12/18/2015 - Bill Laggner: Corporate & Sovereign Bond Defaults To Send Shock Waves Into The Currency Markets

Bill Laggner is the Principal and Co-Founder of Bearing Asset management in Dallas, TX. Mr. Laggner and his partner manage the Bearing fund using an Austrian School of Economics lens in terms of identifying boom-bust cycles, value in the market place, bubbles, and distortions created by both fiscal and monetary authorities.

“We started back in 2002, creating the Bearing credit index when we say that authorities would not let the recession play out”

On describing the Austrian School of Economics, Bill says that Austrian economists would categorize their theory as human action and individual decision making and their responsibilities of those decisions being what really creates normal economic activity. He points out how unfortunate it is that today we have fiscal and monetary intervention which distort human actions.

“We create these boom-bust cycles that are magnified by the very interventions that we’re witnessing today”

SAVINGS & PROPER ALLOCATION OF THOSE SAVINGS

Bill thinks that one of the key aspects of the Austrian economic theory that investors should pay attention to is that one has to have savings and a proper allocation of those savings. He also says that people have to quantify both risks and return as well.

“In that environment as well, you would want interest rates to be set by the market place and not a group of bureaucrats who are essentially socializing credit”

On whether we have an inflation or deflation right now: There is a lot of discussion about inflation in the Austrian theory in terms of the phenomena comes about in terms of pricing, in light of that we have deflation in commodity prices which was a function of the excess supply created by false signals coming out of China. According to Bill we are facing a deflationary state as of right now.

Bill thinks China and Glencore are the canaries in the coalmine when it comes to credit cycles in the commodity market.

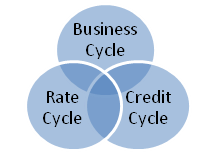

CREDIT CYCLE HAS TURNED

Gord states that the credit cycle is now changing, taking its signals from the business cycle. Bill agrees with Gord, saying:

“We’re at the end of the credit cycle, the whole mal-investment in shale oil…tens of billions of dollars in lost wealth”

For the future, Bill anticipates a massive series of defaults, resulting from huge deflationary pressures and a tightening by the market place, which is basically an unintended result of constant intervention. We are looking at corporate bond defaults, sovereign defaults which will send shockwaves into the currency system.

“We’re probably looking at some kind of new currency system, which looks likely to be gold”

At Bearing Asset Management: They run an aggressive, long-short portfolio.

Bill points out even in the turmoil we’re in he remains optimistic. He thinks that technology will be the savior as the wheels are coming out from the bus, looking at how the internet connects people all over the whole who do business daily.

“We’re coming to a realization that we can look to each other and share expertise, knowledge, goods and shy away from things like speculating in commodities, speculating in real estate, speculating in the stock market and get back to pricing money correctly.”

“The beauty of America is that the entrepreneurial DNA in this country is unlike any other part of the world.”

Gord mentions that if we could take away centralized control and planning from the planners and controllers in a logical fashion, adjustment will happen. He says that “a crisis is nothing but more than change trying to happen.”

If people want to get more information and insight from Mr. Bill Laggner, they can go to bearingasset.com/blog. They write a lot about relevant topics relating to wealth and the financial markets.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/18/2015 - Morgan Stanley’s Ronnie Lapinsky Sax: “Interest rate normalization will provide headwind for investors using bonds for principal preservation”

QUESTION: Can you relate some of your career background in portfolio management and a general description of your investment approach?

ANSWER: I’ve been very fortunate. I’ve only had one job….and have been with the same firm since the beginning, when I turned 21, in 1976. It’s nearly 40 years of managing money for the wealthy. I strive to provide solid investment advice, high levels of service and the confidentiality clients have grown to expect. I am solely responsible for asset allocation and selection for my discretionary clients…. My niche stays within the bounds of retail, working directly with families helping them to achieve their goals. Every year, I am challenged by the change in our economic environment, the continued changes in technological advancements and how these and other factors relate to client allocations. Recently I stepped down as President of The Portfolio Manager’s Institute; Currently I serve as co-Chair of Morgan Stanley’s National Financial Advisory Council. I am proud to say that over 50 families have relied on my advice for over 25 years, some longer. By any measure, it’s been quite rewarding

QUESTION: Can you comment on your currently relating to the recent much talked about Federal Reserve policy statements and interest rate direction and how these could affect the financial markets

ANSWER:- Morgan Stanley’s Global Investment Committee supports that interest rate normalization will provide headwind for investors using bonds for principal preservation, as rates rise its likely longer duration bonds will fall. We show the total return impact of a 1% rise in rates can impact a 30 year bond by a negative 17.9%; which is tremendous. To show the range, if you own a 2 year bond a 1% rise in rates has a negative 2% impact.

– Typically after interest rate hikes the companies with the strongest balance sheets that do not rely on floating debt fare the best

– Rate hikes will likely lead to a rise in interest income on deposit which should help those with larger portions of savings in the bank

– In this environment, Morgan Stanley’s GIC expects housing, mid/lower tier retail, airlines, hotels and leisure’s to benefit. Additionally, we see value in consumer finance and regional banks as consumer confidence is boosted

– It is important to note, we see the initial tightening as a signal of self-sustainability, not the end of economic expansion.

QUESTION: What are the challenges with portfolio management for clients in today’s environment resulting from and characterized by 0% or even emerging negative interest rates?

ANSWER:

– Income more difficult to provide clients, in a zero rate environment many will suggest high yield corporate bonds and leveraged loans to supplement traditional fixed income but many clients are not willing to sacrifice quality for a higher yield.

QUESTION: Do you see any unintended asset price distortions in the financial markets resulting from an extended period of virtually 0% interest rates and from quantitative easing (QE) by many central banks worldwide?

– We found that as the cycle has matured security selection based more heavily on credit quality created dispersion in spreads and opportunities for further security selection. In addition, we see credit spreads have widened significantly creating opportunity for credit selection.6

QUESTION: What types of generic investment classes and investment approaches make sense in today’s environment characterized by very low interest rates, low yields, volatile capital markets, emerging regulations and international capital controls in many jurisdictions including the United States?

ANSWER:

– Morgan Stanley’s GIC continues to recommend equities over fixed income. Within the US we prefer technology, financials, consumer/housing related products and industrials. If you are an investor that is looking for fixed income we would recommend below-benchmark duration and find the US high yield market attractive.

– In this environment, Morgan Stanley’s GIC expects housing, mid/lower tier retail, airlines, hotels and leisure’s to benefit. Additionally, we see value in consumer finance and regional banks as consumer confidence is boosted

QUESTION: Do you advise international and geographical diversification to your clients and if so how can this be factored in to the investment process?

ANSWER:

– While personally I do not have a large diversification to international it is definitely a theme you are seeing in today’s investment sphere.

– Europe is getting the support from the ECB with quantitative easing and the GIC expects European equities to continue outperforming in 2015.

Additional Commentary

– Lower energy prices help drive increase in consumer spending despite weak wage growth in 2014. Lower unemployment levels should lead to stronger wage growth going forward

– bullish on housing – We see US consumer confidence at an eight-year high based on the University of Michigan, Consumer Sentiment Index supporting the strength of the middle class and US economy going into 2016.

The individuals mentioned as the Portfolio Managers are Financial Advisors with Morgan Stanley participating in the Morgan Stanley Portfolio Management program. The Portfolio Management program is an investment advisory program in which the client’s Financial Advisor invests the client’s assets on a discretionary basis in a range of securities. The Portfolio Management program is described in the applicable Morgan Stanley ADV Part 2, available at www.morganstanley.com/ADV or from your Financial Advisor.

Ronnie Sax is a Financial Advisor with Morgan Stanley Global Wealth Management in Bethesda, MD. The information contained in this article is not a solicitation to purchase or sell investments. Any information presented is general in nature and not intended to provide individually tailored investment advice. The strategies and/or investments referenced may not be suitable for all investors as the appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/16/2015 - Yra Harris: Read “The Rotten Heart of Europe”!

Yra Harris: Read “The Rotten Heart of Europe”!

FRA co-founder Gordon T. Long deliberates with Hedge Fund Manager, Yra Harris about the effects of financial repression and the imminent credit event. Harris is a macro Global Trend Trader and publisher of the Blog Notes From the Underground.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator.

Yra Harris is a recognized global trader who is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

FINANCIAL REPRESSION

“The way governments repay the interest on their debt.”

When governments borrow money, they do not want to pay back the money at any real market rate, instead they artificially hold rates down to pay off creditors. It is about the size of the government debt and being able to debase it; pay it off in less value.

“Financial repression has led to serious inequalities.”

It begins with Tim Geithner, bailing out Wall Street and banks as opposed to bailing out main street. Financial repression has focused its effects on the savers, the people who have been saving for retirement are being seriously damaged and forced to go into the stock market.

A recent paper, The Hidden Cost of Zero Interest Rate Policies by, Thomas Coleman and Laurence Siegel report “Zero interest rates cost $5 trillion per year, or rather 5% of GDP from savers that is being transferred to other entities.[1]”

“When there is too much debt, all financial authorities have a chief goal, and that is to create inflation.”

Many people have called Geithner out on his ill-advised actions. Everybody fell in line with the ‘you have to protect Wall Street’ way of thinking, and to a certain degree that is true. The first QE was mandatory because you had to prevent the mass liquidation of assets. The lessons from the 1930s boldly taught us that the US cannot take such an immense liquidation of assets. People need to begin equating what is the real return on their money, which is the true financial repression because all zero interest rates do is culminate into inflation; the best friend of debtors.

FUTURE RAMMIFICATIONS WITH THE FED

“The French are tired of being ‘Germanized’”

The proof will be what will happen in the yield curve. If the curve were to flatten further the equity markets will retaliate. What the yield curve does, what the dollar does and finally what gold does when the Fed raises rates will be the three indicators we must keep an eye on.

Is it going to be the German euro or the French euro? Germans are hard money advocates because they are savers, and right now what is happening in Europe is the ultimate financial repression. German savers are being severely hurt in order to bail out the rest of Europe. The euro was at 82 cents in 2001 and 2002 because the Germans needed a weak euro in order to get all the labor reforms that were being put in place. They played this card upon the ECB and they got what they wanted.

THE IMPENDING EVENT

“There is something right now eating at the debt markets. It may be in the mining or energy sector, but this market right now is scared of some credit event that it lurking out there.”

There is a credit event somewhere going on, it is evident by how the markets are acting. What is dangerous is that it is taking place now, during the holidays and anything that happens will therefore be magnified. The stock markets are off, if you look at the coordination of them, they are all out of place.

The Fed is aware of this so they must ask what it is that they are not seeing. I will not be surprised if come this Wednesday, they will not raise rates. If the Fed does not raise rates on Wednesday, the stock markets will have a high sell off because people will think what it is that the Fed knows.

Richard Cue has done great work, he has recently written about recent debt developments throughout the world. The debt structure which is supposed to be handled hasn’t been dealt with at all, and the greatest error you can make; borrowing to buy back your stock.

As soon as corporation free cash flows starts to erode, that debt becomes a major issue. We have had a run on this fictitious financial engineering of buybacks that will boomerang and it may be violent. There are symptoms of debt overhang, and global slowdown will reveal to us the weak players that took on too much debt.

[1] Thomas Coleman and Laurence Siegel. The Hidden Cost of Zero Interest Rate Policies, Sept 28 2015.

Subscribe to our Youtube Channel to watch our Program Show – click on the red Youtube button to subscribe:

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

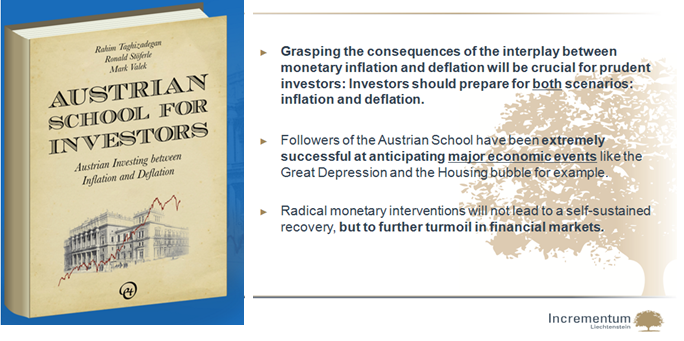

12/11/2015 - AUSTRIAN SCHOOL FOR INVESTORS with Ronald-Peter Stöferle

FRA Co-Founder Gordon T. Long discusses the Austrian School of Economics with German Finance bestselling author, Ronald-Peter Stöferle. Ronald is a Chartered Market Technician (CMT) and a Certified Financial Technician (CFTe). During his studies in business administration and finance at the Vienna University of Economics and the University of Illinois at Urbana-Champaign, he worked for Raiffeisen Zentralbank (RZB) in the field of Fixed Income/Credit Investments. After graduation, he participated in various courses in Austrian Economics.

In 2006, he joined Vienna-based Erste Group Bank, covering International Equities, especially Asia. In 2006, he also began writing reports on gold. His six benchmark reports called ‘In GOLD we TRUST’ drew international coverage on CNBC, Bloomberg, the Wall Street Journal and the Financial Times.

He was awarded 2nd most accurate gold analyst by Bloomberg in 2011. In 2009, he began writing reports on crude oil. Ronald managed 2 gold-mining baskets as well as 1 silver-mining basket for Erste Group, which outperformed their benchmarks from their inception. In 2014 he published a book on Austrian Investing, Austrian School for Investors – Austrian Investing Between Inflation & Deflation.

AUSTRIAN INVESTING BETWEEN INFLATION & DEFLATION

“For an investor it is critical to understand we are not in a cyclical crisis; we are in a systemic crisis.”

Well I have to admit I am not an economist which is why I am open to the Austrian school of economics Complex econometric models that try to forecast future models simply do not work, the 2008 financial crisis is an example of that. The Austrian school of economics simply described is “common sense economics.”

As a practitioner we are writing about the theory of the Austrian school of economics. It is a book dedicated to the practitioners of the Austrian school. What I want to point out is that the Austrian school has a completely different view when it comes to inflation and monetary systems.

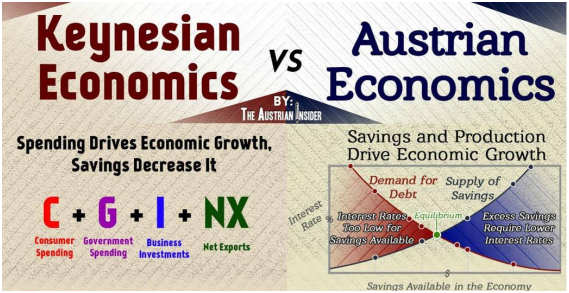

For Keynesian economists inflation is simply a rise in prices. There is no point in discussing the details of inflation, however for Austrian economists it is an increase in the money supply.

The Austrian school shows the new monetary system which began august 1971, when President Richard Nixon suspended the convertibility of the dollar into gold. Since this was done we have seen major misallocation of capital.

“This interplay between inflation and deflation is crucial to understand, this refers to the term, monetarytectonics.”

“If you have an Austrian mindset, you have a great advantage.”

You are able to understand other currencies, thinking outside the fiat money system and as an investor focus on the real results not the nominal results you make.

THE CHANGING CREDIT CYCLE

“In 2016, we very well may face a recession.”

For an Austrian a recession is something that’s normal, it is like a fitness program that prepares the economy for the next stage up. Trying to avoid such a recession will be difficult as QE, fiscal stimulus, monetary stimulus and low interest rates only make the situation more severe.

“The credit cycle leads the business cycle and therefore the fed will have a hard time fighting this falling trend in economic activity.”

To fight against it, negative rates in the US might be implemented. Many academic studies in the US say that evidence from Europe shows that negative interest rates work. The Fed may very well consider implementing negative interest rates. We will see increasing fiscal stimulus. There are many voices saying we should introduce helicopter money, but rather is it now called The People’s QE.

INVESTING ADVICE FROM THE BOOK

To have a nonfragile portfolio, and investing in your own skill set offers a great yield.

A good investor separates from a bad one in times of crisis.

Become an entrepreneur, the Austrian school greatly encourages entrepreneurship.

The Austrian school is very modest in saying we cannot predict the future but be prepared for all scenarios.

It is highly recommended to read Austrian School for Investors – Austrian Investing Between Inflation & Deflation. Many people have interpreted it as a philosophical book that attempts to cultivate and establish this Austrian mindset. It is a pragmatic school of thought which offers great benefits if implemented, and this book is the perfect guide to it.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/10/2015 - PROF. THOMAS COLEMAN & LARRY SIEGEL: The Hidden Cost of Zero Interest Rate Policies – $1 TRILLION or 5% per Year Taken From US Savers

FRA’s Co-Founder Gordon T. Long interview Thomas Coleman and Larry Siegel on their paper, The Hidden Cost of Zero Real Interest Rates. Thomas Coleman is the executive director of the center of economic policy at the University of Chicago Harris School of Public Policy and has spent most of his career in the financial industry mainly in research, trading and model development for derivatives and trading other fixed income derivatives. Larry Siegel is the research director at the research foundation of the CFA institute and also the senior advisor at Ounavarra Capital. He is also an author and public speaker.

$1 TRILLION or 5% per Year Taken From US Savers

On financial repression Larry describes it as the use of market prices, in particular interest rate to transfer resources from party A to party B in this case from savers to government. According to him the government can then borrow at rates that are extraordinarily low and not a reflection of the true value of the money to the lenders.

On the paper, Thomas explains that there are 3 highlights. The First is detailed from a historical perspective. He says that from looking at history we can see that nominal rates are low by historical standards. According to him what really matters are real interest rates. He mentions that when taking into account nominal interest rate and inflation we currently have real interest rates as minus one percent. This means that the real value of saving in a zero rate deposit would be a loss in value at about one percent a year.

“Financial repression is a disastrous ongoing strategy”.

Thomas mentions that one of the costs of a negative real interest policy is that negative real rates potentially distort decision making. He explains that the real interest rate is the price that determines how much we consume or how much we want to consume, the price of consumption today versus consumption in the future and how such a policy disrupts such decisions. Thomas stresses that it is the real interest rates that matter and that one of the reasons nominal rates has gone down below zero especially in Europe is because inflation has trended lower.

“Businesses decide whether to undertake a project based on whether the return they expect to make on the project is greater than the cost of capital. If you force the apparent cost of capital low enough through a low interest rate policy a lot of projects will look good and profitable that aren’t if you applied a normal cost of capital to that product so this motivates businesses and consumers to do a lot of things they shouldn’t be doing”. –Larry

On trying to understand the wealth transfer from savers to borrowers, Thomas likens it to an implicit tax. He says that it is more than just a transfer from households to government but also from one set of households to another, from older to younger there by reinforcing the idea that negative real interest rates are potentially a distortion to the price of consumptions today and consumptions tomorrow and also what we save today versus spend today. The troubling thing with all this according to him is the potential distortions that arise as a result of a negative real interest policy.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/03/2015 - Brett Rentmeester Outlines: APPROACHES TO SOLVING YIELD CHASING & HIGH VALUATION RISKS

FRA Co-Founder Gordon T. Long interviews Brett Rentmeester on Austrian economics and the importance of having an entrepreneurial mindset in investment. Brent Rentmeester is the president of Windrock Wealth Management and has been in the wealth asset management for over 18years. Mr Rentmeester believes the uniqueness of Windrock is its focus on the macroeconomic picture, Austrian economics and what it all means for investment implications as well as an entrepreneurial mindset on how to find investment opportunities.

The Austrian school to him is the “acknowledgement of the influence that central banks have on the business cycle and interest rate and therefore the opportunities left for investment”.

He mentions that the traditional stock, bond portfolio is under a lot of challenge going forward because there is no real and safe income anywhere today. As a result people are becoming speculators and risk takers even when they don’t want to.

Brett believes having an entrepreneur mindset when investing, is the key to addressing the dilemma of income and the future of investment. Secure private lending is lending money to borrowers that is backed by real tangible assets or an income stream. According to him, what makes this a unique category is that it addresses the pockets of lending that is being neglected by the big banks as a result of the financial banking distress that took place in 2008.

On examples of secure private lending, Brett highlights 3 different categories with his examples. He explains that in auctioned rental properties, the government organizations Fannie Mae and Freddie Mac by law are restricted from buying mortgages on such properties until after 2 years, this results in a niche market for private lenders. “In energy markets more states are moving towards a deregulated market”. What this means is that a consumer can buy energy from a variety of energy companies. Now this system is facilitated by third party brokers who go door to door offering this energy from various energy companies. Now because the brokers want the commissions up front and the energy companies can’t provide it, we see people coming in to pay the brokers a discounted fee upfront and then agree to collect the 3year contract provided by the energy companies.

Trade financing

“Global trade happens between different parties but often times it’s financed by big banks, trade receivables. So one party needs to buy goods and a supplier supplies them but someone’s got to finance that transaction and it’s often the third party bank”.

Due to new regulations, banks are required to reserve more capital in such situations, as a result an opportunity is created for private money to finance the transaction between the customer and supplier.

“Rather than taking on more risk you don’t have to today, you just have to be more creative”

– Gordon. T. Long.

Brett echoes this sentiment saying:

“So much of the industry and investors think in a very narrow box of stocks, bonds and maybe hedge funds but there’s a lot of things outside of that, that if you open your mind to the opportunities, are quite interesting to research”.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/20/2015 - PURU SAXENA SAYS: “FINANCIAL MARKETS ARE SO DISTORTED AND SO TWISTED THAT RELIABLE INDICATORS ARE NO LONGER WORKING. EVERYTHING IS BACKWARDS!”

Special Guest: Puru Saxena – Founder and CEO Puru Saxena Wealth Management

As part of the ongoing series of Austrian School of Economics, FRA Co-Founder Gordon T. Long sits with Puru Saxena, of Puru Saxena Wealth Management. Mr. Saxena is the portfolio manager of his firm and he oversees discretionary investment mandates. He is also responsible for heading the firm’s research process and formulating investment strategy.

Mr. Saxena has extensive investment experience and he is a registered investment advisor/money manager with the Securities & Futures Commission of Hong Kong. Highly respected in the investment management business, he is a regular guest on various media such as CNN, BBC, CNBC, Bloomberg, Reuters and a host of other channels. Furthermore, he is regularly featured in several publications such as Barron’s, Hong Kong Economic Times, South China Morning Post, Benchmark magazine, Hong Kong Business and China Daily.

Mr. Saxena is also the editor of a monthly economic report – Money Matters. A highly acclaimed publication is read by professional and retail investors in numerous countries. He first began publishing his monthly economic report in June 2000 and it has now attracted a wide following. Prior to establishing Puru Saxena Wealth Management in 2005, he was a Founding Director and President of financial services firm – Bridgewater (now Tyche Group), where he oversaw the firm’s investment strategy.

LIMITING CENTRAL BANKS BALANCE SHEET GROWTH

“Financial markets are so distorted and so twisted that reliable indicators are no longer working. Everything is backwards”.

People are so conditioned now of believing the stimulus jargon that every time a central bank utters the word stimulus, everybody starts buying stocks again. If you look at japan, they have tried this for nearly 25 years now, and we have had recession after recession. There are zero percent short term interest rates, and not much economic growth in Japan. I don’t think this monetary experiment is going to end very well.

CENTRAL BANKS FUTURE ACTIONS

“I would be very weary by promises from the government and central banks at this point because they have a vested interest.”

I think they will try and inflate this in a typical Keynesian manner. We have negative interest rates already throughout Europe, so it won’t surprise me if you have it in the US.

“The problem isn’t a liquidity problem, it is a debt problem.”

The world has never been so indebted; the debt to GDP ratio is now over 280% globally. When you have this much accumulated debt, history has shown that economic growth slows down. Economic growth, by definition, comes from the private sector taking on more debt. When people borrow, they bring forth tomorrows consumption, today, and they consume without ever buying any assets.

“Whatever they’re doing, it’s not working.”

Central planners do not realize that if somebody is already in debt, they are not going to borrow anymore with interest rates at zero. We are currently in a deflationary environment. Central planners are trying to fight this by implementing quantitative easing, and all sorts of bizarre experiments. But at the end of the day the monetary velocity is at a decade low.

At some point, maybe even next year, we are going to get a recession. We are going to get a global recession which will occur at a time where interest rates at the short end of the curve are already at zero.

“Asset prices are going to deflate quite sharply and when this happens, there will be chaos.”

CURRENT MARKET MISCONCEPTIONS

“Major mistake people have is that QE works, or stimulus works.”

First one is that QE causes hyperinflation and therefore everybody drove up the prices of commodities to multi year highs. Investors still believe QE causes economic growth, I do not believe this. People think stimulus will cause economic recoveries and economic growth. When people realize stimulus actually leads to anti-growth you will see a big sell off in equities.

The one thing I’ve learned from being in this field from 16 years is that markets go up and markets go down. There is no one way street.

TO DIVERSIFY INTERNATIONALLY

“I think investors should keep a large chunk of their money in cash right now and long term treasuries are also a good idea.”

But if you’re look at a long term horizon, (i.e. 5 years+) I think investors should start looking at the beaten down commodity areas. Commodities have been decimated over the last 4 tears. If it was me I would not buy any equities right now. We personally don’t own any stocks on the long side for our clients at the present. The downside risks for many stocks is greater than their upside potential.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/20/2015 - Robert Wenzel – The Fed Flunks! My Austrian Economic Speech at the NY Federal Reserve

Special Guest: Robert Wenzel – Editor & Publisher of Economic Policy Journal.com & Target Liberty

Investing based on The Austrian school of Economics

FRA Interview of Robert Wenzel by FRA Co-founder Gordon T Long.

Across well-known literature, the Austrian school of economics has earned and put its indelible mark on the complicated world of economic analysis and theory. The school of thought varies significantly from the mainstream schools of economics like the classical, neoclassical and Keynesian schools of thought. In essence the Austrian school of thought believes in using logical thoughts to explain and solve economic problems rather than getting technical and going into mathematics to explain the same problems.

“The key to understanding is that what you have with mainstream economists is that they look at things from a very mathematical, very empirical approach… unlike in physical sciences you cannot do that for the science of economics because you’re dealing so many variables like changes and desires”

Unlike the mainstream none-Austrian economists, Wenzel believes that there’s a lot to be understood from the economy based on logical build up from solid premises. He goes on to mention that another key aspect to be understood is that Austrian economists believe that when the Fed injects money into certain sectors of the economy, it’s those sectors that turn to boom. According to Wenzel, when the Feds eventually start tightening this money supply it leads to a crash.

On the current economy:

“We’re in a period of accelerated money supply”

Wenzel thinks there could be an increase in price inflation and the possibility of another dip in the price of oil.

Explaining how we have inflation in some areas and deflation in others when we’ve been pumping money into the system, he explains it by outlining how it depends on how quickly people want to spend the money.

“if there’s a great desire to hold money, you’re not going to see the inflation right away”

When people don’t spend money what happens is you have money building up in cash balances which Wenzel terms “the desire to hold cash balances”. With this you see people reluctant to spend money and hence a low velocity of money.

On the confusing environment of economics and how understanding the Austrian school can help to clear things up …. Understanding the business cycle and inflation comes about in terms of the Austrian school of thought. It definitely helps to clear a lot of things up but even more can be taken from this approach. The methodology additionally helps out in terms of having people analyzing the world through logic rather than attacking it solely with empirical data.

On considering Quantitative easing and going into negative nominal rates …. QE is a method where the fed prints a lot of money and buys long durtion debt. The negative nominal rates idea is based on the Keynesian idea that it’s spending that helps the economy to grow, so the idea is to use negative rates to pressure people to spend their money. Wenzel calls this “a tax on holding money”.

Asked if he sees Hyperinflation in the future:

It could happen at some point. The Fed’s target of 2% could easily go up to three 3% with accelerated printing of money. At this point they might raise rates but if the inflation is at 5% and they raise rates from 12bp to 2% that still won’t be able to fight the inflation. However it may be too soon to say hyperinflation.

The business cycle should be understood as a boom and bust cycle.

“Whatever is going up now does not necessarily mean it will go up long term. The bust will occur but they will pump it up with new fed printing, which is eventually where the inflation comes in”

The infographic above shows some differences in Keynesian and Austrian views. Courtesy of The Austrian Insider.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/20/2015 - Alasdair Macleod – THE FALSE PERCEPTION OF LIVING IN A WORLD OF INFINITE CREDIT

FRA co-founder Gordon T. Long deliberates with Alasdair Macleod, head of research at GoldMoney on the Austrian School of Economics in an Era of Financial Repression.

Alasdair. Macleod began his career as a stockbroker in 1970 on the London Stock Exchange. Through experience he rapidly learned about things as diverse as mining shares and general economics, within nine years he had risen to become senior partner of his firm.

Subsequently, he has held positions at director level in investment management, as a mutual fund manager, and also at a bank in Guernsey as an executive director. For most of his 40 years in the finance industry, he has been de-mystifying macro-economic events for his investing clients. From the accumulation of his experience he concluded that unsound monetary policies are the most destructive weapon governments’ use against people.

“I want to destroy this business of printing money as the solution to everything.”

Mr. Macleod strives to educate and inform the public in layman’s terms what governments do with money and how to protect themselves from the consequences.

WHAT IS AUSTRIAN ECONOMICS

“Prices are entirely subjective.”

It began with Carl Menger who was one of the 3 economics who came up with marginal theory of prices. Where Menger differed from other two was that he appreciated that prices were purely subjective. You cannot forecast tomorrow’s prices because prices are determined by the consumer who always has the option to buy.

“It overturns the cost theory of prices which is what Adam Smith believed in. It is completely irrelevant.”

The law of the markets, the reason you and I work is we go out to earn something. We need to transform our skills into consumption. In a free market economy we have people who use their skills to earn money for consumption; the intermediary in this is money. Money is nothing more than the temporary storage of someone’s labour that is transferrable into goods. If you understand this you will see how unsound money is bad for an economy. The idea by printing money which runs a budget deficit that a government can generate economic growth is nonsense.

“In regards to investing one thing that is desperately important to understand is that asset prices always refer back to their production.”

This applies across every asset that you buy. If you see that the prices of assets have moved away from their underlining productive value then you know that you are in a bubble.

A WORLD OF INFINITE CREDIT

“The world post 1970’s is a completely different world from before the 1970s.”

After 1981 rates had been lifted to a point which stopped the relationship between businesses and savers. This is what killed the price inflation up until the early 90s. Banks not only had the liberty to print credit but also to monopolize and control securities markets, if you combine these two thongs together; it is basically a money making machine, which is what we have today.

The end point in credit comes from the logical conclusion of that development. At every cyclical peak the level of interest rates which collapse the economy gets lower. The reason it gets lower is because this combination of credit control in securities markets does nothing more than just pumps up the level of debt. The overhang of debt means the rise in interest rates to stop the economy from getting out of control is getting lower. You cannot raise interest rates by more than one or two percent without serious economic dislocation.

NEGATIVE NOMINAL INTEREST RATES

“The effect of negative interest rates would be to throw every commodity into backwardation.”

There is no doubt that negative interest would drive up inflation, or rather, it would lower the purchasing power of said currency. Negative interest rates for the reserve currency in which all commodities are priced have a severe risk which we will generate runaway inflation, but in fact it is a collapse. In order to make negative interest rates work you need to ban cash entirely. I have no doubt at all that that is the underlying reason why there is so much emphasis on anti-money laundering.

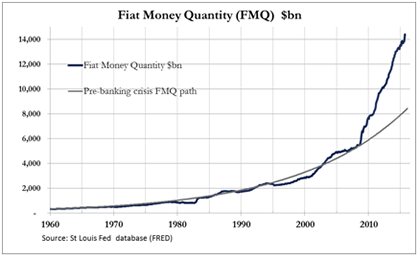

THE FMQ CONCEPT

“The fiat money quantity is the amount of money that would have to be redeemed for gold that once was deposited.”

The fiat money quantity was put together to try to quantify the amount of money that Is being issued in return for the gold that we originally gave to our banks which the banks then handed to the federal reserve.

The reason for doing this is to try to get an idea of how much money is not only in public circulation, but also not in public circulation and potentially in public circulation. From looking at the Feds balance sheet and considering other factors like repos and reverse repos, we see that the growth curve has taken off; and in the very broadest sense we have monetary hyperinflation.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/13/2015 - Round Table with Charles Hugh Smith & Rick Ackerman – What We Should Expect From the Fed

Special Guests: Charles Hugh Smith – OFTWOMINDS.COM; Rick Ackerman – rickackerman.com

Charles Hugh Smith is an American writer and blogger. He is the chief writer for the site “Of Two Minds”, which started in 2005. His work has been featured on a number of highly acclaimed sites including: Zerohedge.com., The American Conservative and Peak Prosperity.

Rick Ackerman has professional background including 12 years as a market maker on the floor of the Pacific Coast Exchange, three as an investigator with renowned San Francisco private eye Hal Lipset, seven as a reporter and newspaper editor, three as a columnist for the Sunday San Francisco Examiner, and two decades as a contributor to publications ranging from Barron’s to The Antiquarian Bookman to Fleet Street Letter and Utne Reader. Rick Ackerman is the editor of Rick’s Picks and a partner in Blue Fin Financial LLC, a commodity trading advisor.

Co-founder of The Financial Repression Authority, Gordon T. Long has an in-depth discussion on the current financial situation with Charles Hugh Smith, of OfTwominds.com and with Rick Ackerman, trader and forecaster of Rickackerman.com.

THE OUTLOOK ON QUANTITATIVE EASING

Rick:

“I’ve been shouting from the rooftops that the fed will never raise interest rates.”

If you want to find out if QE is working the first person you have to go to is the retiree. The whole idea of stimulus should have been refuted simply by the fact that savers have been cheated for so long.

Charles:

They may go ahead and do the quarter point rates increase because they have built up so many expectations to that. They will need to do this to create the allusion that the economy is recovering or else it’s robust.

Gordon:

The market may be a key driving factor, not because of the wealth effect; but because of collateral.

THE STATE OF JAPAN:

Charles:

“The Juggernaut of deflation is so huge now, that there isn’t going to be any time to react. Keep a shoebox full of cash because on that day we might wake up and the banks won’t be open, we will need that cash.”

I don’t see the possibility of massive inflation. The only viable way of getting money into the system is to borrow it into existence.

Japan, is a developed economy that has been in a deflationary setting for almost 25 years now. We can see what they’ve done and what effects it has. They have attempted to stimulate their economy by improving roads and infrastructure. But it has not worked. Japan refuses to cleanse their financial system to allow real investment so they have consequently brought in mal-investment with borrowed money.

Rick:

Japan had something over the last 20 years that we didn’t have, and that is us. Japan has a global economy to export into; we were the buyer of last resort.

NEGATIVE INTEREST RATES

Rick:

“If you can extrapolate a somehow positive benefit from negative interest rates, where would this benefit be and how long would it last?”

The idea is if people can no longer park money anywhere, they can only spend it or invest it, we have to ask, where are they going to invest or spend it? It’s inconceivable that money can find itself into somewhere in the economy that would promote growth and economic health.

Charles:

In a current example of negative interest rates we see what is happening with Sweden who is actively pursuing negative rates. The net result is that it is taking their housing bubble and inflating it even further. Basically it is pricing everybody out of housing and creating a credit bubble.

COLLATERAL GUARANTEES

Gordon:

“It is in the cards, in the middle of the next crisis.”

We have an approximately $500 trillion swaps market that is underpinned with collateral. So if bond prices were to drop it would be a horrendous situation. We were able to stop the 2008 crisis, we did not fix it we only stopped it. Now it will be a global issue, and the central banks will be forced to come in and pay attention to these collateral values. We have a huge pool of bond ETF’s that have exploded in the past few years, somebody has to sell these bonds but they are not easily transferred. The central banks will have to intervene in a massive way. I believe many people are betting on this, and are therefore taking risk adjusted positions.

Rick:

“We are really talking about a quadrillion dollar bubble.”

Much of borrowing and leveraging shifted into rehypothecation. It occurred mostly in London markets that were more unregulated than US markets. So when we had the real estate bust in 2008 we needed something to pledge as collateral.

When you look at the entire quadrillion dollar enchilada, somebody may say the actual size of the bubble is only several hundred trillion dollars. When in reality the gross amount is something everyone involved in the daisy chain thinks they have a claim on a particular asset.

Charles:

We must own real assets, and have no debt. Whatever financial wormhole we are going to go through,we must own the right tools, because the tools will still exist after we get through the wormhole.

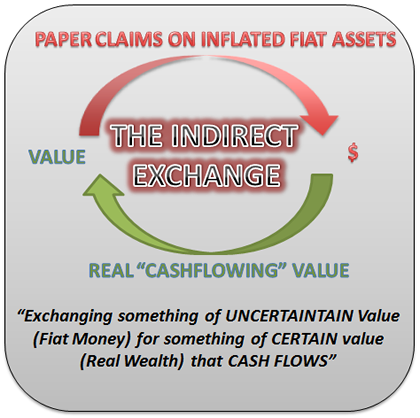

THE INDIRECT EXCHANGE:

Regarding a recent show with Warren Buffet, and Ty Andros, Editor at Tedbits Newsletter,

Warren Buffet so masterfully utilizes the indirect exchange. He takes paper, which is his entire insurance side of business and plows it back into real hard assets that will sustain themselves at a fair price. Buffet has don’t this so consistently for so many years and that is why balances; paper products (insurances, bonds, and structures against real assets). Buffet has certainly been a consistent winner without question.

Rick:

Buffet has also resisted the temptation of going after easy money. His money is not in Uber, Dropbox, and Instagram etc. It’s simple to see that it is not going to end well, not only for the companies but for the whole city, if I were to short any city in this country it would be San Francisco. Everything is so pumped up in that city because there are companies that hire these people that are extremely overvalued.

Buffet has demonstrated amazing restraint and discipline for sticking with the nuts and bolts, instead of going after the alluring high attraction companies. He has found real businesses with real products that have a sustaining capability to survive during good times and bad.

Charles:

Raising the issue of risk, how do we deal with the kind of systemic global risk that we currently have? Risk is extremely misrepresented to the average middle class American. We are trying to help people make a realistic assessment of the global risk they are engaged in by having a 401k that is involved in these risky financial assets.

CLOSING REMARKS

Rick:

“You can’t look at what’s in prospect as hypothetical, if you don’t think there is going to be a collapse then you don’t understand the problem.”

There is no way we can continue to muddle on, for one its taking a lot more debt to create the dollars’ worth of GDP growth at the margin. We are really going to face a day of reckoning. The most important thing is for us to be resourceful and ready for when it comes.

Charles:

“This enormous supernova of debt is going to implode and whatever is left will not be a financial instrument.”

Gordon:

“Crisis is nothing more than change trying to happen.”

We have so many global imbalances. We have political, economic, and financial systems that are not correct, we are still running from a Bretton Woods; post WWII model. And during this process, mal-investment, lack of price discovery and mispricing are rampant.

But on the flip side, for those who have prepared themselves for this storm, I think the world is going to see its greatest years. The advancements in technology, and so many other endeavors is staggering. !5-25 years out will be an incredible time for the world but meanwhile we are going to go through some rough times, but there will be winners and there will be losers, and the winners are always the ones who prepare.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/31/2015 - Ty Andros – The Austrian School of Economics Uses the “Indirect Exchange” to Capture Real Wealth

Special Guest: Ty Andros – CIO Sanctuary Fund, Publisher of “Tedbits”

FRA Co-Founder Gordon T. Long deliberates the Austrian School of Economics with Ty Andros of Tedbits Newsletter. Ty Andros began his commodity career in the early 1980’s and became a managed futures specialist beginning in 1985.Mr. Andros attended the University of San Diego, and the University of Miami, majoring in Marketing, Economics and Business Administration. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis.

WHAT IS AUSTRIAN ECONOMICS?

“Austrian economics is just human behaviour, and common sense, and history.”

“But what’s happening is human behaviour, nonsense, and history. We are at a period where people have forgotten history and are doomed to repeat it. “

“Austrian school and capitalism are one in the same.”

“Austrian Economics is production of wealth, producing more than you consume. Meeting people’s needs and doing it in a superior manner; in other words, capitalism.”

The historical school, had argued that economic science is incapable of generating universal principles and that scientific research should instead be focused on detailed historical examination. The school thought the English classical economists mistaken in believing in economic laws that transcended time and national boundaries.

APPLYING AUSTRIANISM TO INVESTING

“You have to prey on paper.”

“The only real way the middle class will get to success is going out serving others and getting rewarded for it.”

“Austrian school is just history, common sense, and the production of wealth; everything else will flow from there. The reason middle classes cannot rise is somehow the public has gotten the idea that they are going to raise their lifestyle through the stroke of a pen at a central bank or other government bodies.”

THE INDIRECT EXCHANGE

“In today’s world economic growth is a function of a printing press; consumption presented as production.”

It is a situation in which goods, services, etc. are traded between two countries using the currency of a third country. Real wealth can only be created by growing it, mining it, building it, manufacturing it; being rewarded for providing more goods and services for less to consumers. What we have now is phony capitalism, which is more money for less goods and services, while consumer demand is being mandated by government planning and controlled by central banking.

EVENTS TO UNFOLD IN THE UPCOMING YEARS

“We are in a death event.”

“If you date interest rates going back 600-600 years, we have never once had a scenario where they were kept at zero for 6 years. What we have is a flat line; just like in any medical monitor a flat line is fatal.”

“The system is dead, we are just sitting there on the fumes and they can’t relight it because they have outlawed free enterprise capitalism, and wealth creation. Look at the health care system right now, it is just a leviathan. They went in there and wrote Obama Care for themselves and that’s how they became supporters. It was government sanctioned.”

“Just look at Japan, we are headed right there.”

“The long term the yield curve is going to invert, but it is going to invert near zero. There is no growth, the only growth there is, is just credit creation. To spurt credit creation they have to make it easier for people to borrow so people can miscalculate their returns.”

CURRENCY EXTINCTION

“Currencies expire when people wake up, the value that currencies hold are only values within people’s minds.”

There is absolutely no value in them. As long as they are perceived as having real worth, you can purchase real things; this is the indirect exchange. Money is a store of value because it is not pegged to anything, as long as this allusion is there; we are substituting it to grab a hold of real cash flowing assets.

THE LEVERAGE COLLAPSE

“The dollar is going down, and it is going to die; but it will be the last to die.”

“They really have people thinking that the dollar is a risk free asset, and it is not. It is a worthless junk bond. Currencies don’t float, they just sink at different rates, and the sinking is managed by the BIS and the ECB, Bank of England, Bank of Japan etc. and they all mange the theft of remaining value with their printing presses.”

“The financial systems were given the keys to the castle. These economies are not run for the benefit of the entrepreneur; they are run for the benefit of the financiers. It is a game that the central banks have been playing since the 1600’s when the Rothschild’s went after the Bank of England. We are in troubling times and we need to be well informed. If you are an investor and you do it right, it will be the greatest time in history.”

“A Depression is incoming and this one will be nasty, in fact it will be the worst one ever.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/30/2015 - Chris Casey: The Austrian Case for Inflation

Special Guest: Chris Casey – Managing Director, WindRock Wealth Management

FRA Co-Founder, Gordon T. Long interviewed Chris Casey of Windrock Wealth Management on the concept of inflation and other applications of Austrian economics to investment theory. Mr. Casey, an Austrian economist, is a frequent speaker and writer on macroeconomic topics and their related investment implications.

WHAT IS AUSTRIAN ECONOMICS AND WHY DOES IT MATTER?

The Austrian school offers the “most realistic interpretation” of society and economics according to Mr. Casey. Gordon agrees in noting that “mathematical models are only as good as their assumptions.” While equations and models may be useful as a construct to frame concepts, any social science cannot be scientifically tested due to the inability to control the countless variables at work. As such, Mr. Casey prefers the Austrian approach which “looks at basic self-evident axioms as it relates to mankind in nature and then uses deductive reasoning to describe how the real world works.” According to Mr. Casey, the unique Austrian explanations of inflation and the business cycle (recessions) have direct applications to practical investment ideas.

THE AUSTRIAN EXPLANATION OF RECESSIONS

Most mainstream economists believe recessions are inherent to capitalism since their repeated cycles largely began during the industrial revolution. The Austrian school recognizes a different causation occurring at the same time: fiat money with or without central banking. By artificially increasing the money supply through fiat money, interest rate levels are temporarily lowered. This incents businesses and individuals to make investment decisions they would not otherwise have made: in short, malinvestments. Recessions to liquidate the inevitably follow monetary mischief.

THE AUSTRIAN EXPLANATION OF INFLATION

The Keynesian school of economics has two theories of inflation which fail to comport with reality and are theoretically faulty. Their “demand-pull” explanation requires full employment and full capacity in an economy, but Mr. Casey demonstrates that fails to account for a doubling of prices during the 1970’s during economic weakness.

The “cost-push” theory is equally wrong. By blaming a particular price increase in a commodity such as oil for all price increases, it would have predicted pronounced inflation and deflation over the last 15 years as the oil price gyrated wildly. In addition, it is theoretically faulty as more money spent on oil means less money is spent on other goods and services – which lowers their prices and renders the overall price level largely unaffected.

“Prices are merely a function of the supply and demand for money” states Mr. Casey. More supply means dollars are worth less while higher demand lowers prices as people seek to increase cash balances by selling goods and services through lower prices.

WHEN WILL WE EXPERIENCE INFLATION?

Mr. Casey believes that “once we have another downturn, the Fed . . . will step right in. Once we have that . . . we’ll really start to see the inflation take off.”

What will the Federal Reserve’s next move be? They have other options besides another round of quantitative easing. Mr. Casey notes they may stop paying interest on excess reserves held by commercial banks at the Federal Reserve, and they may also lower the reserve requirement which could have a pronounced and immediate impact on increasing the supply of money.

WHAT SHOULD INVESTORS DO?

“Timing is everything, so utilize investments which pay well now, but in an inflation will be a home run.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/30/2015 - Doug Casey: Retirement & Living Overseas for Americans – The Growing Trend (& Need!)

Special Guest: Doug Casey – Casey Research Personal Freedom Through Financial Freedom

FRA Co-Founder Gordon T. Long interviews Doug Casey on the different and emerging trends that are taking place in the U.S. Doug is an author, investor and founder of Casey Research.

On trends and changes in the U.S, Doug relates it to a “lush, comfortable and well maintained prison”. In his opinion th

e country is gradually degrading. He points out that the standard of living in other countries is steadily going up unlike before when the standard of living in the U.S was clearly ahead of others.

He agrees with Gordon on the fact that very soon people will be forced to retire outside of the U.S due to the rising health and medical costs. Doug points out this trend will only just increase because for years the current good standard of living being enjoyed by the U.S is a result of the heavy borrowing that has been taking place for years.

“When you take on debt, you are either mortgaging your future or you are consuming capital that somebody has saved in the past and lent to you to increase your standard of living now, but when you pay the debt you reduce your standard of living by more than that amount because you have to pay interest on it in addition”.

He predicts that when interest rates start going back up, things are going to get bad quickly, and he advises people to take precaution now by diversifying both politically and geographically while they can. He also recommends that people should acquire as many gold and silver coins as possible as it would be a great way to conserve capital.

“I don’t think in today’s high tech world, the government serves a useful purpose. There’s nothing that the state does that could not and would not be done better and cheaper and without coercion by the free market”.

“If you are the citizen of a country, the government considers you as its property this is why you are better of living in a country where you are not a citizen, and so they treat you as a guest to be cultivated as opposed to a milk cow that has to be milked”.

On the issue of people renouncing the U.S citizenship, Doug believes that this trend will simply keep on increasing. He likens this increasing exodus to what happened in the past, when the American predecessors left England in search of greener opportunities. He advises that Americans’ who value their freedom should look into getting dual citizenships.

“The quality of medical care is at least as good outside the U.S as it is in the U.S and it is much much less expensive”.

Doug believes that the popular belief held by most people, that the medical coverage you get when traveling the world is of a lesser quality as that in the United States is wrong. In his opinion you receive a cheaper and much better service.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/30/2015 - Robert Blumen: The Core Tenets of the Austrian School of Economics

Special Guest: Robert Blumen – Follower of the Austrian School of Economics

FRA Co-Founder, Gordon T. Long interviewed Robert Blumen, noted follower of the Austrian School of Economics, on the Core Tenets of the Austrian School and the Key Elements for investing in an Era of Financial Repression.

CORE TENETS

1. All economic understanding must be based on individual action

2. Subjective valuation drives prices

3. Marginal utility

4. Entrepreneurship

5. Time preference as the basis of interest and profit

6. The role of capital in production

7. Savings is required to create capital

8. Price Theory: – prices determine costs, not the other way around

9. Money as an evolutionary solution the problem of barter

10. Precious metals as an evolutionary solution to the choice of the best money

11. The purchasing power of money as a price that balances money supply and money demand

12. Non-neutrality of money (Cantillon effects)

13. The importance of money prices

14. Money is a good, and like any good, money does not have constant purchasing power. Stable money does not mean stable prices.

15. Mises’ “critique of intervention”: one thing leads to another

16. The “impossibility” of socialism (central planning)

17. Macro-Economics must be founded on micro economics

18. Macro-economics is based on Say’s law.

19. The rejection of the Keynesian revolution in macro.

20. Money and money substitutes (bank deposits, bank notes).

21. Banking with 100% gold reserves

22. Fractional reserve banking. The Austrian critique of fractional reserve banking

23. Central banking. The Austrian critique of central banking.

24. Austrian business cycle theory – the theory of unsustainable booms drive by fractional reserve banking and central banking.

Inflation is not just rising prices, it distorts production as well.

b. Distortions are unsustainable

c. The “crack up bust” as one possible ending to the unsustainable boom

25. Deflation:

Deflation has been demonized by the Keynesians.

b. Natural slow deflation is the result of increasing production.

c. Deflation is the correction process from inflation.

d. Deflation is not a mouse trap that the economy gets stuck in and cannot escape.

26. An Austrian understanding of recessions and depressions through Say’s Law, entrepreneurship, and market price theory

KEY ELEMENTS IN AN ERA OF FINANCIAL REPRESSION

1. Entrepreneurs create wealth by employing scarce resources in production within the context of the price system.

This requires real markets with real prices.

2. Central planning can not replace market prices.

3. Central bankers have it backwards. Counter-cyclical policies create the business cycle.

4. Interest is not a number you can set to anything you like for “policy” reasons. It is a price and it cannot be zero.

5. Attempting to keep interest rates at zero creates unsustainable distortions in the productive part of the economy.

6. Something that is unsustainable must stop – at some point.

7. In the end there are two choices – market prices or destruction of the monetary system

8. Investors think in terms of money, but money itself is unstable.

9. The path from fake prices to real prices will be difficult.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/29/2015 - Michael Snyder Says: “We Are Approaching A Global Economic Collapse!”

Special Guest: Michael Snyder – Lawyer, Author, Publisher – TheEconomicCollapseBlog.com

FRA Co-Founder Gordon T. Long interviews Michael Snyder on financial repression He is an author and publisher of the economic collapse, blog and other blogs.

FINANCIAL REPRESSION

On financial repression Michael prefers to look at it from the angle of who is doing the repression, which in his opinion is being carried out by the governments and central banks. He believes that markets work best when free market forces are allowed to play out without interference, and that the governments and central banks are anathemas to the market.

He says the area that has witnessed the greatest distortions as a result of outside interference are the emerging markets. He goes on to explain that the period of easy money and quantitative easing flowing into the markets caused a boom in the lending of money to emerging markets all over the world. As a result of these markets gorging on all this cheap money with low interest rates, a lot of debt has been accumulated, and most of that debt is denominated in U.S dollars.

As a result of a crash in commodity prices, the emerging markets are getting less for their exports and due to the reduction in quantitative easing, the dollar is increasing in value and its taking a lot more of their currency to service and pay these debts.

Michael noted that there is no easy way out from this, He believes that the current crisis will keep on getting worse especially as global economy is slowing down.

“I think that what we are seeing already is just going to accelerate we are going to have emerging markets really struggle and this is carrying on into global trade”. This is a global problem created by a global bubble that was created by the Federal Reserve and others and so I don’t know that there is any easy solutions and in fact, what we are seeing now is just the initial stage of a crisis that is going to get much much worse”.

He expects that initially major financial institutions all over the world will get into trouble with some of them even failing resulting in the banks refusing to lend to themselves and us thereby causing a credit crunch or freeze, which in turn will bring economic activity to a standstill and as a result cause a short severe period of deflation.

“I believe we are going to see financial crisis financial crash more intervention which is going to cause other problems, ultimately I believe we are going to see major financial intuitions all over the world fail, I believe we are going to see a loss of faith completely and entirely this time around in the central bank of the world and governments and I believe this is going to causes economic chaos around the globe in a scale we have never seen before in our times, and I believe this is going to be a tragedy that is going to play out over years and it’s going to fundamentally transform our standard of living and the world around us as we move forward”.

PREPARATION

On what can be done to prepare for this eventuality Michael advises that as for the short term people should evaluate financial assets that could crash in value. He also advises a 6month emergency fund at the very least. On long term protection, he recommends gold, silver and precious metals as ways people can protect their wealth. As for a longer term of protection he suggests people should have supplies of food and supplies in the event of a long term emergency, as well as having some cash at home in the event of bank holidays or shutdowns. Finally he strongly recommends a greater level of self-sufficiency from the system as he believes that it is going to fail soon.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/23/2015 - John Butler – Investing Based on the Austrian School of Economics

Special Guest: John Butler, Amphora Commodities Alpha

FRA Co-Founder Gordon T. Long discusses the Austrian School of Economics with John Butler and how its methodologies can be applied to the current global economy. John Butler has 18 years’ experience in the global financial industry, having worked for European and US investment banks in London, New York and Germany.

Prior to launching the Amphora Commodities Alpha Fund he was Managing Director and Head of the Index Strategies Group at Deutsche Bank in London, where he was responsible for the development and marketing of proprietary, systematic quantitative strategies for global interest rate markets. Prior to joining DB in 2007, John was Managing Director and Head of European Interest Rate Strategy at Lehman Brothers in London, where he and his team were voted #1 in the Institutional Investor research survey. In addition to other research, he publishes the Amphora Report newsletter which appears on several major financial websites

THE AUSTRIAN SCHOOL OF ECONOMICS

“It is the no free lunch school of economics.”

The Austrian school believes that economics systems are ultimately information systems. Some of those systems use information more efficiently and effectively than others, and in particular systems of which authorities of various kinds meddle with the market. Authorities may do this by extracting capital from the market via tax rates or even by manipulating the money of that market through some sort of artificial interest rate policy.

“From the Austrian schools point of view, anything that impedes the free price information flow of an economic system will result in a sub optimal economic outcome.”

Without the rule of law, without the ability to strongly enforce property rights, without the ability to prosecute fraud, and various other legal frameworks; the Austrian economic model cannot work.

“Our goal is to make sure economic information flows as efficiently as possible within a solid legal structure.”

HOW THE AUSTRIAN SCHOOL CAN BE APPLIED IN INVESTING

Austrianism teaches us that the future is unpredictable. The economy is made up of the billions of people in the world, with each person making transactions almost every day. Each decision is an individual’s choice, and each decision, even the decision not to spend your money has some effect on the economy.

“Austrian school provides you a way to identify distortions, a powerful way that is caused by a fiscal and monetary policy set such as interest rate or fiscal policy manipulation. Austrians are able to look at these policies and be able to see how they are impacting the investment environment. This gives you a sense of where the distortions are. In theory you get an idea of where you should be overweight and underweight from an investor’s point of view.”

CURRENT EVENTS AMPHORA IS FOCUSED ON

“Currently we are seeing a general overvaluation of risky assets that has been caused by truly an unprecedented set of highly expansionary monetary and fiscal policies throughout most of the world.”

Income growth has not kept up; assets are expensive relative to incomes. So the correct strategy is not simply to short assets, which is dangerous; but if indeed they do look for ways to stimulate aggregate demand more directly rather than through the banking system.

The correct strategies to have today are those that will perform if incomes begin to catch up to asset prices, it could be asset prices declining towards incomes or vice versa. It is impossible to know which one is going to happen, but it is highly likely looking forward that a conversion of the two will happen.

POSSIBILITY OF NEGATIVE NOMINAL INTEREST RATES

“Policy makers have become almost pathological; they have a relentless attitude to make their policies work.”

“Problem with this is, once you get to this point, you can no longer question your original set of assumption. Austrian school of economics knows that the original sets of Keynesian assumptions that have gone into forming this unconventional and aggressive policy mix are themselves flawed. We are on this course where if it were left to run itself, policy makers will operation in these counter-productive directions because they will not question whether their assumptions are wrong.”

“Banning cash will prevent people from making even the simplest transaction in their own neighborhoods; it will lead to complete riot and chaos.”

“Putting a ban on cash is a terrible idea. It is terrible for them and for the economy as a whole. Sadly, with the way things are going, policy makers are going to teach everyone a very hard lesson about blindly accept anything the bureaucracy tells you to do.”

CENTRAL BANKS ROLE IF ASSET CORRECTION OCCURRED

“If you do get a major correction in asset markets that causes collateral problems in financial markets, the policy makers are out of options. The only thing they could do is begin capital controls”

Prevent investors being able to freely liquidate or withdraw funds from their existing investments. This of course is very anti-capitalist, very inti-market. It goes directly against everything that a free enterprise economy should stand for; but when you follow these policies you will eventually get to a dead end.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/09/2015 - Leland Millar Talks Quality of China’s Economic Reporting

Special Guest: Leland Millar – President, China Beige Book International

FRA Co-Founder Gordon T. Long interviews Leland miller, the president of the china beige book international and discusses financial repression in the context of the Chinese economy. He describes himself as a Lifelong china watcher who decided to do something about the complete lack of data in china.

“One of the things that the china beige book plans to do is to give people a real picture of not just the growth dynamics, but also the labor market, the credit dynamics, the macro implications of Chinese growth, indications of future Chinese demand, implications of commodity markets around the world, we try to give the people a much better picture on what’s actually happening instead of just relying on official data and press release”.

FINANCIAL REPRESSION

Leland describes the Chinese reform as a reversal of financial repression and this repression in the context of the Chinese economy is the oppression of consumers and households by state organizations through its economic systems.

“It means reversing this long time economic model, where the state will profit through the economic system at the expense of the consumers and household, and one of the things that the new leadership is intent on doing in order to create consumption is to empower consumers, so they spend more and stop empowering state organizations which are fuelling the overcapacity and the massive debt bubble”.

What should investor know about china?

He explains the biggest misconception concerning the Chinese economy is believing the GDP tells you much about how china is doing.

“It is a broad, blunt indicator that doesn’t measure productive growth or credit dynamics”.

On some of the challenges of getting reliable data in china, Leland explains that he and his team had to ask Chinese firms and consumers on ground what is happening in the country, and set up a number of polling units across sectors in order to get reliable and accurate information.

Economic trends in china

“For years we have been talking about the Chinese slowdown; it’s inevitable, despite the fact that the economy has been slowing”.

He goes on to explain that although the market sentiment has gone from optimism to “Armageddon” in recent months, the actual data is at odds with these sentiments. As a result of china’s economic slowdown, there is great vulnerability among emerging markets. Now, the reason for this is that for years these markets have relied on china’s demand without factoring the likelihood of a decline or certainty of a decline in china’s demand.

On China’s view of America, Leland has this to say

“The Chinese look at America as a model that they are interested in taking pieces from; they like the dynamism of the economy and the global status. On one hand, they see us as a model to learn a lot of things from but also as a serious threat that is looking to constrain their inevitable and ultimate rise”.