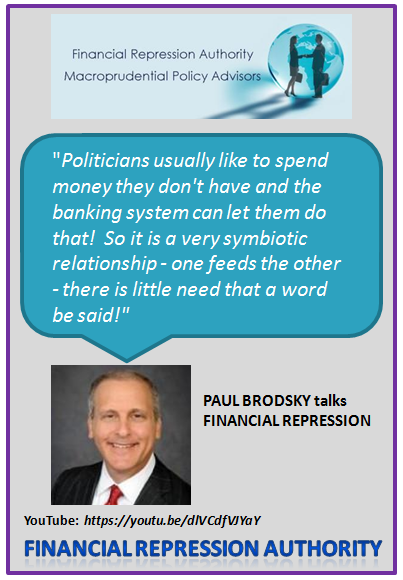

07/16/2015 - James Turk on Financial Repression

07/16/2015 - James Turk on Financial Repression

Special Guest: James Turk – Founder & Managing Director, GoldMoney.com

With a career in International Banking, including managing the Abe Dubai Investment Authority’s Commodities Portfolio, James Turk is an experienced professional whose insights should be thoughtfully considered. He feels strongly that the US needs to return to the sound money principles the framers of the US Constitution outlined and which the US has unfortunately and perilously veered away from.

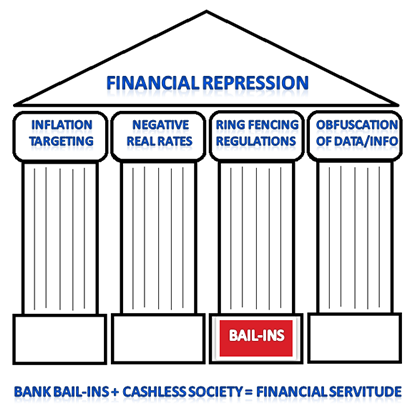

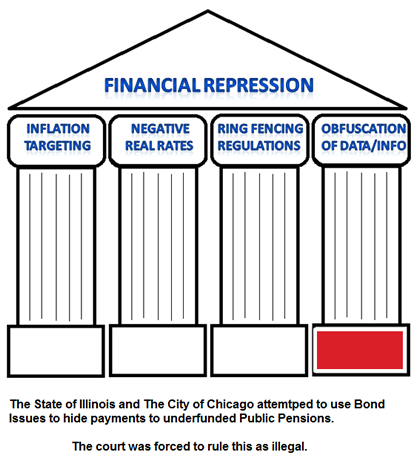

FINANCIAL REPRESSION

“Financial Repression is government intervention in the market system which distorts the market’s signals. …. Government intervention not only distorts the markets but in fact is counter-productive because many times it is government policies which the market are reacting to!”

Instead of changing the policies, governments try and convince the markets (through intervention) that the policies they are following are the correct ones, when in fact they are not.

James feels strongly that governments need to be outside the markets and be primarily focused on maintaining the ‘rule of law’ and ensuring there is a level playing field for competitive capitalism to operate on. Government intervention results in distorting that playing field to the advantage of themselves and their special interests.

“(Governments & Central Banks) are following policies that basically are not sustainable!”

“The government’s ‘make believe’ is that they are creating wealth through creating currency and distributing it through their various programs. That is not creating wealth, but rather debasing the currency. When you debase the currency this is the worst type of financial repression because you are essentially destroying people’s ability to interact entirely voluntarily within the market place, as we fulfill our needs and wants.”

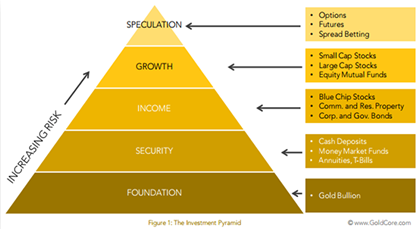

UNDERSTANDING WEALTH

There is only so much wealth in world. It needs to come from somewhere if it is to be distributed in a meaningful way. James Turk believes wealth fundamentally comes in two forms: Tangible Wealth and Financial Wealth.

Financial Wealth comes with counter-party risk and the exposure to insufficient cash-flows required to support the leverage that inevitably comes with pyramiding and the interconnection of financial wealth.

James Turk believes we are presently destroying wealth. Financial Wealth gets destroyed because of the eventuality of insufficient cash-flows (Free DCF) to support the over financialization of the economy.

…. there is much, much more in this fact filled 24 minute Video.

WAR ON CASH & BAIL-INS

- The Holy Alliance

- Perpetuating the Welfare State

- Why we can’t trust the banking sytem anymore.

- How banks have become Hedge Funds versus lending institutions,

- Why we need to separate the banks function of being a payments system versus being investment fund managers.

CRYPTO CURRENCIES

- What is the real purpose is of money,

- How the current environment is a historical aberration. We have moved away from a sound money system as the constitution framed.

- Why we need to return to the wisdom of the framers of the US constitution,

- Why Gold and Silver’s proven historical track record is important.

GoldMoney & BitGold MERGER

- Why GoldMoney and BitGold Merged,

- What James sees the future to be for the merger.