12/11/2015 - AUSTRIAN SCHOOL FOR INVESTORS with Ronald-Peter Stöferle

12/11/2015 - AUSTRIAN SCHOOL FOR INVESTORS with Ronald-Peter Stöferle

FRA Co-Founder Gordon T. Long discusses the Austrian School of Economics with German Finance bestselling author, Ronald-Peter Stöferle. Ronald is a Chartered Market Technician (CMT) and a Certified Financial Technician (CFTe). During his studies in business administration and finance at the Vienna University of Economics and the University of Illinois at Urbana-Champaign, he worked for Raiffeisen Zentralbank (RZB) in the field of Fixed Income/Credit Investments. After graduation, he participated in various courses in Austrian Economics.

In 2006, he joined Vienna-based Erste Group Bank, covering International Equities, especially Asia. In 2006, he also began writing reports on gold. His six benchmark reports called ‘In GOLD we TRUST’ drew international coverage on CNBC, Bloomberg, the Wall Street Journal and the Financial Times.

He was awarded 2nd most accurate gold analyst by Bloomberg in 2011. In 2009, he began writing reports on crude oil. Ronald managed 2 gold-mining baskets as well as 1 silver-mining basket for Erste Group, which outperformed their benchmarks from their inception. In 2014 he published a book on Austrian Investing, Austrian School for Investors – Austrian Investing Between Inflation & Deflation.

AUSTRIAN INVESTING BETWEEN INFLATION & DEFLATION

“For an investor it is critical to understand we are not in a cyclical crisis; we are in a systemic crisis.”

Well I have to admit I am not an economist which is why I am open to the Austrian school of economics Complex econometric models that try to forecast future models simply do not work, the 2008 financial crisis is an example of that. The Austrian school of economics simply described is “common sense economics.”

As a practitioner we are writing about the theory of the Austrian school of economics. It is a book dedicated to the practitioners of the Austrian school. What I want to point out is that the Austrian school has a completely different view when it comes to inflation and monetary systems.

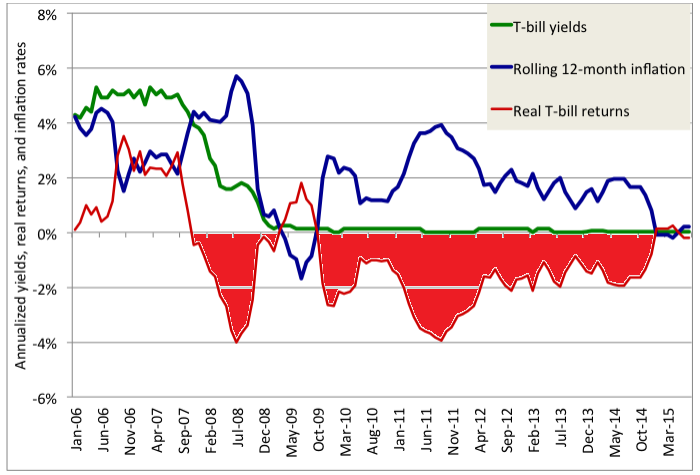

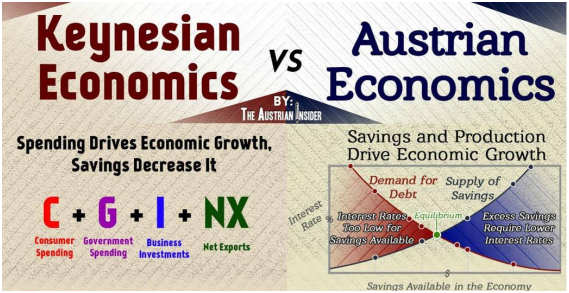

For Keynesian economists inflation is simply a rise in prices. There is no point in discussing the details of inflation, however for Austrian economists it is an increase in the money supply.

The Austrian school shows the new monetary system which began august 1971, when President Richard Nixon suspended the convertibility of the dollar into gold. Since this was done we have seen major misallocation of capital.

“This interplay between inflation and deflation is crucial to understand, this refers to the term, monetarytectonics.”

“If you have an Austrian mindset, you have a great advantage.”

You are able to understand other currencies, thinking outside the fiat money system and as an investor focus on the real results not the nominal results you make.

THE CHANGING CREDIT CYCLE

“In 2016, we very well may face a recession.”

For an Austrian a recession is something that’s normal, it is like a fitness program that prepares the economy for the next stage up. Trying to avoid such a recession will be difficult as QE, fiscal stimulus, monetary stimulus and low interest rates only make the situation more severe.

“The credit cycle leads the business cycle and therefore the fed will have a hard time fighting this falling trend in economic activity.”

To fight against it, negative rates in the US might be implemented. Many academic studies in the US say that evidence from Europe shows that negative interest rates work. The Fed may very well consider implementing negative interest rates. We will see increasing fiscal stimulus. There are many voices saying we should introduce helicopter money, but rather is it now called The People’s QE.

INVESTING ADVICE FROM THE BOOK

- To have a nonfragile portfolio, and investing in your own skill set offers a great yield.

- A good investor separates from a bad one in times of crisis.

- Become an entrepreneur, the Austrian school greatly encourages entrepreneurship.

- The Austrian school is very modest in saying we cannot predict the future but be prepared for all scenarios.

- It is highly recommended to read Austrian School for Investors – Austrian Investing Between Inflation & Deflation. Many people have interpreted it as a philosophical book that attempts to cultivate and establish this Austrian mindset. It is a pragmatic school of thought which offers great benefits if implemented, and this book is the perfect guide to it.

Abstract written by Karan Singh karan1.singh@ryerson.ca

{kind=link}