01/26/2018 - The Roundtable Insight: Chris Whalen, Yra Harris & Peter Boockvar On 2018 Trends & The Return Of Volatility

01/26/2018 - The Roundtable Insight: Chris Whalen, Yra Harris & Peter Boockvar On 2018 Trends & The Return Of VolatilityDOWNLOAD THE PODCAST IN MP3 HERE

FRA: Hi. Welcome to FRA’s Roundtable Insight .. Today we have Yra Harris, Peter Boockvar and a first time guest, Chris Whalen. Yra is an independent trader, a successful hedge fund manager; global macro consultant trading foreign currencies, bonds commodities in equities for over 40 years. He was also CME director from 1997 to 2003. And Peter is the Chief Investment Officer for the Bleakley Financial Group and Advisory at Bleakley and he has a newsletter product called The Boock Report. BoockReport.com. It offers great macroeconomic insight and perspective with lots of updates on economic indicators. Chris Whalen is an investment banker, author and Chairman of Whalen Global Advisors LLC which focuses on financial services, mortgage finance and technology sectors. He was a Co-founder and Principal of Institutional Risk Analytics from 2003-2013. He has held positions in organizations such as the House Republican Conference Committee…

Christopher Whalen: Yeah, talking about that.. (laughs). That’s okay. Most recently I ran and built up the Financial Institutions Group at Kroll Bond Rating Agency which was a lot of fun. Kroll is really an ABS house, first and foremost, commercial real estate and the rest of it. It’s still very small from competing with giants, but it was a lot of fun.

FRA: Great. And also he was on the board of directors for the Global Interdependence Center (GIC) in Philadelphia.

Christopher Whalen: Yes, that was David Kotok’s little project. You know it’s fun to mix business with pleasure. Fishing, central bankers go fishing.

FRA: Yes, I am actually going next month to the GIC conference in Buenos Aires and going fishing before that. There’s also fishing afterwards, sort of the Camp Kotok in Argentina.

Christopher Whalen: Well, some of them go to Maine. Ramiro Lopez Larroy and his kids will just show which is about 15 hours by plane. It’s a lot of fun. They are great people – A very diverse group at GIC. We’re going to Germany this year, the Bundesbank, so if you like monetary policy that would be a very good trip to go on. I would recommend that.

So, what would you like to talk about this morning?

Peter Boockvar: The Bundesbank has disappointed me for the last few years how they give Draghi the license to do what he has done.

Christopher Whalen: Well, they kind of had no choice. I find it amusing that northern Europe is cranking, and my relatives in Holland are having a great year, and yet southern Europe is not. That dichotomy is ultimately going to be very difficult for them to deal with. The Germans look at southern Europe and they just see more checks to be written. The politics of that is slowly undermining Merkel. It’s very interesting to watch. And then Berlusconi coming back in Italy – Isn’t that great?

Everyone: (laughs)

Christopher Whalen: I always tell people to read about Berlusconi and you’ll see where America is headed.

Yra Harris: Draghi will be making trips to Italy.

Christopher Whalen: Yeah. Draghi has been trying to keep Europe on ice by pushing debt cost down to zero, but the debt keeps growing. So, what are we really about here? There’s no fiscal discipline anywhere in the Western world and the Chinese don’t care. It doesn’t matter in China – It’s a political issue. That’s why I was writing about H&A recently because ultimately, whether that company survives or not, will be determined by uncle Xi. That’s how it works in China. There is no church and state, there is just the state.

Peter Boockvar: He may want to set an example though.

Christopher Whalen: Yeah, there were a little ostentatious, a little floppy with the parties, pasting their names on the side of office buildings around the world. I think we have 3 of them in New York. It’s quite fascinating.

FRA: A few weeks ago, Chris, you wrote an article, Bank Earnings & Volatility, I thought we could begin with some thoughts there. How have the Federal Reserve and other central banks’ actions affected the credit market, the financial markets and the economy, in general?

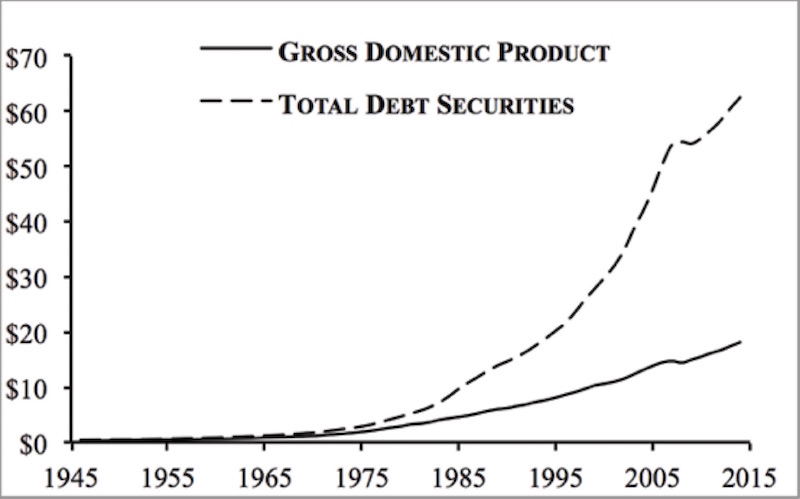

Christopher Whalen: Well, what the central banks have done is that they have removed a lot of assets from the market. They’ve gone out with a variety of new money, in the U.S. case: excess bank reserves, and they’ve bought treasury bonds and they’re bought also mortgage bonds. Of recent vintage, Fannie Mae, Freddie Mac, Ginne Mae paper which have 3, 3 ¼ and 3 ½ coupons with very low pre-payment rates. Those bonds are going to be around for a long time. In fact, one thing I remind people of is that about 30% of the market today is the FHA and Ginnie Mae and those loans are assumable so they will stay with the house. And the house will trade and the loan will be conveyed to the new buyer. It could be very interesting, over time, to see how that affects the portfolio. But essentially, the central banks have taken all of this duration out of the market and since they’re end investors, they are basically buying the paper on credit and they don’t hedge it. So the capital markets activity that you used to see around a lot of these positions when they were held by trading firms, banks and other who were going to trade the assets and cared about mark-to-market every quarter has greatly diminished — There’s no hedging. The Fed’s sought out hedging it’s block and it’s a problem now because the Fed is now illiquid. They can’t sell without creating a loss and they dare not do that because it gets them in trouble with the Republicans and the House who don’t understand monetary policy at all, but have a lot of opinions on it. And so you have this weird situation where the Fed essentially has their hands tied. They’re going to wait for the book to run off which they hope is about $20 billion a month. And I think that they could be wrong. I think that they could too wishful in terms of the runoff rate in terms of the mortgage paper. The mortgage companies are going to be around forever and the pre-payment rate is going to be very low, especially if rates continue to move up. That’s kind of what I see. The trading line on Wall Street, the earning will be greatly diminished by this. Then you have the vote to rule. So all of the books, the investment books that the banks use to trade every day, just the value of the assets are passive now. You put those 2 data points together and you will understand why Goldman Sachs and why all of the banks have seen an enormous reduction in their trading buy-ins.

The other issue is that the mortgage market is down so there is less hedging. The forward market for hedges, what’s called the TBA market, has a lot less activity. We’ll do a $1.5 trillion in mortgages this year which is down. The peak was $4.5 trillion during the 2000’s; we don’t want to do that.

Peter Boockvar: Yes and why aren’t we seeing an CNI loan growth?

Christopher Whalen: The banks had to slow down. They had a pretty good run in 2015/2016. We had a little scare from oil which didn’t really materialize. Most U.S. banks did fine on oil credits. There was some restructuring, but the banks we follow like Cadence, which is a small lender that was built to do energy – They have no problems. But now a lot of banks have run up to a regulatory limit on commercial real estate loans, multi-family…there’s a big shtick now for the smaller banks. They’ve essentially run out of customers in certain markets too. The OCC, for example, is forcing regionals to peel back their multi-family exposure because the prices have gone up so much. They just look at that go whoa, wait a minute. And they’re right. Loss rate on these assets, multi-family assets, are negative. So if the loan defaults, you’re going to sell the property for a lot more than the loan and that’s reflected in the ABS numbers too. It’s an interesting time in terms of different asset classes, but I don’t see a lot of growth in the book. I really don’t. BA had a really good quarter at year end, but that was the exception. Most of the big guys were not growing. And of course PMC had a very good quarter and had a nice tax number. I think overall, don’t look for alpha in the banking industry. Between the regulatory changes and just the tenure of the economy you would be in the bond market, right? Anybody could raise money in the bond market in 2016 and part of 2017. So, we had a bull market in fixed income which has driven a lot of strategies and I’m sure Yra has some thoughts on that.

Yra Harris: Let me ask a question in regards to that. I was really taken by it because it was such a good point. With the ECB, BoJ and certainly the Feds, the dynamic hedges are missing from the market, but they are going to resurrect themselves as more paper winds up in the hands of private holdings whether it be by pension funds or insurance companies. But do you think that Jerome Powell…You know I go back and read some of his earlier stuff and of course his initial position as a Fed governor, he had a lot of issues with the massive build-up of the balance sheet. Do you think that he might be quicker to say that we can hold the rate at 2%…Do you think that it’s a possibility?

Christopher Whalen: I think that the snippets from the minutes that have sudden found people’s attention…which is very funny, right? We only pay attention to chairmen. It’s a cult of personality. So here you have Powell saying some very interesting things, very forthright, not an economist, he’s a financial guy, and I’m told he’s fairly decisive although he’s quiet and he listens. He knows how to make decisions. On this he’s got politics because the congress, if you remember years ago, they confiscated the Fed’s surplus to pay for a highway bill. And the idiots in congress, I wrote about this for the American Conservative, keep permittences from the Fed as revenue. They don’t understand that it’s an expense foregone. It’s not revenue. You’re just making the debt go away. Every year they look at this money coming in and the CBO and everyone else say: Oh look, it’s revenue. But it’s a snake eating its tail because the Fed and the treasury are one. It’s like a Hindu god, but in economic terms they are the same. And Bob Eisenbeis, who I interviewed, is wonderful on this issue – He is very funny. I think that Powell is going to be a lot more straight-talking then the others have been and I fault Yellen and Bernanke on this because they should’ve gone out and said to the congress: “No, you can behave like this. This is ridiculous. You don’t go confiscating our surplus.” It was just part of Washington politics, but the Fed didn’t respond. If Paul Volcker was there he would have been up on the hill kicking the shit out of them. And the problem is, these are bureaucrats, they come from academia. They have no money and so they don’t know how to behave in big league politics – It’s a tragedy. I think Powell will be much better. I am very hopeful about his 10-year as chairman. It desperately needed change. We got to get the economists out of the temple, I’m sorry. I love them, but they can’t make financial decisions. You want them on the staff, Yra, you don’t want them trading.

Peter Boockvar: We wish that was the case 10 years ago and now Powell gets to clean up the mess.

Christopher Whalen: Exactly and you know, Volcker cleaned up a lot of messes too. They always clean up other peoples’ messes so it’s a public service.

Peter Boockvar: And this is the biggest mess the world has ever seen.

Christopher Whalen: Oh yeah. No question.

Yra Harris: And with Bernanke he had the courage not to act.

Peter Boockvar: Right. Bailing out people doesn’t take courage. It’s not bailing them out what is courageous.

Christopher Whalen: Well precisely. And the Fed has not said no in a long time. They haven’t said no to accommodating treasury options and they haven’t said no most recently with this lunacy of QE. I mean the first one was fine. They had to reliquify the banking system as Walker Todd put it out to me a while back, but the rest of it was crazy. Selling all the short-dated stuff and loading up the book with long-dated treasuries so they own mortgage backs with an average life of around 12 years now. They have extended a lot, by the way, over the last 18 months. Even if the portfolio gets smaller, the duration has got to go up.

(laughs) How about that?

Peter Boockvar: Chris, what was their thinking in their models with operation twist to say okay, in their models, let’s flatten yield curve and that will be good for growth. And then today they express worries over the flattening yield curve.

Christopher Whalen: Well I know, but this is the point. When you have central banks take all this duration out of the market, nobody is hedging the position; well obviously it’s going to be hard to get those maturities to back up. There is just nobody selling euro/dollars, nobody doing swaps or anything – There’s nothing. So there is market is in stasis and they’re going to push up the short end, but there’s nobody pushing up the long end. So it’s gone up a bit, but I keep wondering…I wrote about it this week. I’m kind of hedged on my bull market 10-year trade, right? But, there is still nobody out there selling it. So I do think you have a flat curve in prospect, I agree. It’s bond market basics. It’s got to be somebody at that table in Washington who understands the bond market and I think Powell does – There’s hope.

Yra Harris: But in understanding the bond market, Chris, do you think that he will move to try and steepen the curve by maybe holding the front end, by saying hey, we don’t have to raise rates. If I get it to 1.75 on the Feds’ fund rate or 2%, I’m basically in a neutral real yield. That’s where I am. That’s probably about neutral on the front end. Maybe the real yield on the front end goes to 50 basis points positive, but I don’t think he goes there. Would it not be in his optimal mindset to say let’s start shrinking the, as Peter would say, quantitative tightening on the longer end on the duration. If the yield curve steepens out to 120-150 basis points it’s not necessarily a bad thing.

Christopher Whalen: I totally agree with you. If the Fed were acting rationally they would be doing all of that. They would have even been hedging a bit of the buck. Just trade it. Go out and hedge on the duration.

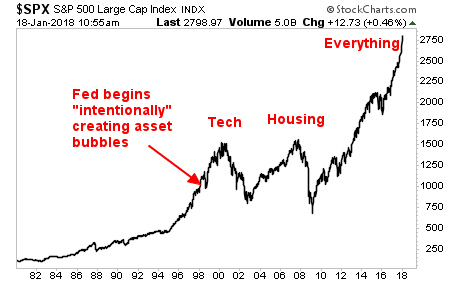

Peter Boockvar: Definitely afraid of affecting its bubbling asset prices.

Christopher Whalen: That’s part of it – True.

Peter Boockvar: That’s behind their entire thinking.

Christopher Whalen: But bureaucratically in Washington terms, they don’t want to take a loss because then the remittance to treasury goes away. And believe it or not, in the small minded world of some of these Fed people, that’s what they worry about. So, vector that into your thinking too because he’s absolutely right – They should be trading the book. They should have been doing a lot of things, but they’re not thinking like market people. They are thinking like Keynesian and academic economists and that’s scary — It really is.

FRA: In your article you mention also that this is likely going to result in a volatility returning to the markets that were all short volatility – Can you elaborate on that?

Christopher Whalen: Well that was the comment from Powell. He said at the end of that snippet from 2012 that they were going to unwind their short volatility position. In classical terms, if you buy a portfolio of RMBS it should give you a relatively short position, but in this case I think the other part of it is our perspective, the market. We’re sitting here and he’s got all the duration and we’re buying. Now, all of a sudden, he says that we aren’t going to buy anymore and we’re going to let it run off. So eventually private market participants are going to take up that duration, think of it as the weight that they have to support with capital, and they’ll have to hedge. So you will see market activity return. I think that the Fed has missed an opportunity to get a little bit more of this done quickly and figure out how much the street is willing to support. That’s the thing that we don’t know. The Fed has been supporting everything.

Peter Boockvar: The Fed lost their opportunity. The Fed had a chance to raise 3 times in 2015, 3 times in 2016, now they’re entering a situation where maybe the Fed fund rate tops out at 2-2 ¼. And they have now an issue with this falling dollar and bubbling inflation pressures. Just imagine when we do hit a wall and they start to cut rates and what the dollar is going to do in that scenario.

Christopher Whalen: I think it’s a lot simpler than you put forward which is: go ahead and keep your little quarter point march and if you see spreads start to widen, you stop. It’s the basic Irving Fisher test, right? That was the playbook for Bernanke.

Peter Boockvar: That is too much of a free lunch for me. I think that there is no free lunch in reversing this policy that they have implemented.

Christopher Whalen: So, you think we go to 6%? That’s what Yellen said years ago.

Peter Boockvar: We don’t need to go to 6% to cause a major problem. All the 10-year has to do is go to 3.5%/4% and you’ve got, I believe, a recession on your hands. I think the sensitivity to changes in interest rates is dramatic, as it’s been. You’ve got duration levels that are as high as they’ve ever been globally – That’s where the risk is.

Christopher Whalen: Well you’ll certainly see defaults go up because we’re hiding a lot of defaults with the artificial manipulation.

Peter Boockvar: And it’s not just that. Well you need a zero interest rate to go back to zero and $9 trillion of paper is going to lose a lot of money mark-to-market

Christopher Whalen: Hey, I know that’s why…

Peter Boockvar: Actually, I take that back. It’s more than mark-to-market — It’s real life losses.

Yra Harris: From a trader’s point of view…That position is enormous that they are carrying and more people have synthetically created that. Now you’ve got to realize that all of this volatility selling is all from people who are mimicking that risk parity trick. You can mimic it whatever way…You can recreate this trade synthetically in a million different ways. So when you have to actually start unwinding it, it’s almost like the long-term capital of 1998, we’re not going to be able to get out of that door because a lot of people are going to be racing out that door at the exact same time that you want to go because they have the same position whether you realize it or not.

Christopher Whalen: Well of course. And the VIX is just a popularity contest – There’s no basis for that contract. It’s just a matter of supply and demand. It’s like CDS. There is no basis on the underlying credit anymore.

Peter Boockvar: Well sure, but the VIX is still being determined by a lot of participants placing their bets and puts and calls.

Christopher Whalen: Absolutely. A lot of them weren’t hedging the past few years. Everyone was leaning in one direction.

Peter Boockvar: Of course.

Christopher Whalen: You would see default rates double in Peter’s scenario, easily. I think that’s from latency in the system. If we see the 10-year go up to like 3%, I think the windows will be shaking.

Peter Boockvar: And I read a stat over the weekend that of the roughly 2,000 companies, 40% of the debt is floating rate. And that cost goes up every single day with what LIBOR is doing. Even the 2-year note yield today is up to 2.12.

Christopher Whalen: That’s what I’ve been wondering about is to imagine the reissuance of equity that was bought in by these guys as they desperately try and pay off this debt. That could be a lot of fun.

Peter Boockvar: Yeah. The 1-year bill today is now where the S&P 500 is.

Christopher Whalen: We’ve had 4 years of amazing record bond market activity of each year in terms of new issuance and I would say 1/3 or ½ of it was to fund stock repurchases. It’s been quite something.

Yra Harris: And you know what, there’s another part…When the BoJ and ECB are busy buying corporate assets, there’s no hedging that goes on there either. And there’s also no stock re-lending. Another issue that I’ve raised…

Christopher Whalen: Yeah, that’s true. They may not lend the assets. That’s right. The Asian central banks are very, very conservative on that stuff. They won’t re-hypop.

Yra Harris: Yeah. There’s no rehypothecation of anything so now all of a sudden the game gets even more interesting and the question becomes: Do all the ETFs rehypothecate? Or does that result then with everything in that basket we get way late off the market and make it even more expensive for short sellers. So we’re not getting any short selling for some of these companies that are involved in ETFs are really miserable companies. So the whole dynamic here is shifted. And I don’t know that the players have really shifted.

Christopher Whalen: I don’t know about the ETFs. I would suspect those assets are available, but the central banks are the big thing. When they buy all of this paper and just put it away, you’re right, it doesn’t come out. It doesn’t get loaned. It reduces liquidity – That is, to me, the key thing.

The fascinating part is to look at the Swiss. Swiss National Bank is now buying stocks. Why? Because if they don’t, the currency will appreciate. That is their chronic problem. They just can’t keep the money out and even with penalty rates, they still can’t manage it. So if they stop, it will go up.

Peter Boockvar: That’s what one of the interesting central bank comments this week was from the deputy governor of the Swiss bank in Sweden, who has also gone down that rat hole of negative interest rates, and she said that they are not going to wait for the ECB to start raising rates. They’re going to probably start doing it this year. So I think that there is an end in sight to this negative interest rate experience over the next 2 years.

Christopher Whalen: Well, the whole system has way too much debt and a lot of debt that is mispriced. So like I said, you’ll see the banks start to lean into this too. I think you’ll see provisions gently go up from where they are. I was surprised to see the credit cards up this much this quarter.

The mortgages are still real quiet. And commercial is still really quiet because the collateral values have gone up so much. A loan you made 2 or 3 years ago, the building will get sold easily for the principle on the loan which is typically a 50 LTV (loan-to-value) loan. Look at the equity that has been created in multi-family and commercial real estate over the past 4 or 5 years – It’s ridiculous. And it was all levered up again.

Look at New York. New York is going to be a lot of fun. We have compression underway right now.

Yra Harris: Will the balance bring back foreign buyers to the U.S. market to hold this mark up a little longer?

Christopher Whalen: I don’t know. I’ve been trying to get some good data on that because it depends on a lot of things. There was certainly a gold rush for a while, but then the Chinese shut the door. They changed the rules rather significantly. That’s what H&A is about. I think that for Europeans too, things have calmed down a bit so you don’t have that crazy flight capital that we saw in New York in 2015 and 2016. But the bid for high-end condos, that foreign big is definitely waned. I know a couple of brokers who just do that market and there’s a lot of stuff for sale.

Peter Boockvar: There are a lot of signs that commercial real estate has peaked out in this cycle.

Christopher Whalen: Oh yeah — Definitely. But you know a lot of markets are completely on fire, just look at Denver, downtown Denver…

Peter Boockvar: Yeah, with certain demographics.

Christopher Whalen: Yeah and they’re leasing them.

Peter Boockvar: A lot of population growth.

Christopher Whalen: Yes. That city has exploded. The city has almost reached the airport. And for those of us who remembered when the airport opened, it was really far away.

Peter Boockvar: Yeah, I was at that airport 2 weekends ago.

Christopher Whalen: Yeah, and now (highway) 70 has expanded to the airport. It’s about a 40 minute run. That whole area with Colorado Springs and everything else has just completed exploded in terms of development.

Yra Harris: When they built that airport I said: Why are they taking away the old stable that said, “Stupid”. What vision I had.

Christopher Whalen: Now people are going to start expanding east away from the airport. That’s already happening.

Yra Harris: Wow. It will be in Nebraska.

Christopher Whalen: Exactly. But anyway, markets are going to be very interesting. I think that the fact that the dollar has been trading off the way that it has been is going to make for a very interesting year…

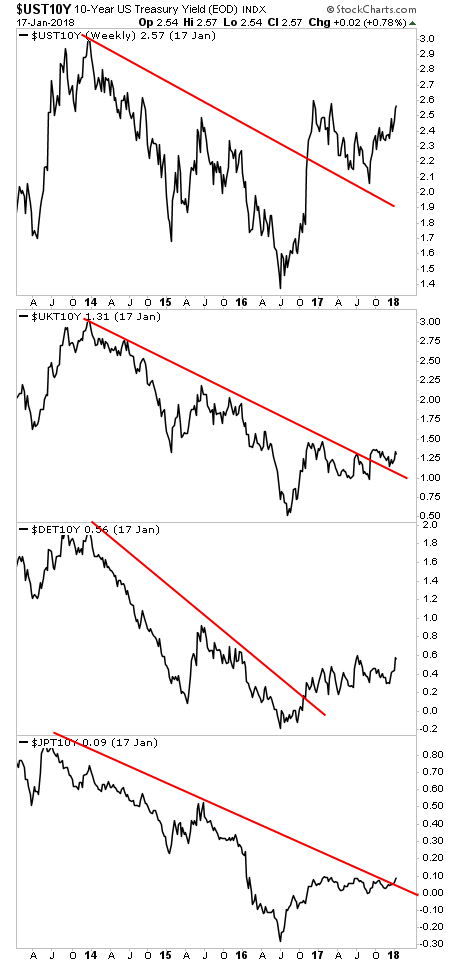

Peter Boockvar: And what we’re seeing in front of our eyes is the air leaking out of the bond bubble. Whether it’s here, whether it’s in Europe with the German 10-year breaking out above this multi-year range. I don’t necessarily know the pace of it from here, but things are changing before our eyes with interest and currencies. If there was going to be a major risk to this whole tranquil environment that it’s perceived to be, it’s the rise in interest rates and certainly a big draw down in the U.S. dollar. I mean commodity prices are at multi-year highs, the CRB printing 200 yesterday and holding them today. I think things are changing and there’s still a lot of nonchalance in the face of that.

Christopher Whalen: Of course. Markets sometime just sort of trade around numbers for a while for no particular reason and then you have an event that wakes everybody up and it moves, like the election. If you look at most charts for the bond market, there’s this big discontinuity around November 2016 and what do you do? Now it’s moved. And it moved again for a variety of reasons. China used to be the excuse, but I don’t think we’ll have that now. It will be a fairly boring inward look at China.

FRA: Chris, on your article you mentioned there could be downward pressure on long-term bond yields as the U.S. treasury concentrates future debt issuance on the short-term majorities.

Christopher Whalen: Yeah, that the schedule. And again, going back to our earlier conversation, you’re the Fed and you see treasury in the market with huge issuance. I can put a lot of pressure on short rates such that they may blow past the targets and keep going. Imagine that. Meanwhile the Fed isn’t going to sell anything outright and they’re not doing anything on the long end. They should be selling the futures at least. You don’t want to sell the cash positions? Fine, but do something because otherwise we’ll flatten just like Peter said. I totally agree with that. And it may happen quickly. It could happen in weeks – Imagine that (laughs).

Peter Boockvar: I still expect a creep higher in long rates.

Christopher Whalen: Yeah, it will bounce up, but it could easily rally. You want to be careful because there is so little paper. If they reopen the old issues which they can do, then you’ll know that somebody is yelling in that building saying, “Hey! You should be issuing longer dated paper.” The pit was planning to take their runoff and invest in the short end stuff the treasury is issuing, right? But their runoff may be so slow that they might not have that much net cash if they want to keep up with that $20 billion decline in the overall portfolio. So, I think it’s a funny situation. It goes to what Peter was saying. We could have a really nasty market environment because the Fed can’t help, the banks can’t help, they’re not allowed to anymore. So the street has no strong hands here that come in and push out a bad auction or push on the dollar if it gets messy. They would just have to intervene.

Yra Harris: And if they were to actually start…If Powell says, “I want to sell off…” to go back to your first point Chris, is that they are going to incur losses. And then they’re going to say, “Hey, we’ve got losses on our books this year because we’re actually taking some losses on the long end stuff that we bought.” So they’re kind of locked in that situation. And the situation on the front end has gotten so interesting that I actually called someone at the CME and said that I think it’s time for them to dust off the old contract and bring it back because it may become useful besides with the euro/dollar.

Christopher Whalen: Well no, this is the thing, the Fed economists in Washington were bragging about the fact that they made money on QE and they don’t understand. To your point though, Yra, what Powell has to do is get up and say, “We’re going to be selling some bits of the portfolio to help accommodate the treasury’s issuance and to rebalance because it’s far too long.” And they can do that in a variety of ways, but then he’s got to look at them square in the eye and say, “By the way, this going to reduce remittances for years.” They have a little account called the negative asset; they came up with it, where they put the losses. The congress capped the Fed’s capital at $40 billion when they confiscated the surplus for highways. So this is the situation you have and they don’t want to be insolvent. If there’s a big number in this contra account and they have $40 billion in equity, people can do the math. That’s the politics of this. It’s very strange. You got to realize that they are central bankers, they are very funny and it’s a big factor.

So, if Powell will change that? That’s a big deal.

Peter Boockvar: I think also a key factor is how much control these central banks can have over their external environment. I am of the belief that markets are going to force their hands. I still believe that cyclical inflation pressures are going to force their hands whether it’s commodity prices, wages or supply chains. I read an article yesterday on the front of the Wall Street Journal on how it’s almost impossible to find a truck to deliver your goods and people are paying hand-over-fist to just try and find drivers. I don’t think it’s necessarily fully in their hands. I mean Powell is going to have to start watching the German 10-year yield every day. Behind the scenes, obviously, a liquidity flow is turning into more of a drip and that all of these central bankers have to look at each other because what one does is really going to influence what the others do both on the upside and downside. When you think about this rise in interest rates, as some of these banks start raising, it gives other central banks cover. So, you’re less inclined to keep rates low if other people are doing it on the upside just as we saw the reverse. Peer pressure cut the rates to nothing and it’s going to do the reverse on the upside. I think that also feeds on itself. I am just amazed at people believing that this is going to be a smooth process and historically it never is.

Christopher Whalen: It’s even worse now because they took cash flow out of the system by forcing rates down. Forcing rates down is a debtor-friendly policy. It’s meant to transfer value from savers to debtors. So now, you have more volatility in the system because it’s less cash flow. People also have very little fat. There’s not a lot of embedded savings in the system from carry because your assets don’t throw off that much cash flow. It’s stunning when you look at Bank of America and the gross yield on their book is 4% — They’re not making money. The whole industry has got a negative risk-adjusted return because the return on assets is so low. In fact, I think that the number for the industry now if 0.75% on earning assets across the board. It used to be over 1.00%. And so the central banks by constantly forcing rates down, they’re taking carry out of the system and it’s not good – It’s deflationary, ultimately.

But I looked at the debt thing, Peter, and I totally agree on it. I’m going to have a lot of fun watching this. I was doing comments today for one of the regulators on whether or not they should allow different credit scores for underwriting loans – What do you guys think? Do you think that’s a good idea to have more than one way of measuring something like that?

Peter Boockvar: It makes sense.

Yra Harris: Yes, it would. I think the whole cycle from a private perspective, you know having my kids go through this stuff, and honestly it’s ridiculous. It’s truly ridiculous in the way that they measure it and they hold everyone accountable to the same standard. I know, it made the banks comfortable with time and there was a need for it, but if I ran a small community bank I would never do business like that. And I know they saddle with them. That’s not how you properly do business.

Christopher Whalen: Well, that’s what I’m telling them Yra. Like you said, the government shouldn’t be in the business of picking one. You let the people who underwrite loans figure this out and then the markets are going to tell them whether they like it or not because they’ll price the pools accordingly. So, I think we can figure this out real fast.

FRA: Just as a final question if you can go around to give your thoughts on where central bank: monetary policy and government fiscal policy is going this year in 2018.

Your thoughts, Chris?

Christopher Whalen: Well, for monetary policy I think that they are going to try and stay on the program as far as rate increases. But you get the 10-year stuck and it keeps moving Fed funds up – You’ll have a flat curve. And I think they’ll have to stop at that point.

Fiscal side: I don’t see any inclination of discipline in Washington – It’s a train wreck. They’re going to have to figure out a way to raise some revenue otherwise we’re staring at some pretty scary deficits. And I think eventually the credibility of the United States will suffer.

FRA: And Peter?

Peter Boockvar: Well, I think the weakness in the dollar is beginning to reflect the worries of those depths and deficits. That maybe we do have a $1 trillion budget deficit again in 2019. Obviously fiscal policies, in terms of tax cuts, are in place. Everyone’s got their fingers crossed that it actually improves economic growth as opposed to just improving earnings per share. We are seeing some wage growth which is a good thing, but one thing that we’ve seen is that the assumption on Wall Street was that the tax cuts all that would flow to the bottom line and we’re seeing that not all that will flow to the bottom line.

Christopher Whalen: Oh yeah. And the repatriation narrative is infantile. I cannot believe that people with PhDs in economics can sit there and go on and on about how cash is going to be brought back and invested in the United States. That’s not the way corporate finance works.

Peter Boockvar: Yeah, and a lot of that cash has been spoken for anyway with all the debt accumulation to buy back stock. So companies have already frontloaded the repatriation by taking on all this debt.

Christopher Whalen: Of course. But if you look at tax shelters like you saw they hit the Goldman because they are the great tax shelter shop. And a lot of that stuff is not going to come to light. You think everybody is going to go to the IRS and turn themselves in? The case with Dow last year that the Supreme Court declined to hear was a big deal. Donald Trump has the same tax lawyers as Dow. Trust me, the IRS now, any corporate they go to sham partnerships with as tax shelters, they basically just have to write a check. They have no appeal. There’s trillions of dollars at stake here. Trust me, these corporates are not going to come forward and say we did this wrong. Nope.

Peter Boockvar: I continue to believe that the other side of the easing mountain is upon and that creates the biggest risk for markets and the economy. People say that we’re not going to have a bear market until the economy goes into a recession and I argue that it’s going to be the rise in interest rates that leads to a decline in stocks that then leads to the recession. A trillion dollars of liquidity coming out from the Fed just in a loan is going to be a big deal as we deeper into the year. That’s what we have to look forward to over the next 2 years. The Fed taking out a trillion in loan the next 2 years after beginning that last year, the ECB ending QE, and that’s a $600 billion reduction in their run rate in 2018. And then the elimination of negative interest rates. So that’s what we have to look forward to over the next 2 years in terms of interest rates and I don’t see risk assets just whistling past that.

Christopher Whalen: Oh no. Look, everything is compressed. The whole curve is going to expand. Yra?

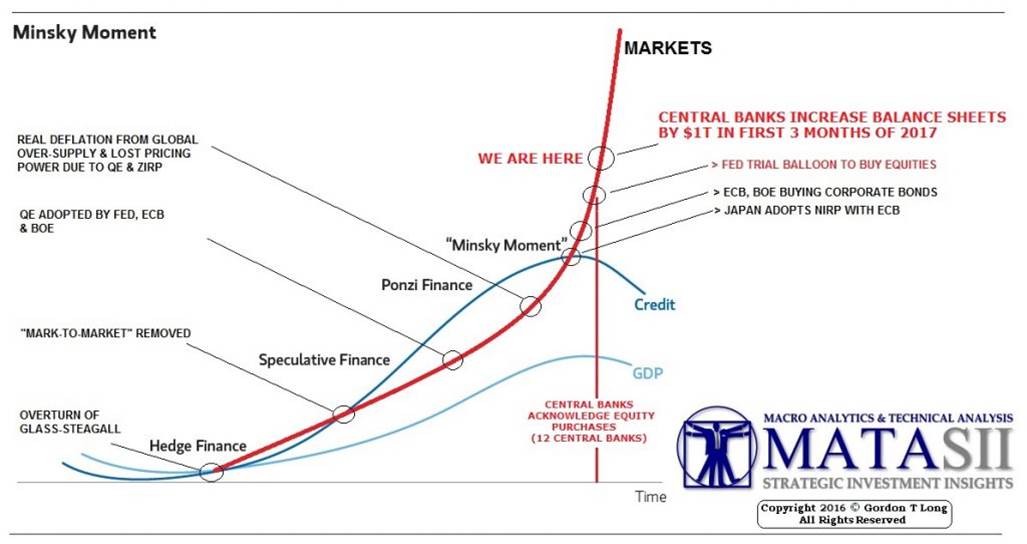

Yra Harris: Yeah, everything that was talked about and then you throw in the infrastructure spending package Trump is going to get through. I mean he’s not only selling the world today. You should watch how he probably hijacked Davos because they couldn’t lick his boots fast enough and he’s disruptive…So he’s got all this more debt coming on. He’s got really got discussions going on, in the United States of course, about financing debt. We are going to find out if his interest rates are going higher. We know the answer to it, but the rate of the world is going to have to find out. You have the ECB who took the Bernanke model and did everything they could to explode it with the amount that he could buy and he’s still…Peter and I know, he’s going to end in September, but it’s going to have a massive amount of assets on that balance sheet in the ECB and with the Germans breathing down their neck…There is nothing good going on there. There is nothing good and it’s going to come back to haunt. Now we have Joe from China and he’s reminding us about Minsky. The Chinese are reminding us about Minsky so we know we are in a very difficult situation and the world is just sleeping through it because you wake up in the morning and you see your stock portfolio is doing a whole lot better so you go, “What’s the difference. We’re all good here.” And they carry on. So, I think it’s going to be this year. I don’t think it’s going to wait for 2019. Some of these issues that people have chosen to pretend don’t exist. And it’s all bound to, we always know it. I think the 3 of us would agree that all crises come up from the debt market. Credit and debt markets determine everything and we’re there. It’s just what’s going to be the actual start that sets it off. I am not sure. I do agree with Peter that it’s going to be central bank oriented and it’s going to come as a change of direction. I think, Christ, you would agree with that too, it’s just how they do it. And Jerome Powell is going to be an interesting guy to see how he reacts to it.

Peter Boockvar: I think a very important question is: Where is the out-of-the-money put strike price right now on the Fed? What level, what percent decline, tells Jerome Powell that he needs to stop his tightening or reverse it? I think that’s going to be an important question.

What’s his tolerance level if these asset markets reverse themselves?

Christopher Whalen: But that’s an important question you’re asking because the tolerance level was very low. In other words, they wouldn’t tolerate any market upset. With Powell, it may be a little different.

Peter Boockvar: Because Powell has more tolerance.

Christopher Whalen: Yeah, I think he does.

Peter Boockvar: I agree.

Yra Harris: …Selloff in the equity markets? I don’t know.

Christopher Whalen: That’s the question Yra.

Yra Harris: Yeah.

Peter Boockvar: The irony is that you get a 20% correction then you’re just back to where you were last year.

Christopher Whalen: Oh, Powell has an easy button on his desk. The question is: Does he push it?

Peter Boockvar: Right.

Yra Harris: Yep, I think that’s absolutely right.

Peter Boockvar: As we speak, interest rates are breaking out today. The 10-year is up to 2.67% now. The 3-year is approaching 2.13%.

Yra Harris: And the Europeans…Today they’re not the catalyst; other times they are the catalysts. I’m interested to see it.

Peter Boockvar: Yeah, the dollar rallied for a couple hours after Trump tried to defend it and went straight back down again.

Yra Harris: And you know what? We didn’t even get into our discussion with the Swiss because they get the alchemy award of the last millennium. The game that they played here and pulled off is unbelievable to me. It tells you about the state of the world…

Christopher Whalen: Well, Peter’s right. They could take a loss on all that corporate exposure that they have. That would be a lot of fun.

Yra Harris: You know what, Richard, they finally admitted now that they are going to be the cryptocurrency capital of the world. They have been the currency capital of the world. But I think that is absolutely right. And it’s interesting, Peter, that is the Yen that turned when Kuroda was speaking at Davos today. The Yen turned very hard.

Peter Boockvar: Yep, it did. He said he’s getting more comfortable as inflation is going to their target.

Yra Harris: Yeah, and I think the Japanese are waking up that the Trump administration is not too happy with the Yen being so relatively weak. And Draghi and Kuroda can pretend all they want…And what was that comment yesterday from that one guy, and I know that they went back to that damn G20 meeting in Washington, which I kind of thought that they would, but he said, “Monetary policies that have a negative effect on currencies, that’s just an effect, that’s not a targeted currency.” Right…And that’s why every central bank when they release the statement about their interest rate intentions cites the level of the currency. Everybody in the United States, that is. Everybody talks about the level of the currency. Everyone discusses the level of their currency as being one variable in determining how they’re going to set interest rates.

FRA: Interesting times and great insight on the credit markets, financial markets and the economy. Thank you very much gentlemen for being on the podcast programmed show.

Great discussion.

Yra Harris: I’d love to do this again. This is great.

FRA: Just as a final word for our interested listeners. How can they find more information about your work, Chris?

Christopher Whalen: Just go to my website: www.RCWhalen.com. It’s the same handle on Twitter. And the Institutional Risk Analytics which is a free newsletter.

Peter Boockvar: Go to www.BoockReport.com and look at the asset management business: www.Bleakley.com.

FRA: Great. And finally, Yra?

Yra Harris: You can find my blog at www.YraGHarris.com and sign up for Notes From Underground which is also free. Whenever I write which is sometimes 4 times a week or sometimes 1 time a week will be sent you. And listen to the FRA podcasts. I think that they are very informative.

FRA: Great, thank you guys and maybe we can all do this together sometime.

Great discussion.

Yra, Peter, Chris: Thank you.

Transcript posted by Daniel Valentin