02/23/2015 - GRAHAM SUMMERS on Financial Repression

“QE was never meant to create jobs or generate economic growth… it was a desperate ploy by Central Banks to put a floor under the bond market so rates wouldn’t rise.

… It’s also why Central Banks have kept interest rates at zero or even negative. They cannot afford to have rates rise.

In the US, every 1% increase in interest rates means between $150-$175 billion more in interest payments on our debt per year.

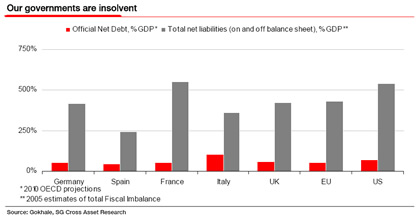

when you include unfunded liabolities, this problem is endemic throughout the Western world and has been for years.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/23/2015 - MyRA to Become TheirRA?

Speaking at AARP headqusrters in Washington, President Obama will announce ORDERS to the Labor Department to write new rules for financial managers who handle retirement accounts for working Americans.

THE COVER

As USA Today reports, The White House says the goal is to end “hidden fees that hurt consumers and back-door payments that help Wall Street brokers,” deals that costs retirees billions of dollars in savings.

THE AGENDA

White House officials said they want new fiduciary standards that would require financial advisers to put clients’ interests ahead of their own… and “buy our bonds.”

We wonder how long before there will be an official asset allocation by dictat…??

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/23/2015 - Dr. Pippa Malmgren: Governments are Imposing Prices on the Market

Matterhorn GoldSwitzerland interviews former financial market adviser in the U.S. White House .. discussion on how there is no price discovery anymore by the market, & governments are imposing prices on the market .. also a discussion on the closer ties between Russia & China, Germany’s gold reserves, the phenomenon of financial repression .. 38 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/21/2015 - Paul Craig Roberts PhD Talks Financial Repression

Special Guest: Paul Craig Roberts PhD – Chairman of the Institute for Political Economy

Dr. Paul Craig Roberts is extremely meticulous in examining the central problems facing America and the developed economies today. You may not like nor agree with what he says but there is little double as a former high level Treasury official, academic professor and Wall Street Journal editor, that he knows what he is talking about.

FINANCIAL REPRESSION

“It is going on on several fronts conducted by different people for their own agendas, though they all seem to be mutually supporting.

1-FINANCIALIZATION OF THE ECONOMY by the Big Banks. – “What that means is that they are converting the entirety of the economic surplus to paying interest on debt. They are draining the economy of all vitality! There is nothing left for the expansion of consumer demand, business investment and old age pensions. It expropriates the economic surplus that is created beyond the maintenance of the current living standard into interest on debt.

2-OFF-SHORING OF MIDDLE CLASS JOBS by Corporations & Wall Street – “What the Corporations and Wall Street have achieved by off-shoring manufacturing jobs and tradable professional job skills such as software engineering & information technology. What they have done by moving these offshore is to recreate the labor market conditions and wage exploitation of the late 19th century.”

3-MANIPULATION OF THE BULLION MARKETS by the Futures Market Bullion Banks – “There is no free market in the futures markets. These are markets that are manipulated.”

COLLUSION BETWEEN PARTICIPANTS

“I think there is a lot of collusion. For example the government colluded with the banking system in financial deregulation. For example they repealed Glass-Steagall. They expressed this absurd claim that financial markets are self regulating.”

“They turned the financial system into a gambling casino where the bets are covered by the tax payer and central bank.”

The cancer which started in the US Financial System has spread globally. The carriers of the cancer has been the International Banks.

WASHINGTON ANSWERS TO WALL STREET

“Some of the Financial Repression is collusion of government serving the financial interests because Wall Street is a huge supplier of political campaign funds which you are highly dependent on to get re-elected. So you answer to the donors. You don’t answer to the public interest. It doesn’t give you any money.”

“You answer to:

Wall Street,

The Military-Security Complex,

The Agri Business like Monsanto,

The extractive Industries (Oil, Timber, Mining)

These are the powerful interest groups that use the government to serve their interests.”

THERE ARE NO LONGER COUNTERVAILING POWERS IN WASHINGTON

With the destruction of the manufacturing jobs in America through off-shoring, it has reduced the power of the unions and destroyed the Democrats independent source of campaign funds.

“You now have two parties with the same head and reporting to the same masters. There is no longer any countervailing power”

You no longer have the Democrats supporting workers against the Republicans supporting business. Both parties represent them.

“This is the reason you can’t do anything about Financial Repression!”

NEO-CONSERVATIVE CONTROL OF FOREIGN POLICY – $6T TRILLION IN WAR DEBT

We have been in 14 years of wars and added $6T of national debt to finance these wars “without adding five cents of investment for the country having taken place.”

“We now have the Neo-Conservatives driving the conflict with Russia (which is insane), with China (which is insane). The United States doesn’t have the power to try and dominate Russia / China. Especially now that the two countries have a strategic alliance”

“You have much of the world turning away from the United States because of Washington’s

Abuse of the Dollar as the World’s Reserve Currency,

Abuse of the dollar based payment system,

Imposing unilateral sanctions which are acts of war,

Threatening people with expulsion from the clearance mechanism and people saying we won’t have any part of this,

The BRIICS establishing their own version of the IMF,

The Impact of the Spy Scandals and people saying they will build their own internet,

All of this is not only going to effect business it is going to effect American power. It is going to start shriveling!”

“If you have these crazed Neo-Conservatives demanding control of the world, faced with declining power, you don’t know what they will do! It is a very, very dangerous situation. I’m surprised it has taken the world so long to realize the threat the US poses to the rest of the world.”

“The US Dollar payment system is essentially a system for looting. This, Globalization and Neo-liberal economics are tools of American economic imperialism. Countries are beginning to realize this. The looting of countries by American imperialism has now reached the point where it is turning on itself – Greece for example.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/21/2015 - Financial Repression has allowed Governments to get deeper into Debt

“The anti-austerity sentiment appears to be gaining momentum even in the core nations of Europe .. Even the president of the European Commission recently questioned the usefulness of austerity, noting its results so far have only been shrinking growth and social suffering .. Austerity in Europe is on life support, but the insatiable desire to spend is not limited to just Europe .. Seduced by low interest rates, governments all over the globe are yearning to return to their former big spending ways. Using the cover derived from lower deficit to GDP ratios—caused by record-low rates–politicians are emboldened to return to their first love .. deficit spending. For example, the interest payment on the national debt in the U.S. is lower today than it was prior to the financial crisis, despite the fact that the national debt is $9 trillion higher .. When interest rates rise above these currently manipulated low levels, not only will payments for debt service soar, but the asset bubbles created by central banks over the past seven years will burst.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

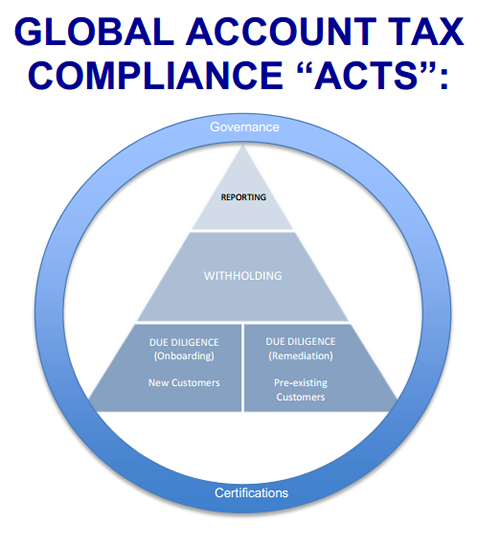

02/21/2015 - The Global “Doomsday” Book – Haydon Perryman Talks GATCA/FATCA

Special Guest: Haydon Perryman, CGMA – FATCA Program Manager

“This a modern day “Doomsday” Book, the same asWilliam the Conqueror implemented in 1066 after conquering England. He needed to know where the wealth was so he could tax it”

“This is Not Really About Tax There are Easier Ways to Solve Tax Tracking – Its about a Common Reporting Standard. Its about the ability to track Capital”

“FATCA is a decoy for the Common Reporting Standard”

“There is an incredibly aggressive urgency of implementation – an unprecedentedly quick agreement between 57 governments”

Why?

Either to Tax it , Expropriation it or Control Its Free Movement

There will also be considerable customer backlash to FATCA and the documentation it requires. In the age of social media this matters, if this sounds like hyperbole please have a look at this URL

At a most basic level FATCA, the IGAs and the CRS are about making tax part of standard KYC/AML procedures and then reporting, for tax purposes, to those jurisdictions, in which the account holder has tax residence or citizenship.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/21/2015 - Kevin Warsh on Financial Repression

“In this environment, policy makers are finding their authority, credibility and firepower being tested. In turn, they are finding it tempting to pursue ‘financial repression’—suppressing market prices that they don’t like. But this is bad policy, not least because it signals diminished faith in the market economy itself. In environments of financial repression, businesses are keener to retrench than recommit their time, energy and capital to new projects. Trillions of dollars of private capital remains on the sidelines. And the private-sector engine that drives prosperity sputters .. Financial repression is sometimes the effect of policy even if it is not the intent. It manifests itself, for example, when policy makers react more forcefully to declines in asset prices than to increases. Price increases tend to be treated with benign indifference. But declines often lead policy makers to respond with force, deploying fiscal stimulus and monetary accommodation. Market participants then conclude that governments have their backs .. The Federal Reserve’s continued purchase of long-term Treasury securities risks camouflaging the country’s true cost of capital .. With financial repression at play, we risk missing early warning signs from markets that our debt burden is intolerable .. Financial repression embeds the wrong incentives—obfuscation begets delay, and a robust recovery becomes unattainable .. Financial repression is a tactic that may help get us through the week or month or year. But it will come at a substantial cost to our long-term prosperity.”

– Kevin Warsh, Former Federal Reserve Governor, a distinguished visiting fellow at Stanford University’s Hoover Institution, on the Steering Committee of the Bilderberg Group

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

Axel Merk emphasizes the advantages of investing in gold to address the investment challenges in the era of financial repression .. points out how the days of low or 0% interest rates is moving into negative interst rates in several countries – this is a form of financial repression where savers earn less than the inflation rate to discourage saving & the purchasing power of your assets loses value over time .. on gold, highlights how the purchasing power of gold has not changed all that much & therefore it presents itself as an investment asset for financial repression .. Merk explains how the interests of government on their massivie debt are driving policies to mechanisms of financial repression to “debase the value of debt” – negative interest rates, inflation loss of purchasing power, & currency debasement .. “Differently said: interests of the government and savers are not aligned. More broadly speaking, investors – be that in the U.S., Japan, Europe, can’t rely on their government to preserve the purchasing power of their savings.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/19/2015 - Insurance Companies Will Be Raising Insurance Premiums Because of Financial Repression

Dr. Marc Faber* says central bankers are professors who never worked a day in their lives & whose easy-money policies will ultimately be disastrous for markets .. That’s why he says he thinks gold could be the “trade of the century” & why he recommends additional exposure to gold through junior miners. He explains his investing strategy today on Commodities .. says insurance companies will be raising insurance premiums to much higher levels due to the financial repression of very low interest rate & low yields .. thinks sovereign wealth funds will begin investing in gold .. 7 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/19/2015 - Dr. Marc Faber Talks Financial Repression

Special Guest: Dr. Marc Faber – Editor and Publisher of “The Gloom, Boom & Doom Report”

Dr Marc Faber feels strongly that the current money printing policies “will not end well”!

He feels that:

“Governments are not smart enough to have thought the current scheme out. The professors, academics (who have never worked a day in their lives in the private sector) and central banks think by having artificially low interest rates you can solve problems. Actually, they aggravate the problems!”

“When central banks print money nothing begins to make sense!” — “It is no longer a free market. Markets are now manipulated by governments and notably by their agents, the central bankers.”

FINANCIAL REPRESSION – An “Expropriation”

“Basically what central banks have done around the world is to push interest rates to extremely low or even negative rates. I don’t call it a repression. I call it an expropriation of the savers because before the intervention of the banks occurred post 2008, a saver got a decent rate of interest. Now they get nothing at all! So either they speculate or they lose purchasing power over time!”

The purchasing power of money is depreciating. Financial Repression or what Dr Faber calls “expropriation”, he feels is very negative for the middle and working class.

The current government and central bank policies “are leading to huge asset bubbles in stock, real estate, commodities, collectibles, art and so forth.” Inflation and Deflation work much the same way according to Marc Faber. All prices do no go up or nor decline at the same time.

“We had the collapse of the Nasdaq after March 2000. Then the Fed created the housing bubble and after it collapsed after 2007, it had a devastating impact on a very large number of households. Then in 2008 we had a commodities bubble with oil going to $147/bl and now you know where oil is trading at. Its now 1/3 of what it was at that time basically. The Money printing leads to bubbles which they deflate and hurt the majority at the expense of a few people. This is not going to help the economy in the long run – PERIOD!”

PENSION AND INSURANCE “MODELS” – In Serious Trouble

The pension plans and Insurance industry is in deep trouble. They are basically forced to speculate on something. That speculation will end very badly!

WHAT SHOULD INVESTORS DO?

Dr Faber says quite honestly,

“I am an economist, strategist and investor. The answer to the question of what should an investor do is – I DO NOT KNOW! But people expect me to know so I can tell you what I would do. In the absence of knowing precisely how the end game will be played we should invest in a diversified portfolio of different assets. Some in real estate, some in equities, some in cash & bonds, and some in precious metals.”

“For an investor to not own some precious metals at this point is almost irresponsible!”

MORE QE IS COMING

“I don’t believe we have currency wars but rather the central bankers, one after the other, prints in a ’round about'”

“Money printing has never ended well in history. It can postpone the problems, but it will make the end result even worse.”

“I believe the Fed will intervene at some point with another round of QE!”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/18/2015 - Pension Obligations in Times of Financial Repression

Allianz report gives great insight for pension fund risks & challenges in this era of financial repression – negative interest rates, low yields, inflation, regulatory challenges, capital controls …

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/18/2015 - Paul Brodsky on Financial Repression

Boom Bu$t .. discussion with Paul Brodsky on how financial repression seems to be the order of the day on monetary policy, with negative interest rates rife throughout government bond markets in Europe – explains where financial repression is leading central banks & explains what kinds of strategies you can devise to get around it .. 1/2 hour total program

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/17/2015 - PIMCO: “Financial Repression is now a Truly Global Phenomenon.”

PIMCO viewpoint on how financial repression has compressed & highly correlated yields on government bonds from developed countries .. “With the Fed acknowledging international developments in their last Federal Open Market Committee (FOMC) statement, financial repression is now a truly global phenomenon.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/14/2015 - Jim Rickards on Financial Repression: Governments are holding Melting Ice-Cubes to Reduce their Debt Burdens

From a USA Watchdog interview a few years ago, Jim Rickards explains how financial repression can be used to address the debt burdens of governments: “The answer is 4% inflation. It doesn’t have to be that high, it just has to be persistent. It’s like holding an ice cube in your hand. It just melts away. Well that’s what the Fed is doing, and that’s what financial repression is all about .. Financial repression only works if people cannot own gold.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/14/2015 - Financial Repression – Capital Controls

INET video interview with Boston University’s Professor Kevin Gallagher on his new book .. discussion of international capital flows, how it is causing destabilizing effects in developing countries .. Gallagher points out that today a number of emerging economies, including Brazil, Taiwan, & South Korea, have been successfully experimenting with new capital account regulations (CARs) to manage volatile capital flows .. Gallagher develops a theory of countervailing monetary power that shows how emerging markets can & should counter domestic & international opposition to the regulation of cross-border flows, even as he acknowledges powerful attacks from a multiplicity of interests, seeking to undermine those very regulations .. 20 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/14/2015 - Professor Laurence Kotlikoff Talks Banking & the “Fiscal Gap”

Special Guest: Professor Laurence Kotlikoff – William Warren FairField Professor of Economics at Boston University

Professor Laurence Kotlikoff believes the current banking system needs to be restructured into “Limited Purpose Banking to remove excess leverage and opacity; that the bureaucrats are having a field day with new ineffective regulations and the US government is financially bankrupt when accounted for correctly.

FINANCIAL REPRESSION

To Professor Kotlikoff the Financial System needs to be understood as a Public Good. It is a market place which needs coordination and banks & financial intermediaries are there to facilitate the operation and management of that public good. Regulators are there to keep the public good working. The question is what kind of regulation do we need that will ensure the financial system keeps working.

“Today the system is in bigger danger than 2008 because fundamentally the banks are being allowed to operate with dramatically larger leverage than would keep things safe!”

Additionally, the banks are being allowed to operate with full opacity. They don’t have to tell what they own in terms of assets or liabilities. Therefore depositors don’t know the risk they are taking which can lead to bank runs which we saw in 2008 where banks didn’t trust other banks.

“We are all set up to see this happen again because of all this leverage and opacity. The system is more fragile!”

THE FIX

In his book Jimmy Stewart is Dead, Professor Kotlikoff talked about shifting from a “Faith Based” banking system to a “Show Me!” banking system where financial intermediaries disclose all the assets they are holding. Instead of borrowing money to invest in assets we can’t see, they would sell shares through equity finance. They in effect would be equity financed Mutual Funds.

The purpose of “Limited Purpose Banking” which Professor Kotlikoff is proposing in his book is that all the financial middle men who are running the “public good” not be allowed to gamble with it. To most people their banking would be through:

Cash Mutual Funds – For the Payment System

Mortgage Mutual Funds – Instead of Fannie Freddie

The leveraged derivative element of the current speculative banking system would be run in a similar manner to modern parimutuel betting system polls. Dodd-Frank legislation has not made the system safer and instead sees only one regulator agency (the “Federal Financial Authority”) which oversees disclosures versus 130 entities in Dodd-Frank!

THE $210 TRILLION FISCAL GAP

Economists like Professor Kotlikoff feel the ‘Fiscal Gap’ is what we should be measuring, not one part of it which is the National Debt. The Fiscal Gap according to the CBO is presently $210T while the National Debt approximates $13T. We are focused on the $13T but really we need to be focused on is the $210T.

Over 1200 economists and 17 Nobel Laureates have endorsed a bill that mandates that the CBO & GAO do ‘Fiscal Gap’ reporting to look at the big picture.. Information on this bill can be found atwww.theinformact.org.

The current shortfall is 10.5% of GDP, each and every year. To offset this would require a 60% increase in taxes or for a 35% cut of all expenditures and benefits.

“The US is actually fiscally broke!”

The banks are holding a lot of the governments debt which is unpayable. Governments that cannot pay their bills print money. Eventually this inevitably leads to inflation. This will make the bonds worth less money which would highly likely put the banking system underwater.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/13/2015 - Financial Repression: Swiss National Bank Hints at Capital Controls

Zero Hedge reports from news sources that the Swiss central bank may be considering & is now hinting at implementing capital controls – one of the pillars of financial repression .. this would be an attempt by the government to restrict capital flows causing unwanted effects in the Swiss financial system, such as a strengthening currency .. “The question becomes who imposes capital controls first: Greece, where the specter of whoelsale bank insolvency is now raging across the nation, and where a capital lockout may well be imminent, or Switzerland, which knows that the moment Greece is pushed too far and a Grexit is perceived inevitable, is the moment it will be flooded with a tsunami of Euros desperate to find safe haven in a new, Swiss Franc denomination, somewhere deep in the vaults under the Swiss Alps. A tsunami which would crush SNB credibility all over again, and when capital controls will also become inevitable .. Perhaps the best way to preserve some of said credibility, especially if it is already borderline non-existent, is to frontrun capital controls tomorrow, by imposing them today.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/12/2015 - FINANCIAL REPRESSION ACTIONS TO BE EXPECTED – The Roadmap from government officials

1) Those in charge of regulating the system will lie, cheat and steal rather than be honest to those who they are meant to protect (individual investors and the public).

2) Any financial problem that surfaces will be dealt with via fraud or lies rather simply allowing those who screwed up to be fired or go to jail.

3) When the inevitable collapse finally does hit, it will be individual investors and the general public who get screwed (not bank executives or politicians).

4) The problem will be prolonged as much as possible, likely fixed years down the road, if ever and individuals will have little or no say in how it pans out.

This is the likely template for what’s coming.

The following is the proof cited that the above can be expected:

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/12/2015 - Sprott’s Rick Rule on Financial Repression

Interview transcript with Rick Rule on the economy, global counterparty risks & the natural resource sector .. on the issue of capitulation in the finacial markets for natural resources: “We came close last October. There were some moments of absolute panic .. but we didn’t follow through with a capitulation… Capitulation usually follows a protracted period of diminished volume… I have never seen a bear market in the juniors end without one .. just because I haven’t seen it doesn’t mean it has to be that way.” .. identifies financial repression: “The fiscal regime that has been in place since the financial crisis is one where the political class has decreased the interest rate artificially, allowing the very large money center banks to borrow at extraordinarily low costs both from their retail deposit banks but also from their central banks and lend the money back to sovereigns. In effect what happens is that the central governments loan the banks money at .75% or 1% and borrow the money back from the banks at 2.5% or 3%, giving them a 1% or 1.5% interest rate carry at very, very, very low risk. That’s the way the Japanese subsidized their banks and made their banks solvent again after their currency crises.” .. 28 minutes accompanying video

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/08/2015 - Axel Merk: “We have Financial Repression Everywhere.”

Is deflation or inflation on the financial horizon? .. here is what Axel Merk thinks: “For me, it’s a slam dunk. We are going to get inflation. There are negative real interest rates in the developed world as far as the eye can see. Just about every country has negative real interest rates, and we have financial repression everywhere. I think we cannot afford positive real interest rates over an extended period. Just think about the U.S. with the entitlement wave coming against us. We got strong incentives in place to have negative real rates when the government has too much debt and when consumers have too much debt. The reason why we have this battle with inflation and deflation is we are clearly facing a deflationary bust, and central banks are fighting against it. If we didn’t have central banks, I’d be fully onboard with deflation, but because we cannot have bankruptcies, we will inflate our way around it .. Ultimately, inflation is going to first come up in the U.S., and that inflation is going to be exported to other countries.” .. 18 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/23/2015 - GRAHAM SUMMERS on Financial Repression

02/23/2015 - GRAHAM SUMMERS on Financial Repression