09/18/2017 - The Roundtable Insight – Nomi Prins On The How G7 Central Banks Are Coordinating Monetary Policies Together

09/18/2017 - The Roundtable Insight – Nomi Prins On The How G7 Central Banks Are Coordinating Monetary Policies Together

FRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Nomi Prins. She is a renowned journalist, author and speaker. She is currently working on a new book, “Collusion”, formally called, “Artisans of Money” that will explore the recent rise of the role of central banks and the global financial and economic hierarchy. Her last book, “All the President’s Bankers”, is a ground-breaking narrative about the relationships of presidents to key bankers over the past century and how they impacted domestic and foreign policy. Before becoming a journalist, Nomi worked on Wall Street as a managing director at Goldman Sachs, ran the international analytics group as a Senior Managing Director at Bear Stearns in London, worked as a strategist at Lehman Brothers and an analyst at Chase Manhattan Bank. Welcome Nomi.

NOMI PRINS: Hi – Thank you very much Richard.

FRA: I thought today that we would focus on a recent writing you have that stems from your emerging book, “Collusion”, it’s titled, “A Decade of G7 Central Bank Collusion – And Counting”. It’s a great piece and it’s available on your website and has been reprinted elsewhere as well. I was just wondering if you would like to give us a brief synopsis of that.

NOMI PRINS: That piece comes from some of the conclusions that relate to ongoing monetary policy globally, particularly with the G7 central banks. When I talk about collusion, in terms of the importance of setting monetary policy to the G7 for the G7, there have been, since the financial crisis of the United States, so many multiple meetings, background meetings, calls, statements between the central bank leaders and so forth which collectively have created a monetary policy that is zero percent interest rate and has also connected to it a substantial amount of asset buying or what we now know under the term, quantitative easing, by the major central banks in particular. It’s not that other central banks haven’t been co-opted or have retaliated by trying to set their own monetary policies in their own countries, but it just so happens that this has been a G7 process that has been led by central bank of the United States, the Federal Reserve, and particularly the G3 central banks: the Federal Reserve, the European Central Bank and the Bank of Japan, that has together kept interest rates on average zero and are set on course, since the last year and a half, have raised interest rates up to one percent. But while that happened, 19 countries in Europe including the ECB have rates at negative as well as does Japan, and the Japanese central bank on average comes out to zero percent. And it’s not an individual policy – it’s a collusive collaborative policy.

FRA: So, it’s almost like the collective set of G7 central banks are acting as a unified central bank. Can that be stated?

NOMI PRINS: Yeah. They are absolutely acting as unified and occasionally they have independent commentary to their regions whether that be throughout Europe, in the United Kingdom, or Japan. But the idea is that, even if you take these individual statements and meetings and media coverage separately, the reality is, this is a coordinated effort. For example, last year when the Fed had raised rates and it caused a lot of chaos in the markets in the beginning of 2016. Immediately, some of the other major central banks in Europe and Japan had cut their rate down and it was like a balancing act. But the way the coverage works in general is that it tends to be independent and so what I looked at for the book is all of the communications, collaborations and the timing of all the various monetary moves, which again, have collectively averaged to zero. But there is a process along the way, after the financial crisis, where the Fed first embarked upon zero percent interest rates – They were the first to embark upon quantitative easing by simply buying US government bonds, treasuries and very soon after that, US mortgage bonds from the private banks that needed the liquidity and capital. But this sort of grew and you have the European central banks buying corporate bonds; you have the Japanese central banks buying collections of equity here and there. So the process segued into different details, but it was very much coordinated and over the years, for example, there was a particular problem with debt in 2012 in Europe with a potential credit crisis, after all of these years of cheap money and the potential for defaults, that’s when again central banks got involved and acted in a unified fashion. So throughout the period in the last 10 years since the US financial crisis began, there have always been these iterations of collaboration and them acting as a unit even though their individual leaders tend to behave within their own countries, to their own government, as if they are acting independently.

FRA: It almost seems sort of like a game of passing the baton like an Olympic team running event. I remember back in 2014 there was a time when the Japanese central bank, the Bank of Japan, seemed to have taken over the baton, if you will, from the Federal Reserve and it almost seems that when one of the countries get into trouble they let that country run with more quantitative easing. Do you feel a lot of examples of that?

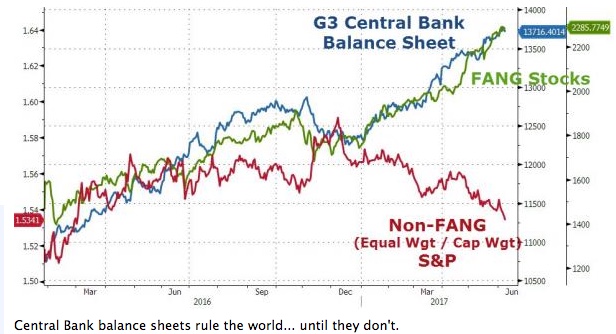

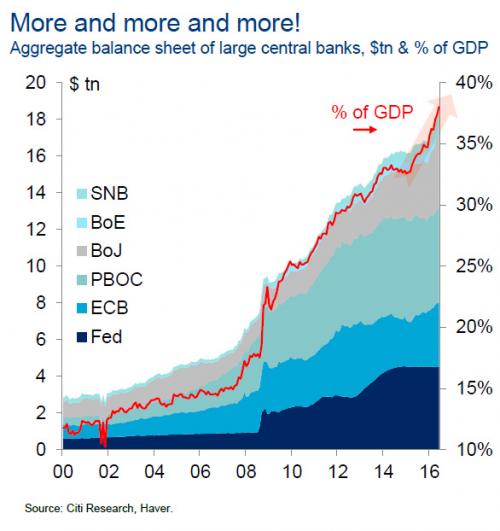

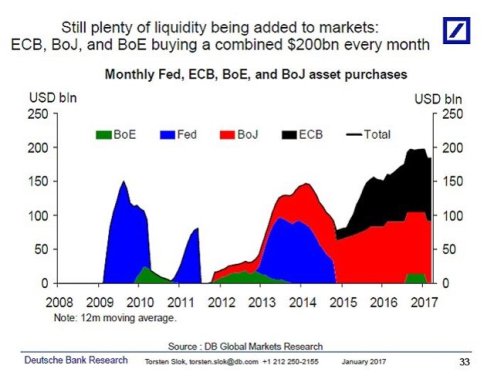

NOMI PRINS: Yeah, it’s actually interesting. If you look at just the chart of the easening and then hone that into the G3 from the last 10 years, you will see exactly what you’re saying. And then what began in 2013 is that the central bank governor and the Bank of Japan’s [Haruhiko] Kuroda when on this crazy, very fast accelerated pace of quantitative easing. And so what wound up happening was, if you look at a chart of purchasing of Japanese government bonds by the central bank, all of sudden the line went up in almost a straight-line fashion – A very steep line upward because two things happened: the president of Japan and the central bank of Japan were incoordination as well within the country. So there was coordination between letting the Bank of Japan go nuts on quantitative easing and then it worked within the fiscal policy promises of Shinzō Abe, who had just come in as well as the leader of Japan. He wanted to improve the economy. His concept was that he had 3 pillars of an economic policy, one of which was having cheap money and that worked with what the central bank leader wanted to do because he is quite international as well and saw his opportunity to increase quantitative easing. And that also had the effect of accelerating the Japanese stock market, had the effect of accelerating the flattening of the yield curve, purchasing of government bonds and so forth. As recently as a few weeks ago, the central bank leader of Japan, Kuroda, was talking about this idea of unlimited capacity to continue to buy bonds or to continue the quantitative easing process which also is what Mario Draghi, in slightly different words, was doing in Europe. So, it is a passing of the baton and you would think that after 10 years of what began, according to the Fed anyway, as emergency measures in the wake of the financial crisis and the idea of if we go back then was that there was no liquidity in the banking system, and that there was a fear that was stoked by the Treasury Secretary Henry Paulson, the Federal Reserve head at the time Ben Bernanke and the New York Federal Reserve president Tim Geithner who all basically got together and colluded to indicate that: unless there was an immense amount of liquidity offered to the banking system, everything would seize up and people wouldn’t be able to get their money of out ATMs. And so they created this bailout from the standpoint of congress, but the bigger bailout was what the Federal Reserve and central banks did which was at the time, start to bring bank rates down to zero at the end of 2008 and then start to buy bonds. Then when the Feds stopped, the European central banks started and it accelerated and then the Bank of Japan continued to accelerate. And then you have smaller central banks involved such as the Bank of England who have half a trillion or so assets on their books. They have kind of dibbled in and out, but recently they have talked about expanding their quantitative easing program, Mark Carney did, the head of the central bank there. And they kind of use it as this tool – They promote it as this tool, to either stimulate growth in economies or to create stability in opposition to some type of a problem or a process. When we had the problems with Hikoshimi, we had the other G6 central bank governors get together and promise that they would help with whatever liquidity was needed for Japan to navigate that crisis. So, what began as an emergency measure has become normalized.

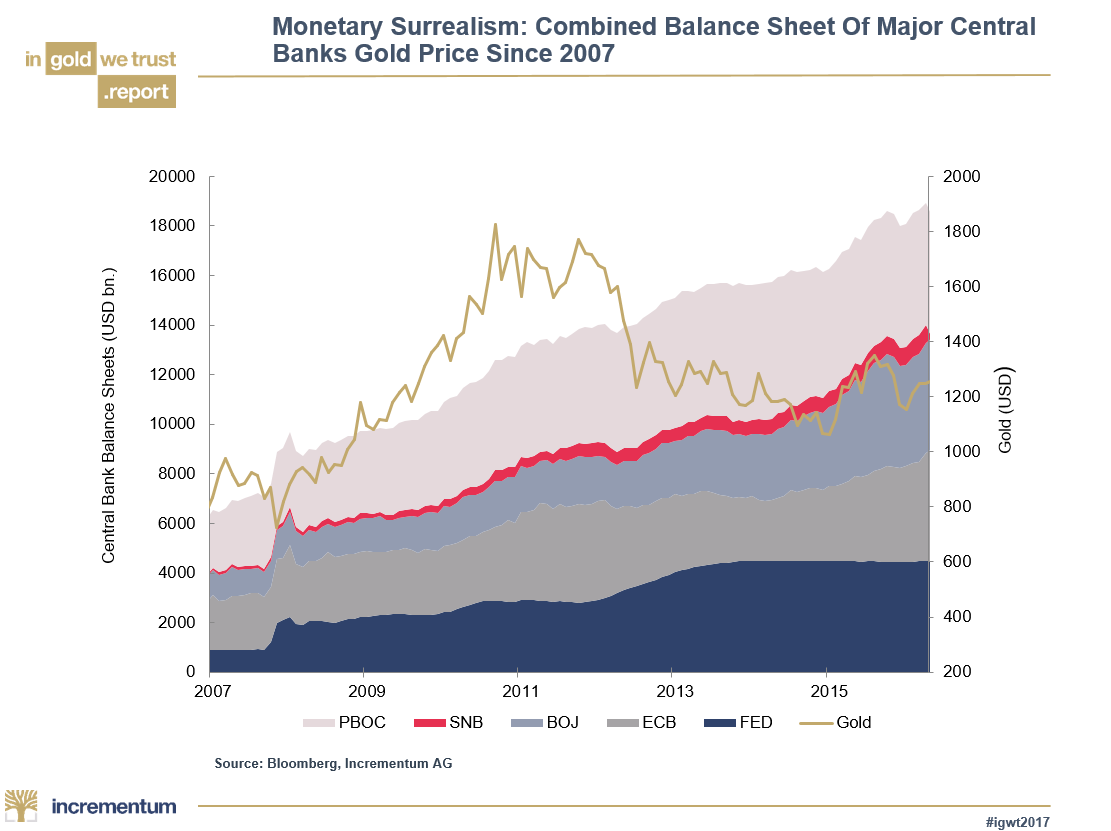

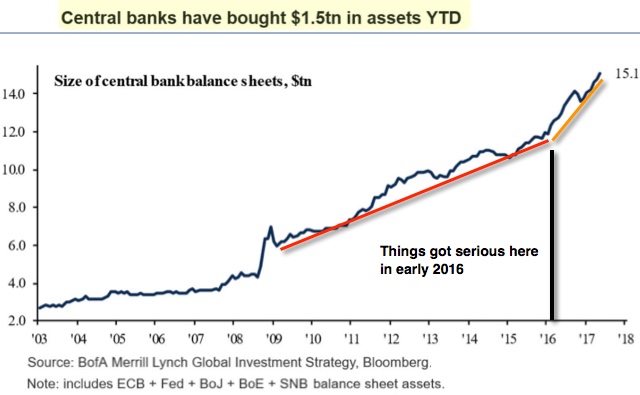

FRA: In the collusion article, you mentioned that the central banks have amassed assets on their books worth nearly 14 trillion. Is that for the big 3 central banks or the G7?

NOMI PRINS: Yeah – that is exactly right. The G3 are at about, give or take, 13½, then you add in the UK, Canada and other banks and it’s probably a little bit more than that, but on average it’s between 14-14.3 trillion – It’s a fairly large number. If you consider that that number was basically zero 10 years ago.

FRA: And you mentioned the result of all this is the fuelling of bubbles and money that isn’t serving any productive real economy purpose because it happens to be in lockdown. Can you elaborate on those?

NOMI PRINS: So if I’m a central bank and over some period of years I decide to create electronic money, we refer to it as printing money, but the idea is: creating some fabrication for money that is then used in an exchange process for either government bonds or, in the case for the US for example, mortgage debt from the banks. What that does is puts this fabricated money into the system which didn’t come from tax receipts or organic growth in companies, it was merely manufactured. And it was an offering return for the Fed amassing debt on their books – Debt in the form of treasury bonds and mortgage bonds. So, what that means is that it effectively created 14½ trillion dollars of money that did nothing but an exchange for debt. And if you’re just exchanging debt and you can’t determine how that debt would’ve been spent anyway, then it’s really just sitting there on the books for no apparent purpose. Now it’s not the Fed’s job, technically, to do this, but if you had examples conceived of a process by which instead of exchanging fabricated money for debt, you invested it in some sort of a national bank or you develop roads or railways with it or energy systems or whatever it might be – That is productive. Whatever the process is there could have been productive ways to utilize fabricated money to actually enhance the real economy, but if you’re just buying debt, then you can’t trace that debt to the real economy. In fact, for mortgage bonds, all you’re really doing is giving banks liquidity or giving them capital to do other things with because you’re not telling them what they can or cannot do, you’re not stipulating what kind of loans they can and cannot make, it’s just capital that is given to them – Then, that money is not being used for any productive purpose. It is on lockdown at the Fed because they basically offered it out. They have in exchange received these bonds or this debt and they are not going anywhere – They are just sitting on the books not being used for any financing or any productive purposes, real growth, wages, hiring people, research and development or really anything. And that’s been copied in Europe as well on the European central bank in terms of trillions of dollars, on the books in the Bank of Japan and so forth. So none of that money is really being used, but the way it gets discussed is that it somehow is connected to economic stimulus, but if it was actually stimulating the economy then you wouldn’t have a 10-year policy where it has to keep continuing. So, what you have now after 10 years is the central bank leaders, for example Mario Draghi at the European central bank recently, who is saying, “Hey, you know what? This is the only thing that needs to done. Creating a monetary policy alone or low interest rates and buying bonds alone isn’t enough to stimulate the economy”. So, after 10 years they are saying we have to keep going because what we did wasn’t enough and somehow if we keep doing it and other measures get put into that, such as a type of fiscal policy, then altogether after we have done this for 10 years somehow it will relate to the economy. So, these people themselves are basically saying that this process: their collusions, methods, strategy and policies really haven’t done anything for 10 years.

FRA: You even point out how Stan Fischer who was the Vice Chair of the Federal Reserve, who recently just stepped down from that role, essentially admitted that the Fed caused low interest rates globally while failing to achieve the economic growth as promised.

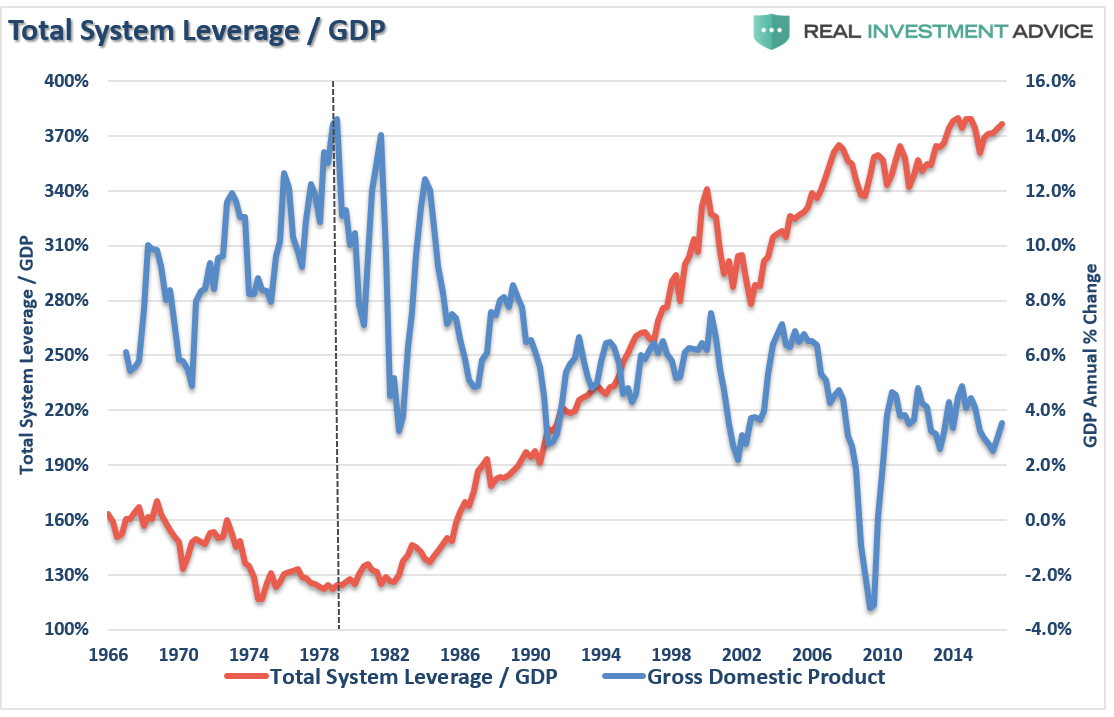

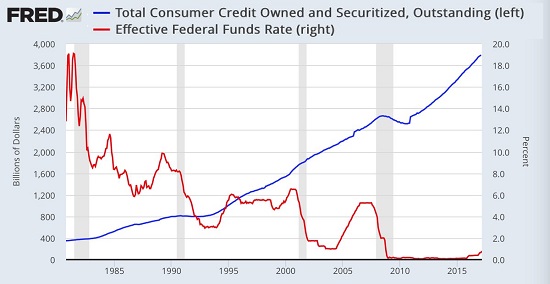

NOMI PRINS: Right. Stanley Fischer was the academic mentor for the doctorate for both Ben Bernanke and Mario Draghi who ran at different times with some overlap, between the Federal Reserve and the European central bank so it’s interesting that Stanley Fischer, who was also the Vice Chair of the Fed for a number of years before resigning, was one of the supporters of this policy throughout his years of a mentors as well of his years of being at the Fed itself. So he was one of the very people who would’ve voted at various meetings and so forth to continue to keep rates low and the effect of the Feds keeping rates low was that they were kept low globally. Now what he didn’t say was that they were actually kept low globally because they are having communications with each other and that this was not a choice, it was kind of a mutual decision and it unfolded that way in terms of events and in terms of when rates were reduced versus when assets were bought by the various central banks. And at the end admitted that it really didn’t stimulate growth and not only did it not stimulate growth, but even the Federal Reserve itself had a report out a few years ago where it indicated that after a number of years of these policies in the US it actually increased inequality. The way it does that is that this money that is being created is really only going to top bankers and through governments – It’s really not trickling down into the real economy which means that cheap money is also being used to fuel these bubbles. If rates are at zero on a 2-year or close to zero on a 10-year depending on the country, you’re not going to be investing in government bonds – You are going to be looking for something else to get returns out of. And you have this money coming to you cheaply, but not if you’re a regular person. If you’re a regular person, you are not getting money at zero percent or close to zero percent like a bank does, like a bank can give it’s major clients or like major corporations can raise debt for themselves. A regular person is stuck with much higher rates whether it’s personal loans, credit cards, student loans or even mortgages – They don’t have the benefit of the cheap money. They suffer the consequences of not having more secure investments like government bonds or even CB’s or even good rates on a savings account like they would’ve had historically. So, they’re sucked into this vortex of the stock market whether they are actively involved or not whether through their pensions, their life insurance contracts or whatever it might be because there is nowhere else for those pools of money to invest and get a return that even keeps up with a very low inflation that we’ve had globally in the last 10 years and we’ve had very low growth. The bubbles are a result of these policies and even some of the superbanks/development banks such as the IMF indicated that this is a problem, that bubbles are a problem. Everybody is aware that these policies don’t promote growth, create bubbles in the riskier markets and yet they can do nothing else but continue them.

FRA: So with all of these failed policy experiments behind us after what has happened, this brings us to the big question that you ask: Why should we have faith that the Fed or any other central bank has any clue about what to do next?

NOMI PRINS: Right – Because all they’ve done for 10 years is effectively the same policy which they then admit has not gotten them any closer to what they had indicated the policy was initially supposed to do, which was to stimulate growth. In emerging countries it is more volatile, but slightly higher, but in terms of real growth it’s not there. In terms of being able to invest in more secure bonds for the population or for again, pensions and insurance, you can’t do that. And so what are they going to do if there’s an actual crisis. A crisis can come in any form. It could’ve come from, unfortunately, the hurricane that just happened in Florida. I’m not saying that will create a crisis, but you have a situation where a lot of development, real estate, leverage and cheap financing going into these larger development companies and through the main banks and so forth, is hit was a stoppage in occupancy rates. Or having to rebuild and having to wait for money to come in and that trickles in to potentially defaulting on certain payments or loans. It could be anything that starts to crack these asset bubbles whether that’s a natural disaster, a geopolitical thing, a new war or whether it’s simply that rates do get raised enough in one area, and I don’t believe the Feds are going to raise rates again this year for all of these reasons, but all of these things start to become cracks to let the air out of these bubbles at which point what do central banks do? They will double-down or triple-down on what they have done. That could work for a year or two years, but it’s still an artificial stimulant to the global economy. It’s still not healthy. It’s still an external source of capital that is unlimited and unregulated from the standpoint of a policy, and that’s very artificial and creates a lot of ongoing inequality and inability, ultimately, for people to have money invested in the future and be secure about it.

FRA: Given this lessening faith or growing sense of lack of faith in central banks – Could we get a Wile E. Coyote moment in the financial markets where there is all of a sudden a large drop in the equity markets?

NOMI PRINS: You could in the extent that something happens from an external perspective whether that’s a sector that continues to default or something happens to the real estate sector or the energy sector, right now energy is going to be a little better because of what just happened, retail which was just shifted in terms of the way in which people shop such as consumers losing confidence – A lot of external things can happen that deflate confidence in what is actually a stock bubble that could drive things down. Now this policy, these 10 years, has been really unprecedented in terms of this collusion between central banks. If it were not a global policy, it would be more likely to crack in one area which would reverberate throughout the world, but because it’s collaborative, artificial and collusive, there has been this way of keeping the house of cards up. Any major thing that happens can also take that down very quickly. The one thing we learned just studying crises historically is that there has never been a global reaction of this magnitude to a crisis. What tends to happens when something hits the markets is that they do tend to go down faster than they went up. That hasn’t happened yet, but if there’s a confluence of the wrong events, it definitely could.

FRA: If that were to happen, do you foresee the central banks again coming in in a consorted way to save the day? Especially, considering that there’s a concern on pension funds and insurance companies with large holdings of equities and the central banks are not looking forward to bailing them out if there was another financial crisis affecting them.

NOMI PRINS: I don’t think they care so much about pension funds and insurance companies. They care about the financial system as a whole and I do think that the first thing that would happen in the event, this happened in 2016 which showed a precursor to this, is in the event that something catalyzes a very fast day or two fall in the stock market, that central banks do come in and coordinate some sort of policy that boosts them up, but the fact is there is no ideas for them to do that this time simply because they are almost collectively at negative, aside from the Fed. The fed could go down by the point it’s gone up since December 2015 and it could go negative, but there is not much more room to go. It would boost the markets again though if things really fell and the Feds say that they’re going to reinstate quantitative easing in order to stabilize the economy or stabilize the financial system or promote growth or whatever it is they’ll say they’re doing it for. So, then you’ll just have volatility in the markets in that way. You could have a very steep drop followed by the sort of “save the day” efforts on the part of the major central banks and you’ll have an uptick. Then let’s say confidence goes down because there isn’t a lot of room to continue to do that in the same magnitude, then the markets go down again. You can kind of see how that might precipitate a jagged type of bear market with major ups in between when central banks do announce movements, which they would announce to try and save the market. All of this just means that their main function has become to continue to keep these asset bubbles inflated. A couple months ago when the private banks in the US had to give the results of their stress tests, basically stressing their books to the extent of what could happen in certain crises situations, and the Feds said that they all passed with flying colours while having mostly not passed the year before. So, somehow in a year they managed to magically change. They turned around and said that rather than saving extra capital or whatever, we are going to just buy our own stock. That just creates more inflation of these bubbles and that why the financial sector increased by so much more than some of the other sectors because all of a sudden they were given a green light by their own regulatory body, the Federal Reserve, to just use this, effectively 1% or less, money to buy their own stock and to pay themselves dividends that amount to two more than that – Effectively using the Fed’s policy to freely inflate their own stock by paying themselves dividends on their own stock that they bought. It’s kind of market manipulation if you think about it, but it’s legal because the regulatory body that is supposed to control this sort of thing green-lighted it.

FRA: So when does this all end? You mentioned ongoing emergency procedure spells an eventual recipe for disaster if you think about growing levels of central bank assets, you mentioned 14 trillion, and given the coming even much higher numbers on unfunded liabilities that may need to have central banks monetize further debt by governments, but is the end point limited by perhaps the interest rate? Or if you sort of look at it as a lever between debt and interest rates for servicing debt, is the end point involving interest rates?

NOMI PRINS: At some point, what’s going to happen is the interest rates will continue to remain low and again, I don’t think any of these banks are going to move rates up this year, but when a disaster happens, so not necessarily when rates get raised a smidge although that certainly does push that lever when the fact the Feds have moved rates by even just 1%, has created some more instability in terms of defaults and international corporate defaults and so forth because you have companies that have been mostly funded through US banks and other major private banks in dollars. They have multinational operations and have to repay them in dollars, but their currency isn’t worth as much, and the interest rates go up again for them so they lose twice, and they’re not growing as fast so don’t have as much profit to cover it. So that stuff is happening throughout the world organically. The lever is really when those numbers start to tip, but I don’t know when that is. I used to try and find the end point, such as when the European central bank actually stops using their quantitative easing program and then they get to the date where it’s going to stop and then they extend it. They have this ongoing elasticity in terms of their policy, but what will happen besides monetary policy in central banks is that the sheer development and growth of companies that are highly, highly leveraged relative to even how they were before the financial crisis, just simply aren’t making enough money to cover even the minutest of interest rate payments on their debts. That’s when stuff starts to collapse, not necessarily if they’re raised, although that would certainly hasten it and that’s why it’s kind of stopping right now, but when they’re actually simply not growing enough organically to make their own payments. And there’s a lot of that happening. For example the son-in-law of the president of the United States, Jared Kushner, he’s a real estate person; his major building 666 Fifth Avenue in New York City is completely overleveraged and it’s occupancy rates continue to become lower, which means he can’t pay for even the debt he has with the people who are supposed to be renting out space in his building – That’s an organic problem. On one hand it’s because you’ve taken out too much debt, on the other hand it’s because people won’t pay you for the provision, space, service or whatever because they don’t have the money or want to spend that. That’s when things start to collapse from an organic perspective, unless again we have a major war or a major sect or something like that happens more acutely and will more quickly create some sort of collapse.

FRA: But not really in terms of the time frame?

NOMI PRINS: Well if we go back into discussing negativities with North Korea, if the defaults have been increasing in the various sectors throughout the world continue to increase at a more rapid rate – You could see a crisis happening within the next year even though you’ll have the cavalry of central banks attempting to double-down or triple-down on what they’ve done simply because there will at that point be nothing on the gross side at all to enable companies, particularly small-medium sized companies that hire a lot of people, to pay off their debts. And if they don’t hire people they have to fire people. If they fire people and they aren’t paying people, people can’t buy stuff. If people can’t buy stuff, it all goes down very quickly and becomes a very quick spiral. You’re starting to see that. You’re starting to see defaults in various sectors and if that continues it could spiral down within the next year and that would happen naturally.

FRA: That’s great insight Nomi. How can our listeners learn more about your work and also when is your new book, “Collusion”, coming out?

NOMI PRINS: Collusion is slated to come out on May 1st of 2018 and in terms of anyone who wants to read more of my books or any of my writings I do have online or just in general, you can come to my website which is just my name, NomiPrins.com, and just check it out.

FRA: Great – Thank you very much Nomi.

NOMI PRINS: Thank you so much Richard.

Transcript by: Daniel Valentin <daniel.valentin@ryerson.ca>