09/11/2017 - The Roundtable Insight: Alasdair Macleod And Jayant Bhandari On The Rising Synergistic Asian And European Economies

09/11/2017 - The Roundtable Insight: Alasdair Macleod And Jayant Bhandari On The Rising Synergistic Asian And European EconomiesFRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Alasdair Macleod and Jayant Bhandari. Alasdair is head of research for GoldMoney and an Austrian economist. He has a background as a stockbroker, banker and fund manager. Jayant is constantly traveling the world looking for investment opportunities, particularly in the natural resources sector. He advises institutional investors about his findings. He worked prior 6 years with U.S. Global Investors in Texas, a boutique natural resource investment firm, and also for one year with Casey Research. He also is a follower of the Austrian School of Economics. Welcome, gentlemen.

Alasdair Macleod: Thank you for having us.

Jayant Bhandari: Thank you very much, Richard.

FRA: Great, today I thought we’d do a discussion on currencies, commodities, cryptocurrencies, what’s happening there. An update from India, and also just what monetary policies are doing by the major central banks, some recent writings by Alasdair in that regard. So to kick things off, just wondering Jayant if you want to give an update, we were just talking about the recent announcement by the Reserve Bank of India?

Jayant Bhandari: Richard, a very funny thing came out a few days back by the Reserve Bank of India. Firstly, the reality is that in this electronic age, when you have deposited all the money into the banking system the government should have released the effect of the demonetization very soon after the end of December 2016. And I’m talking about the demonetization process that has started in November 2016. Now a few days back they came out with a new saying that 99% of the demonetized currency had been deposited with the bank by the end of March 2017 which basically means that more than 100% of the money in circulation was actually deposited. Which basically if you try to understand what this means is, not only legal tender was deposited, the counterfeit currency in circulation also ended up getting deposited with the banking system. So not only did the banking system of India completely failed to stop corruption or black money, they actually converted counterfeit currency into legal currency. Now also if you read the recent news releases, they have also come out with the latest survey reports, which now tell you that the economic growth has fallen to 5.7% which is now much lower than that of China. And it clearly shows that the Indian economy is now starting to stagnate. In my view, it was stagnating 6 months back and it’s actually regressing in my view. Two more things before I go complete my response here Richard. Most of the growth can be attributed to destruction of the informal economy and transfer of that economy to the formal economy. Which in real terms means that they are destroying the economy, not improving the economy. Also, a huge amount of GDP increase is a result of massive increase in government spending. Which is of course as you and I know is not sustainable and it’s actually not helpful to the economy or to the society. So there are constantly negative news coming out of India right now.

FRA: Your thoughts Alasdair?

Alasdair Macleod: Well I find that fascinating. It doesn’t surprise me, before we came on we were just sort of remembering last time we spoke about this, and I think you Richard agreed this is going to be economically destructive. Yet the Reserve Bank of India count money has been sorted, which means that there’s got to be some money that which money in there. And the economic growth figures has been fiddled with. There is no way that you can destroy the money and then expect a growth of any sort to occur because economic growth or contraction is purely a reflection of the money SKIP Economic growth simply collapses. It seems to me that what’s happened is that the figures have been filled one way or another, as Jayant suggests, to come up with something that looks reasonable in the circumstances. I wouldn’t believe for a moment that there’s been economic growth of 5.7%. I don’t actually hold any SKIP. Is completely meaningless, because you can’t get at what is going on in the economy, whether it’s progressing or not. I would say that that figure is completely false and anyway pretty meaningless.

FRA: Jayant, what has been the effect on the currency? The exchange rate and purchasing power and inflation/deflation?

Jayant Bhandari: So food prices in the country have now started to rise. So if you remember, Richard, when we talked initially soon after demonetization, I was telling you that food prices had fallen drastically. Food prices were down about 50% or so. That seems like good information to most people, but the reality is that food prices fell so much because poor people were unable to feed themselves. Hundreds of millions of people had lost their jobs, and they had no option but to reduce the food consumption. Now that also meant that farmers could not really make money, and they did not sow properly for the next season which now means that food prices are now increasing across the country. So that is the harm that has been done to the inflation/deflation situation. Deflation happened for the wrong reason and now inflation is happening for the wrong reason in the country.

FRA: And what has been the effect on gold prices in rupee terms locally?

Jayant Bhandari: So Indian currency has surprisingly done very well in the last 7 months. Now, these are all in the short term. I don’t think should pay attention to the currency prices because these changes tend to be noise. And there is another thing that is happening that Western institutional investors continue to be very euphoric about India; the reason why they keep pumping money into the Indian stock market. And as a result of that more Western money keeps flowing into India which has helped the Indian currency. Now another thing that is happening is the situation with gold and Bitcoin. Bitcoin is being bought by Indian states, a lot of people now come to me asking about Bitcoin and a lot of people have increased their consumption of gold. They have also increased the storage of gold in Hong Kong, Dubai, and Singapore. This is what rich Indians are doing, so in my view from what I see, gold consumption has gone up and Bitcoin consumption has gone up in that country as well.

FRA: And you were mentioning earlier about the rise of other metal prices like the base metals over the last year period, can you provide some commentary on that, Jayant?

Jayant Bhandari: Well I mean this is, of course, a good sign in my view that China continues to consume a huge amount of commodities. Which in my view underpins the future of China which is that China continues to grow. And I continue to be very optimistic about China and therefore commodities and I continue to be optimistic about gold, but for the wrong reasons which is that many of the third world countries continue to stagnate and suffer as a consequence of bad policies.

FRA: Alasdair, your thoughts on the rise of base metals and how that relates to the precious metals?

Alasdair Macleod: I think Jayant is absolutely right about China. China if you like, is a mercantilist economy. It’s driven, if you’d like, by policy from the center. And the policy from the center on various 5-year plans, and they’re on the thirteenth 5-year plan now, is basically to create an industrial revolution throughout Asia. At the same time, the spice route spice road projects the OBOR project is beginning to cut down substantially the transcontinental shipment times. There’s an enormous number of trains now going between China and Europe. And we’re now in a position where SKIP can put a brand new car on a train, ship it over to China on that train and have it in a showroom in Beijing in 15 days. That time is going to come down too, around about 10 or 12 days eventually and probably in the not too distant future. And this compares with sea transport times of at least 30 days for the same thing. At the same time, you have companies in Europe like Zanussi Italian white goods manufacturer. They’ve got factories in China and they’re shipping their white goods by rail now in contain raised shipments. And again they’re getting the benefits of their goods coming into Europe within literally almost a fortnight out of the factory. Now, this is very very beneficial and China is in effect driving the economy of the whole of the Europe and Asian continent. It’s becoming particularly visible in the Asian part, it is becoming more visible in the European part. The German economy is going like a train, it really is. Other Eurozone economies are if you’d like, they don’t have the manufacturing porous but nonetheless, they are beginning to recover. And this is really the story I think for the next 2 or 3 years at least as far as Europe is concerned. So when it comes back to base metals, the demand for base metals I don’t think we’ve seen anything yet. There is another aspect of this and that is the currency aspect. What China basically wants to do is to do away with using the dollar as a settlement currency for her trade. And she’s made enormous strides to achieve this end. And there will come a point where she will take a view on her reserves, which total roundabout $3 trillion equivalent, most of it is in dollars and about a trillion of it is invested in T-bills and bonds, treasury bonds and so on. There come to view about that relative to other currencies. And I think we’re on the edge of China reducing her reserves in favour of buying base metals because she needs copper in particular. She’s redoing the whole of her electric metalwork, her grid. Air conditioning is a huge market in China. And the building of these cities, I mean we think these are just castles in the sky, but they’re not. Actually what China is doing by building these cities is she is seeking to rehouse huge numbers of people, up to 200 million people is the plan, where the get redeployed from low-value agriculture and that sort of subsistence existence into these satellite cities where they will be redeployed in manufacturing. You know in all the sort of activities if you’d like that go with the modern economy. The Chinese economy, it is becoming rather like the European economy if you take a 5-year view on it. It’s going to become service driven, you’ve got middle classes and all the rest of it. And middle classes want things like air conditioning, they want electricity that works. And so this is the demand for copper that we’re seeing. And when it comes to all the construction, the railroads the improvements that are going on, the industrialization of the whole of Asia, that’s where things like iron and steel come in. And of course, you have all the other metals. Golds relation to this, well there are two ways of looking at it I think. The first is that the price of base metals, the price of anything energy as well, is a lot more stable over the centuries measured as gold as it is in paper currency. And I think that’s a very important point to bear in mind. So if you see the base metal complex rising in price, then it is likely that that will put an upward stimulus on the price of gold as well measured in paper currencies. And the reason for that is that its paper currencies that are losing their purchasing power, not gold. So that’s the first point. The second point that I would make about gold is that if China is serious about doing away with the dollar, the Yuan as currently constituted is not a satisfactory substitute for the dollar. So what she must do is offer trade partners if you’d like, the ability to settle in something else. And this is where gold comes in. We’re seeing this on the futures exchanges in Shanghai. There’s a Yuan contract already on the futures market for gold, the next contract that’s coming in, and it’ll come in by the end of this year, is a Yuan contract in oil. So what this means is that a country like Iran who exports a lot of oil to China, because Iran doesn’t want to use the dollar and she is restricted very heavily on what she can do with dollars, she doesn’t want anything to do with the dollar, she doesn’t necessarily want to take Yuan. So what she’ll do is through the futures exchanges she’ll cover her shipments, the payments that she expects her shipments to China through the futures market. First of all converting oil into Yuan, and then another futures contract converting Yuan into gold. And this is going to produce I think a demand for gold which will not be satisfied by China indecently, it will be satisfied through the markets, deliveries through the market which will put quite a drain on global gold resources. So this is another way in which China is going to move away from settlements in the dollar and that is to provide the facilities if you’d like as an entrance stage for her trade partners to accept payment in effect in gold by bridging through the futures. Eventually what she has got to do is she’s got to formalize the relationship between the Yuan and gold. And that I think will happen in time, how long is difficult to say. All I can say is that the moment that is done, almost actually the moment that Iran can go and just literally sell oil to China in return for gold by using the mechanism of the futures markets, then this is almost like a financial nuclear attack on the dollar. And I do see the dollar is very very vulnerable to this. The timing on this I think in a sense has been speeded up by the election of Donald Trump, because that’s produced a huge air of uncertainty in international trade relations. America is isolating herself in this. But I think that the Chinese, they will move cautiously but watch North Korea, watch Afghanistan, that’s another thing. Also watch the relationship between China and Russia which is very very close. And I think Russians might have some input as to the timing on when they if you’d like pull the rug out underneath the dollar. So I think we’re living on sort of a cliff edge if you’d like as far as the dollar is concerned and this is a fascinating time. And I think anyone who basically doesn’t hold any gold or silver for that matter which is a geared play on gold in financial terms, I think could find themselves with egg on their faces. So it’s a very interesting time and I would be very positive I think on what’s going on, on base metals and also on gold and all to do with China. China is developing the most amazing economy for the whole of Asia. I think Europe is a major beneficiary, Europe will overheat very quickly on this by the way so there’s got to be a very sharp reversal in monetary policy by the ECB. But guess who’s not in the game at all? And that’s America. America has just isolated herself from the gold game and she’s sitting there thinking what to do about it.

FRA: Jayant, you spend a lot of time in Asia, do you see the same type of dynamics from your perspective as Alasdair has elaborated on?

Jayant Bhandari: I’m certainly extremely bullish on China, I go to China quite often and I have talked with you about this several times Richard. I continue to see good growth taking place in China. And I see whenever I go to villages, towns, and cities in China I see improvements. Sidewalks get constructed, coffee shops come up, the coffee shops get cleaner and more hygienic as time passes by. So China is actually improving consistently as time has gone by. One thing very interesting to add to what Alasdair was talking about is to look at the currency chart, the comparison of the Yuan with the U.S. dollar. Now, two years back people were starting to feel very pessimistic about the Chinese currency, they were thinking China was going to start regressing or stop growing. And Chinese currency actually did continue to fall for about 1.5 years. But then people don’t really talk much about the Chinese currency because since the beginning of this year, Chinese currency has improved massively and has gained back at least half of the losses it has made in the earlier 1.5 years. So this is also a reflection of the fact that Chinese economies actually doing quite well.

FRA: Alasdair, you’ve recently written about the Jackson Hole speeches of Yellen and Draghi, omitting commentary about the burning issues of the day. And you list a few of those, one is the question: why is the ECB injecting 60 billion per month if the great financial crisis is over? In the same writing you also indicate in reference to the Fed normalizing interest rates: will take nominal rates only 1-2% to set off another financial crisis. So how do you see things playing out? Do you see what you just mentioned earlier as putting more pressure on the ECB and the fed?

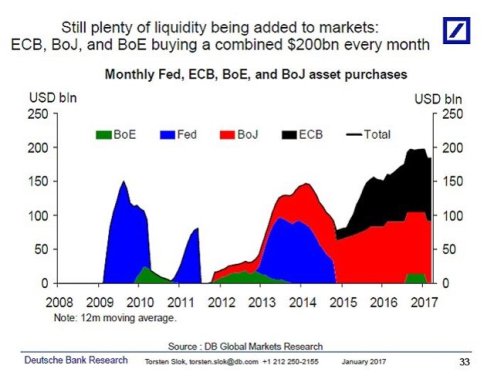

Alasdair Macleod: Yes, I do. I think the importance of the China story is that everybody has got commodities to export, everybody who has territory if you’d like on the Euronation continent is going to benefit from what China is doing. America is not, America doesn’t have any friends really in the trade sense. She’s even turning around under NAFTA and telling Canada and Mexico: “we don’t like this arrangement, we’re going to rejig it”. They’ve already given up on any sort of trans-Atlantic and trans-pacific idea. I mean this is absolutely crazy, America has isolated herself. Where this translates into economic performance is that I view the U.S. economy as still being in a recovery stage from the great financial crisis, and by that I mean the credit cycle. The next phase of the credit cycle is the one of expansion. The expansion of credit, when banks actually start competing to lend to the 80% of the economy, which is the medium size and smaller business. We’re not there yet I think in America, and we probably will never get there because of the trade policies and the isolationism of President Trump. But Europe is a very different thing, Europe is turning around very very quickly. And I noticed in the Jackson Hole speech that Mario Draghi made, he made reference to the time difference in terms of recovery between the Eurozone and America. And he got it completely wrong, he said you’re ahead of us in the recovery. No, Europe is actually ahead of America. Europe is now expanding very rapidly, we’ve yet to see it really I suppose, in normal statistics, but the anecdotal evidence-and if you just watch what’s going on and you just look at the situations. I mean I described the situation for a company like SKIP. There is a major Italian company, whose doing incredibly. Got the most manufacturers, particularly the German manufacturers, I mean this is amazing. And the interest in Europe is actually going to go one further, very soon I think you will find that Germany SKIP for the Eurozone. And what that means is there will be a break with the American lead NATO arrangement. Whereby America says “This is who we’re going to have sanctioned, and everybody is going to fall in with us,” I think this is going to stop. And this is terribly important because SKIP. Mario Draghi and the ECB doesn’t seem to recognize SKIP. Here we are, we got banks who despite money at the ECB, have a negative interest rate of -.4% the interest rate from the ECB is 0% so you’ve got somewhere between negative interest rates and zero rates. They are doing quantitative easing of 60 Billion Euros a month. And they’re still doing this. And in my judgment, in a credit cycle, they have moved from recovery and they’re moving into expansion. Monetary policy in the ECB is completely inappropriate for what’s going on. So I see the big shock, if you’d like, by the end of this year has got to be a complete SKIP fast, by the ECB when it comes to monetary policy. We’re already getting wind of this, the Euro has risen from I don’t know, 1.05 against the dollar it’s now currently knocking at 1.20 to the dollar. And of course you’ve got all the manufacturers in Europe turning around and saying “oh the currency is too expensive, how dare you raise interest rates and make the situation worse” so the ECB’s got itself into this hole, which so often central banks who are behind the curve find themselves. And this is going to be very very difficult for them. First of all, stop QE SKIP. Also, and that is with the dollar declining, eventually she’s going to have to think quite seriously about raising interest rates to avoid a huge great debt problem in the economy. Which really means that over in debated business are going to find that the cost of money starts going against them and they are going to start failing. So it’s an interesting one you go back to the Eurozone, you also got the problem SKIP and the banks are all up to their necks at the moment in government debt. And that government debt is wildly overvalued. It’s overvalued on the basis that the ECB is in there buying relatively scarce bonds pushing down yields. The moment that stops, there are going to be huge great losses on the Italian banks, all the losses that they haven’t dealt with from the financial crisis. So I can see the worst nightmare I think for a central banker is that we move from this sort of this recovery phase, which just rumbles on and rumbles on and rumbles on. They don’t have to raise interest rates, they ignore things like unemployment and inflation sort of stays somewhere around about 2% and you know everybody is happy with that. If you actually get an expansion of credit because things are going like a train or beginning to go like a train, SKIP because I think must hope that we are in a permanent stage of repressed recovery. But I don’t think that’s going to be the case unfortunately with the Eurozone because of the Chinese stimulus across the whole of the Asian continent.

FRA: And so from this, what is your outlook on the Euro, the U.S. dollar, and gold prices?

Alasdair Macleod: Dollar down, gold prices up, Euro up. I think there’s going to come a point where the Euro- I don’t know whether the Euro outpaces gold or not. At the moment gold is outpacing the Euro I mean if you look at gold measured in Euros, it’s only up by about something like 3% something of that this year, it was actually down 2% until fairly recently. So basically to answer your question, I think that gold is going to go up. One thing that really really light a fire under gold I think is when the Chinese come in with the oil to Yuan contract on the futures market. And then you’re going to get Russia, you’re going to get Iran, you’re going to get various of the oil producing Asian countries using that facility to not buy dollars, but to just sell their oil for gold. And I think that’s going to make a huge difference.

FRA: Jayant, your views on ECB policy and Fed policy and your outlook for the currencies and gold?

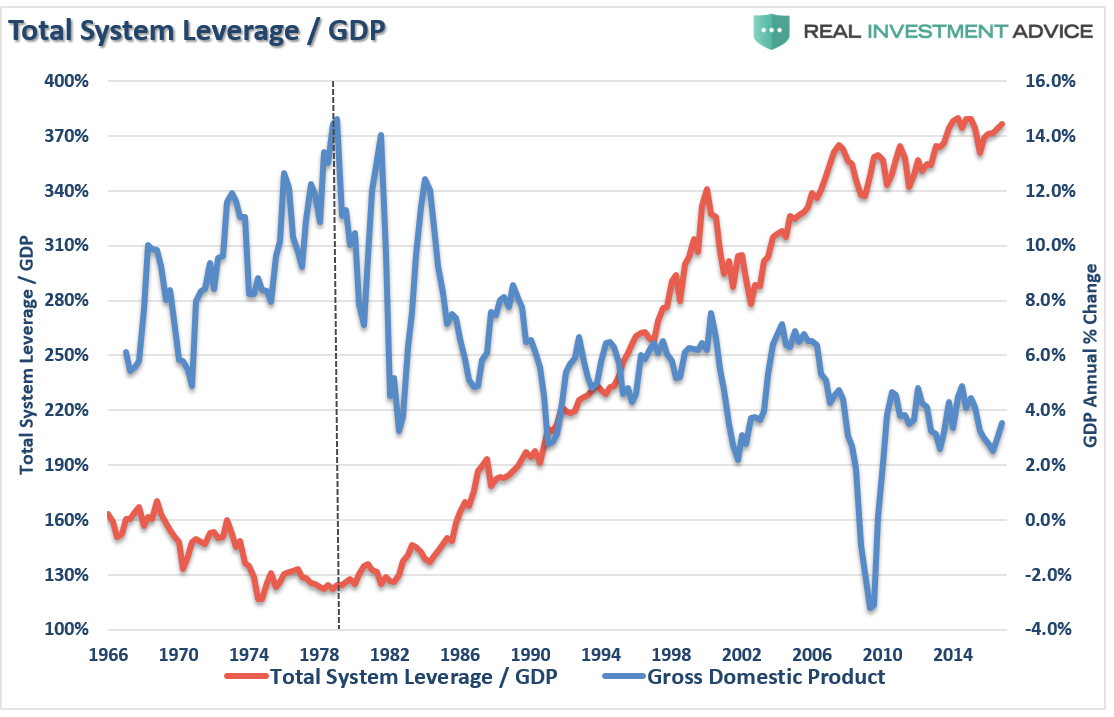

Jayant Bhandari: Well I’m very optimistic about the gold price and virtually every sign tells me that gold is going to go up. Not only the monetary policies but also what I see as stagnation I see happening, economic stagnation in the third world countries, except for China of course. Also, the North Korea situation is very likely to continue to push the gold price up. I might add some comment on Canada, Canada has recently increased the interest rate. And as we know the housing prices have been going up continuously in Vancouver and Toronto. And the Canadian society is hugely in debate, the private debts are huge. So it will be amusing to see what happens if Canada continues to keep the interest rate at what they have now declared or actually increase it going forward.

FRA: Interesting, great insights gentlemen. Just wondering how our listeners can learn more about your work, Alasdair?

Alasdair Macleod: Well, I publish an article every Thursday, around about midday I guess in Eastern Standard Time. You can access it by the website, or the other way to access it is open an account and we’ll send you an email. But basically yeah, I publish an article once a week on the Thursdays. I also do a market report on the Fridays. And what I try and do is look as dispassionately as possible at both what’s going on if you’d like in the futures market, the physical markets, if I have good information. And I don’t rely on charts at all on that. I mean what I will do is I’ll quote charts because other people use charts. But I try to get to the nitty grittiest of what the balances are and you know, where the interest is in market. And that’s quite fun, that’s on Friday, I write that on a Friday before we get the commitment of traders figures so it’s a slight leap in the dark, but anyway those are my two things, regular contributions if you’d like.

FRA: Great, and Jayant?

Jayant Bhandari: Everything I do, Richard, is on my website http://jayantbhandari.com/

FRA: Great, thank you very much. We’ll do another session again, thank you, guys.

Alasdair Macleod: Thank you.

Jayant Bhandari: Thank you very much for the opportunity, Richard.

Transcript written by Jake Dougherty <Jdougherty@ryerson.ca>