The Dallas Texas pension fund is in trouble – the mayor there is warning of 130% property tax hikes will be necessary to avoid a collapse of the pension fund .. it’s the unintended consequences of financial repression .. “Over the past year, the biggest casualty to emerge as a result of global NIRP (or close to it) monetary policy have been pension funds, which have had two choices: either suffer losses as yields on new fixed income investments barely cover (and in some case don’t), or scramble for duration (or outright risky investments like junk bonds and high beta stocks) .. So what do pension fund managers do when perpetually declining interest rates continue to drive their funded status lower and lower despite one’s return profile? Well, there is little choice: one has to move further and further out the yield curve in an attempt to match asset duration with that of one’s liabilities. That, or reach for the skies by buying the riskiest assets possible, and pray for a home run.” LINK HERE to the article

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/11/2016 - Russell Napier: Financial Repression Will Intensify

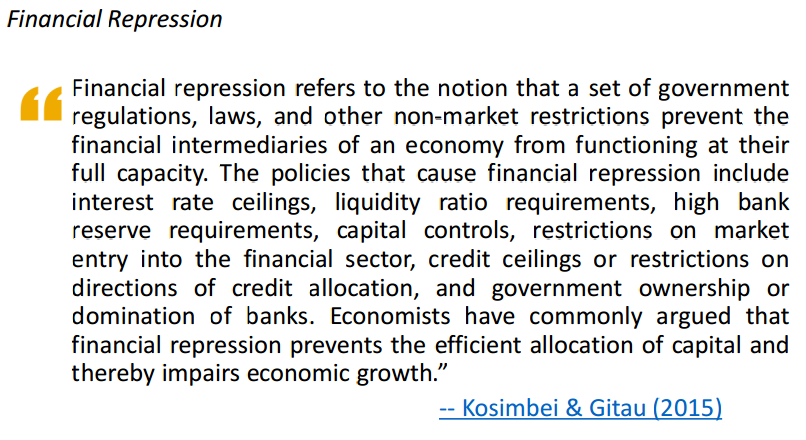

“Government will bring measures to stop you and I gearing up, which is the elements of financial repression. They have to try and force you and I to buy government debt even though it is a virtually guaranteed loss-making proposition, and they have to bring in controls that would stop us behaving naturally as a response to negative real interest rates. Now, those historically have been some horrific things .. A lot of people think central bankers will keep going forever, but if we ever go to inflation, they clearly have to stop expanding their balance sheet, but somebody has to buy the government debt .. So let’s say the fiscal policy comes. It succeeds. We get growth. We get inflation. Central bank balance sheets cannot expand in the growth and inflation. So who’s going to buy the government debt? The answer is you are. Particularly if you work for a regulated financial institution. It’s much better if you’re an individual. But regulated financial institutions are the people who will be expected to do that, and that is financial repression.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/11/2016 - The Roundtable Insight: Peter Boockvar & Alasdair Macleod On The U.S. Elections’ Implications To The Economy & Markets

FRA is joined by Peter Boockvar and Alasdair Macleod in discussing the effects of the US Trump presidency on the global economy and the resulting shifts in financial markets, along with infrastructure spending that will likely occur in the near future.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University.

PETER BOOCKVAR: EFFECTS OF THE US ELECTION

The reverse on markets is in hopes that Trump’s easing of the regulatory burden and cutting of taxes will kick-start the US economy. Inflation pressures have been building going into the election. We’re seeing this short rise in long-term interest rates. Interest rates are spiking at the same time that stocks are rallying.

We saw a bottom in the 10-year yield at 1.53% right after Brexit, and right now we are basically fifty plus points higher. It’s not because the US economy has gotten much better, but interest rates are likely to continue to rise in the long end and the Fed is going to be playing catch-up when they raise rates in the short end. It will be a challenge for stocks to continue to rally in the face of the rising rates, as a large part of the bull market in stocks predicated on artificially low interest rates.

There’s no such trend that the fall in the bond market represents outflows from the bond market would then be taken back as inflows into the stock market. A lot of people had long puts going into the election, hedging against a potential Trump victory, and now we’re seeing massive put-selling which lends upward pressure to the market. We’re seeing some overvalued stocks that are being challenged today by the rising interest rates.

INFRASTRUCTURE AND GOVERNMENT STIMULUS

In 2008 we had an almost trillion dollar ‘stimulus package’. The government is always throwing money out there and spending it, and it’s not always the most efficient use of money. There are plenty of estimates out there saying the multiplier effect is below zero, so the idea that we’re building bridges as panacea are hugely misplaced. An increase in infrastructure would potentially contribute to the trend of rising inflation if the demand for raw material exceeds the supply. The continued deficit spending would be potentially inflationary as well.

In terms of Fed policy, it would be extraordinarily dangerous if there was a greater linkage between fiscal policy and monetary policy. Trump is likely to take a step back and stop criticizing the Fed. Janet Yellen’s term is up in January 2018 and she’s just going to retire and be replaced by someone else.

FORECAST ON DIFFERENT ASSET CLASSES

The action of the bond market is the main driver of the equity bull market, with the suppression of interest rates to near zero and multiple rounds of quantitative easing. We’ve built this economic construct based on an artificial level of interest rates that, if rising, potentially threatens economic activity and market multiples. If interest rates continue to rise, there will be some short-term correction in the stock market.

The reflation trade is going to continue. Commodity prices have been in a five year bear market, gold and silver in particular, and we’re going to see a rise in inflation and fall in real rates. Cash is also a good asset right now, and emerging markets are still an attractive place. Interest rates will rise in December and next year as well if inflation continues to creep higher. The last position the Fed wants to be is being forced to raise interest rates rather than doing it from their own volition.

MORE EFFECTS OF THE TRUMP PRESIDENCY

That’s the potential danger of the Trump presidency. Tariffs and protectionism is essentially a tax, and that in itself is inflationary as well. So it would be a toxic mix if he actually implemented it. The hope is that he’ll surround himself with more rational economical minds and that a lot of what he said is just talk.

We’re already seeing the 10-year yield move up 20 basis points. The level of infrastructure spending could be limited by what the financial markets are reacting to. The market multiplier in government spending, in many cases, is barely above zero and some will argue below. The hope is that the regulatory noose that’s been put around the banks will ease up, but regulations across the entire country will hopefully ease up on businesses and individuals. Areas that have been driven down by the fear of a Hilary presidency are bringing back the market.

People have to keep their eyes on interest rates. That’s going to be the main driver of interest rates, which need to normalize and go higher. There’s going to be a painful transition to more normalized interest rates, which is needed in the big picture. The debasement of currencies will continue, and will get worse if we continue to build up all these debts and deficits.

ALASDAIR MACLEOD: EFFECTS OF THE US ELECTION

The problem is not infrastructure projects. Trump’s real problem is that everyone is underestimating how rapidly government finances are deteriorating. There’s going to be a pickup of inflation in 2017, which means government incomes get squeezed. The index of non-food raw materials will rise, getting more expensive than originally thought, and at the same time the lags in tax collection means government income will not keep up with the pace of inflation. The underlying budget deficit is going to keep getting larger. It’s difficult to see how Trump will finance infrastructure projects while cutting taxes as it is too dangerous to borrow excessively.

Base metals are going up, and the effect of these raw material increases is going to feed through to wholesale and retail prices. The Fed is going to find itself in a place where inflation at the CPI level is at 4%. They’re worried about raising interest rates because of the level of indebtedness in the economy, and if interest rates rise more than 2.5% there’s a severe risk that the whole economy will fall over from the outstanding debt. The last thing you want is to exacerbate that by borrowing money to finance tax cuts and infrastructure spending.

EFFECT ON DIFFERENT ASSET CLASSES

The bond market has peaked and is falling considerably. The falls in US treasury prices are likely to transmit into falls in sovereign debt prices around Europe, which in turn will threaten the European banking system.

If you get rising bond yields, you get falling stock prices. Equity markets will fall considerably on the back of rising bond yields. In the endgame, equities will become a way to protect yourself from inflation.

Property turns out to be very good protection from hyperinflation, but the amount of gearing in residential property market is staggering. If we get a rise in interest rates from the current level, a lot of people are going to be in severe difficulties. It will put off buyers on the market and possibly force sellers onto the market as well.

PRECIOUS METALS

In the short term, the reaction by which gold prices went up was quite natural. We see inflation picking up, bond yields falling, and interest rates rising but not enough to deal with the inflation problem. The Fed raising interest rates will be very aware of causing a systemic crisis if they raise rates too much. We have a potential for crisis with the rise in Fed funds rate to as little as 2.5%. If inflation goes to 5%, the Fed can’t respond to it, and gold will begin to anticipate that. Silver moves about twice as much as gold, and may be quite rewarding for speculator play. Gold is sound money and the dollar is less sound money, and that translates to higher gold prices.

The yields on bond will go up next year, in line with rising inflation, and there will likely be quite a lot of distress selling from people who went long in that market at the wrong price.

THE NEXT PHASE OF THE FINANCIAL CRISIS?

We will probably have a banking crisis of some sort – possibly in Italy – and as that crisis spreads, central banks will print money and this time it will be inflationary. China is already in the market for raw materials and putting in huge infrastructure to take her population into the middle class. The rush for infrastructure spending is happening in various countries at the same time, and this means rising commodity prices across the board.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/04/2016 - The Roundtable Insight – Alasdair Macleod & Uli Kortsch On The Unintended Consequences Of Massive Government Debt Levels

FRA is joined by Alasdair Macleod and Uli Kortsch in discussing global levels of government debt and the challenges in servicing that debt, providing economic growth, and its effect on central bank policy.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

Uli Kortsch is the Founder of both the Monetary Trust Initiative (MTI) and Global Partners Investments (GPI). Currently most of his time is spent on MTI whose mission is to bring transparency and authentic principles to our monetary system. As President of Global Partners Investments and other ventures Mr. Kortsch has worked in over 50 countries, written a bill for Congress, and conferred with approximately 15 national presidents, ministers of finance, and ministers of commerce. He has served on numerous corporate boards with both for-profit and not-for-profit organizations.

PRIVATE AND PUBLIC DEBT CRISIS

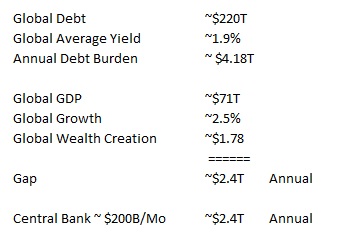

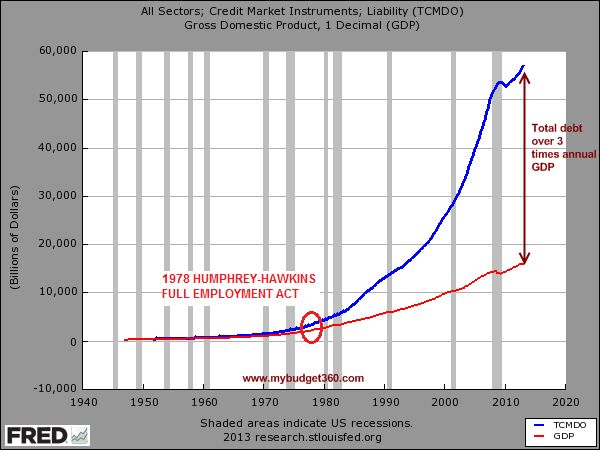

There’s a slow back and forth between private and government debt. When there’s a deleveraging in the private sector there’s a massive pickup on the governmental side, and vice versa. Global debt today is at about 110% of global GDP. The level of outstanding debt at the end of 2015 is about $200T. This doesn’t take into account the shadow banking system, which can’t really be quantified.

The whole system is in a debt crisis. If the Fed Funds Rate rises to 2.5%, that will trigger a complete collapse in the economy. It is virtually impossible for the Fed to have any control over outcomes if the only room they have is to raise interest rates by no more than 2.5%. If we have inflation picking up next year, we are likely to have a situation where we have no economic growth and inflation at the price level beginning to pick up, the Fed is faced with a dilemma. They can’t raise interest rates to the level where it will stop price inflation.

The next recession isn’t going to be a normal recession at all. If we end up with a situation where we have official stagflation, we will move into a hyper-inflationary situation if the general public begin to understand that the paper money only has as much value as they give them, and then the whole thing enters a very dangerous slope.

Even economic collapse has always resulted in wealth destruction, which occurs due to the collapse of the purchasing power of the currency. By the end of the firs World War, the only way Germany could function was to print money. And that culminated in 1923 with the collapse of the currency. Nowadays we have a different set of circumstances, but the burden is at least as painful as reparations. An inflation rate of 4% for 10 years will reduce the debt by half. That has been the preference of governments and central banks over the years.

US DOLLAR PURCHASING POWER

The banks have been drawing down on their reserves over the last couple of years. If you look at LIBOR rates and compare that with what they get for leaving it in reserve at the Fed, there is a huge incentive to gradually move some of this money out. The Fiat Money Quantity (FMQ) includes money that is reserves held by the Fed and the Austrian True Money supply. That has been increasing at an accelerating rate. If you look at M2-M1, then you see a recent acceleration above trend. That suggests there is a demand for money somewhere outside the Fed and US banking system. International debt is tending toward contraction, which is likely creating a demand for dollars. The debt is still the dominant factor.

Recently Brazil targeted a specific rate of inflation, which ultimately led to a much higher rate of inflation. It’s very difficult to keep the inflation target at a certain level once it gets going. The value put on the dollar in terms of purchasing power is up to the people, not the Fed. This is the point the monetary planners miss: they can never control the purchasing power of the currency.

EFFECT ON US ELECTION – FISCAL PLANS?

Debt has not been on the discussion at all. The candidates say things to get votes, but what’s interesting is how the press has been on Hilary’s side to become president. Trump has achieved astonishing results. Hilary’s campaign has literally become a “woman’s lib”. The motivation for the FBI, when it comes to reopening Hilary’s case, can only happen if there has been a decision taken by the security services as to who they actually want to support.

The good news is that Donald Trump will be on side with the establishment. It is actually the establishment that is switching side. Whoever becomes to the next president will likely be a one term president. There are no answers in our current economic system to deal with the accumulation of debt.

Recently Trump has been going after the Fed, and there certainly is the possibility that the next president will put in several of the new governors. The next president will definitely be able to stack the deck in the Fed’s favor.

FORWARD GUIDANCE AND FINAL THOUGHTS

Forward guidance has a place if you actually understand economics and what is happening to money. Then you can use forward guidance to tell the banking systems look, we’re moving back to freer markets and this is the schedule, so banks can prepare for it and the transition becomes possible. To use forward guidance to pursue current policies is a horrendous mistake.

In 2017, the story is going to be stagflation. Escaping from that isn’t going to be as easy as it was in the 1970s; it’s going to morph into something far worse on the inflationary front.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

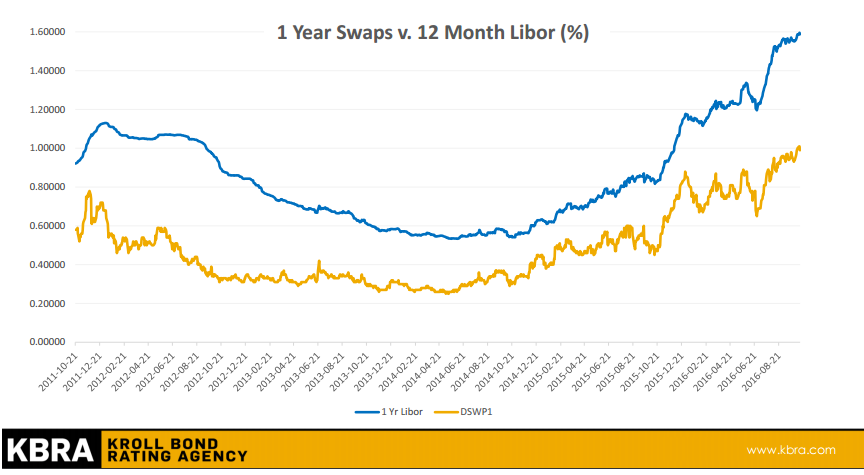

11/02/2016 - Dodd-Frank represents Regulatory Policy that assures sub-standard credit and job growth in an Era of Financial Repression!

Dodd-Frank represents Regulatory Policy that assures sub-standard credit and job growth in an Era of Financial Repression!

According to Christopher Whalen of Kroll Bond Rating Agency (KBRA) the 2010 Dodd-Frank law represents another “phase-shift” in regulatory policy that implies sub-standard credit and job growth for years to come, regardless of the level of interest rates or open market purchases (QE) of securities by the Federal Open Market Committee (FOMC) and other global central banks.

As a result, low levels of job creation and growth which are exacerbated by deflationary effect of low/negative interest rates, are driving a populist political backlash in the US and in Europe. The “surprise” result in the BREXIT vote this summer is likely to be repeated in future elections because of the ground swell of popular discontent at failed economic policies.

Markets are now starting to price in these risks, as evidenced by the widening gap in cost of dollar funding in the US and EU.

Christopher Whalen of Kroll Bond Rating Agency (KBRA) has just released a presentation discussing this. The presentation makes the following additional key points:

The “single mandate” for all governments is job growth, both for economic and political reasons. The FOMC pretends to have a “dual mandate,” but in fact the Humphrey Hawkins law makes “full employment” the paramount policy mandate before price stability or stable interest rates can even be considered.

Since the 1970s, fiat money and the singular focus on full employment has gradually forced interest rates down to zero or below. The secular decline of interest rates, which is the centerpiece of “financial repression,” necessarily also drives deflation by taking income (carry) out of the economic system.

With negative interest rates, global central banks are depriving the global economy of trillions of dollars in income and thereby fueling a diminution of private capital and economic activity. Low interest rates and QE also lead to bad investment decisions, as in the case of oil, residential and commercial real estate, shipping and other asset classes.

The fixation of global monetary authorities with targeting employment has significant costs, including a steady level of underlying inflation that undermines consumer purchasing power (thus, today’s discussion of “income inequality”). The single mandate of full employment also facilitates periodic financial bubbles and crises resulting from the manic swings in monetary policy.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/30/2016 - Dr. Albert Friedberg: Distortions Created By Central Banks Have Blunted Our Navigating Instruments On The Financial Markets

Dr. Albert Friedberg*:

Rarefied Air: The Lack Of Liquidity

In The Financial Markets Is Real

“The distortions created by central banks over the past seven years have blunted our navigating instruments. If a storm is approaching, we are unable to see it. We navigate by instruments, valuations, historical precedents, official opinions and reassurances. Even when a gigantic tsunami overwhelms one of the ships in a perversely calm sea, we reject the warning, chalking it up to its conductor’s carelessness. That mighty sterling can collapse 6% in a few seconds says only that the Brexiters made a bad choice. Really? Our senses apprehend that all is not well, but we look around and can’t see it .. Stepping back from the metaphors, I offer that vanishing liquidity (defined as the ability to rapidly execute large financial transactions at low cost with limited price impact) is the lonely indicator of serious trouble ahead. Liquidity to markets is the equivalent of air to humans. And permitting myself one more incursion into the figurative world, air gets thinner, more rarified, the higher one climbs. Historically, bull markets have always been accompanied by rising volumes and rising liquidity. They died when far-sighted, sophisticated sellers overwhelmed the throng of new, enthusiastic, short-sighted buyers. This seven-year-old bull market is different. Precious few buyers with conviction and enthusiasm can be spotted. It’s a lack of sellers that has fortuitously allowed the paucity of buyers to drive up prices. This liquidity constriction is felt in our own skin. Positions that were easy to put on months ago have become increasingly difficult to exit. It now takes five to eight days to get out of positions if we do not wish to noticeably affect prices, compared with one to three days in months past. The loss of liquidity is not an empty term; it’s real .. Not until volume rises significantly above the recent pace will we be confident that risks are being properly priced in and that prices are indeed clearing.” .. Friedberg is bullish on gold, sees the prices as having bottomed out about a year ago .. LINK HERE to get the PDF

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/29/2016 - The Roundtable Insight – Alasdair Macleod & John Butler On Rising Inflation & Gold

FRA is joined by John Butler and Alasdair Macleod of Goldmoney in discussing the impact of stagflation on the global economy, along with the effects it would have on equity markets.

John Butler is the Vice President and Head of Wealth Services for Goldmoney, Inc, the world’s leading provider of savings, payments and other financial services all fully backed by physical, allocated gold. Prior to joining Goldmoney he had a 15-year career as a macro investment strategist at Deutsche Bank and Lehman Brothers, among other firms. He is also the author of The Golden Revolution, a book analysing the causes and consequences of the 2008 financial crisis and exploring ways in which gold could re-enter the international monetary system.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

THE EFFECT OF PRINTING MONEY

Theory would have told you, years ago, that all the money printing during the crisis of 2007/2008 would eventually turn into rising price level. There tends to be a relationship – albeit a very unstable one – between expansion of the money supply and a rising nominal price level. It can’t be modeled precisely, which is why the bulk of the economic profession doesn’t bother to even think about it.

We’re finally starting to see that the vast expansion of money supply that happened in all major economies in 2008/2009 is following through into a general consumer price inflation. We’re seeing in commodities, which have bottomed, and in wages. Wages are picking up.

We have passed an inflection point with growth generally weak in most economies around the world. This combination of CPI inflation rising and growth that is weak or slowing further makes for a stagflationary mix, which is a horrific environment for investors as it implies a potential under-performance of both stocks and bonds.

The fact that the fiscal profligates are talking about fiscal stimulus spending more aggressively than they have been for a while, is clear evidence that the inflation inflection point is behind us. They simply want to inflate their way out of the massive debts they have created for their own political reasons. That is the world we’re now living in. It’s amazing, in a way, how openly they are discussing helicopter money.

There is an assumption among the Keynesians and Monetarists that if the state expands the quantity of money in circulation, it will stimulate the economy. As a one-off, it is certainly possible as it fools people into thinking there is real extra demand in the economy. The payment for that extra money is a tax on all the existing money in circulation that gets realized gradually over time, so you find that prices start rising when that new money is spent, and then the price rises gradually ripple out from that point. There is a gradual wealth transfer because the purchasing power of an individual’s wages and savings is being debased by price rises which are emanating as a result of this extra money being injected into the economy. What you’re doing, in effect, is making a few people wealthier by printing money and giving it to them first, but making the vast majority of people impoverished. To do this continuously guarantees that there is no economic recovery at all in the economies that suffer from this money printing. Stagflation is essentially the early stages of a price inflation that risks morphing into a hyperinflation. We have a situation today where there is so much debt around that it is impossible to conceive of a situation where the central banks could raise interest rates to a level that can slow down the switch in preference away from money and into goods.

A RISING CPI

There is going to be a huge reluctance on the part of central banks to tackle the situation. The CPI deliberately understates the increase in the general level of prices in the economy. If you had a true representation since the Lehman crisis, you would find that as a deflator on GDP, we would be showing negative growth since the Lehman crisis. Everyone is getting poorer from the wealth transfer effect resulting from printing money and credit.

The trend toward rising consumer prices is the legacy of all the stimulus we have seen today. It’s almost as if central bankers love the smell of inflation. They have this obsession with it, even though it’s destroying the middle class’ purchasing power.

Since Brexit, the Sterling has weakened considerably. If you look at producer prices, falls in producer prices have now reversed due to higher commodity prices and because of lower sterling. It reversed from -20% to +25% BPI inflation in Sterling. What will that do to the inflation rate in the UK in 2017? Businesses will go into recession, unemployment will rise, and we will likely to have headline inflation rates in excess of 5%.

EFFECT ON EQUITIES AND ASSETS

At the moment, bond markets are controlled by central banks because they can’t afford for there to be a bear market in bonds. At some stage, the market will win, and that would cause a very substantial rise in bond yields and a very substantial fall in equity prices. The UK has routinely 80% loaned value mortgages, so all the assets that have been puffed up and sustained since the Lehman crisis are at risk. When that market rigging starts cracking, it could be extremely expensive for anyone who has invested in conventional assets.

Since gold is an asset that cannot possibly default, prices tend to rise with inflation. Stagflation is an even better environment for gold because it will outshine equities dramatically. It is the best environment for gold outright, in price terms, and relative to stocks and bonds. Stagflation only occurs in the occasional economic cycle, and then those cycles that tend to be those that follow major crises. As an investor, you cannot responsibly create a portfolio for a stagflationary environment that does not have a material allocation to gold in it.

When you get inflation, you do get conventional markets being destabilized, and the social ramifications are extremely unsettling. We mustn’t look at this stagflation scenario in just the narrow terms of the financial effects; there are also social effects and it is the interplay of the social effects and the financial effects that make it worse for conventional assets.

HOW IS THIS TREND AFFECTED BY KEY ISSUES?

We need to understand how distressed the European banking system really is. It never materially recapitalized deleveraged anything after 2008. There have been all kinds of accounting shenanigans that have been deliberately engaging in structured transactions whose only purpose is to disguise the fact that they are under-capitalized vis a vis regulatory requirements. There is overwhelming but circumstantial evidence that even the biggest banks in Europe are in even worse shape than they were in 2008. The market is kind of telling you that they’ve figured this out, but the problem is that in a global economy, if one financial over-leverages and not capitalize itself properly, then you have these cross boarder linkages. It happened in the 1920s and 1930s, when an Austrian bank catalyzed a cascade of solvency issues and defaults across the entire world. If it could happen then, it could happen now.

If you look at the Italian situation, Italian non-performing loans, which are all in the private sector, are officially admitted at 40% of private sector GDP. It’s a very clear indication of the underlying state of the Italian economy and why almost 50% of youth are unemployed in Italy. The banks will go under, but the underlying situation is impossible as well.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/22/2016 - CENTRAL BANKERS CAN’T STOP THE BUSINESS CYCLE – NOR THE DEATH BLOW OF A POST US ELECTION RECESSION

CENTRAL BANKERS CAN’T STOP THE BUSINESS CYCLE

NOR THE DEATH BLOW OF A POST US ELECTION RECESSION

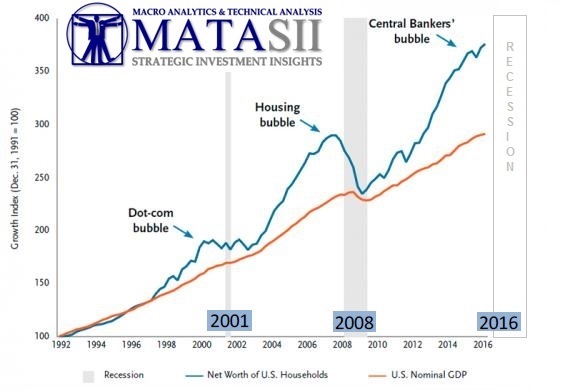

The central bankers are capable of achieving many extraordinary results but not all economic and financial problems can be solved by central bankers. Central Bankers for example have the power to solve liquidity issues, but it is impossible for them to solve solvency issues. Central Bankers through Financial Repression can transfer risk , however they can’t remove it from the system. Additionally, Central bankers may be able to delay a recession temporarily, but they can’t prevent the business cycle from running its natural course.

This inability to control the business cycle has the potential to be the unavoidable trigger that brings the great Central Bank Bubble to an end.

The US after eight years is by most comparisons overdue a recession. Unfortunately, the next recession is going to happen when the central bankers are least capable of further attempting to slow the inevitable. The central bankers may have delayed a US recession about as far as they are capable of doing.

A NEARLY PERFECT STORM BREWING

The market technicians of all persuasions are almost unanimously now calling for a major correction. What is most troubling in their work is that their indicators are not just short and intermediate term measures but critical long term indicators:

KONDRATIEFF CYCLE: The 55 Year generational Kondratieff Cycle shows an overdue major downturn with a cleansing of debt as part of the end to what has been termed the “Debt Supper Cycle”,

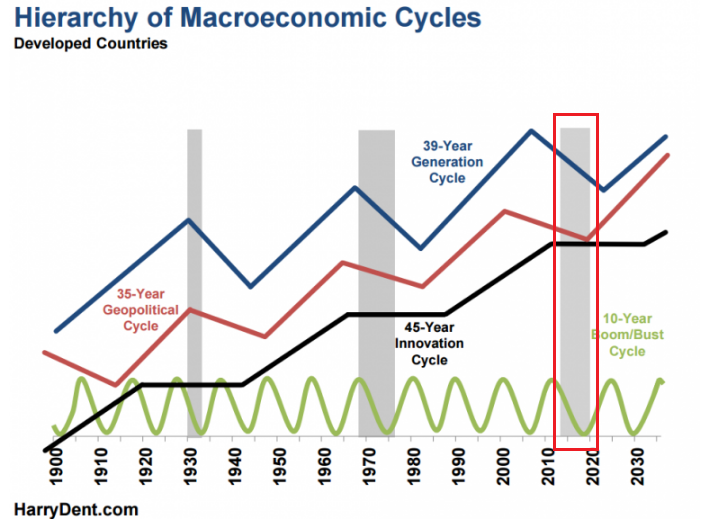

DEMOGRAPHIC CYCLES: Harry Dent has done some major work on Demographic Cycles and cycles overall. I interviewed him for the Financial Repression Authority where you can find the video and he lays out the seriousness of the shifting demographics and how it overlays of many different types of cycles he has studied.

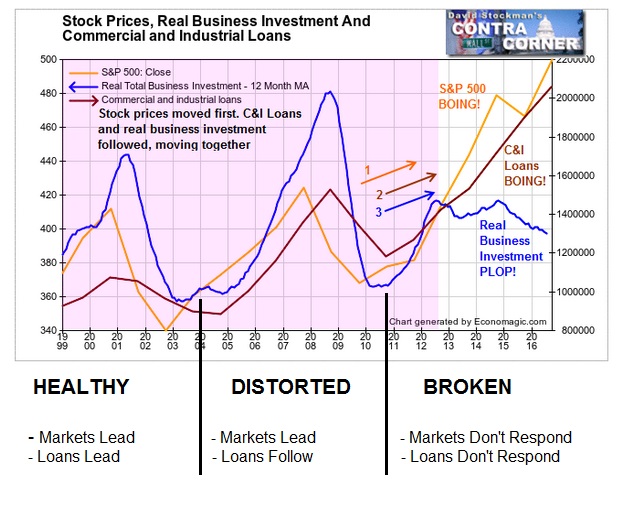

The mal-investment that recessions normally purge as part of a healthy capitalist system has reached such a level that deteriorating real total business investment has diverged from the S&P 500 Index as well as C&I Loans. In our opinion (which we have labeled here), sound business investment has shifted from being distorted to what can now only be described as broken. Corporate profits, sales revenues, margins and EBITDA cash-flow are all falling or are rolling over.

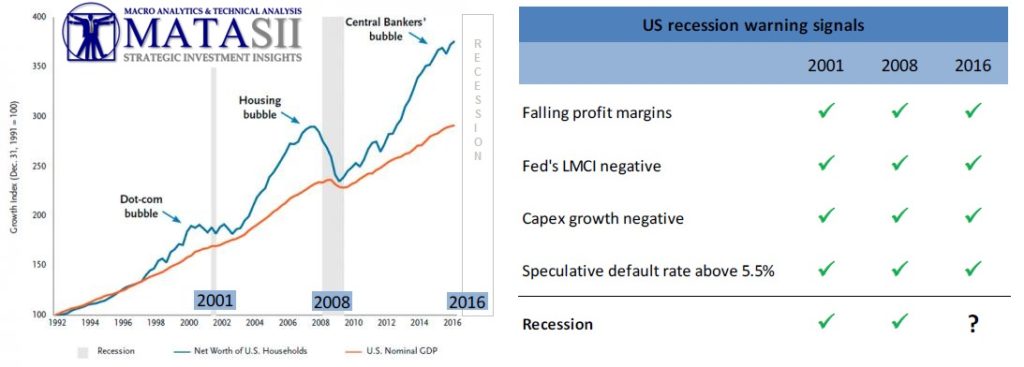

Every recession on record since the end of WWII (but one) has signaled the four warnings outlined here. That one exception had a completely different economic climate than the current one. The chances of a US Recession in 2017 should be considered highly likely.

The problem with the next US recession is that the magnitude of distortions and leverage in the system will potentially quickly cascade into a full scale, unmanageable economic problem and likely a full scale protracted recession (or even worse).

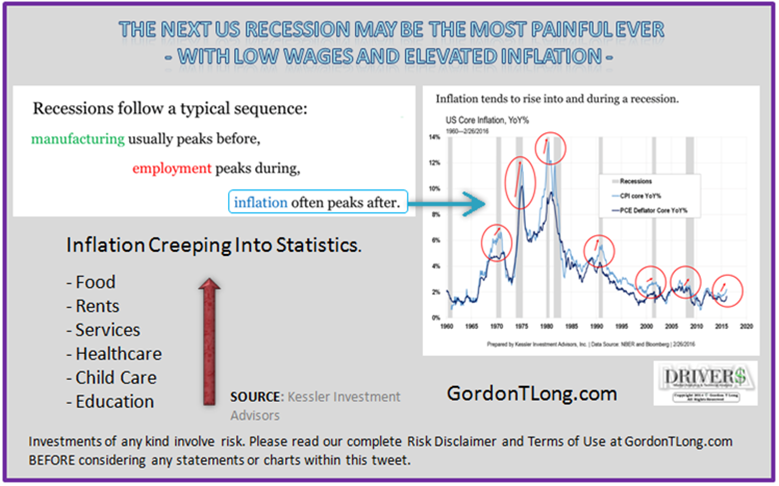

A “WHIFF” OF INFLATION

Few market watchers appear to appreciate that inflation tends to rise into and during a recession.

Consumer prices in U.S. rose in September at the fastest pace in five months. The Year-over-Year inflation rate is now the highest it has been since October 2014. Few are yet paying attention.

What this suggests is that the Fed will most likely remain on course for an interest-rate hike this year, immediately following the US Presidential election.

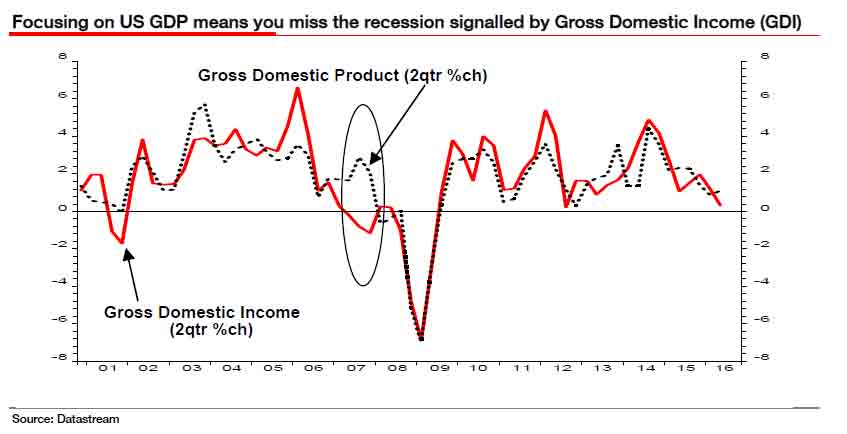

To many this is exactly the wrong medicine for the economy at exactly the wrong time especially when you consider Gross Domestic Income (GDI). Fed actions would almost assure the recession.

All US Recession discussion (currently “embargoed” by the mainstream media) will become headline discussion immediately AFTER the election, as the blame game then ensues on how the unprecedented negative campaign rhetoric was actually the root cause. This will be the politicos “cover” for massive fiscal spending and increases in the Fed’s balance sheet. Of course it won’t stop the recession nor the financial damage that will ensue.

Don’t say you weren’t warned!

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/21/2016 - The Roundtable Insight: Yra Harris on Deutsche Bank, Systemic Risk and the U.S. Elections

FRA is joined by Yra Harris in discussing the impact of the potentially failing Deutsche Bank on the global economy, along with the state of US markets as election day draws closer.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator.

He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

DEUTSCHE BANK

We don’t know if Deutsche Bank is a buy-in opportunity. It’s based on the fact that the EU and Germany will not allow Deutsche to fail. This extensive systemic risk because of the fact that Deutsche Bank is one of the world’s largest notional derivative books – of about $46T at the end of last year – represents a lot of risk in terms of derivatives meltdown between counterparties. While the ECB balance sheet has grown from €2T to €3.4T in just 18 months, there’s only about €7.5T outstanding Eurozone sovereign debt. It represents a challenge going forward in a very quick period of time, in terms of the overall systemic risk to the European banking system.

Its risk profile is based on Deutsche’s own models, so we don’t really know what the exposure is. It ought to be a higher risk rating than they reveal.

CAN’T LET DEUTSCHE FAIL – WHAT THEN?

It would be extremely difficult to bail Deutsche out or bail it in. If you want to see financial repression, watch what the ECB is doing to the savers in Germany. They’re bearing the bailout of the entire European project. If there was a bail-in, that would cause even more political angst. If that balance sheet grows big enough, no one can escape the EU ever, and the German taxpayers will be on the hook for this forever.

The German government is boxed in. It could go in the direction of a bailout of 100M to potentially a bail-in, as part of financial repression where there’s a wealth confiscation of assets that take place at the capital structure layers, anywhere from bank depositors to senior secure bond holders. It could happen either way or a combination of both. Or you could have both, or have the European Central Bank step in and monetize a lot of the bailout in terms of assistance for quantitative easing programs.

Mario Draghi would like to increase QE, but there’s no chance of that happening. He’s under a lot of pressure, and wants to build that balance sheet up bigger and bigger. Central bankers are running out of tricks and ammo.

The US equity market has now broken out of the uptrend. The equity market is fairly valued, but vulnerable to a sell-off. Wall Street would prefer Hillary, but she will certainly raise capital gains or the holding period in which you can obtain capital gains. People who have been in this market and have long term capital gains will likely sell that which they can before the end of the year, which makes this market vulnerable. Corporations have piled up so much debt that it weighs on this market dramatically. The amount of debt piled on the balance sheets around the world is just enormous.

The markets are vulnerable from the perspective of overvaluation measures and overhanging debt, but also from the potential of helicopter money for doing projects like infrastructure to provide a stimulus to the financial markets as well as the economy. The asset markets will have to go down significantly to some level to prompt fiscal authorities to bring the political will together to create fiscal stimulus. With increasing central bank buying of stocks, that will likely artificially support stock markets.

US PRESIDENTIAL RACE

Trump makes the markets nervous, because they don’t like unknowns translating into high volatility in the markets. Trump might be anti-trade, which could affect international companies, but Clinton might bring geopolitical events that could negatively affect the markets as well.

Several people have laid out the possibility that if Trump pulls out a surprise upset victory on election night, there would likely be calls to say this was Russian tampering and that election results should be put on hold until it could be determined if foreign interests undermined the election. This will likely provide a great deal of social unrest, which could translate into a lot of economic uncertainty. There’s a lot happening outside of North America that could work to propel the US markets higher with a strengthening dollar.

US DOLLAR STRENGTHENING

Last week we saw, for the first time since February, the US dollar move above 97.50 on the dollar index. It’s starting to look like the makings of an upside break-out in the dollar index. When you look at the problems around the world, it’s hard to believe the Euro is still above par. The Yen is still 20% higher on the year. The dollar ought to be higher, but it’s not. The central bankers are working to manage the stability of currencies relative to each other, but overall we’re looking at the decline of purchasing power of money regardless of currency.

This is about global assets – they’re all somewhat in trouble here.

PORTFOLIO CONSTRUCTION AND ASSET ALLOCATION

Treat everything as short term trades. If you can turn it into a profit, go ahead, and go on to the next one. It’s very difficult to say in a medium or long term sense because of the strong tug of war between inflation and deflation type forces. We have strong deflationary forces that are naturally happening in the financial system being counterbalanced by the very inflationary forces provided by central banks. It could go either way in a medium term. It would be difficult to quickly change your portfolio, but perhaps a diversified portfolio in the medium-long term with this short term trading strategy.

Another way is looking at companies with little or no debt, high discounted free cash flow with little or no leverage.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

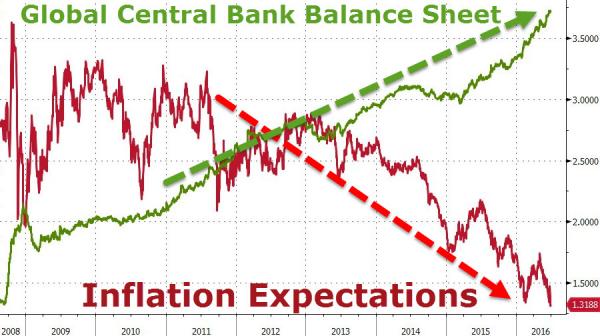

10/17/2016 - FINANCIAL REPRESSION IS NOW “IN-PLAY”!

FINANCIAL REPRESSION IS NOW “IN-PLAY”!

A FALLING MARKET CANNOT BE ALLOWED – at any cost!

The Central Bankers have clearly painted themselves into a corner as a result of their self-inflicted, extended period of “cheap money”. Their policies have fostered malinvestment , excessive leverage and a speculative casino approach to investments. Investors forced to take on excess risk for yield and scalp speculative investment returns, must operate in an unstable financial environment ripe for a major correction. A correction because of the high degree of market correlation that likely would be instantaneously contagious across all global financial markets.

Any correction more than 10% must be stopped. As a result of the level of instability, even a 10% corrective consolidation could get quickly out of control, so any correction becomes a major risk. What the central bankers are acutely aware of is:

If Collateral Values were to fall with the excess financial leverage currently in place, it would create a domino effect of margin calls, counter-party risk and immediate withdrawals and flight to areas of perceived safety.

The already massively underfunded pension sector (which is now beginning to experience the onslaught of baby boomers retiring) would see their remaining assets impaired. This could lead to social and political pressures that would be simply unmanageable for our policy leaders.

A falling stock market is the surest way of alarming consumers and signalling that things are not as “OK” as the media mantra has continuously brain washed them into believing. In a 70% consumption economy, a worried consumer almost guarantees a further economic slowdown and a potential recession.

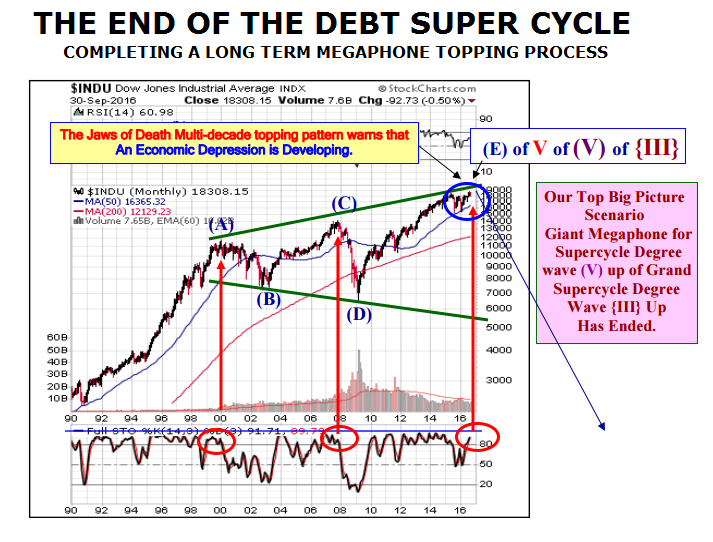

As our western society continues to consume more than it produces, productivity is not increasing at the rate that justifies the developed nations standard of living as well as the current levels of equity markets. A possible corrective draw-down to the degree shown in this chart is simply “out of the question”! The central bankers acutely aware of this.

MARKETS TEMPORARILY HELD UP

The markets are presently, temporarily held up due primarily to three factors:

Historic levels of Corporate Stock Buybacks,

The chasing of dividend paying stocks for investment yield in a NIRP environment,

Unusual Foreign Central Bank buying (example: SNB)

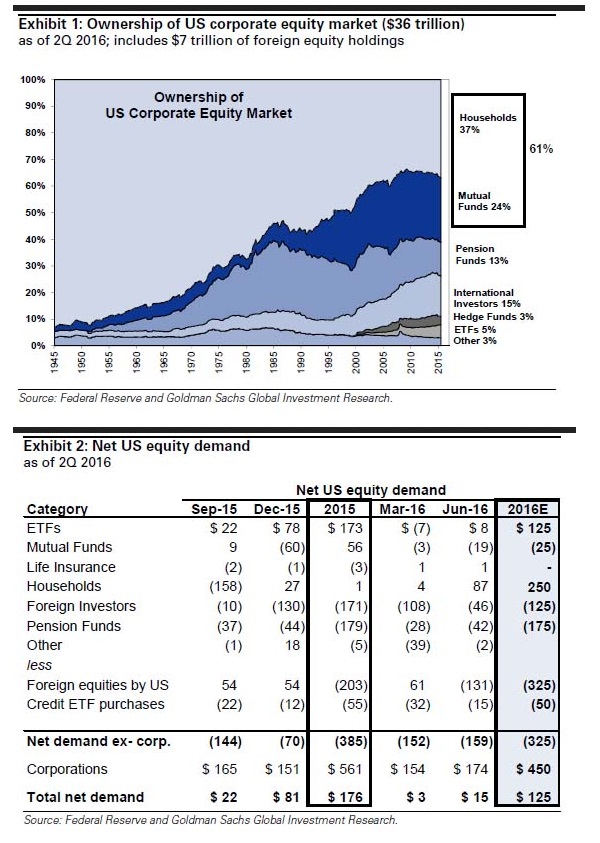

Professionals, institutions, hedge funds etc have been steadily lightening up on equity markets (or simply leaving completely) leaving the public holding the bag.

It is estimated that the $325B that will leave the US equity markets in 2016 will be replaced by an artificial $450B of corporations buying their stocks. With corporate cash flows now falling and debt burdens triggering potential credit rating downgrades, this game is quickly slowing. The central bankers are aware of this.

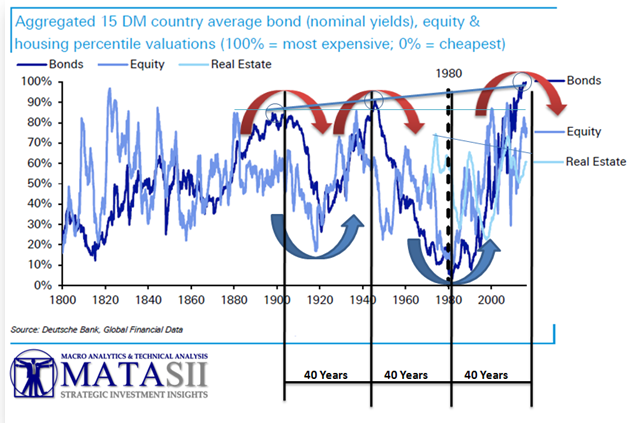

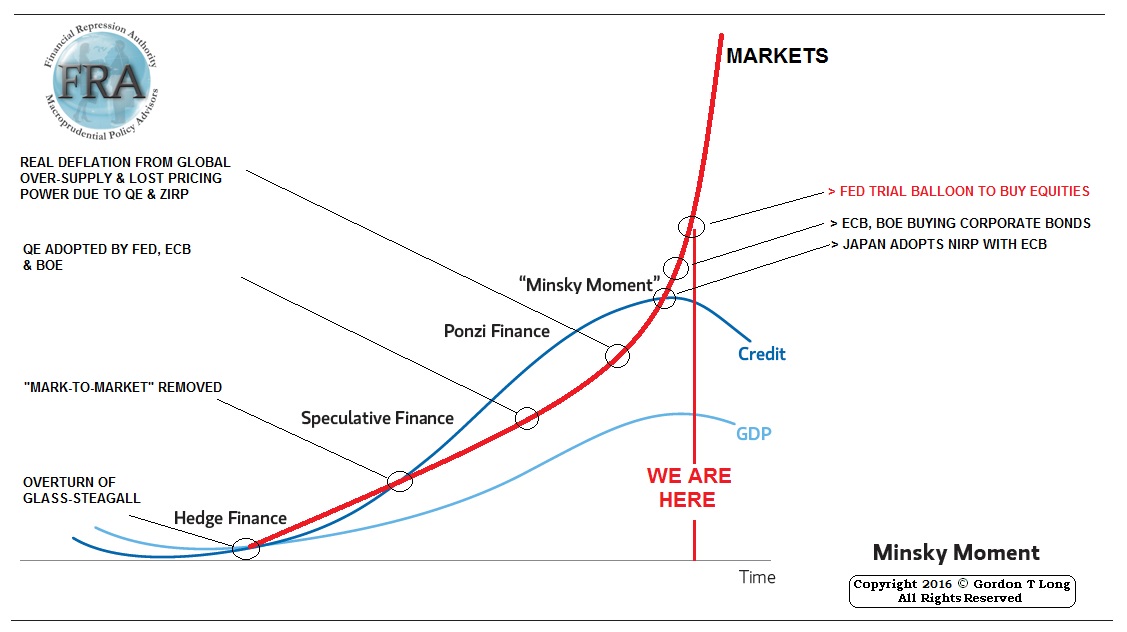

TECHNICALS INDICATING AN END TO THE DEBT SUPPER CYCLE

The Market Technicians of all persuasions are almost unanimously calling for a major correction. What is most troubling here is that their indicators are not just short and intermediate term measures but critical long term indicators.

KONDRATIEFF CYCLE: The 55 Year generational Kondratieff Cycle shows an overdue major downturn with a cleansing of debt as part of the end to what has been termed the “Debt Supper Cycle”,

DEMOGRAPHIC CYCLES: Harry Dent has done some major work on Demographic Cycles and cycles overall. I interviewed him for the Financial Repression Authority where you can find the video and he lays out the seriousness of the shifting demographics and how it overlays of many different types of cycles he has studied.

ELLIOTT WAVE

The technicians who study Elliott Wave see clear evidence that we are now completing a multi-decade topping pattern in the form of a classic megaphone top.

I could keep on illustrating the types of warnings we are seeing, but let me share what the central bankers are likely most concerned about regarding Correlation, Liquidity and Volatility ETPs.

The markets have become so correlated (think of this as everyone on the same side of the boat) with asset correlations not only being higher, but the correlations themselves are becoming more correlated. While traditionally rising cross-asset volatility has resulted in volatility spikes, that is no longer the case due to outright vol suppression by central banks. While central banks may have given the superficial impression of stability by pressuring volatility, they have also collapsed liquidity in the process, leading to less liquid markets, a surge in “gaps”, and “jerky moves” that are typical of penny stocks.

The greater the cross asset correlation, the lower the vol, the greater the repression, the more trading illiquidity and wider bid ask-spreads, and ultimately increased “gap risk”, which becomes a feedback loop of its own. Global central banks are now injecting a record $2.5 trillion in fungible liquidity every year – in the process further fragmenting and fracturing an illiquid market which is only fit for notoriously dangerous “penny stocks.”

“More than $50 billion has poured into low-volatility indexed exchange-traded funds over the past five years or so, in the wake of the 2008-09 market meltdown. There are now 14 “lo-vol” ETFs with assets exceeding $100 million each, and many more with less. Whenever the market hits a pothole, these ETFs enjoy a bump-up in assets.”

Even more concerning are Volatility ETPs (Exchange Traded Products) which are derivative of some underlying asset. Volatility ETFs are particularly strange animals since you’re buying a derivative (ETF) on a derivative (the futures contract) which itself is based on a derivative (the implied volatility of options) and those options themselves of course are derivatives which themselves are based on the S&P 500. Getting the picture? The folks at Capital Exploits warn:

….everyone is on the low volatility side of the boat, because the central banks have managed to create a sense of calm in the markets exhibited by record lows in volatility and investor have used linear thinking extrapolated well into the future assuming ever greater risk ignoring market cycles and extremes at their peril.

Every time you sell volatility you get paid by the counter-party who is typically hedging the volatility (going long) of a particular position and paying you for the privilege. This is not unlike paying a home insurance premium where the insurer takes the ultimate risk of your house burning down and you pay them for the privilege. The difference however between selling volatility in order to protect against an underlying position and selling volatility in order to receive the yield created is enormous. And yet this is the game being played.

The central banks have managed to create a sense of calm in the markets exhibited by record lows in volatility and for their part Joe Sixpack investor has used linear thinking extrapolated well into the future assuming ever greater risk ignoring market cycles and extremes at their peril.

Again, none of this is going unnoticed by the increasingly worried central bankers.

THE NEXT FED POLICY SHIFT

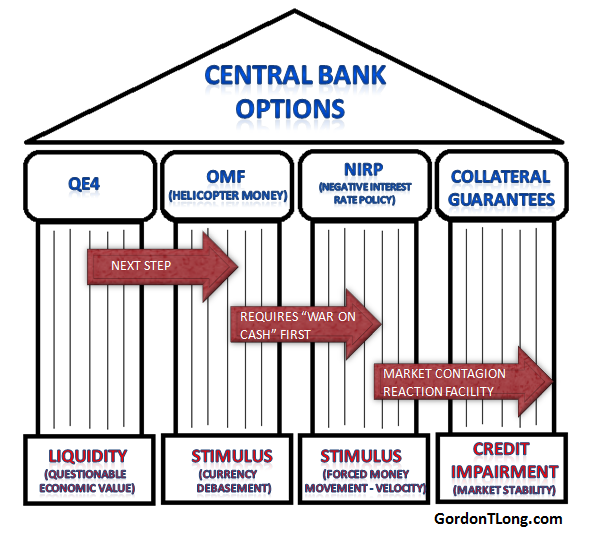

So what can the central bankers be expected to do? We laid out this road-map at the Financial Repression Authority well over a year ago. We anticipated in our macro-prudential research much of what has now become mainstream discussion:

Helicopter Money (now openly discussed)

Fiscal Infrastructure Stimulus (has become part of all candidates election platforms)

Collateral Guarantees

Buying Corporate Bonds – DONE (ECB, BOE)

PLUS more on Collateral Guarantees

We now believe the Central Bankers and Federal Reserve specifically is preparing for more in the way of Collateral Guarantees.

We believe it will actually take the form of direct buying the US stock market similar to what the Bank of Japan is already doing with ETFs.

THE “MINSKY MELT-UP”

My long time Macro Analytics Co-Host, John Rubino concludes in his most recent writing “Flood Gates Begin to Open“:

Individual countries have in the past tried “temporarily higher rates of inflation,” and the result has always and everywhere been a kind of runaway train that either jumps the tracks or slams into some stationary object with ugly results. In other words, the higher consumption and investment that might initially be generated by rising inflation are more than offset by the greater instability that such a policy guarantees.

But never before has the whole world entered monetary panic mode at the same time, which implies that little about what’s coming can be said with certainty. It’s at least probable that a combination of massive deficit spending and effectively unlimited money creation will indeed generate “growth” of some kind. But it’s also probable that once started this process will spin quickly out of control, as everyone realizes that in a world where governments are actively generating inflation (that is, actively devaluing their currencies) it makes sense to borrow as much as possible and spend the proceeds on whatever real things are available, at whatever price. Whether the result is called a crack-up boom or runaway demand-pull inflation or some new term economists coin to shift the blame, it will be an epic mess.

And apparently it’s coming soon.

It is our considered opinion that the monetary policy setters are presently even more worried about the current global economic situation than we are – if that is possible?

If you want to know what could create a Minsky Melt-up, this is it!

Here is our latest Financial Repression Authority Macro Map illustrating what we see unfolding. We believe the dye has been cast!

The US Federal Reserve can soon be expected to get congressional approval for equity purchases.

Of course this will take a post election scare and a new congress to receive.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/16/2016 - Bill Gross: Martingale Strategies Of Central Banks Are Destroying Capitalism

“This Cannot End Well” Bill Gross* Warns

“Low/negative yields erode and in some cases destroy historical business models which foster savings/investment and ultimately economic growth .. Central bankers cannot continue to double down bets without risking a ‘black’ or perhaps ‘grey’ swan moment in global financial markets. At some point investors — leery and indeed weary of receiving negative or near zero returns on their money, may at the margin desert the standard financial complex, for higher returning or better yet, less risky alternatives. Bitcoin and privately agreed upon blockchain technologies amongst a small set of global banks, are just a few examples of attempts to stabilize the value of their current assets in future purchasing power terms. Gold would be another example — historic relic that it is. In any case, the current system is beginning to be challenged .. It is capitalism itself that is threatened by the ongoing Martingale strategies of central banks. As central bank purchases grow, and negative/zero interest rate policies persist, they will increasingly inhibit capitalism from carrying out its primary function — the effective allocation of resources based upon return relative to risk .. Central bankers have fostered a casino like atmosphere where savers/investors are presented with a Hobson’s Choice, or perhaps a more damaging Sophie’s Choice of participating (or not) in markets previously beyond prior imagination. Investors/savers are now scrappin’ like mongrel dogs for tidbits of return at the zero bound. This cannot end well.” LINK HERE to the monthly outlook

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/16/2016 - Yra Harris: Global Politics Will Keep Volatility Elevated

“Increased volatility is not debatable. It will be the outcome of the uneasiness of global politics. It seems that the present state of affairs reflects the vast chasm between those who have benefited from GLOBALIZATION and those who have seen their lives and incomes being disrupted by a world experiencing dynamic change. Brexit was a vote of the nationalists versus the Davos crowd, or those seeking the comfort of the world they know versus those who have profited mightily from the first mover advantage of being prepared for the post Berlin-wall global economy. The central banks’ efforts to prevent a massive liquidation of global assets and harm that would have befallen the global economy has left many participants in a state of financial repression. The outcome of the maintenance of ZIRP–and now NIRP–has been an increased amount of global debt as businesses, consumers and governments add more and more debt in an effort to keep the economic growth expanding. The efforts of the central banks have pushed the structure of global finance into very dangerous over-leveraged situation.” – Yra Harris LINK HERE to the commentary

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

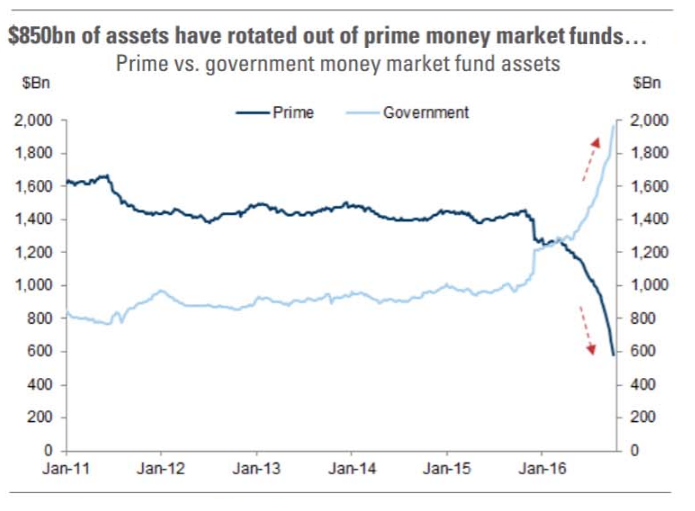

10/14/2016 - New SEC Regulatory 270-2a-7 Has Pushed Nearly $1T Prime Money Markets into Government Funds, Treasuries & Agencies

ADVANCING FINANCIAL REPRESSION

New SEC Regulatory 270-2a-7 Has Pushed Nearly $1T Prime Money Markets into Government Funds, Treasuries & Agencies

The SEC’s 2a-7 money fund reform adopted in 2014 has now gone into affect.

REGULATORY “REFORM”

Requires prime money market mutual funds which invest in non-government issued assets such as short-term corporate and municipal debt to float their net asset value.

Prime MMFs are allowed to delay client withdrawals under adverse market conditions.

The intent of the regulation according to the SEC’s final ruling was to prevent the sort of chaos that hit the money market after Lehman Brothers Holdings Inc.’s 2008 bankruptcy.

GOAL

Give investors a way to monitor a fund’s health by tracking its fluctuating net asset value and

To contain the fallout that could be caused by many investors cashing out at once

RESULT

Many Prime MMFs are and have been converting their assets to government funds,

Are not buying CDs anymore and

Moving into Treasury’s and Agencies.

Nearly $1 trillion in assets have rotated out of prime money markets into government funds. – ZeroHedge

According to the WSJ, the new money-market fund rules “have made life more difficult for corporate treasurers and chief financial officers” because they face a sometimes unfamiliar array of investment options as they seek both to preserve and earn some return on their collective trillions.

SEC’s changes make it possible for some money funds to lose value, limit redemptions, undermining their appeal – WSJ

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/14/2016 - The Roundtable Insight: Uli Kortsch On Infrastructure Without Debt

Hedge Fund manager Erik Townsend of Macro Voices is joined by Uli Kortsch in discussing his project Infrastructure Without Debt and the ways it will impact the current banking system.

Uli Kortsch is the Founder of both the Monetary Trust Initiative (MTI) and Global Partners Investments (GPI). Currently most of his time is spent on MTI whose mission is to bring transparency and authentic principles to our monetary system. He was asked to organize a conference on this topic at the Federal Reserve Bank in Philadelphia, the proceeds of which are now published as a book. He is a regular speaker at various conferences in different countries.

As President of Global Partners Investments and other ventures Mr. Kortsch has worked in over 50 countries, written a bill for Congress, and conferred with approximately 15 national presidents, ministers of finance, and ministers of commerce. He has served on numerous corporate boards with both for-profit and not-for-profit organizations.

INFRASTRUCTURE WITHOUT DEBT

The average infrastructure cost is twice the principle amount. The moment you talk infrastructure without debt, you’re saving 50% of all our infrastructure debt.

Right now most people think all of our money is created by private banks, when it’s actually created through deposit creation. If you sign a contract with the bank, that’s an asset to the bank that deposits into your account. The money was created out of nothing. We call that deposit creation, and that’s where our money comes from. If you were charged an interest rate, that interest payment is income for the bank, but the principle is destroyed. It did not exist at the beginning of the loan, and it does not exist when the loan is paid off.

That means in order to have price stability, as our overall production increases then the amount of money in circulation must also increase. And the only way that can increase is through more debt. So we’re constantly increasing the debt load. The US debt load ends up as part of the global debt load of all those who use US dollars. This is a very slow, long term process. Slowly we get to the level where this is not possible. It isn’t just that the government runs deficits, it’s the structure of our whole economy.

WAYS TO SOLVE

One of the way of solving this is to change who gets the seigniorage on the creation of that money. Today the indirect seigniorage goes to the bank, and they use it to charge you interest. People think that banks intermediate funds by moving funds from savers to investors and that the money moves in a circle. Long term, this will result in a crash. Short term, there are ways of solving that. President Lincoln used US notes to pay for the civil war and build infrastructure. It’s Treasury money deposited in the Federal Reserve bank with no interest rate, and the seigniorage goes to us as taxpayers. And that is infrastructure without debt.

Essentially it’s the creation of new Federal notes as opposed to Federal Reserve notes, which could be used to purchase infrastructure.

We are living in a temporary period of time where this could be done easily, because other than asset inflation we do not see much consumer inflation. We live in a time where this would work really well. The Federal government should create Federal Treasury money without the debt created when the Federal Reserve is used as an intermediary.

WHY INFRASTRUCTURE WITHOUT DEBT?

Private banks should not have the ability to create money. That should be taken away from them and given back to the government, so the amount of money created is equivalent to the increase in production. The current disinflationary state we’re in allows for temporary steps, and this has been done before multiple times over the course of history. Guernsey, for 200 years, has also used this method and the results have been spectacular.

No inflation has been triggered by this, though there was a strong inflationary during the 1870s and 1880s, but that had to do more with the terms of trade with the gold-based rest of the world. Because they do not create debt, there is no such thing as equity accounting in government accounts.

POSSIBLE DANGERS

What if this keeps going? This is a nuclear option and can be abused. The assumption is that the banks won’t be allowed to create money anymore, which takes the inflationary part out of this because the price stability portion is locked in. Part of the control is that it should never be 100%. So the US Federal government makes very few decisions about infrastructures; almost all of it is made by municipalities. The funding should never be 100%.

The danger is there, we’re headed for a major crash, and at that point it would be better for the system to radically change. If we could run infrastructure without debt for a few years, people might want to change the entire banking system.

HOW DO WE CONTROL THIS?

According to the system we’re using today, the government only owes what’s on its credit card. Government saving bonds are the “credit cards” of the government, and it only owes the issuance of its Treasuries. What does it actually owe in contract that it’s signed? Here in the US, we owe $205T.

Our money supply is constantly increasing through debt. We stabilize that through interest rates and the desires of banks to lend and borrowers to borrow. We are not going to increase the money supply; we’re currently doing that through debt anyway. We’re just shifting the methodology of how that money is created; only the seigniorage will go to the taxpayers. The amount of money created is identical.

The amount of money that is created, just as it is now, is strictly dependant on our ability to produce. Instead of gold-backed, this is production-backed money. The system is self-regulating, other than the control of the money, which you hand to a deliberately separate group of people under very strict rules. The downfall is that the banks will still make money.

A POTENTIAL SYSTEM FOR THE FUTURE

Under the infrastructure without debt system, banks are divided into two windows dependant on function. There’s the depository window, which keeps your money as yours since there’s no merging of the funds. On the income and investment side, things are mutualized and equity based. During the crash of 2007*2008, mutual funds didn’t go bankrupt because they’re equity-based.

Government insurance can only protect against one bank failing, not a systemic run on the fractional reserve banking system, only a run on an individual bank. It’s nowhere near big enough to protect against a systemic run. In the US, by law, the FDIC has to hold 1.15% of the aggregated deposits.

This whole international system is running on models, and their models are the most important thing, and this should change to human well-being. We need to run our decisions based on true results, rather than what we think the model is.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/13/2016 - INDONESIA Forced Defensively to Aggressively Adopt Financial Repression.

INDONESIA Forced Defensively to Aggressively Adopt Financial Repression.

NOTE FROM FRA: Gordon T Long

NOTE: “Starting in 2016, the government (Indonesia) now requires non-bank institutions to increase the proportion of government bonds in their portfolios to at least 10-20 percent in 2016 and to 20-30 percent in 2017.”

NOTE: “Separately, the government has also lowered various interest rates by force. This year, the micro lending rate has been squeezed down to 9 percent and is expected to be slashed further to 7 percent in 2017.” This tells us that lending and borrowing is primarily about Currency risk.

NOTE: “Indonesia might be tempted to utilize cheap funds provided from some countries like China and Japan that have systematically used financial repression but are now at the end of the cycle struggling to boost global demand by exporting capital. But the government must understand the aim of these countries is to create artificial demand so trade protections must be carefully considered. We can see how aggressive Japan and China export capitals have been to Indonesia ranging in many forms from China-led Asian Infrastructure Investment Bank loans to a series of acquisition by Japanese banks.” Is this one of the real reasons for the creation of the $55T AIIB?

Financial repression policy to maintain economic growth

The end of the commodity boom that peaked in 2011 has forced the government to consider more sustainable ways to cultivate economic growth. With the mining sector struggling mightily, it is easy to fathom why the manufacturing sector is now the government’s favored sector. Most of the recently released regulations aimed at supporting producers at the cost of consumers.

With declining revenues from commodity exports, growth has been sluggish since 2011. Direct investment has become less attractive without sufficient US dollar liquidity to import capital goods.

Private consumption, contributing 55 percent to the gross domestic product (GDP), is usually the stronghold of growth, but government regulatory tendencies are repressing rather than stimulating private consumption. Government spending has been the savior of economic growth, but shrinking state revenues has reduced room for fiscal stimulus.

The budget deficit has consistently widened since 2011, forcing the government to seek alternative sources of income, ranging from tax intensification and extension to the tax amnesty program.

Even with the additional revenue from the tax amnesty program, an increase in outstanding government debt is inevitable to finance aggressive infrastructure spending. To compensate for the remaining revenue shortfall, a form of hidden taxation known better as financial repression, is already well under way.

Financial repression policies include forced lending to governments by domestic financial institutions, interest-rate caps, capital controls, macro-prudential policies and other policies that are aimed to capture and under-pay domestic savers (McKinnon 1973).

The unconventional monetary policy called Quantitative Easing of the US Federal Reserve, European Central Bank , Bank of Japan and Bank of England is also considered financial repression since the goal is to keep interest rates low and create captive domestic audiences (Reinhart 2011).

Starting in 2016, the government now requires non-bank institutions to increase the proportion of government bonds in their portfolios to at least 10-20 percent in 2016 and to 20-30 percent in 2017.

Separately, the government has also lowered various interest rates by force. This year, the micro lending rate has been squeezed down to 9 percent and is expected to be slashed further to 7 percent in 2017.

Additionally, the government has also set the maximum level of time deposit rates for certain banks to only 75-100 basis points (bps) above the 12-month policy rate (previously the Bank Indonesia rate) arguing that currently banks are enjoying too high margins.

This policy is clearly an effort to subsidize the borrower and tax both the lenders and savers, while at the same time encouraging the acquisition of more government bonds. This can also be seen as an attempt to soothe the crowding out effect resulting from the soaring public debt.

The growing middle-income segment could also provide additional strength since the bedrock of the strategy is to provide abundant cheap capital as well as labor. But again to attract foreign direct investment (FDI) and increase competitiveness at the same time, the government must maintain productivity growth running faster than inflation adjusted wage growth.

Starting this year, the government has set a legal formula for the fair amount of annual labor wage adjustment to prevent excessive increases. Labor unions are unlikely to be placated by wage increases being restrained as such so we can expect to witness more angry demonstrators on Labor Day years ahead.

To complete the export-led capital investment growth model, the government has launched numerous economic policies mostly aimed to lure FDI and boost export competitiveness. Mining sector wise, the government has set rules to discourage raw commodity exports, including minerals and crude palm oil (CPO), and is attempting to keep more resources such as coal for domestic needs. But this could mean mining producers receiving lower prices than what global markets can offer.

BI, besides maintaining foreign currency reserves in excess of US$100 billion, is also promoting tighter restrictions on international financial flow, ranging from the mandatory use of the rupiah for domestic transactions to the maximum purchase of foreign currencies. This is another clear example of financial repression. BI argues that the policy is crucial to maintain the stabilization of the rupiah.

In short, financial repression and the export-led capital investment strategy will push growth away from reliance on consumers toward producers instead. The benefits are obvious; Indonesia can escape from the curse of being reliant on natural resources while grabbing a larger share in global supply chains. FDI can more easily be attracted with Indonesia becoming a strategic and efficient production base.

But to be successful, this policy must be accompanied by a realistic long-term industrialization plan with export promotion as the main theme. China, Japan, and South Korea have taken this path and become large and efficient exporters of manufactured goods and have transformed themselves from net capital importers to exporters.

Yet some risks are unavoidable. It is important to note that financial repression goes against the law of economics by preventing adjustment of many macro variables such as interest rates, wages and exchange rates. Like the commodity based growth, this export-led capital investment growth model can easily lead to chronic economic imbalances. Global imbalances helped fuel the 1997 Asian Financial Crisis, even though it was not the initial primary cause. Grasping what went wrong in previous crises could be a good start as a precaution.

Indonesia might be tempted to utilize cheap funds provided from some countries like China and Japan that have systematically used financial repression but are now at the end of the cycle struggling to boost global demand by exporting capital.

But the government must understand the aim of these countries is to create artificial demand so trade protections must be carefully considered. We can see how aggressive Japan and China export capitals have been to Indonesia ranging in many forms from China-led Asian Infrastructure Investment Bank loans to a series of acquisition by Japanese banks.

Moreover, in most cases, a financial repressor country will support trade protection and at the same time promote an undervalued currency not only to maintain competitiveness but also as another way to discourage the demand for imported goods although this can’t be likened to import substitution-industrialization policy.

This could nourish a great systematic risk in the future considering what misery exchange rate controls can bring to Indonesia, a country with huge foreign currency liabilities. To avoid this situation in the future, the speed of how the government can raise the onshore participation in domestic financing is crucial.

______________________________

The writer is an economist at PT Samuel Sekuritas Indonesia. The views expressed are his own.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/03/2016 - Allianz’s CIO Andreas Utermann says: Expect to Suffer a Generation of Financial Repression

Andreas Utermann, Allianz’s Global CIO was commended recently by Tom Keene on Bloomberg’s Surveillance for willing to even mention Financial Repression on a public broadcast, a subject it appears that is frowned upon in polite, well connected Wall Street circles.

What comes out in this short video interview by Bloomberg is that Allianz’s CIO expects Financial Repression to be around for the next generation. It simply isn’t about a few more years but rather about the next generation learning to live with it.

“It isn’t a question of years but about generations!”

He firmly believes it has become quite evident that the current policy targets aimed at increasing inflation to 2% are not working. Policy makers just don’t know how to solve the problem. However, this will not stop the Macroprudential policies of Financial Repression.

Maybe most significant in the Bloomberg interview is that Utermann is willing to state publicly that he believes the Federal Reserve is intentionally behind the curve. The Fed want’s rates to rise behind increasing rates of inflation.

The Federal Reserve is intentionally behind the curve.

Because of Financial Repression the Fed want’s rates to rise behind increasing rates of inflation.

Listen to how Allianz believes you solve today’s yield problem …

Utermann: Suffering a Generation of Financial Repression

Andreas Utermann, global chief investment officer at Allianz Global Investors, discusses the factors holding back global central banks from normalizing interest rates, differing economic philosophies in the Eurozone, and dealing with chronic financial repression. He speaks on “Bloomberg Surveillance.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/30/2016 - The Roundtable Insight: Macleod, Stoeferle, Boockvar, Townsend On Central Bank Effects

Hedge Fund manager Erik Townsend of Macro Voices is joined by Alasdair Macleod, Ronald Stoeferle, and Peter Boockvar in discussing the effects of central bank policy on global markets, along with debating the option of investing in gold versus mining stocks.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

Ronald is a managing partner and investment manager of Incrementum AG. Together with Mark Valek, he manages a global macro fund which is based on the principles of the Austrian School of Economics. Previously he worked seven years for Vienna-based Erste Group Bank where he began writing extensive reports on gold and oil. His benchmark reports called ‘In GOLD we TRUST’ drew international coverage on CNBC, Bloomberg, the Wall Street Journal and the Financial Times. Next to his work at Incrementum he is a lecturing member of the Institute of Value based Economics and lecturer at the Academy of the Vienna Stock Exchange.

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University.

EFFECT OF US PRESIDENCY ON GLOBAL MARKETS

Trump has managed to appeal to the disaffected masses, so we have very little clue how he’ll perform if elected president. The possibility he’ll win is higher than the polls and media discount, as the public seems to be disgusted with the political establishment and want change. But regardless of who the next president is, in the early part of their term they’re going to preside over a recession. Both will face the same challenges. Central banks have manhandled markets over the past eight years, and will still be the deciding factor.

Trump has set up a situation where if it looks like he’s going to be elected, markets will tank. And Hilary will keep things at the status quo, where the government and policies are still for sale to Wall Street through bribe money in the form of political campaign contributions.

FED POLICY AND A BEAR MARKET IN BONDS

Increasingly the central banks are trying to stop a bear market in bonds from materializing. If you look at central banks in Europe, some of them are overloaded with sovereign debt. If you get a substantial bear market in sovereign debt, those banks basically go under. 2017 is going to see an acceleration in price inflation, to the point where the Fed and other central banks are going to have to raise interest rates, but they can’t do that without breaking the system.