Special Guest: Jordan Eliseo – Chief Economist, ABC Bullion, Australia

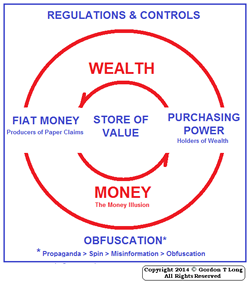

FINANCIAL REPRESSION

“The subsidizing of debtors and the attempt to provide essentially a fake support for asset prices – while punishing savers and mis-allocating capital!”

“In Australia we have some of the highest debt levels in the world. Some people in Australia like Financial Repression because it is making it easier for them to pay off their mortgage (or at least afford their mortgage). The flip side is retirees, or people trying to live off fixed income and the like, are finding life very very difficult now because they have taken a very significant “pay cut” on the income which they were able to earn on the capital that they had been able to save throughout their working lives.”

WHAT’S DIFFERENT IN AUSTRALIA?

“Australia is effectively “catching down” to the rest of the world. – it is approximately four to five years behind western word.”

“Australia was incredibly fortunate the first time around to. We had a huge stimulus from China which lead to quite literally an unprecedented boom in capital investment in our mining sector. Trades stayed incredible strong because iron ore, coal prices and even gold was supported from a long time. Also because even at this point Australia has a a government debt level that is still quite manageable”.

“Imbalances have continued to build over this period and now that the mining boom is over, iron ore prices are closer to $60 dollars (not $160) and capital investment is drying up – we are finding we don’t have anything to re-balance to with private debt levels preventing any real pickup in consumer spending in any meaningful way!”

“Australia is about to enter a fairly serious “lull”‘

EXPECT DECLINING STANDARDS OF LIVING

The next phase in Australia that Jordan Eliseo expects “is where people begin to lose faith with Central Banks and start to more fully appreciate the complete lack of connection of what is going on in the real world / real economy and what is going on in asset / financial markets.”

“I think that when that happens financial markets have a lot of “catching down” to do!”

“The road that the government and central banks have led us down is actually a road that is going in the wrong direction! Standards of living are going to continue to decline as we go down that road and it is going to be a very difficult period for investors and individuals just trying to maintain their standard of living.”

WALL STREET IS DISCONNECTED FROM MAIN STREET!

“The end result of current economic policies have caused the disconnection (between Wall Street and Main Street). You can understand the emergency measures that were taken during the financial crisis but all it has done is fuel rampant asset speculation. We haven’t seen any meaningful growth in corporate capital investment or a rise in full time job creation (with a real living wage).”

“If you look at what is happening around the world we are seeing the prioritization of asset speculation over actual investment. It is impacting everyone from individuals, to CEOs, to Boards in making decisions around dividends / stock buybacks versus investing in their own operating businesses!”

“People in Australia on paper are more wealthy because their house price keeps going up, but they have less money to spend because the money they earn on their term deposit & savings continues to decline!”

… and much, much more in this 36 minute VIDEO interview on global macro issues …

- Why the Central Bank play book is very clear for investors,

- Why we will see a growing appetite for Precious Metals & why it is now imprudent not to acquire some element of precious metals within portfolios,

- Why we have $5T in Negative Nominal Sovereign Bonds,

- Why Superannuation is the only investment for 22M people in Australia,

- Why lower interest rates are ahead for Australia,

- Why Financial Diversification. Liquidity and Internationalization have become so important.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/19/2015 - Financial Repression Obfuscation: Measuring Inflation

06/19/2015 - Financial Repression Obfuscation: Measuring Inflation