International Man’s Jeff Thomas writes about the increasing level of legislation that controls what individuals are allowed to do with their own wealth – financial repression .. “Many people who see the writing on the wall are doing whatever they can to exit the banking system as much as possible, in spite of the fact that the banking system is essential to most types of economic transactions.” .. Thomas sees a move towards electronic money, away from physical cash .. “After this is completed, confiscations will occur. Again, these will be implemented by the banks. But in order to maximize the amount that will be taken, it will be necessary to force people out of other forms of wealth storage and into bank deposits.” .. Thomas highlights the potential effects on bank-based safety deposit boxes – governments & the banking sector will likely try to herd the wealth from safety deposit boxes into bank deposits to make it easier to do bailins .. “Banks are now a time bomb for depositors. Wealth storage in safe deposit boxes looks to become a thing of the past.” .. Thomas advises non-bank wealth-storage facilities for storing precious metals.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/04/2015 - Deutsche Bank: The Federal Reserve is Embracing Financial Repression

Deutsche Bank now says that the Federal Reserve has been, through their monetary policies, destroying the capital markets & the economy .. “We think the Fed is obliged to talk up the economy because if they were brutally honest, the economy .. could quickly evaporate .. At issue is whether or not the Fed in particular but the market in general has properly understood the nature of the economic problem. The more we dig into this, the more we are afraid that they do not. So aside from a data revision tsunami, we would suggest that the Fed has outlooked not just horribly wrong, but completely misunderstood .. the idea that the economy is ‘ready’ for a removal of accommodation.” .. Deutsche Bank thinks the Federal Reserve is embracing financial repression rather than the “uncertainty of asset price deflation and a debt default cycle.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/01/2015 - Jim Rogers Talks Financial Repression

Special Guest: Jim Rogers – Investor, Bestselling Author & Financial Commentator

FINANCIAL REPRESSION

“Financial Repression can mean many things but basically in a nutshell it is a lack of free market finance and human activity, where the government thinks it is smarter than we are!”

“History has shown many times that we are smarter than governments, politicians and the bureaucrats – but they don’t like to give up power. When they make mistakes they blame it on us and try and make us pay for it! When they see a problem arise their first instinct is to try and suppress the public and markets. They try and do things they think will make things better, but of course it doesn’t, and only makes things worse!”

GOVERNMENT CONTROLS & REGULATIONS

“When problems arise they put on exchange controls which is a time honored tradition of politicians and bureaucrats to correct mistakes they have made. We will have exchange controls in the US again – no question. We already have exchange controls to some extent such as FATCA and other things to make it more and more difficult for Americans to do anything as far as finances are concerned. They will put on trade controls, tariffs quotas – they will come up with all sorts of things.”

Politicians don’t know what they are doing. History proves many times that politicians make things worse instead of better because what they do since they don’t know anything themselves, they ask the bureaucrats how they can save themselves. The bureaucrats rush in and say “this is the way you save yourself”. “It isn’t your fault, it is the markets fault and those evil speculators and the people! They then come up with regulations and controls. They don’t know what they are doing!”

Regarding ZIRP, Operation Twist and three rounds of Quantitative Easing, Jim Rogers predicts:

“We are going to have to pay a horrible price for yet another mistake made by the bureaucrats”

WHAT SHOULD INVESTORS BE THINKING ABOUT?

“The first thing investors should do is only do things they know a lot about! Don’t listen to me or anyone else who you don’t know what they are talking about. Do not so something that you yourself don’t understand perfectly.”

“Everyone should know about having assets outside their own country. We all have fire insurance which we hope we will never use. Look upon international diversification as a kind of insurance. … diversify internationally.

“If you don’t know about other asset classes then please, for goodness sake, learn about them because there are going to be many strange things happen in the next decade.

THE CERTAINTY OF ECONOMIC SLOWDOWN

“History shows in the US we have had economic slowdowns every four to seven years since the beginning of the republic. We are going to have them again no matter what people tell you. If someone tells you we will never have another economic slowdown – please put your money in your pocket and head as far away as you can!”

“It is going to be much, much worse than 2008. There is higher debt everywhere than previously!”

“We have never had history all the central banks printing such vast amounts of money at the same time! There is a hugh ocean of liquidity floating around out there!”

… and much more

Coming Exchange, Trade and Quota controls,

The dangers the coming Cashless Society,

The $5T Nominal Negative Interest Rate Sovereign Bonds,

The destruction of the US savings and working class,

The slowing Chinese Economy,

Why recessions are healthy. Why the avoidance of recessions leads to serious malfeasance.

The importance of investing in productive assets.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/01/2015 - Thorsten Polleit PhD – The Natural Interest Rate

The “Natural Interest Rate” Is Always Positive and Cannot Be Negative

Some economists have been arguing that the “equilibrium real interest rate” (that is the “natural interest rate” or the “originary interest rate”) has become negative, as a “secular stagnation” has allegedly caused a “savings glut.” The idea is that savings exceed investment, and that a negative real interest rate is required for bringing savings in line with investment. From the viewpoint of the Austrian school, the notion of a “negative equilibrium real interest rate” doesn’t make sense at all.

The market interest rate is the outcome of the supply of and demand for savings in the market place. It can be observed, for instance, in the deposit, bond, or loan market for different maturities and credit qualities. The originary interest rate is a category of human action, saying that acting man values goods available at present more highly than goods available in the future. In other words: Future goods trade at a price discount relative to present goods. For instance, 1 US$ available today is preferred over 1 US$ available in one year’s time.

If 1 US$ to be received in one year’s time is valued at, say, 0.909 US$, the originary rate of interest is 10 percent. (1 US$ divided by 0.909 minus 1 gives you 0.10, or 10 percent, for that matter.) 10 percent is here the originary interest rate (disregarding any other premia).

The “Originary Interest Rate” Reflects a Value Differential

The originary interest rate is expressive of a value differential, which results from so-called time-preference. The term time-preference denotes that acting man prefers an earlier satisfaction of wants over a later satisfaction of wants. Time-preference is always and everywhere positive, and so is the originary interest rate. This is, first and foremost, what common sense would tell us.

The notion that time-preference and the originary interest rate could be zero, does not only sound absurd, it is also a logical impossibility: Positive time-preference and a positive originary interest rate are logically implied in the irrefutably true “axiom of human action.”

Human action is purposive behavior, implying the use of means to achieve ends. Action requires time (it is impossible to think otherwise). Thus, time is an indispensable and scarce means for achieving ends. As such, it must be economized, which necessarily implies that an earlier satisfaction of wants is preferred over a later satisfaction of wants.

For (praxeo-)logical reasons, therefore, time preference and the originary interest rate cannot fall to zero, let alone become negative. The implications of a negative originary interest rate cannot even be conceived by the human mind: A zero originary interest rate already implies no action ever into eternity.

The End of the Market Economy

Should a central bank really succeed in making all market interest rates negative in real terms, savings and investment would come to a shrieking halt: as time preference and the originary interest rate are always positive, “capitalistic saving” — the accumulation of goods designed for improving the production process — would come to an end.

Capital consumption would ensue, throwing mankind back into poverty. It would be the end of the market economy.

The True Purpose of Negative-Interest-Rate Policy

For some reason, those who argue that the originary interest rate has become negative seem to overlook that the originary interest rate is a phenomena which is not confined to credit markets. It pervades all markets in which present goods are exchanged for future goods. For instance, the originary interest rate prevails at each stage of the economy’s time-consuming roundabout production. The originary interest rate also exists in the stock market, where investors exchange present money against a claim on future money (that is a firm’s dividend payment).

If they wanted to be consistent, the believers in a negative originary interest rate would have to call for a policy that does not only make interest rates negative in real terms in the credit market, but also in the markets for, say, stocks and housing.

However, a policy that advocates destroying firms’ values and peoples’ housing wealth wouldn’t be taken too kindly by the public at large; and those economists recommending it couldn’t expect being cheered.

The consequence of a policy of a negative real market interest rate should have become obvious by now:

It is an actually perfidious policy for debasing the real value of outstanding debt; and it is a recipe for wreaking havoc on the economy.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/31/2015 - Mark Nestmann on US Foreign Investment Taxation

Special Guest: Mark Nestmann – Lawyer, International Taxation Law

After establishing a noted career in international investment, Mark Nestmann left the US for three years to study for his “Master of Law” (LL.M.) degree in international tax law at the Vienna University School of Economics and Business Administration in Vienna, Austria. This is an indication of the seriousness and rigor with which Mark tackles issues in International Taxation for his high net worth clients. He shared his views with the FINANCIAL REPRESSION AUTHORITY in this exclusive interview.

FOREIGN ACCOUNT TAX COMPLIANCE ACT – FATCA

Passed in 2010 and hidden as part of a “Military Pensions Act”, no one fully understood what it meant or paid much attention to it.

“The Foreign Account Tax Compliance Act, is one of the most arrogant and one-sided laws ever passed by Congress. The idea behind FATCA, which Congress enacted in 2010, is simple: Demand that other countries enforce America’s imperialistic tax laws. And do so by the confiscation of foreign assets, if necessary.” – Why FATCA Is a Train Wreck Waiting to Happen – Mark Nestmann

“What is happening is foreign financial institutions (which is defined very broadly in the act) under the law are required to identify their US clients and force their US clients to self identify and turn over information to the IRS.”

“If the banks or countries don’t comply then 30% of their US source income (and in some case 30% of source gross sales revenues) of things like stocks, bonds, CDs etc are withheld – this is a pretty big number! The only way banks can avoid the 30% withholding tax is to essentially act as unpaid IRS informants.”

“Not surprisingly, FATCA and numerous other laws that require FFIs to enforce US money laundering, anti-terrorism, and securities regulations have led most of these institutions to fire their US clients. Perhaps one in 10 – and possibly fewer – non-US banks still permit US citizens or permanent residents to open accounts. That leaves little choice for Americans but to deal only with banks that have agreed to toe the IRS line.” – Why FATCA Is a Train Wreck Waiting to Happen – Mark Nestmann

“Non US persons investing in the US are also effected by FATCA. If their foreign bank don’t comply their US investment is whacked 30% as well – It isn’t just Americas who should care about this but basically everyone in the world!”

This is not a good time to have unreported financial accounts in countries that have already signed FATCA agreements with the US, or are about to. If you’re in this situation, you might want to seriously consider retaining a tax attorney to enroll you in the IRS’s latest Offshore Voluntary Disclosure Program.

PASSIVE FOREIGN INVESTMENT COMPANY – PFIC

“PFIC is another aspect of Financial Repression and aspect of regulatory restrictions on investment choices.”

“If you have an investment vehicle registered outside the US the IRS will consider it a PFIC. As an example of the way this tax is very unfavorable is that unless an offshore Mutual Fund qualifies as a US Mutual Fund when you sell it (or deemed to sell it) you have to file not only a return on the income by also a “throwback” interest charge for EVERY YEAR you held the fund. Additionally the tax rate is computed at the highest marginal rate in that year!”

“What happens is that people who held offshore mutual funds for a long period of time windup losing every penny of income in that fund because it is paid out in taxes and interest penalties.”

… there is much, much more in this 26 minute video interview covering:

CITIZENSHIP TAXATION (including the absurdity of 1986 Tax Legislation for “Mars”??)

UNOFFICIAL CAPITAL CONTROLS NOW IN PLACE,

US 2008 “EXIT TAX” (for citizens and Green Card holders on unrealized gains),

INHERITANCE IRS TAX GRABS,

THE NEW EX-PATRIOT ACT,

INVESTING ABROAD,

THE RATE OF ACCELERATION OF RESTRICTIVE FOREIGN CHOICES FOR AMERICANS,

THE GROWING MOVEMENT TOWARDS SECOND CITIZENSHIP PROTECTION,

WHY THE LEGAL ABOLISHMENT OF CASH IS COMING.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/30/2015 - Macroprudential Policy Driving the Financial Markets

Citigroup note confirms macroprudential policy (financial repression) is driving the the financial markets: “If there were any lingering doubt, this week’s gyrations demonstrate neatly that it is central bank liquidity, not fundamentals, driving markets. It is the flow, not the anticipated stock, of QE which counts .. Central bank policy pronouncements are almost the exclusive driver of market movements at the moment, not fundamentals .. with central bank liquidity the ultimate source of all market movements, investors are forced to shun fundamentals and instead hang on the central banks’ every word. At some point, of course, the risk is that the taps are turned off: recent speeches from Yellen, Draghi and others do demonstrate an increasing unease with market behaviour, and an increased emphasis on financial stability and the need for structural reforms. But with the underlying economy still weak, and vulnerable to a sharp sell-off in markets, we fear they will find that mangling, once started, is hard to stop. Particularly when they remain at least partly in denial as to the extent of it.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/29/2015 - John Mauldin Talks Financial Repression

Special Guest: John Mauldin – Financial Author, Writer & Publisher

FINANCIAL REPRESSION

“My recent book ‘Code Red’ was really all about Financial Repression. We were talking then about Currency Wars which has come to be played out. We were talking then about Central Banks driving down interest rates on savings to force retirees and savers into other types of investment and take more risk. They want them to move more out onto the risk curve which the central bankers believe will stimulate the economy. What they don’t understand is that taking it from savers, it takes it from their consumption behavior patterns.”

They are robbing from Peter to pay Paul, but in this case Paul is the banks and Wall Street Interests. It is not for the guy on main street.

“When the central banks start messing around with the markets they change the price of money and it has all sorts of unintended consequences!”

SEVENTH ANNIVERSARY OF ZERO INTEREST RATES

“This period of zero interest has created an extraordinary set of malinvestments as a result of unintended consequences. One example is they have money real cheap for Texas oil men. When you make money cheap for Texas oil men they punch holes in the ground. They moved out ‘onto the edge’. It created employment and drove rig prices up.” … “It changed behaviors, it changed how we think the world works – we will see how it works out!

BOND LIQUIDITY CRISIS

“Investors have been moving into high yield (HY) bonds. We are issuing risky HY bonds that are much more risky than 2007 with less covenants. Its like we didn’t learn anything! People feel they have to have more yield and can’t survive without it. We have bond funds where people are chasing longer duration bond funds. If interest rates on the long end of the curve grows by 1%, these longer duration bond funds (2 of the largest funds in the world) could lose 20%. Investors in 401K’s who see 20% losses will panic and hit the sell button. Because we wrote a bill called Dodd-Frank, which basically says you banks can’t get involved in providing liquidity to this market because we don’t want you to take the risk – they have shoved the risk to investors who will all try and get out the door at the same time!”

“It would not surprise me in the next crisis (and it will happen) to see the Federal Reserve step in and start directly funding Mutual Funds and ETFs trying to provide liquidity into a panicking market!”

A ‘SKYROCKETING’ DOLLAR

As John wrote in “code red” he sees a continuing strengthening in the US$.

“The dollar is going to get stronger than any of us can even imagine!”

“The BIS cites that emerging markets have borrowed some $9T in US$ terms.” As emerging markets weaken they must pay their loans in appreciating dollars. There is presently a mad scramble ensuing to cover this carry trade. Mauldin believes it will get even worse because of Japan.

“Japan is just continuing to print money. They are just going to print more money! When that doesn’t work they will print even more money. They have a sovereign debt crisis that the only way they can solve it to trash their currency and to move the debt they have generated from banks and pension funds unto the balance sheet of the central bank. That is their only solution. Today the 10 Year JGB market (it used to be one of the most liquid in the world) if the BOJ is not buying there are no trades! That is just shocking and is going to put pressures on currencies all over the world!”

“This is movie we just don’t believe will end well!”

LIKELY SCENARIO

A couple of countries have a major crisis,

It may possibly roll from country to country,

The Federal Reserve will supply SWAP lines to central banks around the world,

“Investors at this stage should start to consider what is their exit strategy!”

… and much more in the video discussion…. John gives his advise on what things investors must now be concerned with and how they should be preparing.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/29/2015 - Jim Rickards* on War on Cash, Repressive Interest Rates, Capital Controls, Potential Bailins

Latest Jim Rickards* interview with the Physical Gold Fund .. Rickards covers several aspects of financial repression happening – from the war on cash, to repressive interest rates by central banks, to capital controls & potential bail-ins, bank account freezes, how the zero interest rate policy (ZIRP) is taking money out of the pocket of savers & giving it to big banks .. very interesting: Rickards sees a time coming when the magnitude of the next financial crisis will be bigger than central banks can create liquidity for – he says in 1998, Wall Street bailed out a hedge fund, then in the financial crisis, central banks bailed out Wall Street, but in the next financial crisis, the IMF will be needed to bailout the central banks .. 1 hour

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/29/2015 - Financial Repression: The War on Cash

Mises Institute’s Dr. Joseph Salerno recently spoke .. Today cash is under attack like never before. Ultra low interest rates are the norm for commercial bank accounts. In Europe, as the ECB ventures into negative nominal interest rates, certain banks threaten to charge customers for depositing cash. Meanwhile, certain European bonds now pay negative yields, effectively turning them into insurance products rather than financial assets. And some economists now call for the outright abolition of cash, which shows just how far some will go in their crazed belief that economic prosperity can be commanded by forcing us to spend rather than save .. The War on Cash is real, it’s about financial repression & it will intensify .. 28 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/29/2015 - Gordon T Long Discusses The War on Cash

Financial Repression: The War on Cash

Wall Street for Main Street’s Jason Burack & Gordon T Long discuss the escalating war on cash .. why it is happening, when cash could be abolished .. what the real drivers of this movement are .. discussion on financial repression developments.. about 1 hour

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/27/2015 - John Richardson Talks FATCA & US Citizenship Taxation Abroad

Special Guest: John Richardson – Lawyer, FATCA & Citizenship Counselling

FINANCIAL REPRESSION, FATCA & US TAXATION

JOHN RICHARDSON, is Canadian based lawyer with a specialized practice of US Taxation abroad for US Citizens. He is the publisher of the web site:citizenship solutions.ca. He tackles the following head-on with “no holds barred”!

You will never view US Taxation the same after listening to this 38 minute podcast.

– How citizenship taxation has made U.S. citizenship a disability in the modern world

– Why renouncing U.S. citizenship is an excellent investment for “U.S. citizens” not living in the U.S.

– How the U.S. “Exit Tax” triggered by renouncing U.S. citizenship operates to confiscate non-U.S. assets outside the U.S.

– How citizenship taxation imposes a “capital tax” on any country that has U.S. citizens resident in it

– How FATCA allows the U.S. to increase its tax based by expanding the definition of citizenship

– How FATCA lowers the international standard of human rights in the world

– How FATCA compliance costs will keep the poor countries poor

– The FATCA Sanction and the “Weaponization of Finance”

– FATCA English and FATCA Forms

– Why the U.S. will always prefer FATCA to GATCA

– FATCA and the future of the dollar as the major world reserve currency

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/26/2015 - Ellen Brown Talks Banking

Special Guest: Ellen Brown – Founder of the Public Banking Institute, Author and Lawyer

Ellen Brown has written to popular books on banking, is the founder of the Public Banking Institute and ran for California State Treasurer in the last election. She knows a thing or two about banking. What she has to say is no pretty.

BANKING IS IN WORSE SHAPE

Loans for small business is harder to get,

Big Banks are lending less,

Big Banks have more derivatives than ever with 98% controlled by the big 4,

Small to Medium size banks are having more difficulties making loans because of Dodd-Frank and Basel III. (Rules which favor big banks).

The rules are effectively competitively disadvantaging the small to medium sized banks in favor of the banks who got us into the financial crisis in the first place and have the lobbyists to secure favorable advantages. It is the smaller to medium sized banks that have traditionally funded small business growth and innovation in America.

STEALTH BAIL-IN VERSUS BAIL-OUT PROVISIONS

In 2010 the congress moved to stop future bailouts but brought in “bailins”. In the future if the big banks fail due to risky loans they will be forced to recapitalize themselves but with unsecured creditor funds. This means using depositor funds who are the largest unsecured creditor class of the banks. The public is generally unaware of this shift.

“Cyprus-style confiscation of depositor funds has been called the “new normal.” Bail-in policies are appearing in multiple countries directing failing TBTF banks to convert the funds of “unsecured creditors” into capital; and those creditors, it turns out, include ordinary depositors. Even “secured” creditors, including state and local governments, may be at risk. Derivatives have “super-priority” status in bankruptcy, and Dodd-Frank precludes further taxpayer bailouts. In a big derivatives bust, there may be no collateral left for the creditors who are next in line.

WHY NEGATIVE NOMINAL BOND YIELDS?

Ellen suggests that the reason we are seeing $5T in Sovereign Bonds now trading with negative nominal yields is because the larger banks need them for collateral in the Repo market. The Fed has reduced the availability of bonds and the banks need the bonds for leverage. They simply don’t mind paying a small price to obtain the lending leverage.

PROFITS IN DERIVATIVES

As Citigroup CEO Chuck Prince so infamously cited prior to the 2008 Financial Crisis, “you have to get up and dance while the music is playing!” Today Ellen believes the pursuit of yields and use of derivatives is about short term profits with little regard to the longer term issues where depositors will be on the financial hook. The banks senior secured debt holders now receiving large interest fees will once again be protected. Shareholders, depositors and those lower on the capital structure will be the losers.

OTHER SUBJECTS

The secretive issues with the stealth TPP (Trans-Pacific Partnership),

Campaign finance, big money and running for public office,

A public bank solutions and the North Dakota model,

Coming Infrastructure spending,

…. and much more in this 32 minute video.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/25/2015 - The War on Cash: Ken Rogoff & Willem Buiter Meet in London

Martin Armstrong is one of the few who have picked up on the “secret meeting” in London between Ken Rogoff of Harvard & Willem Buiter of Citi – they will both be addressing the central banks & advocate the elimination of cash .. “What is concerning me is the silence on this meeting where there are more and more reports about a cashless society would be better. What we better keep one eye open for here at night is this birth of a cashless society coming in much faster than expected. Why the secret meeting? Something does not smell right here.” .. financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

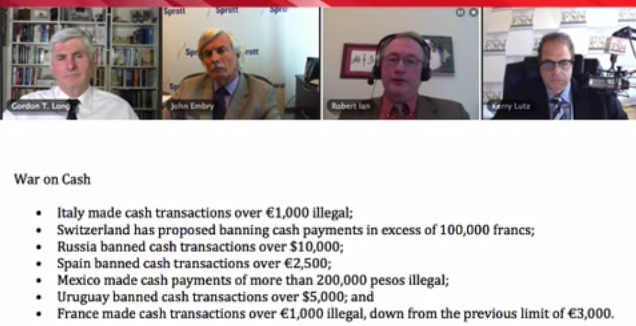

05/24/2015 - Sprott’s John Embry Talks Financial Repression, War on Cash, Gold

Webinar with Sprott’s John Embry (the Special Guest), Conquer Change’s Robert Ian, Financial Survival Network’s Kerry Lutz, and Financial Repression Authority’s Gordon T Long.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/24/2015 - Sprott’s Rick Rule Talks Financial Repression, War on Cash, Gold

Webinar with Sprott’s Rick Rule (the Special Guest), Conquer Change’s Robert Ian, Financial Survival Network’s Kerry Lutz, and Financial Repression Authority’s Gordon T Long.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

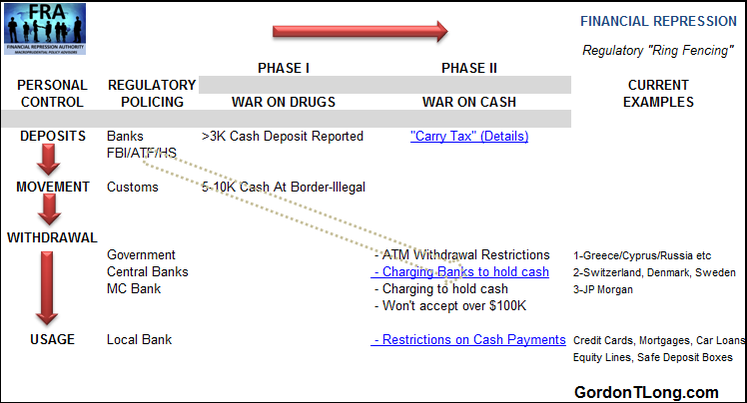

05/23/2015 - Federal Reserve Paper Suggesting a Carry-Tax on Cash

Graham Summers on the war on cash – part of financial repression .. identifies a Federal Reserve paper written back about 15 years ago calling to do away with cash entirely .. the idea proposed was to implement a “carry tax” on physical cash using an expiration date if depositors are not willing to spend the money .. “The idea here is that since it costs relatively little to store physical cash (the cost of buying a safe), the Fed should be permitted to ‘tax’ physical cash to force cash holders to spend it (put it back into the banking system) or invest it .. The way this would work is that the cash would have some kind of magnetic strip that would record the date that it was withdrawn. Whenever the bill was finally deposited in a bank again, the receiving bank would use this data to deduct a certain percentage of the bill’s value as a ‘tax’ for holding it .. The Fed has declared a War on Cash, and a ‘carry tax’ is coming.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/23/2015 - European Bank Bail-ins Coming?

– Euro banks no more stable now than in run-up to financial crisis crash – Banks in France, Spain, Italy are “highly vulnerable to failure” – Low quality bank equity not sufficient to withstand shock – Risk to system “enormously underestimated” – Investor deposits at risk of “bail-ins” – financial repression

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/20/2015 - REGISTER NOW for our Free Webinar with RICK RULE and JOHN EMBRY on The War on Cash, Financial Repression, Solutions to these Risks

FinancialSurvivalNetwork.com and FinancialRepressionAuthority.com present: LIBERTY MASTERMIND LIVE WEBINAR. Join Kerry Lutz, Gordon Long and Robert Ian (ConquerChange.com) as they interview renowned financial and precious metals experts JOHN EMBRY and RICK RULE. Mr. Embry is Chief Portfolio Strategist at Sprott Asset Management and

Mr. Rule is Chairman of Sprott U.S. Holdings. This LIVE event will feature up-to-the-minute analysis of the markets with a discussion of current events/trends including the War on Cash, Financial Repression, Gold and Silver, and YOUR QUESTIONS.

This Webinar is presented by the Liberty Mastermind Symposium and is sponsored by:

FinancialRepressionAuthority.com – Macroprudential Policy Advisors – educating investors globally in understanding the challenges of investment and protection in the unfolding Era of Financial Repression.

FinancialSurvivalNetwork.com – Helping you survive and thrive in the new economy.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/20/2015 - The War on Cash – What You Can Do Now

Mark Nestmann essay focuses on the war on cash, offers helpful suggestions to investors & savers .. Here is Nestmann’s advice: 1. draw down bank reserves & accumulate cash – document the withdrawals to prove the legal origin of the cash in the future 2. make sure you get newly issued bills because more than 95% of circulating bills are tainted with drug residues which under U.S. law allows the cash to be confiscated 3. convert a portion of assets in banks or in cash to gold – store it outside of the banking system 4. keep the assets you maintain in banks which are strong to avoid the coming bail-ins 5. consider putting some assets into electronic-based currencies [like Bitcoin, BitGold etc.]

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/19/2015 - Mark Thornton PhD Talks Financial Repression

Special Guest: Mark Thornton PhD – Senior Fellow Mises Institute

ACCUMULATION OF DEBT

Debt levels are now at critical levels:

Excess accumulation of debt has become a critical burden to the productive capacity of the global economy,

Significant levels of global investment is presently malinvestment,

Excess global capacity has been used to produce none-productive assets,

Lack of Price Discovery and Mispricing of Risk are distorting economies and investment behavior,

Many parts of the economy are fragile and a recssion is now knocking on the door of the US,

…. and more

AUSTRIAN PRESCRIPTION

The Federal Reserve needs to get out of the interest rate markets and allow the markets to work properly,

The Federal Government needs to balance budgets and cut back spending tremendously,

The Government needs to signal to markets particpants that they are not going to see their taxes increased significantly,

The Government needs to demonstrate they are going to do something about the national debt and unfunded liabilities.

These policy positions would begin to incent investment very quickly.

The Central Problem is Unsound Money

FINANCIAL REPRESSION

“A financial scam of the government over the private economy … It is aimed at taking advantage of their citizens, savers and investors.“

Government authorities are:

Printing money,

Issuing enormous amounts of debt,

Suppressing interest rates,

.. all with the intention of exploiting the worker and inflating the value of the goods they buy, as wages fail to keep up. Savers are now receiving negative real rates of returns which is the government extracting resources for themselves at the expense of the common man.

WAGING WAR ON SAVERS

WINNERS: The policies of Financial Repression help:

Banks

Large Corporations,

Government,

Large Borrowers,

LOSERS: The losers are:

Savers,

Consumers,

Producers,

Laborers,

Entrepreneurs

POLICIES: The world wide economy is suffering as a result of the policies which include:

Inflation,

Zero Interest Rates

Quantitative Easing,

Heavy Regulation (Healthcare and Banks)

This is an enormous problem in the modern context.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/05/2015 - Financial Repression Risk: Bank-based Safety Deposit Boxes

06/05/2015 - Financial Repression Risk: Bank-based Safety Deposit Boxes

Gordon Long and Robert Ian (ConquerChange.com) as they interview renowned financial and precious metals experts JOHN EMBRY and RICK RULE. Mr. Embry is Chief Portfolio Strategist at Sprott Asset Management and

Gordon Long and Robert Ian (ConquerChange.com) as they interview renowned financial and precious metals experts JOHN EMBRY and RICK RULE. Mr. Embry is Chief Portfolio Strategist at Sprott Asset Management and