01/19/2022 - Louis-Vincent Gave on Russia, China and the U.S. Dollar

“China and Russia are the most obvious natural trade partners in the world, right? Russia produces all the commodities that China needs. And China produces all the consumer goods and the finished goods and the capital goods that Russia needs to continue industrializing. So, you know, for them to, you know, if there’s one, you know, sort of bilateral trade relationship where you can imagine that trade will continue to expand at many times the rates of GDP growth, it’s got to be that one. And so, you know, and you know, the more trade you have between two countries, usually, you know, if you’re a believer in Ricardian equivalency and Ricardian comparative advantages, then, you know, you got to look at it positively.” – Louis-Vincent Gave on MacroVoices

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/19/2022 - The Role of Central Bank Digital Currency in the Coming Financial Reset

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/29/2021 - Felix Zulauf Interviews and Public Domain Quotes

“I do believe that we are looking at a very important medium-term peak. But I do not believe that is the end of this current market cycle. I think the market cycle will most likely stretch into 2024. But what we are facing now is a is a medium-term top in the next few weeks, and then a very decisive decline. And this is because, first of all, I see the world economy weaker or slowing (faster) than the consensus. I think the overshooting of retail sales on the pre-pandemic trend by 16% in the US, is an aberration and will be corrected because the fiscal impulse that was so positive will turn negative in 2022, negative by about 4 – 6%. This will dampen economic activity; real personal income is now negative and not positive anymore. I think the rest of the world is slowing too, particularly China, which continues to slow and is in a recession and will most likely stay in a recession into midyear. And while they are loosening up the tight policies, they are not stimulating yet. I expect that (to happen) from spring on, only not before. And all of this tells me that the world economy and the US economy will most likely disappoint in terms of growth, and particularly in the first half… Usually when a market corrects, you have a plain vanilla 8 – 12% correction or anything on that order. But we have had tremendous excesses of capital flows into equities. US equities, including equity products, was on the order of over $1 trillion in the last 12 months. And this compares to the same amount for the last 20 years combined. So, this is an excess of a century. And usually, when you go into a correction, highly positioned, highly leveraged, high margin accounts surprise on the downside. So, it’s very possible and conceivable that when we have usually a 10% correction, all of a sudden, it could trigger a 20 – 30% correction. And therefore, I think the first half of the year, will most likely show a very serious correction. And that could shake the authorities. And instead of the interest rate hikes that the Fed has been forecasting, I think they will rather turn around and stimulate again around the middle of the year, when the correction in the market arrives. And that should give us the next run-up to new highs. So, I could see equity indices, declining 30%, and then go up 100% to the Peak in 2024. And if the peak in 2023 – 2024 is a better economy, I think you will have another run in the commodity complex; you will have wages going higher, and you will then see the CPI probably around 10%. And, at that time, you have higher bond yields, and you have a central bank and probably around the world that has no choice but to tighten. And that I think will be the end of the bull market that we have been seeing from 2009. And that will lead to major crises probably for a few years thereafter. So, the big picture has been stretched a little bit. But, nonetheless, I see a serious and painful decline in the first half of 2022.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/29/2021 - Dr. Lacy Hunt Interview

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/20/2021 - Dr. Marc Faber on the Markets, Inflation and the Economy

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/20/2021 - Yra Harris: The Week That Was

“By week’s end the global stocks were down as the onset of OMICRON concerns were spreading fear of additional global restrictions. Over the weekend, it was reported that the DUTCH were shutting down and other nations raised their protocol levels. That should stem travel, especially during the winter holidays. Be patient as this is a liquidity-starved week and the algos will be delivering plenty of volatility.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/13/2021 - Yra Harris – Coal for Some Stockings?

“THE MOST HAWKISH OUTCOME OF THE FED THIS WEEK WOULD BE TO END ALL PURCHASES OF SOVEREIGN DEBT AMD MBS AS IT WOULD MAKE ALL OF 2022 FED MEETINGS LIVE FOR RAISING RATES. Powell’s FORWARD GUIDANCE PROMISES WERE THAT THE FED WOULD NOT BEGIN TO RAISE RATES UNTIL TAPERING OF BOND PURCHASES WAS COMPLETED.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/08/2021 - Yra Harris: It’s Hard to Believe

“If the G-7 nations would coordinate their policy decisions and the DOLLAR were to weaken, then the U.S. YIELD CURVE would probably reverse its recent FLATTENING action. Pay attention to currency levels. A critical currency outlier continues to be the Chinese yuan as it continues to rally in direct contravention to conventional wisdom: weak Chinese economy, weak currency. It is making a 40-month high Wednesday. Does this mean a further commodity rally as the CHINESEECONOMY shifts to more domestic consumption? .. There was a Financial Times piece last week by Ruchir Sharma titled, “China is Faltering, but the World is not Feeling the Effects.” Sharma, a Morgan Stanley global strategist noted “exports have fallen as a share of China’s GDP from above 35 percent before 2010 to less than 20 percent today.”I s this the sea change in the global economy that Professor Michael Pettis has been discussing for many years? If so, what will the impact be on the world economy and especially will the disinflationary force of China’s one billion workers be felt through higher prices as the Chinese export less and consume more?”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/30/2021 - Alejandro Tagliavini – Las penas son de los pobres, los dólares son ajenos

” La violencia siempre destruye, ya lo sabía Aristóteles -y lo repitieron muchos como santo Tomás de Aquino- al que, obviamente, no leyeron en el Gobierno. Y no solo que no lo leyeron, sino que creen todo lo contrario, creen que los problemas de la violencia se solucionan con más violencia. Como dice Roberto Cachanosky “Un control lleva a otro, hasta que se termina ahogando por completo la actividad privada o el Gobierno termina hundiéndose en una catástrofe económica, social y política”.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/24/2021 - David Rosenberg on Inflation, Japan, Gold

“According to our models, valuations are much more compelling in Asia than they are in the United States. Thus, I like Asia over the U.S., particularly in the case of Japan. Japan is one of the most inexpensive stock markets in the world. And, with the recent victory of the Liberal Democratic Party, the political outlook has eliminated a source of uncertainty. What’s more, in the past few months, Japan has done a stellar job in getting their COVID case count down and their vaccination rates up. And of course, the recent cheapening of the Yen is a boon for their large cap exporters.

It is still very difficult to get a pulse of the Japanese consumer, but the business sector seems to be in very good shape. I think the industrials will perform well, especially with the upcoming fiscal stimulus and the weakening of the Yen. So large cap exporters will probably benefit the most.

If you’re looking for a hard asset that is unloved and underowned, gold and gold mining stocks will be a very good place to be. Very recently, gold has been firming despite a strong U.S. dollar. If I’m right with my forecast and the dollar depreciates next year and real interest rates stay negative, this will be a very important tailwind for gold. There’s also the prospect that China continues to embark on its regulatory crackdown on crypto currencies, which should also be a positive for gold. Finally, you see it on a technical basis: Gold has been breaking out.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/22/2021 - Yra Harris – Odious, Indeed

“The main concern for the world is not TRADE but the massive amount of DOLLAR-DENOMINATED DEBT. In the last decade, global debt has grown to $330 trillion from $200 trillion, according to IMF, BIS and IIF. The dollar’s status as the world’s reserve currency means a large percentage of the DEBT is denominated in U.S. currency, especially because the Fed’s aggressive QE policy has sustained very low interest rates to enable DOLLAR funding for many emerging market businesses.

Many emerging market central banks have begun raising rates to keep their currencies attractive so as not to create stress for their private sector dollar borrowers. But how high can rates go in Brazil, Mexico, Russia and others before their economies begin to slow?

The Europeans need to be more concerned about its policy of LOWERFOR LONGER sending the DOLLAR to levels that cause global systemic stress in the DEBT markets. Lagarde is pursuing a one-dimensional goal in a multi-faceted world. While some may not think this is ODIOUS it will prove to be reprehensible. Market signaling mechanisms are broken in the face of massive QE purchases so there are no market forces to upset the ECB agenda, or the BOJ’s. The FED is going it alone … maybe. Perhaps it’s time for a G-7 meeting?”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

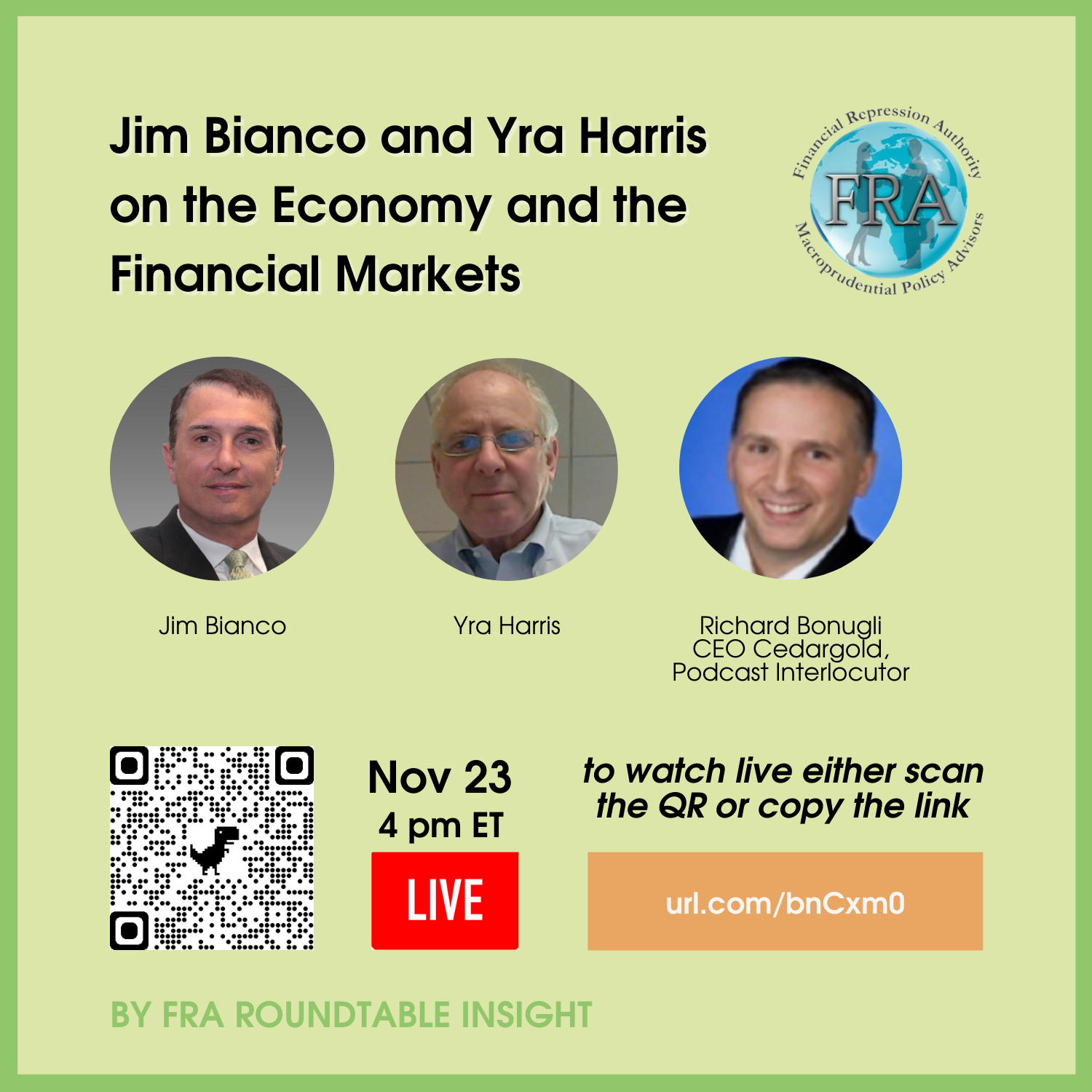

11/16/2021 - Live Podcast on Nov 23 – Jim Bianco and Yra Harris

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/16/2021 - Alejandro Tagliavini – La nueva moda global, la estanflación

” ‘Estanflación’, estancamiento con “inflación” -suba del IPC, en rigor-, es un término acuñado por un político británico, Iain Macleod, en 1965, cuando muchos economistas dudaban de que una economía con poco o ningún crecimiento y tasas de “inflación” más altas de lo normal fuera posible, según cuenta Laura Sánchez de Investing.com. La peor estanflación que se recuerda en EE.UU. ocurrió durante la década de 1970.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/15/2021 - Yra Harris: A Possible Solution to the Central Bank Dilemma

“THE GOLD/CURRENCY SPREADS DISCUSSED IN THIS BLOG HAVE BEEN A MARKET RESPONSE TO THE LOOMING CREDIBILITY GAP OF ALL CENTRAL BANKS IN A FIAT CURRENCY WORLD. Listening to the recent speeches from ECB and FED members there still seems to be a race to be the greatest liquidity provider in a QE-dominated world. The move to buy the precious metals in the face of rising short-term interest rates is a response to concerns that the CENTRAL BANKS HAVE NO ANSWERS TO THE TRAP OF FORWARD GUIDANCE AND ITS MANTRA OF LOWER FOR LONGER.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/08/2021 - Yra Harris: What Turned the Markets On Friday?

“If my conjecture is correct get prepared for increased volatility, especially in the U.S. DOLLAR and precious metals, but be patient as this story will unfold in the wake of Congress finally passing an infrastructure bill.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/04/2021 - Alejandro Tagliavini on Elon Musk and The Natural Market

“As I have explained in previous notes, succinctly, today there are three economic theories. Keysianism, which we know for being a great setter of bubbles, print and print money bills believing that this is how they move the economy and what they achieve is an artificial balloon that when explodes destroys more than what eventually achieved. Then, the neoclassical economic theory -the preferred one of market operators who distrust exaggerated issuance- whose characteristic consists in believing in the equilibrium -of the supply and demand curve- of the market, which implies that perfect knowledge has been reached and, therefore, that it is static and rigid: the company is only a productive function, a means to transform inputs into products.

nd, finally, the theory of the natural market (“free” from artificial State interference), initiated by the Spanish scholastics of the School of Salamanca of the 15th and 16th centuries, and taken up, to some extent, by the Austrian School of Economy that knows that there is no equilibrium -because there is no perfect, static knowledge- but a specific environment in permanent movement, which tends towards equilibrium at the rate at which market players find new knowledge that is always perfectible and pose new horizons that move the point of balance.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

11/01/2021 - Yra Harris: The Odious Designs of ECB Policy

“The coordination of central bank policies for the last decade is what is truly ODIOUS but its continuation provides trading and investment opportunities. Our job is to find those and put the lowest risk strategies to work. Now onto the FOMC meeting this week.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/29/2021 - Dr. Albert Friedberg on Inflation and Commodities – Quarterly Podcast

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/25/2021 - Marc Faber on the Federal Reserve and the U.S. Dollar

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/18/2021 - Yra Harris: Shedding Some Light

“The FED wants to proclaim how noble its efforts have been but the DEBT created in its name have not had its day of reckoning. Maybe, that is why inflation is deemed to be the best cure to the massive problem providing a SPECTRE that haunts the world. This will be a theme for the fourth quarter here at NOTES FROM UNDERGROUND.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/19/2022 - Louis-Vincent Gave on Russia, China and the U.S. Dollar

01/19/2022 - Louis-Vincent Gave on Russia, China and the U.S. Dollar