05/06/2017 - The Roundtable Insight: Yra Harris On The Bond, Currency, Equity and Commodity Markets

FRA is joined by Yra Harris to discuss the current state of bond, currency, equity, and commodity markets.

Yra Harris is a recognized Trader with over 40 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through a combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC.

Yra highly recommends reading The Rotten Heart of Europe – send an email to rottenheartofeurope@gmail.com to order

BOND AND CURRENCY MARKETS

We’re just coming off a Fed meeting in which they called the first quarter transitory, which means they’re not worried about it, yet they made no change to the current policy of maintaining the Fed balance sheet. The $4T will remain at $4T, and whatever expires will be renewed by the purchasing of whatever duration expires by the new instrument. With the Fed raising rates, even though GDP turned out to be low, there are other elements that are slowing down. Right now, if the Fed was looking to start unwinding its balance sheet, which would mean a dynamic act of actually starting to sell some of their assets, the first move would be for the curve to start to steepen. A lot of potential buyers would step back, and market would say ‘show me what you’re going to be doing’. You’re going to have others trying to front run the Fed, because the Fed model says there should be no problem. But what the Fed doesn’t model is the effect on the marketplace, and they’re hoping the marketplace allows them to do this. What the Fed is worried about is whether the market will be cooperative with what they want to do. It’s why they don’t want to acknowledge any pre-program. It’s the same problem the ECB has. A lot of people front run the ECB, and the market tries to rush ahead of it.

If the Fed tries to unwind by an aggressive type of action, which is selling the debt to unwind in a quicker way, the long end of the curve will go up higher than the short end in the immediate period, because the market will race ahead of them. We don’t know how the curve ought to be steepening in that environment. With the Fed doing nothing but raising rates, the curve has actually flattened quite a bit.

It’s interesting how the US 2-10 curve, the ‘investor’s curve’, just mirrors the German 2-10 despite negative rates in Germany. These two just continuously mirror each other. Ultimately, if the Fed is too aggressive in unwinding the balance sheet, that’ll tip us into a very flattening curve, which will fly in the face of what we think should happen. There’s going to be all sorts of things here because the market is going to set the tone. If the Fed were to actually embark upon an unwinding, the market will then set the tone unlike QE. Right now the curves are telling us that the Fed is a little too aggressive, and that’s why it’s flattening.

Everything is ‘transitory’. The Fed is not going to do this in a vacuum. If Marine Le Pen wins the election and throws the entire financial system into turmoil, the Fed has to change their perspective too. So we have a lot of things in play here. Yellen will be very reticent to raise rates too quickly; they want to see more from Trump and Congress before they get more aggressive.

OTHER FACTORS THAT COULD INFLUENCE USD AND BOND MARKETS

In the first quarter, central bank buying totaled a trillion Dollars in assets. The amount of liquidity is huge. The Dollar and all currency markets are all relative value plays. Even if everyone is moderately up, some are doing better and offering a higher return, but the US equity market is close to what we may discern as full value based on historical metrics. In a fairly stable world, the US is not where we should be chasing assets right now. The Mexican Peso and stock market is probably the most undervalued asset class in the world. People are pushing India as a great place to invest, but India has a lot of enormous infrastructural and political problems that they’re trying to work on.

The best place for investment right now is Germany. If the Germans agreed to do whatever it takes to hold the EU project together, you’ll experience some inflation in Germany but the currency will be weak. On the other hand, if things got so bad that the whole EU project fell apart, you’re buying Germany with a low currency. If it were to pull out for some reason, German assets would convert to Deutschmarks. Germany could be bullish on assets, and you get the use of a weak currency. We get a cheaper currency with a much stronger economy. This is not an easy world to invest in. The political risks are phenomenally great; Italy is still a massive problem for Europe, Greece has not gone away, and there’s no trade in Japan’s JJB.

When you look at how central banks have single handedly destroyed the bond market, you don’t have to look very far. The Fed may be too self-confident, but their models have no respect for market reaction and they still think they can extract themselves with very little pain. If they deem to shrink their balance sheet, they’re going to find out the pent up power of the market and its ability to cause them a lot of pain.

THE GLOBAL MINSKY MOMENT

At the end of the day, interest rates aren’t high enough to attract people into leaving the comfort zone. They won’t let interest rates go high enough to ease some of this burden, so people take comfort in the equity market. Minsky must be spinning in his grave that we’ve gotten to this point and it’s so controlled by the central bank. The central banks have created a global Minsky moment because everyone is complacent. It’s everything approaching the Minsky moment because where are you going to go? There is a cost to everything; just because you don’t see it today doesn’t mean it won’t pop up tomorrow. This is all the outcome of central banks not knowing when enough is enough. QE1 in the US was absolutely needed to prevent a mass liquidation of US assets, but after that it stopped making sense. QE2 and QE3 were totally unnecessary and has created this mess that we are now in.

SILVER-COPPER RATIO TO EQUITY MARKET

Gold has depreciated against silver significantly over the last few weeks, while the equity markets have been holding up pretty strong. Usually silver tends to outperform because it also has industrial usage. Copper has a tendency to outperform the other metals when the equity markets are doing well, because people correlate it to the economy. Copper has been dramatically outperforming silver over the same period, which is highly unusual when the equity markets are holding.

The Chinese have gigantic warehouses full of commodities, which wreaks havoc on that market. You do hear some bad things about what’s happening in the Chinese economy. If that’s the case, commodity prices may come under pressure as some of the lenders call the collateral and start pushing it on the market to raise some cash to secure loans.

INVESTMENT POTENTIAL OF COMMODITY ASSET CLASS

The agricultural sector is a good sector to be in. We have massive crops around the world and prices are relatively strong historically. We’ve had a bit of a rally in the agricultural products in the last few weeks, but it’s something to pay attention to. You should take a look and see if there’s an opportunity for you. The one thing that we’re sure of is that China and India need grain, end of story. As their income levels move up, agricultural products and higher protein products are in demand.

The great thing about the commodity market, unlike the commodity markets which are manipulated, is that farmers and miners react to price. The markets do work.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/03/2017 - The Roundtable Insight: Megan Greene On The Current Status Of The European Economy

Tonight’s podcast includes some insight on Europe’s current economic and political states, and how it translates into current economic trends. We have seen the rise of the anti-European and anti-EU mindset all across Europe. This movement not only impacts European politics, but the entire state of the European economy as well, and has direct influence over Western economics in terms of trade agreements, investments in the European market, and the value of our currencies.

Megan Greene, an accomplished economist with a specialty in European economics, explores what Europe needs at the moment and what is most likely coming up in the European economy.

FRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Megan Greene. She is [the] Managing Director and Chief Economist of Manulife Asset Management. She’s responsible for forecasting global macroeconomic and financial trends, and analyzing the potential opportunities and impacts to support the firm’s investment teams around the world. Formally, she was with Roubini Global Economics, where she had a focus on the Eurozone, and she also holds a Masters [degree] in European politics from Oxford University. So, quite a focus on Europe and we would like to explore Megan’s thoughts on Europe. Welcome, Megan.

Megan Greene: Thanks for having me.

FRA: What are your thoughts, what’s happening in Europe? The political situation there, the rise of anti-Europe parties, how that all affects what’s happening as far as the economics and the financial situation of the Eurozone and the European central bank?

Megan: Sure. So I would say, first of all, that the far greatest risk coming out of Europe for this year, probably the next year (too) is the political risk. Europe has an incredibly busy election schedule over the next year-the next election coming up is actually in France. It’s coming up quite soon; their two-round presidential election. It seemed at first very likely that it would be a runoff in the second round between the right-wing populist national front’s candidate, Marine Le Pen, and the independent candidate Emmanuel Macron. But more recently, actually, two other candidates had a lot of momentum and those are the right candidate Fillon, and the communist candidate Melenchon. This matters in large part because Le Pen and Melenchon both are running on a platform that’s very anti-European, very populist, and both have said in some form that they would like to renegotiate France’s relationship with the Eurozone, and potentially hold a referendum to see if France might want to leave the Eurozone. There is a chance that the second round of that election could be a “Le Pen, Melenchon” runoff, and that would be a market event for sure; it would be dramatic. More likely is still a “Le Pen, Macron” runoff, and it does seem most likely that Macron will end up winning. Even if Le Pen, the most anti-European candidate won, there’s a parliamentary election at the end of this year, and it seems very unlikely that her party would do well in those elections. It does seem that parliament would still be controlled, in which case it might be very difficult for Le Pen to actually have a referendum on France’s membership in the Eurozone. Even if they had a referendum, actually, the most recent opinion polls suggest that the French would vote to keep France in the Euro(zone). I don’t think that it’s very likely that, first of all, Le Pen would win, but secondly, that even if she did, that France would go ahead and exit the Eurozone. It’s a very low probability event, but such a high impact event-it’s something worth looking at.

The much bigger risk of a Le Pen win isn’t actually exiting the Eurozone, it’s just a series of bank runs starting in France but maybe spreading a bit wider. That would obviously have implications on the markets. Even bigger as a risk for the Eurozone than the French elections, I think, are the Italian elections which are due to be held by March of next year. It’s possible they might be held early…but probably not before the fourth quarter of this year. In any case, according to most opinion polls, the populist, anti-European five star movement isn’t in the top slot. It’s unlikely in an Italian election that the five star movement would actually win in absolute majority. They would have to find coalition partners and that won’t be easy given their ideology and the ideologies of the other political parties in Italy that might want to form a coalition with them. So even if the five star movement were to win the Italian elections, it’s not totally clear if they would make it into government. But if they did make it into government, they said that they too would like to have a referendum on Italy’s membership of the Euro(zone). Unlike in France, Europe is much less popular in Italy so it does seem plausible that if there were a referendum in Italy that Italy could end up choosing to leave the Euro(zone), and that would be dramatic-to have Europe’s third-largest country leaving the European project, that could really pose an existential challenge for the Eurozone. So those are two countries that could end up following in the footsteps of the UK in terms of leaving the European project.

Scotland is another country that could end up, actually, leaving the EU in its attempt to leave the UK. Its hopes given, of course, how pro-European Scotland is would be to rejoin the EU but they might end up having to get in the back of the line. That’s one concern. And then of course one issue that has been at the forefront of European risks since the beginning of the crisis, the global financial crisis, is Greece. Greece hasn’t been solved by any stretch of the imagination, it’s just garnering a lot less attention from the markets these days. Whereas before, the real concern was that there would be a stand-off between Greece and its creditors, and Greece would end up leaving the Eurozone almost by accident. Now, it’s very different. It’s very clear that the Greek government will just end up caving every time its creditors ask new reforms of this government, and just recently they came up with a deal for another round of funding to ensure the government is signed up to what the creditors demanded. The problem now is that creditors themselves can’t agree on what they want, so the IMF would really like to see Greece have debt relief, which is necessary in my view. The other creditors, particularly Germany, don’t want to commit to debt relief now, particularly not in advance of the German elections coming up. If they don’t come up with a solution, the IMF could end up leaving the bailout program in which case there is a real risk that Germany, and more recently the Netherlands, has said that they wouldn’t participate without the participation of the IMF. If these countries don’t participate, then the bailout program would fall apart. Greece would have no means for funding, and could end up leaving the Eurozone, not because it was specific strategy on the part of the government or even on the part of the creditors, but again, almost by accident. There is a risk that you could have some EU and Eurozone breakup, even though the risk isn’t as high as it once was.

In terms of the actual economy in the Eurozone, in aggregate, I think that the Eurozone is roughly a 1.5% growth economy, but again that’s in aggregate so it masks the big divisions between the core countries like Germany and the weaker countries like Greece and Portugal, and Italy as well. Data has been looking better; much as in the US, much of the confidence data has looked good, a lot of the soft data, the PMI data for example, has been really improving. It’s the hard data that’s not looking as great so things like industrial production, new factory orders, that hasn’t really come in yet. Lending is actually expanding, so we might expect some improvement of the hard data such that there is a sustainable economic recovery in the Eurozone. That recovery can only really be so strong as long as the approach remains that if all the weaker countries doing all the adjusting and all the core countries just carrying along as they always had. Evidence in that is Germany’s current account surplus which continues to hit new record highs every month. Germany and other core countries aren’t adjusting at all and the weaker countries continue to cut their wages and pensions. In Greece’s case at least, we haven’t seen much wager-pinching growth, and they continue to try to increase their national savings as a percentage of their GDP to match Germany’s again, and that just means there’s not a lot of consumption or investment happening in the weaker parts of the Eurozone. That really cuts off any avenue towards domestic demand, it means that most of the Eurozone is relying on exports for growth. There is an economic recovery happening in the Eurozone, it’s just muted by the fact that it’s all the weaker countries doing all the adjusting and none of the stronger ones. I think that we can expect that to continue in the absence of any major policy change, so I think the Eurozone in aggregate will continue to be a 2% growth economy.

In terms of what the ECB is doing, the ECB would love to normalize monetary policy but it’s just taking them a while because the recovery is so weak and because inflation isn’t coming in. I think that the ECB will probably announce a tapering of their QE program at the end of this year, and at the end of next year, they might have to wait until the beginning of the following year. The ECB is very much going in the footsteps of the US in trying to very, very gradually normalize monetary policy. I think that if some of these political risks I mentioned materialize, then it’ll be incredibly difficult for the ECB to hike rates in to that for sure. There are other risks, in the banking sector for example, particularly in Italy, that might make it really difficult for the ECB to tighten monetary policy.

FRA: You mentioned earlier on bank runs, could those be initiated from a catalyst of something other than one of the countries pulling out, like Italy or France, pulling out of the European monetary union? Would it be other factors potentially, in terms of the bank runs?

Megan: Yeah, you could see bank runs happening as a result of financial instability in in of itself. Particularly in Italy, there are a lot of banks that are still requiring recapitalization, non-performing loans in Italian banks. Portuguese, Irish, Greek, even French banks are really elevated and it used to be that they would work at their non-performing loans by creating bad banks because they can’t create the same bad bank that they used to be able to. That’s no longer a solution which means that none of these countries really know what to do with the massive heap of MPL’s that are sitting on their balance sheets, and so if you see those non-performing loans start to be realized and turned into defaults you could end up having a real scare.

The Eurozone has made some progress on institutional change in terms of creating a banking union, but they haven’t gotten all the way there yet so rather than saying they have a banking union I’d say they have a loose banking federation. There’s still no risk sharing in terms of banks in Europe so that means that not only is there not a common deposit guarantee in Europe, but I do think that if any country that has a big bank that really needs to be wound down. Now, governments aren’t allowed to step in and bail them out, and I think that wounding down a big bank is absolutely politically toxic for any leader so faced with that choice, most leaders would just break the rules and completely undermine the banking union and that in itself could spark off bank runs as well.

FRA: Do you see the potential for a move towards a fiscal union in terms of creating an actual European bond or just conducting fiscal policy across the entire Eurozone?

Megan: I think part of a fiscal union is needed, though I don’t think we need, for example, a common fiscal authority. I think we do need to see asset class in Europe that is liquid and deep enough to withstand any sudden stops, so I do think they need to create mutualized debt like a Eurobond. But then actually I think that the private sector can go ahead and step in rather than having a fiscal authority. If we had a capital markets union, I think that that could go a long way towards achieving what a public fiscal union could achieve and I think that’s necessary because I just don’t think that there’s any political will either in the core or in the periphery to actually have a fiscal authority and have everyone sign up to the same rules. So I think that it’s unlikely and would be a waste of political capital to try to create a fiscal authority.

One way of explaining what I think that the Eurozone needs is a mutualized debt so a Eurobond, but then in terms of the private markets governing cross border investments and exposure, it’s a bit like our credit card companies like VISA and MasterCard, that’s mutualized debt with no real central authority to manage it. There is some precedent for, I think it’s possible, but I don’t think it’s possible to see a full fiscal union with a single fiscal authority. Unfortunately, Eurobonds aren’t at all on the agenda now. It would require several more acute crises, and existential crises in the Eurozone to get the core members and the peripheral members to sign up for it, but particularly Germany because Germany doesn’t really see why they should accept other countries’ risk, and they’re worries about creating a moral hazard by going ahead and mutualizing bonds. So I think it’s very unlikely, but I do think that we need Eurobonds eventually for the European project to stay together.

FRA: And actually just recently this week US president Donald Trump made some comments on the dollar that it was too strong and so there was some movement on the dollar going lower; pushing the euro higher. Could that be a trend, and if that were to happen, if the euro would strengthen, could that cause global havoc and the countries’ struggle on their economy and debt burden?

Megan: Well, I think that’s its really unlikely that the general trend will be that the dollar weakens, I think that it’s much more likely that the dollar ends up a bit stronger even though the US president is trying to talk down the dollar at the moment. It’s really hard to conceive of a situation in which it’s in the US government’s best interest to see the dollar depreciate. The only scenario I can really think of is if there were huge problems in other economies, and the US fed opened up slop lines with other central banks to essentially fund their QE program so the Bank of Japan and the ECB, and the Bank of England. I think that’s really unlikely. We have seen the dollar weaken a little bit but the general trend is for the dollar to strengthen and that’s relative to a basket of currencies but that includes the Euro. I think generally the Euro will be weaker. Also, we will have movements, depends on your time frame of course, but I think if the French election results in Macron at the helm of government, then I think that the Euro could strengthen off the back of that. But if Le Pen were to win for example, I think the Euro would weaken off the back if that, so it will depend to some degree of political developments and in the long term, I do think that the Euro will probably weaken relative to the dollar. Not so much necessarily because of the factors that mean the Euro should be weak but in large part because of what the US and the fed are doing.

FRA: Given these political developments, do you see Germany continuing to bear the debt of the rest of Europe in terms of transferring its current account surplus to the less fortunate states of the union…or could it be that Germany considers on leaving the Eurozone?

Megan: I think that Germany has really been taking on risk through the target to balance this at the ECB, so the target to imbalances is now at record high, or higher than they were back in 2012, when there were much greater concerns about countries leaving the Eurozone. That’s largely because of Italy, actually, so it’s largely because of German investors pulling out of Italy. Now that only becomes a problem if a country actually leaves the Eurozone and that seems unlikely, I think. It’s certainly not my base case scenario over the next couple of years. Otherwise, Germany isn’t really funding everybody else’s debt, but I do think that there is a discussion about whether it’s really in Germany’s best interests to stay in this project. I think that it definitely is. Germany benefits from an artificially weak currency because it is connected to so many weaker countries, and that’s been really helpful for Germany given that their growth model has been pretty reliant on exports for the past several years so the domestic demand now stand for a slightly larger percentage of GDP than it has in the past, but its only really slightly larger. Germany is still dependent on exports for growth. If Germany were to go ahead and leave the Eurozone, it would probably see its currency appreciate massively and that would completely undermine its entire growth model so it would have to come up with an entire new model and that’s not really in Germany’s best interests so I do think it’s in Germany’s best interests to stick in the Eurozone.

I will say that I’ve spent a lot of time talking to the EU governments and my argument with them has always been that Germany always had a very high national savings rate, and so they’ve had a really low national investment rate, which hasn’t really served them well. I mean they’ve invested in Greek government bonds, and Portuguese retail, and Irish property, which (those investments) turned out to be really bad investments. It also means that German investment domestically has been really low, so Germany suffers from chronic underinvestment and as a result their roads are in bad shape, their bridges are in bad shape, so my argument has always been that maybe the German government should encourage domestic investment and that would boost Germany’s growth, and that would also trickle out and help the growth of the rest of the Eurozone. The German government’s response to me every time is to ask me why they should care about growth, which as an economist you can imagine, seems like a weird question but according to them, they don’t have incredibly high growth but they have a really high standard of living and very low unemployment. In their view, growth is kind of an Anglo-Saxon obsession and they’re doing just fine. So this approach to growth in Germany, and this approach in the entire region whereby Germany does the same as its always done and everybody else tries to look more like Germany, I think that’s here to stay for a number of years.

FRA: Interesting. And what are your thoughts on the UK and Brexit, how that’s playing out, and could there be any changes between now and the next two years after they receive their Article 50 notice like a few weeks ago?

Megan: I think there are still some that are hoping that the UK will take back triggering Article 50. I spoke with the guy who wrote Article 50, John Kerr, and he says you can and he intentionally left wiggle room in it. I think it’s very unlikely that the government will do that given that they’re acting on a mandate that was given to them by the people. Also if they were to go ahead and revoke it, they probably would have already damaged their relations with the rest of the EU given that they’re negotiating to leave.

I did a lot of consulting on Brexit and testified in the House of Lords, and before Brexit I would’ve said that the worst possible option was the UK going for a so-called “hard Brexit”, which means leaving the single market all together. Now, I think that’s no longer the worst option, I actually think it’s the most likely option. The prime minister has said that’s what they’ll pursue. I think there’s a worse option out there which is that after two years of negotiating, both their divorce from the EU and their new relationship with the EU, they actually don’t have any agreement on what their new relationship with the EU should be, at which point the UK would just kind of stumble out of the EU. They would have to rely on the WTO for their trade relationships. The problem with that is that right now the WTO has relatively robust rules and some credibility, but in two years from now it actually might not, so, you could conceive for example the US government trying to implement a border adjustment tax which is most likely illegal according to WTO rules. Having the WTO turn around and say, “Well, that’s illegal you can’t do that” and the US administration could just reply by saying well, “We don’t care anyhow”. That would completely declaw the WTO. That’s just one example and there are a number of potential trade policies coming out of the US in particular that could really undermine the WTO, so the UK’s plan is to actually rely on WTO rules so that at the end of two years the WTO might be severely undermined by then, in which case, that’s a terrible plan for the UK. I think that’s the worst scenario.

The only way, I think, that the UK could actually have a deal at the end of two years is if they cut and paste it from somewhere else. Two years is not a lot of time to negotiate their divorce from the EU first, and of course not much will get done before the French elections, and then the German elections in September, and then the Italian elections in March, so, there will have to be breaks in negotiations. They’ll have to negotiate the divorce and then they’ll have to negotiate an entirely new relationship-that’s a lot to do in two years. If they can cut and paste a new relationship from somewhere else, they might be able to pull it off. One way to do that is to copy the deal that Canada and the EU struck: the Ceta deal. The problem with that is that it doesn’t include anything on services and more than half of the UK’s economy is services so they’d have to write an entire new chapter to cover services, and that in itself could take two years. That’s problematic. There’s one other option that’s currently being discussed behind closed doors in the UK and that’s to copy the deal that the EU just struck with the Ukraine which does include services so that is really feasible. It is mainly being talked about behind closed doors because the UK doesn’t want anyone to realize that they’re trying to follow the Ukraine as a model. That is one option but it’s too early to say whether really is possible or not but it’s something that they’re looking at.

FRA: Finally, just wondering your thoughts on the investment environment, what this all means, not mentioning any specific companies or securities, any thoughts on asset classes or types of investments that could make sense in Europe given all the scenarios, assuming there could be some investments that could make sense regardless of all the different scenarios like whether Germany stays, whether they pull out and different countries leaving, the effect of political parties getting elected. And would it make sense for Europe in general now from a contrarian perspective? Perhaps like German corporations or German real estate, if they were to pull out their currency would appreciate, but if they stay in there could be more inflation generated to ease to burden of debt across the Eurozone. Your thoughts?

Megan: German real estate certainly is one potential opportunity but generally I would say given even all the risks that I’ve highlighted particularly the political risks, I think that the most likely scenario over the next year or two is that we go through all these elections and actually in the end we just have the status quo, which would be market-positive. I’m hesitant to get too excited about that because I do think that there are real restraints on the economic recovery in Europe because of the politics as they currently stand, so the status quo means that would continue. Still, I think that would be a risk on development in which case given that you have the ECB continuing to ease now and I think that they’ll continue to maintain accommodative monetary policy going forward, and you have the fed in the US tightening actually, that does means that there might be opportunities and equities in Europe generally so I do think that that is one place that investors could look. In terms of banks in Europe, there are some real problems in terms of the health of bank balance sheets particularly in Italy, Portugal, even France, but banks are incredibly cheap so there might be some valuable investments there. Generally I do think that the valuations for companies in Europe will go up so I would say that European equities are probably a good opportunity now.

FRA: Great. Great insight. How can our listeners learn more about your work?

Megan: You can follow me on twitter, its @economistmeg to not only see what I write myself but to also see my commentary on the latest, greatest in Europe and the rest of the world.

FRA: Great, thank you very much for being on the show and again, thank you.

Megan: Pleasure, thanks for having me.

Abstract by Tatiana Paskovataia, tatiana-p28@hotmail.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/26/2017 - Dr. Marc Faber: Indebted Western World Economies Are More Fragile Than Ever Before

Marc Faber thinks there will be 20 – 40% pull back in the markets, we are still in the Trump euphoria stage. He goes on to say that Trump will beg Janet Yellen not to raise interest rates and to keep on printing. Tax reform will not really help the U.S. The U.S. and western economies are terminally sick. The Debt loads are huge and the economic conditions are more fragile than ever before.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/26/2017 - The Roundtable Insight: Richard Duncan On A Recipe For Disaster

Richard Duncan is the Chief Economist at Blackhorse Asset Management in Singapore. He is the author of numerous books including, The New Depression: The Breakdown of the Paper Money Economy, andThe Dollar Crisis: Causes, Consequences, Cures, an international bestseller that predicted the current global economic disaster with extraordinary accuracy. Since beginning his career as an equities analyst in Hong Kong in 1986, Richard has served as global head of investment strategy at ABN AMRO Asset Management in London, worked as a financial sector specialist for the World Bank in Washington D.C., and headed equity research departments for James Capel Securities and Salomon Brothers in Bangkok. He also worked as a consultant for the IMF in Thailand during the Asia Crisis.

Richard has appeared frequently on CNBC, CNN, BBC and Bloomberg Television, as well as on BBC World Service Radio. He has published articles in The Financial Times, The Far East Economic Review, FinanceAsia and CFO Asia. He is also a well-known speaker whose audiences have included The World Economic Forum’s East Asia Economic Summit in Singapore, The EuroFinance Conference in Copenhagen, The Chief Financial Officers’ Roundtable in Shanghai, and The World Knowledge Forum in Seoul. He runs a blog called https://www.richardduncaneconomics.com/ where he has a video newsletter service called Macro Watch, which is available to our listeners at a 50% discount using the code word: authority

I coined the term ‘Creditism’ to describe an economic system driven by credit creation and consumption, in contrast to Capitalism, which was driven by investment and savings. Creditism replaced Capitalism when money ceased to be backed by gold nearly five decades ago. But Creditism requires Credit growth to survive. The evidence presented in this video suggests that Creditism is in crisis globally because Credit is no longer increasing fast enough to drive global growth, even with record low interest rates. It is not possible to understand the global economic crisis without taking account of the exhaustion of Creditism.” – Richard Duncan

Current Creditism trends:

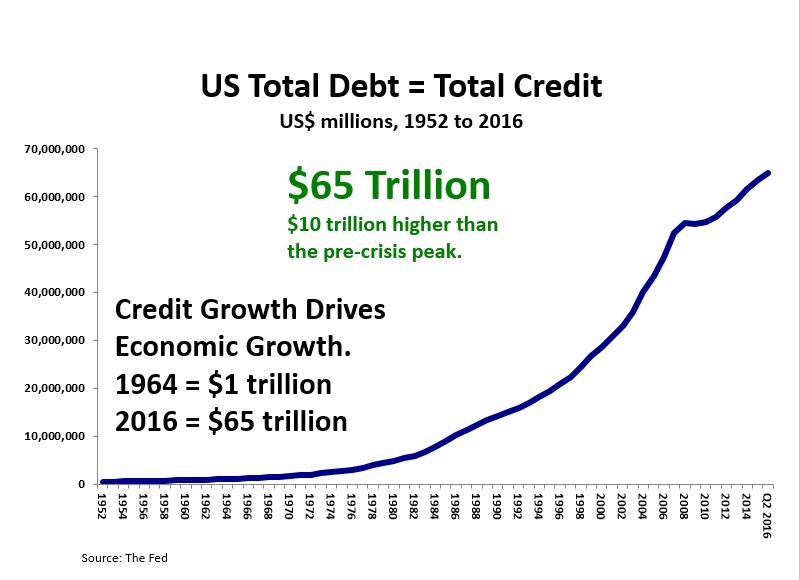

Once we stopped backing money with gold in 1968, the nature of our economic system changed very profoundly. Credit growth became the driver of economic growth. When we were still on a gold standard, there were constraints as to how much credit could be created, but after we stopped backing money with gold, all those constraints were removed and credit absolutely exploded. Total credit or total debt in the United States first went through one trillion dollars in 1964, and now it’s 66 trillion.

So it’s expanded 66 times in just over 50 years. This extraordinary explosion of credit in the US has completely transformed the global economy. It ushered in the age of globalization, it allowed countries like China to be revolutionized from a very poor, developing country, to the second largest economy in the world. What I’ve seen is even adjusted for inflation, every time credit has risen by less than 2% in the US going back to 1950, the US goes into a recession. And the recession doesn’t end until we get another big surge of credit expansion. So it’s crucial to be able to forecast credit growth if you want to be able to understand what’s going to happen in terms of economic growth. And it’s been very weak since 2008; we’ve now hit the point now where the private sector, the households, are so heavily in debt that they just can’t continue taking on new or additional debt to make credit expand enough to drive the economy.

So this is the real point: once credit started to contract in 2008, the global economy began to spiral into a new great depression. And it was only the expansion of government debt that prevented that from occurring. US government debt has more or less doubled since 2008, it is roughly $19 trillion now. It was the expansion of government debt that kept total credit expanding, and that prevented the world from collapsing into a depression.

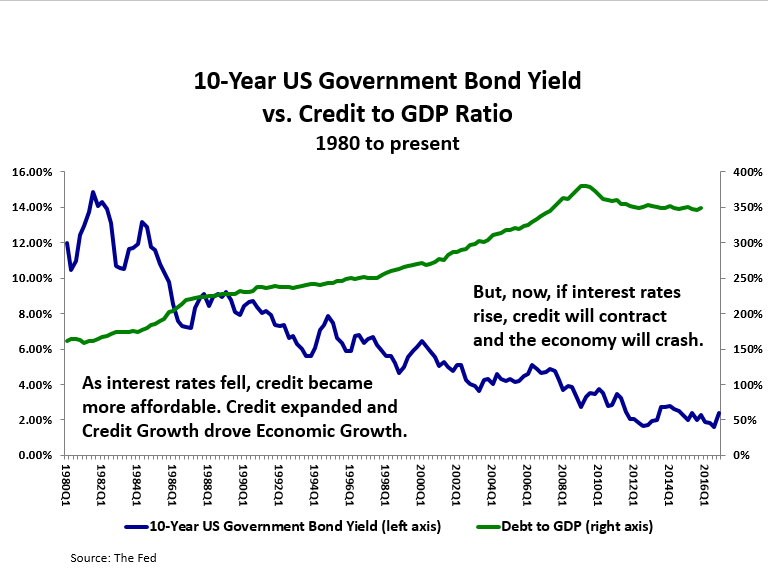

The key as to what is going to happen next to the US economy and the global economy is interest rates. Interest rates are crucial to the future of Creditism as I call it. Going back to 1980, interest rates in the United States have gone down very steadily.

The 10-Year US Government Bond Yield in the early 80s was as high as 15% and now it’s gone down to around 2.2% today. And as the interest rate fell, this made borrowing more affordable, so the Americans were able to afford more debt. They became increasingly indebted, and we can see this by looking at the ratio of total debt to GDP in the United States. Now when I talk about total debt or total credit, I mean all the debt in the country. The government debt, the household sector debt, the corporate debt, financial sector debt, all debt. In 1980, it was only around 150% total debt to GDP, now it’s about 350%. So as credit expanded, the credit growth drove the economic growth in the United States. And as the US economy expanded, US imports from other countries grew, and that drove the global economy.

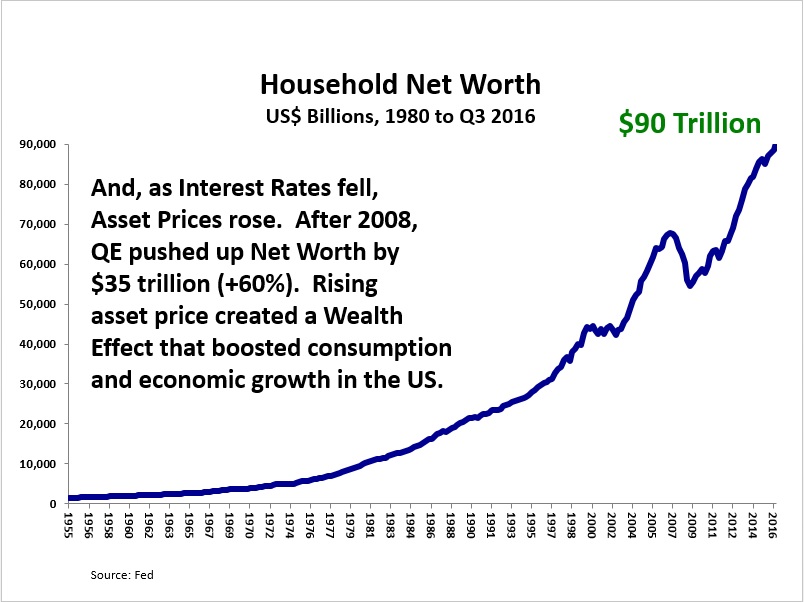

As interest rates have fallen, Asset prices have gone up. The stock market, property market, bond prices, they’ve all gone higher as interest rates have gone lower. The best measure of total wealth in the United States is household sector net worth.

Household net worth is now $90 trillion, it’s gone up by 60% since the post-crisis low in 2009. The reason this wealth has expanded is that the government and the fed took very aggressive action to reflate the global economy after 2008. The fed and the central banks around the world had interest rates to near 0% and reflated the global economy.

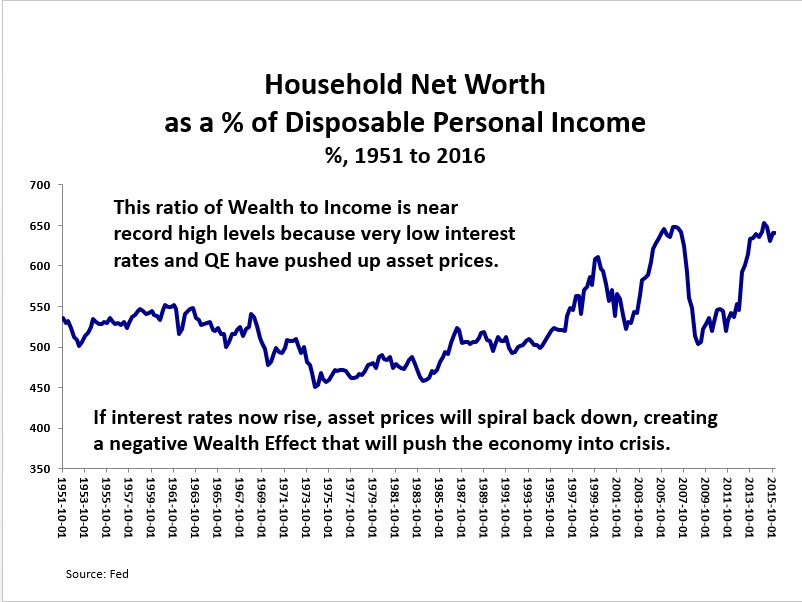

Going back to 1950, the ratio of wealth to income has averaged about 525%. During the property bubble, this ratio went up to about 650%, and of course, the property bubble blew up, and the ratio went back down to its normal level of about 525%. But now this ratio has once again expanded and is now at its back at its all-time peak level at 650% once again. And this is telling us that asset prices are very high, and the stock market is very expensive, property prices are expensive. And that means interest rates now begin to move higher, then asset prices are very likely to fall. So we’re seeing a situation now where interest rates are the key, because if interest rates move higher then credit is going to contract. That’s going to throw the economy into a severe recession, and on top of that asset prices would have a very significant correction or crash, that would cause a negative wealth effect, and that would also cause a US economy and the global economy to go back into severe recession, or worse.

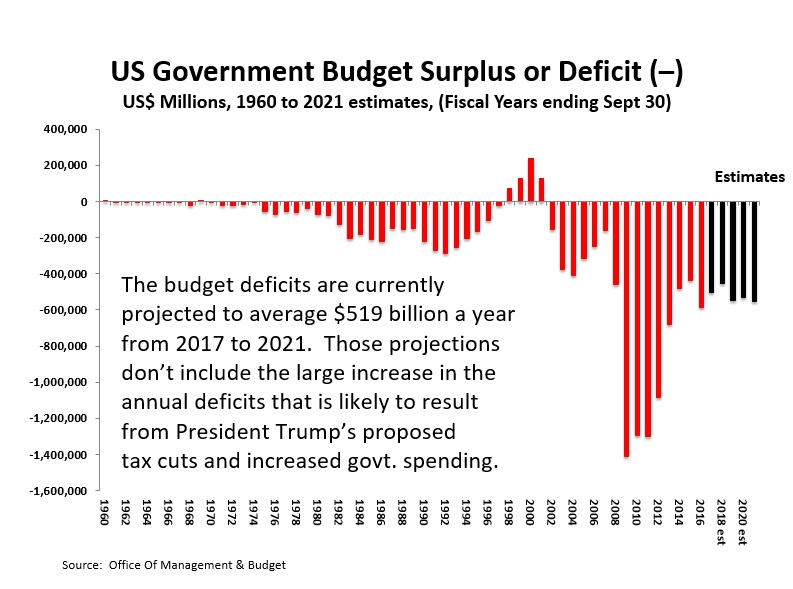

The US budget deficit

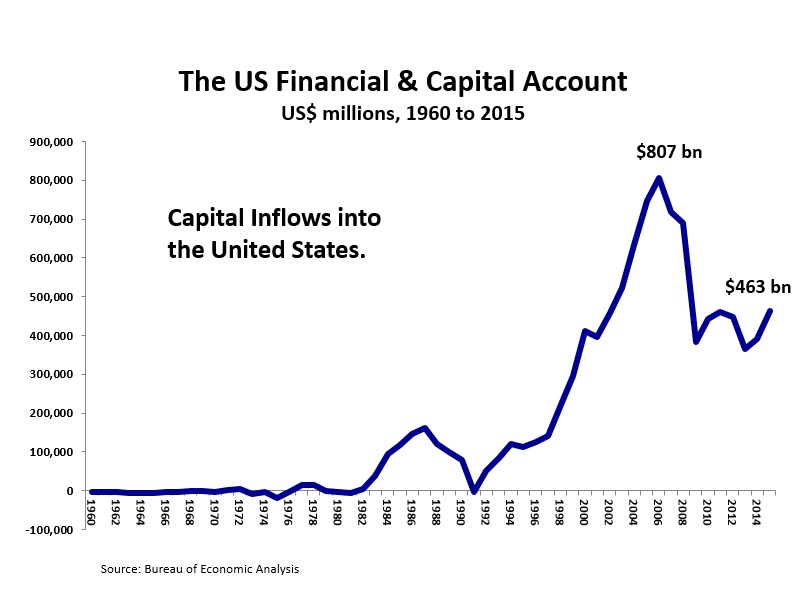

When the government borrows money it tends to push up interest rates. For instance, if the government doesn’t borrow anything then there’s less demand for money and interest rates will be lower. But if the government were suddenly to borrow $3 trillion, then that would suck up all the money available in the economy and that would push interest rates to very high levels. So when the government borrows more, it tends to push up interest rates. This is assuming all else is unchanged, but over the last many decades, something very important has changed. Once the Bretton Woods system broke down in 1971, the United States discovered they could run very large trade deficits with the rest of the world. This is important because it means the US will have very large capital inflows. When the US has a large trade deficit, it will have an equally large amount of capital inflows coming into the country to finance that trade deficit. The larger the capital inflows are, the easier it is to finance the government’s budget deficit at low interest rates.

In 2006 we had about $800 billion in capital inflow, and that was enough to finance the entire government budget deficit that year a few times over. So these inflows are very important financing the budget deficit at low interest rates. If Trump is successful in his promises to cut taxes and increase government spending, then it’s going to make their budget deficit considerably larger.

The Capital Inflows are the mirror image of the Current Account deficit. When the Current Account Deficit grows larger, the Capital Inflows also grow larger, making it easier to finance the budget deficit. But, when the Current Account Deficit shrinks, Capital Inflows also shrink, making it more difficult to finance the budget deficit at low interest rates.

President Trump’s plans to force US companies to bring their factories back to the US, to renegotiate trade deals and/or to impose trade tariffs on China and Mexico would all cause the US Current Account deficit to shrink. A smaller Current Account deficit would cause the capital inflows into the United States to shrink, too. Less capital inflows would mean less demand for US government bonds. That would push up interest rates and pop the asset price bubble. So, we must keep a close eye on the US Current Account Deficit because it will determine the size of the capital inflows.

What Could Cause Inflation to Rise?

Inflation has fallen since the early 1980s because increasing trade with low wage countries has pushed down US wages and the price of consumer goods. Now, however, if the US imports less from low wage countries, the price of manufactured goods will rise, US wages will rise, and inflation will rise. Forcing companies to bring their factories back to the United States or imposing trade tariffs on imported goods would cause inflation to increase. Increased government spending could also cause inflation to pick up.

The Undesirable Consequences of Eliminating the Trade Deficit

If the US reduces its imports, the global economy will shrink. If the US eliminates its $1 billion a day trade deficit with China, China’s economy could collapse into a depression that would severely impact all of China’s trading partners, and potentially lead to social instability within China and to military conflict between China, its neighbors, and the US. Additionally, if the US Current Account deficit returns to balance, the global economy will suffer from insufficient Dollar liquidity, which could cause economic stagnation or worse. A reduction of imports from low wage countries would cause US inflation to rise, which would push up US interest rates. The elimination of the Current Account deficit would cause a sharp reduction in capital inflows into the US, which would also cause US interest rates to rise. Higher interest rates would cause credit to contract and a sharp fall in US asset prices, which could cause the economy to go into recession. It could also cause a wave of credit defaults in the US and around the world, potentially leading to a new systemic financial sector crisis.

Moving Forward

The US could stimulate the economy “the old fashion way” by increasing military spending and starting a war, or they could invest in 21st century industries and technologies. We could invest a trillion dollars over the next 10 years in developing renewable, green, solar energy. And if we did that, we could then re-structure the entire US economy, and induce a new technological revolution that would be so profitable, that we would pay off these investments many times over. We could grow out of this crisis, rather than collapsing into a new great depression.

Conclusions

The proposals outlined thus far by President Trump suggest that:

The budget deficit would grow larger (due to tax cuts and increase government spending);

The current account deficit would shrink (due to renegotiating trade deals, bringing US factory jobs back to the US and possibly trade tariffs);

And inflation would pick up (due to increased government spending, higher US wages, pressure on China to push up the RMB and, possibly, tariffs).

More about Macro Watch

Macro Watch is a video newsletter published by Richard Duncan. Every two weeks a new video is uploaded describing something important going on in the global economy, and how that’s likely to impact asset prices. Macro Watch monitors and forecasts credit growth and liquidity to measure and anticipate economic growth. You can subscribe to Macro Watch at https://www.richardduncaneconomics.com/ where you can save 50% with the discount code: authority

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/16/2017 - The Roundtable Insight: Charles Hugh Smith On The Commercial Real Estate Bubble Caused By Financial Repression

“What we’re really discussing is a mismatch between the amount of money pouring into commercial real estate and the actual return on that investment”

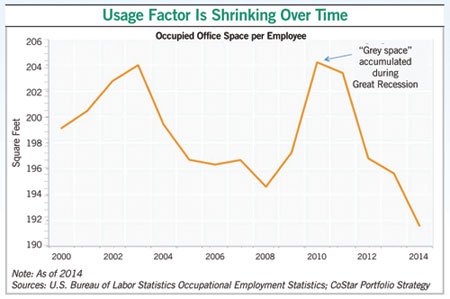

We have a large supply of commercial real estate out there but the supply is still increasing, they’re continuing to build and have overbuilt in many areas. Meanwhile, the demand side is low and is still moving downwards. There have been very high vacancy rates in the U.S. specifically in the office and retail sectors.

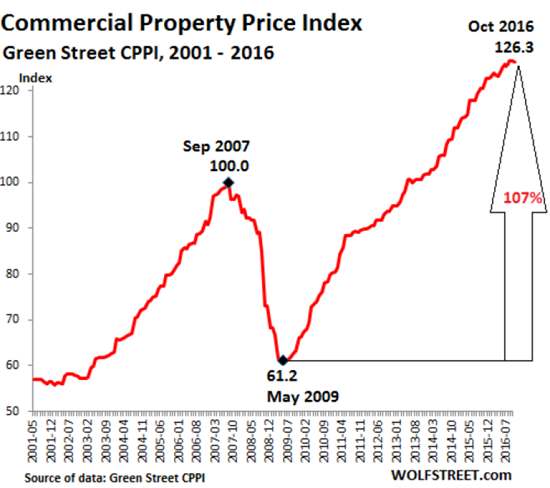

There is also generational trends in play, there is less demand for office and retail space because millennials are causing the office space standard to rise and retail is more often done online at websites such as amazon. At the same time, there are valuations that are sky-high, even higher than the financial crisis. This could boil over as soon as 2018, but the central banks should have enough tricks up their sleeves to save the system one more time, but they’re running out of rope to do that a third time.

From the podcast:

Charles: The commercial property price index has now exceeded the previous bubble top in the 2007-2008 period by about 25%. So we’ve got a bubble that exceeds the previous high, and that should alert us to the potential for some downside here.

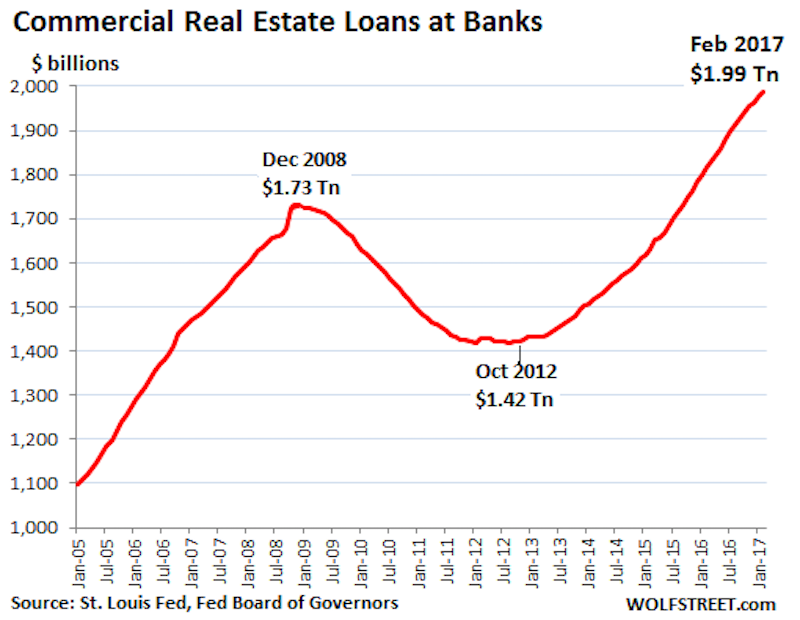

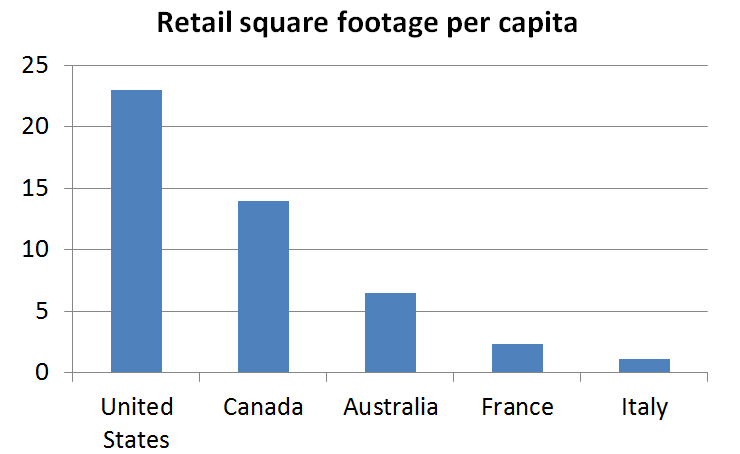

And if we look at commercial real estate loans at banks, then we see the chart is almost just an exact overlay of the price action. In other words, we’ve got more loans by about 25%, basically $2 trillion of U.S. commercial real estate loans. What makes that sobering is if we look at the retail square footage per capita.

We find that the United States has multiples, and so does Canada actually, has multiples of what other countries, advanced post-industrial companies like France and Italy. They have 2 or 3 of square foot per person and the U.S. has almost 25 and Canada has almost 15. So it looks like we’ve got a situation where there’s a lot of leverage debt on an overbuilt sector.

FRA: And you mention also that they’re still building and a lot of places have been overbuilt?

Charles: Yeah, I dug up a chart called Retail Space under Construction, and this was a year ago first quarter 2016, but there are millions of square feet of shopping centers, malls, and specialty centers still under construction.

Now if these are all in extremely hot markets like Toronto, or Vancouver, Silicon Valley, Brooklyn, then of course there’s going to be a demand for this kind of space, but these white-hot markets are fairly limited and so there’s a suspicion that there’s a lot of space being added to an already extended inventory.

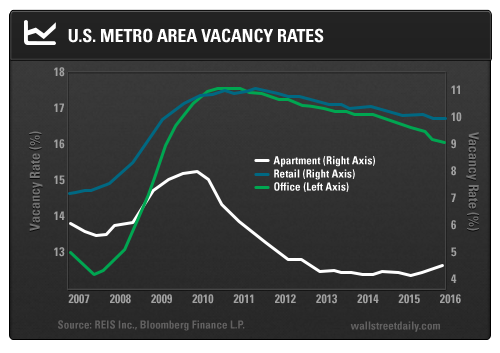

Charles: We can see that the residential vacancy rate has plummeted from the 2010 post financial crisis peak. And it’s essentially near zero, around 3% or 4%. But the retail and office vacancy rates are still hovering around 9% or 10% which is way above where they were in 2007 and 2008. So this vast expansion of credit and some of that money is pouring into retail and office commercial real estate, but the demand really isn’t there. And we know that because of these high vacancy rates.

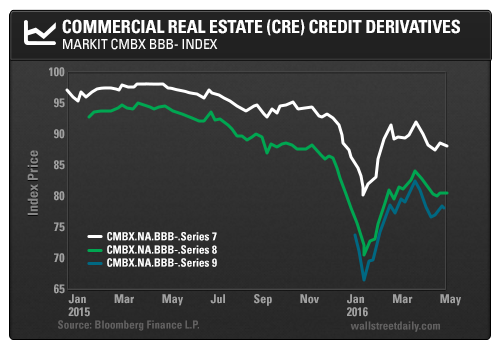

FRA: You also add a chart on commercial real estate credit derivatives which gives an indication of the risk inherent in commercial real estate, is this indicative of rising risk in that sector?

Charles: Right, this chart is credit derivatives and it’s a fairly high-risk series, its BBB not AAA, so this is the kind of credit derivatives that are sensitive to risk and interest rates. And there was a very steep decline, a spike down about a year ago, the first quarter of 2016 in these commercial real estate credit derivatives which showed that there was a heightened sense of “we better get out now” and limit our exposure to the credit derivatives on the commercial real estate sector. And it’s recovered, but it’s recovered to a lower high then it was. It was quite stable all the way through 2015. So this is telling us that the financial people that are exposed to the commercial real estate sector are starting to hedge their bets and starting to pull the trigger to minimize their exposure, which means they see a heightened risk.

Charles: This chart shows how much space employers now provide to each of their employees. And that number is plummeting from 2010 as businesses have to get more efficient, they need less office space. And if you combine that with flex work and working at home and teleconferencing its hard not to conclude that we as an economy are going to need less office space. And in the retail sector, the number of stores closing is at an all-time high, it’s far exceeded the 2008 financial crisis peak.

So what we’re seeing is a huge fleeing and closure of the retail sector, and a lot of subletting going on in the office space sector, so there are corporations and retail business which are shedding space because that space is no longer generating sales and profits.

If you would like to learn more about Charles Hugh Smith’s work, you can visit his website at http://www.oftwominds.com/ where you can look at his archives and read free samples of his books.

Summary written by Jake Dougherty<jdougherty@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/14/2017 - The Roundtable Insight: 5 Top Money Managers Discuss Austrian School Investing – Now Published

Today we have five panelists from around the world, Russ Lamberti from Cape Town, South Africa, Mark Valek from Liechtenstein, Chris Casey from Chicago, Bill Laggner from Dallas, and Mark Whitmore from Seattle.

Chris is the Managing Director of WindRock Wealth Management. He combines a degree in Economics from the University of Illinois with a specialty in the Austrian school of Economics. He advises clients on their investment portfolios in today’s world of significant economics and financial intervention. He’s Also written a number of publications on a number of publications on websites including the Ludwig von Mises Institute, Zero Hedge, Family Business, Casey Research, and Laissez Faire Books. He is a board member of the Economics Development Council with the University of Illinois, a Policy Advisor for The Heartland Institute’s Center on Finance, Insurance, and Real Estate.

Bill is a Co-founder of Bearing Asset Management, he’s a partner with Kevin Duffy that manage the Bearing fund using an Austrian School of Economics lenses in terms of identifying boom-bust cycles, value in the marketplace, bubbles, and distortions created by both fiscal and monetary authorities. He’s a graduate at University of Florida, began his investment industry career in the late 1980s initially as a stockbroker, and then moved to the buy side at fidelity investments. He’s been featured also in Barrons, Reuters, and CFA magazine.

Russ Lamberti is the founder and chief strategist of ETM Macro Advisors. Which provides Macroeconomic intelligence and strategy services to asset managers, family offices, and high net worth individuals. He is the Co-Author of “When Money Destroys Nations”, a book about Zimbabwe’s hyper-inflation, and he’s a contributing author at the mises.org institute.

Mark Valek is a partner investment manager of incrementum, he’s a Chartered Alternative Investment Analyst (CAIA) and has studied business administration and finance at the Vienna University of Economics. From 1999 he worked at Raiffeisen Zentralbank (RZB) as an intern in the Equity Trading division and at the private banking unit of Merrill Lynch in Vienna and Frankfurt. In 2002, he joined Raiffeisen Capital Management and in 2014 he published a book on Austrian Investing. He’s one of the authors of “Austrian School for investors”.

Mark Whitmore is the Principal, Chief Executive Officer of Whitmore Capital. Mark has been managing personal portfolio assets, periodically publishing newsletters and blogs, and providing pro bono financial planning/investment consulting since leaving law in 2002. His specialties are currencies and international economic analysis. He obtained a B.A. in Political Studies from Gordon College, graduated Summa Cum Laude at the University of Washington he earned a Masters of International Studies (MAIS) at the Jackson School and a J.D. from the School of Law.

Austrian School of Economics Explained:

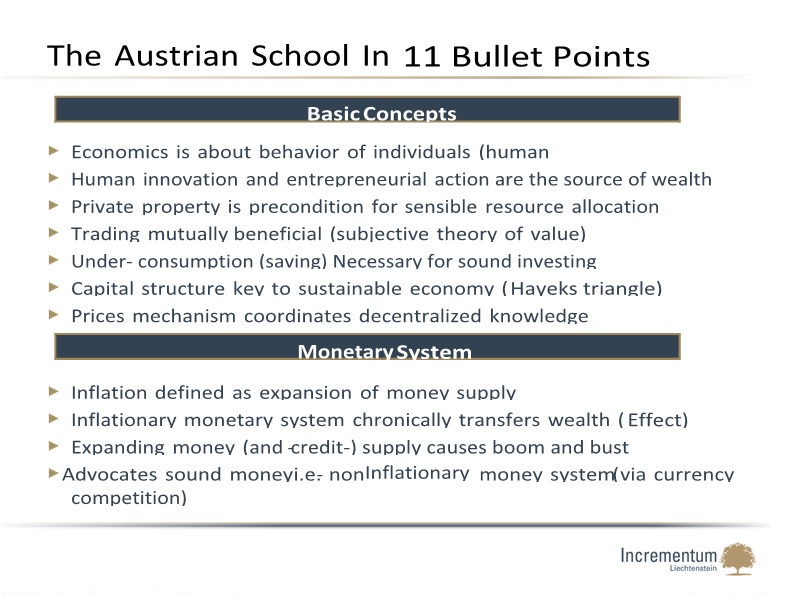

Mark Valek defines some basic points and differences of the Austrian School as: Economics about the behavior of individuals and human action, The Subjective value theory, under consumption of savings is necessary for sound investing and growth, capital structure being key to a sustainable economy, and price mechanic mechanism coordinates the centralized knowledge. Perhaps the most important distinction of Austrian Economics is its view towards the monetary system. Some of these points are inflation being defined as expansion of the money supply and finally expanding money and credit supply causes a boom and bust cycle in the business cycle theory.

He points out that these are the typical differentiating points, but this is by no means a complete list, and you can discuss the differences between the Austrian School and traditional Keynesian theory.

Russell Lamberti thinks that one of the key differentiators from a practical analytical and investment perspective was that the Austrian school draws a very straight and consistent line between microeconomics and macroeconomics. He notes that at the microeconomics level, Keynesianism is very similar, but when they aggregate it up to the macro, a whole different theoretical framework is used and there’s essentially no consistency between neo-classical and Keynesian micro and macroeconomics so there’s a fundamental break down there. He ends the thought by saying in today’s Macro world it’s only really the Austrians who are talking about the unsustainability of certain demand trends because of misallocated capital and misallocated productive resources and that’s why he thinks the Austrian Business Cycle is such a key distinguishing feature of the Austrian school.

Chris Casey discusses why Austrian Economics can provide new insight, saying that Austrian Economics is the only one that really puts man at the center of the discussion. It boils economics down to man in the context of nature as it relates to scarcity for his needs and wants. And in so doing they then use a number of first principles that build on from the deductive reasoning standpoint to create a consistent and sound economic school and economic philosophy. And that’s what really makes the difference from the other economic schools out there. It’s not just the conclusions, it’s how we arrive at those conclusions.

Mark Whitmore adds that specifically, the role of central banking is something that is really distinct from an Austrian perspective vs Keynesianism. Specifically the asset price inflation that you’ve seen has largely been ignored by Keynesians in the last two bubbles. Now we’re into a third bubble I would argue as well. And essentially the Fed and the Keynesians will continue to point to there being really no headline inflation pressure and hence there’s really no reason to begin to normalize or adjust or move up interest rates meaningfully. And I think that from an Austrian standpoint, this exacerbates this boom-bust cycle which we’ve seen which has been really compressed in terms of time lately versus what has historically been the case. Since the mid to late 90s the amplitude of bubbles to the upside has just been far greater. He highlights Henry Hazlitt’s two points as far as critiques of Keynesianism. The first one being that fundamental flaw in terms of interest, with Keynesians tending to service the visible minority at the cost of the invisible majority and again it gets to this whole issue of government being the problem solver, the one that can allocate assets essentially, in its view, the most effectively from a Keynesian perspective in a counter-cyclical effective way, where the Austrians are much more skeptical of the accuracy of that. And second,the propensity under Keynesian Economics to over-consume in the present generation at a cost of creating massive debt or future debt for future generations to essentially somehow deal with, we’re sort of seeing that today in all developed parts of the world.

How it’s used in past, present and future Economies including how and why the 2007-2008 financial crisis happened:

Bill Laggner says what was interesting was that the internet created this initial innovation wave decentralization wave, and of course due to excess credit creation, money creation, you had a bubble and then a subsequent bust. And then instead of letting the system purge and heal, the central banks led by the U.S. came and lowered interest rates and you segued from a technology bubble to a private sector credit bubble. And of course it went longer then everyone on this call thought it would, and it eventually hit a wall and again tried to cleanse and it’s interesting central banks let certain groups fail and then when things started to get out of hand, they stepped in and bailed out a number of politically connected contingents and then laid the foundation for this third bubble, and this third bubble’s gone on longer I ever imagined or my business partner imagined that it could. He also points out that the distortions are epic, and that this won’t end well.

Mark Whitmore chimes in discussing Kurt Rickenbacker’s idea of “Ponzi finance” which is a powerful analytical insight that essentially the boom-bust cycle is endogenous to the particular type of finance credit system you have in place.Credit can thus becomes increasingly untethered to any kind of historic connectors such as sound collateral. One increasingly witnessed these signs of the economy going off the rails in the upward direction in a trajectory that was simply unsustainable. So indeed that bubble went longer than most of us expected, and this one is truly epic.

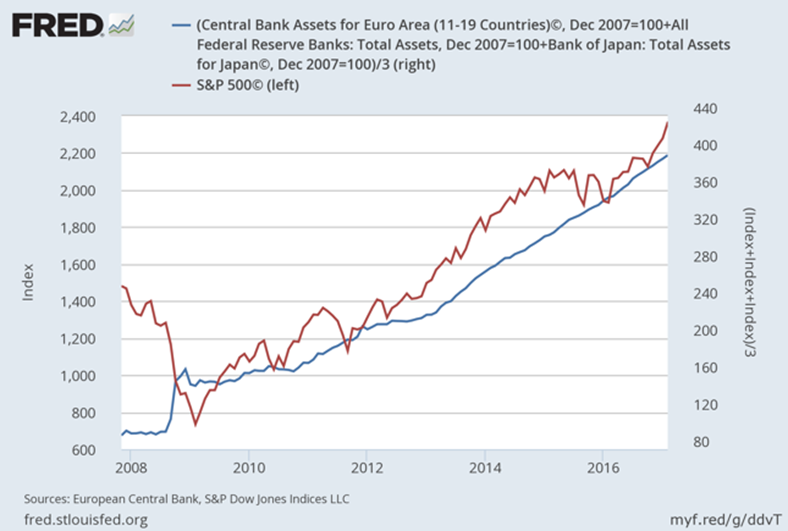

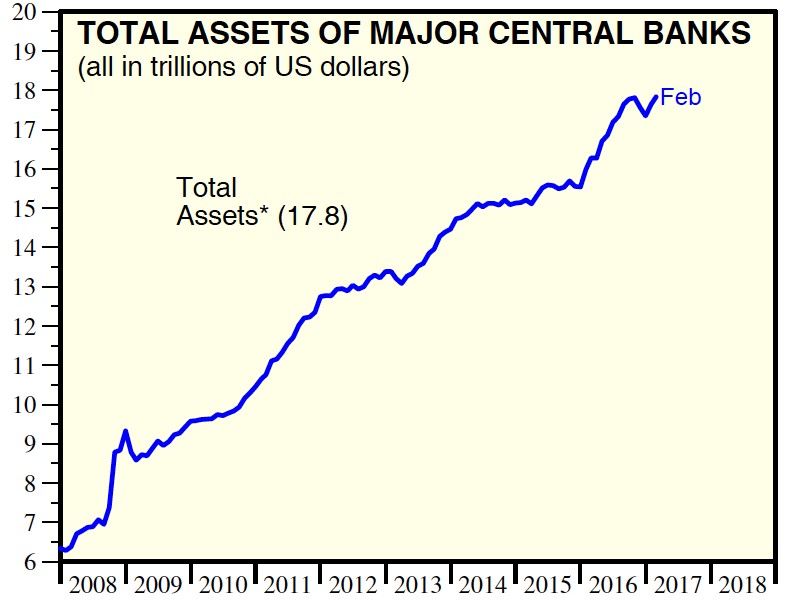

* Includes the US, ECB, BOJ and PBoC.

Sources: Yardeni Research, Inc. (www.yardeni.com); Haver Analytics

He notes that the curve and amplitude of the line showing the increase in central bank assets seen above is almost exactly the same as the line showing the increase in the S&P 500. He calls this the engine that’s driving what’s been taking place in terms of asset price inflation and ends by calling it highly unstable, and saying again that this will not end well.

Russell Lamberti emphasizes the importance in looking at this as three very big bubbles in a row, but also to think about the compounding effects of repeated malinvestment that has been essentially dis-allowed from correcting and from reallocating promptly. He also discusses this unwritten law against recessions, saying this is not just a problem in America, this is a problem everywhere in the world. Politicians don’t like recessions. As they push back through repeated cycles we have chronic malinvestment, chronic poorly allocated capital. And this creates a hostile working lifetime of living in an essentially very strange unreal financial and capital structure. He ends by saying: we’re in a third very excessive state of distortion and the best case scenario that we can hope for is a sharp, painful clear out of chronic malinvestment. That is the fastest path to genuine economic progress again, I hope we get there soon.

Chris Casey adds that when discussing how Austrian Economics explains the 08 crisis gives us some guidance to future bubbles in economic recessions, it’s worth recounting what can not explain the 08 crisis, and that is mainstream economics. And it’s worth remembering that in 2002 at Milton Friedman’s 90th birthday party that Ben Bernanke stood up and literally apologized for the great depression, and he basically said something to the effect of “we won’t do it again” and so that tells you central bankers pretty much around the world do not understand the causes of recessions at its most fundamental level. “They can’t explain why it occurs, they can’t explain why it’s a cycle, they can’t explain what Austrians call ‘the cluster of error’, why all these businesses have made horrendous investment decisions. They can’t explain why every recession is proceeded by monetary inflation, they can’t explain why certain industries are far more cyclical than say consumables. So it’s just something that cannot be explained, the Austrians do, and for the listeners who may not be all that knowledgeable on the Austrian School, in short, whenever you inflate the money supply, you are decreasing interest rates which distorts the whole structure of production, it forces economic actors to make investments they would not have otherwise done, that they would have otherwise deemed unprofitable, and it creates this malinvestment in the system, as my colleagues here today mentioned, we’ve already seen this play out twice in the last 20 years. And the response, if that’s the causation of a recession, the response should be hands off.”

The Austrian School Investing, Investments/Asset Classes/Investment Strategies

Bill Laggner discusses how knowing the Austrian business cycle theory is helpful in fact, during the second bubble, the credit bubble, he wrote an article with a colleague called “collateral damage”. And what he found fascinating about writing the article was the Bearing Credit bubble index created back in 2004 when it was pretty obvious that we were segueing into this new bubble. He says: I kept looking at the types of asset backed securities are being created mainly, and mortgage arena, and then the derivatives wrapped around it, and then attended a few conferences. But I started focusing on the collateral because it’s a confidence game, right, I mean people have confidence when these troubles start, they grow and what was interesting was in 2005 the home-builders had started declining severely and writing down land values ext. but subsequent to that you had maybe 12-18 months of watching paint dry. I mean the other related industries kind of kept chugging along. And it wasn’t until early 07 where the secondary market for certain types of mortgage backed securities just locked up. And that was the beginning of the end. So to me, when I look at excess credit creation through the socialization of credit by the central bank and or other government agencies like Fanny and Freddie in the U.S. I was looking at collateral that was kind of a helpful sign that we were near some kind of inflection point. I think what makes this cycle so much more difficult, and look full disclosure I mean we’ve had a net equity short bias for the last several years, and it’s been pretty painful. I think this cycle, because they’re all playing the same game, they’re all in together. Is there any limit to what the central bank balance sheets can go to? I mean, how many bonds can the central bank give Japan or the ECB or the Fed purchase, and I think it’s pretty clear that since all the chips are in the middle of the table, they’re going to continue to buy bonds, and try and hold certain parts of the yield curve suppressed to keep the game going.

Chris Casey discusses how it’s unclear if Austrian Economic principles are necessarily applicable to investing, but Austrian Economic conclusions certainly are. He goes on to say “They certainly are as they relate to the macroeconomic phenomena of recessions and inflation. Because these are the two forces that create the greatest risk factors regarding ones investment portfolios. The recessions are going to pop any bubbles that are out there pushing the equity markets, and inflation will destroy the bond markets. And when you’re looking at equities or bonds, these obviously make up for most people the vast majority of their investment portfolio or at least the core of the investment portfolio. So if you’re able to use Austrian economics to navigate these two risk factors, I think it presents a tremendous advantage for investing. As far as whether or not there’s been empirical evidence demonstrating this, not to my knowledge, I think it would be difficult to construct such a study for a couple reasons. One being the time period that we’re looking at. Austrian economics hasn’t been utilized in this form for very long. And secondly would be the sheer number of people using Austrian Economics in this fashion. It’s a very limited set. The people here on the call know that they represent a good portion of that universe, may be the universe, of people managing money with Austrian Economic concepts in mind.”

Mark Whitmore also tends to be somewhat skeptical as far as can you look at Austrian Economics as instrumental tools for specific kinds of investment analysis or recommendation. What he think is incredibly valuable is how you explain the efficient market theory; this idea that whatever the price of the given asset is at any time, it’s the “right price”. Because all the information is being priced in so trying to outguess the market is kind of a fool’s errand. And I think that one of the most basic, the most essential insight of Austrian Economics is this idea of subjectivism, and that prices are wholly derived by human beings, and one of the other schools of economic thinking that I think dovetails nicely with the Austrian school is Economic behaviorism, this idea that individuals are driven by greed and fear, and as a result, and this feeds very much into the boom bust cycle of the Austrian framework, that you get these ridiculous, unexplainable run-ups in asset prices that leads to catastrophic losses.

Russell Lamberti thinks it’s about creating a coherent perspective of macro-reality, saying how there’s so many investment firms, you go on their websites and they talk about how they like to find miss-priced assets because they believe that the market doesn’t always effectively price assets. But they’ve never really got a coherent reason why. He goes on to say “I think the nature of clusters of error of boom and bust cycles, of the business cycle creates a very coherent reason why you get big distortions and big mispricing. And what I try to do for my clients is I say to them that ultimately using Austrian principals is essentially about creating a coherent perspective of reality, and also using that coherent perspective of reality to compare it to the market narratives that emerge. Donald Trump gets elected, and there’s a narrative there that emerges, a reflationary narrative. A narrative might be that he’s going to deregulate and the market finds an excuse to run even higher. And you’ve got to kind of test all these market narratives against really sound perspectives of reality. In addition to that I’d say a few things: one is that an Austrian perspective gives you an understanding that you’re not in a free, unfettered market, you’re in a market where the state plays an incredibly dominant role and is essentially trying to plunder private resources. And so a huge element of investment strategy from an Austrian perspective has to be at the sense of you are defending your wealth against the plunderers”.

Mark Valek thinks knowing Austrian Economics provides you with a potentially huge edge. He points out that even though you can read about it online at mises.org or on other websites, many people don’t care enough or are not aware of it. He thinks another large edge is that Austrian Economists in general are able to understand alternative currencies much better. They are able to think about it outside of the money system just as we all think so much about the current system, that helps us for instance when bitcoin currency came up. So knowledge of Austrian Economics can provide a good investing edge sometimes in an indirect way as long as it’s utilized properly. He also discusses the potential weaknesses of using the Austrian system, saying that strictly speaking from an Austrian School, you don’t get any help regarding the timing of when we would expect to happen, however, you can still use other theories to help with that aspect. The last potential risk he discusses is that Austrians have a dogmatic bias and tend to be very cautious in an investment space.

Ethical Issues:

Russell Lamberti points out that “We all have to make a decision about leverage. In a system where debt is created by fractional reserve banks, we understand that the core of business cycle problems arises from creating debt liabilities without prior saving – this is a systemic problem. And of course when you participate in that system, there’s two ways you can look at that. You’re ether participating in the bank and leverage system as a defence mechanism against that system, but you can also argue that you’re aiding in advancing that system, so I think every investor has to answer some pretty tough questions about leverage and about the kind of leverage.” Bill Laggner agrees and adds “I think people are leaving tax-free bonds or government bonds and doing other things with their capital, getting involved with private local businesses. I don’t want to get too far off track but I think that is something clearly playing out”.

How Austrian Economics help you when looking at investments from a risk-return standpoint:

Chris Casey recalls what Mark Whitmore pointed out and added “hopefully I’m not misinterpreting him, but I believe Mark made a point that Austrian Economics doesn’t help us analyze any particular investment vehicle or perhaps even investment asset class, and by that I mean just because one company has more or less debt then another company doesn’t make it more or less Austrian. Or just because a company operates in such and such industry doesn’t make it more or less Austrian. Austrian Economics helps us because of the explanations as to inflation and recession. It helps us protect portfolios it helps us minimize risk. It also helps us profit from macroeconomic developments when they occur. Primarily meaning any kind of pops in bubbles or bond markets, whether stock or bond markets. So there you want to look for investments that will do well in that context, or that will weather the storm so to speak and do well regardless as to what happens. So you want to consider industries that potentially have high growth that will not be negatively impacted or at least will not shrink or be reduced in size through the effects of inflation of recession. Maybe you want to look at investments that historically have done well when you have inflation, meaning you want to consider gold, you want to consider farmland, things like that. So, I think Austrian Economics again helps us from an investment portfolio standpoint, minimize risk, and really seize onto some great opportunities as these things transpire. But as far as analysing any particular asset or asset class, I don’t think they lend that much value.”

Mark Whitmore adds “this notion of efficient market theory which attempts to just buy and hold the market no matter what, being completely price indifferent is clearly suboptimal. And that’s really key, as that Austrians, I think, have a sense of value in the marketplace naturally. And it doesn’t come from any unique insight of the Austrian School, other than the fact of the combination of the subjectivism coupled with the inherent boom-bust cycle makes those of us who use Austrian Economics very sensitive to issues of price and value. I think a cynic is often defined as someone who knows the price of everything and the value of nothing and I feel like Austrians are exactly the opposite. Whereas other investors are chasing price action if you’re somebody who’s sort of a trend follower or you’re simply buying and holding, there’s a greater tendency among Austrian investors to appreciate value.”

Mark Valek: http://www.incrementum.li/ and he has a book called “Austrian School for Investors” available on amazon.

Abstract:

Austrian Economics takes into account the behavior of man, and has different views than traditional economic theories on monetary policy, and differs from Keynesian economics greatly on the macro level. It can also be used to identify when there is too much debt and when bubbles are in danger of bursting. Austrian Economics can be very useful for observing the overall behavior of the economy and can often help an investor make more informed decisions.

FULL TRANSCRIPT

FRA: Hi, Welcome to FRA’s Roundtable Insight. Today we have a special treat for our listeners, it’s a discussion on the principals of the Austrian School of Economics and how those principals can be used in investing. Today we have five panellists from around the world, Russ Lamberti from Cape Town, South Africa, Mark Valek from Lichtenstein, Chris Casey from Chicago, Bill Laggner form Dallas, and Mark Whitmore from Seattle.

Welcome Gentlemen

So I thought we’d have a discussion initially about what exactly is the Austrian School of Economics and how does this school of economics differ from other schools such as the Keynesian School of economics. Mark Valek, would you like to begin?

Mark Valek: I’d love to, thanks for having me, very excited to discuss basically an economic school which is from Vienna, my hometown, unfortunately Vienna, in the University doesn’t really teach Austrian Economics anymore. However, I think the topic of the Austrian School is a big one, one can talk for hours on end on how it differs, we actually tried to make the Austrian School to list the 11 of 10 bullet points, we came up with an 11th one so we could describe the Austrian school in 11 bullet points. And this is by no means a complete observational but just some basic concepts we put together, we refer to them:

Economics is about behavior of individuals, it’s basically about human action

They can point human innovation and entrepreneurial action of a source of wealth creation

Private property is preconditioned for sensible resource allocation

Trading is mutually beneficial (The Subjective value theory. Theory of Value)

Another point would be under consumption of savings is necessary for sound investing and growth

Also, very important point I think which differentiates the Austrian school is its view towards capital structure. So capital structure is key to a sustainable economy. Thinking about Hayek‘s triangle for the guys who know what I’m talking about here.

And price mechanic mechanism coordinates the centralized knowledge.

So these were some basic, basic concepts and they are not only found in the Austrian School, perhaps what does differ more is the view towards the monetary system. And I just want to add 3 or 4 points regarding the Austrian view on the monetary system:

Inflation, for instance, is defined as expansion of money supply, something very central to Austrian Economists

Inflationary monetary systems chronically transfer wealth, I’m talking about the Cantillon effect, something I think the other schools really don’t talk about at length and it’s something very interesting for society also these days.

And finally expanding money and credit supply causes a boom and bust cycle in the business cycle theory

So these are perhaps the more typically differentiating points, especially from the Austrians, but this list is by no means complete, just a few thoughts perhaps to put on a discussion.

FRA: And Russ you’re perspective on the Austrian School of Economics