03/17/2017 - Paul Brodsky: “Stagflation On The Horizon”; Coordinated Currency Devaluation Ahead

“We argue the US economy, US assets, the Fed and US fiscal policy makers are displaying obvious signs of late-stage fatigue associated with protecting the current global regime at all costs. As in the 1970s, the triggers for goods and service inflation within a slowing global economy will be currency related and a dearth of supply flowing through the trade channel, but rather than oil, this time the world will lack an adequate supply of increasingly scarce dollars needed for debt service.

Milton Friedman famously noted “inflation is always and everywhere a monetary phenomenon”. In the post-Bretton Woods monetary system, the pricing and supply of money and credit are not determined by production, but rather by monetary and currency exchange policies. Central banks and treasury ministries manufacture inflation through policy administration .. The organic need for more production in the US (and everywhere else) is falling, as evidenced by declining global output growth. The only lever US policy makers will soon have left to pull, if they want to maintain the USD-centric global system, will be coordinated currency dilution (i.e., devaluation) .. The Fed will have to turn on the spigots and create dollars for US and foreign creditors and, if they are lucky, debtors too. Stagflation will appear. The markets should begin getting a whiff of this soon.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/13/2017 - The Roundtable Insight: Charles Hugh Smith On Inequalities And Distortions Caused By Central Bank Policies

FRA is joined by Charles Hugh Smith in discussing income inequality as a result of central bank policies

Charles Hugh Smith is a contributing editor to PeakProsperity.com and the proprietor of the popular blog OfTwoMinds.com. He is the author of numerous books, including Why Everything Is Falling Apart: An Unconventional Guide To Investing In Troubled Times.

ENGINES OF INEQUALITY

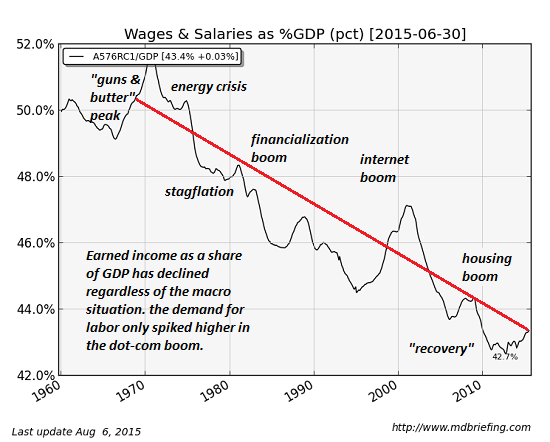

A lot of people are connecting the dots between rising income inequality and central bank policy. Wages as a percentage of GDP is a very broad-based method of saying how much the economic activity in a nation is ending up in the hands of wage earners as opposed to owners of capital or rent-seekers. We want to differentiate between rent-seeking – monopolies and cartels getting the government to protect their income streams and eliminate competition – as opposed to the innovative, creative destruction side of capitalism where growth and income inequality might be rising because the most talented and the most successful at allocating capital are benefiting. We can see that both of those forces are at work. A lot of people have noted that the top 5% of wage earners are scooping up most of the gains in wages while the bottom 90-95% are seeing stagnating wages.

If you look at GDP as a percentage of wages, it’s been declining since 1970. Something else is going on. Why are wages declining for decades? Clearly it’s connected to policies. 1970 coincides with the decoupling of the USD from gold, so from that point it all comes down to central banking policies and interventions by the Fed in the US.

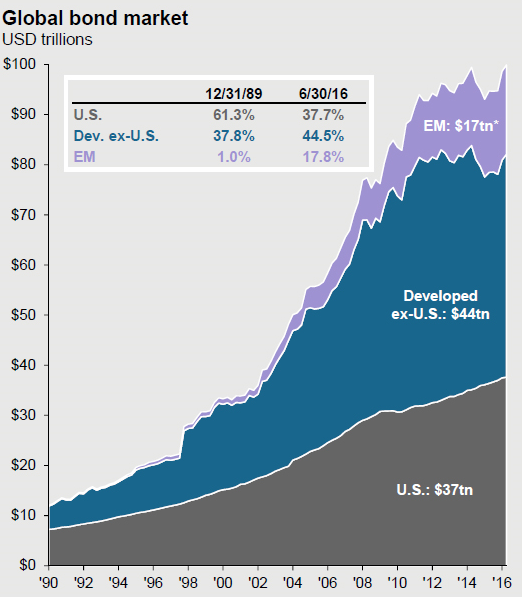

We can also look at debt. The primary function of central bank policies over the last few decades seems to be facilitating the expansion of debt at a rate that’s far faster than the expansion of GDP. The global bond market is basically the creation of debt instruments, and from 1990 there was about $10T in global bond market debt, and now it’s pushing $100T. We have to ask if the major economies of the world increase tenfold, and the answer is no. Looking at US sovereign debt, around that period it went from $3T to $20T. We can kind of follow that narrative and see what happens when debt is awarded and the acquisition of debt is easy for those closest to the money. There is a tremendous conservation of central bank policies, which is to lower interest rates and make it easier for banks and corporations to borrow money. This is one of the key drivers in wealth and income inequality.

When the rent-seeking, exploitative part of the economy that used to be a relative modest percent of the economy, grows to 10-20% of the economy, it leaves less actual capital for innovators. We want to encourage innovators, but in the US we have a system where if you’re already extremely wealthy, then the Fed policies have enabled you to enlarge your rent-seeking at the expense of everyone else. Increasing levels of debt are yielding less economic growth over time, requiring more and more debt to get the same level of increase in economic activity.

DEBT AND DISTRIBUTION OF WEALTH

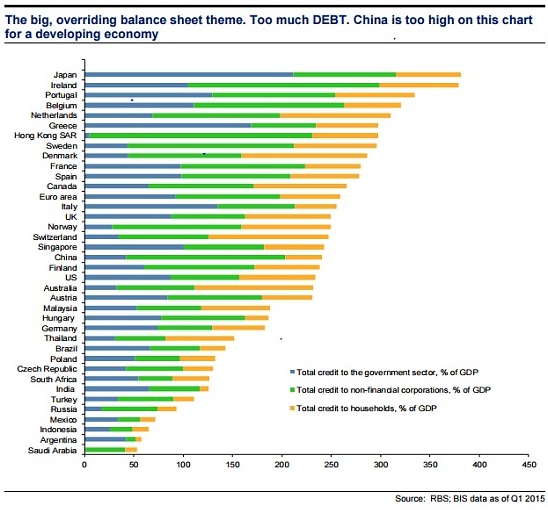

The debt has soared, and so has global financial assets, but not as much. There’s been a healthy expansion, but it’s completely asymmetric to the amount of debt that’s increased. In China, within a decade their total debt load has gone from $3T to $30T. A lot of other nations have followed that same pattern of skyrocketing debts and assets that have gone up but not by the same proportion.

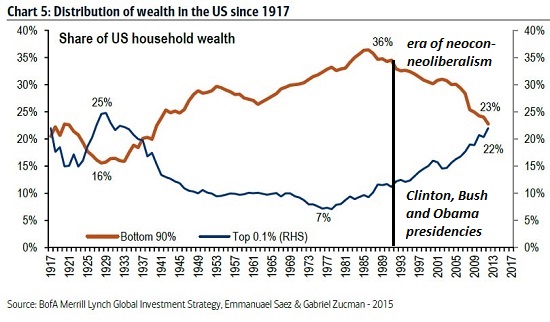

Distribution of wealth in the US since the 1917s has favored bottom 90% the most in the 70s and 80s, and then about 1990 it’s gone against wage earners. We can perhaps extrapolate these vast changes in wealth and income inequality and ask what the social changes are. A lot of people have pointed out that the election of Trump, Brexit, and the rise of the “right” parties in Europe are connected to the social disorders that are arising from this wealth inequality.

There’s potential for misattribution by the general public on why the financial crisis happened and why income wealth inequality is getting worse. Both Canada and Mexico has a larger, broader-based middle class than the US, and the Gini coefficient reflects that. Mainstream media doesn’t explain that the wealth effect only benefits those with assets or access to cheap credit that can be used to buy assets. This is where the central bank has created a vast social injustice, and that’s why the social cohesion is being lost. People recognize that these central bank policies are exacerbating social injustices. The fallacy of the central bank idea that if they create all this wealth in the wealthy class, some of it will trickle down and benefit the bottom 95%. But that trickle effect is very modest and not something the central banks can control. That’s a structural flaw in central bank policies.

The way you deal with financial crises is by forcing people to take losses all the way along the line. You don’t create moral hazard and bail people out and make it easy for people to avoid losses, because then you pile up a lot of bad debt that is hidden. Policy makers at central banks don’t address inequality, perhaps because they know they’ve failed in that area and it’s a problem they don’t have any influence on.

LOOKING FORWARD

Millennials are quite financially conservative and are aware that the generational burden is falling on them. They might not cleave to any of the political lines that we’re used to. It’s interesting because they favor more socialist agenda, in the sense that it reduces the inequality and injustice that is rising, but they may very well be conservative financially instead. There may be a hybrid political solution going forward.

We could get rid of central banks or limit them to providing liquidity in liquidity crises. If we went back to a market of private capital, that would instantaneously remove a lot of the benefits rent-seekers get from central bank policies and everyone would have a transparent market for capital. That would open up the capital market to innovators in a way the central banks have repressed.

There is a huge potential benefit to innovators and small enterprises in decentralized crypotcurrencies. These currencies have great value as they’re outside the control of central banks. If we can decentralize money and capital, that would open the door to a lot of solutions.

These distortions are building up systemic risk that’s beneath the surface. Right now central bank policies are all about masking risk, but the systemic risk is rising at the same time that benefits of adding more debt to the system are diminishing. There’s going to be a banquet of consequence in the next few years, and we can see it being prepared right now.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/12/2017 - Bill Gross: The Financial System Is Like A Truckload Of Nitroglycerin On A Bumpy Road

“In 2017, the global economy has created more credit relative to GDP than that at the beginning of 2008’s disaster. In the U.S., credit of $65 trillion is roughly 350% of annual GDP and the ratio is rising. In China, the ratio has more than doubled in the past decade to nearly 300%. Since 2007, China has added $24 trillion worth of debt to its collective balance sheet. Over the same period, the U.S. and Europe only added $12 trillion each. Capitalism, with its adopted fractional reserve banking system, depends on credit expansion and the printing of additional reserves by central banks, which in turn are re-lent by private banks to create pizza stores, cell phones and a myriad of other products and business enterprises. But the credit creation has limits and the cost of credit (interest rates) must be carefully monitored so that borrowers (think subprime) can pay back the monthly servicing costs. If rates are too high (and credit as a % of GDP too high as well), then potential Lehman black swans can occur. On the other hand, if rates are too low (and credit as a % of GDP declines), then the system breaks down, as savers, pension funds and insurance companies become unable to earn a rate of return high enough to match and service their liabilities.

Our highly levered financial system is like a truckload of nitro glycerin on a bumpy road. One mistake can set off a credit implosion where holders of stocks, high yield bonds, and yes, subprime mortgages all rush to the bank to claim its one and only dollar in the vault. It happened in 2008, and central banks were in a position to drastically lower yields and buy trillions of dollars via Quantitative Easing (QE) to prevent a run on the system. Today, central bank flexibility is not what it was back then. Yields globally are near zero and in many cases, negative. Continuing QE programs by central banks are approaching limits as they buy up more and more existing debt, threatening repo markets and the day to day functioning of financial commerce.

The U.S. and indeed the global economy is walking a fine line due to increasing leverage and the potential for too high (or too low) interest rates to wreak havoc on an increasingly stressed financial system. Be more concerned about the return of your money than the return on your money in 2017 and beyond.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/12/2017 - Rob Arnott On Why Valuations Matter, Contrarian Investing And The Unintended Consequences Of The New U.S. Administration’s Policies

Rob Arnott Of Research Affiliates:

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

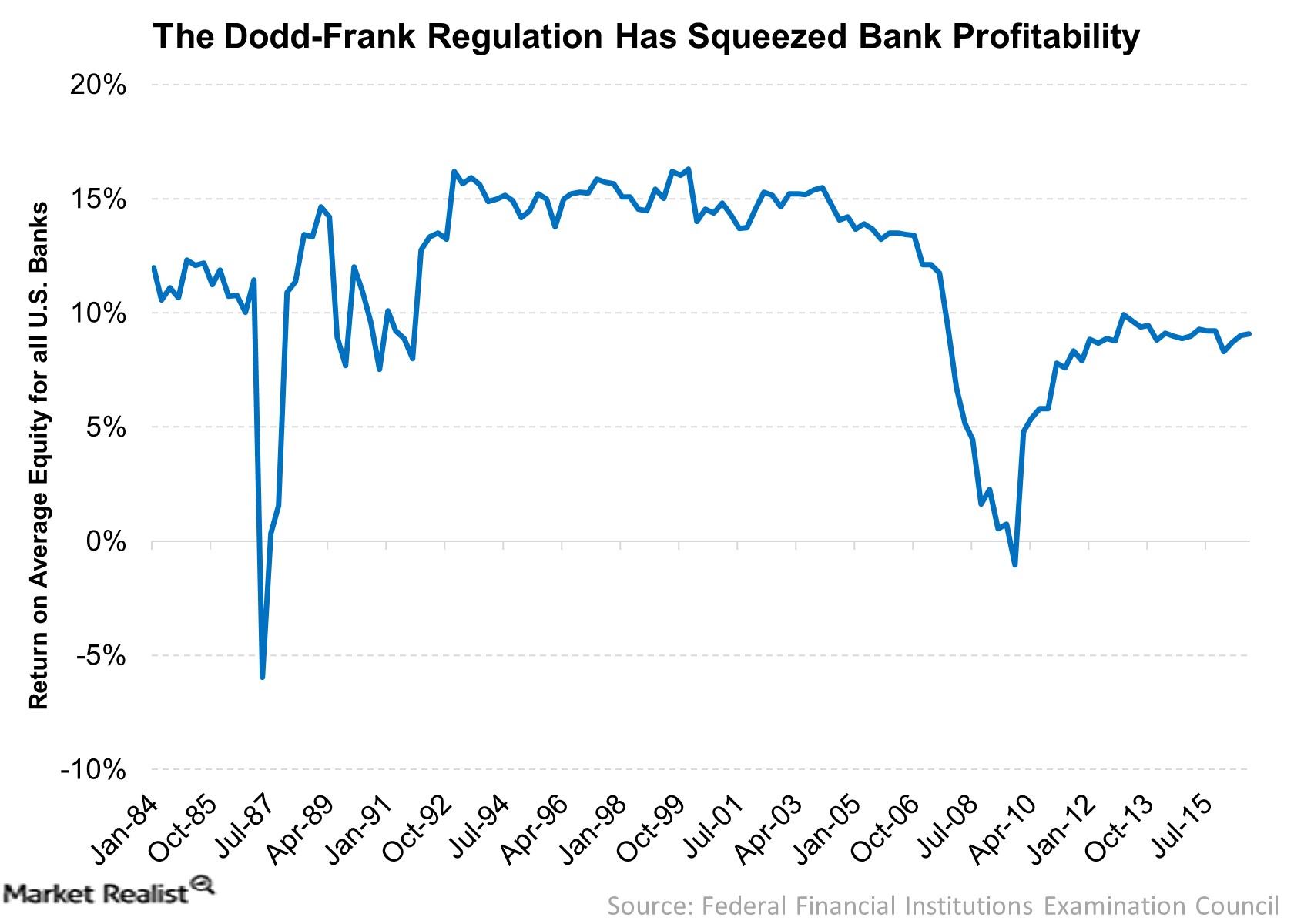

03/12/2017 - Potential Effects Of Changes To The Dodd Frank Act

WHAT IS THE DODD-FRANK ACT?

The Dodd-Frank Wall Street Reform and Consumer Protection Act, first passed in 2010, was set up to regulate and restrict banks’ influence in the financial markets. It was put forth with the goal of reducing the “too big to fail” status of banks, end bailouts, and to protect the consumer from abusive financial system practices while promoting transparency and accountability. The Act added new regulatory bodies in an attempt to maintain stability in the financial markets, and restricted their ability to engage in proprietary trading.

Primarily, the Act created the following:

The Financial Stability Oversight Council (FSOC) that regulates and responds to risks to the financial stability of the US, and promotes market discipline. This includes demanding banks they consider too large to increase their reserve requirements.

The Volcker Rule, which reduced the amount of speculative investments banks could engage in, thereby banning conflict of interest trading that banks could use to increase their own profits. This includes hedge funds and private equity funds.

The Consumer Financial Protection Bureau, which promotes transparency and accountability of banking practices, and allows financial irregularities to be reported.

As of February 2017, Trump has called for the reduction of the scope and regulations of the Dodd-Frank Act.

EFFECT OF POTENTIAL CHANGES

Some of the changes suggested directly target the Volcker Rule, which could give banks more freedom in engaging in speculative investing to increase their profits

Dave Sheaff Gilreath of Sheaff Brock Investment Advisors LLC notes that a decrease in regulations would have positive effects on stocks in the financial sector. Already stocks of big banks have jumped since the announcement.

As for small town banks, loosening the restrictions would make it easier for them to provide loans to local small businesses – their primary customers. Bank capital levels and credit quality would also be checked less often, and the overall compliance burden would be reduced. For smaller banks, this change could mean the difference between going into the red or not.

As Peter Boockvar notes, “Dodd Frank discourages traditional market makers to provide liquidity.” Large amounts of equity funding would help banks cope with a financial crisis.

Along the same lines is the likely delay of the fiduciary rule, intended to force investment advisors to recommend lower-fee investments to their clients, and to act in their best interest financially. However, this could also discourage banks from working with low net worth clients as it will definitely reduce income.

In addition to all this, Trump is going to replace Janet Yellen with someone sympathetic to his administration apparently one of his Wall Street compatriots, making it highly likely that future financial decisions will be weighted in favor of Wall Street and bankers.

Unfortunately, the eventual outcome is highly uncertain as it is still unclear what sections of Dodd-Frank will be repealed, rolled back, or modified. Regardless, Trump has made it clear that he intends to empower Wall Street despite what he says about helping Main Street.

By: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

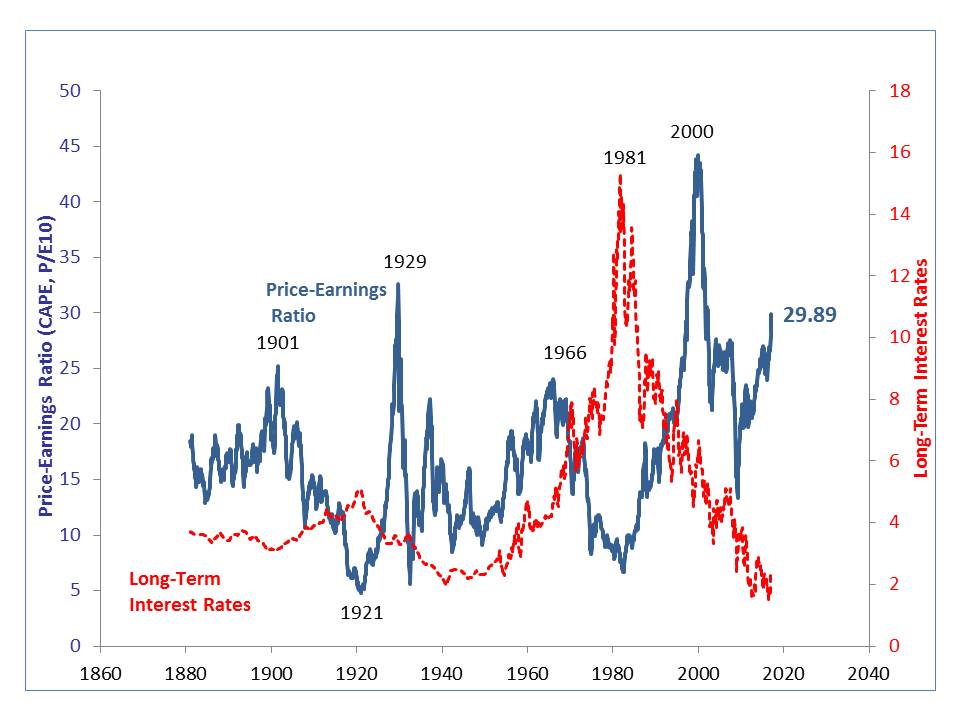

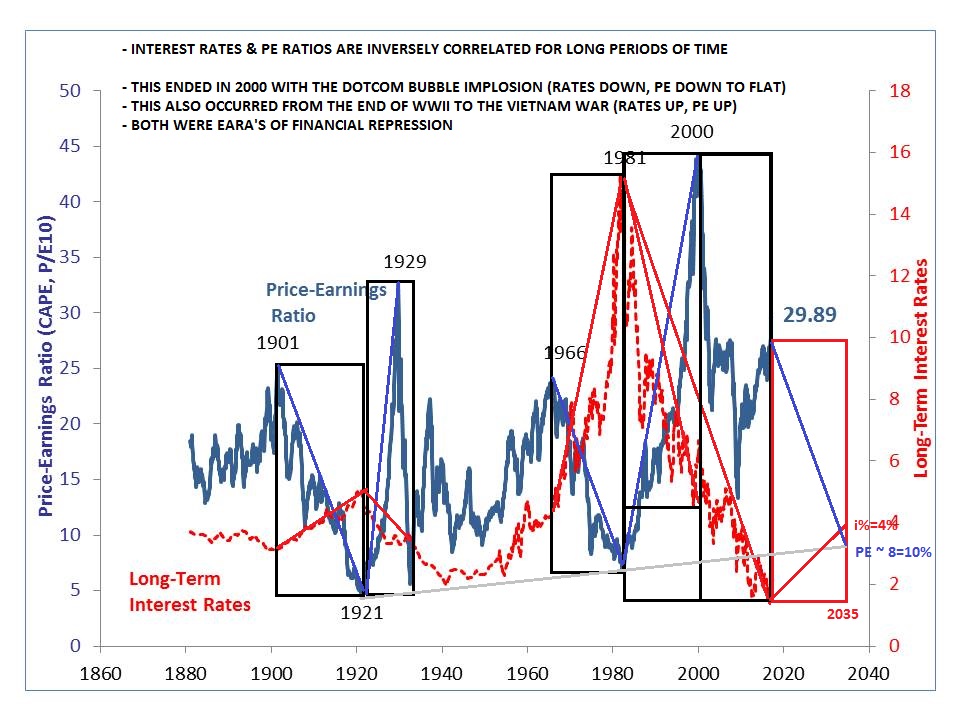

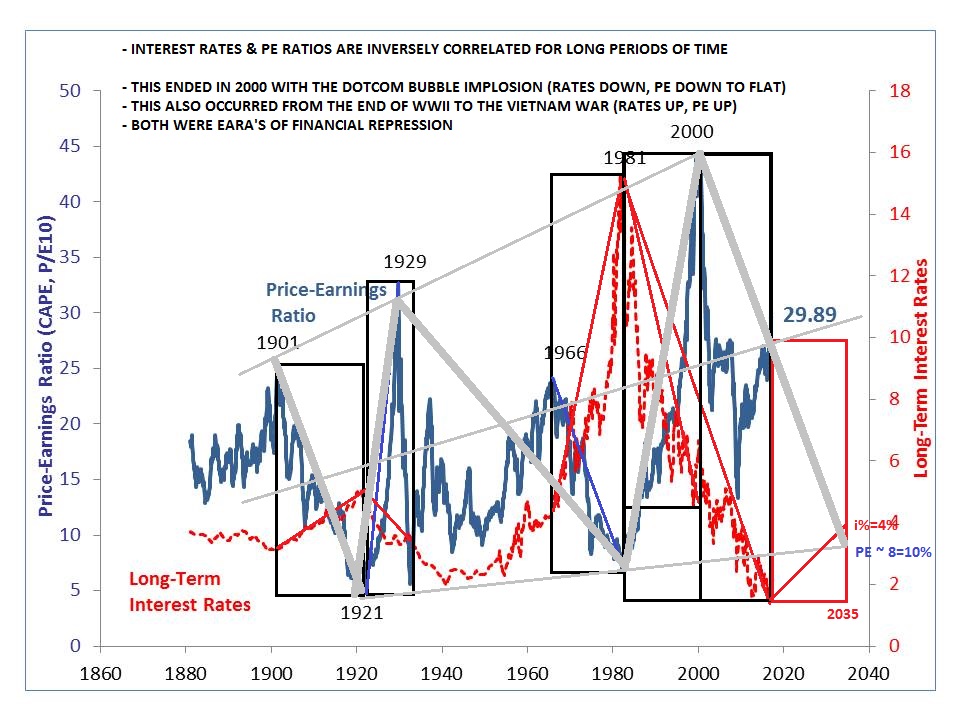

03/11/2017 - THE SHILLER CAPE, RATE CYCLES & FINANCIAL REPRESSION

THE SHILLER CAPE, RATE CYCLES & FINANCIAL REPRESSION

The Shiller CAPE (Cyclically Adjusted Price-Earnings) Ratio is found to be inversely correlated to interest rates over long periods of time. Generally you would expect PE’s as well as the 10 year Shiller CAPE to expand as interest rates fall and to contract as they rise.

What may be more important is that in periods of stability interest rates trend higher or lower for long stretches of time. The chart below “blocks” those periods when the inverse correlation was followed.

You will notice above that there are two periods when interest rates and the Shiller CAPE were not inversely correlated but followed the same direction:

The 1930’s through to the Vietnam War.

After the Dotcom Bubble in 2000 through to the 2008 financial crisis.

What we know about these two eras is that Macroprudential policies of Financial Repression were followed by the US Federal Reserve to address excessive government debt buildup as well as a period of very slow to contracting economic growth.

Following 2008 the Shiller CAPE and Long Term Interest Rate ratio appears on the surface to have established its inverse relationship.

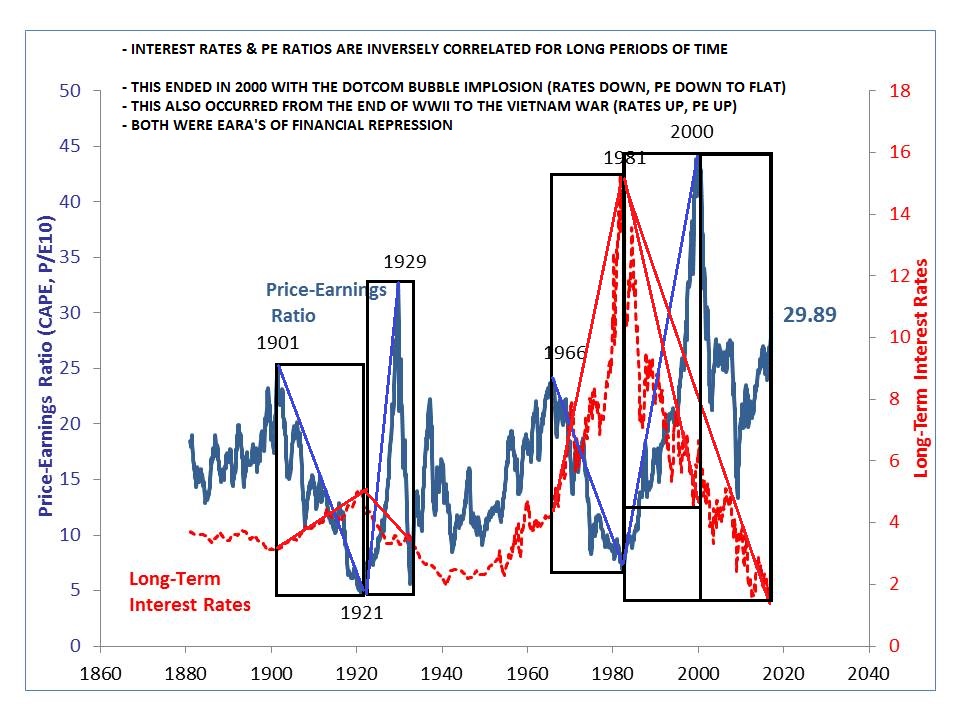

Does this mean Financial Repression has ended or is the expansion in PE’s since 2008, while rates fell, something else and in fact we are still in an Era of Financial Repression which will continue for an extended period into the future? Our chart correlation appears to become somewhat confusing?

The way to clarify where we are and what is likely to unfold is to consider the Shiller CAPE in isolation. When we do this it is pretty evident that we are very close or approaching a top and subsequent reversal in expansions in the Shiller CAPE

If this is the case, then it suggests the Federal Reserve will soon ‘lose out’ to market or political forces in controlling Financial Repression policies regarding interest rate policy. The grey trend lines below suggest major secular waves are hard for central bankers to overcome.

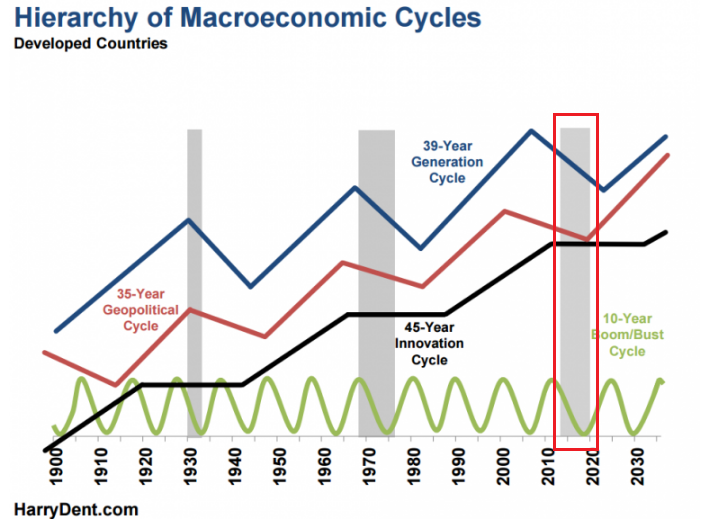

Our Financial Repression interviews with cycle experts such as Harry Dent and Martin Armstrong, as well examination of the Kondratieff Cycle, suggests this to likely be the case.

The chances are now high that by 2020 when most of our long cycles reverse that the gig will be up for the central bankers!

The charts suggest that the Shiller CAPE may possibly begin a return to its historical levels of 8-10% while Long Term Interest rates move towards their more historical norms of 4%

Maybe we are simply reading too much into the charts but it is an interesting set of correlations to consider during this period of maddening market messages!

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/25/2017 - Yra Harris Warns Of Massive Global Slowdown If U.S.$ Appreciates 20% On Top Of A 20% Border Adjustment Tax

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/24/2017 - The Roundtable Insight – Have Central Banks Reached The “Coffin Corner”?

FRA is joined by Uli Kortsch and Jayant Bhandari in discussing global interest rate trends and growth, along with the likelihood of another recession.

Uli Kortsch is the Founder of both the Monetary Trust Initiative (MTI) and Global Partners Investments (GPI). Currently most of his time is spent on MTI whose mission is to bring transparency and authentic principles to our monetary system. He was asked to organize a conference on this topic at the Federal Reserve Bank in Philadelphia, the proceeds of which are now published as a book. He is a regular speaker at various conferences in different countries. As President of Global Partners Investments and other ventures Mr. Kortsch has worked in over 50 countries, written a bill for Congress, and conferred with approximately 15 national presidents, ministers of finance, and ministers of commerce. He has served on numerous corporate boards with both for-profit and not-for-profit organizations.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

RELOADING THE AMMUNITION

We’re going to have another recession. Who knows when it will come, but it will come. We’re close to having the longest buildup growth since the last recession, so we’ll have another one fairly soon. The problem is that under our current system, we use interest rates to stimulate the economy. It appears negative so we increase interest rates and make money more expensive, so people stop borrowing. The interest rates globally are so extraordinarily low that in order to stimulate growth during the upcoming recession, there’s not enough movement without going back into negative interest rates. If we do have another recession fairly soon, we’re going to go into negative interest rates.

Most of the savers are older and trying to live off a certain portfolio or expecting a certain kind of income. When you have negative interest rates, the more money you have the more expensive money becomes. You lose money off your money, so the net result is that consumers save more. Instead of negative interest rates stimulating the economy, they actually slowed down even further.

We have an intersection of the interest rate of the economy and the world is able to handle, and where central banks are desperately trying to increase the rate.

If we increase the interest rates, the governments cannot afford their own debt. If we were to pay normal interest rates on US federal debt right now, we would have a deficit of above $1T. We currently have $10T in global debt denominated in USD. As the interest rates go up, those companies can’t afford those either. If you have a crash internationally, we are so linked today that no one will be spared. It’s this coffin corner where you’re damned if you do and damned if you don’t. You’ve got to raise the interest rates, but if you do you’ll crash the economy.

If you look at the last century, western economies mostly grew at a faster rate than the rest of the world. What actually was happening was that the non-western economies had negative real interest rates, and a lot of western economists don’t recognize that. The same disease might’ve entered the western economy society over the last decade or so. We might have over regulated businesses so much that the capital no longer has capacity to generate economic growth. Even negative interest rates might not be enough to help these companies add economic growth to their society. The emerging markets are clearly facing this problem right now, except for East Asia.

INFLATION: US AND INDIA

We continue to be in such a strongly deflationary environment, but it would be more of the Japanese style of deflationary stagnation versus the stagflation we saw in the 70s and 80s. If you look at the demographics that are changing everywhere, plus IT developments that reduce prices, plus global trade, plus the debt overhang, it’s strongly deflationary. Every single major crash in over a hundred years has been deflationary, so why are we so concerned about inflation?

Inflation will continue and the government of India is preparing itself to spend a lot of money. Governments are trying to get emerging markets to go cashless so they can destroy their informal economy and move the money to the formal economy. In a lot of these countries, because they’re trying to force people to move their money, they’re reducing the interest rate in the formal economy but actually destroying the growth in the informal economy and that is where economic growth lies in countries like these. The result is that there will be inflation in these emerging markets.

Even in the US, the majority of the growth is in new companies and for the first time in decades the two lines have crossed negatively where if you graph the birth and death of new companies, we’ve gone negative. We are now destroying more companies than we’re creating, and this has never happened before since these statistics were kept.

We’re locked into this Keynesian world view that this is how we do things, but we’re going to face a major crash if we stay with this paradigm, and there’s no way out of it. If we keep on doing what we’re doing, we’ve only got a few years. If we are willing to switch from the Keynesian paradigm to the Fisherian paradigm, we could solve this.

Keynesian economics have become a part of us that it’s almost impossible for institutions and governments to understand that there’s an alternative. In their view, the printing press is a solution to all their problems. All these emerging markets have become very big believers in these things, and this has already led to a huge amount of malinvestment in the west and even more in emerging markets. If you go to Africa and Latin America, private debt levels are much higher as a proportion of their GDP. Those people have taken out massive private loans for consumption, not for investment purposes.

THE CHINA FACTOR

Under Trump and where trade is at, there is a possibility of another Smoot-Hawley. If there’s a sudden decrease in the value of the Yuan relative to the USD, there will be a decrease in trade. The amount of money that’s available to support the Yuan is a lot less than what they’re officially publishing. We would have to be very careful and very wise to not immediately do something stupid like blocking trade. If the Yuan had a significant crash, that would affect the whole Asian bloc.

If the Yuan falls for any reason, it will be extremely harmful to every emerging market. The Yuan is very competitive compared to other smaller manufacturing places, so if it falls for any reason, it will be disastrous for these smaller economies. But it’s so closely linked to the international market as the factory of the world; it operates differently from other currencies. The PBOC’s support mechanism effectively creates a currency board.

When the US acts as a global reserve currency, there has to be a constant leakage of Dollars out, which gives us a negative Current Account standing. If we were to reverse that, there would be an enormous Dollar squeeze globally that will backfire like there’s no tomorrow. The

INTEREST RATES IN THE COMING MONTHS

You’d have to have some real balls to do this, and there’d have to be timing involved, but it’s likely they’re not going to be able to reload the gun in time for the next recession. When you think the height of the Fed rate has been reached, you can buy US Treasuries. You can make a lot of money, but it’s a risky play.

International institutions have recognize that a lot of corporations in the developing world don’t produce as much as they thought they should, and the result has been that these corporations are basically extensions of governments in these countries. There has been pressure on governments to reduce interest rates on these corporations so they can survive. They’re forcing investments to shift from the informal economy to the formal economy, which is leading to a drop in interest rate which is good for the government. But the way they want to structure the monetary might be destroying the informal economy and the livelihoods of a major part of their population.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/22/2017 - Satyajit Das: Financial Engineering Is Masking The Global Economy’s Precarious Health

“It is time that businesses and governments focus on helping the real economy to solve large problems including debt, lack of growth, industrial stagnation, slowing innovation and productivity, aging demographics, income inequality, resource scarcity, and environmental threats. Financial engineering masks the true performance and health of companies and nations. But the damage goes much deeper, deluding decision-makers into thinking that things are better than they are, and that solutions to problems can be deferred.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/22/2017 - Will A Trump Administration Cause Rising Inflation And Rising Interest Rates?

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/19/2017 - The Roundtable Insight: Doug Casey On The Economic State Of The World

FRA is joined by best-selling author and world-renowned speculator Doug Casey in discussing current economic state of the world, from India’s demonetization to Trump.

Doug literally wrote the book on profiting from periods of economic turmoil: his book Crisis Investing spent multiple weeks as #1 on the New York Times bestseller list and became the best-selling financial book of 1980 with 438,640 copies sold. Then Doug broke the record with his next book, Strategic Investing, by receiving the largest advance ever paid for a financial book at the time. Interestingly enough, Doug’s bookThe International Man was the most sold book in the history of Rhodesia. And his most recent releases Totally Incorrect (2012) and Right on the Money (2013) continue the tradition of challenging statism and advocating liberty and free markets.

He has been a featured guest on hundreds of radio and TV shows, including David Letterman, Merv Griffin, Charlie Rose, Phil Donahue, Regis Philbin, Maury Povich, NBC News, and CNN; has been the topic of numerous features in periodicals such as Time, Forbes, People, and the Washington Post; and is a regular keynote speaker at FreedomFest, the world’s largest gathering of free minds.

Doug has lived in 10 countries and visited over 175. Today you’re most likely to find him at La Estancia de Cafayate (Casey’s Gulch), an oasis tucked away in the high red mountains outside Salta, Argentina.

CURRENT WRITINGS

Speculator is the first of a series of six novels following our hero, Charles Knight, going to Africa to look at a gold mining project he got lucky on. It’s an adventure novel about a bush war in Africa and how he made a couple hundred million dollars, and it’s actually an excellent novel. The second in the series explains the drug business the same way we explain the mining business.

THOUGHTS ON THE CURRENT STATE OF THE WORLD

We entered the hurricane in 2007. The governments of the world papered it over by printing scores of trillions of new currency. It’s surprising that we haven’t gone out of the eye of the hurricane and into the trailing edge, but we’re entering the trailing edge as we speak. It’s going to be much different and much longer lasting, and much worse than the unpleasantness of 2008-2009.This is going to be the biggest deal since the Industrial Revolution 200 years ago, and not in a good way.

The Euro has always been an Esperanto currency. If the US Dollar is an “I owe you nothing” on the part of the bankrupt US government, the Euro is a “who owes you nothing”. It’s a disaster waiting to happen. The European Union itself is likely to break up, and that’s a good thing because most people are unaware of the fact that Brussels has gone from a sleepy little town to one that holds 50000 employees of the EU who serve no useful purpose. If the Europeans want a free trade zone, all they have to do is drop duties. You don’t need a gigantic bureaucracy in Brussels to do that.

We’re going into a time of real chaos. One of the big things we’re going to see is migration from Africa, especially Africa south of the Sahara. There’s a 1-1.5M migrants that came to Europe this year, but in the future there’s going to be scores of millions. Most people are unaware that 42% of the world’s population will be African by the year 2100. It’s going to be an invasion of Europe by Africans; that’s going to continue and compound. At the same time, the Chinese are taking over the continent. It’s going to be a race war. A lot of Europeans are going to be coming to South America. That’s the big picture.

DEMONETIZATION AND DEBT

It’s incredibly stupid on the part of Modi; half the people in India are earning 1-2 dollars a day. Unfortunately, this is something that’s happening to one degree or another around the world. Governments are trying to get rid of cash, and this is catastrophic from an economic point of view and a personal freedom point of view. Without cash, everything you do goes through a bank and is monitored. There is absolutely no privacy at that point, especially in India which is technologically backward. It’s a complete disaster.

It’s definitely going to happen in the US and Canada as well. All these government officials talk to each other and seem to share a common philosophy.

When you look at US government spending, we’re going to be running trillion dollar deficits as far as the eye can see. As the world goes into the next stage of the greater depression, it’s going to go well above a trillion dollars. The US government is going to be manifestly bankrupt. They can only get the money by selling the debt to the Fed, and when debt is sold to the Fed they pay for it by printing money. We’re going to be seeing much higher levels of inflation, and the Dollar is eventually going to turn into a hot potato.

TRUMP’S PROTECTIONIST POLICIES

It’s going to be worse than stagflation. If these countries stop putting up tariffs, people can’t sell to you at the same time; they don’t have the ability to buy from you. What’s going on in the US with the Trump administration is an excellent chance and the same thing will be going on in Holland and France and all through Europe.

Every four years, there’s about 2% more of the kind of people who voted for Hilary. Trump is a one term president at best, and the next president is going to be in the middle of an economic catastrophe. Americans are likely to vote for somebody that’s going to promise the government’s a cornucopia.

INVESTING IN A TRUMP WORLD

One of the good things about Trump is that he’s moving to gut the EPA. It means that mining is going to have a resurgence in the US. That’s the best place to be because the stock market is grossly overpriced by any reasonable parameter. That’s an accident waiting to happen at this point, and the bond market’s even worse. We’re at the bubble end of a 35 year bull market in bonds. Bonds are the biggest bubble in world history, at this point.

Commodities are very cheap right now. In the inflationary environment we’re going to have in the future prices are going to go way up. Food commodities are the place to be.

You should go where your money and yourself are treated best, and that’s no longer in the US.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/18/2017 - The Roundtable Insight: Jayant Bhandari On India’ Demonitization And Investing Using The Principles Of The Austrian School Of Economics

FRA is joined by Jayant Bhandari in discussing emerging trends resulting from India’s demonetization, along with suggestions for investment in a Trump world.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

UPDATE ON INDIA

India is becoming crazier by the day. In the last two weeks, the Indian government has come out with two new regulations which now make it illegal for people to do transactions of more than 300000 Rupees ($4500USD) in cash Remember this is a country where more than 95% of consumer transactions are cash-based. This country is becoming increasingly a police state. Everywhere people are losing jobs, food prices have fallen quite a bit, and farmers are going to face horrendous problems. In a country where more than 50% of the population lives on daily wages, if you have an economic crisis they will go hungry.

About 75-80% of Indians live in rural areas, but even in towns often there is no electricity. Only about 25% of India is connected by internet, and the connection is fairly unreliable. In rural areas there might be a bank among 50 villages. These people might need to walk 30-50km to take cash out of the bank if the government forces them to deposit. If you earn $1-2 every day, would you have time to walk for three hours each way to deposit your cash? This is an impossible situation.

EMERGING TRENDS

This has completely disrupted the economic structure of the country. Food prices have fallen quite substantially in the last few months, not because of excess supply, but because there has been a significant reduction in demand. This tells you only one thing: poor people cannot afford to buy food. Farmers can’t make money because prices have fallen so much, which means they’re dumping their produce. This means in the next cycle, these farmers will not be producing food. Food prices will be higher three months from now than they were before demonetization happened.

In the smaller villages, people have taken up bartering, but bartering only works well with tribal peoples. In a modern economy, bartering doesn’t work because you can’t do all of the transactions.

This is going to fail mostly because Modi wanted to impress a western audience that he was very pro-market, and he’s failed so badly that this will hopefully delay western governments approaching cashless societies.

AUSTRIAN SCHOOL OF ECONOMICS

Keynesian economics is superstition and irrationality. Keynesian economists believe that by running the printing press you can generate wealth. The only way to understand the world is through the understanding of Austrian economics, which is nothing but the common sense of rational economists.

The reality is that cash has no inherent value. It’s based on regulatory edict. Investors should stay outside the currency system. Money should be kept in jurisdictions where you have more trust in – internationalize to protect yourself. The more you spend outside the cash and banking system, the better it is for you.

There are property companies in Hong Kong and Singapore that are trading for 50% of their net present value. These companies offer you anything from 5-10% dividend yield. When you focus on countries that provide you very good downsize support, and you invest in companies with almost assured revenue and profitability, you put yourself in a situation where you continue to make a profit. There’s so much similarity between value investing and Austrian economics. One is how to invest your money; the other is an understanding of economics, and there is a huge amount of overlap. You want instruments that provide a higher yield than what the bond markets offer.

Precious metals are a great way to store your value. You could invest in properties, or property companies. Diversify yourself internationally and invest in countries that have a very good history of protecting your properties.

INVESTING IN A TRUMP WORLD

One does not necessarily have to agree with Trump’s policies, but he’s trying to do what he promised to do. There’s no other example in modern politics where a politician tried to do what he promised to do during elections. He’s trying to improve America’s position in the world, so if he succeeds America’s economy will improve quite a bit.

Trade can be a gray area, and it might be a negotiating ploy that Trump is using. Maybe he wanted to get Mexico to approve building a wall by making the subject much bigger than it actually was so Mexico would ignore the key thing – building the wall. Freedom of movement is important, but a lot of immigration is creating a lot of problems for the western world.

Nothing he’s doing is destroying the economy of the United States. It’s entirely possible that you can reduce the prices and improve the profitability of American companies and increase employment in the US, provided that Trump continues to do what he said he would do. As long as he’s taking the country in the right direction, countries and the stock market and investments will respond to that.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/14/2017 - Thorsten Polleit: The Major Central Banks Are Coordinating To Provide, As Needed, Unlimited Amounts Of Liquidity To The Financial System

“All major central banks around the world — the European Central Bank, the Bank of Japan, the Chinese central bank, the Bank of England, and the Swiss National Bank — have joined the liquidity swap agreement club. They also have agreed to provide their own currencies to all other central banks — in actually unlimited amounts if needed. It is no wonder, therefore, that credit default concerns in financial markets have declined substantially. Investors feel assured that big banks won’t default on their foreign currency liabilities — as such a credit event is considered politically undesirable, and central banks can simply avoid it by printing up new money .. The close cooperation and coordination among central banks under the Fed’s tutelage amounts to an international cartelization of central banking — paving the way toward a single world monetary policy run by a yet to be determined single world central bank .. The Fed’s policy has made the world’s financial system addicted to ever greater amounts of US dollars, easily accessible and provided at fairly low interest rates. From this the US banks benefit greatly, while average Americans bear the brunt: they pay the price in terms of, for instance, boom and bust and an erosion of the purchasing power of the US dollar .. Ludvig von Mises’s sound money principle calls for ending central banking once and for all and opening up a free market in money. Having brought to a halt political globalism for now, the new US administration has now also a once in a lifetime chance to make the world great again — simply by ending the state’s monopoly of money production. If the US would move in that direction — ending legal tender laws and giving the freedom to the American people to use, say, gold, silver, or bitcoin as their preferred media of exchange — the rest of the world would most likely have to follow the example.”

Dr. Thorsten Polleit, Chief Economist of Degussa, Honorary Professor at the University of Bayreuth, and Partner of Polleit & Riechert Investment Management.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/12/2017 - Jim Rickards: Real Assets Can Mitigate Risks During Financial System Lockdown Periods

“Central banks have printed so much money already, it’s not obvious that they can do it again from the current levels without destroying confidence in the dollar, and all major currencies. The question is, where will the liquidity come from in the next financial crisis if it can’t come from the central banks? The answer is the IMF. The International Monetary Fund has the only clean balance sheet out of the major financial institutions. It can print money. They call it the SDR, the Special Drawing Rights. I call new world money .. When it comes time for the IMF to issue world money (SDRs) to reliquify the world, there’s going to be a negotiation period. It will to take months to complete. During the last crisis this took 11 months. That was when the crisis hit in September, 2008 we saw Lehman Brothers hit a crisis, the IMF began to issue SDRs in August 2009 .. Even though they react on a case basis, it’s going to take, an estimated 3 or 4 months at least to get SDRs issued. In that interim period between the crisis and the time the IMF can react, central banks will be paralyzed. They’re likely going to lock down the system.

When I say lock down, they’ll start with money market funds. I can’t think of a greater misnomer than the money market funds .. If you lock down money market funds, people are just going to take their money out of the banks. Then you’re going to have to close the banks. Then people are going to sell their stocks, then you’re going to have to close the stock market. Every time you shut one path to liquidity, people are going to turn to another path.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/12/2017 - Danielle DiMartino Booth: An Insider Exposes The Fed

Danielle DiMartino Booth, former analyst at the Federal Reserve Bank of Dallas, has just released the book Fed Up: An Insider’s Take On Why The Federal Reserve Is Bad For America.

The Federal Reserve is controlled by 1,000 PhD economists .. The Fed continues to enable Congress to grow the U.S.’s ballooning debt and avoid making hard choices, despite the high psychological and monetary costs. And the addiction to the “heroin” of low interest rates is pushing America’s economy towards yet another collapse ..

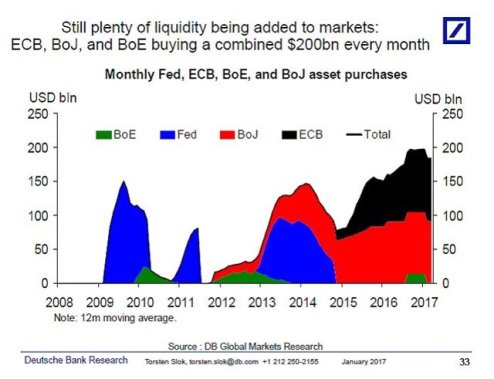

“That’s the trillion-dollar question. We didn’t used to call it that did we? We used to call it the million-dollar question. But it’s now the trillion-dollar question. The punditry up there will tell you that The Fed has been in tightening mode since the taper began several years ago, but I say hooey to that. What we have today is absolute fungibility with central bank purchases on a global basis. You’re talking about something upwards of $200 billion every single month. What the global bond market now revolves around, and relies upon, is the assumption that somebody somewhere will be conducting quantitative easing. As long as they do that, we’re operating in a bond market that is assuming that every single bond purchased by a central bank globally has been expired permanently .. You’re taking supply out of the system, which is the only thing that could get you to justify where bond yields are and, therefore the mirror image of that, where bond prices are, which is at record highs or close to record highs. That I think is at the crux of central bankers’ global dilemma. The first central bank that even hints that they are going to reduce the size of the balance sheet or even worse, sell off a single bond, it is game over at that point for the world bond market.”

On The Ticking Pension Time-Bomb: “The problem with pensions is that the sins are compounding over time. They are piling up. Every single fiscal year that goes into the history books with a 6%+ gap between what was assumed versus what was returned piles on to the next year of equal, if not worse, relative underperformance .. You’re talking about having to make up for all of that lost time, but in spades — at multiples of what the current rate of return assumptions are. Going forward, on an ongoing basis for years to come. Which is highly unrealistic when you are staring down the barrel of an almost 40-year bull market in bonds and the second longest bull market in US history. The assumptions are simply Herculean in magnitude and impossible to achieve. That’s why you’re seeing rate of return assumptions begin to come down. This is all good, fine and well until you completely square the circle and understand that every time a municipality or a state pension plan reduces their rate of return assumptions, some entity, whether it be the state, the school district, some entity has to write a bigger check in order to make up for the cash flow that is no longer being assumed in by the actuaries via rate of return investments. It doesn’t work. You can’t do it for very long when you’re not bringing money in as a state municipality.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/11/2017 - Alasdair Macleod: Central Banks Are Creating Economic Distortions & Inequalities

“Central banks must be increasingly aware that critics of monetary policy are getting some traction in their arguments, that not only have monetary policies failed in their objectives, but they are creating counterproductive economic distortions as well. Chief among these is the transfer of wealth that comes with monetary debasement .. An expansionary monetary policy rewards spendthrifts and penalizes savers. The benefits and costs are distributed unevenly, and are economically and socially disruptive. We have moved a long way from the Keynesian concept of deficit spending being limited to when the economy appears to be failing. Today, intervention has become continual, with the emphasis on monetary policy. Inevitably, the consequences must be distributional, otherwise the policy would not have been embarked upon in the first place .. The headline statement, that there is little or no evidence that monetary policy since 2008 has contributed to social inequality, is misleading, and deflects blame for society’s ills away from monetary policy. The implication is blame must lie with fiscal policy or free markets themselves. And while central banks and finance ministries apportion responsibility for policy failure, it never occurs to either party that ordinary people do far better running their own lives with sound money.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/10/2017 - The Roundtable Insight: Yra Harris & Peter Boockvar On Implications Of The Border Tax, Dodd Frank Act Changes, And Steepening Yield Curves

FRA is joined by Peter Boockvar and Yra Harris in discussing their predictions for Europe and the actions of the ECB, along with the Fed’s behavior and potential consequences.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

Yra highly recommends reading The Rotten Heart of Europe – send an email to rottenheartofeurope@gmail.com to order

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University. Check out Peter’s new newsletter service at www.boockreport.com.

EUROPEAN PREDICTIONS

What has been going on in Europe even with the ECB’s aggressive QE program is that the 2/10 has a far different character from other yield curves like the 5/30. The 2/10 is an investor curve and the 5/30 is much more speculative. Those curves have been steepening out fairly dramatically. Sophisticated investors and speculators are selling into the ECB buying the long end. Usually steepening curves are not good for currency in the short term, because they reflect that the economy is hotter than the central banks have prepared for.

The Greek curve has inverted again, significantly so. That’s sending a signal that the Greeks are having problems on the 2-year end. People are very nervous about Greek’s ability to make it through the next phase of the lending crisis.

There’s a rise in inflation expectation. We know that the markets are testing out the ECB, and that come April their monthly purchases will be reduced 20%. They’re extending the term of QE but on a flow basis they’re cutting it by 20%. Adding it all up, it helps to explain that steepness. You can pick apart that it’s good if it’s responding to growth, and it’s not good if it’s responding to inflation or the ECB backing off. Europe’s been buying less foreign bonds, which implies that they’re buying less of their own bonds. This is happening in the face of the ECB purchases. The Germans are furious that they’re seeing inflation to the extent that they are and the ECB is still going full steam ahead. That pressure is only going to grow.

The overnight deposits at the ECB are at an all-time high, and the repo rate isn’t moving in Europe. People in Europe are very nervous; they’re willing to give the ECB their reserves. This is a great signal that investors are getting nervous. The European equity markets are stalling out and US markets are carrying on like this doesn’t affect them, but any of these problems are systemic in nature at this point. The amount of sovereign debt purchased by all domestic banks in within the old established nations is so bad that if this seizes up, the repercussions will be felt globally.

EFFECTS OF INTERNATIONAL CAPITAL FLOWS

It’s possible that in times of nervousness that people repatriate money back home. Why else would you have record deposits when you’re being taxed 40 basis points? US money may leave Europe if there’s a problem and come to the US, but European money is not necessarily going to leave Europe if they have their own liquidity and balance sheet issues. Safe haven trades don’t play out the way people think they will, because they’re not one dimensional.

If the US puts on the border tax, the hit to the global financial system would bring on a wave of deflationary liquidation of assets that could really wreak havoc. The main thesis behind the border adjustment tax is that we’re going to tax goods that are imported, not exported, and importers don’t worry because the Dollar will rally 20% which offsets the 20% tax and everything will be fine. But overhauling the US tax code on the corporate side and placing all your chips on foreign currencies and the Dollar is incredibly stupid. Maybe the Dollar rallies, maybe it takes three years to adjust, and in the meantime the economy goes into recession because the price of goods rises to an extraordinary extent on an economy that’s dependent on consumer spending. And you throw in the $10T of Dollar related debt held by companies overseas that will get killed by the strengthening Dollar.

If the Dollar weakens from this border adjustment tax, then the US goes into recession.

CHANGES TO THE BANKING ACT

Banks will still have to hold a lot of capital, and hopefully we’ll have incentives for banks to lend. In terms of effect on the US economy, we still need a willing lender and a willing borrower, and hopefully this will facilitate that.

If you’re a commercial bank, you should have to adhere to the rules. The problem is that if you’re a bank and you want to leverage yourself off, you have to reveal daily what your risk profile is, and you can’t get FDIC insurance if you hit a certain risk level. Banks like everyone else should pay commissary value for the risks they’re taking.

The best part of Glass-Steagall was that it separated commercial banks from investment banks. It’s the small banks that had been most burdened by Dodd-Frank, but it’s the small banks that will hopefully get the most relief from the changes.

FED WOEFULLY BEHIND THE CURVE

The stock market is at an all-time high and the Fed Funds rate is at 0.65%. Historically the Fed Funds rate is 2 points above inflation. Even to get real interest rates back to zero, the Fed Fund’s rate should be at 1.5-2%. In the eighth year of an economic expansion, the Fed thinks negative interest rates is the right policy. That’s extraordinarily dangerous, and the Fed seems to be realizing that they’re caught and if Trump is successful in creating faster growth, it’s going to be hugely inflationary while they sit at 6.5%. They may raise in March, since they’ve shown that they like to raise on the day of a press conference meeting.

A lot of this year is going to be determined by central banks and interest rates, and less so Trumponomics. Germany is doing fairly well, with 1.7% inflation and a 2 year yield that’s negative 80 basis points. Germans should be borrowing money hand over fist to buy hard assets, since that’s where things are going to play out. Yes, the US is going to have tax and regulatory relief, but it’s a played out game. It’s a good value to buy things, in Germany, that have to be vastly undervalued.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/09/2017 - McAlvany Commentary On The Uncertainty Hedge

The “Uncertainty Hedge” Gold up 6.6% so far this year. Stock Market Price/ Earnings Alarm sounds…Highest since Tech Stock Bubble. Hussman says stocks are Overvalued, Overbought & Over-Bullish… sees 50% possible drop.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/09/2017 - Bill Gross On The Financial Methadone Provided By Central Banks

“What’s wrong with financial methadone? What’s wrong with a continuing program of QEs or even a rejuvenated U.S. QE if needed? Well conceptually at first blush, not much. The interest earned on the $12 trillion is already being flushed from central banks back to government fiscal authorities. One hand is paying the other. But the transfer in essence means that monetary and fiscal policies have joined hands and that the government, not the private sector, is financing its own spending. At an expanding margin, this allows the private sector to finance its own spending and fails to discriminate between risk and reward. $600 billion in the U.S. for instance goes into the repurchase of company stock, whereas before, investment in the real economy might have been a more lucrative choice. In addition, individual savers, pension funds, and insurance companies are now robbed of the ability to earn rates of return necessary to maintain long-term solvency. Financial Armageddon is postponed as consumption is brought forward and savings suppressed and deferred .. While a methadone habit is far better than a heroin fix, it has created and will continue to create an unhealthy capitalistic equilibrium that one day must be reckoned with. Yields will likely gradually rise (watch 2.60% on the 10-year Treasury), yet they will stay artificially low due to the kindness of foreign central bank quantitative easing policies. But that is not a good thing.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/06/2017 - Grant Williams: A Punch To The Face For Central Banks

Peak Prosperity special .. Grant Williams, publisher of the economic blog Things That Make You Go Hmmm and principal of Real Vision TV, returns to the podcast this week to discuss his expectation of a return of volatility to the markets .. Grant warns that over the past seven years, the various financial markets around the globe have melded into a single world market dominated by trading algorithms and the central banks. This new system only knows how to operate effectively in one direction: Up .. Grant is very concerned that a return of volatility will act as a wrench tossed into the gears, quickly throwing the world financial system into panic.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

03/17/2017 - Paul Brodsky: “Stagflation On The Horizon”; Coordinated Currency Devaluation Ahead

03/17/2017 - Paul Brodsky: “Stagflation On The Horizon”; Coordinated Currency Devaluation Ahead