01/09/2017 - Dr. Marc Faber: Federal Reserve Likely To Launch QE4 In 2017

“Let’s say the Fed realizes that the deficits for the U.S. go up and that interest rates increase and that the economy slows down, do you really think that they will increase the Fed funds rate three times in 2017? Never. What they will aim at, then, is to essentially bring interest rates down, especially if by then the dollar is still strong. And so they will probably launch QE4 in 2017. I think that will be a surprise for many people — not for me, but for many people that will be a surprise.”

Also recommend watching the below video interview: Dr. Marc Faber sees emerging markets as outperforming the U.S., the U.S. Treasury Bond Market likely to correct (go higher) in the short term, & the U.S.$ likely peaking in 2017 .. sees the world’s big central banks – Federal Reserve, Bank of England, ECB and Bank of Japan – as coordinating monetary policies together on a global basis.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/07/2017 - The Roundtable Insight – Update On India’s War On Cash From Jayant Bhandari

FRA is joined by Jayant Bhandari in discussing the continued effects of India’s war on cash on the Indian economy.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

INDIA’S WAR ON CASH

With respect to Alasdair Macleod’s recent writings, India will completely fail in trying to making this country cashless. They don’t really have the competency, it’s a technologically backward country, and almost a billion people do not have internet or telephone connections, even in big cities. Electronic transactions won’t be able to work.

This is a country of GDP per capita of $1700, the government has done absolutely no planning, and in the last 55 days since they announced demonetization, they have released 70 notifications of changes. The government has done no planning. All they have done is print two different bank notes, and they are extremely badly printed, with errors and poor quality paper and ink. Imagine how incompetent the Indian government must be, that they can’t even print in a printing press properly.

The whole situation is absolutely crazy, and the government is incredibly incompetent.

WHAT’S HAPPENING IN THE ECONOMY

There have been reports showing how economic activity is beginning to fall precipitously. Things are cheaper than they were two months ago, and the reason is that poor people don’t have the cash to buy anything. Remember that 80% of this country is poor, and this is the population that works in the informal economy. They don’t have jobs and can’t buy food. Food prices have fallen and the middle class is happy, but these are the people who are the backbone of this country. When they lose jobs, they will riot and create crime, and at the end of the day the formal economy sits on the back of the informal economy. These people earn $1-2 a day, and they can’t make banking part of their lifestyle.

70-80% of India’s population will go half-bankrupt. When the next cycle starts, farmers won’t have the money to plant seeds anymore, which means that food production will fall in the next few months and food prices will go up. This hits the middle class and the formal economy, and the formal economy is already very badly hit. People are sitting on their money because they can’t do anything with their money since government tax collectors are rapacious and corrupt. There’s so much anxiety and fear among small businesses and savers.

CURRENCY PROBLEMS

There likely won’t be a currency collapse because the government has a monopoly on currency and all the money in your bank account is frozen. The biggest problem is that one person has a monopoly on the economic blood circulation of the society, and he has completely destroyed it. The economy will suffer, and socially and culturally this society will face horrendous problems going forward.

India has always been a totalitarian country, but it’s increasingly become more and more totalitarian over the last seven years. We are reaching the peak where this will become completely totalitarian, and the only result will be massive chaos and problems in the society and possibly the disintegration of India.

The stock market is going down in Rupee and Dollar terms, but the Rupee is continuing to fall. But if you’re invested in this stock market you can’t really take your money out. The reality is that when foreign investors understand what India is doing, they might stop bringing their money into the country and the result may be that the stock market will fall extremely quickly. India has been a negative yielding economy forever and now that they have destroyed the economic backbone of the country, the stock market can and should fall going forward.

A lot of bartering is starting to happen in rural places where economies aren’t very complex. The transaction costs for bartering are huge, and create massive anomalies in the economy. It doesn’t work in more sophisticated environment where you are doing proper business and exchanging modern goods. Hopefully people will start exchanging gold in place of cash for bigger transactions, because governments’ monopoly on cash is disastrous and extraordinarily risky for any society.

EFFECTS ON GOLD

There is a chronic fear in the society and raids are happening. The government has told people that anyone owning more than 500g of gold might be assessed for tax. The problem is that you can’t prove to the government that you own gold that has been passed down or gifted. This boils down to paying unnecessary taxes and a huge amount of bribes. Corruption has skyrocketed in the last two months because this is now a police state and in a police state you don’t question the police.

The price of gold went up to $3000/oz a few days after the demonetization was announced, and now has fallen to the international rate. The street price is 10% more than the international price because there’s a 10% customs duty on imports of gold. Most of the gold come through smuggling channels, and these smugglers make a massive amount of money.

BitCoin or something similar will likely be important tin convincing Indian to move their money out of the country. The reality is that Indians have been very inward looking. But now for the first time people are considering how to move their money and gold out of the country. Governments will almost certainly institute capital controls and put restrictions on gold ownership sooner rather than later. If they don’t, people will buy gold with credit or move their money abroad using foreign exchange channels. The government will remove those possibilities in the near future.

Historically people have moved their money into silver and farmland, and Indians will do that to protect their wealth from the government.

India was never growing at 7.5%. The Indian economy is stagnating and this country continues to be irrational and tribal. They haven’t been using the technology they’ve gotten from the west, food habits have gone bad, and disease is growing rapidly. There’s a huge amount of chaos, and will likely disintegrate in a few years’ time.

GLOBAL PARALLELS

Similar things are happening in the rest of South Asian countries and the Middle East. Much worse is happening in Africa. These 2.5B people are in chaos right now. All of these people are tribal societies with a natural organic inclination to become tribal again. A lot of these countries will change their shape over the next few decades and go through major problems.

The problems of the emerging markets – particularly the South Asia, Middle East and Africa, is extremely high and bad.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/06/2017 - The Roundtable Insight – Peter Boockvar And Yra Harris On The 2017 Outlook

FRA is joined by Peter Boockvar and Yra Harris in discussing their expectations for 2017, along with predictions for Europe and the global debt crisis.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University. Check out Peter’s new site at www.boockreport.com.

2017 OUTLOOK

There’s going to be this tug-of-war over Trump and the tax and regulatory policies he hopes to pass and initiate, and financial conditions that will continue to tighten in the interest rate perspective. Since November, the focus has been on the positives of Trump, and when people start looking at the details, people will have to acknowledge that what got us to record highs in the stock market was QE and zero interest rates. At some point we’ll have to shift back to interest rates and the uncertainty of what Trump will pass and the offsets in terms of tax policy.

What you failed to see materialize was a lot of year-end tax selling, except for losses. This is not a Reagan phenomenon. There are so many vast differences, mainly the debt load piled on the US and global economy. For every 100 basis point increase in interest expense is $470B. Despite all this excitement over the corporate tax income cut, there’s not enough attention being paid to the potential offsets. There’s a potential border adjustment tax, and a credit addicted economy where they may be taking away the deductibility of future interest expense.

Debt has to be serviced. It’s not all coming due in this year, but we don’t know how much of it is floating. If Trump changes the tax code, a lot of people will see when interest deductions will not be part of the equation anymore, just how great the impact will be on corporate earnings. If Trump doesn’t get these offsets, the corporate tax rate isn’t going to make it to 15-20%. People are going to start digging into the details of the Trump plan, and they’re going to realize there’s no free lunch here. Because of the size and depth of the deficit, he can’t just cut taxes. There’s going to be an offset, and that’s what people have to start paying attention to.

FISCAL DEBT DRIVING US DEBT

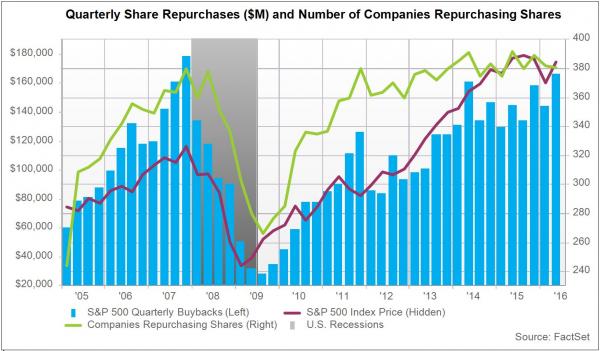

Entitlement obligations are now at 10% of GDP and rising. This trend is expected to escalate, give then trillions of unfunded liabilities obligated toward entitlement. On the private side, corporations have taken out about $620B for the share buybacks, and if rising interest rates begin to reverse that trend, that’s a big factor that could have the markets going in the other direction.

We’re seeing some political maneuvering from Trump, who’s controlling his narrative. We’re about to see the difference between campaigning and governing, and the reality of the latter.

KEY THEMES GOING INTO THE NEW YEAR

Rising inflation; slowing growth

US growth is still around the 2% level, but the question for 2017 is how much of the positive sentiment numbers that we’re seeing in manufacturing etc. is hopes and how much is actual improvement in business activities. Right now it’s still hopes, and GDP for 2017 is still going to be around the 2% level and we’re not going to see the benefits of Trump until 2018. Inflation levels are moving higher, partly due to the rate of change of the base effects of the decline in energy, on top of high prices of medical care and rent. We’re seeing inflation expectations rise in Europe and the US, and it gets down to how the Fed responds to that.

Interest rates may mug the markets and trump over reality. What got us here was QE, negative interest rates, and zero interest rates in the US. To think that that can reverse with no pain, and somehow fiscal policy will offset that, is delusional.

THE PROBLEM OF GERMANY

The most important area is going to be the Euro. The only way out of some of the mess that they’re in is for Germany to have higher inflation. Right now with the Deutschmark 10% lower, the German current account surplus is about 8.5% of GDP. And yet, there’s nothing they can do about it because Germany is tied into this weak economic consortium, and they’re benefitting from it with phenomenal growth. The weaker the Euro goes, the more benefit Germany gets anyways. This is the year where Germany will have to decide if they’re going to be the transfer agent for all this growth. The operative question for this year is: who guarantees the ECB’s balance sheet?

We’re going to see firsthand the fallacy of demanding 2% inflation. Draghi doesn’t realize the epic bond bubble that he’s created. When you have huge amounts of negative yielding bonds in Europe and anemic levels of interest rates, and at the same time he wants 2% inflation. He’s desiring something that’s going to blow himself up.

As we head into 2017, Europe is going to become the centerpiece of the global financial system. It was a 50% decline in the value of Japanese and European banks that finally got them to realize flattening your yield curve into the ground is not a good idea. We are in the last inning of this last bout of monetary easing. People should not lose sight that interest rates, while still extraordinarily low, will move higher in the coming years and they should be prepared for that.

The markets are beginning to take some control. We’re going to get a rise in interest rates, and we have a very sensitive equity market.

As of 2015, of the profit pie, labour got the smaller share since WWII. That’s now beginning to shift, but there’s a lot of catch up on the labour side in terms of wages. While that’s good for earners, it’s not going to be good for corporate profits and companies will have to either slow down hiring or absorb those costs, or pass it on as higher prices.

EFFECTS OF CHINA

Right now non-performing loans in China are at 15-20% of GDP levels. China’s fallen into the same trap as the US, where it takes more and more debt to generate more GDP. This obsession with 6-7% growth has put them in this trap. The level of credit it takes to generate this level of GDP is out of their control. Growth will continue to slow, and debt will continue to become a big problem, but China’s one big black box in the sense that they could throw a lot of things under the rug and keep it there in some controlled way. It’s very difficult to forecast how Chinese authorities are going to manage that.

If China were to implode and let their currency depreciate, then we’d have to change our scenarios because that could send a tidal wave of disinflation around the globe and they’ll just be exporting regardless of price. Their problem is far too much capacity, and unless they can miraculously shift their economy from an export oriented to a phenomenally domestic economy, and that won’t be an easy task with that debt load. If China makes the transition, food will be an important thing.

COMMODITY MARKETS FOR THIS YEAR

Gold’s going to trade where real interest rates are, and if you think Janet Yellen will be slow in raising interest rates in response to a rise in inflation, then you should be positive in gold and silver. It’s handled two rate hikes and a 14 year high in the dollar, and it’s still a hundred off the lows of last year. That was the bottom in this bear market, and higher prices are expected. With respect to emerging markets, Brazil and South Korea have good political direction and should be positive.

If you see the German inflation numbers, it’s obvious they’re debasing their currency as a way to bail out the EU.

BitCoin is up 150% year over year. Over the last couple of months it’s doubled. There’s something very wrong that BitCoin is doubling like that while gold is suffering. There’s a push for a non-fiat type currency. Right now they’re buying BitCoin, but the difference between gold and BitCoin is nonsensical.

The ECB will become the big issue for the German elections come September.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/05/2017 - Former Goldman Sachs Managing Director Nomi Prins On Artisanal Money To Support Government Debt

“Why is this all happening? We had a financial crisis. It was scary for a lot of reasons. It was started in the United States. The biggest six banks in the United States have not really suffered in the wake of this financial crisis. The biggest six banks were at the core of the financial crisis are now 86% bigger in terms of assets, they are 43% bigger in terms of deposits. They have more tract in the derivatives market. They have more tract terms of the trading assets market. They are simply more powerful than they were before. They are continuing to be batted with settlements for crimes ranging from mortgage related crimes (the crux of the crisis), to libor scandals, to rigging foreign exchange to scamming customers. These crimes manifest in several ways, as we saw when Wells Fargo, one of the big six U.S banks, charged fees to its customers that they did not even have .. These banks have only been subsidized by, first our Federal Reserve and then internationally the cooperation of central banks – in a way that has never existed before. In the wake of our crisis, when the Federal Reserve brought money down to zero, they created Artisanal Money. It is not actually printing money. It does not require physical activity. It is the idea of creating money in all sorts of different ways to make its availability easy, its cost zero (or negative), of buying bonds (to continue to support government debt). They have made a policy supporting government debt by moving it to the central banks – in terms of purchasing. These central banks have created a whole dislocation of the nature of pricing in every single asset class.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/05/2017 - Former Fed Advisor Danielle DiMartino Booth’s “FED UP”

Amazon: “An insider’s unflinching expose of the toxic culture within the Federal Reserve. In the early 2000s, as a Wall Street escapee writing a financial column for the Dallas Morning News. Booth attracted attention for her bold criticism of the Fed’s low interest rate policies and her cautionary warnings about the bubbly housing market. Nobody was more surprised than she when the folks at the Dallas Federal Reserve invited her aboard. Figuring she could have more of an impact on Fed policies from the inside, she accepted the call to duty and rose to be one of Dallas Fed president Richard Fisher’s closest advisors. To her dismay, the culture at the Fed–and its leadership–were not just ignorant of the brewing financial crisis, but indifferent to its very possibility. They interpreted their job of keeping the economy going to mean keeping Wall Street afloat at the expense of the American taxpayer. But bad Fed policy created unaffordable housing, skewed incentives, rampant corporate financial engineering, stagnant wages, an exodus from the labor force, and skyrocketing student debt. Booth observed firsthand how the Fed abdicated its responsibility to the American people both before and after the financial crisis–and how nobody within the Fed seems to have learned or changed from the experience. Today, the Federal Reserve is still controlled by 1,000 PhD economists and run by an unelected West Coast radical with no direct business experience. The Fed continues to enable Congress to grow our nation’s ballooning debt and avoid making hard choices, despite the high psychological and monetary costs. And our addiction to the ‘heroin’ of low interest rates is pushing our economy towards yet another collapse.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/05/2017 - Peter Boockvar Observations Going Into 2017 – The Boock Report

“No one should be so naïve to think that US growth and the price of assets won’t be impacted by higher interest rates, whether Fed induced on the short end or market driven on the long end. We’ve pulled forward economic activity (autos in particular) and returns in a variety of markets (bonds, stocks, and commercial real estate most notably). Financial conditions will tighten further in 2017 and I include this quote from my friend David Rosenberg, ‘There have been 13 Fed rate hike cycles in the post WWII era, and 10 of these landed the economy in recession and the three that were aborted – the mid 1960s, the mid 1980s and the mid 1990s – were only aborted because the economy either slowed precipitously or there was a financial accident that forced the central bank to the sidelines. There has never been a Fed hiking cycle that ended benevolently’ .. The ECB and BoJ will continue to damage the business model of their banking systems due to negative interest rates and suppression of market rates that has flattened yield curves.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/04/2017 - India: Eliminating Cash Leading To Economic Downturn

Financial Repression In India:

Eliminating Cash Leading To Economic Slowdown, Loss Of Confidence In The Currency

“The Indian government’s clumsiness in banning R500 and R1,000 notes is certain to lead to an economic and financial crisis. Looking on the bright side, it might lead to the collapse of the Modi government. If that happens, it may delay the same medicine being dispensed by other governments to nations in a similar state of development and tempted to pursue similar objectives .. The expected gains to the state are obvious, and one can see why politicians will favor the deployment of financial technology, such as mobile banking, to achieve these ends .. It appears all countries are going down this digital route .. What’s particularly concerning for the individual is the way nations appear to be ganging up together into an unelected unaccountable super-state .. We are already used to the state controlling the interest we pay and receive on our money. Banning cash increases the depth of this control, with savings and deposits being taxed through negative interest rates. The super-state’s cabal of central banks coordinates managed interest rate policies, either by liaising directly, or through the forum of the Bank for International Settlements. Quantitative easing, the direct control of bond prices through central bank purchases, reduces the risk that the market will challenge central bank policies, at least for the short-term .. Eventually, governments will destroy themselves following these political and economic policies, because the states and their experts delude themselves that they understand economics.They do not wish to understand the reasons why markets free of government interference lead to prosperity, and why government micro-management always ends in tears. Consequently, they do not see the risk to statist domination, because it comes not from private individuals, but from the states themselves. Banning cash will almost certainly speed up the decline of an electronic currency’s purchasing power, because its public rejection has the potential to become instantaneous .. Just watch how the cashless rupee behaves. Compare the potential for price inflation in a cashless economy with the Weimar or Zimbabwe inflations, when cash generally had to be obtained before it was spent. Rudolf Havenstein, President of the Reichsbank in the early-1920s, had the printing-presses working twenty-four hours a day churning out currency notes to meet an escalating cash shortage. Today, not only is access to money instant, but it is to credit as well. Currency collapse could be the greatest threat to planned national socialism. During a currency collapse a state’s liabilities will rise along with everyone else’s .. A prosperous economy is one where individuals keep and invest their wealth productively, as all experience has shown.” – Alasdair Macleod link here to the reference

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/04/2017 - JP Morgan On Financial Repression From Central Bank Policies

JP Morgan: “‘True Believer’ central banks have created unprecedented distortions in government bond markets. Bond purchases and negative policy rates by the ECB and Bank of Japan led to negative government bond yields. Whatever their benefits may be, they also resulted in profit weakness and stock price underperformance of European and Japanese banks. The poor performance of European and Japanese financials was a driver of lower relative equity returns in both regions in 2015/2016.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/24/2016 - Outlook For 2017

Here is our view of the macro-economic state of the global economy and the risk factors going into 2017.

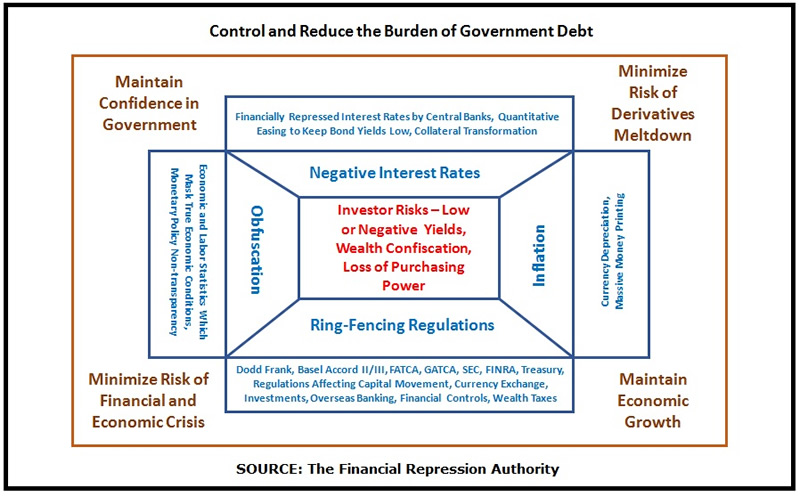

Overall, we continue to see ongoing adverse risks to investors from the unintended consequences of generally good-intentioned central bank and government policies and regulations arising from the challenges of managing escalating debt and fostering economic growth:

The results of these central bank and government policies and regulations are now being manifested as worsening public and private debt, a stagflationary global economy, an emerging public and private pension crisis, and unsustainable entitlement obligations.

4 pillars of financial repression – negative interest rates (whether in nominal terms or in real terms), forced inflation, ring-fencing regulations and obfuscation – are in turn resulting from the above-mentioned central bank and government policies and regulations.

In turn these 4 pillars are presenting the adverse risks to investors. For investors, the focus then becomes identifying assets (both public and private) and more importantly appropriate risk management in order to meet the investor goals of getting yield, preserving purchasing power and creating wealth.

Let’s look at the results mentioned above which are now being manifested – worsening debt, stagflation, pension crisis and entitlement crisis – as the key factors affecting the global economy and the financial markets heading into 2017:

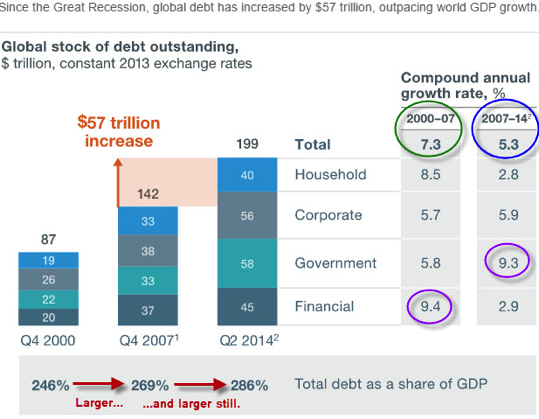

Escalating Debt & Debt Servicing Costs, Unsustainable U.S. Entitlement Spending, A Slowing Global Economy

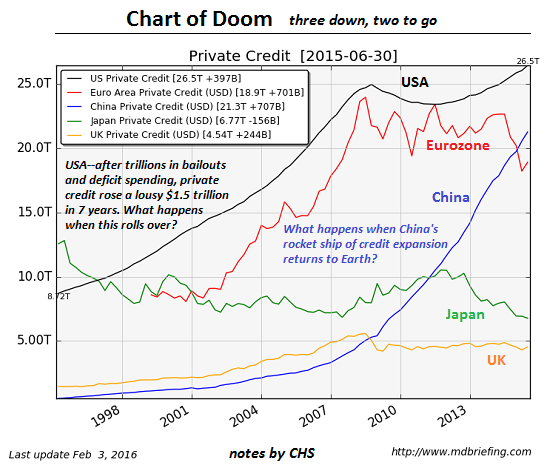

The combination of rising interest rates and escalating debt is causing debt servicing costs to escalate. This is putting a damper on global economic growth. Some charts on this are shown below. Central banks have attempted to alleviate the challenge through negative interest rates and forced inflation – 2 of the 4 pillars of financial repression. The debt challenges are not only in the U.S. – in China for example, non-performing loans are now at 15%-20% of GDP levels (according to Moody’s) .. and in Italy, the non-performing loan numbers may be closer to 25% of GDP levels!

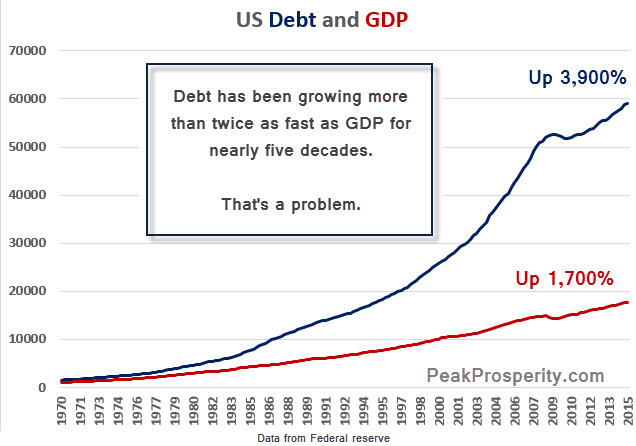

Courtesy of Peak Prosperity

Courtesy of Peak Prosperity

Courtesy of Charles Hugh Smith

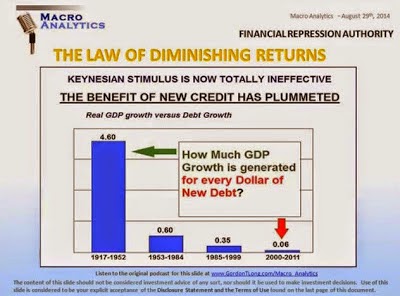

Courtesy of Gordon T Long and FRA

On the fiscal challenges driving U.S. debt, entitlement obligations are now at 10% of GDP and rising! This trend is expected to escalate U.S. debt levels, given the trillions in unfunded liabilities obligated towards entitlements.

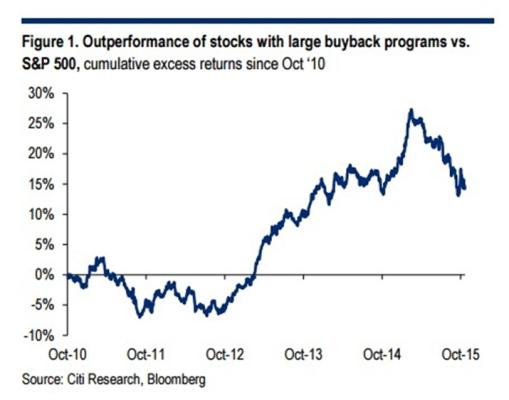

In addition, corporations have taken out a significant level of debt to use in buying back their equities – it has been estimated that there has been $620 Billion borrowed & used in this regard during the last 12 months alone.

This corporate debt will be a challenge in managing going forward, especially in a rising interest rate environment.

A Stagflationary Global Economy

Given the push by the new U.S. Administration through President-Elect Donald Trump to lower U.S. corporte taxation rates from 35% to 15%, this could be a major positive on the economy and the financial markets. In addition, Japan, Canada, the U.S. and China are implementing or are planning for major infrastructure fiscal-stimulus spending – although it may not be until into 2018 for the infrastructure spending in the U.S. and Canada to be implemented.

Putting all these developments together – the escalating debt challenges mentioned above, rising interest rates, rising inflation and global fiscal stimulus spending in a world of slowing global trade – this is all resulting in a stagflationary environment.

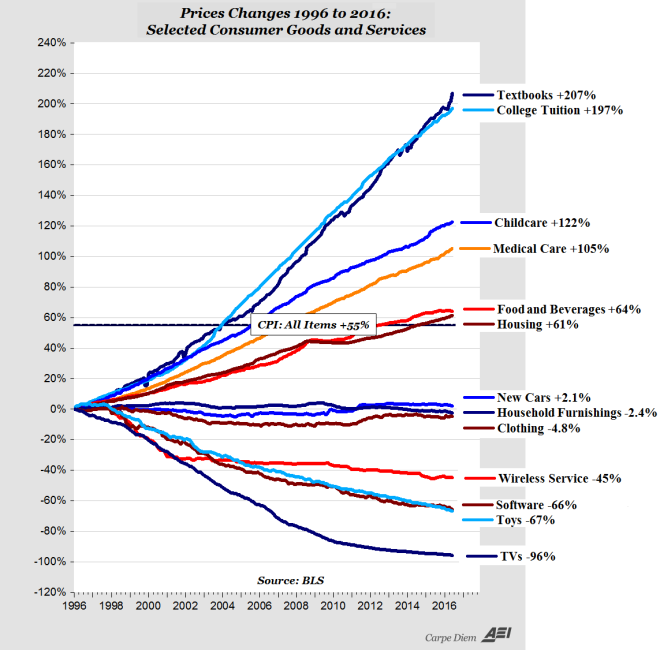

There is rising price inflation, generally being seen in things that people need – food, education, health care, and insurance – versus things where globalization or technological development has significantly brought costs down – electronics, consumer products, outsourced services, etc.

Shrinkflation – smaller food volumes at the same price

Shrinkflation – smaller food volumes at the same price

Courtesy of Charles Hugh Smith

Courtesy of JP Morgan – Inflation and Inflation Forecasts

Courtesy of AEI – U.S. Inflation Breakdown

Hedge fund manager Dr. Albert Friedberg of the Friedberg Mercantile Group:”We are going to see an expansion of the federal deficit, we are going to see long term interest rates going higher, we are going to see a Federal Reserve chase after inflation going higher .. Our forecast, and the direction taken by our portfolios, is for accelerating inflation over the coming months. This phenomenon will take markets and officials by surprise, and I believe that it will change the world we know today. Financial repression will continue to be the order of the day, partly because central bankers will remain in intellectual denial and partly because of fears that rate normalization will bring economic activity tumbling down.The early part of this period of accelerating inflation should prove beneficial to many assets, among them commodities and well financed equities. Coming out of denial — beyond our investment horizon — will be painful and very damaging to debt burdened sovereigns and corporations.”

An Emerging Pension Crisis

The developed world is in an escalating pension crisis – both at the public level & at the private level. Pension funds are finding it increasing difficult to meet their obligations, given the very low or even negative interest rate financially repressed environment.

Danielle DiMartino Booth – Former Advisor to the Dallas Federal Reserve President: “There is a distinct cerebral pleasure, relief even, derived from lapsing into a state of suspended disbelief .. Add up all our great states and Moody’s math comes up with $1.75 trillion in what will be pension underfunding by the time we’ve said adios to fiscal year 2017. That represents a 40 percent jump from fiscal year end 2015 .. The Federal Reserve is fully aware of the inferno burning under the surface of the nation’s public pension system and the direct effect their interest rate policy has had in exacerbating pension underfunding .. Unlike other countries, whose pension disasters will also be all consuming, U.S. laws allow accounting chicanery that obfuscates the gravity of the degree of underfunding. But have no doubt, these chickens will come home to roost though these manias always last longer than we can envision.”

Here is a table showing underfunding challenges for some corporations:

Investment Environment Implications

Many of the fund managers, economists and industry leaders we follow and interview see the following potentials for the investment environment:

selective opportunities in equities with the potential for a “Minsky Meltup” (see commentary by FRA’s Co-Founder Gordon T Long below)

the potential for infrastructure-related and innovation-related investments, including those involving public-private partnerships (PPP)

the potential for a strong commodity market, especially in base metals and agricultural commodities

depending on the strength of the U.S. dollar and the unwinding of U.S. dollar denominated corporate debt, the potential for investments in emerging markets, especially those which have a focus in base metal and agricultural commodities

the potential for a short-term bounce in U.S. Treasury bonds, before going lower for the medium-to-long term trend; this trend is bearish for most bond markets

the potential for store-of-value assets in safe storage and secure jurisdictions of the world

the potential for basic businesses with little or no debt, with little or no leverage and with high discounted free cash flows

A risk-mitigated approach to addressing the market, credit and operational risks can help an overall investment strategy. For 2017, we see intensifying operational risks – the war on cash and gold spreading, along with tightening capital and currency exchange controls, new regulations adversely affecting the freedoms in the movement of capital, new and increased wealth taxes at all levels, and adverse changes to rules affecting registered retirement and pension fund accounts.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/23/2016 - The Roundtable Insight: Danielle DiMartino Booth & Peter Boockvar On The Market Outlook Into 2017 & Consequences Of Federal Reserve Policies On The American Dream

FRA is joined by Danielle DiMartino Booth and Peter Boockvar in discussing the impact of the Trump administration on the market, along with its effects on US pension funds.

Danielle DiMartino Booth makes bold forecasts based on meticulous research and her years of experience in central banking and on Wall Street. Known for sounding an early warning about the housing bubble in the 2000s, Danielle offers a unique perspective to audiences seeking expertise in the financial markets, the economy, and the intersection of central banking and politics.

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University.

FINANCIAL MARKETS AFFECTED BY TRUMP

The market is celebrating the possibility of major tax reforms, regulatory changes, and infrastructure. The main focus right now is tax reforms. The trade issue is not necessarily going to be one thing; it’s potentially going to be a variety of things as things progress rather than anything particularly planned. The market is celebrating the possibility that we can break out of the 2-2.5% GDP range over the next couple of years. It’s driven by tax policy that’s more conducive to capital investment, which has been a drag on GDP. That’s the optimism; the question is whether it’s going to get passed and when it’ll be impactful. If it does pass, we’re not going to feel the impact until 2018-2019. In the meantime, there are still challenges the US economy faces, both in terms of US growth, global growth, and changes in monetary policy and a different direction in interest rates globally. There’s a tremendous amount of optimism going into the New Year, but it’s really going to come down to timing. After inauguration day we might see markets take a step back.

Infrastructure spending is going to be the second thing administration focusses on. They want to get this tax bill passed, and they need to do it as revenue neutral as they can. They’re going to spend the most amount of capital on that, and infrastructure spending is not happening any time soon and shouldn’t even be part of the discussion right now. Trump will be expending quite a bit of his political capital on appointing someone to the Supreme Court right away, as well as gathering up the money needed to push through the infrastructure spending. February 2017 will be the third longest economic expansion in the post WW2 era, and you have to ask yourself if this economy is going die of exhaustion.

Interest rates are moving higher and historically those long term long time expansions have been tripped up by rises in interest rates. What got us here was a decade of zero interest rates and massive quantitative easing, and now we’re seeing no QE and rising interest rates. We’ve built this economic and market construct that’s addicted to low levels of interest rates. So we can all be excited about Trump liberalizing the US economy, but he still has to deal with the unwinding of the biggest bubble we’ve ever had. And that’s not going to be painless.

A CHALLENGE TO INFRASTRUCTURE SPENDING

Politically speaking, it goes back to the support Trump is going to find within his own Republican party. You can pass spending bills of the magnitude of something like Obamacare much more easily if borrowing costs for the government are 1.8%. If you look at US debt, you’re talking $47T of debt. Not all this debt matures in the same year, but over the next couple of years we have massive debt maturities and that’s going to happen at a higher cost of capital. Higher interest expense is going to eat into the benefits of lower corporate tax rates and other regulatory letups from the government. When you create a debt bubble and then get a rise in interest rate, that’s going to hurt people who are over-levered and don’t have enough cash to offset that.

Rising interest rates could present a formidable challenge and you add to that the sheer amount of supply that’s coming online, whether you’re talking about the hotel sector, the multifamily sector, the amount of shadow inventory weighing down the office sector, and retail. We’ll be seeing more announcements of brick and mortar locations closing after this holiday shopping season. At some point, the simple number of units of supply implies that refinancing is going to be extremely difficult because you won’t be able to offset the increase in interest rates. There’s too much capacity in real estate and the economy is only running at about 70%. Trump can lower taxes to zero but we still have to work through the extra capacity built up in a variety of industries. This is going to take years to work through, regardless of Trump and the policies he passes.

INTERNATIONAL EFFECTS

Europe is plagued by slow growth, enormous amounts of debt, and the ECB has distorted their entire financial system. The European bond markets are unprepared for any rise in inflation and any taper whatsoever. China should be in the forefront again, as they’re trying to moderate their property market without crashing it. Japan’s bond market will be part of the global rise in interest rates. With markets overvalued in many different error classes, there’s no margin for safety and no room for error. There will be a lot of focus in the coming year as it pertains, especially to China, to how quickly they can run through their reserves.

The cost of hedging out your currency has gotten to the point where it’s not profitable to do so unless you can get a really high rate of return. It’s easier said than done. One of the potential unforeseen hiccups going into 2017/2018 as we see the potential for the global economy to slow more, is that there might be a need for a lot of the amount of money flowing into the US commercial real estate from foreigners to go back home.

It appears that Trump has put some rational people in with him, and someone has told him that China does not qualify, on paper, as a currency manipulator. Even threats of it from Trump are enough to slow things down.

TREND AGAINST PHYSICAL CASH

With Trump in office, we have the chance to put rational people at the head of the Fed who don’t want to abolish cash. You’ll have many people in this country revolt if they threaten to get rid of any denomination of cash. This country is much less conducive than India to pull something like that off. A lot of it is more talk than action, especially in the US where people voted for Trump because they were anti-establishment, and getting rid of cash is the epitome of an establishment move. Our central bankers here have been able to benefit from and learn from Japan’s failure at implementing negative interest rates. Central bankers worldwide have a blueprint of how to not eradicate cash, because of how severely it’s impacted India and the people who live inside who’ve been devastated by it.

DESTRUCTION OF THE AMERICAN DREAM

Even though we’ve had quite a bit of deleveraging, household debt has become a way of life for Americans. The average American family today has $1600 in credit card payment, and the interest rate was at 19%. Central banks placate the masses with household debt and making it accessible, rather than forcing the government to make more difficult choices and allowing us to continue to be a save and invest economy. Other countries that have different cultures than ours have their sights set on the weaknesses it exposes in our social fabric.

As noble as central bankers think they are, in practice all they’re doing is encouraging you to borrow money. That’s why they think lower interest rates are good and higher interest rates are bad. Now we’ve reached a point where the US economy has levered up to such an extent that we are so sensitive now to any changes in interest rates and financing that debt. Instead of creating a savings and investment culture, we’ve created a borrowing and spending culture instead. That’s something that has to flip around and reverse itself, but it’s going to be a messy process.

STRUGGLING PENSION FUNDS

There’s not enough time to make up for what’s been lost by the assumed rate north of 7% not being compounded all these years and having gone in the opposite direction, to say nothing of what will happen when markets correct and take down the liquid part of pension portfolios. They’ll be left with the understanding and realization that private equity is not only an inappropriate investment risk-wise, but also a devastating investment because of the lack of liquidity. Pension funds were piling into real estate at the peak of a cycle, they were piling into private equity just as there’s a possibility that the Trump administration is going to end tax deductibility of interest expense on new debt accumulated going forward, which dramatically damages the entire private equity model. It’s chasing yesterday’s winners, and pensions have done it over and over again.

They’re not being honest with their constituencies who think that their retirement money is there. That money does not exist, but the politicians out there aren’t being honest with their constituencies.

The political appetite for government bailouts on pensions are going to be very low. Could it be possibly forced in time? Possibly. But we’ve got four years of someone in the White House who will veto these measures.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/15/2016 - The Roundtable Insight: Repercussions Of India’s Demonitization; Challenges With Trump’s Infrastructure Spending Plans

FRA is joined by Jayant Bhandari ad Ronald Stoeferle to discuss further repercussions of India’s demonetization and the results of Trump’s presidency on US infrastructure and pension plans.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

Ronald Stoeferle is a managing partner and investment manager of Incrementum AG. Together with Mark Valek, he manages a global macro fund which is based on the principles of the Austrian School of Economics. Previously he worked seven years for Vienna-based Erste Group Bank where he began writing extensive reports on gold and oil. His benchmark reports called ‘In GOLD we TRUST’ drew international coverage on CNBC, Bloomberg, the Wall Street Journal and the Financial Times. Next to his work at Incrementum he is a lecturing member of the Institute of Value based Economics and lecturer at the Academy of the Vienna Stock Exchange.

DEMONETIZATION OF INDIA

The situation in India is absolutely chaotic. People are getting desperate and every single small business is failing as anything between 20-80% of their revenue is down. Even a 5-10% drop in revenue leads to losses. People can’t find jobs and are being laid off, and a large proportion of the population has been taken out of the system. They have declared 80% of the monetary value of the currency in circulation illegal, and that has created all this desperation in the society today.

Most of the money that banks are issuing right now are 500 and 2000 Rupee notes. The smaller denomination bank notes have gone under the carpet right now because people perceive those to be the safest instruments. Bad money drives out good money from circulation, and that is happening. It is not necessarily causing inflation; there has been deflation in most of the things that we buy, and this is because poor people are not competitors in terms of buying, and people are mostly abstaining from buying things that they don’t necessarily need. This is only causing inflation in gold price, because savers want to buy as much gold as possible but that market has now gone underground because of the problem and risk associated with the government.

The government has imposed regulations on gold for many years now. Rich by implication means that anyone who owns more than 500g of gold can now be assessed for tax, which automatically means a huge amount of bribes to the government. There are many unintended consequences, and these consequences only hit us after a long delay. The war against cash is already going on, and the things going on in India are the most drastic measures, but we’re seeing so many similar measures going on around the globe. If people should lose confidence in fiat currencies, then there will be consequences for the holders of those.

At the moment, for some reason, the confidence in the US dollar and other fiat currencies are pretty strong. People will find ways around the black market and gold will be very strong. People have switched to silver in India, and BitCoin is making new records.

This will fail in India because India doesn’t have the infrastructure to go cashless in the first place. The government is trying to force as much cash as possible into the banking system so they can go more negative yielding by forcing the cash into the hands of the government and by forcing people to invest in two instruments the government likes. None of this will work; it will destroy the economy and people will find ways around it. The end result will be that the gold consumption will go up, it has already gone up, we just don’t have the real numbers because most of the gold market has gone underground. There is a huge demand for gold in the country.

US NEW PLANS ON TRADE AND INFRASTRUCTURE

It’s a huge divergence we’re seeing at the moment, meaning a significant increase in inflation expectations. Our inflation indicator switched to disinflation a couple of weeks ago. The enormous strength in the Dollar, the heightening of the Reserve and the significant rise in Treasury yields is incredibly deflationary. We should not forget that in the bond market, $1.8T USD in paper value was destroyed over the last few weeks. This is clearly deflationary, and all these Keynesian programs Trump wants to implement will be successful. He’s not a new Regan; the setup is completely different. The US will likely hit a recession next year.

What politicians say and do are two completely different things. Even if they want to do the right thing, the bureaucracy might not want to follow. The only thing that can reduce financial repression is by reducing regulations. Infrastructure spending won’t work because it’ll only be inflationary unless you reduce regulations. People in markets are overestimating the immediate effect of all those stimulus packages. It’s a bit naive to believe all the infrastructure packages will have an immediate effect on the economy. Confidence is getting better, but that’s on very thin ice. Looking at employment numbers, the US in the last four years created 430000 new jobs, mostly waiters and low paying jobs while in the manufacturing industry more than 70000 jobs were destroyed. The re-industrialization of the US is a nice story, but it just won’t happen that quickly.

So far what we’ve seen from Trump was very disappointing, because most of the things he promised in the campaign he broke in the first few days. There’s too much confidence in the market and greed is greater than fear at the moment.

THINGS HAPPENING IN EUROPE

Everyone is bullish on the US these days. You can make a case for a very strong dollar, but the consequence is that emerging markets will suffer big time. A strong dollar is pretty deflationary and no one wants a strong dollar. The whole 2017 year will be a very political year, and everyone will be busy promising things.

Emerging markets haven’t really done well. They’ve copied western technology over the last 20-30 years instead of developing their own technologies. The result is that these people consider US dollars to be gold, and this trend will likely continue. Trump may be positive in terms of controlling migrants flowing into the US.

POSSIBLE PENSION FUND CRISIS

Governments will try to avoid a pension fund crisis, but the question is whether or not they’ll be able to. There’s kind of an illusion that the politicians and central bankers can keep the market under control. The reality is that by manipulating the paper market to continuously create wealth, you actually destroy wealth as a consequence of it. What pension funds and the welfare system really needs is an increase in wealth and the paper market can’t create that, it only destroys that. The requirements of the welfare system are increasingly too big for the capability of the wealth creating aspect of the society to handle. They have to keep bringing in new people to support pensions, and if they don’t it’s a paper palace that will collapse at some point in time.

ASSET CLASSES TO PROTECT WEALTH

You should try to diversify out of the financial system. Counterparty risk will be more of an issue in the next crisis. It seems that gold has gotten very positive and robust aspects for every portfolio. So in the context of an anti-fragile portfolio gold definitely makes sense. Mining stocks are also good right now. People should follow volatility strategies going forward and from a strategic point of view, US 10-year Treasuries are oversold and there will be a bounce. Equity markets are massively overvalued and there will likely be a correction in the next year.

In terms of investment, East Asian markets are undervalued. Western people should look to China and Hong Kong for keeping some of their cash and wealth in. People should own a lot of gold and consider storing it in places like Singapore and Hong Kong because of the respect to private property these countries still offer. New Zealand and Australia are good places to diversify into, as they are western countries still unaffected by the social problems currently happening in Europe and North America.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/15/2016 - Edelweiss Journal: The Challenge Of Preserving Capital In The Financial System

Edelweiss Journal: “After a decade of extreme monetary experimentation, it is now commonly accepted that global fiat money, expansionary money policies and central planning have served to distort the price-finding role of the free market and, as a consequence, the valuation of all assets .. The bifurcation between financial and real economies has grown ever larger, and this has been to the benefit of participants in the financial economy. Precisely because of the scale of this gap between the two, and because of their very different modern natures, a transition back to the real world provides an insurmountable challenge for most who have spent their careers developing skills suited now only to the financial system .. In this scenario, owners of real productive assets, which are genuinely scarce in nature and unavailable to most, seem best placed to prosper. For they do not require liquidity within the financial system, nor to be told what the current price of their company’s shares is. Furthermore it is likely that, in times of real adversity, the best of these businesses will find opportunities to strengthen their position further.” LINK HERE to the report

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/11/2016 - ABOVE ALL FINANCIAL REPRESSION: The politics of negative interest rates has backfired

Above all, financial repression

The politics of negative interest rates has backfired

Kenneth Rogoff is a highly respected U.S. economist. In 2011, he received the Deutsche Bank Prize in Financial Economics, and sooner or later he will probably receive the Nobel Memorial Prize. But Mr. Rogoff also belongs to the elite in which voters in the U.S. and elsewhere no longer trust.

I met Mr. Rogoff when he received the Deutsche Bank Prize. At this occasion, he was asked how the huge debt accumulated in the run-up to the financial crisis could be reduced again to a tolerable level. His answer was: through financial repression. With this, he meant a monetary policy aimed at keeping interest rates low while raising inflation, so that government revenues would rise while interest expenses would be depressed. With this method, the U.S. succeeded in reducing the public debt incurred during World War II. When the U.S. entered the war in 1941, federal debt amounted to 49.5 percent of GDP. As a result of the war expenses, the debt ratio rose to 119 percent of GDP in 1946. Thereafter, it fell again to about 57 percent of GDP in 1959. In 1941-1959, the U.S. Federal Reserve kept the interest rate on long-duration government bonds at 2.6% on average. With an average inflation rate of 4.2%, the real interest rate amounted to -1.6%. Thus, negative real interest rates helped cut the government debt ratio by about half between 1946 and 1959. In the early 1970s, the policy-induced depression of real interest rates was labeled “financial repression.”

Since the financial crisis of 2008-09, central banks have been trying hard to boost inflation. Only few of them admit that their true objective is to push real interest rates into negative territory, with a view to easing the debt service burden of their governments. Only the Bank of Japan has committed itself to fix the interest rate on 10-year government bonds at 0% while aiming to drive inflation above 2%. So far, however, neither the BOJ nor other central banks have succeeded in generating financial repression. Inflation has stubbornly remained low.

Economists like Mr. Rogoff conclude from this that nominal interest rates need to be pushed into negative territory if financial repression cannot be created by rising inflation. “To say that negative real interest rates caused by inflation are unfortunate but negative nominal rates are unnatural is to promulgate financial illiteracy,” he wrote in the Financial Times on Oct. 11. For the technocratic economist, it does not matter how the real interest is pushed into negative territory to create financial repression. If inflation does not increase, nominal rates have to decline. And if citizens flee into cash to avoid negative interest rates on deposits, then cash needs to be abolished.

Economists like Mr. Rogoff cannot imagine that for ordinary people, positive nominal interest rates are related to negative rates like water to ice. The drop below the zero line leads a change in the aggregate condition in both cases. In the “fluid,” positive area, economic agents see interest as a reward for the postponement of consumption. The borrower brings spending forward in time and needs to take care that he uses the borrowed money such that he can repay the lender the principal with interest. In the “frozen,” negative area, economic agents see interest as an illegitimate tax imposed upon them by unelected technocrats. They may just tolerate the tax levied through negative real interest rates when it is the result of unexpected inflation. But they resist taxation through negative nominal rates even more than normal taxation, because it lacks democratic legitimacy.

The politics of negative interest rates has backfired. Banks are bleeding, and people rebel against them. Like Mr. Rogoff, central bankers belong to the elite. But they cannot be voted out of office.

However, people can withdraw their trust in the money they create.

Thomas Mayer is the founding director of the Flossbach von Storch Research Institute in Cologne, Germany.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/08/2016 - China Curbs Gold Imports To Slow Capital Flight

“While all eyes were on India (as rumors swirled of an imminent gold import ban), The FT reports that China curbed gold imports in the wake of government attempts to clamp down on capital leaving the country, according to traders and bankers.” LINK HERE to the article

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/08/2016 - India Confiscates Gold, Even Jewelery: Global Financial Repression

Mish Shedlock*: “Global financial repression picks up steam, led by India. After declaring large denomination notes illegal, India now targets gold .. It’s not just gold bars or bullion. The government has raided houses, no questions asked, confiscating jewelry .. Evidence suggests the politically connected, and their friends, knew about the ban on cash and acted in advance. Everyone else is stuck .. India’s raid on gold reinforces its ban on cash. Short term aside, these kinds of actions will increase demand for gold .. I keep wondering: what’s next? People pretend they know, I admit I do not. However, I am quite sure a currency crisis is coming. Where it strikes first is unknown, but the list of likely candidates increases every year .. My spotlight has been on Japan, China, and the EU. India caught me off guard, but it adheres to my general theory this pot will eventually boil over in a cascade from an unexpected place, outside the U.S. .. U.S. actions may cause a currency crisis, but I believe a crisis will hit elsewhere first. If I am correct, gold will be the safe haven, regardless of currency, but especially where the crisis hits.” LINK HERE to the commentary

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/02/2016 - The Roundtable Insight – The Repercussions Of India’s War On Cash

FRA is joined by Mike Shedlock and Yra Harris to discuss the repercussions of India’s war on cash, along with implications for the rest of the world and what we can expect from global policies that are occurring.

Mike Shedlock / Mish is a registered investment advisor representative forSitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. He is also a contributing “professor” on Minyanville, a community site focused on economic and financial education.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

MAJOR FINANCIAL REPRESSION IN INDIA

It’s been estimated that 82% of the entire physical cash currency is now out of circulation, and that’s devastating the economy. The price of gold is going through the roof to upward $3000 USD/oz.

The impact will be different from what a lot of people think. It’s not as financially repressive and they believe it’s an effort to raise more taxes. There’s a lot of black market activity that takes place in India and they’re trying to recoup some of that tax, but it’s interesting that it comes on top of efforts by Larry Summers and others to go to a cashless society. That’s the ultimate act of financial repression because then they can take rates as low as they want and there’s no penalty because everyone is going to spend what they have instead of hoarding their cash.

A lot of the housing transactions are done with black market cash, so this might act to cool off some of the wild inflation we’ve seen in Indian home prices. We can say for sure that central banks around the world are watching this to see what they can do and what they can get away with. The Bank of Japan would like to outlaw cash, the EU banned the 500 Euro note, and Larry Summers in the US is proposing banning the $100 bill. All of this is allegedly to stop the black market in currency, but that’s not the real target. The real target is to get rid of cash, make sure the government can track your spending, and make sure you pay taxes on everything you should be. The reason people aren’t paying taxes is because taxes are too high and banks aren’t safe. The real reason behind this is so governments can confiscate cash at will, so no one in the long run is benefiting from this move.

WHO BENEFITS FROM NEGATIVE INTEREST RATES?

Interest rates have been negative for the last decade, other than the financial crash when the prices of everything crashed. Rising productivity is inherently deflationary. We have more goods produced by fewer people with less effort and less money. Central banks don’t want that. The BIS did a study last year and their perspective was that routine CPI deflation are not damaging at all. The only time you’re going to find it is going back to the Great Depression, and that was an asset bubble bust, not just routine price inflation bust. What central banks have done in their fight against cash is elevate the price of assets until they’ve created bubbles.

White anger sponsored by the Fed helped elect Trump. People still don’t understand the Fed and central banks brought about the very thing they’re railing against by repressionary financial tactics and promotion of inflation.

ITALIAN REFERENDUM

On Dec. 4th, two things happen: we have a referendum in Italy and Italian president Matteo Renzi vowed to step down if the referendum failed, and an election in Austria where Norbert Hofer is anti-immigration and the odds have been very good for him. He will be the first anti-immigration nationalist president of any nation in Europe since the end of WWII.

If Renzi loses, he’s not going to be allowed to resign. They will go with the crisis mode and Renzi is far better off if he loses. It’s extremely difficult to see how things will play out. We’ve got these multiple simultaneous battles going on in France, in the Netherlands, in Austria, and in Italy. There is a serious risk of fracture.

INFRASTRUCTURE SPENDING

It takes an authorization from Congress for Trump to build a wall, and he’s probably not getting it. If Trump can actually divert funds from somewhere to build a wall, as far as wasteful spending goes it’s not the most wasteful thing in the world. If you want to stop people from coming to the US for free handouts, you stop the free handouts, not build a wall. The stock market is mostly reacting to the premise of all these tax cuts and how inflationary this is going to be.

When we look at a potential collapse in global trade, a potential collapse in housing market and stocks, if bond yields, we’re looking at a deflationary outcome. We are not necessarily going to get immediate inflation out of this. Down the line, possibly, but the immediate picture in light of productivity enhancements coming online, millions of taxi jobs vanishing, and a possible collapse in asset prices, this is a very deflationary setup and a rising dollar exacerbates that.

With a huge amount of debt, this is nothing like a Reagan redo. It’s a far different picture from Reagan’s time. If we expect to go through this massive fiscal stimulus in infrastructure and “full employment”, they should be raising rates by 100-200 basis points because that’s what the model says to do. If Trump is able to get real tax reform, it will be a phenomenal presidency.

If Hillary won the election, the stock market would rally because it was more of the same in peoples’ minds. We’re not going to get a huge amount of year end selling of capital gains because a lot of people are going to hold off until 2017 because they think they might see a lower capital gain rate. A lot of people were expecting that selling to take place and it has not shown itself.

Podcast and youtube will be available and posted here shortly ..

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/30/2016 - Carmen Reinhart: Financial Repression Requires A Captive Audience

Carmen Reinhart

On Financial Repression

“Experience teaches that countries reduce debt relative to their income in five ways: economic growth, substantive fiscal adjustment or austerity plans, explicit default or restructuring of private and/or public debt, a surprise burst in inflation, and a steady dose of financial repression that keeps real interest rates low (usually negative). The last two options — inflation and financial repression — are only viable for debts denominated in domestic currency .. As they have historically in the aftermath of financial crises or wars, central banks have been increasingly resorting to a form of ‘taxation’ that helps liquidate the huge overhang of public and private debt and eases the burden of servicing that debt. Such policies, known as financial repression, usually involve a strong connection between the government, the central bank and the financial sector. One of the main goals of financial repression is to keep nominal interest rates lower than would otherwise prevail. This effect, other things being equal, reduces governments’ interest expenses for a given stock of debt and contributes to deficit reduction. However, when financial repression produces negative real interest rates (yielding less than the rate of inflation) and reduces or liquidates existing debts, it is a tax on bondholders and a transfer from creditors (savers) to borrowers and, in most cases, governments. Other features of financial repression vary across countries and time. In the past, measures also included directed lending to the government by captive domestic entities (such as pension funds or banks), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and generally a tighter coordination between governments and banks — either explicitly through public ownership of some institutions or through heavy ‘moral suasion’ by officials. In connection with keeping interest rates low, regulatory policies with financial repression features aim to create or expand a captive audience for government debt; Basel III rules fit this mold, as they provide for the preferential treatment of government debt in bank balance sheets.” LINK HERE to the essay

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/30/2016 - Yra Harris: Financial Repression Coming From Negative Interest Rates & A Cashless Society

“Trump will be playing a dangerous game if he turns his back on those who had greater hope for the draining of the swamp. There is a euphoria from the entrepreneurial class that tax reform and the lifting of some burdensome regulations will take place under Trump but a massive fiscal stimulus will have to be financed and rising interest rates will place a burden upon the budget plans being discussed. Even Druckenmiller was talking about robust growth fueling a rise in long-term rates. He noted a level of 6%. As previously discussed, DEBT will be the most important factor overhanging any Trump-inspired growth strategy .. Where Druckenmiller discusses NOMINAL RATES my focus will be on REAL RATES. At zero interest rates around the world, monetary policy has been in uncharted territory as central bankers sought to ease the burdens of a global balance sheet recession (Richard Koo). Getting back to interest rates as a signalling mechanism will restore classic fundamentals to a premier position in global macro analysis .. The point of a cashless society has been raised by Larry Summers as a way to deal with his beloved theory of secular stagnation. In a cashless society a central bank could impose NEGATIVE INTEREST RATES of say 3% and not worry about cash being hoarded. Only a fool would keep being charged on deposits and thus there would be a rush to spend every digital cent. So we will continue to monitor the financial repression in India. Interesting that this took place after Raghuram Rajan was replaced as the Governor of the Indian Central Bank.” LINK HERE to the commentary

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/26/2016 - The Roundtable Insight – Barry Habib & Jayant Bhandari On Rising Interest Rates & The War On Cash

FRA is joined by Barry Habib and Jayant Bhandari in discussing India’s socioeconomic state, along with the wealth taxation there and in the USA.

As founder and CEO of MBS Highway, Barry is also Chief Market Strategist for Residential Finance Corporation, a leading national mortgage banker. Barry has also enjoyed a long tenure as a market commentator on FOX and CNBC Networks. He can be seen presenting his Monthly Mortgage Report on “Squawk Box,” the early-morning CNBC business news show. Barry also serves as a professional speaker on the financial markets, housing, negotiation, technical trading analysis, sales training, building relationships and motivation. He is also co-creator and currently Principal Managing Director of Health Care Imaging Solutions.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

INDIA’S WAR ON CASH AND GOLD

On Nov. 9, Prime Minister Narendra Modi banned Rupee 500 and 1000 banknotes, equivalent to $7.50-15USD, which represents 88% of the total monetary value in circulation. These two are the most commonly used by poor and rich people alike. He banned them despite the fact that 97% of the consumer economy is based on cash, which means in this country they have pretty much banned cash and brought the economy to a standstill. They coincided this with the US election so the world would not pay much attention, but this is creating a massive crisis in the country to maximize tax collection irrespective of what it does to Indian society.

People are now in a desperate situation and savers are pouring their money into gold, because people are forced to use the cash they have. The price of gold is going up in both Rupee and USD. The Rupee price should be about 10% higher than the dollar price, but right now it’s almost 100% higher in India than the US. The reason is that the sudden repression of cash has forced people to divert their cash into physical gold. All the lower denomination bank notes are rapidly going out of circulation and India’s economy is rapidly going into paralysis.

Indians did not resist when the government imposed a ban on currency notes, which is really confiscation of private property. Moral instinct is being taken away from Western societies using socialist, welfare, and warfare economies. Eventually people in Western countries will become incapable of resisting the government whey they start seizing private properties. When governments have no more capabilities to print money, they will go confiscate peoples’ money.

INTEREST TREND SINCE US ELECTION

The long end of the yield curve is going higher in terms of interest rates, coupled with rising inflation. We’re currently at a really important juncture. We’re so oversold on yield that we could see a bit of relief where we’ll see yield drop. The same thing applies for mortgage-backed securities.

Rates started to rate in mid-September when Central Banks in Europe and Asia went to negative rates. It diminished the appetite for bond buying. There was so much money to be made on capital appreciation and with negative interest rates there was theoretically no longer a floor and you could theoretically make an infinite amount of profit as long as rates kept going down. Since then we’ve seen zero become a rational floor across the globe.