10/04/2017 - Yra Harris: Does A Printing Press “Guarantee” The Balance Sheet Of A Central Bank?

“Over the past 15 months, I have made light of Fed Governor Jerome (Jay) Powell because of his answer to a question I had asked him at a symposium presented by the Chicago Global Initiative. I asked Governor Powell, ‘Who guarantees the balance sheet of the ECB?’ Without hesitating, Powell said, ‘THEY HAVE A PRINTING PRESS.’ If this is his answer to issues of debt overhang I will be closely watching the precious metals if Powell actually became Fed Chairman. Janet Yellen has proven far more competent than Jerome Powell would be under any top of stressful central bank situation .. In my mind Powell would prove to be a new G. William Miller: A weak Fed Chair that was inept in a crisis situation. The current global financial situation is too fraught with danger for Powell’s PRINTING PRESS ..

There was a major article in the Nikkei Asian Review titled, China Sees New World Order With Oil Benchmark Backed By Gold. The article begins: ‘China is expected shortly to launch a crude oil futures contract priced in yuan and convertible into gold in what analysts say could be a game-changer for the industry.’

This has the POTENTIAL to be a great disruptor because China is the world’s largest oil importer. This can have major consequences for the entire global macro world for many reasons. First, the DOLLAR will have an alternative for its status as the benchmark for global commodities. Second, the ability for countries laboring under the threat of U.S. sanctions that are imposed through the SWIFT transfer system can not be avoided by receiving payment in YUAN while being guaranteed by gold. Third, China recently initiated a GOLD CONTRACT settled in YUAN so large OIL EXPORTERS will have the ability to hedge their revenues in a liquid contract further undermining the power of U.S. exterritoriality and quickening the demise of Pax Americana. Fourth, China’s ability to MONETIZE GOLD is a direct assault on the United States’ ability to manipulate the global financial system to its advantage, a remnant of the Bretton Woods Post-World War II global system. The monetization of GOLD really has piqued my interest. It certainly sheds light on the theory that China has been accumulating GOLD. Now, let’s see if they are bi-metalists that can bring SILVER into the equation. XI, what say you?”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/02/2017 - Gordon T Long: The Next Financial Crisis Will Be Global And The Federal Reserve Will Not Be Able To Control It

“That is correct, and it won’t be something that is gradual, it will be very abrupt .. The system will break… and the financial markets will freeze up. When they come out of the other end of that freeze, and it may be a number of weeks because the next crisis will be global and much more complex than 2008. We could control that with the Federal Reserve . . . and this one you cannot do because you cannot get agreement with all those countries. Never mind understanding the complexity .. So, when we come out on the other side . . . there will be a massive revaluation in the U.S. dollar .. They will have to put some stability in the monetary system, and the only way they can do it is having something they cannot print. This is what has gotten us into this problem. We have to get back to sound money.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/01/2017 - The Roundtable Insight – Charles Hugh Smith On Why Wages Are Stagnant In The Developed World

FRA: Hi – Welcome to FRA’s Roundtable Insight. Today we have Charles Hugh Smith. He is America’s philosopher as we have called him in the past. He is the author of 9 books on our economy and society including: A Radically Beneficial World: Automation, Technology and Creating Jobs For All, Resistance, Revolution, Liberation: A Model for Positive Change and The Nearly Free University and the Emerging Economy. His blog, OfTwoMinds.com has logged over 55 million page views and is number 7 on CNBC’s top alternative finance sites. Welcome Charles!

C. H. SMITH: Thank you Richard. I always wonder if I can live up to that glowing introduction.

FRA: You always do. You have great insight as always. I thought maybe today we take a look at a topic you have written a lot about and that is on stagnant wages, particularly in the developed world such as the U.S. and Canada, and what the challenges are behind that…Why it’s happening and if there are any solutions to get out of that trend.

C. H. SMITH: Right – Well it’s an excellent topic. It confuses the conventional economic commentators because as of right now we all know in the developed world, at least in North America, the unemployment is quite low – It’s less than 5 percent which is considered full employment. Normally when we have full employment then employers have to start bidding higher wages and benefits to attract the most productive workers. A rising tide raises all ships and in other words wages tend to rise across the board. When you have full employment and a rising gross domestic product, but we have rising GDP and very low unemployment, according to the statistics, and our wages remain stagnant so something has changed. So I think that is the question that we are going to try to explore.

FRA: And as your writings have indicated that there are a lot of explanations that include automation, globalization, offshoring, the high cost of housing, the climb in corporate competition, the failure of the educational complex to keep pace, a global labour arbitrage as a big factor. What do you make of those explanations?

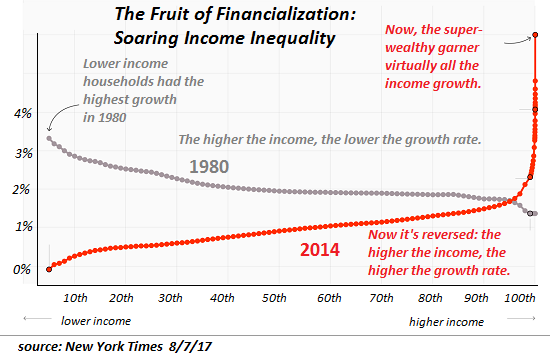

C. H. SMITH: Yeah – I think all elements and part of what we’re proposing here is that there is not just one explanation. If we could just nail it down to one cause then we might be able to change that which policy, but what you’re talking about is these very large structural forces such as globalization and the fact that the economy is changing faster than our higher education systems can change so they are falling behind what employers actually need employees to know. And so these are structural and very difficult to modify or change with just a few policy tweaks here and there. That’s not even mentioning the impact of financialization and financial repression which we all know has kicked into gear in the 21stcentury. That has also changed the distribution of the gains we’ve made from productivity. I have a chart here that the New York Times published in August indicating that virtually all of the income increases over the last few years are now going to the top half of 1%. That’s completely different than it was in the 80’s and 90’s where the distribution of increasing incomes was skewed to the lower end income and middle income sectors. That to me shows the impact of financialization because we know the top 0.5% are generally not people inventing something wonderful, they are not Steve Jobs, they are people that are simply getting nearly free money from central banks then using that cheap money to leverage it into ownership of income streams. They are not creating any income streams they are simply acquiring them with all the evil fruit of financial repression, cheap money, limited liquidity and high leverage.

FRA: For our listeners, Charles has made a collection of charts that provide good insight and we’ll have those charts in the write up of this podcast as well for everybody to look at. If you could go into what is the need for rising wages – the whole system is based on rising wages, could you go a little bit into that and why stagnant wages is a problem?

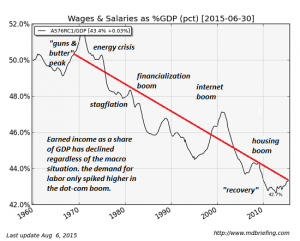

C. H. SMITH: Yeah – That is a critical point because our whole economy, the advanced post-industrial developed economies, they are all consumer economies – They depend on consumers buying goods and services on a permanent basis. So you have to have higher wages in order to support more consumer spending and more consumer borrowing because if we are going to borrow more than we need to make more net income so we can service that higher debt. So stagnant wages throw a monkey wrench into the whole permanent growth and expansion of consumption that our economies are based on. Now we can question that model and say what we really need is a growth model where we are actually getting more happiness and satisfaction with using less resources are earning less income, but that’s a discussion for another day. The economy we have is one that starts falling apart if wages stagnate or decline. I have a chart here of wages and salary as a percent of GDP and it’s quite interesting because it goes back to 1960. It’s basically a measure of how much of the economic activity or output of the economy is going to wages and salaries. What we find is is that it’s dropped quite a bit. In the 70’s, about 50% of all the GDP went to wages and salaries such as working and self-employed people, now it is hovering around 42% or 43%. That is a significant chunk because the GDP currently is about 18 trillion, so if you’re talking about 7% of that then you’re talking about a trillion dollars that used to be directed to wages and salaries and now is going to corporate profit or financier profits and basically financialization. So that’s a big change, but it’s secular, in order words it started in the 1970’s with the stagflation of the 70’s then it continued to climb in the financial boom in the 80’s and the only counter trend was in the Dot-com era, then the percentage of the GDP growth that went to wages and salaries actually increased, but when that boom ended it went back to a decline.

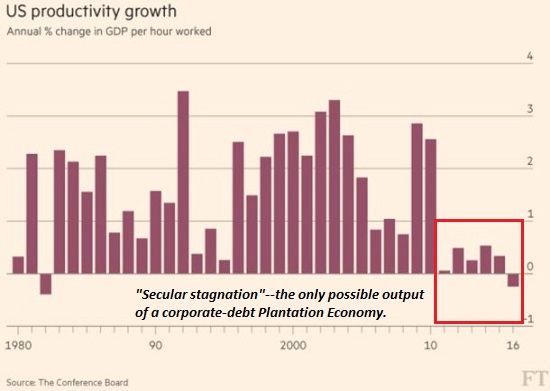

So we have to look for answers that don’t just start 5-10 years ago, we have to look back and say something has been happening for a decade or two. One possibility is productivity, that if we look at productivity growth – I have a chart here that goes back to 1980. Obviously it’s a volatile metric, it goes up and down depending on if the economy is entering a recession or not, but recently even though we’ve had strong growth in the GDP, the productivity has been very anemic and not just for a year or two but since 2010. That’s another change that’s undermining wages and salaries because all real growth comes from increases in productivity.

FRA: Now in some parts the local governments, which have growing budgets tied to increased collection of property taxes due to rises in housing prices, that could also become problematic in a similar way in the public sector if the housing prices stagnate or decline. How are property taxes going to be maintained or increase based on budgets that are factored in for growth?

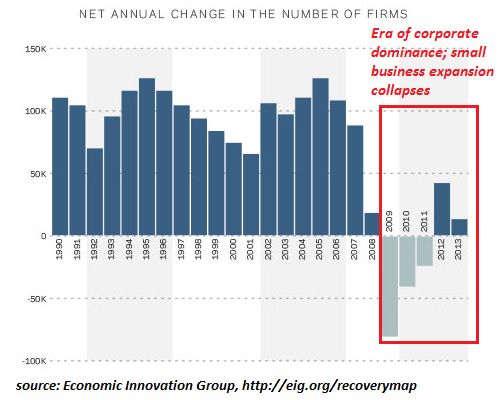

C. H. SMITH: That’s right and an excellent point – And especially for municipalities and states where the majority of the local government income is largely based on property taxes rather than sales or income taxes. And of course if wages stagnate then people have less money to spend so sales taxes stagnate, they have less income so income taxes stagnate and then they can’t afford to move up to more expensive housing if they can’t afford the property tax. I think we can see the local governments around the U.S. are feeling a dwindling, a stagnation of their revenues. Another thing is I have a chart here of the annual change in the number of new firms or in other words how many new companies are emerging and succeeding enough to hire employees and pay taxes and all the good stuff that we expect of new business growth – That has been stagnant or declining since the 2009 global financial crisis as well, compared to the previous decades of very strong growth of new small businesses. That’s another element, it’s becoming more difficult to start a new business and to succeed. That also means that there is less opportunity for wage earners because the fast growing small businesses tend to be the engines of employment because they are growing fast and need talent and are willing to outbid existing corporations for the best talent and so they are a big part of higher wages. That is also causing stagnation in wages and salaries.

FRA: So, if we consider the big reason of financialization as the reason that wages have stagnated and that the economy is optimized for financialization, can we focus on that to explain what is financialization, how does it work, what does it mean to the average consumer and so what’s exactly happening behind financialization?

C. H. SMITH: That’s a great question. It’s a word that has various definitions. My personal definition is that it’s the commodification of everything in the economy into something that can be marketed globally. So for instance, home mortgages in North America, back in the ancient days or 20 year ago banks would originate a mortgage and hold it. It was a very slow, steady, low-risk business with a guaranteed return. Once that financial industry got financialized then the mortgages were packaged into financial instruments that can then be marketed globally as investments and then they could be sold as AAA-rated instruments to credulous investors and huge profits could be spun off of this. So that’s an example of how financialization works, is that it’s basically taking what was once a low risk industry and hyperfinancialzing it so it could be sold off and traded for immense profits. The high risk that is generated from that is then passed onto other people. The role of central banks in financialization is that the cheaper you make money, the more speculation that you enable. For example in the housing bubble of 2007-2008, that speculation was fueled on both ends of the spectrum. You had small-time players getting liar loans, which were of course enabled by central bank liquidity. And then you’ve got financiers that were selling F-rated financial instruments as AAA-rated. Nowadays, because of the credit-tightening and the regulations that were finally imposed on the banking sector, the small fry doesn’t really have the same access to liar loans and easy money, and so now it’s congregated up in the very top of the wealth power pyramid that if you’re a financier or a corporation, then you have almost unlimited access to cheap money. You can sell bonds at low rates or borrow money from a money centre bank at rates that no normal employee can possibly match. So the corporations can do thing that would not have been possible without financial repression because if they had to pay 7% or 8% to borrow the money, then it would no longer make sense to buyback so many millions of shares of their company in order to boost their wealth and capital gains. So it’s the cost of money and the availability of money to the apex of the wealth power pyramid and that’s why the chart from the New York Times shows that the vast majority of income gains over the 21thcentury are congregated over that very small part of the population that has access to unlimited liquidity at very low interest rates and then they can buy the income streams and outbid everybody else. I think that is one of the devastating impacts of financial repression, that the benefits are not evenly distributed. If you and I could go borrow a billion dollars at 1%, we could do some amazing things because all I would need to do is buy bonds that pay 3% and I would be skimming 2% for nothing. I would be earning 40 million dollars a year simply because I have access to cheap money. That is one of my favourite examples of how financialization works.

FRA: And you’ve got a great quote from one of your blog writings earlier this month saying, “Financialization funnels the economy’s rewards to those with access to opaque financial processes and information flows, cheap central bank credit and private banking leverage.” Those aspects cover what a lot of what financial repression is about such as cheap central bank credit – The whole money printing and quantitative easing aspects of central bank activities.

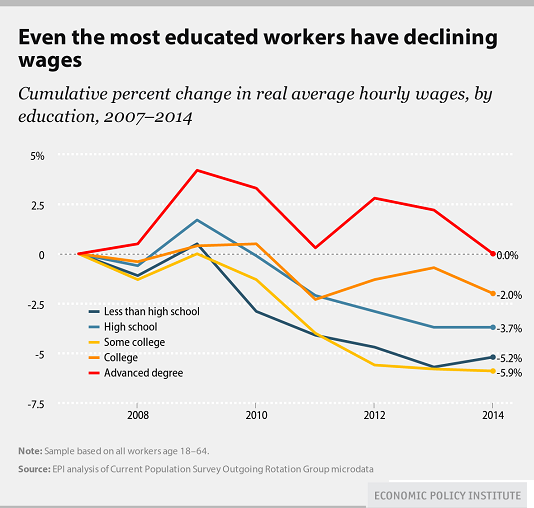

C. H. SMITH: Right – And the fact that for the 99.95% of us, we can borrow money to do something specific, modest and limited such as buying a house or getting a small business loan if we jump through a lot of hoops, but we can’t go borrow money with the size and leverage that the big players can – That’s why they’re scooping all the income gains. If we look at the chart here of declining wages for all layers of the educational accomplishment, in other words even the workers with advanced degrees, their wages are stagnating too while those with less education may actually be declining once you adjust for inflation. This is quite amazing that even the highest educated workers are no longer making gains. That shows how pervasive the damage is with financial repression.

FRA: That is an interesting chart. And if we can now ask what is the way out of this – Are there any solutions? Could a repeat of the dot-com bubble, where there was a break in the trend, be repeated through the revolutions we have going on like in blockchain, bio-tech, energy & environment, robotics. There are a whole bunch of revolutions that are happening in different industries. Could any one of those or perhaps collectively altogether duplicate a dot-com effect?

C. H. SMITH: That’s a great question and I think the more we learn about each of these scientific and technological revolutions, the more potential we see. Just as a beginning comment: there is a lot of media coverage of the replacement of human-beings such as the self-driving driving vehicles which are going to get rid of millions of drivers, that is definitely a real possibility, but we have to also make mention of something that is less sexy which is that a lot of technology tends to augment human labour. For instance, an industrial robot on a factory floor, it doesn’t just do it’s thing with no human interaction for months on end, years on end. More and more you need to change your product line very quickly and modify your production and so you actually need skilled humans to reprogram the robot. There is a lot of this kind of technology where the tool increases human productivity, but humans are definitely still the key part of the whole chain of production. So I think there is a definite possibility for higher wages which would basically mean the higher productivity that’s flowing from technological advances would go to those doing the work as opposed to those who own the income streams. But I have to say we are going to have to find some way to limit the predation of financialization in order to press those gains down the wealth power pyramid to those who are actually doing the work and creating the advances. That’s going to require certainly a political change that puts limits on financialization so there is more of the nation’s income left to be shared with the workers.

FRA: Could all of these trends have deflationary effect on the economy in terms of the need to sell assets for generating enough income to service debt and to pay ordinary everyday expenses? Do you see that potential in terms of deflationary effects on the economy in general?

C. H. SMITH: That’s a great question because it calls to my mind Japan, which as we know has been sort of in a deflationary cycle for roughly 25 years. When we look at Japan there are many aspects we can comment on and it’s stagnating too in terms of it’s wage structure and it’s growth. But one thing we might posit is that Japan’s export industry, it’s most productive sectors like automotive and various technology sectors, their productivity is increasing enough that Japan’s national economy has been able to stumble forward in a very low growth and stagnate way, but the very high productivity of the industrious sectors of Japan how allowed that to be modified. In other words, without those high productivity industries, then Japan would be in a real perhaps deathbell of deflationary dynamics. My point here is that if you have these very productive revolutionary technologies, they may be a small sector of the overall economy in terms of a percentage of economic activity, but in terms of the gross and productivity that they create, they have an outsized impact. So we might see something like that and we may be already be seeing something like that in the U.S. where the sectors that are growing fast and creating a lot of value are keeping the U.S. economy from entering a deflationary cycle. And because we know one cause of deflation is technology lowers costs and so things get faster, better, cheaper, or at least that’s the idea. That’s not a very complete answer to your question, which I think is a good one, but my point being is that technological revolutions can lower the cost of goods and services which is deflationary, but their productivity gains can increase the GDP which tends to counter that deflationary impact – In other words the whole economy can be growing even as prices decline.

FRA: That’s interesting and great insight – How can our listeners learn more about your work, Charles?

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/01/2017 - The Roundtable Insight – Casey Research’s Nick Giambruno On The War On Cash, The Future Of Cryptocurrencies, And Investing As The U.S. Pension Crisis Unfolds

FRA: Hi – Welcome to FRA’s Roundtable Insight. Today we have Nick Giambruno. Nick is Doug Casey’s globetrotting companion and is the Senior Editor of Casey Research’s International Man. He writes about economics, offshore banking, second passports, surviving a financial collapse, foreign trusts and companies, geopolitics, and value investing in crisis markets, among other topics. He is also the Senior Analyst of the Crisis Investing publication. He’s lived in Europe and worked in the Middle East, including Beirut and Dubai, where he covered regional banks and other companies for an investment house. Nick is a CFA charterholder and holds a bachelor’s degree in finance, summa cum laude. Nick is a frequent speaker at investment conferences around the world. Welcome, Nick!

NICK GIAMBRUNO: Great to be back with you Richard.

FRA: I thought today we would focus on a number of interesting topics that are in the news and public highlight including what’s happening with the pension crisis in the U.S. and the war on cash with the overall theme of central banks intervening in the economy and in the financial markets. Maybe we could begin with your thoughts on the war on cash. Where do you see that trending? Do you see governments getting involved with cryptocurrencies to move away from cash?

NICK GIAMBRUNO: Well, let’s start by looking at the war on cash. And not to mince words, the war on cash is evil – It’s all about restricting peoples’ choices and forcing them into digital systems that can track, monitor and control every penny you earn, save, borrow and spend. It’s really a totalitarian-type control system and there really is no redeeming values of it whatsoever in terms of benefits that are worth the trade-off of basically looking your absolute financial privacy. So first thing is first – It’s just an awful thing, but nonetheless it is a growing trend. It’s not naturally popular in academia and with governments because it’s all about transferring governments more power and control over people. That is uniformly a bad thing, but nonetheless, it is a growing trend not just in the United States, but around the world. Your listeners might remember back decades ago in the United States there used to be $500 bills, $1,000 bills, and even a $10,000 bill. Those have all been gotten rid of, I think, in the 1960’s and 1970’s with the usual excuse of, it’s only being used by drug dealers, terrorists, money launderers and that sort of thing. So, the largest bill we have since then is the $100 bill and the purchasing power of the $100 bill has gone down drastically since the 1960’s and 1970’s. Inflation is an important component on the war on cash because if the governments don’t issue larger denominations of bills to keep up with inflation, it has the de facto effect of forcing more people to use cards and digital payments than they otherwise would because it’s just not convenient to use cash since the largest valued bill has been inflated away. And I see the same sort of demonization that the governments, the media, and their academic cohorts have used in other areas such as the very large denominations of U.S. dollar bills back in the 1960’s and 1970’s. I see the same language used by the same type of people towards private cryptocurrencies and that is a scary thing because it shows that they are gunning for this. It is important to distinguish between a private cryptocurrency and a cryptocurrency which is controlled by the government. In my opinion, I think it’s a wonderful thing to have these private currencies because the ultimate power and control these systems is not with the state or any government – It is distributed and decentralized. That’s why we see governments talking about how it is only used by terrorists, drug dealers, and money launderers. That why we see people who are intimately involved in the current system, banking and central banking system, which is as you are fully aware a fraudulent system, like Jamie Diamond coming out and saying Bitcoin is a fraud, these are signs that they are gearing up towards an assault on this. And we can go into the reasons why, but I think it’s going to be extremely difficult for them to crackdown on these private blockchain and cryptocurrencies, I think the cat’s out of the bag on this. But nonetheless, all of these issues are intertwined.

FRA: Do you think that governments will allow the private-based cryptocurrencies to coexist? I know you said the cat’s out of the bag and they are uncontrolled, but maybe in the future if governments try to control or regulate then do you see the possibly or allowance by the governments for private-based cryptocurrencies?

NICK GIAMBRUNO: Honestly, I don’t think that they have a choice. They can try to control it and regulate it, but I don’t think that they are going to have much more success than say Venezuela does in trying to control currencies that they don’t like which would be the U.S. dollar and other currencies. So, I think the U.S. government is not going to have a whole heck of a lot more success than say Venezuela does or any government does in regulating currencies that they don’t like their people to use, which in itself is a terrible thing. Why should some bureaucrat tell you what kind of currency you would want to use voluntarily? It’s really a terrible thing. Also another thing to point to, a similar technology, is BitTorrent. Now BitTorrent is a decentralized file-sharing technology that allows people to share any kind of file they want whether it’s a Hollywood movie that just came out in theatres, an E-book or anything, you can share anything. Anyways, this technology has been around for over 15 years and despite the U.S. government’s best efforts to shut down BitTorrent, it’s’ still decentralized. It’s like a game of Whack-A-Mole and despite their best efforts it is still easily accessible to anybody on the internet. Bitcoin is similarly decentralized and maybe even more decentralized. So sure, they can say that Bitcoin is illegal and you cannot convert your dollars into Bitcoin. It will just shut down these exchanges, but it’s not like Bitcoin is going to die or that it’s going to be impossible for you to get Bitcoin – It might be a little harder. I think it’s basically impossible for the U.S. government, Chinese government or any government to totally eliminate these private cryptocurrencies other than shutting off the internet and keeping it shutoff, quite frankly.

FRA: Great points. On central banks – Do you see central banks as being favourable to a war on cash to make it easier for bank bail-ins for central banks to implement their policy, for example, negative interest rate policies and those types of things?

NICK GIAMBRUNO: Certainly – The central banks are all on board and on the same wavelength of the folks who are advocating for the abolition of cash. So, the central banks are fully on board for this and I think one of the main reasons for the war on cash is because central banks want to use negative interest rates, which is a bizarre thing in the first place when you actually think about it, it’s like getting paid to borrow money – It makes absolutely no sense. And it wouldn’t happen in a free market. Negative interest rates basically couldn’t exist in a free market. They only can exist in a manipulated and controlled market such as the system that we have with central banks and fiat money. But the thing is, they want to implement negative interest rates because of their wrongheaded belief that instead of losing money from the sting of negative interest rates, people will think: We better go out and spend it quickly before we lose money from it. And that it will somehow stimulate the economy. It is completely wrongheaded in the sense that it will encourage people to save more money because it will be harder for people to save money to spend on their basic necessities. That’s not going to spur people to spend more, it’s going to spur people to save more because they are going to have less money available to spend on rent, food and so forth. It’s not going to make them go out and buy the iPhone 8 or the next ridiculous fad as they would like them to. Anyways, the whole point of the war on cash is to force people into the banking system because cash represents an escape hatch for people who want to avoid negative interest rates. It’s no coincidence that in countries that have the worst cases of negative interest rates, you see people saving more in cash. Look at Japan. Japan has had record sales of safes that people would install in their house to store cash because Japan has negative interest rates and people don’t want to lose money from negative interest rates. So, it’s a completely wrongheaded and destructive policy, again, that has no redeeming values whatsoever that could not exist in a free market where there are voluntary interactions between buyers and sellers – It can only happen via coercion in a government controlled financial system.

FRA: Do you consider cryptocurrencies to be a store of value or investments? Will Bitcoin, for example, retain its current valuation or will it come down a little bit towards what the cost to produce a Bitcoin in terms of electricity and computers, I think it’s around $1,000 now. What are your thoughts on that?

NICK GIAMBRUNO: Yes – I think the real value of cryptocurrencies, in my opinion, have yet to be established that these are reliable stores of value for anything other than the very, very short term. Nonetheless, they are extremely valuable as transfer mechanisms to move a value from point A to point B instantly. You don’t have to keep it in the cryptocurrency, you can convert it into other things such as goods, services, fiat money, gold or whatever you want. In terms of moving it from point A to point B, I think they have a tremendous amount of value, but as a store of value I think it’s going to take some time to establish that. Personally I favour gold and silver as long-term stores of value. But with the cryptocurrencies which is really, really interesting is that you don’t need anybody’s permission to send money to anybody anywhere in the world and it doesn’t need to be backlogged by the bank and have the compliance department check it out to make sure it’s fine, it doesn’t need the approval of SWIFT, it doesn’t need the approval of the U.S. government. You can simply send cryptocurrencies to anyone in the world and there’s pretty much nothing anyone can do about it and that’s a really wonderful thing.

FRA: Great points. Going on that theme of movement internationally of capital – What are your thoughts on globalism? You’ve written a lot about that and the end of globalism on the economy. Will that lead to protectionism or more local freebased markets?

NICK GIAMBRUNO: Well, I think the jury is still out on that, but I think it’s important to also define our terms because these terms are thrown around a lot and I think it’s important that we have a common definition of these terms so we know what we’re talking about. Globalism, in my view, is simply the centralization of power on a global basis, that’s it. That’s all it means. You look at the people who advocate for these things in centralized global power structures, that is globalism. Now whether globalism has reached it’s venus and is now declining – I think there’s a good chance it is. The European Union is a perfect example of globalism because it’s centralization of power of all these nation states into one global, one giant, super-national institution. So, we are talking all about the centralization of power. And it’s interesting because cryptocurrencies tend to go in the opposite direction – They tend to be centralized power and I am 100% for decentralization. Decentralization is always a good thing and centralization is, generally, always a bad thing. What we’re looking at here is what is going to happen if and when globalism and the ideology behind globalism, which is universally ascribed to by the elites in the academic, the political, the financial, the media elites in the U.S. and the greater Western world. In my view, it is a bankrupt philosophy and I think it’s sort of akin to Communism in terms of, this is a bankrupt ideology that is going to be relegated to the dustbin of history sooner or later. So, what is going to replace that? I think that is an open question. Are we going to move towards a more decentralized, voluntary society? I would like that to happen. Or are we going to move towards nationalism and protectionism which is just replacing centralization of power on a global basis for more of this tribalism and nationalistic feeling which isn’t necessarily a good thing either. So, I think the jury is still out on that whether we are going to move towards a more nationalistic, protectionist type of a world or we’re going to move towards a more voluntary decentralized type of world – I think the jury is still out on that.

FRA: You’ve written a lot recently on the U.S. pension crisis. John Mauldin has pointed out that he thinks the bubble in government promises is arguably the biggest bubble in human history. He gives an estimate of 2 trillion, but says that that’s based on an average 7% compound return, of 2 trillion of unfunded liabilities for state and local governments on the pension crisis. But, assuming the market could go down 40%, then you have unfunded liability in the range of 7-8 trillion so it’s enormous. What are your thoughts on the U.S. pension crisis?

NICK GIAMBRUNO: This is a perfect example of the extreme corruption in the U.S. and the extreme corruption in government and financial markets. It’s a total mess and quite frankly the pension crisis is an unsolvable problem. There’s nothing that can be done to solve this problem – It’s simply too big. The issue at hand here is that the government, these local governments: municipalities and state governments, all over the place, they are making extravagant promises on retirement benefits that they simply can’t deliver on that gets them the support of their government employees, unions, police officer unions, teachers unions and these kinds of things. But they’re really promising these people, their own employees, benefits that they can’t deliver on. What’s interesting is that pensions are pretty nice benefits. I mean think about, you basically get or pretty close to get your last year’s salary adjusted for inflation until you die and that’s a pretty nice benefit. Pensions don’t really exist in the private market anymore. About only 4% of private U.S. companies offer pensions anymore just because it’s not possible for them to do, but for a government they can promise these extravagant things. Another thing is is the accounting method of pensions. Governments get to use different accounting standards than private pensions do. And the single most important number in the whole pension crisis is the assumed rate of return on the assets of the pension because that assumed rate of return is used to discount the future liabilities of the pension. If they use an artificially high assumed rate of return, their liabilities are magically shrunk. These pensions are assuming that they’re going to earn a better return in the stock market than Warren Buffet into perpetuity which is ridiculous. They’re not using anything towards realistic assumptions in their accounting – They are using Bernie Madoff accounting; it’s a fraud. If they were in the private sector they would be going to jail for fraud, but nonetheless they are in the government sector and, magically, what is fraud in the private sector becomes acceptable in the public sector, which is totally unreasonable. Be that as it may, what they’ve done is they’ve promised these extravagant retirement benefits to their employees and now we’re really close to the tipping point because these pensions plans are basically bankrupt and that’s at a time of a stock market bubble and a bond market bubble of historic proportions. That should pump up the value of these and it has pumped up the value of these pension plans, but nonetheless they are still paying out all this money in benefits that even with an enormous stock and bond market bubble these things are still insolvent. And even with using unrealistic return to discount the future liability – They’re still insolvent. So, the next time the market has any sort of minor recession or downtown a lot of these pension plans are going to go bust. What does that mean? That means the taxpayers and the states are going to be on the hook to pay for these extravagant benefits. People in the private sector don’t get to use benefits, so they are extravagant benefits. How are they going to pay for them when the whole thing has gone bust? Well, they’re going to increase taxes and what taxes are they going to increase first? – Property taxes. We’ve seen this in Illinois. Recently property taxes are going through the roof in Illinois. Illinois is hardly the only place that has a pension problem, many many jurisdictions do. If your town or your state or your municipality or your city has a pension problem, the likelihood of your property taxes doubling, tripling or even going higher is very likely. It’s not just in the U.S., any jurisdiction that gets into financial problems always turns to higher taxes and property taxes. Greece is a perfect example. I think Greece’s property taxes have gone up 4 or 5-fold in recent years as they’ve looked to squeeze people for any penny they can get out of it. So, really to me this is an illustrative example of just how rotten the political system is, how rotten the financial system is and it’s all wrapped up into one nice crisis. This thing is going to come to a head sooner than later, certainly within the next cyclical recession which we are way overdue for in the U.S.

FRA: And the same thing here in Ontario, up in Canada. The debt per capita is multiple times worse than in Greece so it’s only a matter of time. We already see the property taxes going up and use fees, for example, licenses across the board going up here and there.

NICK GIAMBRUNO: Yeah – It’s frustrating. And really I think we should take a step back to think about property taxes and property rights because how can you say that you own something and that you are the owner of a piece of property and that you have to pay a never-ending and ever-increasing annual fee on? – It’s ridiculous. Think if you had to pay property taxes on your sofa or your T.V. Could you really say you owned your sofa or your T.V. or are you merely renting it from whoever was charging you that fee? I think it’s the same thing and I think property taxes are a terrible thing and hopefully, I’m not holding my breath, but hopefully they’re done away with at some point in the future, but unlikely, they are probably going up.

FRA: And also, you’ve written on the pension crisis where you’ve suggested two asset classes that investors could consider: gold related and cannabis related investments. Can you elaborate on that rationale?

NICK GIAMBRUNO: Sure, okay. Let’s start with gold. I think the pension crisis is going to be terrific for gold because as I mentioned, this is an unsolvable problem in the traditional sense. These state and local government could double, triple, even quadruple taxes and it’s not even going to make a dent in this problem and that’s assuming that the tax revenue they receive after increasing taxes, the collection rate, would stay the same – It wouldn’t though because higher taxes are going to drive people away from these states. We’ve seen this already in Illinois and Chicago in particular. I think 3,000 millionaires have left Chicago because of higher taxes in recent months and there was a study done that this was like one of the single-most outflows of wealthy people in the entire world, not just in the U.S., not just in North America, in the entire world. So, I think you have to take a step back when you see all of these productive people, these wealthy people fleeing the city that there is an issue here. Certainly there is a point of diminishing return that comes with raising taxes that has already been reached in a lot of these places so they can’t raise taxes and they can’t cut benefits either because a lot of these benefits are enshrined in the state constitutions that they can’t cut these pension benefits. Isn’t that a nice thing? You’ve got the government who says they basically guarantee these benefits and it’s against the state constitution to renegotiate or lower these benefits so it’s already bankrupting these places causing local debt crisis. They are going to default on these obligations one way or another. But ultimately, what’s going to happen is that the federal government is not going to just sit back and let all of these states and cities not make good on their promises to their own employees. It’s just politically going to be impossible for the U.S. federal government to step back and do nothing. That’s the whole point of having the central bank. They are the “lender of last resort”, which really sanitizing what they really do. They print money and give it to people so they basically socialize the cost of these things through money printing and higher prices and inflation. So, that’s what is going to ultimately happen, is that the federal government and the federal reserve is going to step in and paper over this pension crisis by printing money. That’s the bottom line of what is going to happen eventually with this pension crisis and that’s going to be good for gold. So that’s the rationale behind gold because simply, there is no other way to solve the pension crisis besides the printing press. That’s what ultimately is going to happen. Number two, the states are so desperate for any penny they can get. They are going to start to look for alternative means of revenue and I think they are going to look at the states who have recently legalized cannabis and they’re going to find the opportunity too good to pass up. There’s 100’s of millions of dollars being flowed in with new tax revenue from the legalization of cannabis in various states such as Colorado. I think it’s estimated that next year when California goes live with legal recreational cannabis, that they could bring in about a billion dollars in cannabis-related tax revenues. Nonetheless, this is not going to solve the pension crisis. A couple billion here, a couple billion there – It’s not going to solve a multi-trillion dollar issue. And I know that you cited earlier that it was a 2 trillion dollar problem, but that’s using the unrealistically rosy rate of return assumption of a 7% which is what most public pensions use. If you use a realistic discount rate, we’re looking at 5 trillion plus problem. So, a couple of billion here, a couple of billion there from legalizing cannabis is not going to solve this problem, but nonetheless because these states are so desperate it’s not going to hurt. They are going to look to get every penny they can get and cannabis is going to be a beneficiary of their desperation. That’s the rationale for the second investment.

FRA: Very interesting. In addition to cannabis, what controls: monetary policies, fiscal policies, government regulations do you see coming in the near future that governments and central banks will employ to deal with the increasing burden of government debt and unsustainable spending and deficits?

NICK GIAMBRUNO: Well, I think we talked about those a little bit earlier. I think we’re definitely going to be seeing negative interest rates spread because negative interest rates, of course, benefits the borrower and who are the biggest borrowers in the world? – Our governments and they’re the largest borrowers, the U.S. government in particular. I think we already have negative interest rates in the United States, not negative nominal interest rates, but certainly negative real interest rates when you consider the nominal interest rate and the rate of inflation. Sure, they give you this phony CPI number of like 1-point-something percent, – It’s much larger than that. Everybody knows that. Just go to a grocery store and look at how much groceries cost, your medical insurance, your tuition, anything, the prices are going up more than 2%. It’s an insult to peoples’ intelligence that that’s the number that they use. Anyway, I think there already are negative real interest rates in the United States. The little measly couple of basis points you get for putting your money in a bank – that doesn’t keep up with inflation. So there already are negative real interest rates in the United States. I think they’re going to get more negative either with higher inflation or lower nominal rates. I think that’s baked into the cake because that’s going to support the U.S.’s ability to manage that debt. Lower interest rates makes it easier to manage that debt and that debt is going nowhere. I mean there is nowhere but north for where the U.S. debt is going. It’s politically impossible. I think it’s a pretty safe assumption is that we’re going to continue to see that. If we’re going to see more and more negative interest rates that means they’re going to need to ramp up the war on cash because negative interest rates really aren’t effective unless you trap peoples’ money in the banking system. Well you can’t really trap peoples’ money in the banking system if you give them the option of having a bunch of cash stashed under their mattress. So, I think we’re going to see negative interest rates ramped up and that necessarily means we’re going to see the war on cash ramped up. And we already are seeing this. I think the head of the Harvard business school or Economics department, Kenneth Rogoff, he’s a huge advocate for the war on cash. And he’s a trendsetter, obviously being a top academic at a top institution, he kind of sets the trends on this stuff and I wonder what motivates this guy because I don’t think he’s stupid, I think he knows what he is doing. He is like the kind of person who wakes up in the morning and looks for ways to try and restrict peoples’ abilities to use cash and I think he’s clearly a sociopath. Unfortunately, this kind of wrongheaded thinking is gaining current so I think we’ll see more of that.

FRA: As the last question here, do you see any political movements within the U.S. to extreme socialism as a backlash, perhaps led by the millennial generation, that could severely affect the economy or the financial markets?

NICK GIAMBRUNO: I think that’s very likely. For better or for worse, probably for worse, these people are the future generation in the U.S. and who is one of the people that they idolize? – Bernie Sanders. And there is a really interesting article that Bernie Sanders wrote about how Venezuela is the success story of socialism. Obviously this was written a few years ago before their hyperinflation and major problems they have right now, so I encourage your listeners to check that out. Bernie Sanders basically wrote a glowing review of Venezuela and said, “Hey, we gotta bring this to the U.S.”. Well, Bernie Sanders represents the economic views of these people so, yes, I think we are going to see a lot more of socialism, collectivism and all the stuff that entails in the future, unfortunately.

FRA: Great. How can our listeners learn more about your work, Nick?

NICK GIAMBRUNO: The easiest place to do that is on the International Man website. That is: InternationalMan.com. We talk about all of these issues and more importantly how you can protect yourself and your family from these terrible things that we’ve been talking about today. The situation is not hopeless. There are things you can do to not only protect yourself, but profit from the distortions that will inevitably be caused by all of these wrongheaded policies.

FRA: Great. Thank you very much for all the great points and insight, Nick – Thank you.

NICK GIAMBRUNO: Thank you Richard – Great to be with you.

Transcript by: Daniel Valentin <daniel.valentin@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/29/2017 - The Roundtable Insight: Yra Harris and John Browne On The End Game For Europe, The Euro And The ECB

FRA: Hi, welcome to FRA’s Roundtable Insight .. Today we have Yra Harris and John Browne. Yra is an independent Floor Trader, successful hedge fund manager, a global macro consultant trading foreign currencies, bonds, commodities, and equities for over 40 years. He was the CME Director from 1997-2003. And John is the Senior Market Strategist for Euro Pacific Capital, he’s a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee as Chairman of the Conservative Small Business Committee. And also as a Principal Advisor to the British government on issues relating to geopolitical matters. He’s worked for Morgan Stanley as an investment banker and he’s also worked for other firms, Barclays Bank and Citigroup. Welcome, gentlemen.

Yra Harris: Thank you, Richard.

John Browne: Thank you, thanks for having me.

FRA: So today I thought we’d discuss the implications of the recent elections in Germany on the EMU, the Euro, ECB policies, financial markets, and the European economy. Your thoughts? I guess we can start with Yra, what you think happened and what are the implications?

Yra Harris: Well you know Richard, we’ve talked about this and you know I’ve written quite a bit about it over longer than I care to think about, but the results were to me a phenomenal loss for Merkel because she not only slipped from the vote totals but it was a very big slap in her face. And like in the Brexit vote, they want to sell it as anti-immigration and I think it’s so much bigger than that. I think this part of the vote .. and if we go back to when the AfD first began, I think in 2013 when it was founded by various economists, the issue is far more financial than anything else. Yeah, the AfD attracted some fringed wackos as we might call them, but most importantly, the Free-Democrats resurrected themselves. I think this is a pretty big statement as to how Germany will face what Macron has been trying to push down, I would say Macron and Draghi have been trying to push down the throats of German taxpayers but of course, it never had the okay from German voters. So, I think that this has a long way to play out, it was a very important vote .. the biggest winner from here may be Theresa May. But we’ll leave that for further discussion.

FRA: And John, your thoughts?

John Browne: Well, I’m very interested by what Yra said because I think you’re absolutely right. Theresa May may be the biggest winner of this because Merkel is very pro-German industry and that points towards a mutually favourable Brexit from Germany at least. And Germany really runs the European Union, although it’s meant to be everybody, but basically Germany runs the whole show. And that’s a very important thing that Yra mentioned. I agree with Yra that Merkel had a big loss, she was elected as forecasted but there was nobody else, she’s weakened significantly. I mean the interesting thing was that combination, again getting back to what Yra said, it wasn’t all immigration. It was partly to do with the financial environment. The Alternative für Deutschland, the Alternative for Germany, went from 0 seats to 88 and the Freedom Democratic Party went from 0 to 69 seats. 132 seats against Merkel’s 217, so it’s a big block in there. And it’s going to sober a lot of the left wing in Germany, the Greens lost and the Left both lost seats. And so, I think that’s very interesting in my view and I agree with what Yra said. I think its going to boost the thing for Brexit because Merkel is going to be favourable to a good deal with German business. As far as the ECB is concerned, I think there’s going to be continued press for EMU, the European Monetary Union. The Euro has faired fatally basically because it doesn’t have a unified economy and so, each threat to the Euro is going to be used by the European elite to force closer and closer fiscal unity on the way to becoming a superstate. And talk about undemocratic, I mean I’d call it the Euro Soviet. So, a good reason is they say they offer a parliament, which is duly elected and I think quite fair with proportional representation, but of course they give that parliament no power, just as happened in the Soviet Union. And the other thing is they’re already talking now immediately of giving huge amounts of money for electoral reasons rather then taking money away from the politicians to be elected, making it less of a money game, they’re going to give much more. But only to parties that fully support the European ideal, the parties that go against it will have no funding. So, it’s becoming less and less democratic and right down the road of what I think justly called the Euro Soviet. And I think regarding the Euro, it’ll be used as a weapon to increase togetherness and of course a superstate. As regards commodities and things, what we’re living with masses of money, masses of credit and liquidity that’s falling value, bonds are going up because of zero interest rate policy and quantitative easing. And equities have risen on this thing, hugely, record highs in both bonds and equities all over the world. But of course, that is all organized by the swamp. If the swamp starts to get eroded, then the reverse is going to happen. Bonds are going to be probably the biggest bear trap in history, equities are going to be a problem and of course commodities and precious metals will rise, certainly in dollar price and also in value. And so, I think the whole thing depends on how effective it is to get rid of the swamp. Realizing both parties in Britain and America that have ruined the countries in the last hundred years. If you take an actual number of it, in 2014 in January when the Fed opened its doors, that dollar today, it would be only worth, it other words two cents of that dollar would buy a present dollar. The Fed has devalued the dollar by over 98% and in those days, there were 8 Dollars to the Pound, and now there’s 121 .. And this has been done by the swamp which is both parties and the question is, how long will it take for reality to dawn? Whether they can put it off with another type of QE, giving people money, not even QE but just giving us all a cheque like the Republicans did under Bush. But a massive cheque, like $10,000 a piece or that sort of thing, to fend off that awful day that reality may dawn.

FRA: Your thoughts, Yra on this and the possibility of fiscal integration in the EMU?

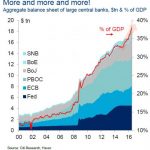

Yra Harris: Well, it’s like John and I have been talking our whole lives. But he uses this term the European Soviet, and you know Richard I’ve talked about it quite a bit so John, I don’t know if you know Bernard Connolly but he’s a very dear friend of mine. So, when I hear you throw that out it reminds me of his great book, The Rotten Heart of Europe. But I’m going to answer your question Richard, this is all about the fiscal harmonization, this has been the program pushed by the likes of George Soros and what I call the Davos crowd and I don’t mean that as a conspiratorial, that’s just what they’ve been pushing. And now Mario Draghi has a very serious problem. And the speech yesterday was horrendous and stupid, he should have cancelled that press conference that he had scheduled before the German election because its just not going to happen that fast. And it puts Draghi now as I would say the only game in town. Which is why these people or those people including Peter Boockvar and I, have gone back and forth on this. There will be no quantitative tightening yet from the ECB because Draghi is now going to be in a bigger hurry to keep piling on sovereign debt onto the balance sheet of the ECB because only through that effort can he synthetically create the Eurobond that they’re craving for. So keep loading it on, keep loading it on, and then they’re going to the Germans and go “well you can’t possibly not be the guarantor of this bond, you have to. We have all this debt piled on the ECB, you’re going to have to be the one who has to guarantee this.” Otherwise we go into a massive debt default and the world goes into a major Depression. That’s what’s happening and this is all being done by Mario Draghi and if Mario Draghi hears this broadcast and he wants to go head to head with me and argue this, I relish the day.

John Browne: Well I totally agree with Yra. And it’s interesting, I was an investment banker in London and we were asked to be managers of a Eurobond issue. Not a Euro like the currency, but European Bond Issue .. everyone wanted to do it in Europe except for Germany .. Germany said, “we’ve got terrific concerns about inflation from the Weimar we will never forget it, and we certainly are not putting the German signature to a European bond.” And I personally despite all the talk and the movements that are taking place, believe that is at heart in the average German. I mean what Germany has done since the Weimar is to say “Okay, you German women and men work hard, save your money, and we as the government will ensure that saved money is still worth the same as when you put it in. Unlike the Anglo – American governments that have stolen from every saver.” And so, I think Germany, now that Merkel is weakened severely by most interestingly right-wing parties effectively. Both financial and immigration wise, I think she’s going to be under bigger and bigger pressure not to put the German signature to that Eurobond. And I think that’s been pushed back and this is of course is a big problem for Draghi whose been depending on it and it’s going to become a tremendous issue. Germany, as Yra said, is going to be faced with collapse on the one hand if they don’t sign, but a collapse of support politically if they do sign. And I personally think Germany would stand in the long run to win by not signing a bond to hell, because that’s going to go for the birds. I mean its going to just follow the Sterling and the Euro down the drain. And we’ve got bigger challenges then just the rest of the world. We got China that’s now issuing a forward contract in oil, measured in Yuan, which the Yuan will be convertible into gold. So, if you buy your contract for Yuan and then sell it for Yuan at a profit, you can convert all those Yuan back into gold. Now that’s going to really challenge the prime reserves status of the dollar and that’s a huge question mark. And if they do it for oil, what not other important international commodities like copper for example. I think we’re facing severe challenges and China is just waiting her time to strike. Whereas we’re spending fortunes on military equipment, China is spending it on making sure that she’s going to win economically and financially. And as the greatest generals have said, the greatest way to victory and power is to put your enemy in a position where they have to capitulate without firing a single shot. And I think that’s what China will do.

FRA: And John, do you think that there’s a possibility for the ECB to begin to buying Germany equities if German bunds become scarce in the overall ECB asset purchase program?

John Browne: Yes, absolutely. They’ll do anything above the law, around the law, they have no laws. They would do anything to save that Euro against the disaster that I see coming unless the Germans back it. And the price for Germany backing it is German rule of the European Union. Which Germany tried three times an empire, Franco-Prussian war, first World War, second World War. Each time and I think they’ve now realized that the Deutschmark i.e. money, is the key and the key to this is either the Deutschmark or the Euro to win their empire which will be Europe. And Britain is hopefully going to be leaving it.

Yra Harris: I think that John is exactly right and the Chinese are interesting to watch. More interesting is the amount of dollar borrowing that Chinese corporations and individuals are doing, Chinese real estate markets, they’re doing these huge dollar bonds. And I’m paying attention to that because first, it puts the Fed in a terrible situation and this is I think where John goes with not having to fire a shot, because the Fed, you know Bernanke beats his chest to talk about how great he’s been and how great it was. I think Janet Yellen has done a much better job by the way, but he just kept adding on and adding on and adding on, and this money had to go somewhere. And it went into the borrowings of, of course emerging markets. So, we’re so borrowed up in dollars now that if the dollar, if the Fed were to move here aggressively, which they’re not going to do, but we’ll create they’re favourite counterfactuals and let’s say they do that. The rally to the dollar would be fairly severe, especially because Europe is going nowhere now, so the dollar would rally more and because there are all these borrowings in dollars which means people are short dollars essentially, it would put a huge rally to the dollar which would wreak havoc across the Emerging markets, and it’s the Emerging markets that are now driving the global economy. Don’t believe the nonsense of European growth, I still see European unemployment hovering at 10% and I’m being kind because I’m using their numbers, the United States has tepid growth at best. So, it’s the Emerging markets and if they were to get into a situation where the dollar became expensive and the amount of dollars that they’d have to go raise to start paying just the interest on the debt. It would cause a very severe contraction. And that’s with the Chinese, I can’t agree with John more, it’s interesting to see who is hoarding gold here. And again, people say oh you’re a gold bug, I’m not a gold bug and I listen to John, he’s not a gold bug. But I’m not a Fiat currency bug either because I see the games that they play. So, I don’t love any of any investment that much, there’s nothing that I see but I just try to protect myself and to see where the world is going to have to go to. So, I’m in total agreement with what John is putting out there. And the ECB, Mario Draghi is the most dangerous person right now in the world, right now. Because he’s in a hurry and he’s now lost his key supporter who was Angela Merkel. Merkel is really going to have problems and if you follow the news today Schäuble is already out as Finance Minister which means that its going to be Lindner who’s the head of the FDP who gets the Finance Ministry and he’s already drawn a line in the sand that he won’t go to for fiscal harmonization in Europe. So, this now gets very interesting and nobody is even talking about the fact that Schäuble is going to take the Presidency in of the Bundestag which I haven’t written about but I’m going to write about it this afternoon or later .. You’re going to have Schäuble, whose a fiscal conservative at heart, you’re going to have Lindner .. I think this now gets very interesting.

John Browne: That’s what I think, that’s fascinating what you say, I totally agree with you about Bernanke, Yellen, and those things. China of course has been borrowing hugely in dollars, of course has got a lot of dollars in terms of securities and Treasury bonds as its second largest holder after Japan, well of course the Fed is the largest holder with about 4 trillion, Japan is about 1.05 and China’s about 1.02 trillion and it ties with Japan for being the second holder. And of course, they will be paying back any debts they borrow. It’s like balancing, by borrowing dollars they’re balancing the dollars they own, which I think is entirely sensible. And even if they borrow more then they have, if they borrow more then 1.02 trillion, they’re going to be paying back in peanuts! And so, I see that as a great strategy for Japan. Regarding gold, its rumored, I mean we’re told America has 8300 tons of gold in Fort Knox, and it may still be there .. but nobody knows who owns it anymore. Its rumored and I say rumored, that already over the last five years China’s been accumulating gold by all means possible, through shipments and out of London through Switzerland and so on, that its now the largest holder and now has more gold then America, but that’s a matter for rumor. But I think they’re very gold conscious, and in the end, I think they see a totally depreciated dollar which they will be paying back the excess debt, they can write off the debts they have against the dollars they own and then they can pay the overspill of the debt in depreciated dollars relying on gold. And I think that’s a serious risk for the dollar and the dollar still is one of the most important things in the whole world economy. And so, if the dollar really collapsed it would create mayhem in the world. That’s why people are buying Bitcoin and all this stuff. I mean the average Joe who elected that Doctor yesterday in Alabama over the established swamp Republican, if people are getting sick of it, and that’s why people are saying if big banks like J.P. Morgan won’t even allow us to hold cash in our own safe deposit box, what we’re paying for. They’re now dictating we can’t hold, we can’t hold cash and all that sort of thing. They’re moving to get rid of cash? Well lets get into Bitcoin or gold or precious metals or something where we actually own the thing. And although I think some of these cryptocurrencies are highly speculative and have had fantastic gains recently, but I think highly speculative, that the people are going for it in desperation to get out of clutches of big government, swamp government that’s just robbing them blind.

FRA: And John, what are your thoughts on the current status of Brexit and the potential for other exits in the EU, EMU?

John Browne: Well first of all I thought May, I saw her first speech and met her very briefly. I thought she was terrific when she got in and even when the Brexit vote happened last summer, 2016 I mean. And she was strong and everything. But then she was advised by these two incompetent people to go for an election trusting the polls which were all wrong on both the Trump election and the Brexit vote and to trust those polls. And she went in and got heavily defeated in the polls, she’s still in the government but she’s severely weakened .. I thought her speech in Florence last week was very weak, I mean offering to pay, Britain is the European Union’s second largest contributor, why on earth should Britain pay anything? Let alone billions of dollars and she sort of gave way a bit on that, I thought that was disgraceful. And also lengthening the time of the transition. We want to stick strictly to the two-year transition so that if people want to have a divorce where the divorce is put off until after the financial arraignments, which is the reverse of any other human thing, you have the divorce first and then talk about the finances. They want the reverse. I think that’s obscene for Britain which was the second biggest contributor is outrageous and she’s giving way and that worries me .. this is just as Yra said right at the beginning, I think Merkel’s election has actually strengthened her hand a little. So, she’s almost back to where she started a week ago. But still it’s a touchy business, and you ask what of the other things? I think the European Union if Britain wants to stop Britain getting out, its largest contributor and everything else and I think there are only four countries where Britain enjoys a trade surplus, all the rest have trade deficits, have trade surpluses with Britain. So, it would be a severe blow both tradewise and economically if Britain leaves and they want to make sure Britain doesn’t leave .. they’re going to tie Britain down and punish Britain as an example to anyone else like Spain, Italy, Greece, who wants to leave, or Poland. You can’t leave, you’re going to be crucified, look what we did to Britain, and Britain was rich. And we still smashed her. And so, it’s a huge thing ahead of us now and until this Sunday I felt very depressed that May had given away so much, but then with Merkel’s erosion of her vote I’m feeling slightly more bullish.

FRA: And Yra, your thoughts on the potential for other exits in the EU, EMU?

Yra Harris: 100% I agree with him 100% their going to be punished, to be made an example and the Brits don’t really realize how good they are getting out because when you go to fiscal harmonization if they go to that, and I think it was a weak possibility before I think it’s been much weakened, it’s going to cost them a fortune. Anybody who has any money and the Brits have money. And why do I know that? All you do is have to open your eyes and look to see what’s going on with who is funding through the individual national central banks in Europe. The Germans are accepting the liability for the entire project and nobody ever asked them. Otmar Issing himself wrote that article two years ago they put it in the FT, he talked about no taxation without representation and this is going to become the battle cry in Germany because you cannot escape from it.

John Browne: Exactly, completely agree.

Yra Harris: First of all I wouldn’t pay them a dime, I’d say to them you know what, come and get it. Come and get it. They couldn’t bomb Libya so I don’t even know what Europeans are talking about. They had to get the ordinates and weapons from the United States to bomb Gaddafi. So, this is not 1914 .. you’re not coming to get it, you’re not getting paid because you’ve gotten all you got from us and we’ve got nothing in return, you’re trying to steal the financial centre of Europe out of London the French have had their eyes on this forever and now they think that they have a free pass at it. I’d give them nothing and tell them you know what, you’re lucky I don’t send you a bill for all the aggravation and all the court costs that I’ve had to endure and all the other things that we’ve had to endure. And John’s point about Germany and Britain industrially being tied into it is absolutely right and the Brits should start playing that up more and more. And if I was May I would turn around and give them a bill and say this is what you owe us for our good offices all the time that we’ve had to put. It’s ridiculous.

John Browne: I quite agree, I totally agree I just like that one point, was when that wrenched man Brown was Prime Minister, no relation to me, he was asked to give the British a contribution of gold into the European Central Bank which was the second largest of course. And he was so ashamed of the thing that he didn’t want the television or news picking up truckloads of gold being shipped to Frankford from London. So, he sold half of Britain’s gold reserves at just over $300 an ounce and lost Britain billions and billions of dollars on that transaction alone just to save his face. So, he could wire the money rather then send it in gold. It moved Britain from being the fifth largest owner of gold down to about the tenth. It was staggering, really. All these countries that save money like Germany and France have large gold holdings .. they all have large gold holdings. Switzerland is trying to get rid of its gold because its Swiss Franc is so strong and they’re trying to do everything to weaken and be like members of the deprecation gang to get their Swiss Franc’s cheaper because it’s hurting their trade. But that’s a false indication, Swiss basically are like the Germans and savers and are sound money people and savers as a result. The American world has turned savers into spenders, and for spenders, depreciated money is the name of the game. Financial dishonesty really.

Yra Harris: Yeah, you know the name of this show is “Financial Repression Authority” .. financial repression – the Fed was number one but now number one of course is the ECB. But to close I just want to pick up with what John talked about with the Chinese hoarding gold. John, I think you will appreciate this, if you go back to I think it was November 2nd 2009, when the IMF had its last gold sale, it sold 200 tons of gold to the Indian RBI at $1,048. Now that’s been a very important level for me. In fact, the last move down in gold stopped at $1,045 and that’s been a very significant level because the Chinese were furious that the IMF sold that gold to the RBI because the Chinese wanted to buy that gold. So that becomes a very critical level of look at all this into what the Chinese truly want to do. And you know what, I think the 3rd or 4th largest gold owner in the world is the IMF even though they cry if they don’t have enough funding, you know I always say oh all those good Keynesians at the IMF and I have no problem with Keynesians, but they have a problem from the gold perspective. Why don’t they monetize that gold and turn it into gold-backed bonds? IMF issued gold backed bonds. And you watch how the Chinese would scoop those up in a minute which is why they won’t do it, because they know who’s waiting there to take and accept that hoard of gold.

John Browne: The net position of gold verses currency is that gold is real money .. It means reality will dawn .. If the central banks of the world are united underneath by making sure reality does not dawn. But history has a habit of eventually something happens and reality does dawn. And of course, one of the countries that’s really interested and very powerful in having reality dawn in the west is China. And that’s why I think China will win this battle without firing a single shot. And it’s a sad thing, I don’t think any shot is going to be used if our currency collapses which is what the real threat is.

Yra Harris: And if we know the Chinese, they’ll be bimetallists and because they got a little evening to settle with the Brits over the silver situation in the 1800s so they’ll probably be bimetallists by that time.

John Browne: Oh yes, the precious metals, but the big boys use gold. That’s why silver is a greater investment at the moment because at the moment if you were to imagine a bell curve we’re on extreme left-hand end very very few people compared to the worlds population own precious metals. And of course, an ounce of gold at $1,300 is a lot of money for the average Joe .. But at $20 for a coin in silver is not so bad. And therefore, the mass market will go for silver and that’s a huge on the bell curve and would drive silver up much faster then gold. But gold is the real money in the end and this will defeat players play.

Yra Harris: Right, and I’ll tell you from a trading standpoint, John and you probably know this, is that there’s not a real precious metal rally that takes place without silver leading the way. That’s a fact. When gold ran up to $1,900 it was silver that lead the first leg of it by a lot. So, I keep waiting for that to happen, somebody has their foot on it but we’ll see.

John Browne: It comes from the average Joe .. If those people are worried about their money they buy silver. And that’s why I still believe in silver so I agree with you entirely.

FRA: Well that’s great insight, gentlemen. I know you have a time constraint John but how can our listeners learn more about your work, John?

John Browne: Well I write for europacificcapital.net (http://www.europac.com/) it’s a website and I write for that and there are a lot of articles and things like that. That’s mainly what I do and I sometimes get asked to go on Fox, CNBC, and CNBC Asia to speak about these things, but I never know when that’s going to happen.

FRA: Great, and Yra?

Yra Harris: You can reach me at Notes From Undergroundor yragharris.com and you click on notes from underground which is where I blog at, but I’m on the Santelli Exchange all the time, and I gotta tell Rick Santelli to get John Browne on! He needs a British voice.

FRA: Excellent.

John Browne: Thank you very much, Thank you very much Yra.

Transcript written by Jake Dougherty<jdougherty@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/28/2017 - John Mauldin: The Bubble In Government Promises Is The Biggest Bubble In Human History .. Pension Storm Warning

“‘The bubble in government promises’ I think is arguably the biggest bubble in human history. Elected officials at all levels have promised workers they will receive pension benefits without taking the hard steps necessary to deliver on those promises. This situation will end badly and hurt many people. Unfortunately, massive snafus like this rarely hurt the politicians who made those overly optimistic promises, often years ago ..

The graph we showed earlier stated that unfunded pension liabilities for state and local governments was $2 trillion. But that assumes an average 7% compound return. What if we assume 4% compound returns? Now the admitted unfunded pension liability is $4 trillion. But what if we have a recession and the stock market goes down by the past average of more than 40%? Now you have an unfunded liability in the range of $7–8 trillion ..

We throw the words a trillion dollars around, not realizing how much that actually is. Combined state and local revenues for the US total around $2.6 trillion. Following the next recession (whenever that is), the unfunded pension liabilities for state and local governments will be roughly three times the revenue they are collecting today, and that’s before a recession reduces their revenues.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/28/2017 - Great Chart On Bubbles