what the bank of Japan did should be very dollar positive and I believe it will be proven to be the case”

“We are in such a central planning oriented world that what has been driving markets in the short term is perspective on what central banks are going to do.”

An Imploding Bond Bubble

The bond bubble is the bedrock of the financial system, it is over $100 Trillion in size, and is going to take years to deflate. The first wave of deflation was the high yield bond market, which has begun to implode. It will also feature emerging market corporate debt defaulting. Slowly, one by one each foot will fall until we will reach the sovereign bond default but it will take months, if not years.

“Oil experiencing a 60% price collapse in about a 6 month period in 2014, was really the bond bubble, the junk bonds in the energy sector blowing up. The bubble we’re dealing with right now is the crisis to which 2008 was the warm-up, and it will take much longer to unfold than people think.”

Gold

Gold was in a bit of a bubble in 2011, it was so far overextended above it’s overall bull market trend line, it was bound to collapse. When that collapse is combined with central bank manipulation and the effort to suppress gold, you’re going to see an asset class struggle for years to find it’s legs again.

Since China devalued the Yuan in August – September, gold has begun to outperform stocks. Since Japan went to NIRP this process has accelerated dramatically. It appears for the last 6-7 years, investors were loading into stock as a hedge against central bank policy, and gold would also benefit from this. This trend reversed in 2011, investors continued to use stocks as a hedge against central bank policy, but they abandoned gold. That seems to have reversed, investors are now moving into gold as a hedge against central bank error and stocks are suffering. The reason gold is having such a dramatic move is that the gold market is so much smaller than stock, that when you start seeing large scale chunks of capital moving into gold, the movements become very significant.

Custodial Risk

Graham explains that custodial risk is the question of what an individual actually owns. He uses the example of buying stock and how individuals no longer receive a paper certificate, and the assets are held digitally, usually in a broker’s account. If the financial institution who is sitting on these assets for you, goes out of business, what are people to do with their money? Graham illustrates that gold and physical cash is so appealing due to the lack of custodial risk.

“Central banks hate physical cash because the custodial risk does not exist”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/19/2016 - Leo Kolivakis: Financialization is causing Inequality, which is limiting aggregate demand growth!

Gordon T. Long, Co-Founder for the Financial Repression Authority, interviews Leo Kolivakis, Publisher and Editor of the Web Site “PensionPulse.blogspot.com“. Mr. Kolivakis is an independent senior economist and pension and investment analyst with years of experience working on the buy and sell-side. He has researched and invested in traditional and alternative asset classes at two of the largest public pension funds in Canada, the Caisse de dépôt et placement du Québec (Caisse) and the Public Sector Pension Investment Board (PSP Investments). Also Mr. Kolivakis consulted the Treasury Board Secretariat of Canada on the governance of the Federal Public Service Pension Plan (2007) and been invited to speak at the Standing Committee on Finance (2009) and the Senate Standing Committee on Banking, Commerce and Trade (2010) to discuss Canada’s pension system.

You can follow his blog posts on Bloomberg terminal and follow Mr. Kolivakis on twitter @PensionPulse where he posts links about pension and investment articles.

In this 45 minute video interview Leo Kolivakis discusses the importance of a good pension system with strong governance being critical in insuring the average persons retirement security. Pension liabilities are going up while bond yields are going lower which is going to create a huge amount of stress on pensions!

Contributory Pensions and 401Ks have proven to be a failure compared to Defined Benefits programs. History will eventually show that the transition from Defined Benefits to Contributory Benefits was in fact is detrimental to the global economy.

Structural Issues

Leo Kolivakis believes we have entered a period of long deflation due to six major structural issues:

The global jobs crisis

Aging demographics

The global pension crisis

Rising inequality

Technological Advances

High and unsustainable debt all over the world

Each of these structural factors is significantly contributing to global deflation. Together they are a domino effect, exacerbating deflationary headwinds in the world. They are causing rates to remain ultra low and will continue to for years to come .

Rising Inequality

What is not understood and fully appreciated by economists is how the dramatic rise in inequality brought on by low interest rates is limiting aggregate demand growth.

Investing in an Era of Low Aggregate Demand

Bond yields are going lower to negative and you must prepare for a lower returns, for a very long time

Question: If rates remain ultra low, won’t that be good for residential and commercial real estate?

“Not necessarily. If deflation becomes entrenched, low rates will exacerbate debt and increase unemployment at the worst possible time. It can easily spiral into a debt deflation crisis and you’ll see rising vacancy rates and/ or declining rental rates.In this environment, real estate is the asset class that makes me most nervous.”

But it’s not just real estate that will suffer if deflation becomes more entrenched.

“All asset classes will exhibit a prolonged period of low or negative returns except for…good old nominal bonds!”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/19/2016 - Dr. Marc Faber: “They Will Bankrupt the World!”

Dr. Marc Faber joins FRA Co-founder Gordon T. Long in an exciting discussion of monetary malpractice, negative interest rates, the influence of current geopolitical risk and much more. Dr Marc Faber was born in Zurich, Switzerland. He went to school in Geneva and Zurich and finished high school with the Matura. He studied Economics at the University of Zurich and, at the age of 24, obtained a PhD in Economics.

Between 1970 and 1978, Dr Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. Since 1973, he has lived in Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In June 1990, he set up his own business, MARC FABER LIMITED which acts as an investment advisor and fund manager.

Dr Faber publishes a widely read monthly investment newsletter “The Gloom Boom & Doom Report” report which highlights unusual investment opportunities, and is the author of several books including “ TOMORROW’S GOLD – Asia’s Age of Discovery” which was first published in 2002 and highlights future investment opportunities around the world. “ TOMORROW’S GOLD ” was for several weeks on Amazon’s best seller list and is being translated into Japanese, Chinese, Korean, Thai and German. Dr. Faber is also a regular contributor to several leading financial publications around the world. A regular speaker at various investment seminars, Dr Faber is well known for his “contrarian” investment approach. He is also associated with a variety of funds and is a member of the Board of Directors of numerous companies.

JAPANESE NEGATIVE INTEREST RATES AND THEIR GLOBAL IMPLICATIONS

“It’s an experiment by few mad professors that occupy senior positions in central banks.”

Over the last 5000 years of recorded human history, interest rates have never been as low as they are now. The time value of money is the natural state. It is the markets way of pricing today’s money and the future’s money. The higher the uncertainty of future money is, the higher the rate of interest will be. What central banks are doing at the present is incomprehensible to me, unless it means an expropriation of money.

The central banks in their madness believe this will result in economic growth. But in reality it will force people to become insecure. For example if you received 6% on your money, and then rates become zero and in this case become negative which in other words you’re being penalized for your deposit. Does that rate make you save more or spend more? One thing I will never understand is despite us having democracies, somewhere, somehow, the system has given so much power to a bunch of well understood, unelected academics and most of them have never worked for the private sector for a day. The Fed, Bank of Japan, ECB are all likeminded people; they all believe money printing boosts economic activity and tight money is negative.

“They will bankrupt the world.”

We do not know how badly it will end, but an interesting thing to note is if you look at the 2008 financial crisis, which sector got the most bailout money? It was the banks and the fund managers. Then you look at the performance of their stocks, it is a disaster. Bailout money and money printing doesn’t help at all. In fact it has made matters worse for the average American. I side with Americans who support Bernie Sanders because he is expressing the views of ordinary people that the Wall Street guys and the banking lunatics have essentially cheated the people.

“In every instance where they have negative interest rates, the exact opposite of the objective occurs.”

This view of central banks to distort the free market and capitalist system is a view of the paternalist; some people that think they know better. They think they can steer the economy like how you would drive a car.

FED RAISING RATES

“As a working man it is hard to believe the world has handed so much power to a bunch of ignorant and arrogant people.”

Firstly Janet Yellen was the president of the San Francisco Federal Reserve which is in charge of California, Arizona, Nevada and another state. In her district we had the biggest real estate bubbles ever. Now she is the Fed chairman and slashed interest rates. We have had eight years of zero interest rates, and now she increases it by a quarter of a percent which is meaningless. She should have increased rates when there was a strong recovery in 2010 and 2011 but she waited. She waited right until the world is entering a very deep recession. She will go down and have a front portrait in a museum as a central bank failure.

IMPLICATIONS OF MONETARY MALPRACTICE

“There are reasons to believe that central banks will go bust.”

Systemically I think they have allowed the debt level to expand, particularly they have allowed government credit to expand as a percentage of the economy. You have to understand that when you try to supress individual risks in a system, eventually you end up with systemic risk. We will eventually have a huge crisis and investor will not know how to deal with it.

People like Bernie Sanders are not blaming the Fed, they are blaming Wall Street. In other words they are blaming rich people for the hardship or ordinary people. The Fed essentially threw money at Wall Street and naturally they kept it for themselves. Yes, there is a trickle-down effect which makes them give their waiter a slightly larger tip; it is insignificant.

ISSUES OF CURRENT GEOPOLITICAL RISK

“Everything the US touched in the Middle East and Central Asia, from Afghanistan to Iraq, Syria, Egypt and Lebanon, it all turned into a complete disaster.”

The Neocons had this brilliant idea to start making trouble in Ukraine, not understanding it is Russian territory and historically until the early 20th century Ukraine was part of Russia. Also not understanding that Crimea is of huge strategic importance to Russia, just like what California is to the US. Russia will never give up Crimea, I can promise you that. This is because it is a warm water port and they need it to have the access to the Mediterranean, without it they are at the mercy of America.

The Europeans are equally as incompetent. Angela Merkel just follows the US without understanding she is hurting the business interest of Germany. Russia and Germany were historically, culturally and politically very close. The interventions are very poorly thought out.

In the case of China, it is the second largest economy in the world with a population of 1.3 billion people. It is a highly advanced economy, especially in defense technology. A pivot to Asia by the US is seen by the Chinese as an aggression. It is a threat to the sovereignty and security of China which has created another set of geopolitical tensions.

FEAR OF A COLLAPSING PETRODOLLAR

Under Mr. Greenspan the central bank enjoyed a lot of prestige. He had done better than his predecessors; his only major mistake was deliberately creating the NASDAQ bubble.

“However, Bernanke and Yellen are complete chaos. I don’t actually believe that they make the decisions; they are told by someone what they should do.”

It is difficult to tell what people think but if you look into the Japanese negative interest rates, the intention was to weaken the Yen. Not that the weak currency helps anyone, but by slashing interest rates and having them below zero 10yr Japanese bond will cause you to lose money unless the Yen appreciates. The idea was to have negative interest rates cause the Yen weaken but it actually strengthened.

INVESTMENT OPPORTUNITIES IN ASIA

The area of Indochina is a boomtown. Not Thailand but Cambodia exports are rising at about 20%/annum. Vietnam has huge inflow of foreign direct investment, partly because the Taiwanese, Koreans and Japanese can invest in Vietnam and produce goods there.

There are a lot of investments coming from China and South East Asia. The US is afraid of China gaining too much influence in that part of the world so they waste money there by trying to displace the Chinese. The Chinese will go to Cambodian government and say they are going to make a road or a bridge and in 6 months it will be built. Whereas the US will send a team of useless characters to go check out the scenery then come back in 3 months to check out more scenery and 5 years later nothing will have been done. All the while in this time the Chinese will have built roads, bridges, tunnels and all kinds of infrastructure.

ADVICE FOR INVESTORS

“My advice is to have a diversified portfolio. You have to have some equities, some bonds, real estate and precious metals.”

In my view it will not end well. This era of artificially low and market distorting interest rate structure will end terribly. There is a popular notion now of ‘sell everything’ but this is a flawed idea. You sell everything and you have all this money now, what will you do? Deposit it in banks? What happens when the bank goes bankrupt? In practise it is very dangerous to have all your money with one bank.

Abstract written by, Karan Singh

Karan1.singh@ryerson.ca

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/10/2016 - Felix Zulauf talks Financial Repression & Warns of What is Ahead

FRA Co-founder Gordon T. Long recently interviews Felix Zulauf, Founder and President at Zulauf Asset Management AG.

FELIX ZULAUF has worked in the financial markets and asset management for almost 40 years. He started his investment career as a trader for a large Swiss Bank and received training in research and portfolio management thereafter with several leading investment banks in New York, Zurich and in Paris. Felix joined Union Bank of Switzerland (UBS), Zurich, in 1977 and held several positions over the years including managing global mutual funds, heading the institutional portfolio management unit and at the same time acting as the global strategist for the UBS Group. After two years with a medium-sized Financial Organization as a member of the executive board, he founded his wholly owned Zulauf Asset Management AG in 1990, allowing him to independently practice his own individual investment philosophy.

Mr. Zulauf focused on macro and strategic issues within the firm. In spring 2009 Zulauf Asset Management was split in two parts and Felix Zulauf fully owns the split-off Zulauf Asset Management AG focusing on some advisory activities to selected family offices and institutions including a US based global macro fund. Felix Zulauf always believed that the world economy and the financial markets move in cycles. That has helped him avoiding all the major casualties in the financial markets since the 1973/74 bear market in equities. He has been a member of Barron’s Roundtable for over 20 years.