We posed this question to former Federal Reserve Advisor Danielle DiMartino Booth on Wed Nov 29 – her answer is very interesting and we will post the podcast interview shortly ..

11/30/2017 - Will Private-based Cryptocurrencies Be Allowed To Coexist With Government-based Cryptocurrencies?

11/30/2017 - Will Private-based Cryptocurrencies Be Allowed To Coexist With Government-based Cryptocurrencies?We posed this question to former Federal Reserve Advisor Danielle DiMartino Booth on Wed Nov 29 – her answer is very interesting and we will post the podcast interview shortly ..

11/27/2017 - Mike Novogratz On Bitcoin And Cryptocurrencies

Mike Novogratz on Bitcoin and Cryptocurrencies:

“This whole revolution came out of a breakdown of trust. It came out of the ’08 financial crisis when people said we no longer trust financial institutions, we don’t trust governments and, in parts of the world, today still. If you’re in Venezuela, it’s really hard to trust the central bank, or in Zimbabwe. So, the decentralised revolution, which Bitcoin is really the poster child of, is a response to the breakdown in trust.”

11/27/2017 - Danielle DiMartino Booth On The Federal Reserve’s Biggest Fears

“The Fed’s biggest fear is they know darn well this much credit has built up in the background, and the ramifications of the un-wind for what has happened since the great financial crisis is even greater than what happened in 2008 and 2009. It’s global and pretty viral. So, the Fed has good reason to be fearful of what’s going to happen when the baby boomer generation and the pension funds in this country take a third body blow since 2000, and that’s why they are so very, very intimidated by the financial markets and so fearful of a correction.”

“Look back to last year when Deutsche Bank took the markets to DEFCON 1. Maybe you were paying attention and maybe you weren’t, but it certainly got the German government’s attention. They said the checkbook is open, and we will do whatever we need to do because we can’t quantify what will happen when a major bank gets into a distressed situation. I think what central banks worldwide fear is that there has been such a magnificent re-blowing of the credit bubble since 2007 and 2008 that they can’t tell you where the contagion is going to be. So, they have this great fear of a 2% or 3% or 10 % (correction) and do not know what the daisy chain is going to look like and where the contagion is going to land. It could be the Chinese bond market. It could be Italian insolvent banks or it might be Deutsche Bank, or whether it might be small or midsize U.S. commercial lenders. They can’t tell you where the systemic risk lies, and that’s where their fear is. This credit bubble is of their making.”

“I don’t think any of us know what the implications are for a $50 trillion debt build since the great financial crisis (of 2008). It is impossible to say. We have never dealt with anything of this magnitude.”

“To me, Bitcoin is a reflection of panic. It’s a reflection of people trying to get money into a safe place knowing the major governments of the developed world have got their printing presses running 24/7. It is a reflection of anxiety in fiat currencies and the fact it’s not practical to go back to a gold standard. What scares me about Bitcoin is the central bankers are studying it to figure out how the blockchain works. . . .They are going to be controlling our spending with blockchain technology that is being perfected in the crypto currency universe.”

“2017 is the record for quantitative easing (money printing) globally. We have never, not even in the darkest days of the financial crisis, central banks have never injected as much money as they have into the markets. . . . I am not a gold bug, but we do know that in times of corrections that there is no place to hide in traditional asset classes that you can get at your Merrill Lynch brokerage. Gold and silver in the precious metals complex are the only places to hide and get true diversification and safety.”

11/27/2017 - Citi: “There Is A Growing Fear Among Central Bankers They’ve Lost Control”

“In a fairy tale, turning points come suddenly and unexpectedly. Everything that has long been taken for granted is suddenly in pieces. In that sense markets are not all that different. People have gotten used to the paradigm that has been built up since the Great Financial Crisis. It has been tested on several occasions – 2011, 2012 and 2015 – and on each occasion central banks have overcome the challenge, thus ultimately reinforcing the regime.

The emperor in Andersen’s story was only able to parade around naked because the social norms, customs, conventions and vested interests that had built up over time were so strong that even the blatantly obvious was better left unspoken.

Similarly, the low risk premia, the low level of volatility, the lack of responsiveness to tail risk and spillover of systemic events, the reluctance to sell etc. to us are all indications that the market now has an almost Pavlovian response to central bank liquidity. The mere thought of it is enough to still leave us salivating, even when it is patently in the process of being turned off. Yes, excess liquidity will remain in the system even after central bank net asset purchases fall to zero, but as we have argued, if that money has chosen to stay out of the securities market now, then why should it seamlessly come flowing in at these valuations when the backstop is moving out the money?”

11/23/2017 - Yra Harris: Central Bank Policies Are Causing Massive Distortions In The Credit Markets

“Corporations are able to borrow for stock buybacks and increased dividends but creditors are accumulating assets based on risk premiums established by central banks’ QE programs and are causing massive distortions in the credit markets. Central bank policies initially prevented a liquidation of global assets and a world depression, but its robotic response to keep the presses rolling is causing a dangerous crushing of risk premiums. Also, the financial repression has resulted in even-greater wealth inequality as the world’s wealthy are much better situated to ride the tsunami of wave of central bank QE programs. The distortions caused by financial repression are being felt in the rise of fringe political parties appealing to the very visible outcomes of asset inflation caused by the endless infusions of liquidity. It seems Mario Barada Nikto is necessary for the Salvator Mundi.”

11/22/2017 - The Great Debate About Bitcoin, Cryptocurrencies and Gold – David Kotok & Others

David Kotok: “Following up on our recent commentary, and with permission, we continue to quote the excellent work of Nick Colas and Jessica Rabe of DataTrek Research .. ‘Do cryptocurrencies like bitcoin meet the definition of an ‘Asset class’ for investors that care about that designation? At the moment, the answer has to be ‘No’. A few reasons why:

• They are too small ..

• Cryptocurrencies do not yet have as robust a regulatory framework around them as stocks, bond, currencies or other traditional asset classes ..

• Cryptocurrency exchanges and wallet operators around the world operate with varying levels of know-your-customer and anti-money laundering laws. There is no absolute assurance, for example, that a bitcoin you just purchase online didn’t have a member of the North Korean military or Iranian Revolutionary Guards ultimately on the other side of the trade ..

• An asset class needs some level of homogeneity among its constituent investments. GM and Facebook are wildly different companies, but the equity of each represents the same type of claim on residual corporate cash flows. Bitcoin and Ethereum – the two largest cryptocurrencies by market cap – are not the same in terms of structure or purpose. In fact, they aren’t even close ..

• There is not enough history to assess the price relationship between cryptocurrencies to other asset classes.’ ..

Meanwhile, Kerry Smith, a retired Stanford law graduate and serious student of the electricity grid, emailed an observation about how crypto is a large consumer of electricity. He notes that risk. We contrast it with a gold linked token which can use block chain successfully but is not subject to the electricity constraint. We shall see if gold tokens catch on. The turmoil in the Middle East may be the catalyst.”

Oliver Garrett in Risk Hedge:

#1: Cryptocurrencies Are More Similar to a Fiat Money System Than You Think.

#2: Gold Has Always Had and Will Always Have an Accessible Liquid Market.

#3: The Majority of Cryptocurrencies Will Be Wiped Out

#4: Lack of Security Undermines Cryptocurrencies’ Effectiveness.

#5: Hype and Speculation Continue to Drive Cryptocurrencies’ Value

#6: Cryptocurrencies Do Not Have Gold’s History as a Store of Value

Mike Novogratz on Bitcoin and Cryptocurrencies:

“This whole revolution came out of a breakdown of trust. It came out of the ’08 financial crisis when people said we no longer trust financial institutions, we don’t trust governments and, in parts of the world, today still. If you’re in Venezuela, it’s really hard to trust the central bank, or in Zimbabwe. So, the decentralised revolution, which Bitcoin is really the poster child of, is a response to the breakdown in trust.”

11/20/2017 - European Central Bank Proposes End To Deposit Protection

‘covered deposits and claims under investor compensation schemes should be replaced by limited discretionary exemptions to be granted by the competent authority in order to retain a degree of flexibility.’

11/20/2017 - Dr. Albert Friedberg Sees Accelerating Inflation Ahead, Will Be Problematic For Central Banks

LINK HERE to the quarterly podcast

11/11/2017 - The Roundtable Insight: Yra Harris And Peter Boockvar On The Trends In The Financial Markets And Monetary PolicyFRA: Hi welcome to FRA’s Roundtable Insight. This is Richard .. Today we have Yra Harris and Peter Boockvar. Yra is an independent trader, a successful hedge fund manager; global macro consultant trading foreign currencies, bonds commodities in equities for over 40 years. He was also CME director from 1997 to 2003. And Peter is the Chief Market Analyst with The Lindsey Group and the co-chief Investment Officer with Bookmark Advisors. Peter has a newsletter product called The Boock Report. Spell book B-O-O-C-K-REPORT.COM. It offers great macroeconomic insight and perspective with lots of updates on economic indicators. Welcome gentlemen.

Peter Boockvar: Thanks Rich.

Yra Harris: Thanks. Rich.

FRA: It’s great today to start off with a quote that you had in your recent writings, Yra, on flattening yield curve. “It’s the ECB and Bank of Japan policy that is flattening global yield curves as investors search for extra yields” and you made the analogy to something similar which may be happening to the 1994 Orange County bond disaster. Just wondering if you can elaborate on your thoughts.

Yra Harris: OK. So when we look at this you know we were comparing it to Orange County. I do because that was a classic case .. it was actually a meltdown as the Fed started to raise rates and everybody was crowded into a bond trades. We saw first of all the yield curve seeping out dramatically even though it was a shortened because so many people crowded into that trade. But what you really found out what Orange County exposed is that Robert Citron, who was the Treasurer for the Orange County at the time, was busy chasing a little bit extra yield 25-30 basis points and there are many sell side firms who came to him and they were offering him these products and they were exotic products, very exotic at the time. And so in order to please his bosses he chased extra yield, very little. So at 25, 30, 35 basis points and I know this from Sheila Bair’s committee, which I sat on in Washington, in which we analyzed what went wrong there. So I had a pretty good behind the scenes look at it and it reflected in that. So when I look at the world today and I know Peter’s written to me this is a real problem in that people are taking on so much risk in an effort to chase so little return when you’re in a world where Italian bonds are yielding 1.75. You take on all kinds of risk as you search for an extra 30, 35 basis points because 35 basis points in today’s world is a lot. And for those who are trying to outperform the market and these are people who manage institutional money and big pension funds and insurance companies. They are taking on a lot of risk and that’s what keeps me up at night. And I think we’re getting close to crunch time in which some of these trades you know as Warren Buffet would say you know when the tide goes you can find swimmers naked. Well I don’t think there’s many babies who have been sold at all so I think we’re probably more what is it called the hedonism. I’m too old to know and to partake in that. But I think we’ll find out that there’s a lot of nudity in the waters of central bank liquidity.

FRA: Peter do you see a similar 1994 Orange County environment.

Peter Boockvar: I like that analogy. That was great. Yeah I do. It’s good to follow the money. OK so next year even in January when the ECB cuts their QE in half and the Fed goes from draining 10 billion a month to 20 billion a month. Liquidity is going to go to almost zero. Between those two central banks. So that’s a major change. I mean this year on a run rate the ECB was buying net of 700 billion euros of securities and you cut that in half next year and then you subtract what the Fed is taking out and that is almost going to nothing. And that is a really big deal. At the same time the Fed is raising interest rates and the BOJ is buying less ETFs and they’re buying less JGBs. That liquidity flow is going to turn into a drip next year and leaves no room for error anywhere else.

FRA: What about if we look at the U.S. Yra you asked how does the Fed deal with a flattening yield curve in your most recent writing. Noting it’s gone lower than 73 basis points. Any thoughts on that? I mean you did suggest something on the cutting the short term rates on that to make it similar steepened like the German 2/10s.

Yra Harris: Yeah because I compared, Peter and I actually went back and forth of this yesterday on this because I showed them that German 2/10 versus U.S. And if you were a wagering person you say well the ECB is doing all this buying. The Fed is as Peter says has stopped. And in fact is now in contraction. You say well the curve should actually be steepening in the U.S. based on those mechanics. And we should be flattening in Germany, but it’s absolutely the opposite. German curve is out to three year highs and 110 basis points while the U.S. curves was at 70 basis points and flattening. So when you look at this it was a word you used yesterday. You’re absolutely right. They said this is like wild. I said yeah that’s exactly what it is. It makes very little sense and makes in fact no logical sense whatsoever and I don’t know how the Fed, Ron Paul going to have to face this because the Fed has already told us they don’t understand that their models have been wrong and they really don’t understand what’s going on in the inflation world. They don’t understand it. So now they are going to tell us that they don’t understand why the curves are flattening. Because when you look at it and you throw in this tax plan is not tax reform it’s a tax cutting and it’s stimulative by everything that I hold dear to me. This curve should be seeping dramatically. Bond should be getting terrified of what they’re facing. And as Peter says you know next year they’re going to be shrinking. This curve should be steepening and yet it’s not. So if they do and then they’re going to tell us they don’t understand what’s going on with the curve and I know that the curve is one of the big indicators. So if you don’t understand that, you don’t understand inflation. You’ve made a four and a half trillion-dollar wager on the effectiveness of the QE programs. That doesn’t go well with me. So I think that’s what it was. So you can either cut rates which would throw the markets in absolute turmoil. That’s just the way it is there’s nothing else they can do or they can as I say they could increase the amount that you know .. I say if next January if the ECB was cutting to 30 billion or maybe the Fed should be always be selling more than the ECB is buying and you get the curve to steepen and I guarantee that.

FRA: Peter your thoughts?.

Peter Boockvar: Yeah I agree. You know just to quantify the dramatic effect that the ECB had on the entire yield curve in Europe relative to the U.S. and the Fed is that the Fed when they were doing QE infinity, they never bought more than the net issuance of debt that the U.S. government was issuing. In Europe the ECB was buying 7 times the net issuance. It was just so dramatic it was literally the elephant that was stomping everything in its sight. And granted having negative interest rates continuing into 2019 will certainly keep a big anchor on the short end. But because of the dramatic extent that the ECB was buying bonds I have to believe that there is going to be some response when they stop buying bonds. Now again the negative interest rates in the short end will be an anchor. But you know imagine even when that ends. I mean one thing that that we have to take notice, Draghi is now becoming more defensive about negative interest rate. He’s now having to explain himself. Here we are this is three and a half years after he initiated negative interest rates and he is still defending negative interest rates. You have the European Bank Stock Index that is still below where it was three and a half years ago. So I think that the politics around negative interest rates will get more and more difficult as bank profitability continues to be under pressure. And you know that there’s no question that accidents are going to occur here. I just know none of us are smart enough to know how it exactly plays out. But come January when things are shifting in a more dramatic fashion, I think everyone has to be really really careful.

FRA: And so what will happen, your thoughts on the new Federal Reserve chairman nominee Jeremy Powell. How do you see his policies and what will his monetary policies be like in the coming years? Yra you want to start?

Yra Harris: You know I’m not sure .. when I had the opportunity last year to directly ask a question, you know about who guarantees the ECB. It was a two-part question that I asked was who guarantees the ECB and do you think that all sovereigns should be carrying zero weight. Because I know what his expertise, his strength is within the Fed and he was subdued. I was wild about the answer so I would have given him some crap, but I do think that he’s a good choice because he’s very pragmatic and I think he’ll know how to adjust or hopefully. So his response to me on the ECB was they have a printing press, which he didn’t even have to think about that and that came right to him. And the fact that there’s zero weighted. That’s all we have to care about. They are zero weighted and I was never comfortable with those answers, but I think he brings more to the table. I think he is unlike some of the people who do sit in that room with their high level math and Ph.D.’s are too arrogant for the job ..

FRA: And Peter?

Peter Boockvar: Yeah I mean I think while he is very similar to Yellen in that he voted for every QE, he voted for keeping interest rates at zero for as long as they did. So he voted for the committee every single time. There is talk that he was not a big fan of QE. So that’s a positive for the sake of manipulating markets. It won’t necessarily be a positive for markets when we get the next 10 to 20 percent decline and everyone’s screaming oh the Fed save us, the Fed save us. I think he’d be less inclined to be the markets sugar-daddy, which I think is a good thing, but maybe it’s not what the market necessarily wants to hear. Now he’s not going to obviously be as potentially hawkish as Taylor or Warsh would have been. But I think if the market thinks he’s a Yellen look like I think they may be a bit disappointed that he’s going to be thinking more outside the box and he’s not going to believe in John Maynard Keynes to the same extent that Yellen has.

FRA: Just going along the discussion from Europe. Peter you’ve written recently on how higher inflation in the Eurozone is a very under-appreciated risk. Can you elaborate?

Peter Boockvar: Yeah. I follow the market monthly numbers and I like to read their commentary now it’s very anecdotal. So we have to separate the anecdotal commentary from business surveys that they do from the actual consumer price index that the Eurozone comes out with. But on Monday we had the Eurozone services and manufacturing composite index come out and I’ll just read to you what the inflation commentary was. Inflationary pressures have meanwhile lifted higher with price charges for goods and services rising at a rate not seen for over six years. Some price rises merely reflect the pressures of higher cost, but companies are also reporting stronger pricing power as demand conditions continue to improve. Which suggests underlying inflationary pressures are becoming more ingrained than yesterday. Market came out an index on German construction and they talked about intense supply chain constraints contribute to a sharp rise in input costs. The incidence of delivery delays is one of the greatest seen for over a decade while purchase price inflation was pushed to a six and a half year high. And they also reported a retail Purchasing Managers Index for the region and they talked about gross margins facing Eurozone retailers continue to be squeezed. Contributing to this was another rise in average input prices. Moreover, the rate of inflation quickened to a fifty seven month high and remained substantially greater than the long run average. So how that translates into actual inflation. I don’t know what PPI will eventually look, like what CPI will eventually look like I don’t know. But to me when I read that tells you that there’s price pressures that are .. any potential surprise on the inflation numbers in Europe I think will be to the upside using this as as potential evidence. And even with cutting QE by 50 percent there’s still going to be buying 30 billion a month and they still have interest rates deeply negative. So they’re wholly unprepared for a multi-month march to lets just say 2 percent CPI. And I think that that is a major risk for the European bond market. And to me the European bond market is the epicenter of of of the global credit bubble.

FRA: Do you see similar conditions Yra as the biggest bubble being the European bond market?

Yra Harris: Well yeah Peter’s been on the strength of growth and on Europe as he says you know he’s been very bullish in European equity markets, but he’s a more than a little concerned as he’s just talked about about what the banks have done because the interest rate policy is of course the ECB. But you know the issue where we may differ is do I think that Draghi cares about what inflation is? I don’t think so because you know as I’ve talked to Peter and I have discussed I think I’m with you Richard that he has a bigger thing going here and that he’s trying to load that ECB up with as much debt as possible because it’s the only outcome can be of course would be the creation of a Eurozone bond .. The European Commission has not been able to move it forward and you know the talks that came from the Crown was to push it farther and faster. And you know there is of course Germany is more than reticent because they know what’s going to be settled here. So he keeps going and going and going. I agree with Peter once we get over 2 percent inflation. I know what the response is going to be because that’s what you know. They basically use the same kind of dynamic stochastic models that the Fed does and others well you know they’ll call transitory they’ll call this so if it’s the same .. Then if it’s the same for three or four months they’ll have a serious problem and you could see that there is pushback. You know he didn’t talk about it at meetings but there were five dissenting votes to even the cut of 30 of 30 billion, only big movie from 60 to 30 billion and leaving the negative interest rates. And with all that forward guidance so there was pushback and the pushback is coming from just where were the sources from the Dutch the Austrians and now we’ll see even more from Austria because of their political situation. But Merkel’s in severe trouble .. Germany may have to go to a new election because they cannot put together a coalition here because the Free Democrats, they want the Ministry of Finance which, Schäuble used to run and he was fairly hawkish. But they want more. And their issue is you know of course you know with the ECB and their overall policy and that’s the effect on German savers. So this is very very dangerous. In fact, one of Merkel’s ministers, one of her close people came out .. They’re trying to load back the Social Democrats. I don’t think that’s possible. So because the Social Democrats would have to eat such a phenomenal crow it would be it would be the end of them. They could be in this coalition. Well they’ll continue to lose power, but if Germany winds up going into a new election, Merkel is going to get trounced because there’s no way .. So there’s a lot of things yet to play out in Europe again and this is more laid out as Peter and I started the discussion offers her new letters. There were of course was that there’s so much complacency in the world and yet these things are on the boil and I know we haven’t even gotten to the next topic you’re going to go to which puts it more, but Germany is still an unknown yet. And it’s the unknown not because of anything really positive for Europe. It’s a negative for Europe. So she’s got to figure out just what’s going to go on here and who’s going to get one. And she’s trying so hard not to give the free Democrats win there the Ministry of Finance because then he’ll really have a voice. And it’s not going to be a pro-European voice. So a lot of things to be played out here. And as Peter has talked about, where are the banks .. who have really so badly underperformed with this .. the banks are way under-performer as they are in Japan. I mean I’ve been owning Japanese stocks for longer than I care to admit but at least I’ve had some dividends in earnings and they haven’t done anything. But if things are so good why aren’t the banks rising. We’ve seen fairly significant rallies this year in the U.S. Banks and that’s you know even with a quote unquote flattening yield curve. So there are so many uncertainties.

Peter Boockvar: I mean just just to quantify the Japanese TOPIX Bank Index is still 20 percent below its 2015 high. I mean I think the reaction of banks has basically repudiated negative interest rates and central bankers desire to basically destroy their yield curves. And if banks are the transmission mechanism of this sort of policy you wonder how central bankers can contain the circle of damage and profitability of the banks, but continuing on the same path of monetary easing.

FRA: What about now the effect of Saudi Arabia. We’re seeing some incredible events happen over the last week. And you know given all the complacency well how could Saudi Arabia, what’s evolving there affect the financial markets and the global economy. Yra do you want to start.

Yra Harris: Well I believe that you know and I’ve blogged about this the other day too. And this is truly one of my areas is the great strength is the geopolitical events are taking place. And usually it’s for the North Korea statements or nurse those are one off things and I always caution people you know what those moves you can trade them, but don’t look at them as anything longer than a one-day trade or two-day trade because wars don’t push gold higher; wars you know or let’s say some type of conflict. Those are quick one off moves, but what’s going on and I go back to October 5th when we had a seminal event in international relations which is that the King, not the crown prince, but the King of Saudi Arabia went to Russia to meet with Putin for the first time. And as I tongue in cheek say it’s like Nixon going to China. Very unexpected. And ever since that day you can plot a chart take a look at it. Oil prices have risen eight dollars in a steady upward beat and then you had what came out this weekend. But it’s been a steady thing the oil keeps rallying. It’s not a headline grabber. But there are movements of foot here and the Saudis are very concerned about the Shiite influence throughout the Middle East. The role in Syria, the role in Iraq, the role in Lebanon. And then you get of course you know Hariri, who is the Lebanese prime minister, who was in Saudi Arabia and resigned on Saturday night. Now really is interesting because Hezbollah actually assassinated his father. And Hezbollah is a Shiite militia and you know somewhat of a governing group that the Saudis are very worried about as are others in the region. And that has now shown to be even more and then of course you have the downing of a helicopter. So on the Yemen-Saudi Arabian border with some high level Saudi officials supposedly .. You know as I say it’s like the Gulf of Tonkin. We don’t know certain things, but there are movements afoot here and that is you know the Middle East is still a very significant area. It’s significant for China not as much of the United States is used because we don’t get as much oil there. But this is a very dangerous time. And again the equity markets don’t price any of this risk in. It’s like you know I watched Sunday night with what went on and I was amazed that the market was short gold. And I said I’m getting I figured I was going to lose 10 or 20 dollars. It opened basically unchanged and lower. I got this a reprieve I actually turned around and went long. So you know but the market none of this is like if it doesn’t occur on Twitter nobody cares. These are the type of systemic events that take place underneath the radar screens that will when they start to be exposed.

FRA: Peter do you see similar impact from Saudi Arabia and what will be the effect on oil prices?

Peter Boockvar: Well I agree. I think Yra said everything there was to say. I just want to add on that what’s going on with the oil is you know we’ve also had multiple years of a big reduction in the rate of them investment in oil production particularly offshore. You’ve had trillions of dollars of projects get canceled. Yes. And we’ve seen that also in the mining space in the industrial metal space. You know that’s what their markets do and that’s when companies start to focus on returns on capital and cash flow. They spend less on drilling and mining and I think it’s really been the supply side that’s been under more discipline that has created a lift in oil and industrial metals and this rising commodity prices. So I think that’s something to pay attention to that. Yeah this is partly geopolitical, but I think there has been a concerted effort in trying to control at least the supply side and even in yet in the U.S. I think people are waking up to the economics of shale and that markets aren’t necessarily going to be so friendly to continue to finance all the shale drilling where a lot of these companies aren’t generating any cash flows. So while U.S. production will grow over time I think a lot of it’s going to be cash flow driven and less of that just the reckless spending just to drill a hole and create more barrels ..

Yra Harris: And you know what Peter brings up a very good point. For another reason but with the rise in oil prices has pushed the high yield debt of energy companies to the highest levels not yields levels but price levels. And yet when I look I’m looking at JNK the high yield ETF HYG and JNK and those are both have moved underneath the 200 day moving averages which is another warning. There are signs that are developing because what would drag them down, you know last year we did or what sent high yields of course when the energy bonds and all the structured notes that they did were under trouble. Now they rise in the value and yet the high yield indexes, the yields are rising .. So that’s another one of these divergences that really is flashing for me.

Peter Boockvar: Yes, I agree. I think this rise in the cost of capital and expansion .. But you have to remember that the rise in short term interest rates is a really big deal because there’s hundreds of billions of dollars that are seeing a rise in their cost of capital every single day. With this rise in short term interest rates I mean the one-year T-bill is yielding 152 today, the S&P 500 dividend yield is 1.9 percent. These are still obviously very low numbers, but in a world of many years of zero interest rates ..

Yra Harris: In what Peter said that’s such a great point. You know that I’m celebrating 152. I mean world where you know I’m dancing and I’m doing this just because you know.

Peter Boockvar: It’s like shocking to say.

Yra Harris: It’s shocking.

FRA: And maybe we can end with your thoughts on New York Federal Reserve president William Dudley stated “we had a woefully inadequate regulatory regime, it as much better now in place, there is still more work to do” .. In reference to the financial crisis and what’s happened since. Yra you mentioned that was pure rubbish.

Yra Harris: I mean really it’s pure rubbish because the Fed had all the macro prudential tools that they needed, if they wanted to put a halt ..

Peter Boockvar: Yeah and I think Dudley’s comments reflect just an extreme level of delusion that Bernanke had as well. And that for them to, with a straight face, saying that it was regulation that was not in place. That was the cause of the crisis, I’m trying to think the right word, but it’s actually dangerous because they’re deflecting any self blame on monetary policy. I mean monetary policy is the liquor that feed the drunks and where for Dudley and Bernanke before to say well it was the lack of regulation that was the cause. It’s actually scary to hear because it tells you that they don’t understand. They don’t understand and they don’t want to admit the unintended consequences of price fixing the cost of money and that typically goes awry and it has in the past and it is now and it will again. And to think that it’s a regulatory structure in place and that a bunch of bureaucrats are going to somehow manage the economy from that perspective and and create these buffers around economic cycles is just I don’t know if it’s hubris or just complete delusion.

Yra Harris: Really That’s like sums it up and it was a when somebody responded in a blog and I wrote look at Greenspan not only did he not try to curb it he encouraged it. He said use your house as a piggy bank .. refinance it and create demand by spending the money that you can extract from this taking out of course more debt at the same time .. And number two Bernanke he didn’t, as Peter rightly said, they fueled this; this is contained which is no worry here .. They did nothing. I mean at first blush they could have raised reserve requirements to start squeezing the leverage that the banks were employing … Well how do you know it’s a bubble and what if we’re wrong. Because monetary is a blunt instrument you know squeezes the entire economy. Well you know what. Don’t tell me that you didn’t have the tools and you had the tools.

FRA: Exactly agree very much on those thoughts. And that’s great insight. Gentlemen how can our listeners learn more about your work Yra.

Yra Harris: Send money. No Bitcoin .. J just kidding .. I post blogs and Notes From Underground. If you can find register to look up to you but that is a little humor.

FRA: Peter?

Peter Boockvar: You can go to boockreport.com – you can see my daily writings and also you can go to bookmarkadvisors.com.

FRA: Great. Thank you very much gentlemen.

Submitted by Boheira Manochehrzadeh <bmanoche@ryerson.ca>

11/05/2017 - Yra Harris On The Greatest Act Of Financial Alchemy

“The Swiss National Bank (SNB) has pulled off the greatest act of alchemy by printing copious amounts of Swiss francs (CHF) and turning the currency into real corporate assets. The SNB has grown its balance sheet to CHF800 billion from CHF500 billion in 2015, 85 percent of which is foreign exchange holdings in various forms. As the SNB struggled to weaken the franc to prevent the ultimate safe-haven currency from strengthening and putting the Swiss economy into a DEFLATIONARY SPIRAL. The Swiss experiment began January 15, 2015 .. The recent rally in BITCOIN pales in comparison to the wealth created by the Swiss printing presses.”

Notes From Underground: A Celebration Of The Greatest Act Of Financial Alchemy (Ever)

11/05/2017 - Dr. Albert Friedberg: Military Conflicts And Inflation Remain The Two Largest Risks Facing The Market “We remain very bullish about our present positions, though ever cognizant of the possibility of sharp setbacks on the way to final heights . Military conflicts and inflation remain the two largest risks facing the market; the former is difficult to hedge but not so the latter, where we feel the risks are manageable and may even lead to trades that will be conducive to interesting profits.”

11/03/2017 - The Roundtable Insight: Daniel Lacalle On How Central Banks Are Nationalizing The Economy

11/03/2017 - Chris Whalen On The Return To Derivatives By Big Wall Street Banks To Manufacture The Appearance Of Profitability

“For some time now, we have been concerned that the FOMC’s overt manipulation of credit spreads has embedded future credit losses on the balance sheets of US banks. But now we are starting to see even greater signs of stress as the large Wall Street banks again return to derivatives in order to manufacture the appearance of profitability ..

The moral of the story with Citi and other large banks is that there is no free lunch, but sadly no one on the FOMC seems to appreciate this subtlety. When the Fed pushes down interest rates and then manipulates credit spreads to achieve some illusory goal in terms of monetary policy, the result is a change in the behavior of investors and lenders that is profound.”

11/01/2017 - The Roundtable Insight: Alasdair Macleod And Bosko Kacarevic On Why Physical Gold Makes SenseFRA: Hi welcome to FRA’s Roundtable Insight. This is Richard .. Today we have Alasdair MacLeod and Bosko Kacarevic. Alasdair is the head of research for GoldMoney and an Austrian economist. He has a background as a stockbroker, banker, and fund manager. Basko is the president and CEO of Kindigo Capital, a Canadian based private equity firm in Windsor, Ontario, Canada. The whole financial licenses and commodity derivative stocks mutual funds and private equity. Welcome gentlemen.

Alasdair Macleod: Nice to be here.

Bosko Kacarevic: Thank you for having me.

FRA: I thought we’d do a focus today on physical gold. Why physical gold why does it make sense where to store it, how to store it. And then perhaps a comparison to what’s happening in the Cryptocurrency world, sort of Gore versus cryptocurrencies debate and further where we kick it off with if you want Alastair with why physical gold why does it make sense?

Alasdair Macleod: Well the the the basic sense behind physical gold is that it’s nobody else’s liability. It is Money, is money not an investment. And I think that’s an important point. But as money it tends to retain. In fact, over a period of time it tends to increase its purchasing power measured against commodities and if you like the items that are manufactured of commodities. And if you want proof of this basically from 1969 to the present day the dollar priced in gold has lost over 97 percent of its purchasing power. So that’s how strong on gold is. But if you’re going to hold gold in paper form someone can come away and change the rules. Your paper might go bust if let’s say you’re in an ETF, which invests in synthetic gold. If you try and invest in gold on the futures exchanges, sort of rolling contracts. That again is subject to really try and take delivery. You may not get your delivery. The one thing that really matters is that you have the physical gold. Now obviously you can store all your gold at home if you’ve got any significant level of assets. So you need to find if you like a really good LBMA registered faulting company who will store all your gold and that’s basically what we do is go money. We act as custodian; our customer’s gold is not on our balance sheet it’s it. It operates on the Canadian Belman laws. I think that’s the technical term. So if we have some sort of financial accident, there is absolutely no dispute about the ownership of gold which we have as custodians, it belongs to our customers. We have both a metal audit and also financial audit every quarter. So that again you know it’s all recorded, it’s yours and you’ve got a choice of vault around the world. So if you’re an American and you have a fear that the American government might be in a sort of command you to submit your gold in America. It’s not under the American government control, it be put it into a foreign jurisdiction. I mean we you know Switzerland or Singapore or somewhere like that. I wouldn’t say that you break the rules but it just makes it a bit more difficult for your government to get the gold. So there are all sorts of ways in which you can ensure that your money capital if you like is is is safe at all times and that basically is the function of gold stored in a proper vault.

FRA: And your thoughts Bosko.

Bosko Kacarevic: Yeah I have to agree with Alasdair. We approach the gold as a form of currency. We already regulated securities dealer in Canada as an exempt market dealer. So we provide as well storage facilities for investors in physical gold. Our one of our recent announcements was a we have a platform where RSP investors retirement accounts can put physical gold into their retirement accounts and have it stored in LBMA approved vault and they can trade the gold buy and sell it at any time. When the gold is in your RSP account because it’s in trust for the retirement then it can’t and the clients can’t take delivery of it. But the physical gold is there it’s accountable, it’s audited, and there we offer a basically a non fungible system. So when our clients purchased their gold it’s in a specific container, it’s allocated, and segregated to their account. So the exact same gold Maple’s gold bars that someone purchases is the exact same that they’re going to be selling. So we try to explain to people that you know a properly diversified portfolio should have some physical gold and silver in it depending on suitability. You know you might have 10 percent or 20 percent, but it all depends on the rest of the portfolio that the client is holding and at Kindigo we focus on our clients are mostly accredited investors. So there’s considerable due diligence that we do. And the KYC forms that have to be filled out, according to the compliance requirements in Canada.

FRA: And Alasdair what are the risks for for storing gold or ways in which you can have it from your perspective in terms of the industry. Like what are the advantages and disadvantages of different ways of storing gold?

Alasdair Macleod: Well obviously that I think we’ve just agreed the best way to store it, but you know unless you’re talking about small change at home if I can describe it that way is in LBMA registered vault. And again if you have it in a different jurisdiction from the one in which you live that you like is another safeguard. The other safeguard that’s a proper LBMA registered vault gives you is that gold that goes into the gold basically is proper bullion. We ensure that anything that comes in for our customers is bullion and not Tungsten painted gold colour, that unfortunate experience that happened in Canada earlier this week. So that’s terribly important say you’ve got to ensure that you know the gold comes from proper refiner. So it’s not conflict gold. This is another thing which is becoming an increasing issue in our politically correct world. So I would when it comes to dealing with set incentives, such as some of the refiners in Dubai. I sometimes wonder what the source of that gold is. So it is important I think to to deal with reputable people. Storing gold at home does give you potential problems because if you’re careless and you let someone know that you might have an gold at home then you know you’re probably open to being robbed. And if it’s a lot of gold then you know the story gets out then you could actually be robbed by some very very nasty people. So I think that is what I would keep at home is probably fairly limited. I would actually look past having a proper vaulted gold. Physically yes I think we’re OK. But you’ve got to understand that that you don’t have possession of the gold, you have possession of a piece of paper which gives you an entitlement to some gold and you may not even have a direct entitlement to some gold because when it comes to submitting your ETF shares, well stock in return for gold usually it can only be done through authorized banks who are on the list to be able to do it. So that again is is a bit of a problem.

FRA: And your thoughts Bosko.

Bosko Kacarevic: Yeah. You know our system is a closed loop system so we eliminate any possibility of any counterfeit gold products entering our platform because it’s all done through our office. I inspect every product that goes into the vault for my clients and we are providers to the Canadian man to other gold refiners. We have direct relationships. So there’s no that gets out into the public. The the article that Alasdair mentioned regarding the Canadian Mint at RBC you know it seems there was a case I think a few years ago that they found the gold bar or counterfeit bar at a jeweler and always seems that it’s a jeweler or a pawn shop that these things are discovered. You know I haven’t experienced any counterfeit products coming through our business. I don’t think any anyone who wants to pawn off any counterfeit products would go through our business or Alasdair’s business. I’m sure that these people that are attempting this are staying away from reputable dealers because they’ve been caught right away. The Canadian Mint has issued a statement to their defence. I mean I guess we’re an approved a billion and a dealer with the Canadian Mint. So they said that that the gold product was and wasn’t even produced by the Canadian Mint in the Royal Bank is saying that they didn’t even sell their product. So how this came into being I don’t know. But I think people need to understand too that you know the the ownership contract that you own the gold and you know people have to do their due diligence in their background checks on who they’re dealing with. Because at the end of the day when you want to sell you have to make sure that you know the gold is available for you that you’re selling. So when it’s in our vault you have title ownership of the gold and even the clients that are keeping their gold at home. You know we don’t pay out to people when they come into our office right away. We have the gold inspected and we always just to cover ourselves. We tell them they have to wait 24 hours before they receive their funds. So anyone trying to pawn off a fake gold bar isn’t going to leave our office and let us inspect it for 24 hours so we’ve never come across anything like that. And I think this is an isolated incident. But I think people need to be aware of it. If the ownership contract when you’re storing your gold in a vault the title ownership of your gold is what the important thing is.

Alasdair Macleod: Richard can I just add to Bosko saying there, one advantage that you guess of having gold in a proper LBMA vault is that it should be properly insured. And we also have to ensure all our customers gold. So I think that’s a very important point. Another important point to realize is that if you take delivery if you go ahead and you want to sell it, you have to effectively make sure that you know to convince the buyer that it is authentic and that will involve it being tested. So the marketability of gold which leaves the vault is not nearly as good as gold that is kept in the vaults. I just wanted to add those two points.

Bosko Kacarevic: I agree with that it’s very important, the insurance aspect too. We have clients that are storing, some people even for a large quantity of gold and silver at their homes and it’s just too risky and then what eventually happens is when they want to sell it you know in the case of silver. People are holding a few thousand ounces of silver. It gets pretty heavy and it cumbersome moving it you know. And when it’s in the vault for us it’s very easy to identify. Each container has a specific number. I have clients you know across the country and in Europe that they just pick up the phone they call us. We sell the specific holdings and wire them the funds so that people are unable to do that when you have your gold at home and you’re travelling or you’re you want to liquidate it quickly because one of the other issues that comes about is when people call and they want to sell it. If the market’s moving fast or are very volatile I won’t lock in a price for a client unless the gold is in our office. You can’t call me. But if the gold is in the vault I know it’s there. I know the identity of it so I can lock in a price for a client over the telephone and send them the money. But if they have it in their basement and they want to lock in the price you know it’s not possible they have to bring it in person. And once it’s in my possession then we can discuss locking in price.

FRA: Now in this day and age with the advent of cryptocurrencies does physical gold still make sense? So if we look at what’s happening with Bitcoin and other Cryptocurrencies. Is there a migration of investors holding physical gold towards holding cryptocurrencies either together or as an alternative, Alasdair?

Alasdair Macleod: What a fascinating question. I think Richard the answer to your question whether there’s a migration from buying gold into buying Cryptocurrency. I think there must be. Yes. We can’t deny that. The reason I would say that is because so many people who deal in anything really don’t actually understand the underlying economics of what they’re doing. What they understand I think a trend and quite simply if you see a trend moving or speculating you just jump on the trend. So you are going to have people who will see who take the view that gold is less exciting than Cryptocurrencies, has potentially less return over at whatever time frame that they’re putting in their mind. So they will sell gold and buy Cryptocurrencies, of that I have absolutely no doubt whatsoever. What is interesting in this however and I did actually write a piece on this in I think dated August the 10th. So for anyone who’s interested if you go on to Goldmoney sites and go into research and go into the insights then you will find. August 10th I wrote “Cryptocurrency- its status as money”. Now this is very important because I won’t get through the article. Basically my conclusion is that Cryptocurrency are not money. I mean it is not just a question of volatility, its the origins of it and all the rest of it. But cryptic currencies are the media for speculation par excellence. And you know with the limited supply and all the rest of it and the fact is that so far the people who got into it are basically geeks. If I can be that rude to call them that. The hedge funds are beginning to wake up to this. The authorities are beginning to wake up to it. I mean they even bought it yesterday the CMA decided that they’re going to introduce a bit you know a Bitcoin future. Various governments have sort of taken on the technologies, some are being frightened away by the volatility in the things in it. So I think the Chinese have sort of tried to close down Chinese based operators, but basically the public has yet to buy it. And if you look at any bubble which is essentially what the Cryptocurrencies are, it’s only when the public are really into it that you can say this is time to get out. It is getting dangerous. It is going to collapse. We are some way from that. But what I can’t see is what’s going to stop these Cryptocurrency is rising in the meantime because you know if it’s becoming you just my street futures exchanges and so on and so forth you are going to get asked a lot of hedge fund type money, speculative institutional money if you like yet to buy these things. So I see them going considerably higher than this. You know please don’t hold me to that. That if you like is the theory if you like the madness of crowds as Charles Makai wrote back in the 19th century. We are seeing it and this is pure. It’s like tulips without the bulbs. I mean it is amazing. I get very unpopular for saying this by the way because everybody in Cryptocurrency is convinced it’s money, convinced it’s some sort of new paradigm. And it was ever thus, every bubble is like that everybody involved believes that this is a new future and whatever. What fascinates me you know we’ve looked at it so far in terms of Crypto versus gold, which was the basis of your question. But I think at some stage it’s going to move on from there. What we’re going to be looking at is that potential for Cryptocurrencies to destabilize paper currencies. I’m trying to get this one. Trying to get my head on this one at the moment and I’m planning to write an article on this front shortly. So this to me is a fascinating topic. It really is.

FRA: Could the momentum into Cryptocurrencies keep a lid or a cap on the price of gold in U.S. dollar terms Alasdair?

Alasdair Macleod: As a follow-up, no I don’t think so. There is actually a far bigger story going on gold and it’s all to do with the declining use of the dollar in international trade and this is something that’s being forced on to the rest of the world outside of America by China and Russia working together as head of the Shanghai Cooperation Organization. I think that we’re likely to see. I mean my information is that we’re going to get in an oil contract settled in Yuan on the Shanghai futures exchange by the end of this month, November, and between Yuan on contracts countries like Iran, who either off a bit to deal in dollars or out of their choice, would not want to go anywhere near a dollar. Will have the facility to buy gold in Yuan. And that I think is something that is likely to lead to a significant rise in the price of gold. The other thing about the price of gold is that there are an awful lot of dollars outside America. We’ve got some people running around saying well you know the American economy is rubbish and the rest of it is just going to collapse and then the end of the purchasing power of the dollar will go up. But the latest figures we have which are over a year old now is that the total portfolios in dollar cash outside America is in excess of 17 trillion dollars. That was midway through the last year 2016. It was barely changed from the level Midway 2015. My guess is that with the dollar having eased over the course of this year we will already be recording a decline in the total value of foreign portfolios, the dollar elements in foreign portfolios. Those figures will be released in next April or May. So we won’t know until then. But just imagine if you go 17 trillion dollars outside America and you have got an economy you’ve got about 19 trillion dollars GDP something like that. This is too much money outside. I think for the situation to be sustained, so I would say the dollar is weak and that is what’s going to drive gold up. And I think it is something which is independent of the Cryptocurrency story, but what does fascinate me is the potential for the Cryptocurrency is to destabilize paper currencies if you like as well. And as I said I’ve got to get my head around that before I write it.

FRA: And your thoughts Bosko.

Bosko Kacarevic: Alasdair and I seem to be in the same camp. I’ve heard actually a number of my clients who have actually sold their precious metals to purchase Bitcoins because it seems like an alternative currency. But you know it’s not officially a currency, but it seems to be operating like one. And you know judging from what’s happening, the attraction to Bitcoin is similar to the attraction to gold. It’s it’s an alternative currency outside the banking system or in government and so on. But the problem with that is is when you’re when you’re comparing it to gold. Gold is still a physical commodity. You can take possession of it. I have a problem with Bitcoin because it exists on the Internet. It doesn’t exist in the real world. You can’t take physical possession like gold or even paper currencies. So there’s a huge cyber threat to the Bitcoin. I mean I find it strange that the person who invented Bitcoin, Satoshi Nakamoto, is still anonymous, nobody knows who he is or where he came from or whatever. That kind of raises a lot of flags for me. Then when you have issues with Bitcoin or let’s say that there’s a hacker that hacks into Bitcoin who are you going to call. There’s no nobody you can sue. When you invest in a company or you buy gold and silver or invest in the stock there are people behind that. When you invest in currencies, there’s a currency broker. The government issuing the currency, there’s essentially nobody behind bitcoin. It’s operating and it exists on the Internet and apparently from what I understand it’s a series of encrypted keys. But you know I think one of the fundamental changes that Bitcoin is introducing, is the blockchain technology that it’s produced on, which I think that there’s a lot of people in the financial institutions are adopting this new form of a distributed ledger and even that’s questionable as to the advantages of that. I think the credit card companies and the banking system the the technology that’s behind their ledger entries and their software accounting systems are doing fairly well. Introducing a distributed ledger, I’m not sure what the advantages of that are, but it seems that a lot of people are attracted to it. And you know mind you people are always attracted to new things like Alasdair alluded to earlier, but you have to remember that when the Internet was introduced and people were adopting there was a lot of, along with the advantages, it brought in a lot of problems. We have high-frequency trading now. So it’s not always a great thing to not have a central authority. In some cases, you want to have a central authority to be the mediator between two parties. So I’m still sceptical about Bitcoin. Obviously, it’s doing very well on a price level but on a value level. You know I still have a lot of reservations about investing in it, but currently, the CMA group thinks that the futures contract would be in demand and people will have the opportunity to hedge their risk in Bitcoin. So for me, it’s too early to get in. I’d like to see how it develops.

FRA: And I saw today an article by Jim Rickard’s on a new research report out by Goldman Sachs discussing this very issue of gold versus Cryptocurrency. Goldman Sachs appears to be leaning on the side of gold. Well as a preservation of purchasing power. They mentioned that Cryptocurrencies are vulnerable to a hacking, government regulation, and infrastructure failure during a crisis. Those are issues of concern and because of the volatility in Cryptocurrencies, they still see gold as preserving purchasing power better than Cryptocurrency, so that those are the results of the research report by Goldman Sachs and any thoughts on that and. Your final thoughts there.

Alasdair Macleod: Well I’d go along with what Goldman Sachs have concluded. I haven’t read their report, I must say, but as you’ve described it it’s hard to disagree with it. But I don’t know. I know that for people who are trading in it, this is all sort of a big issue. But from an economic point of view there is no doubt about it. Gold is money, always has been money whereas Cryptocurrencies are not then merely a medium for speculation. But you know we don’t actually care about that. Perhaps we always say is Bitcoin going up and we’ve got to get in there or in theory or whatever. We’ve got to go and buy it you know because you can’t stand aside and not buy these things. And this is why I think it’s terribly important to understand that actually it is just a whole load of hot air and nothing else, but this balloon I think, if I’m reading market correctly it is in the early stages rather than the final stages of its inflation. And as I said, I mean so far the people who got into it all the people in the know if you like the people who have been following this story from the outset, the early adopters, the institutions yet to get in. And I think that I mean this is this is the thing about the CMA contract it doesn’t settle in Bitcoin at all. All it does is it uses that bitcoin as a reference price. So that’s actually not going to be anything like gold futures contract where the gold is actually deliverable. This is a very very different thing. So I can’t see really that there is going to be the arbitrage between the futures contract and Bitcoin. I can see how that’s going to happen because there’s nothing deliverable. So that is not going to take demand out of the Bitcoin story so much I don’t think as inflating the number of gold contracts in outstanding on Comix definitely takes demand out of the gold market. So to my way of thinking, you know the the the institutions have yet to get into this. They will get into it because these new instruments look like you know go into contracts themselves so forth are beginning to take place. I think the other thing that’s going to happen is that the regulators are going to come in and insist that anyone maintaining accounts for people with Bitcoins or other Cryptocurrencies are going to have to do their due diligence. And I think the industry as a whole itself is likely to turn round and think we’ve got to clean up our act to make ourselves mainstream. I think all that is still ahead of us. And then you know when you think about the public investing in this, investing is the wrong word, speculating is probably better word, they think they’re investing. This is not just a bubble let’s say in the Shanghai stock market or you know if we go back to the tulips in Amsterdam that’s what 1640s or whatever it was all the Mississippi bubble which was France or the South Sea bubble which was which was England and most particularly, not just you know I mean just sort of England within coaching distance of London. That was the source of this. We’re talking about something that is catching the imagination globally and I mean already we’ve got so many imitators I think there are over a thousand Cryptocurrency I read somewhere. Where is proper paper currencies or something like a 170 only so already we’re you know there’s a lot of funny deals being done around in these icy roads and all the rest of it. This is an act which if it gets cleaned up and they will try and clean it up I’m sure that they will though try and clean it up. They the authorities will want to see cleaned up because they want to tax it apart from anything else. And the other thing is I think that the industry itself will want to see it cleaned up and that will open the gates for everybody to get involved. This is this is a theoretical bubble for any student of psychology in the future. They’re going to look back on this as an absolute wonderful example of a pure speculative bubble which is totally out of thin air.

FRA: And your final thoughts Bosko.

Bosko Kacarevic: You know when you compare the standard deviation of gold versus Bitcoin, I read a report recently that over the past 12 months’ gold has had a 12 percent deviation, where a big coin is over 60 percent. So you know I agree that it is a speculative instrument. It’s going to be quite volatile and the attraction of many people to Bitcoin to elude the financial markets. I think that’s going to be taken care of with the regulators are going to get involved obviously to see him now as is adopting it. So this idea of people being able to have a peer-to-peer and to trade outside of regulation or the government size. I think that’s just an illusion because of you ultimately you have to settle these Bitcoins for currency that’s going to be used in the real world. And you know you have to receive it in a bank. It has to be wired from whatever Bitcoin exchange or so there’s going to be financial institutions involved, regulating it. So I mean is it going to go up further. It’s very possible. I mean I think it is in the early stages and you know it’s it’s going to go through the process like anything else that’s brand new. It’s going to weed out the all the weak currencies and will Bitcoin be the winner in the end. I don’t know. Maybe a theory or the other thousand that are available. Who knows how it’s going to turn out, but there is definitely an attraction to it. And it seems to be distracting some gold investors are distracted and selling their gold and silver for Bitcoin and I disagree with it. But you know people like to follow trends and in some cases, they’re going to have to experience the negative part of following a trend and being wrong. So I don’t really know what’s going to happen but it’s interesting it’s a new technology and we’ll have to see.

FRA: OK great. Great insight gentlemen. How can our listeners learn more about your work, Alasdair?

Alasdair Macleod: Well the easiest way is to have open an account Goldmoney, no, but on Goldmoney site I write weekly is published on Thursdays I usually say if you look if you go onto the site, Goldmoney.com, research and then insight, you’ll find that. I also write a weekly market report and that again can be found under the research column.

FRA: And Bosko?

Bosko Kacarevic: People can reach me at our Website at Kindigo.com and you know on there this information about our company, my background, and they can email us through there. We don’t do a call in, but we do keep in touch with our clients and keep them up to date on what’s happening in the gold market.

FRA: Great thank you very much gentlemen for your insight. Thanks for being on the program show.

Submitted by Boheira Manochehrzadh <bmanoche@ryerson.ca>

10/27/2017 - New Zealand Bans Foreigners From Owning Property – Is Canada Next? 10/27/2017 - The Roundtable Insight: Charles Hugh Smith On Will The Private Sector Be Able To Grow Fast Enough To Meet The Demands Of The Public Sector?

10/27/2017 - The Roundtable Insight: Charles Hugh Smith On Will The Private Sector Be Able To Grow Fast Enough To Meet The Demands Of The Public Sector?FRA: Hi welcome to FRA’s Roundtable Insight .. Today we have Charles Hugh Smith. He’s author leading global finance blogger and philosopher, America’s philosopher we call him. He’s the author of nine books on our economy and society including “A Radically Beneficial World Automation Technology and Creating Jobs for All”, “Resistance Revolution Liberation a Model for Positive Change”, and “The Nearly Free University in the Emerging Economy”. His blog of twominds.com has logged over 55 million page views. It is number seven on CNBC top alternative finance site. Welcome Charles.

Charles Hugh Smith (CHS): Thank you Richard. Always a pleasure to join your roundtable.

FRA: Great. And with that today with the focus on the sort of tension between the private sector and the public sector with many types of revolutions, technological revolutions happening in the in the private sector you know in terms of block chain and biotech, energy environment, lots of revolutions happening much like what happened with the with the Internet.com revolution. And the question is will that growth in the private sector be able to to meet the challenges of the public sector in terms of seemingly unsustainable growth and that growth in Entitlement programs. Dr. Albert Friedberg of the Friedberg Mercantile Group recently observed that in the U.S. it’s basically 10 percent of GDP and rising for entitlement programs. So you know that’s the big question. Your initial thoughts.

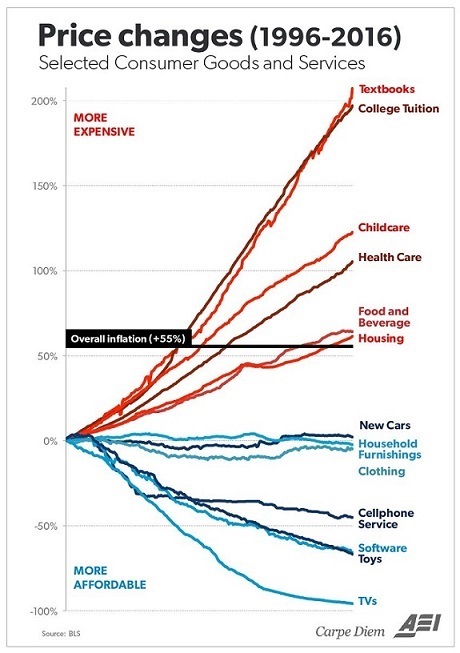

CHS: Well Richard I think that’s an excellent context for you know the points we’re going to make. And one of the first points I would start with is ultimately the public sector in this state what we call the state all all layers of government and government related entities. They all live off the private sector right. That the private sector has to generate surplus. It has to generate wages for employees and those are taxed by the public sector and that’s the source of the public sectors revenues. And so what we’re really kind of discussing is can the public sector generate enough profit and employment to support this fast ballooning public sector. And you mentioned the entitlements growing by 10 percent. And I have this chart of consumer goods and services.

The price changes what what we might call inflation. But it’s actually not. Not entirely inflation it’s it’s the cost of services being provided and how far above or below they’re rising then like people’s wages which household incomes as we all know if and stagnating for somewhere between 40 years and 10 years and depending on which sector of the economy you’re looking at. But we look at what is soaring in price and we look at like 200 percent increases and we find out it’s college tuition and we look at what’s climbing at a 100 percent or or more and it’s like health care and child care. And of course these are the sectors that are heavily controlled or are funded by by the public sector. And what we find is declining in price is cell phone service, software, TVs the kind of things that the private sector provides. So it’s pretty clear when you have competition and when you have exposure to innovation then you get it lower prices or at least you get more for your money. Or there’s there’s hope that innovation will impact the consumers, either the quality of the goods and they’re receiving or the price of the goods and services they’re receiving. So to sort of summarize everything that the public sector controls is skyrocketing in price and the quality is also now suspect right.

Like I’ve written a lot about higher education and I have another chart here showing that literally all of the the the higher education student loans that are being issued are actually funded by the federal government. So it’s it’s actually the federal government is funding these private sector lenders and guaranteeing them profits to fund these students getting diplomas which are declining and real world value. You know in terms of statistically what the earnings are of college graduates and so on that that’s been stagnating just along with the rest the wages. So I would propose that higher education is actually declining in its utility and value despite the cost soaring and many other people would make the same claim about health care at least in the U.S. Is that the cost keeps soaring but the actual you know measures of health of the American population are continue to decline. So this is a really striking difference. I think that’s really what we’re talking about is an enormous difference between the sectors controlled by the public sector and those controlled by the private sector.

FRA: Yeah you’ve written a lot about that in terms of several industries being sort of cartelized, you know with special interest group, lobbyists and just the interest by the government in them. Can you elaborate a bit on that?

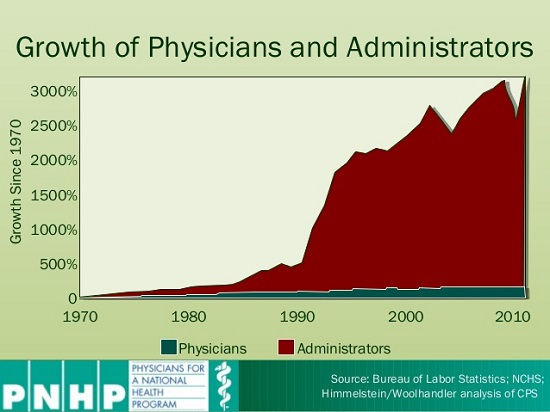

CHS: Yeah I think that’s a great topic. If the public sector controls something like health care which in the US is dominated by the public sector programs: Medicare, Medicaid, and the Veterans Administration. Then the way to maximize your profit is to lobby the public sector, lobby the government agency, to lock in your cartel pricing. And so that’s what we see is that we see these pharmaceutical companies routinely raising prices 30 40 percent or even 400 percent just on a random basis that they make no claims that they’ve invented something new. They simply raise the price on an existing medication and the public sector also imposes a lot of regulations that some of which are of course important and necessary, but many of which are simply you know churn you know they just create more work, but they’re not really creating that not really impacting the patient in any in a positive way.

So I have a chart here of the growth of physicians and administrators in the health care system. And we see that the number of physicians has been flatlines for like 40 years where the growth of administrators from about the early 90s on has has ballooned up like 3000 percent. And so this is there’s no way that a private sector company could could bloat its management by 3000 percent and get away with it unless its revenues and profits were rising even faster.

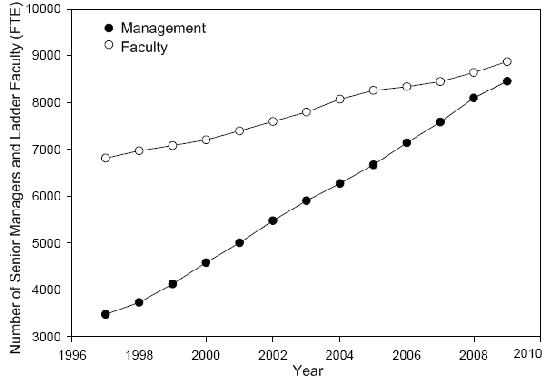

And we see the same thing and I have a chart here of the faculty and management of the of the University of California system and it shows that while the faculty has risen slightly over the last 30 years from about 7000 to about 8500 the number of administrators has risen from about 3000 to like 7500. So we have these enormous ballooning of bureaucracies and all of which are really highly paid positions. And and yet where is the output. I mean where’s the gain in quality or any output. And of course there isn’t any. None that we can measure.

FRA: And associated with this involvement by government is an increase in government debt. And if you look at just debt in general in recent years in the developed world it’s taken more and more new debt to create $1 in GDP. I mean the figures are something like $4, of between $4 to $18. I’ve seen some estimates of new debt to create $1 in GDP. Your thoughts on that.

CHS: Right. Right. And I just read a report from a blog that showed that China has the same similar, very strong diminishing returns on its vast expansion of debt. That it’s expanding debt at rates that are multiples of its GDP growth. And so it’s also the case that even in the developing world the same diminishing returns that you describe is that is the dominant reality. And of course we have to ask why is there such a low efficiency or low productivity rate to this new debt. And and it’s because there’s no there’s no pressure of innovation and competition on how the governments are spending this money. And so there’s really no adaptive pressure in terms of natural selection for them to find more efficient ways to do whatever it is they’re doing. Right. The pressure simply to raise more revenues. And if they can’t do that then to borrow more money and this is where financial repression comes in because the only way the public sector can keep adding debt and it’s at this fantastic clip is to lower interest rates to zero or near zero. And create all these perverse incentives for speculation that we’re seeing now as a result of that manipulation if you will or intervention to keep interest rates low enough so the public sector can keep borrowing and borrowing and borrowing, you know to infinity.

FRA: Any ideas on what the endgame could be here if we consider the level of debt and the level of interest rates for the two lever’s, you know with rising debt at some point even small increases in interest rates could be disastrous. I mean where does this all end.

CHS: Right. Right. I just saw a statistic which I can’t verify of course but it sounds fairly close to me. Somebody said that the point six percent rise in the U.S. Treasury yields. That’s a kind of recent rise in one part of the Treasury bond yield spectrum generated 1.7 trillion dollars in losses right then and there you know just a relatively modest increase in only one part of the total global bond market created almost 2 trillion in losses. And so yeah if we extrapolate the possibility of of interest rates going up two or three percent then you’re talking about losses that could be in you know 10 trillion and up in the bond market and then of course as yields rise historically people sell stocks with low dividend yields and high risk. And then if they take the benefit of a higher yield in bonds and so stock markets tend to go down when interest rates go up as well. So we are the end game there is can they can they keep creating debt at a fast enough rate as the returns on that debt continue diminishing. And by some measures as you know that some people feel the return is already negative, like there is by the time you include debt service and other factors than actually we’re losing ground here. So eventually that will erode the the real economy. And I think that’s that’s really what we’re talking about here is can the public and the private sector outgrow the debt that’s being piled up by the public sector.