Link here to the MP3 Voice Podcast

07/16/2026 - The Roundtable Insight – Charles Hugh Smith on the Risks, Costs and Uses of AI

07/16/2026 - The Roundtable Insight – Charles Hugh Smith on the Risks, Costs and Uses of AI

Link here to the MP3 Voice Podcast

05/14/2026 - Join the CedarOwl team for Geopolitical Intelligence Risk services

05/01/2026 - The Roundtable Insight – Charles Hugh Smith on what it will take to become BullishDownload the Podcast in MP3 for Voice Only

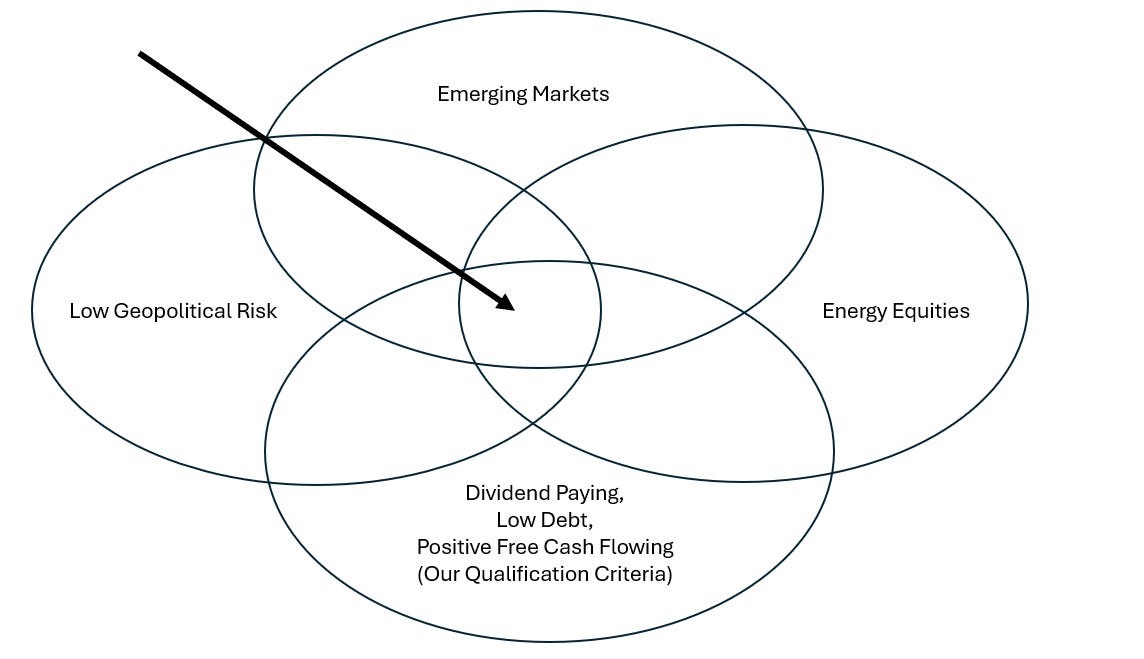

03/11/2026 - The Roundtable Insight – Charles Hugh Smith on the Current Waves and Cycles – Energy, Commodities, InflationDownload the podcast in voice mp3 format link here

to view the venn diagram discussed in the podcast, cedarowl.substack.com – link here:

03/09/2026 - The Roundtable Insight – Trader Ferg on Emerging Market and Dividend-paying OpportunitiesDownload the Podcast in MP3

Substack Link => cedarowl.substack.com

02/19/2026 - The Roundtable Insight: Dr. Marc Faber & Yra Harris on Precious Metals & Where the Financial Markets are HeadingDownload the Podcast in MP3 Format

02/12/2026 - The Roundtable Insight – Louis-Vincent Gave & Yra Harris on Opportunities in Emerging Markets and Asian Currencies

01/13/2026 - The Roundtable Insight – Daniel Lacalle and Yra Harris on Gold and the Intensifying Sovereign Debt CrisisDownload the podcast in MP3 voice here

01/07/2026 - Wow watch again Dr. Marc Faber & Yra Harris in May of 2025 – How Prescient!

Summary of the discussion:

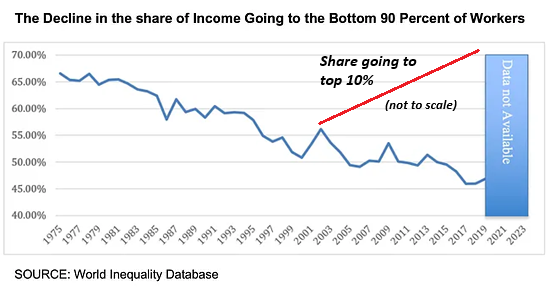

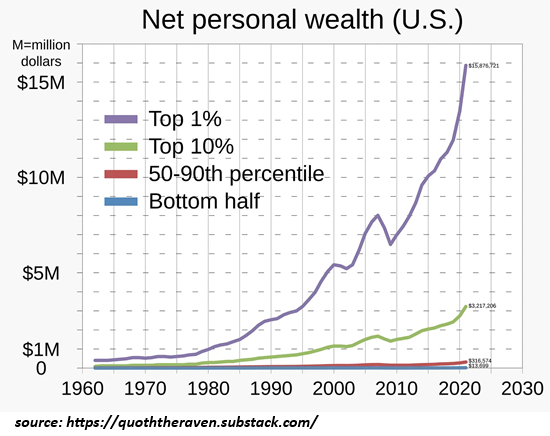

The discussion argues that the post‑COVID global economy is structurally weaker than in 2018–2019, with a “two‑tier” system in which asset owners benefited from inflation in financial assets while the middle and lower classes suffer from real income stagnation, higher living costs, and much higher interest burdens on credit cards and mortgages. The speakers contend that official inflation data significantly understate true cost‑of‑living increases, liken tariffs to hidden tax hikes, and criticize current U.S. policy for squeezing households while preserving an asset bubble supported by years of artificially low rates. They see many households effectively already in recession and point to weaker indicators such as disappointing travel bookings and rising homelessness as evidence of declining real prosperity and affordability.

On policy and geopolitics, they argue that U.S. interest rates were held too low for too long, creating excessive debt at both government and household levels, and warn that cutting rates now would risk signaling that the Federal Reserve has abandoned any serious fight against inflation, potentially pushing long‑term yields higher rather than lower. Tariffs and great‑power rivalry are framed as part of a long historical pattern, with current U.S. tariff policy described as economically harmful “taxation,” while China’s Belt and Road Initiative is characterized as a politically motivated but economically constructive alternative to military intervention that improves market access and infrastructure for participating countries. They emphasize China’s long‑term strategy to bypass maritime choke points and reshape Eurasian trade routes, contrasting it with what they see as short‑term, often militarized Western approaches.

In markets, they argue that U.S. equities have likely peaked in real terms and that the dollar is overvalued on economic fundamentals, anticipating a multi‑year environment where non‑U.S. markets and select emerging economies outperform after a decade of underperformance. They highlight value opportunities in markets such as Brazil, Chile, Colombia, and parts of Asia (including Singapore, Malaysia, Indonesia, and Thailand), with particular interest in Asian banks, while noting that all markets remain vulnerable when U.S. equities sell off. They also describe Singapore as an increasingly important wealth‑management hub benefiting from political stability and personal safety, attracting capital from across Asia and serving as a kind of “Switzerland of Asia.”

On precious metals and portfolio construction, they maintain a constructive long‑term view on physical gold due to chronic fiscal deficits, growing debt burdens, and what they expect to be structurally higher inflation culminating in some form of systemic “reset.” However, they stress that investors are generally underweight physical gold and discuss platinum as a particularly attractive store‑of‑value candidate, arguing that platinum is historically very cheap relative to gold and may offer better upside with less downside risk, even as central banks are more likely to concentrate their reserves in gold. Overall, the conversation emphasizes risk control over return maximization, urging investors to think less about beating benchmarks and more about preserving real purchasing power in an over‑leveraged, politically fragile, and financially repressed global environment.

12/18/2025 - The Roundtable Insight – Charles Hugh Smith on Insane Financial Imbalances and a Social RevolutionDownload the Podcast in MP3 Voice

12/12/2025 - The Roundtable Insight – Peter Boockvar & Yra Harris on the Trends in Yields, Currencies and Investment Ideas

12/03/2025 - The Roundtable Insight – Luke Gromen & Yra Harris on Escalating Liquidity, Debt and Market RisksDownload the Podcast in MP3 Here

11/14/2025 - The Roundtable Insight – Fed Guy Joseph Wang and Yra Harris on the Trends in Liquidity, Repo Markets and Stimulus

11/05/2025 - The Roundtable Insight – Clive Thompson & Yra Harris on Gold and Value Investing Ideas, with Charts from Judd Hirschberg

10/28/2025 - The Roundtable Insight – David Woo and Yra Harris

10/09/2025 - The Roundtable Insight – Judd Hirschberg on Gold, Silver, Platinum and the Financial MarketsPodcast to be posted shortly ..

09/12/2025 - The Roundtable Insight – Rudy Havenstein & Yra Harris on Gold, Inflation and Financial Repression

09/04/2025 - Sign Up Here to the CedarOwl Substack Notice: Effective this month September 2025, we will no longer be maintaining our regular email distribution for the posts. Please subscribe to our partner firm’s substack to get email distribution for the podcasts. Thank you.

Link Here to the CedarOwl Substack

08/26/2025 - The Roundtable Insight – Charles Hugh Smith on AI – the Hype, the Great Positives and the Dystopian Negatives

07/25/2025 - The Roundtable Insight – Rob Arnott & Yra Harris on the Long-Term Trends in the Markets

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority