05/01/2016 - Everbank VP: First ZIRP, Then QE .. Will NIRP Be Next In The U.S.?

Everbank’s VP considers the progression of financial repression in the U.S. – from zero interest rate policy to quantitative easing to the increasing potential for negative interest rates .. “In response to disappointing growth, many central banks are testing a new monetary tool: NIRP. The European Central Bank (ECB) was the first major institution of its kind to adopt NIRP. Others have joined the party. Sweden, Denmark, Switzerland and Japan have also adopted sub-zero rates.2 In fact, around a quarter of the world economy by output is now experiencing official rates that are less than zero.3 Will the U.S. be the next country to implement a negative interest rate policy? .. It seems monetary authorities agree that NIRP might be implemented in the U.S. if our economy enters a sharp downturn. This would have important implications for the markets. In fact, the current negative rates in other countries are already having a major impact on certain asset classes, especially on precious metals.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/29/2016 - Anthony Wile: The Emerging Legalized Cannabis Industry and the Rising Latin Star, Colombia.

FRA Co-founder, Gordon T. Long is joined by Anthony Wile, Founding Chairman and CEO of The Wile Group, to discuss the future of the emerging legalized Cannabis Industry on a global scale, along with the war on drugs and the next upcoming star in the global theater, Colombia.

Mr. Anthony Wile, founding Chairman and CEO of The Wile Group Ltd., is an active investor, business strategist and consultant, financial markets commentator, publisher and author. Mr. Wile founded The Daily Bell, where he served as chief editor until February 2016. He now publishes Wile Reports, a free subscription publication with new material from Anthony Wile and occasional introductions to investment opportunities of potential interest that are being supported by The Wile Group. Mr. Wile is the author of High Alert: How the Internet Reformation is causing a financial hurricane – and how to profit from it. Ron Paul has said, “High Alert should be read by everyone who wishes to educate themselves about the dangers fiat money poses to American liberty and prosperity. I wish I could get every member of Congress to read this book.”

WAR ON DRUGS

“I think the entire world is repressed as a service to benefit a very few.”

I believe that people should be able to invest their capital in whatever way they want to. Bottom line is, we should not be trying to organize society in a way that monetarily determines who is and who isn’t capable of making decisions for themselves.

Special Session of the General Assembly UNGASS 2016 – The meeting happened as a results of several factors:

Some sovereign nations have been jumping ahead of international policy and making their own rules and regulations regarding the war on drugs.

Canada is an example of a country that has moved in its own direction to establish a national marketplace for the distribution of medicinal cannabis products.

Canada’s recently elected Prime Minister Trudeau has made it very clear by some time in spring 2017, there will be legislation in place for an adult use recreational cannabis marketplace.

The world is changing in this respect, and rightfully so.

Authorities discuss how to reduce drug use, which surely we can all agree on, is a noble topic to talk about, but more importantly we must ask, how do we reduce the demand? Too much attention is spent on the supply side of the equation. I think it’s important we begin to consider the demand side as well. A major idea is that if you’re going to educate somebody, you need to know who you are talking to. Today the demand side of the industry is unknown other than as a group, an umbrella which you don’t deal with as a whole; rather, you deal with individual people within the system. The regulation of the industry, like it or not, will ensure that the drugs will be maturely distributed, and as a result of that you will get the appropriate data.

“If we open up the system and have a rational understanding that the demand already exists … We are not talking about normalizing drugs; we are talking about creating a highway system that develops the communication ability for those who wish to impart their views on how you should reduce consumption of these products. By doing this you remove the black market from the distribution side, which then cuts off funding to the ‘terrorism’ of the war on drugs.”

If you want to make a change and cease the funding of these illegal organizations throughout the world, then you must simply cut off their funding source. In many cases, these funds are related to the war on drugs. The rest of the world is beginning to realize that the problem can be alleviated through a mature discussion that recognizes human nature being what it is, and that it is individuals who are deciding for themselves to consume these products. We don’t endorse it; we are simply saying that we must get to know who these people are-; profile, understand and get to know people on a personal and real level.

“This is a big boys’ game that will be handled by the big boys when it comes to the determination of what the products are and how they’re distributed.”

Without a doubt there are investment opportunities in this arena, but people should take their time and not rush in. The regulatory environment has not yet shaped itself. That will determine where the profit margin will lie. Big change is coming, for instance, in distribution. Some of the largest associations in Canada have come out saying that they are behind this shift towards a pharmacy distribution model. This immediately puts an “X” over the revenues that would have belonged to the licensed producers in Canada who distribute through the mail. Today they have the whole vertical, but tomorrow they won’t. As a result, those investments are dramatically affected and thus the viability of anybody who invested in those investments.

Areas of negative environmental impact can be alleviated if the focus is on the cultivation in areas that can generate a positive environmental impact. You will see in the coming future that international bodies will be quite focused on the environmental side of this new industry in which the standards can be determined upfront by the private sector with support of agencies that see this is in fact the better way to approach this.

There is a lot of discussion happening at this point in time within the international circles of how best to embrace, monitor, secure and develop international trade in this industry. For investors who want to get involved in this big shift, I suggest to pay attention to the nations that on a production side are leaving a positive environmental footprint, and are producing medicinal-grade products which are standardized at legitimate price points.

COLOMBIA’S ROLE

“In the war on drugs, Colombia has suffered more than any other nation on Earth.”

Colombia desires to rehabilitate its reputation. The aftermath of the war is a way for Colombia to recreate the way they are viewed by the world. The country is far from backwards in regards to their research capabilities. Their universities are top notch. There is more than enough capability and infrastructure for Colombia to establish a new role in the world with respect to their contribution in pharmaceutical products.

The government has paved the way for a legal business to develop in Colombia. Colombia has means to be a world leader in a scientific and technological way for how these products should be standardized, regulated, and distributed and pave the way by example.

BUSINESS OPPORTUNITIES IN COLOMBIA

“I don’t see a country in the world today that offers as much opportunity as Colombia.”

I try to stay away from global stock markets as much as possible. I am more interested in generating real wealth with real businesses that generate positive and sustainable cash flow. We’re focused in private equity and in Colombia. There are so many areas of Colombia which have been sealed off for decades, inaccessible and totally under-explored in terms of natural resources. There is great opportunity for investing – real estate, tourism, a myriad of opportunities exist. I also think the hemp industry in Colombia is going to develop rapidly; we’re conducting due diligence on that now. It is a nation that is about to spring forward in many ways.

ECONOMIC SHIFTS IN SOUTH AMERICA

The Latin American nations surrounding Colombia are unfortunately lagging far behind. They are not learning as much as they should be from the example of Venezuela. After Colombia, the next rising star would be Chile. It is a country that offers reasonable stability, but it is still difficult to compare the opportunities it offers with those of Colombia.

“At the end of the day, the leading nation in Latin America, in terms of growth, opportunity, and economic prosperity, is undoubtedly Colombia.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2016 - Economist Joseph Stiglitz On The Negative Effects Of Financial Repression

Financial Repression Has

Exacerbated “Extreme Inequality”

Economist Joseph Stiglitz discusses the problem of extreme income inequality in the U.S. & the negative economic impact of macroprudential monetary policy .. 4 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2016 - The Portfolio Effects Of Holding Gold Or Gold Mining Stocks In A Portfolio

Bullion Management Group Inc.:

Gold & Gold Stocks

In A Portfolio

Report by Nick Barisheff of Bullion Management Group Inc. on the effects of holding physical gold or gold mining stocks in a portfolio .. “Mining shares are an investment that can make up a small portion of the overall tactical equity allocation of a sophisticated investor’s portfolio. However, the facts show that gold mining shares are not a prudent long-term strategic investment for most individuals. Physical gold has a long history that spans thousands of years, and it should make up a portion of every person’s assets. The world’s wealthiest people hold bullion to protect their wealth. As Doug Casey, author and institutional investor, says, ‘The hurricane hit in 2008, we have been sitting in the eye of the storm since the last financial crisis and the full breadth of the storm is beginning to hit us once again.’ Globally, the problems we face today are markedly worse than those of the Great Recession. In the coming years, portfolios without physical gold to offset losses in financial assets and currencies will suffer.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/27/2016 - Michael Hudson: “THE WALL STREET ECONOMY HAS TAKEN OVER THE ECONOMY & IS DRAINING IT!”

FRA Co-founder Gordon T. Long is joined by Professor Michael Hudson in discussing his concept of the FIRE economy and its influence on the production and consumption economy, along with some of his writings.

Michael Hudson is President of The Institute for the Study of Long-Term Economic Trends (ISLET), a Wall Street Financial Analyst, Distinguished Research Professor of Economics at the University of Missouri, Kansas City and author of Killing the Host (2015), The Bubble and Beyond (2012), Super-Imperialism: The Economic Strategy of American Empire (1968 & 2003), Trade, Development and Foreign Debt (1992 & 2009) and of The Myth of Aid (1971), amongst many others.

ISLET engages in research regarding domestic and international finance, national income and balance-sheet accounting with regard to real estate, and the economic history of the ancient Near East. Michael acts as an economic advisor to governments worldwide including Iceland, Latvia and China on finance and tax law.

FIRE ECONOMY

FIRE is an acronym to the Finance, Insurance, and Real Estate sector. Basically that sector is all about assets, not production and consumption. Most people think of the economy as being producers making goods and services and paying labor to produce them, and then labor is going to buy the goods and services. But this production and consumption is rife in the asset economy of who owns assets and who owns other things.

The Finance, Insurance, and Real Estate sector is dominated by finance. For instance, 70-80% of bank loans in North America and Europe are mortgage loans against real estate. The only way of buying a home or commercial real estate is on credit, so the loan to value ratio goes up steadily, banks lend more to the real estate sector, and real estate is worth whatever banks are willing to lend against it.

As banks loosen credit terms, lower interest rates, take lower down payments and basically lower amortization rates, interest only loans, they’re going to lend more hand more against property.

“Property’s bid up on price, but all of this rise in price is debt leverage.”

A financialized economy is a debt leveraged economy, whether it’s real estate or insurance or just living, and debt leveraging means a larger portion of assets are represented by debt, raising debt-equity ratios, but also that more and more of people’s incomes and tax revenue is paid to creditors. So there’s a flow of revenue from the production and consumption economy into the financial sector.

WE’RE STILL IN CAPITALISM, NOT CREDITISM

There’s a huge amount of gross savings, about 18-19% of the US economy, coded in part in debt. The savings that are lent out to borrowers are debt. So you have the 1% lending out their savings to the 99%, but the gross savings are higher.

“Every economy is a credit economy.”

“The IMF has this Austrian theory that pretends money began as barter and capitalism operates on barter, and this is a disinformation campaign. This is a very modern theory that is basically used to say “oh, debt is bad”, an what they really mean is that public debt is bad, the government shouldn’t create money or deficit, and you should leave it all to the banks who should somehow run off debt and in-debt the economy”.

“You can usually ignore just about everything the IMF says, and if you understand money you’re not going to be hired by the IMF.

They impose austerity programs that they call “stabilization programs” that are actually destabilization programs, almost wherever they’re imposed.

“When you have an error repeated year after year, decade after decade, it’s not really insanity doing the same thing thinking it’ll be different. It’s sanity. It’s doing the same thing thinking the result will be the same again and again.”

The result will be austerity programs making the budget deficit even worse. The successful era of monetarism is to force countries to have self-defeating policies that end up having to privatize their natural resources, public domain, public enterprise, their communications and transportation, and sell it off.

Everything that the classical economists saw and argued for – public investment, bringing costs in line with the actual cost of production – that’s all rejected in favor of a rentier class evolving into an oligarchy. Financiers in the 1% are going to pry away the public domain from the government and privatize it so that they get all of the revenue for themselves. It’s all sucked up to the top of the pyramid, impoverishing the 99%.

“As long as you can avoid studying economics, you know what’s happened. Once you take an economics course you step into the brainwashing of an Orwellian world.”

KILLING THE HOST

Finance has taken over the industrial economy. Instead of banks evolving from usurious organizations that leant to governments, finance was going to be industrialized. They were going to mobilize savings and flow it back into financing the means of production, starting with heavy industry. In Germany in the late 19th century, banks worked with government and industry in a kind of triangular process. But that’s not what’s happening now. After WW1 and especially after WW2, finance reverted to its pre-industrial form and instead of allying themselves with industry, they allied with real estate and monopolies because they realized they can make more money off real estate.

You had David Ricardo arguing against the landed interest in 1817. Now the banks are all in favor of supporting land rent, knowing that today people can buy and sell property, renters are paying interests, and they’re going to get all of the rent.

“You have the banks merge with real estate against industry, against the economy as a whole, and the result is that they’re a part of the overhead process, not part of the production process.”

THE WALL STREET ECONOMY

“The Wall Street economy has taken over the economy and is draining it.”

Instead of the circular flow between producers and consumers, you have more and more of this flow being diverted to pay interest and insurance and rent. In other words, to pay the FIRE sector, most of which is owned by the 1%. The agency is active politicking by the financial interests and the lobbyists on Wall Street to obtain all of the growth of income and wealth for themselves, and that’s what happened in America and Canada since the late 1970s.

INVESTMENT STRATEGIES FOR TODAY

What all the billionaires and heavy investors do is they’re simply trying to preserve their wealth. They’re not trying to make money, they’re not trying to speculate, and if you’re an investor you’re not going to outsmart the billionaires because the markets are basically fixed. It’s the George Soros principle.

“If you have so much money, billions of dollars, you can break the Bank of England. You don’t follow the market, you don’t anticipate it, you actually make the market and push the market up.”

You have to be able to control the prices and you have the insiders making money but the investors are not going to make money.

The Canadians don’t buy stocks until they’re up at the very top and then they lose all the money, and finally when the market’s all the way at the bottom the Canadians begin selling because they can see a trend, and then they miss the upswing.

“J” IS FOR JUNK ECONOMICS

“It begins as a dictionary of terms just so I can provide people with a vocabulary. The vocabulary that is taught to students today, used by the mass media and government spokesmen, is basically a set of euphemisms. Almost all the words we get are kind of euphemisms to conceal the actual dynamics that’s happening. For instance, “business cycles”. Nobody in the 19th century used “business cycle”. They spoke about “crashes”. They know that things go up slowly and then plunge very quickly. It was a crash, not the sine curve you have in Josef Schachter’s business cycle. A cycle is something that is automatic, and if it’s a cycle then you’d think “oh, okay, everything that goes up will come down and everything that goes down will come up, just wait your turn.” And that means you should be passive. That is the opposite of everything that’s said in classical economics in the progressive era, when they realized that economies don’t recover by themselves”.

“You need the government to step in, you need something exogenous, as the economists say. You need something from outside the system to revive it.”

This idea of the business cycle analysis is, somehow you leave out the whole role of government. If you look at neoliberal and Austrian theory, there’s no role of government spending or public investment. And the whole argument of privatization, for instance, is the opposite of what was taught in American business schools in the 19th century.

The first professor of economics at the Wharton School of Business, Simon Patten, said public infrastructure is a fourth factor of production but its role isn’t to make a profit. It’s to lower the cost of public services and basic inputs to lower the cost of living and cost of doing business to make the economy more competitive.

“The privatization of this adds in interest payments, dividends, managerial payments, stock buybacks, and merges and acquisitions, and obviously bills all of these financialized charges into the price system and raises the cost of living and doing business.”

MORE ON FIRE ECONOMICS

We’re going into a debt deflation and the key is to look at debt. If the economy has to spend more and more money, then the reason he economy isn’t recovering isn’t simply because this is a normal cycle.

“It’s not because labour is paid too much, it’s because people are diverting more and more of their income to paying their debts, so they can’t afford to buy goods.”

Markets are shrinking, so real estate rents are shrinking, and profits are shrinking. Instead of using earnings to reinvest, hire more labor to increase production, companies are using their earnings for stock buybacks and dividend payouts to raise the share price so that the managers can take their revenue in the form of bonuses and stocks and live in the short run.

“They’re all setting up to take the money and run, leaving the companies are bankrupt shells, which is pretty much what hedge funds do when they take over companies.”

The financialization of companies is the reverse of everything classical economists were saying. They can get wrap themselves in this cloak of classical economics by dropping history of economic thought from the curriculum. Following the banks and the Austrian school of the banks’ philosophy, that’s the road to serfdom. That’s the road to debt serfdom.

“It lets universities and its government be run by the neoliberals, and they’re a travesty of what real economics is all about.”

Abstract by: Annie Zhou: a2zhou@ryerson.ca

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/24/2016 - Forced Inflation (1 Of The 4 Financial Repression Pillars) Ahead: Rising Commodity Prices

Will Central Banks Bolster

Commodity Markets To Generate Inflation?

Commodity Trader: “The stupid FED and other Central Bankers around the world acting in unison to artificially raise inflation so that they can hopefully get out of the mess they got themselves into with this low/negative rate. Call me crazy, and I am not a ‘conspiracy theorist’ – but what is happening has absolutely no ‘reasonable’ explanation. So I have to think outside the box… The FED and other Central Banks have already destroyed the equity and other macro-financial markets… it is now turn for the commodities markets… How about the fact that the main drag on the inflation figures has been what? What? FOOD & ENERGY… So is it so crazy to think that Central Bankers all got together in early 2016 and came up with the following equation??? ARTIFICIALLY RAISE COMMODITY VALUATIONS = HIGHER ARTIFICIAL INFLATION = CLAMORING FOR RATES TO BE RAISED.” Dr. Albert Friedberg*: “Value considerations have also moved us to establish a long position in a variety of commodities. The value factor here is the proximity of prices to their marginal cost and the concomitant impact on supplies. Slight changes in demand are likely to bring about relatively sustained increases in prices in at least some commodities. Rather than patiently holding on to a group of commodities, a sort of basket approach, we have asked Covenant to select them on the basis of momentum and have given them authority to raise exposure to about 20% of assets. We are quite confident that their time-tested technical abilities will make an excellent contribution if and when our value proposition plays out.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/24/2016 - Jeff Gundlach: “Negative Interest Rates Are The Dumbest Idea Ever”

In an interview on Swiss Finanz und Wirthschaft, fund manager Jeff Gundlach unleashes his frustration on central banks .. “What you see is that the same pattern has been in place since 2012: Hope for growth in the new year that ends up being revised downwards, over and over and over again. But now we have reached the point at which no one bothers anymore about the comedy of predicting 3% real GDP growth. Even nominal GDP growth isn’t probably going to be at 3% this year. Actually, nominal GDP is at a level that has historically been a recessionary level. It isn’t this time because the inflation rate is close to zero. But no one bothers anymore and the Federal Reserve has basically given up.” .. Gundlach thinks the U.S. stock market is overvalued versus other stock markets .. Gundlach likes gold – “Gold is doing fine. It’s preserving capital in the U.S., it’s been making money over the last couple of years for European investors. That’s why I own gold. Because in a negative return environment anything that holds its value or makes a little is good.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/21/2016 - Mish Shedlock: “EXCUSE ME MR. PRESIDENT, IS THAT A JOKE?”

FRA Co-founder Gordon T. Long is joined by Mish Shedlock in discussing the rigging of gold and silver by Deutsche Bank and the reliability of so called “casino banks” and the state of global banking institutions.

Mike Shedlock / Mish is a registered investment advisor representative forSitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. He is also a contributing “professor” on Minyanville, a community site focused on economic and financial education.

POST G20 MEETING

Christine Lagarde is worried about public finance and declared the need to get public finance in order. At the same time, she wants countries to spend more.

She said the “strong” countries need to spend more and used the US as an example, but the US deficit projections don’t look very good. In fact, we can’t find anybody anyplace that does look good.

“It is just a bunch of hooey attempting to show concern while giving countries another reason to go deeper in debt.”

There’s all these emergency meetings happening and causing a lot of rumors.

French President François Hollande had a public meeting recently. He said, “I think things are getting better”, and was interrupted by a journalist who said “Excuse me, Mr. President, is that a joke?”

“That’s just what we need journalists in the US to do; ‘Excuse me Mr. President, is that a joke?'”

All the big Italian banks were gathered and told to chip in to bail out these other banks that were in trouble. What they came up with was a plan to increase the capital on these small banks by €5B Euros. Supposedly this would fix €360B in non-performing loans. There’s also roughly another €180B in bad loans.

“They’re supposed to fix this huge problem with the Italian banking system with €5B. That doesn’t work.”

DEUTSCHE BANK RIGGING GOLD & SILVER

Everyone suspected that they were cheating on gold trading, and they admitted manipulating the gold and silver market in a court of law. It’s like someone commits $100B worth of fraud and get fined $50B and promises to never do it again. That’s not even like paying the full price.

“My position all along was, yes, they’ve been cheating, but where isn’t there cheating… I’m quite positive it’s in both directions.”

Has there been this overall price suppression on gold and silver? Gold got up to €1900/ounce, and silver got to €44-46/ounce, and is now sitting at €15-16. Was there pressure applied by all the banks? Is gold really down or was there manipulation because the banks were generally on the other side of the trade?

“Is gold about where it would be without this manipulation? I don’t know, and nor does anyone else.”

“CASINO BANKS”

What we saw was Deutsche Bank had €500B+ in derivative profits and roughly €480B in current losses, so roughly €20B ahead. On another page they outline all their derivatives positions and it amounted to €21T. That’s a profit of €20B from €21T in notional values. These are values way out of the money and some of it is genuinely off.

“When you’ve got a €21T casino on your balance sheet, it just goes to show you how much banks aren’t banks.”

This has nothing to do with core bank policies and procedures and lending. It’s a derivatives casino and it’s rigged. They admitted rigging gold and silver, they admitted rigging LIBOR, they admitted rigging Euribor.

For all the rigging, they got caught on gold and silver. Their commodities portfolio of derivatives was only a tiny piece of that €21T, compared to €15T in interest rates derivatives or €5T in currency derivatives. Something is clearly wrong with all these casino banks.

The international swaps marketplace is approximately $600T, compared to the US economy of $25 GPD a year. Most of the magnitude is more than the entire global economy. The risk is way greater than everyone thinks, especially with these credit default swaps.

ATLANTA VS NEW YORK FED GDP REPORT

The Atlanta Fed projected 0.1% growth and revised it up to 0.3% but NY Fed says it’s more like 1%. Originally it used to be 1.1% vs 0.1% and now it’s 1% vs 0.3%, and we don’t know which one is right. However, the New York Fed model has all kinds of nebulous things in it that can’t be explained.

Inflation is probably a lot higher in a lot of places than the CPI admits.

When 24% of the CPI is Owner’s Equivalent Rent, that doesn’t make sense. Rents in Cleveland and Illinois have nothing to do with rents in Seattle, or places where the economy is doing a lot better. They average it out and supposedly this is some sort of aggregate number that tells you it only goes up by 1.7%. I don’t believe these prices can aggregated because there is no basket that we can define as suitable for everyone, but this is what the Fed does and everyone hinges on these numbers.

“We’ve got too much inflation, too much wealth concentrated in the hands of all the people making the money, while the average guy is losing out.”

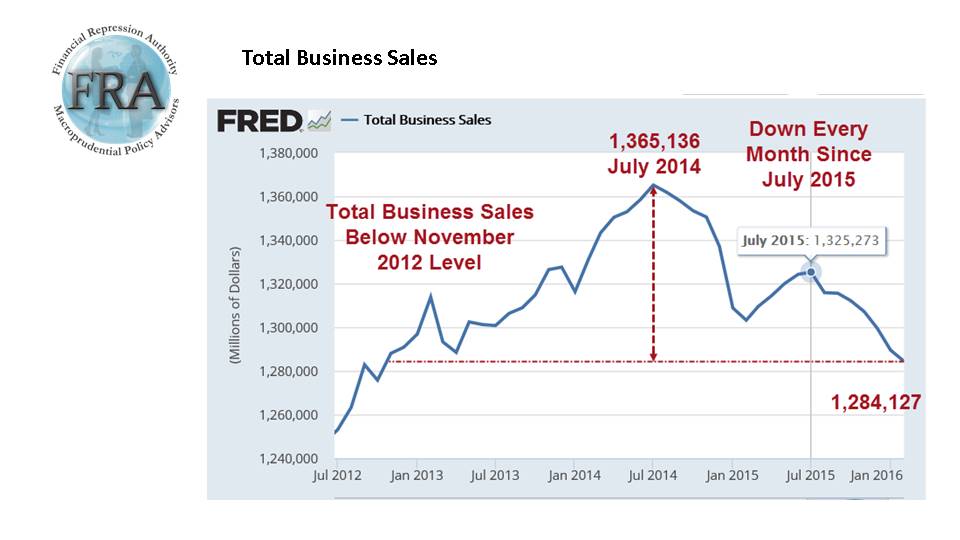

RETAIL CHARTS AND AUTO INVENTORIES

A lot of these charts peaked around November 2014, then there was a little rise back that didn’t recover all of it, and another plunge. Factory sales are down 13 out of the last 16 months, and there’s more things participating now. For instance, auto sales are down 3-4 months in a row. Inventories are at an all-time high. Everyone’s traded in their car; used car inventories are at an all-time high.

35% of all autos sold are on lease, and the residual value of used cars are plummeting. Someone has to take a massive write down since they’re all traded as ABS in the shadow banking system. The US government are the biggest owner of used car assets with $1.1T since they buy all the collateralized loan obligations etc. that go through the government.

LIKLIHOOD OF A RECESSION

“I am still sticking with my forecast that says the recession started in December 2015. I see no reason to revise that.”

We might not know for a year, especially if it’s a small recession. The official harbinger is the NBER, and they get to call when we get it, but we’ve had a recession that ended before they called it. They’re always late. Nothing is coming out of these reports that indicate the call was wrong.

“We’re certainly not in a very strong economy, and there’s no reason to believe it’s going to get any stronger.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/21/2016 - Harry Dent: Stocks Set to Fall 70% By Late 2017 – Gold $400-$800

FRA Co-founder, Gordon T. Long is joined by Harry Dent to have a detailed discussion about the state of the global economy and how investors can be prepare themselves for the turmoils to come.

Harry S. Dent, Jr. is the Founder of Dent Research, an economic forecasting firm specializing in demographic trends. His mission is “Helping People Understand Change”. Using exciting new research developed from years of hands-on business experience, Mr. Dent offers unprecedented and refreshingly understandable tools for seeing the key economic trends that will affect your life, your business, and your investments over the rest of your lifetime.

Mr. Dent is also a best-selling author. In his book The Great Boom Ahead, published in 1992, Mr. Dent stood virtually alone in accurately forecasting the unanticipated boom of the 1990s and the continued expansion into 2007. In his new book, The Demographic Cliff, he continues to educate audiences about his predictions for the next great depression, especially between 2014 and 2019 that he has been forecasting now for 20 years. Mr. Dent is the editor of the Economy & Markets newsletter and has created the HS Dent Financial Advisors Network.

Mr. Dent received his MBA from Harvard Business School, where he was a Baker Scholar and was elected to the Century Club for leadership excellence. At Bain and Company he was a strategy consultant for Fortune 100 companies. He has also been the CEO of several entrepreneurial growth companies and a new venture investor. Since 1988 he has been speaking to executives and investors around the world. He has appeared on “Good Morning America”, PBS, CNBC, CNN, FOX, Bloomberg, and has been featured in USA Today, Barron’s, Investor’s Business Daily, Entrepreneur, Fortune, Success, US News and World Report, Business Week, The Wall Street Journal, American Demographics, Gentlemen’s Quarterly and Omni.

WHAT IS FINANCIAL REPRESSION?

“Financial repression is how the central banks hijack the free market.”

Other than from the aftermath of WWII, this is the first time that governments around the world have just begun frantically printing money to offset the downturns. The most important thing to understand is that central banks do not just set short term rates; they print money and buy their own bonds to set long term rates to zero.

“When you are a baby boomer approaching retirement, due to financial repression you will get zero adjust for inflation returns. Baby boomers are being forced to go into the stock market on higher yield assets and get crucified.”

Pushing long term rates so low forces people to go into stocks and other financial assets as well as allows firms on Wall Street to leverage up. When this happens you get massive misallocation of investment, and have companies borrowing money to buy back their own stocks to engineer mergers that wouldn’t be possible without such low rates. This bubble we are in, which is greater than any we have been in before, is going to burst and when it does it will wipe out all the excess gains. This financial repression is just going to destroy wealth faster than it artificially built up. It comes down to central banks admitting that they created a bubble, but they won’t because nobody wants to take blame for it while they’re in office.

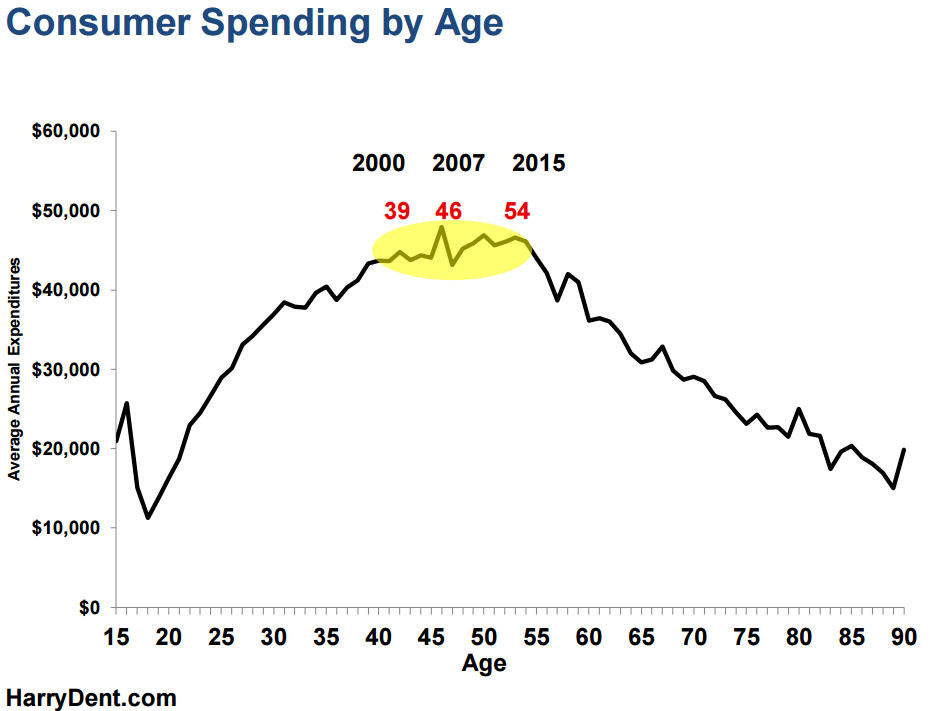

It is a lifetime consumer spending cycle. Most people do not enter the workforce until they’re 20 then they go on a huge spending cycle which eventually slows down at the age of 39 because people buy their largest home well before they peak in spending. We peak at age 46 and continue the trend because of automobile purchasing and especially with QE; the affluent people go to school longer which is followed by their kids and so on. Therefore peak spending for these people happens 6 years later, and it has been magnified due to QE since these are the same people who of the entire population are the ones who tend to own financial assets.

“The combination of financial repression, QE, and extreme income inequality has seriously butchered the middle class in America.”

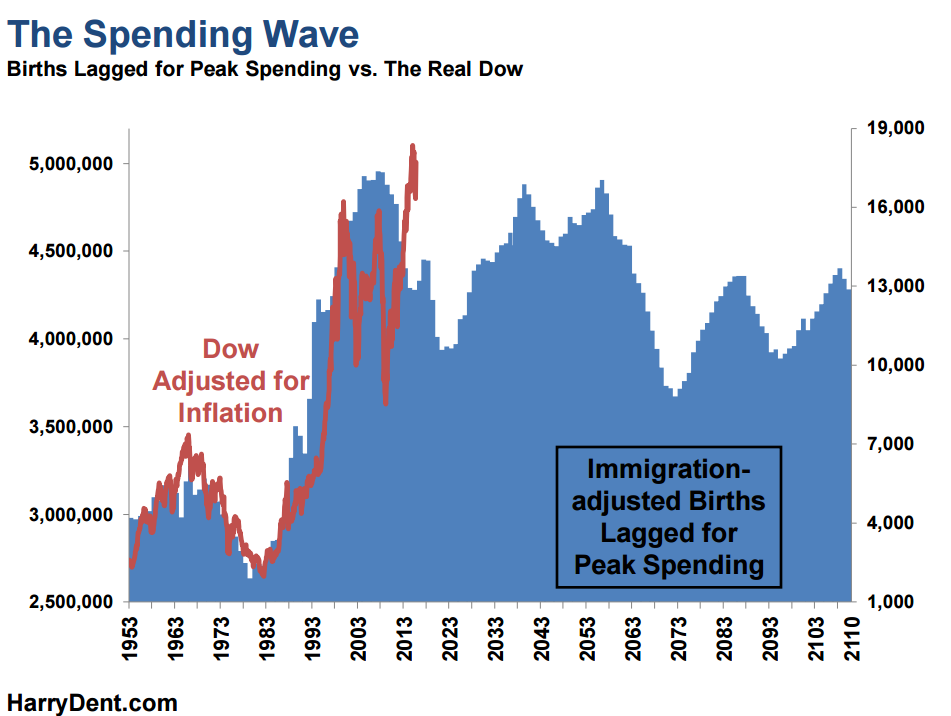

It is a graph of the birth index adjusted for immigration, and then projected forward 46 years for the peak spending of the average person. This is why since 2008 governments have been doing endless QE and stimulus just to keep the bubble going enough so that the affluent people can at least continue spending. This demographic trend will continue to point down until 2022 which is when the next generation comes along. Authorities have been able to hold off the burst as long as they wealthy continue to spend, but they are not anymore.

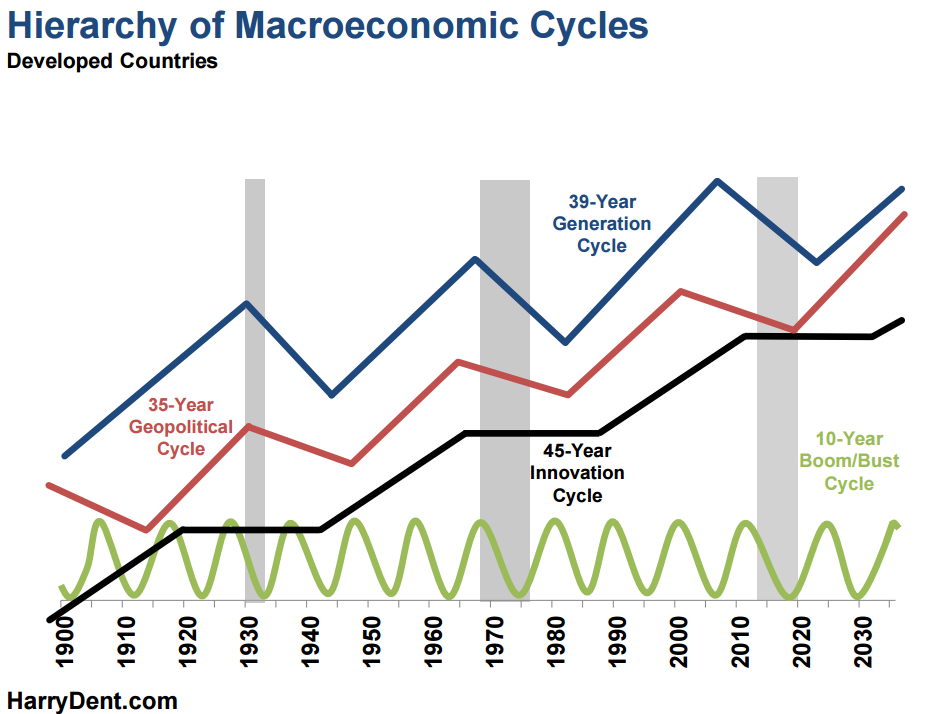

“We are in a bad yield geopolitical cycle, and it is clearly getting worse and it will hit bottom at around 2020.”

The productivity that was created in the 1900s from inventions like the automobile and so on is not present today. Today our economic progression is being backed by Facebook and watching the new viral videos. The point is that these 4 cycles have turned down only twice in the last century before this. It was in the early 1930s, the great depression, and the next major stock crash in the mid 70’s. Governments are fighting the impending crash tooth and nail and have resorted to emergency measures such as zero interest rates and in some cases even negative interest rates.

“This is going to be the final bubble. It’s going to be like the great depression, like the 1974-1975 crash, and without a doubt it will be the worst stock market crash you will see in your lifetime and it is going to happen by roughly end of 2017.”

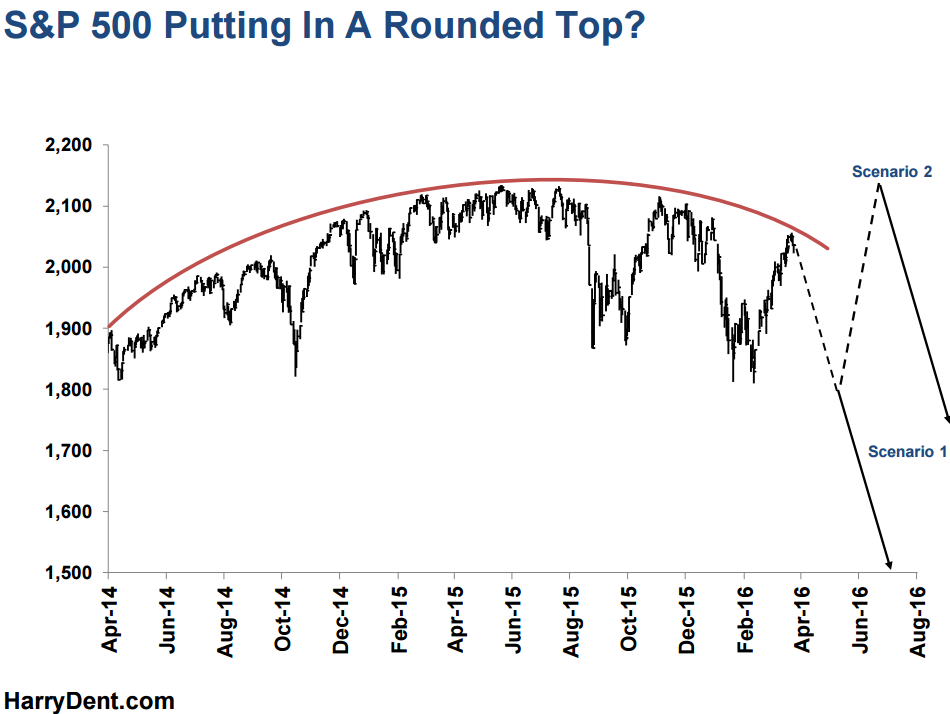

“This chart is for people who intend to sit in the market, hoping to get another 5-10%. From it we can see that since November 2014, we have gone nowhere and we are right now at the bottom of the rounder top and I am confident it will not go up from here.”

Europe going to be in deep trouble. Banks are failing in Italy like no tomorrow, and I predict by end of the year Italy will be the next Greece, effectively marking the end of the Euro Zone. They already have immigration problems, debt problems, and slowing growth despite endless stimulus.

China on the other hand, has the biggest stock market in the world and it crashed by 45% in 2 months, and I predict it is going to crash again by the end of this year. So what can the Fed and central banks in Europe do about that? Once that happens it is going to send a shockwave in commodities and especially real estate, since it is the Chinese after all who are buying all the cutting edge real estate throughout the world.

“The next US President might as well walk into office and openly admit that this is a bubble and talk about actions to deal with it, rather than being like his predecessors and claim job creation and economic growth; there is just no chance.”

HOW CAN INVESTORS PROTECT THEMSELVES?

“Right now you have to get out and do not listen to your stock broker. This is not the time to be taking risk; it is the time to be prudent.”

The idea is to realize that this is a once in a lifetime reset and you have to simply get out of the way. Everything is a bubble that’s ready to pop, just simple get out of risk assets as much as you can. You can either gamble and get 5%-10% return or lose 60%-70% by end of 2017. Bubbles build on denial because everyone benefits, even the average person has a lower mortgage than car payments because of the bubble and zero interest rates. It is because of the fact that everyone benefits that everyone goes in denial.

PRECIOUS METALS AND THE US DOLLAR

“This is a deflationary crisis, and it is the one time that gold will not do well.”

Gold is a bubble as well. Gold went up 8x in 10 years, there are not many bubbles bigger than the gold bubble and now it is bursting. It is bursting because a lot of the gold bubble happened after 2008 as a result of the crisis, and gold went up the most when people thought the massive money printing would lead to inflation but it didn’t. It didn’t because deflation is a trend; when debt bubbles deleverage, money that was created out of thin air disappears. Most of the time in cycles, we either have moderate or extreme inflation, but this is the one time we have deflation and therefore I do not want to be in gold or in commodities.

“The USD has been the best currency; it goes up versus other currencies as it did in 2008. We are still the best house in a bad neighborhood.”

China is going to be the biggest urban disaster in modern history. They have 250 million people that are not even registered citizens working low paying jobs that are primarily focused on building infrastructure for nobody. And when this crash comes, those people are done for.

When stocks crash, price earnings ratios collapse, and risk premiums go up on everything. So if I was in stocks, I would rather be in pharmaceuticals, health and wellness etc. These are the stocks to buy when the Dow goes down to 5500.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/18/2016 - BlackRock’s Larry Fink: The “Biggest Crisis” In The World – Negative & Low Interest Rates

BlackRock’s Larry Fink:

This Is The “Biggest Crisis” In The World

Fink is worried that negative & low interest rates around the world are crushing savers & that those policies are going to become the biggest crisis globally .. “We have become too dependent on central bankers” to boost the global economies, stressing easy money policies were supposed to be a temporary healing .. Over 70% of our clients are retirement plans and insurance plans. Our clients are in pain .. Our clients are very worried how they’re going to be meet their liabilities” because the yields are so low in the bond market.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/18/2016 - Kyle Bass: The Looming “Run On Cash”

“I think this is where the academics are clashing with the practitioners. On paper, negative rates make a lot of sense if you’re running academic models, but in reality they make no sense. Having seven or eight trillion dollars of debt trading at negative rates, having thirty year JGB’s trading at fifty basis points is absolutely ludicrous. This experiment that’s going on will end poorly at some point in time, I just don’t know when that time is .. I think that one of the fears that they have is a run on cash. If they told you and me that they’re going to tax your deposits by a hundred basis points, well it’s better to put it in a safe or under your mattress. And that’s why you see a resurgence in gold. The more they move to negative rates, the more gold is gonna take off because there’s no carrying cost.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/13/2016 - Jeff Berwick: “THEY’RE TRYING TO BRING EVERYONE INTO THE BANKING SYSTEM SO THEY CAN ESTABLISH A ONE-WORLD CENTRAL BANK & TAXATION SYSTEM!”

Jeff Berwick is the founder of The Dollar Vigilante, CEO of TDV Media & Services and host of the popular video podcast, Anarchast. Jeff is a prominent speaker at many of the world’s freedom, investment and gold conferences including his own, Anarchapulco, as well as regularly in the media including CNBC, Bloomberg and Fox Business.

Jeff’s background in the financial markets dates back to his founding of Canada’s largest financial website, Stockhouse.com, in 1994. In the late ‘90s the company expanded worldwide into 8 different countries and had 250 employees and a market capitalization of $240 million USD at the peak of the “tech bubble”. To this day more than a million investors use Stockhouse.com for investment information every month. He has since started numerous businesses including TDV Offshore and TDV Wealth Management to help others internationalize their assets.

FIAT CURRENCIES AND BITCOIN

There’s going to be a lot of chaos this year, beginning in January with the worst first month of the world stock market in history. A lot of financial leads have been warning about it, even saying this is a debt jubilee and will end up in utter collapse if people aren’t careful.

“I think by 2018 they’ll be bringing in a one world currency… All Fiat currencies, including the US Dollar, are going to collapse sometime between 2015-2020.”

The market came up with a solution. Launched in 2009, Bitcoin is a free market currency, and one of the ways that we can avoid this total collapse.

RESPONSE TO AMBROSE-EVANS PRITCHARD

“It looked like a propaganda piece, like it was written by the Bank of England as a press release.”

In no way does this new central bank crypto-currency compete or defeat Bitcoin in any way. In fact, central banks are extremely worried about Bitcoin. They’re trying to bring everyone into the banking system so they can establish a one-world central bank and taxation system. They planned to create a system that impoverishes people to get the wealth into the hands of the 0.0001%.

They want to collapse the entire system so they can bring in a new system. We’re reaching the end of that plan, when every government is insolvent with debt. The US Federal Reserve has essential kept interest rates at zero for eight years, because if interest rates rise the US government would quickly be insolvent.

“With $19T worth of debt, if the interest rate rose to 10%, a very low level, that’d be almost $2T a year in interest payments alone.”

They’re trying to delay that and get everyone into the banking system first. If you try to open a new bank account, it’s very difficult and they want to know every detail because it’s going into a central database so no one can evade taxes. Then they’re going to go even further with negative interest rates and really impoverish people.

If people start getting into Bitcoin, they can’t control it. The only way would be to turn off the internet or the power.

BITCOIN

Bitcoin is an internet-based currency that’s completely decentralized. To get rid of it, they’d have to remove it from the millions of computers around the world, and that’s almost impossible. If you control the money supply, you control the governments. That’s what the Federal Reserve and all central banks do.

“The governments do not control the big decisions. It’s the people behind the scenes who control the money, who tell the government what they want done, and that’s been going on for decades.”

Bitcoin cannot be fraudulent because it’s open-source software. Anyone who wants to can look at the code. There’s no CEO, there’s no central office, and it’s on so many computers they can’t stop it. Central banks want to tax everything and control the economy.

“I don’t call things like Bitcoin a revolution so much as an evolution. It’s creating something that circumvents the entire system completely.”

BLOCKCHAIN TECHNOLOGY

Blockchain type technology could change everything, and goes beyond just money. This could be where everything is based. This technology is also starting to being used be for governance, starting in Africa, as a system of private property. Eventually it could be used to replace the government.

“Your average person still doesn’t know what a big deal is going on behind the scenes, but this is going to revolutionize the world… There’s going to be so many things built on top of this technology that it’s going to change the world.”

BACK TO THE ARTICLE – RSCOIN

Central banks will get rid of fiat currency and use RSCoin instead, but since it’s a crypto-currency it can be tracked even more. The population will likely use it, but it does not “beat Bitcoin at its own game”.

RSCoin will supposedly be good as it gives the government and central bank more control over the money system, and this will apparently make us less prone to boom-bust cycles. However, the central bank’s control over interest rates is what creates boom-bust cycles in the first place.

THOUGHTS FOR THE FUTURE

You want to get your assets out of the banking system, especially anti-system sorts of investments and trades and speculations, ad moving assets out of your own country.

“You want to get assets internationalized. That’s the new diversification in my opinion: not stocks, bonds, or cash, it’s where your assets are, in what countries are they, and under what structures are they.”

We’re headed for a collapse, and how it plays out is anyone’s guess. This is going to be a time talked about in history for centuries, after the collapse happens. We have a global fiat currency that is just computer bits controlled by central bankers with no intrinsic value, and they will return to that.

“Do your own research. There’ a lot more going on out there than most people know.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/12/2016 - Bill Gross: Negative Interest Rates Destroy Savers – The Bedrock of Capitalism

“This reality has profound implications for economic growth: consumers saving for retirement need to reduce spending… A monetary policy intended to spark growth, then, in fact, risks reducing consumer spending.” – Larry Fink, Blackrock “So where does that leave our economy? In the developed financial economies, as a bloc, lowering interest rates to near zero has produced negative consequences. The best examples of this include the business models of insurance companies and pension funds. Insurers have long-term liabilities and base their death benefits, and even health benefits, on earning a certain rate of interest on their premium dollars. When that rate is zero or close to it, their model is destroyed. To use another example, California bases its current and future pension payments to civil workers on an estimated future return of 8% or so from bonds and stocks. But when bonds return 1% or 2%, or nothing in Germany’s case, what happens? We’ve seen the difficulties that Puerto Rico, Detroit, and Illinois have faced paying their debts. Now consider mom and pop and other people who read Barron’s. They are saving for retirement and to put their kids through college. They might have depended on a historic 8%-like return from stocks and bonds. Well, sorry. When interest rates get to zero—and that isn’t the endpoint; they could go negative—savers are destroyed. And savers are the bedrock of capitalism. Savers allow investment, and investment produces growth.” – Bill Gross*, Janus

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

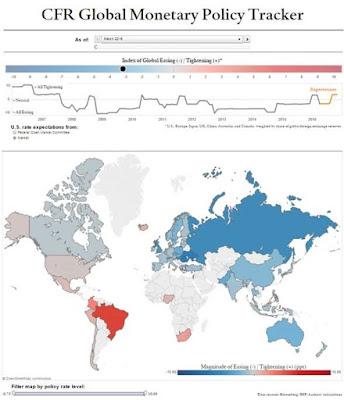

04/12/2016 - Macroprudential Policy Tool

The CFR Global Monetary Policy Tracker is an innovative visual interactive that allows you to see quickly & easily what the world’s central banks are doing at any point in time, individually & in aggregate. All on one screen .. click on the image to activate

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

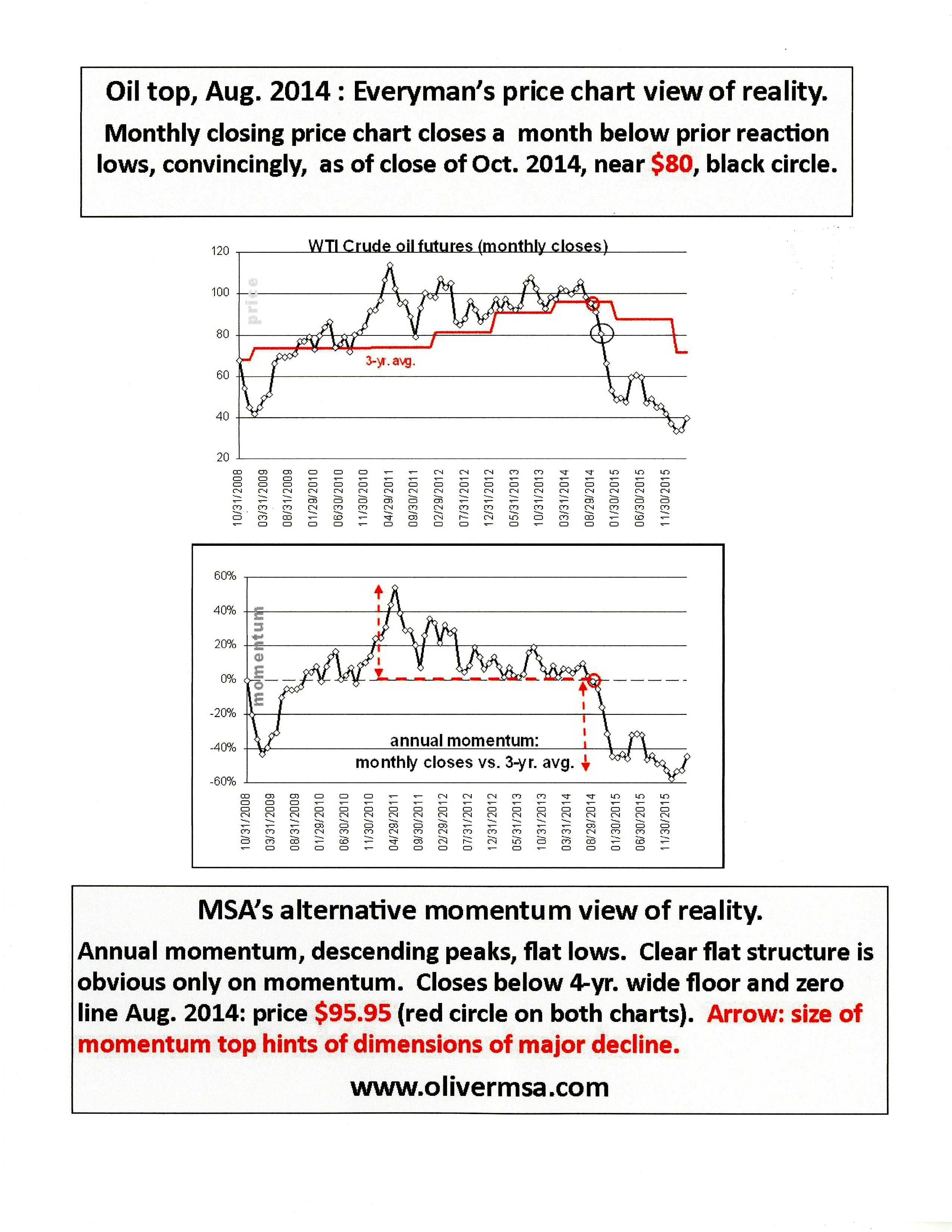

04/10/2016 - Michael Oliver – LIBERTARIANISM, AUSTRIAN ECONOMICS & MOMENTUM STRUCTURAL ANALYSIS – Part II – Analytics

This is the second installment of a two part series in which FRA Co-founder, Gordon T. Long and Michael Oliver, Founder of Momentum Structural Analysis (MSA) break down momentum charts and their unique distinctions in understanding the foundations of Momentum Structural Analysis.

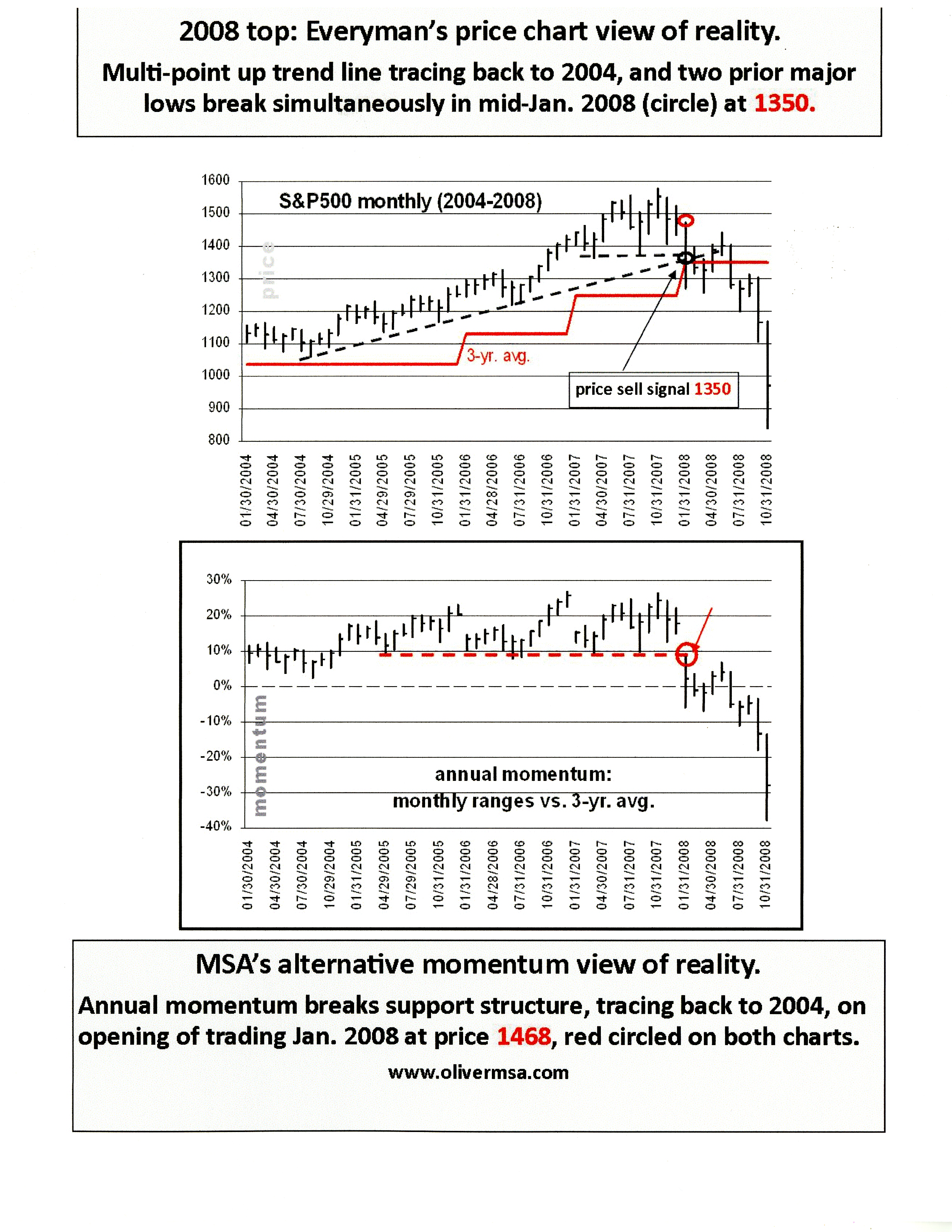

“What we do is we measure means; we do not just lay a moving average on a price chart which doesn’t help at all. One of the great things that momentum analysis does is it finds repetitive market action which can be seen better compared to looking at a price chart. MSA is always focused on the different trends a market might have because markets never have one trend. They may have long term trends which within them consist of counter-cyclical sub-trends which if you’re are not cognizant of can really hurt you. What we try to do with momentum is, since we cannot totally ignore price because it is nonetheless part of the momentum measuring process, we measure price bars in relation to averages of our choice. We oscillate monthly bars in relation to the averages and we get a visual construct of the market once we create the momentum chart which often reveals alarming data.”

Price is comfortably at the high points and far away from any major pivotal lows but from looking at the momentum chart once you break the structure, the rally that followed confides itself to the underlying side of the violated momentum chart.

“The market was a dead man walking and all it was doing from January to august was bumping his head on something he couldn’t get through and finally he just gave up. “

If you were going into an asset that couldn’t be dumped overnight but you had to have committee meetings etc. annual momentum gave you the warning. It gave you time to reorient yourself to the new reality.

At this point annual momentum had not broken down, so all the activity at point 1500 was lateral action in price and momentum. But from looking at the price chart, you could plot an uptrend line going back to a pivotal low in 2004 and connect it with other lows giving you a good price chart trend line. And still sticking to price, you could draw a horizontal line through the two lows of 2007 which gives you these two lines converging. When you opened in Jan 2008 you were almost 100 points above the low in August, giving you a cushion.

On momentum however, you opened below the flow, so again the situation where the moving average changed and you opened at the wrong place at the wrong time. Even the price chart accommodated the break in annual momentum, but as soon as price lows are removed and you ran stops, the market became ‘oversold.’ This instance leads to a double digit percent rally, the rally is inconsequential to momentum but important to price.

In present case, the rally will likely play around in the upper 2000s, not making a new high. If this rally is similar to the rallies in 2008, which occurred after price came down and joined momentum, took out previous price lows and made the picture very clear that you’re in a bear market.

“It is a fact you have to live with; tops especially in stocks are tough to catch.”

Gold is up 17% in the year thus far and this shift is quite significant when you put it on a momentum chart based on spreads. When you plot all these variables together, I predict many seismic shifts to occur, and not just stock declines, but upturns in gold as well.

“Right now I believe we are in a bear market and this is a bear market rally. It is also important to not just look at a market; you have to look at things that are inverse or related to it. I would therefore look at gold and commodities in their relationship to the S&P.”

Many price chart advocates would look at gold and say you’re having problems from being against a channel top, but on the contrary momentum says that same channel tops will be transitory.

“If oil collapsed in 2012 versus when it really did in 2014, it would have severely damaged the stock market, particularly the S&P. Oil waited until the latter part of 2014 which is the same time the S&P began going sideways and which is also where we are now. In effect, by oil holding off, it held back its need to replenish.”

From looking at the price chart you see a sideways action of sorts, but you can interpret it as a price chart advocate as a basing action preceding another leg up, the lows were rising more rapidly than the highs. Then coming down in the late summer, you managed to close below the 3 year moving average. This average was important because in the years prior to 2014, there were a few pullbacks to this average which held throughout. When you convert this to the momentum chart, it shows a descending pattern.

Now what is going on in oil is that you’re building a base. It is possible the low that was made last month as well as the addition of the rally is a setup for a potential final low. When you look at quarterly momentum you see a major pending upside breakout. From looking at the momentum chart you would be shocked. But for this to happen you have to firstly finish the downside, and once that happens and oil closes at any month in the current quarter at $41.20 or higher then you have broken out of quarterly momentum leading me to believe oil will go to roughly $60.

“Now what I am looking at is lesser time scales, even weeklies and trying to find a credible downturn that indicates the rally is over.”

In 2011 people were very comfortable in believing gold was in a congestion zone. For the next year it teetered sideways, and was rationalized to be the next leg for the upside. The problem was that in January you have this price drop from late 2011 to a low in 2012. But when you came down in January, it didn’t do any damage to the price chart but it created an uptrend line on the annual momentum chart and it also took out a major previous low on gold. After this there was a mass amount of time where price didn’t break down, it oscillated until finally in 2013 momentum broke down in a decaying pattern.

Ever since the summer lows in 2013, gold has gently oscillated downwards but also came above that level repeatedly, so we can interpret this level as a midpoint. But during the decline in gold in 2013, most people were looking for collapses but we were not.

Looking at the momentum chart you see a different picture, you see horizontal action. The point at which momentum broke through that base was when price reached 1140-1160, a level well below the current market.

“I think gold has broken out on annual and quarterly momentum; it has paid its dues and I’m getting secondary evidence from foreign exchange. I believe now is a time to be long gold stocks more than gold.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/10/2016 - Michael Oliver – LIBERTARIANISM, AUSTRIAN ECONOMICS & MOMENTUM STRUCTURAL ANALYSIS – Part I – Philosophy

This is the first installment in a two part series in which FRA Co-founder Gordon T. Long delineates the foundations for Momentum Structural Analysis with Michael Oliver, Founder of Momentum Structural Analysis (MSA).

Michael Oliver entered the financial services industry in 1975 on the Futures side, joining E.F. Hutton’s International Commodity Division, headquartered in New York City’s Battery Park. He studied under David Johnston, head of Hutton’s Commodity Division and Chairman of the COMEX. In the 1980’s Oliver began to develop his own momentum-based method of technical analysis. He learned early on that orthodox “price chart technical analysis” left many unanswered questions and too often deceived those who trusted in price chart “breakouts,” support/resistance etc.

In 1987 Oliver, along with his futures client accounts (Oliver had trading POA) technically anticipated and captured the Crash. At that point Oliver began to realize that his emergent momentum-structural-based tools should be further developed into a full analytic methodology. In 1992 he was asked by the Financial VP and head of Wachovia Bank’s Trust Department, then headquartered in Winston-Salem, NC, to provide soft dollar research to Wachovia. Within a year Oliver shifted from brokerage to full-time technical research. Oliver is the author of The New Libertarianism: Anarcho-Capitalism and has lead MSA in providing its proprietary technical research services to financial and asset management clients continually since 1992.

“Everybody thinks they have a handle on what momentum means. If you’re a momentum trader that means you chase ups and downs, and this is not what I do. Price in many aspects is delusional, so I de-trend price and look at price through its momentum action; I create momentum charts and analyze that, then reference price secondarily.”

MOMENTUM STRUCTURAL ANALYSIS

The core of technical analysis is very much outdated for it being based on price chart analysis. It is about time for a change, while it is better than fundamental analysis in some respects there is still many deficiencies embedded in price chart analysis which are overcome through momentum structural analysis.

“It is important to realize that Austrian economists are the key bulwark against central banks. They are very important, and have good analysis which I always agree with, however their timing is lacking and that’s where I come in. It is one thing to be right, and another to be right in a timely manner.”

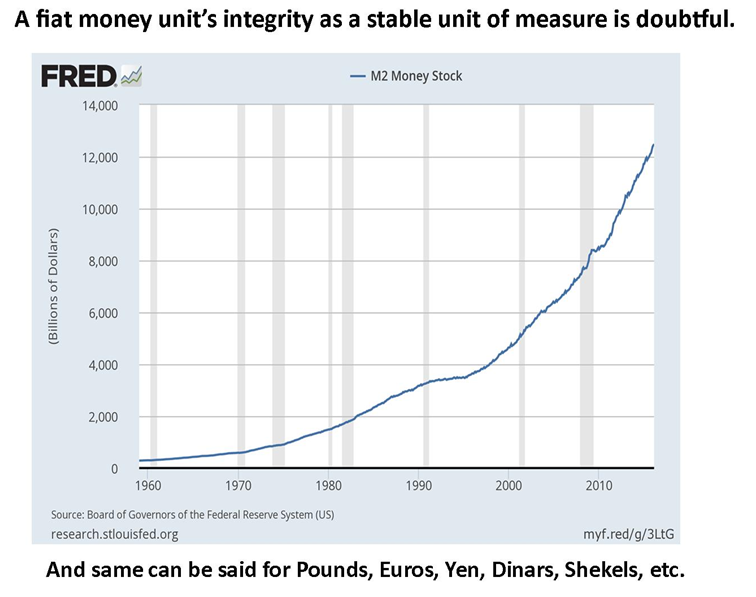

One concept which I adhere to which is pre-politics and pre-economics, is that man is a conceptual being. Man formulates concepts, ideas, circumstances etc. with an underlying basis of some sort of measurement. But there is always a unit of measurement which man needs to build concepts around so that these concepts have consistent validity overtime.

It is essential to have a unit of measurement which remains stable; from this stability you begin to measure and form concepts. The problem with the financial world is that we all use measurements in dollars and it is by no means a stable measurement. Additionally the growth in dollars within the economy is not distributed uniformly everywhere, investors have preferences which tend to shift. Because of this, this unit of measure, the dollar, has to be views with extreme skepticism; you cannot introduce meager metrics like the CPI to compensate.

A well-known orthodox technician, Bob Farrell had 10 rules of investing and #1 was ‘markets always return to the mean.’ This is a widely accepted assumption and a widely overlooked one by trend followers.

“Markets breathe, and failure to acknowledge this is suicide.”

What we do is we measure means; we do not just lay a moving average on a price chart which doesn’t help at all. One of the great things that momentum analysis does is it finds repetitive market action which can be seen better compared to looking at a price chart. MSA is always focused on the different trends a market might have because markets never have one trend. They may have long term trends which within them consist of countercyclical sub-trends which if you’re are not cognisant of can really hurt you.

What we try to do with momentum is, since we cannot totally ignore price because it is nonetheless part of the momentum measuring process, we measure price bars in relation to averages of our choice. We oscillate monthly bars in relation to the averages and we get a visual construct of the market once we create the momentum chart which often reveals alarming data.

“You get a totally different view of the trend reality in the market when you see it through a momentum chart versus a price chart.”

Where momentum plays its greatest role and it is also where most money is lost or made is at the market peaks and bottoms. This is where you experience great swings to your benefit or to your loss.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/08/2016 - Economist Satyajit Das On The Implications Of Negative Interest Rates & Banning Cash

Economist Satyajit Das sees negative interest rates as a radical move by central bankers .. Why would investors go along? There are several possible reasons: 1. Security & safety: Government bonds or insured bank deposits are backed by the full faith & credit of a sovereign nation, which has the ability to issue currency to make repayments. 2. Returns are relative: In Europe, for example, purchasing bonds yielding more that the official rate at the central bank — even if it is negative — is the least worst alternative. 3. Speculation: Investors may be attracted by the opportunity for capital gains from price appreciation if they expect yields to become even more negative. Foreign investors also may be attracted by possible currency appreciation. 4. Real returns: Investors may favor real return over nominal return. Bonds with nominal low- or negative return may preserve or increase purchasing power in situations where the expected deflation is greater than the negative yield, providing positive real yield. 5. Investment mandate: Fund managers may be forced to purchase negative yielding bonds, irrespective of the fact that it locks in a loss. 6. Banks’ and insurers’ mandate:Financial institutions may be forced to purchase negative yielding securities, given liquidity regulations that require these entities to hold high-quality securities. 7. Central banks’ mandate: Central banks with restricted investment choices are also buyers of negative-yielding securities. “The most radical consequence of negative rates would be the abolition of cash itself. In a future economic or financial crisis, current low rates would restrict the effectiveness of monetary policy. Enhancing the ability to use negative rates would provide central banks with additional flexibility and tools to deal with a slowdown. This would be an imaginative, rapid, and durable mechanism for levying negative rates to confiscate savings. Abolishing cash would require a revolutionary change. Despite the increasing acceptance of electronic payment, cash is still extensively used throughout the world In effect, currency remains an important medium of exchange and means of payment for legitimate, legal transactions. Cash use is especially high among both poor and older people. Accordingly, the elimination of currency would have implications for social and financial exclusion. The cost of converting these users to digital payments would be substantial .. Banishing cash would likely meet stiff resistance. People are likely to object to the loss of the anonymity and privacy that cash provides. Where the elimination of cash is linked to negative rates, it would be seen as a tax on savers and the state confiscation of savings. The intrusion of the state and authorities on such a mass scale would undoubtedly become an explosive political issue.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/07/2016 - James Rickards: “The only way every currency can get cheaper at the same time, is not against themselves, but against Gold!”

James Rickards, Chief Global Strategist at West Shore Funds and a widely renowned author is interviewed by FRA Co-founder Gordon T. Long in which they discuss Jim’s just released book The New Case for Gold. They also delve into issues concerning the false perceptions of the world switching back to a Gold Standard and the reasons for a suspected G-20 stealth “Shanghai Accord”.

THE NEW CASE FOR GOLD

James Rickards suggests that there is a new case for Gold and points out that everyone thinks that what they own currently, in terms of stocks, bonds and other financial securities, is actually only “electronic digits” representing claims on assets. The new reality of Cyber war and Cyber attack suggests the real possibility of a single group of people or political regime hacking U.S servers. The potential exists today for investors to lose wealth and there will be almost nothing any one can do to bring back that money, at least in any realistic period of time. Physical Gold cannot be hacked nor simply be erased from the world’s ledger. It is the most tangible and secure way of preserving wealth and James recommends a portfolio with at least 10% being allocated to physical Gold.

Being outside the system, and being non-digital are the two main reasons that smart investors economists suggest will ensure having some sort of security for your wealth. Gold meets both these requirements and in the next big financial crisis will provide you with insurance for the rest of your portfolio.

“They’re not going to bailout the system; they’re going to lockdown the system”

OUTSIDE THE BANKING SYSTEM – The Best Kind if Insurance

The financial system is inherently unstable based on:

1-Complexity Theory and

2- Financialization,

Gold acts as an insurance policy no matter what happens:

1-Inflation,

2-Deflation,

3-Bank failures, and

4-Bail-ins.

Gold is always gold – It’s outside the banking system, can’t be reproduced by fiat, It cannot be “hacked”.

“It is one of the few asset classes that perform well in both inflation and deflation. That is the best kind of insurance,”

Jim talks to FRA about methodically dispelling the decades old arguments and fallacies associated with going back to the Gold Standard. He additionally dispels myths such as:

That John Maynard Keynes Called gold a “barbarous relic” (he didn’t),

That there is not enough gold to support finance and commerce (there is, it depends on the price),

That the gold supply does not grow fast enough to support world growth (it does if we are looking at real growth),

That gold caused the Great Depression (it didn’t, it was the Fed in charge of managing the money supply),

That gold has no intrinsic value (it doesn’t but neither has the theory of intrinsic value).

GOLD IS STILL A MONETARY ASSET & REAL MONEY

Rickards feels that over 40 years of “un-education or mis-education” has resulted in the new generation of economists and youth not understanding the importance or the value behind why gold is so important for our economy. We cannot blame the new generation for this gap inn their knowledge. We have not been teaching Gold as money in university curriculum and along with myths created about gold have virtually disowning it from economic thinking.

“The only way every currency can get cheaper at the same time is not against each other, but against Gold.”

Gold is the one form of monetary value that can’t fight back which is why they have completely stopped educating the U.S public on Gold as a whole.

A POST MONETARY RESET – Gold after the Next Crisis

The current financial system is inherently unstable and may soon have to be reformed. Gold will play a prominent role, if that happens.

The IMF is the third largest holder of official gold reserves after the United States. Gold is at the very center of international finance as the International Monetary Fund (IMF) with its Special Drawing Rights (SDR) reserve currency is regaining prominence. In addition, the current valuation of the SDR could not be calculated without using gold, even though one has to go back to the 1970s to understand why.

China is not only acquiring vast quantities of physical gold, it is also going through the hassle of infiltrating the London gold market and simultaneously setting up its own clearing mechanism in Shanghai. Russia has boosted its gold to GDP ratio to 2.7 percent, higher than the United States percentage of 1.7 percent.

All powers are acquiring gold to have some bargaining power when the international financial system will be reformed.

“The gold to GDP ratio will be critical when the monetary system collapses because it will form the basis for any monetary reset and the new ‘rules of the game.’”

Why? After redistributing the official gold holdings and having monetized everything from bonds to stocks, the world’s governments and central banks won’t have a choice left other than to devalue paper money compared to gold, the same trick President Roosevelt used during the great depression and with the same objective of getting rid of an unsustainable debt burden.

In a monetary reset, gold will be the chips that are used to play a game of poker. Russians, Chinese and even the Iranians are stock piling gold because of this fear. If Gold has a role in the future monetary system, Gold’s price has to go up. Gold cannot multiply at the alarming rate that we will need it for. But we can always increase the price which is why the current monetary system will fail in terms of Gold in the future and will still hold the parity between money supply and demand. James expects a price target of $10,000 for the future if this falls in line.

“You want some assets in TANGIBLE ASSETS!”

James new book The New Case for Gold is available in stores and online now and provides an in-depth analysis on the old and new reasons for why Gold is a necessity in our upcoming monetary system. As always for more analysis and interviews follow us on twitter @FRAuthority or Subscribe to our YouTube channel, Financial Repression Authority for weekly interviews.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/07/2016 - Stanley Druckenmiller On The Importance Of Monitoring Central Bank Macroprudential Policies & Global Liquidity When Investing

Global Liquidity Update –

Japan, Euro Area, &

Emerging Markets All Negative

Financial Sense posted article quotes Stanley Druckenmiller on the importance of monitoring central bank policies & global liquidity levels/movements in the investment process: “Earnings don’t move the overall market… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.” .. the article highlights global liquidity conditions – as measured by BofA Merrill Lynch’s Global Liquidity Tracker, – it shows that global liquidity is still firmly in negative territory as of mid-2015 (bottom panel in the above chart). The most recent data shows a steep drop related to Japan, with 3 of the 4 components (Japan, Euro Area, & Emerging Markets) now below zero. Though the U.S. is fractionally positive at 0.75, the continual tightening of liquidity conditions abroad is the greatest risk currently, aligning with Yellen’s cautious remarks on raising rates. From Bloomberg: “Our real-time Global Liquidity Tracker (GLT) is a composite indicator of liquidity conditions in emerging and developed economies. To estimate our GLT indicator, we employ a dynamic factor model used by global central banks. Our Liquidity Tracker extracts a common unobserved factor reflecting the greatest common variation among market spreads, asset prices, monetary and credit data across different frequencies. We combine our US, Euro area, Japan and EM Liquidity trackers into a global composite using financial weights reflecting the average relevance of an economy in terms of market capitalization and private sector credit. All of this allows us to produce timely estimates of liquidity conditions in an effort to assess the state of the global economy. A reading of zero indicates liquidity at its long-run average while activity between -3 and +3 represents the standard deviation from this average.” Bottom line from the Financial Sense article: “Overall global liquidity conditions are still unfavorable and show increased risks abroad. Japan has seen the greatest deterioration recently, but all components aside from the U.S. are now moving lower into negative (below average) territory. Should this trend continue, the Fed will have ample justification to delay raising rates or, worst-case scenario, eventually be forced to provide liquidity.” LINK HERE to the article

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

“Some politicians want to ban cash .. The first steps in that direction are the withdrawal of big denomination notes and the limits imposed on cash payments ..There is no convincing proof for the claim that the world without cash will be a better one. Even if undesirable behavior is indeed financed by cash, you still need to answer the question: will the undesirable behavior disappear without cash? Or will those who commit the undesirable acts take to new ways and means to reach their goal? .. The plan to restrict the use of cash, or to abolish it step by step, has nothing to do with the fight against crime. The real reason is that states (and their central banks) want to introduce negative interest rates. Although central banks have long pursued inflationary policies that devalue the debt owed by governments, negative interest rates offer a new and powerful tool to do this. But, to make negative interest rates work well, you have to get rid of physical cash. Otherwise, if you apply negative rates on bank deposits, customers in the short or long run will try to avoid the costs that negative rates impose on their bank deposits. So, depositors will, in many cases, hoard cash. To block this last escape route, proponents of the ban on cash want to do away with it. Banning cash is infringing on the freedom of citizens on a massive scale. In withdrawing cash, the citizen is bereft of choice for his payments. After all, the state has the monopoly on the production of money. There is no competition on cash. Thus, nobody but the state can satisfy the demand for money by citizens. The plan to ban cash — step by step — is a sign of the fundamental ailment of our time: the state is destroying more and more of the freedom of citizens and businesses, once it has turned into a territorial monopolist and highest judge of all conflicts. The fight to keep cash may bring something good though: it will shed light on the need to take the power away from the state as we know it, by applying the same principles of law on its actions as on those of each and every citizen. That way, the state’s monopoly on producing cash would come to an end and the citizen wouldn’t need to worry that he may be deprived of his cash against his will.” – Thorsten Polleit, Austrian School Economist

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/01/2016 - Everbank VP: First ZIRP, Then QE .. Will NIRP Be Next In The U.S.?

05/01/2016 - Everbank VP: First ZIRP, Then QE .. Will NIRP Be Next In The U.S.?