05/19/2015 - Russell Napier: The War on Cash will cause gold to be used as money again

The war on cash is an unintended consequence of the financial repression macroprudential policy of the zero or negative interest rates .. if your bank is charging you interest on your bank deposit, why not just get your money & leave it under your mattress at 0% (higher) yields? – so governments & central banks are likely to attempt to abolish cash to eliminate this action .. what will be the effect on gold? – Russell Napier: “In such a world, zero-yielding gold would be a high-yielding instrument. If the authorities ever sought to restrict access to banknotes, then gold would suddenly find itself enfranchised as money for the first time in many decades. So, given the scale of these competing forces, it is just too early to say what might happen to the gold price, but the allure of gold will grow the more it becomes clear that central bank fiat has failed and the age of government fiat is dawning .. The time is ever nearer when the price of gold will rise in an era of deflation. In due course, though no time soon, the full force of government fiat will engineer a reflation, albeit one replete with the misallocations of savings and capital so beloved by the bureaucrat. Then the PhD standard, in which the value of money is linked only to the words of the over-educated, will have ended. The gold price will rise even further, ‘And the words that are used for to get the ship confused will not be understood as they’re spoken, for the chains of the sea will have busted in the night’. And that’s ‘The hour when the ship comes in.’”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/18/2015 - Jim Puplava Talks Financial Repression

Special Guest: Jim Puplava – Founder, President & CEO, PFS Group

SPECIAL GUEST: JIM PUPLAVA is the Founder, President & CEO of PFS Group. He is also the chief author and host for the Financial Sense Newshour. Puplava’s website at financialsense.com was named a “supersite for alternative investing” by The Globe and Mail, Canada’s largest-circulation national newspaper.

Jim Puplava was one of the first researchers to go public with the concept of Financial Repression and the Financial Repression Authority wants to recognize him for this. After studying the writings of Rogoff & Reinhart, Jim Puplava identified shortly after the Financial Crisis the fact that policies of Financial Repression had been used after WWII with success and began writing and talking about them. He was a long voice on the subject.

The difference today and the previous situation after WWII is:

The US is n o longer on Gold Standard (we now have a Global Fiat based currency system),

Most developed economies have record Debt-to-GDP levels,

We now have record levels of Derivative and Securitization which didn’t exist after WWII,

Globalization has changed the level of financial interconnections and dependency.

FINANCIAL REPRESSION

Jim Puplava suggests:

“Financial Repression in essence is a tax on savers! Savers are getting real negative interest rates (before taxes). The work of Keynes advocated robbing savers to the advantage of the government. The losers are savers while the winners are debtors and the government”

PUBLIC IS UNKNOWINGLY CONTRIBUTING TO FINANCIAL REPRESSION

The stock market has seen a net $60-$80B go into the stock market since the rally began after the financial crisis. “The vast majority of individuals have been going into bond funds which by the way is part of the plan of Financial Suppression”.

“Most investors have gone through two bear markets in the last decade where stocks lost 45%. They are now closer to retirement than they used to be and don’t want to go through that again!”

As such they missed out on a historic market rally. “If they had held the course they would be ahead. The vast majority of people kept their money in savings because the headlines were scary.”

“The media did an exceptionally poor job of explaining what was going on in the financial markets. Instead of telling people they needed to capture or take advantage of what Financial Repression was putting into place. Financial Repression supports growth type assets like stocks and commodities (initially coming out of 2009). This is how you re-capture (the prior market draw-downs). That is not what happened.”

A BROAD RANGING DISCUSSION

The broad ranging discussion in the 35 minute interview include:

Market drivers of Corporate Buybacks and broad Central Bank buying,

Outlook for bond rates,

Why Warren Buffet has 90% of his investments in equities,

The scope of taxation on savings and what it means to future retirement planning,

Economic growth and top line growth is not there so corporations are doing “rational allocation of capital”. This is presently driving corporate policy.

Fiscal Policy is missing from the governments economic agenda,

Critically important is the impact of demographics and changing Millennial buying patterns,

Financial Repression will likely go on for a couple more years before it inevitably breaks.

…. and more

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/18/2015 - Financial Repression: The War on Cash

International Man’s Nick Giambruno & Mises’ Joe Salerno .. the financial repression of ring-fencing regulations is intensifying in the war on physical cash .. the goal to eliminate the use of hand-to-hand currency, so that governments can document & control every transaction .. one way this war is being fought is by making it illegal to pay in cash above a certain threshold:

* Italy made cash transactions over €1,000 illegal;

* Switzerland has proposed banning cash payments in excess of 100,000 francs;

* Russia banned cash transactions over $10,000;

* Spain banned cash transactions over €2,500;

* Mexico made cash payments of more than 200,000 pesos illegal;

* Uruguay banned cash transactions over $5,000; and

* France made cash transactions over €1,000 illegal, down from the previous limit of €3,000.

Joe Salerno: The War on Cash is the attempt by governments to phase cash out of their economies. Governments hate cash because they hate the financial privacy cash makes possible. And they prefer that you keep your money in a bank to help prop up an unsound fractional reserve banking system .. The War on Cash reflects the desperation of governments .. it really says that they are bankrupt, both literally, in the sense that they can’t pay what they’ve promised, and intellectually.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

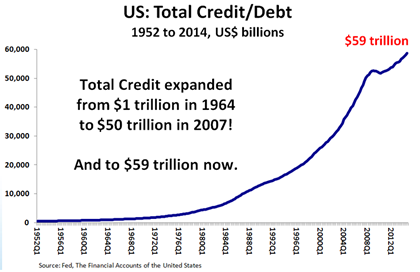

05/17/2015 - “WAR ON CASH” is a Strategic Requirement to IMPLEMENTING SUSTAINED NEGATIVE INTEREST RATES

We Can’t Rein In the Banks If We Can’t Pull Our Money Out of Them

1- Physical paper money provides the check against negative interest rates, for if they become too great, people will simply withdraw their funds and hoard cash.

2- Furthermore, paper currency allows for bank runs. Eliminate paper currency and what you end up with is the elimination of the ability to demand to withdraw funds from a bank.

Complete abolition of cash threatens our very freedom and rights of citizens in so many areas.

THE BARRIER TO SUSTAINED NEGATIVE INTEREST RATES

Paper currency is indeed the check against negative interest rates. We need only look to Switzerland to prove that theory. Any attempt to impose say a 5% negative interest rates (tax) would lead to an unimaginably massive flight into cash. This was already demonstrated recently by the example of Swiss pension funds, which withdrew their money from the bank in a big way and now store it in vaults in cash in order to escape the financial repression. People will act in their own self-interest and negative interest rates are likely to reduce the sales of government bonds and set off a bank run as long as paper money exists.

For depositors, this means they really need to grasp what is going on here for unless they are vigilant, there is a serious risk of losing everything. We must understand that these measures will be implemented overnight in the middle of a banking crisis after 2015.75. The balloons have taken off and the discussions are underway. The trend in taxation and reduction of cash seems to be unstoppable. Government is not prepared to reform for that would require a new way of thinking and a loss of power. That is not a consideration. They only see one direction and that is to take us into the new promised-land of economic totalitarianism.

The movement toward electronic money is moving at high speed and this says a lot about the state of the financial system. The track record of the major financial institutions is nearly perfect – they are always caught on the wrong side when a crisis breaks, which requires their bailouts. The fact that we have already seen test runs with theory-balloons flying, the major financial institutions are in no shape to withstand another economic decline.

The Government Can Manipulate Digital Accounts More Easily than Cash

This may sound over-the-top … but remember, the government sometimes labels its critics as “terrorists“. If the government claims the power to indefinitely detain – or even assassinate – American citizens at the whim of the executive, don’t you think that government people would be willing to shut down, or withdraw a stiff “penalty” from a dissenter’s bank account?

If society becomes cashless, dissenters can’t hide cash. All of their financial holdings would be vulnerable to an attack by the government.

This would be the ultimate form of control. Because – without access to money – people couldn’t resist, couldn’t hide and couldn’t escape.

Its Happening Everywhere there are Financial Problems – Nowhere Else?

The central banks are … planning drastic restrictions on cash itself. They see moving to electronic money will:

Eliminate the underground economy,

Prevent a banking crisis.

FRANCE

France passed another Draconian new law that from the police parissummer of 2015 it will now impose cash requirements dramatically trying to eliminate cash by force.

French citizens and tourists will then only be allowed a limited amount of physical money. They have financial police searching people on trains just passing through France to see if they are transporting cash, which they will now seize.

Meanwhile, the new French Elite are moving in this very same direction. Piketty wants to just take everyone’s money who has more than he does. Nobody stands on the side of freedom or on restraining the corruption within government. The problem always turns against the people for we are the cause of the fiscal mismanagement of government that never has enough for themselves.

GREECE

In Greece a drastic reduction in cash is also being discussed in light of the economic crisis. Now any bill over €70 should be payable only by check or credit card – it will be illegal to pay in cash. The German Baader Bank founded in Munich expects formally to abolish the cash to enforce negative interest rates on accounts that is really taxation on whatever money you still have left after taxes.

EUROPE

There is a growing assumption that the negative interest rate world (tax on cash) is likely to increase dramatically in Europe in particular since it is socialism that is collapsing. Government in Brussels is unlikely to yield power and their line of thinking cannot lead to any solution. The negative interest rate concept is making its way into the United States at J.P. Morgan where they will charge a fee on excess cash on deposit starting May 1st, 2015. Asset holdings of cash with a tax or a fee in the amount of the negative interest rate seems to be underway even in Switzerland.

People can’t pull cash out of their bank accounts – for political reasons, because they’ve lost confidence in the bank, or because “bail-ins” are enacted – if cash is banned.

The Financial Times argued last year that central banks would be the real winners from a cashless society:

Central bankers, after all, have had an explicit interest in introducing e-money from the moment the global financial crisis began…

The introduction of a cashless society empowers central banks greatly. A cashless society, after all, not only makes things like negative interest rates possible, it transfers absolute control of the money supply to the central bank, mostly by turning it into a universal banker that competes directly with private banks for public deposits. All digital deposits become base money.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/17/2015 - One of the 4 Pillars of Financial Repression: Data Obfuscation

Dr Pippa Malmgren, a former U.S. Plunge Protection Team member, explains how governments fudge price inflation numbers .. It’s one of the pillars of financial repression – obfuscation.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/16/2015 - ALLIANZ PRESENTATION SLIDES: Redefining Risk in the Next Phase of Financial Repression

Allianz website to help navigate the risks in the unfolding era of financial repression .. how to find new opportunities & combat new risks in a rising-rate, slow-growth environment.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/13/2015 - Richard Duncan Talks Financial Repression

Special Guest: Richard Duncan – Macro Watch

FINANCIAL REPRESSION

“The Polices that come under the heading of Financial Repression I look at s policies that were necessary once the global bubble began to implode in 2008. The policies the Government, the Fed, the US Treasury, and Central Banks around the world have been putting in place are emergency measures just to try and prevent the next Great Depression from occurring. When you add all these measures together it has become to be known as what is called Financial Repression. I don’t think the policy makers consider don’t review it as repressing anything. They view it as measures that are absolutely crucial to keep the global economy from absolutely imploding. While there are some unpleasant side effects, (like savers not earnings enough money to retire), they view the alternatives as complete economic breakdown which would be far, far worse!”

“Policy makers consider these policies as the bare minimum to prevent the global crisis from becoming the Great Depression – Part II!”

A GLOBAL BUBBLE

“We have a global bubble which started to pop in 2008, but the policy response of trillions of dollars of budget deficit, financed with trillions of dollars of new fiat money creation has succeeded in keeping the global bubble inflated. We still have a massive bubble who’s natural tendency is to deflate. In order to keep it from deflating into the Great Depression policy makers have continued to inject more credit! This is what Quantitative Easing is all about.”

GOVERNMENT NOW “MANAGES THE ECONOMY”

Richard Duncan’s basic premise is that the government has been managing the economy since at least WWII and to make money investors must anticipate what the government is going to do next. As such he uses a framework to monitor liquidity and credit growth to see how they will impact the economy and force the government into what must be done to continue to manage the growth of the economy.

The broad ranging discussion includes:

Developed Economies Stealth Strategy of Government “Debt Cancellation”

The Potential of a Recession in 2015 /2016,

Expectations of a QE4

Reasons for $5T of Global Bonds trading at Negative Nominal Rates,

Global Deflation as a result of Globalization and the resulting Global Over-Production,

…. and more

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/09/2015 - Allianz Global Chief Investment Officer Andreas Utermann on Financial Repression

Allianz Global Investors (Allianz GI) using the following strategies to address investing in the era of financial repression: equity long/short, merger arbitrage, options trading, commodities, volatility, global macro, absolute return bonds, private debt, infrastructure debt & infrastructure equity .. Global Chief Investment Officer & Co-Head at Allianz GI Andreas Utermann: “In an environment of financial repression, characterised by much lower future expected returns from the beta element of all asset classes, these strategies can help investors capture alpha.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/08/2015 - IMF Paper on “Capital Flow Management”: Financial Repression – Capital Controls

Jim Rickards* refers to the IMF’s plan on “capital flow management” as really about capital controls – both mean “We Keep Your Money” he says .. this is an IMF paper: “The global financial crisis underscored the costs of systemic instability at both the national and global levels and highlighted the importance of dedicated macroprudential and capital flow management policies. The IMF has been assisting its members with policy advice as well as developing and making operational their policy frameworks. Multilateral aspects of both policies need to be fully considered, including the interaction with other domestic and international legal frameworks. To the extent that capital flows are the source of systemic financial sector risks, the tools used to address those risks can be seen as both capital flow management measures (CFMs) and macroprudential measures (MPMs).”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/07/2015 - CUSTODIAL RISK QUESTION TO ANSWER: What do you really own when you buy an investment?

In our complex financial world of securities, derivatives, counterparty agreement and rehypothecation of the collateral of assets under management virtually no one has the actual physical share certificates of stocks or other assets held by their custodial financial investment firm.

“Custody Risk is one of the biggest, most important issues to consider if you want to maintain your wealth when the next round of systemic risk hits!” Graham Summers – Phoenix Capital

TWO PROBLEMS

1- CUSTODIANS OFTEN DON’T KNOW WHERE YOUR ASSETS ARE HELD

The SEC recently performed a study of some 400 investment advisor firms. As the SEC itself stated in its report – approximately one-third (140) failed to meet custody rule requirements. What this says is custodians don’t know where their clients funds are! Many didn’t even know they themselves were legal custodians of their clients funds!

2- YOUR ASSETS WILL LIEKLY BE FROZEN WHEN YOU NEED THEM MOST

Even if an appropriate legal framework is in place to eliminate the risk of loss of value of the securities held by the custodian in the event of its failure, it can take weeks or even months to transfer the securities to new custodians. During that time, you cannot close out open positions .. they are effectively frozen.

In the case of MF Global, some investors were locked out of their accounts and couldn’t trade their positions for weeks. As a result many of them incurred massive losses.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/06/2015 - Egon von Greyerz Talks Financial Repression

Special Guest: Egon von Greyerz – Founder & Chairman

RISK & WEALTH PRESERVATION

UNDERSTANDING RISK & WEALTH PRESERVATION

“Wealth Preservation is absolutely critical for the coming years, or even decades and was we set up a special division within Matterhorn Asset Management called GoldSwitzerland to assist investors. We store primarily Gold and Silver outside the banking system in ultra secure vaults in Zurich and the Swiss Alps (which is both the largest and most secure gold vault in the world) along with Singapore and Hong Kong with clients in over 40 countries which includes individuals, family offices as well as institutional clients.”

“We intentionally remove ourselves from counter-party risk. We facilitate the investment in precious metals for investors but the metals are held in the name of the investors and therefore they can go to any of the vaults directly (even without our assistance). GoldSwitzerland is the only company in the world that offers this facility where clients have numbered bars in their own name where they can go directly to the vault to inspect them or withdraw them directly.”

UNPRECEDENTED GLOBAL RISK

“I believe the world is in a bigger mess than I have seen going back in history! The risks are absolutely unprecedented with virtually every major economy now bankrupt. Japan in my view will not survive as an economy and will ‘sink down into the Pacific Ocean’. They are living on borrowed time and sadly at some point in time the Japanese economy will implode. Additionally we have massive problems in China where borrowing has been increased by $20T in the last few years. Europe has no solution to Greece and the Euro is the biggest problem to the world. You add to these Economic risks those of Geo-Political risk and risk is immense!”

“The Black Swans are everywhere and at some point one of them will land somewhere.”

WHY GOLD AS INSURANCE?

“Throughout history gold is the only money that has actually survived. No other form of currency has survived.

VOLTAIRE: “Paper money eventually returns to it’s intrinsic value of zero!”

MARK TWAIN: “Investors should worry about the return of their investment and not on the return on their investment!”

“I am not a gold bug. It is just that we decided in 2002 the world was in a mess and it was going to be in a bigger mess. Therefore people needed to invest directly in gold outside the banking system and preferably outside their own country of residence.”

THIS COMPREHENSIVE 35 MINUTE VIDEO COVERS MANY ASPECTS OF PRECIOUS METALS INVESTING

…. WHICH ONLY ONE OF THE WORLD’S LEADING EXPERTS CAN OFFER

Paper markets are manipulated,

Central Banks do not have the gold they say they have because of leasing contracts,

Produced and refiners are at maximum production based on demand,

Meanwhile, Gold is trading at or near its cash cost,

The more government mis-manage the economy, the more important gold becomes,

… and much more

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/02/2015 - Financial Repression in Australia Will Likely Lead to Investments in Precious Metals

ABC Bullion Chief Economist Jordan Eliseo essay on the Australian Superannuation industry, & investment in gold & precious metals .. he sees increasing numbers of Australians as choosing to self-direct their retirement portfolios in the direction of physical gold & silver “as a natural choice in a low to negative real rate environment, and as the ultimate portfolio protection in an era of financial repression” .. also he expects at some point for institutional players to eventually adopt a strategic allocation to precious metals .. “Record low bond yields, stretched valuations in certain sectors of the equity market, and the prospect of further interest rate cuts will force these funds in this direction. One need not be a raging gold bull to recognise that a more robust and prudent asset allocation strategy for the coming years simply can’t continue to completely overlook the asset at the bottom of Exeter’s Pyramid.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/01/2015 - Obfuscation – One of the 4 Pillars of Financial Repression

Alasdair Macleod points out the obfuscation going on between government economic data & price distortions in the financial markets .. highlights theChapwood Index as a true cost-of-living inflation measure in America – it reports on the actual cost & price fluctuation of the top 500 items on which Americans spend their money on .. as you can see in the above chart, it is much higher than the government reported numbers .. “Understated price inflation fundamentally distorts everything that is macroeconomic, from monetary policy to economic commentary. It misleads central bankers into thinking they are missing their inflation targets when they are in fact exceeding them by a dangerously wide margin. It misleads analysts into thinking we are on the brink of a deflationary slump with prices maybe about to collapse. And most worryingly of all, bond markets have become more mispriced than even hardened bears realise, something that’s very likely to be corrected through a financial shock .. Just think of all those bonds that the banks have acquired as zero risk investments under Basel III rules .. If bond markets discounted, as the Chapwood Index suggests they should, a U.S. inflation rate consistently around 10%, the 10-year U.S. Treasury bond should yield at least that, possibly more. The price would halve to meet those redemption yields, and lesser credit-worthy bonds would fall even more, a development for which all financial markets are wholly unprepared, not to mention the knock-on effects on stocks, derivatives and of course, mortgage rates.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2015 - Graham Summers Talks Financial Repression

Special Guest: Graham Summers – Chief Market Strategist, Phoenix Capital Investment Research

FINANCIAL REPRESSION

“When I think of repression I think of the Psychological concept that repression is the suppression (or pushing back) of something that is too painful to deal with in sort of a conscious way. That is exactly what the central banks of the world have been doing essentially since 2008. What we had in 2008 was the beginning of a debt deleveraging cycle o the dreaded debt deflation. The economists often like to argue that deflation is terrible but they are being overly general because deflation is actually a wonderful thing (we all want to have things we want to buy be cheaper) but the issue for the economists or Keynesian’s is ‘debt deflation'”.

When debt begins to deflate you run the risk of becoming insolvent particularly in the bond market.

“Because we have been in this debt leveraging cycle for over 30 years ( a bond bubble would be the simplest way of putting it) the central banks are all terrified of a bond bear market because that means that almost instantly all developed nations are bankrupt because the way they have papered over the decline in living standard is by issuing more debt. It has gotten to the point now where because we don’t have the money to pay the debt back we are issuing new debt to roll over the old debt (or pay back the old debt).”

“It sounds like a Ponzi scheme and it actually is!It works relatively well while the bond or underlying asset is rising in value because the debt is getting cheaper and the yield is falling

“When it reverses if you don’t have the money to pay back the bond so you start to enter a deflationary cycle which is what we had in 2008.

WATCH WHAT THE FED DOES – NOT WHAT IT SAYS

“Most of what the central banks talk about is nonsense. If you watch their actions it is about how do we stop the bond bubble from blowing up? They have done that by three ways:

They cut interest rates down to zero. By doing this they made it much easier to finance debt.

They began engaging in Quantitative Easing (QE). They essentially print money and buy large assets from the banks. It started out as Mortgaged Backed Securities (MBS) because they were the assets devaluing fastest. The second and third rounds were just attempts to keep the whole thing afloat. By Buying bonds you are basically broadcasting to the world I am going to be buying this asset in the near future. The most obviously trade is then for you to buy the bond before you and then turn around and sell it to you for a profit. Globally investors have essentially been front running the central banks.

They suspended accounting standard. This was so banks weren’t forced to sell devaluing products but could maintain using them as collateral at higher required values.

“Essentially Repression was the Central Banks trying to repress the terror of debt deflation!”

“All of this has manifested a sort of financial perversion where you seeing capital doing all sorts of crazy things and flowing into areas it would have never gone to before because risk has been so mis-priced by the market.”

Troubling Issues

$555T INTEREST SWAPS

All Interest Swaps are trading “hinged” on Bond Collateral which is in a massive bubble,

Something may be up when the Plunge Protection Team takes up increasing residence in Chicago where Bernanke is now consulting to Citadel (the largest High Frequency Trading player in America) also in Chicago.

$72T SHADOW BANKING

The source of the 2008 Financial Crisis has mutated to new instruments to borrow short to finance Student Loans and Car Loans. The Shadow Banking Systems now “hinges” on Repos, Collateral Transformations and Rehypothecation.

USD CARRY BLOWING UP

The $9T US$ carry Trade is hinging on ~$5T in merging Markets which ar now on the wrong side of the trade as the US dollar spikes,

“When it gets serious you can expect the central bankers to lie!“

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/25/2015 - Financial Repression: Negative Interest Rates Now Happening in Australia …

Sovereign Man highlights how Australia has gone into negative yields on its government debt: “This is officially now the latest banking fad—buying government bonds at negative yields. You’ll remember a few years ago when the latest banking fad was handing out no-money-down mortgages to dead people and unemployed bus drivers… or buying ‘AAA-rated’ bonds which pooled these subprime loans together. That didn’t exactly work out so well. Neither will this. In fact there are plenty of similarities between today’s negative interest rates and the early 2000s housing bubble .. Instead of people, though, it’s governments who are effectively being paid to borrow.” .. it’s all about financial repression

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/24/2015 - John Browne Talks Financial Repression

Special Guest: John Browne – Senior Market Strategist, Euro Pacific Capital

FINANCIAL REPRESSION

“It is the financial repression of the ordinary individual in America. It is happening through three main avenues or arteries.

POLITICALLY – The government is increasing its power almost everyday and repressing the public individual and particularly the rights of the individual. Always under the guise that it to help you! Published statistics are highly questionable; growth rates, inflation rates, unemployment rates. They are confusing people and today I read how they are forcing people out of using cash!

ECONOMICALLY – We have had an enormous, unprecedented injection of cash into the economy with a $3.8T QE program. Its an experiment! It was initiated in Japan where two decades ago the BOJ said it wouldn’t work but the politicians insisted they do it. After two decades it still hasn’t worked. We are now doing it on a grand scheme without a pilot program. It is creating a (liquidity) trap. It is a major distortion and is crushing savers.

FINANCIALLY – ZIRP is (also) crushing savers! It is savings which forms investment for the future. 62% of employment comes from small businesses where formation must be incented. That needs capital from savings. This along with increasing regulation is not only killing the consumer but the incentive to start a small business which is the key to the creation of jobs, which is key to the creation of income which is then key to savings and growth in the economy. It has all been killed by these policies.

“I don’t believe the central bank is necessarily evil, just unbelievably Irresponsible!

LIQUIDITY TRAP

“I think we are now seeing a situation which you could call a liquidity trap. There is so much money around that if they start to raise interest rates they are going to discourage people even more from spending. Ordinary individuals have low wages (wages have been flat for six years at least) yet taxes are going up (the number of taxes) as well as charges (licenses and fees)”

“They are pushing on a string. It isn’t liquidity that matters but wages and income!”

“How does the Fed create income without just giving us cash in the post (mail) by just sending us checks?

BY DESIGN

“I’m afraid I believe at the very top it is devious! If I connect all the dots together I cannot feel it is by accident – it by design. I think the president wants to distribute American wealth around America, but even worse is to distribute American wealth around the world. Its killing the economy and its kiliing America.”

“It means (eventually) everyone is going to look towards the government for solutions – that is when totalitarian governments come in (to existence)”

“The only solution is single term politicians – Turkey’s don’t vote for an early Thanksgiving!”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/24/2015 - Financial Repression is Leading to the Death of Money

“Destroying currency amounts to belittling or ending time value, which is a crucial part of gauging and setting risk parameters in the real economy. If there is no time value to money there is essentially no reason to engage in risky behavior. This is what Keynes described as a ‘liquidity preference’, though for different reasons. Instead of individuals holding too much cash, banks will do so because of that same repression. So at the very least, where the central bank is intent on ‘forcing’ spending through negatively manipulating the currency, they are at the same time destroying the financial basis to produce credit – all the while herding financial agents into holding even more ‘currency’ … How do central banks respond to this? … By deciding that currency isn’t dead enough.” – Jeffrey Snider

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/18/2015 - Financial Repression Explained: It’s about Macro Prudential Policies to Control and Reduce Government Debt

WSJ article highlights how as interest rate benchmarks go negative, banks may be paying borrowers .. “Negative interest rates in Europe have created a previously inconceivable problem for some banks: They may soon have to pay interest to customers who borrow from them .. The novel problem is just one of many challenges caused by negative interest rates. All over Europe, banks are being forced to rebuild computer programs, update legal documents and redo spreadsheets to account for negative rates . Banks, hoping to avoid the expense of having to pay their borrowers, are turning to central banks for guidance. But what they are hearing is less than comforting.” .. it’s financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

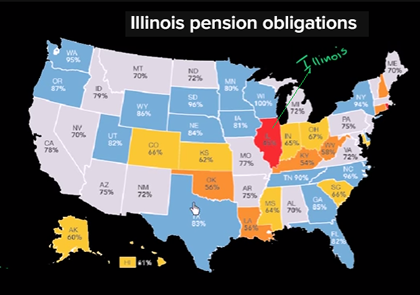

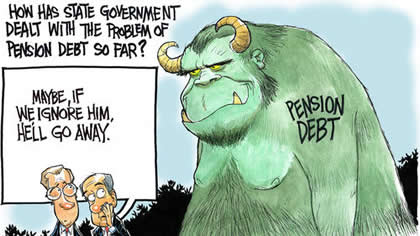

04/18/2015 - MISH SHEDLOCK talks AMERICA’S PENSION PROBLEM

Mish Shedlock talks about the magnitude of the mounting Pension Problem in America and uses his home state of Illinois as a prime example. According to a State Budget Solutions, last year’s state unfunded pensions reached an all-time high of $4.7 trillion. This funding gap state public pension plans are underfunded by $4.7 trillion, up from $4.1 trillion in 2013. Overall, the combined plans’ funded status has dipped three percentage points to 36%. Split among all Americans, the unfunded liability is over $15,000 per person.

ILLINOIS’ PENDING PENSION CRISIS

“Illinois Pension’s in general are 39% funded! This is after this massive rally we have had since 2009 in financial assets. Some of the worst ones are only about 20% funded. I think the Teacher’s Pension Plan is about that and the General Assembly and Judicial Pension Plan are also on the bottom.”

“Various cities in Illinois have problems, Chicago being one of them. The City of Chicago has a huge pension crisis right now. We have things in Illinois like “Home Rule Taxes” where cities can levy their own taxes in addition to the state. That is why we have varying sales tax that range anywhere from 6% to 10%, depending on locality.”

“I believe Chicago is Bankrupt!”

“I have been working with the Illinois Policy Institute. There are a number of cities in Illinois (I am not going to name them), but I am aware of five cities (one of them a major city – not Chicago) that are ready to file bankruptsy – and it is all over the pension issue! The problem is they can’t file bankruptcy because the state doesn’t allow it.”

“The fundamental problem is they have made more promises than they can possibly keep!”

GAMING THE PENSION SYSTEM

The problem is “you have police and fire workers who can retire after 20 years … and collect up to 70% of their earnings based on the 5 highest years salaries. We see a lot of pension spiking in the last few years where for example police work overtime (which counts towards their best five years) so these workers stand to collect far more in retirement (total years in retirement) than they actually ever made while working (total years worked).

“Tax payers are actually funding the employees portion of the pensions by excessive wages and direct contributions “.

“Chicago (has) floated General Obligation Bonds to actually just fund current expenses. That is illegal! We have bonds here in Illinois that are called tax exempt on the basis they are supposed to be funding long term infrastructure expenses that are funding short term needs.”

PROPERTY TAXES THE JURISDICTION OF UNDERFUNDED CITIES & TOWNS

“Taxes in Illinois are are already obscene. A homeowner on a $600,000 home can expect to pay $14-15,000 per year – every year on property taxes. Do you really own your own home in Illinois? On top of tht you have 10% sales tax.”

“Pensions are so underfunded in Illinois that they are going to go bust in the next slowdown. I believe one (a slowdown) is on the way.”

THE NEW, LOOMING PROBLEM FOR STATES, CITIES AND TOWNS

Negative interest rates are sweeping the globe. How will states, cities and towns fund themselves and their pension obligations in an era of potential negative nominal bond rates?

Returns on the heavily weighted funds’ bond holdings are being potentially destroyed , while

State bond offerings are likely to face mounting issues around maintaining investor attraction with such monstrous overhang levels of unfunded pension liabilities.

“How will states, cities and towns fund (attract) long term assets with 15 year negative bonds?”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/17/2015 - Financial Repression is Making Economies Less Dynamic

American Thinker posted essay emphasizes the negative, long-term effects of massive money printing through quantitative easing (QE) & of the zero interest rate policy (ZIRP) .. it’s all about the financial repression of interest rates – the thinking being that if this were not done, the pain of allowing the free markets to determine interest rates would be unbearable – “One need only imagine the bipartisan political panic were the interest paid by the U.S. federal government on its debt to double or triple, squeezing out hundreds of billions of dollars of spending on military and social programs. It is becoming ever more obvious to ever more people that sustaining these ‘financial repression’ policies is making economies ever more comatose; ever less dynamic. Exactly when the accumulating long-term economic damage becomes more onerous to central bankers and politicians than the short-term damage of ending QE and ZIRP can’t be known. But that inflection point will come, desired or not; willed or not. It is not avoidable.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/19/2015 - Russell Napier: The War on Cash will cause gold to be used as money again

05/19/2015 - Russell Napier: The War on Cash will cause gold to be used as money again