10/10/2015 - Financial Repression In China: Capital Controls

Article highlights new financial repression measures by China – annual limitations on cash withdrawals outside China on China UnionPay bank cards .. Cardholders, under the new rules, may withdraw a maximum 50,000 yuan ($7,854) in the last three months of this year & a maximum 100,000 yuan next year .. “The new rules could be the first in a series of measures leading to draconian prohibitions of transfers of money from China. Draconian prohibitions, in turn, could spark a global panic.” .. the article says the global financial community has been focusing on the wrong crisis in China – “Beijing’s efforts to prevent the collapse of equity values by massive purchases of stocks have received wide publicity since early July, but these purchases do not pose an immediate challenge to China’s technocrats.” .. the big crisis is about the currency – with outflows/inflows relating to the depreciation or appreciation of the currency .. “Beijing now finds itself in what looks like a no-win situation. If it does nothing, cash will continue to gush out of China. If, on the other hand, China acts to stem the outflow, it could make an already bad situation worse. Actions that are too radical can create a panic. Moves not radical enough will probably hasten outflows because holders of cash will think they have only a limited opportunity to transfer their wealth to safer jurisdictions. At this late date, confidence is eroding quickly, and China’s technocrats are finding their options narrowing and prospects dimming.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/09/2015 - Leland Millar Talks Quality of China’s Economic Reporting

Special Guest: Leland Millar – President, China Beige Book International

FRA Co-Founder Gordon T. Long interviews Leland miller, the president of the china beige book international and discusses financial repression in the context of the Chinese economy. He describes himself as a Lifelong china watcher who decided to do something about the complete lack of data in china.

“One of the things that the china beige book plans to do is to give people a real picture of not just the growth dynamics, but also the labor market, the credit dynamics, the macro implications of Chinese growth, indications of future Chinese demand, implications of commodity markets around the world, we try to give the people a much better picture on what’s actually happening instead of just relying on official data and press release”.

FINANCIAL REPRESSION

Leland describes the Chinese reform as a reversal of financial repression and this repression in the context of the Chinese economy is the oppression of consumers and households by state organizations through its economic systems.

“It means reversing this long time economic model, where the state will profit through the economic system at the expense of the consumers and household, and one of the things that the new leadership is intent on doing in order to create consumption is to empower consumers, so they spend more and stop empowering state organizations which are fuelling the overcapacity and the massive debt bubble”.

What should investor know about china?

He explains the biggest misconception concerning the Chinese economy is believing the GDP tells you much about how china is doing.

“It is a broad, blunt indicator that doesn’t measure productive growth or credit dynamics”.

On some of the challenges of getting reliable data in china, Leland explains that he and his team had to ask Chinese firms and consumers on ground what is happening in the country, and set up a number of polling units across sectors in order to get reliable and accurate information.

Economic trends in china

“For years we have been talking about the Chinese slowdown; it’s inevitable, despite the fact that the economy has been slowing”.

He goes on to explain that although the market sentiment has gone from optimism to “Armageddon” in recent months, the actual data is at odds with these sentiments. As a result of china’s economic slowdown, there is great vulnerability among emerging markets. Now, the reason for this is that for years these markets have relied on china’s demand without factoring the likelihood of a decline or certainty of a decline in china’s demand.

On China’s view of America, Leland has this to say

“The Chinese look at America as a model that they are interested in taking pieces from; they like the dynamism of the economy and the global status. On one hand, they see us as a model to learn a lot of things from but also as a serious threat that is looking to constrain their inevitable and ultimate rise”.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/04/2015 - The Financial Repression By The IMF: Risks To Your Investments And Retirement

International asset protection specialist Mark Nestmann does not see free markets – rather he identifies the unintended consequences of financial repression in progress by government authorities & the IMF in particular .. gives the example of what China is doing to prop up the markets now – “Their playbook comes from the International Monetary Fund (IMF), which advises governments to engage in ‘financial repression’ to buoy up global markets. The IMF’s recipe to avoid what former Fed Chairman Ben Bernanke calls ‘chaotic unwinding’ includes bail-ins, higher inflation, negative interest rates, and capital controls. The IMF even proposes a ‘one-off capital levy’ – outright confiscation of private savings – at a rate of 10% or higher. But as world markets have demonstrated over the last few weeks, it doesn’t always work. The cause of this chaotic unwinding is excessive debt combined with leveraged bets financed by more debt.” .. the international economy is beset with massive levels of debt – “collateralized, re-collateralized, hypothecated, and semi-hypothecated. Total world indebtedness now stands close to $200 trillion. That amounts to 286% of the global GDP of $70 trillion.” .. Nestmann says financial repression only works as long as the targets – individuals, families, & businesses – don’t catch on .. Nestmann points out many of the world’s wealthy are investing in real physical assets, no financial assets, stored outside of the banking system & internationally, .. these are assets that cannot be “bailin in, hypothecated, or hyper-hypothecated.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/04/2015 - Financial Repression: The Fallacies & Distortions Caused By Central Banks

Taking an Austrian School of Economics approach, Mark Spitznagel just made a billion dollars a few weeks ago & explains the fallacies & distortions being caused by central banks – the unintended consequences of financial repression .. “Great myths die hard. And I think what we’re witnessing today is the slow death of one of the great myths of human history: this idea that centrally planned command economies work, that they’re even feasible, and that they can be successful. It’s one of these enigmatic mythologies of the last hundred years in particular that we’ve been grappling with, and here we are today yet again thinking about this. Let’s remember that in the last hundred years a lot of blood has been shed over this mythology. And here we are today, how did we get here again? .. I think that another generation will look back and say ‘how could you have made that mistake all over again? How could you have failed to understand Hayek’s notion of the fatal conceit, that central planners can’t do better than the dispersed knowledge and signals of free market processes?’ .. When bureaucrats mandate low interest rates it doesn’t spawn long term productive investment. What it spawns is this short term gambling, punting on momentum-driven moves, on levered buybacks. This is the world we’re in today.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/04/2015 - Repressed Interest Rates Cannot Perpetuate A House Of Cards

Free market economist Richard Ebeling points out that when adjusted for inflation, the Federal Funds rate set by the Federal Reserve & also one-year U.S. Treasury not yields have been negative for the last several years already .. “It has cost little or almost nothing to borrow funds in the American financial markets, courtesy of the former chairman Ben Bernanke and current chairwoman Janet Yellen and the other members of the Board of Governors of the Federal Reserve, who possess the monopoly manipulation authority over the quantity of money in the banking system.” .. highlights how the U.S. government has added $8 Trillion to the federal government’s accumulated debt since the financial crisis – “The cost of U.S. government debt payments would be far greater if the Federal Reserve had not kept interest rates artificially low and created the illusion that the interest cost of government borrowing can be almost ignored.” .. these repressed interest rates (financial repression) have caused malinvestment, mispricing of assets & risk, & shafted savers & retirees from earning interest on their savings .. “A healthy restoration of actual market stability and coordination between savings and investment, between supplies and demands, requires an end to the monetary expansion and the reemergence of market-based interest rates that can tell the truth about the availability and cost of borrowing money and the real resources they are supposed to represent, so investments undertaken stay within the bounds or types and time-durations consistent with the saved means of production upon which they are dependent .. While the Federal Reserve has chosen to keep the Federal Funds rate near zero, it is merely delaying the inescapable and inevitable result of its own monetary policy – another needed economic correction that its actions will have generated but which it will, no doubt, blame on the supposed ‘failures’ of the market economy.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/04/2015 - Axel Merk: Financial Repression Could Lead to War

Axel Merk calls upon central banks to abolish their 0% interest rate policy (ZIRP) framework before more harm is done .. “ZIRP is bad for all stakeholders and may even lead to war” .. ZIRP is bad for business – “creative destruction may be undermined through ZIRP” .. ZIRP is bad for investors .. ZIRP is bad for Main Street .. ZIRP is bad for price stability .. ZIRP is bad for peace .. “We believe the key problem many countries have is debt .. The Great Depression ultimately ended in World War II. I’m not suggesting that the policies of any one politician currently in office or running for office will lead to World War III. However, I am rather concerned that the longer we continue on the current path, the more political instability will be fostered that could ultimately lead to a major international conflict .. The Fed needs to have the guts to tell Congress that it is not their role to fix their problems. It requires guts because they must be willing to accept a recession in making their point.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/02/2015 - Paul Craig Roberts PhD Talks About the Alarming Decline In Western Democracy

Special Guest: Paul Craig Roberts PhD – Chairman of the Institute for Political Economy

FRA’s Gordon T Long talks financial repression and the decline in democracy with Paul Craig Roberts. Paul is the chairman of the institute for political economy, he was also the former assistant secretary of the US treasury for economic policy in the Reagan administration.

“As far as I can tell not only has democracy departed the western world but also compassion empathy for others, morality integrity respect for truth justice fairness self-respect western civilization has become a hollow shell there is nothing left but greed and coercion and the threat of coercion”.

He believes this outcome is based on the behavior and statements of the government and the public’s acceptance of it. Part of the reason the public doesn’t care, is due to a lack of information as about 90% of the American media is owned by 6 large mega corporations that manipulate the news.

“The story that is told by the American media is Washington’s propaganda line and of course whatever the corporation’s propaganda line is and there is no challenge to either”.

On the republican debates, Paul questions the aggressive stands that most of the candidates seemed to have towards foreign policy. He states that this stand will simply create distrust among nuclear wielding powers.

“Every American president since John F Kennedy worked with the soviet leadership to diffuse the nuclear issue”.

He says that this shift in culture across the candidates is a combination of both campaign finance and a shift in culture.

“There’s no such thing as a free market in the United States, it requires many producers none of which can affect price…….look at the banks, the banks are so concentrated that they are too big to fail. How do you have capitalism if a failed enterprise doesn’t close down instead it is bailed out by the people or by the Federal Reserve printing money to buy its worthless portfolio. This not capitalism, there’s no capitalism here, this is an oligarchy!”

“What has the government said that’s true? Think of anything, can you think of anything they’ve said that’s true? We know that the unemployment rate they’re reporting is false, inflation rate is false, and the gross domestic product is false. We know all of this, we know that Saddam Hussein did not have weapons of mass destruction, he did not have Al Qaeda connections, that Assad of Syria did not use chemical weapons. We know Russia did not invade Ukraine but they say this over and over and over. I can’t think of one thing that the government or corporate world has said in 20 years that’s true”.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/02/2015 - Jeff Davis Talks Financial Repression & the Effects on the US Banking Sector

Special Guest: Jeff Davis – Managing Director, Financial Institutions Group, Mercer Capital

FRA Co-Founder Gordon T. Long interviews Jeff Davis of Mercer Capital, and discusses financial repression and its effects on the banking sector.

Davis is currently a Managing Director of Financial Institutions Group at Mercer Capital. Davis also provides financial advisory services primarily related to the valuation of privately-held equity and debt issued by financial services companies and advisory related to capital structures and M&A.

FINANCIAL REPRESSION’S EFFECT ON THE US BANKING SECTOR

“Financial repression is a price control that relates to all facets of the economy and has profound impact.”

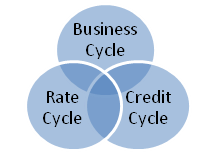

The 3 major cycles: Business Cycle, Credit Cycle and Rate Cycle.

“The banks straddle all 3 to be a key contributor of capital in the US economy. Financial repression impacts at a very base level for all 3 cycles.”

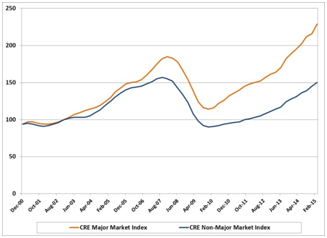

“Financial repression has artificially pumped up asset value.

“Commercial real estate values really pivoted in 2010. There is additional risk in the system now that asset values are pumped up”(See Chart to Left)

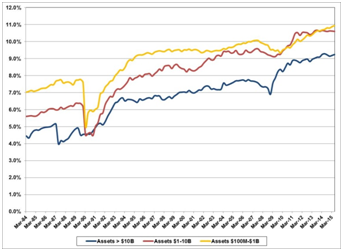

Leverage Ratio

“If you look at the leverage ratio we can see that over the last 20 years the industry has been raising capital. I don’t think that’s a bad thing. We are significantly much better capitalized than Europe which is a good thing, but as it relates to an investor there is a lower return on equity.”(See Chart to Left)

“Regarding financial repression, if you think about interest rates today, it is very painful for an institution to hold cash. There is significant risk taking occurring amongst commercial banks in taking additional credit risk and duration risk. Structurally banks aren’t as spread in terms of their assets relative to their borrowings that fund these assets.”

“Companies don’t go broke because they don’t make money. Companies go broke when they have no liquidity, so what financial repression has done is push liquidity into the system. So now heavily indebted companies are able to borrow money and we will soon see the consequences of that.”

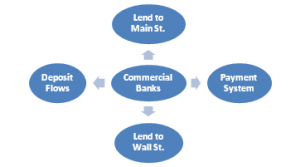

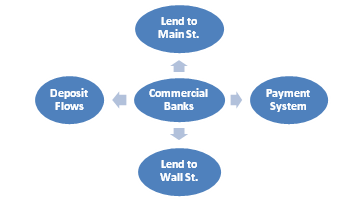

HOW BANKS FUNCTION

“The banks are special for being separated from commerce.”

“The objective for a bank is to earn a spread on assets. Loans being the highest yielding asset, followed by bonds, and finally cash. The banks role is to take the deposits and prudently while still taking risk, lend the money into the economy to help finance the economy.”

SHADOW BANKING

“Over the last several decades the shadow banking system has developed into an alternative lender as well as another place for people to put their money.”

The term “shadow bank” was coined by economist Paul McCulley in a 2007 speech at the annual financial symposium hosted by the Kansas City Federal Reserve Bank in Jackson Hole, Wyoming. In McCulley’s talk, shadow banking referred mainly to nonbank financial institutions that engaged in what economists call maturity transformation.

Commercial banks engage in maturity transformation when they use deposits, which are normally short term, to fund loans that are longer term. Shadow banks do something similar.

“Shadow banking system is separate from commercial banking system, but is a very large piece of the credit allocator. A lot of risk has been pushed out of commercial banks and is now in the shadow banking system, where it is not as opaque as a commercial bank.”

CONCERNS WITH SUSTAINED LOW INTEREST RATES

One day there will be a reckoning. It’s simply a buildup of risk; an attempt by central authorities to guide the economy.

Malinvestment: A mistaken investment in wrong lines of production, which inevitably lead to wasted capital and economic losses, subsequently requiring the reallocation of resources to more productive uses.

“A delay of lost recognition and mass malinvestment which is all a credit risk within the banking systems. However, my biggest concern is a dramatic slowdown in the economy, short rates at zero.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/25/2015 - Don Rissmiller – The Biggest Fed Meeting Since 2008 In Terms of Expectations

Special Guest: Don Rissmiller – Partner & Chief Economist, Strategas Research Partners

FRA Co-Founder Gordon T. Long talks Financial Repression and current economic developments with Don Rissmiller, a founding partner and chief economist of Strategas Research Partners. Mr. Rissmiller has overseen Strategas macroeconomic research since 2006, as well as thematic research, and high frequency econometric forecasting.

“When we think about financial repression, we think about interest rates being below normal levels or below inflation. You would do that if you’re in an environment with a lot of debt. The solution if you have too much debt is to try to make the burden of that debt to decrease.”

Rissmiller highlights the 3 avenues in which the government receives funds through taxes. Taxing income, taxing transactions, and taxing wealth; however financial repression relates by,

“Keeping interest rates below inflation is a fancy way of taxing liquid wealth, taxing cash.”

THE RESULT OF LOW INTERST RATES

“You’re trying to stimulate the economy by implementing lower interest rates.”

The financial repression process begins at the monetary policy level as a response to some shock In the economy. The goal is to get risk taking up in the economy, and that’s complicated with monetary policy because it is not the best policy when it comes to risk taking,

“It may be the best you can do, it may be an appropriate policy response in a time of stress, but it still has consequences that may not all be desirable.”

When you think about where we are going, what you can do is use whatever works. “You have to force other investors to take more risk. You might bid up asset prices, and of course assets are not equally distributed so that has consequences for income inequality.”

THE SEPTEMBER 17th FOMC MEETING

“It was the biggest fed meeting since 2008 in terms of expectations”

The Fed took the approach that they would like to wait a little more and see some more data. This is not uncommon, if we look back to 2013 to see an example of this, the Fed started talking about the quantitative easing taper in the middle of 2013, and by Sept 2013 the expectation was they were ready to go, but they held back for 3 more months because of the tightening of financial conditions.

“This is a reasonable way to look at what will happen in September of 2015, a tightening of financial conditions plus data that wasn’t equate to have confidence in your forecasts leading the Fed to delay.”

FORECASTING THE US ECONOMY

Considering the global slowdown in world trade and commodity prices, Rissmiller shares some foresight into the potential future of the American economy.

“We are seeing weakness in manufacturing that means another sector will have to pick up the slack. The sectors I will focus on are housing, consumer, and the government.”

“In housing we are seeing some improved signs on household formation. As unemployment is looking more normal we have had more household buying.”

“Consumer spending has been growing, we think this can continue because the decrease in energy prices tends to effect consumer spending with a lag and so we are going to continue to see positives to lower energy prices.”

” The government sector has been a drag, there is still one more budget fight coming in the next few weeks and that’s going to be a challenge, but if we get through that we are into the part of the election cycle where government drag turns into a small boost, we are already seeing some rehiring at the state and local level and that is significant as well.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/25/2015 - Stewart Taylor Discussing Financial Repression with Eaton Vance VP

Special Guest: Stewart Taylor – Vice President, Eaton Vance & Senior Fixed Income Trader

FRA Co-Founder Gordon T. Long breaks down financial repression and the future of emerging markets with Stewart Taylor. Stewart is currently Vice President and Portfolio Manager at Eaton Vance Management based in Boston, managing the Short Duration Real Return Fund since 2005.

THE SEPTEMBER 17th FOMC MEETING

“I am sure the Fed is going to move, the Fed knows they have to get away from zero bound.”

To Taylor, financial repression is keeping interest rates below a considered normal level. When asked about the recent FOMC meeting, he had this to say…

“They missed a chance in 2013 to raise rates, they had a free shot at it and they didn’t do it. I think they had a free shot at it again this past month, they didn’t take it, and now it becomes harder as we go along. Particularly, given what we are seeing happening in emerging markets.”

A progressive opening up of more countries to foreign investors has been accompanied by major structural transformations in many parts of the world. Strong economic growth combined with the development of financial markets has led to the expansion of investment opportunities in emerging markets and has reshaped the equity sector.

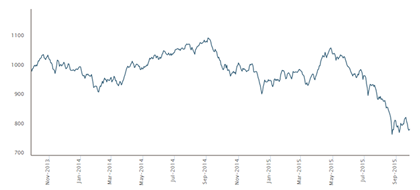

The graph to the left shows a dramatic drop for emerging markets performances of this September. The decline is Indicative to what Taylor had to say regarding the meeting…

“After hearing what the fed said, I don’t think the market feels the Fed has much confidence in the economy right now.”

THE COMMODITY SECTOR

“I am looking for ways to own commodities now.”

When asked about the commodity sector in emerging markets, Taylor states

“Commodities have been going down for the past 3 years while equities have been increasing or staying in the long trading range. I think it is evidence that perhaps equities have become somewhat divorced from the real economy. I certainly think that commodities are more indicative of the economy than equities are. “

THE FUTURE OF BOND MARKETS

Is a shift in the bond market inevitable?

“I do think a shift is coming, but I think the one thing that happens with rates that not many people appreciate is that first of all there is a difference between how rates behave in an inflationary environment, and how they behave in a deflationary environment.”

“I think at some point an abrupt shift will happen, but if you look historically you see that these changes take sometimes decades to complete.”

THE BRICS

“I am a firm believer that too much debt pushes down economic growth, and we are in a world that is constrained by debt and that isn’t going to change anytime soon.”

Taylor compares China’s equity market to America’s; both are very similar, China’s is just multiplied by a greater degree.

“Their equity market isn’t well connected to the underlying economy, so that’s why I dismiss equities as a signal. “

“You look at countries like Brazil that are being hurt by corruption, that’s hugely concerning considering how large of a role Brazil plays in the emerging markets. The BRICS, with the exception of India have all had a really rough time as of late and I don’t see that changing anytime soon.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - BCA Research Chief Economist Martin Barnes: “Financial Repression is Here to Stay”

BCA Research’s Chief Economist Martin Barnes sees financial repression as “here to stay” for the long-term, given the challenges of low economic growth & high debt globally .. Barnes has written a special report to explain why debt burdens are moe likely to rise than fall over the short & long run given demogaphic trends & the low odds of another economic boom .. BCA Research: “If governments cannot easily bring debt ratios down to more sustainable levels, then the obvious solution is to make high debt levels easier to live with. This can be done be keeping real borrowing costs down and by regulatory pressures that encourage financial institutions to hold more government securities. In other words, financial repression is the inevitable result of a world of low growth and stubbornly high debt.Martin argues that central banks are not overt supporters of financial repression, but they certainly are enablers because they have no other options other than to keep rates depressed if they cannot meet their growth and/or inflation targets. A world of financial repression is an uncomfortable world for investors as it implies continued distortions in asset prices, and it is bound to breed excesses that ultimately will threaten financial stability.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - Beware Of Digital Assets Like Brokerage Accounts and 401Ks Jim Rickards Prefers: Silver, Gold, Fine Art, Rare Stamps, Cash, Other Physical Stores Of Value, Private Equity

Jim Rickards shares the key points & themes of his conversation with U.S. 4-Star General Michael Hayden who is the only person to have been director of both the National Security Agency & the Central Intelligence Agency .. the discussion is on financial warfare & where it is happening today .. thoughts on the financial warfare between the U.S. & Russia & other nations .. “With the U.S. putting financial pressure on Iran, Russia, and China, wasn’t it likely that these countries would create their own payments systems, develop their own banks and reserve currencies, and turn their back on the U.S. dollar system entirely? If Russia, Iran, China, Turkey and others no longer relied on U.S. dollars, then control of the dollar system would lose its potency as a weapon.” .. for investors, the implications are to invest in hard assets like silver, gold, fine art, rare stamps, cash & other physical stores of value – in addition to consider investing in venture capital & start-up companies where the ownership is in the form of a written contract – not a digital account .. “My conversation with General Hayden reinforced my already strong view that financial warfare is here and digital assets such as brokerage accounts and 401(k)s are in the line of fire.” .. financial warfare is a form of financial repression.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - The Risks Of Crossing Borders With Gold & Silver Coins

Doug Casey shares some recent experiences on border crossings while carrying gold & silver coins . “What really got my attention was a few weeks later when I was leaving Mauritania, one of the world’s more backward countries. Here, I was also questioned about the silver coins. A supervisor was again called over and asked me whether I had any gold coins. Clearly, something was up .. I haven’t seen any official statements about the movement of gold coins, but it seems probable that governments are spreading word to their minions.” .. Casey suggests this is part of the war on cash .. Casey says it is all about capital controls & financial repression .. “So what’s next? I expect, as the subtle war on both cash and the transfer of capital across borders gains momentum, that gold coins are going to become the next focus of attention.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - Financial Repression Results In Mismanagement Of The Economy

Free market economist Richard Ebeling explains how government policies & central banks actions have resulted in mismanagement of the economy & the financial system .. this has resulted in all kinds of price & market distortions & unintended consequences (financial repression) .. “A variety of key interest rates, as a consequence, have, when adjusted for inflation, been in the negative range most of the time for seven years. Nominal and real interest rates, therefore, cannot be considered to be telling anything truthful about the actual availability of savings in the economy and its relationship to market-based profitability of potential investments. Interest rates manipulation has worked similar to a price control keeping the price of a good below its market-determined and clearing level. It has undermined the motives and abilities of some people to save on the supply-side, while distorting demand-side decision-making in terms of both the types and time-horizons of possible investments to undertake, since the real scarcity and cost of borrowing for capital formation has been impossible to realistically estimate and judge in a financial market without market-based interest rates. Markets have been distorted, investment patterns have been given wrong and excessive directions and labor and resources have been misdirected into various employments that will eventually be shown to be unsustainable.” .. Ebeing issues a call to action for monetary freedom & sound money to return .. “A hundred years of central banking in the United States since the establishment of the Federal Reserve System in 1913 has equally demonstrated the inability of monetary central planners to successfully direct the financial and banking affairs of the nation through the tools of monopoly control over the quantity of money and the resulting powerful influence on money’s value and the interest rates at which savers and borrowers interact. It is time for a radical denationalization of money, a privatization of the monetary and banking system through a separation of government from money and all forms of financial intermediation. That is the pathway to ending the cycles of booms and busts, and creating the market-based framework for sustainable economic growth. It is time for monetary freedom to replace the out-of-date belief in monetary central planning.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - Dr. Marc Faber: Governments Pay Less On Interest Now Even Though Their Debt Levels Are 3x Higher

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/19/2015 - Financial Repression Results From Repressed Interest Rates Set By Unelected Bureaucrats

Mises Institute posted commentary on the Federal Reserve’s decision to hold interest rates .. emphasizes how crazy the situation is today with the decision on the financial system’s most important metric – the Fed Funds rate, upon which so many prices of financial & economic assets depend – being made by a bunch of unelected, unaccountable, anti-market bureaucrats whose identities are completely unknown to virtually all Americans” .. the “elites” of the Federal Reserve“determine the cost of borrowing money across whole economies, we might call that price fixing .. But we live in an irrational world, where the judgments of real economic actors with skin in the game are thwarted by omniscient bureaucrats who openly seek to distort the price of money.” .. quotes Ludwig von Mises on how monetary interventions cannot create prosperity: “Attempts to carry out economic reforms from the monetary side can never amount to anything but an artificial stimulation of economic activity by an expansion of the circulation, and this, as must constantly be emphasized, must necessarily lead to crises and depression. Recurring economic crises are nothing but the consequence of attempts, despite all the teachings of experience and all the warnings of the economists, to stimulate economic activity by means of additional credit.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/18/2015 - Martin Barnes – Why Financial Repression is Here to Stay!

Special Guest: Martin Barnes – Chief Economist, BCA Research

FRA Co-Founder Gordon T. Long sits with BCA Research Chief Economist, Martin Barnes, a highly decorated and well renowned economist of 40+ years to talk Financial Repression and Barnes most recent work, Low Growth and High Debt: Financial Repression is Here to Stay.

FINANCIAL REPRESSION

Barnes defines Financial Repression as,

“An environment where interest rates are kept below levels which most people would consider being normal.”

In a recent publication, Low Growth and High Debt: Financial Repression is Here to Stay, Barnes focused on the problems of continued high debt levels and argues Financial Repression as a legitimate solution to the global debt crisis.

“If you can’t easily get your debt burdens down, then at a minimum you have to make the debt easier to live with, and the only way you can make your debt easier to live with is through Financial Repression. In other words, financial repression is the inevitable result of a world with low growth and stubbornly high debt.”

CONSEQUENCES OF LOW INTEREST RATES

“If money is free, very clever people at some point are going to do stupid things with it. There is no question that low interest rates will encourage some misbehaviour, and speculation. However it is hard to make the claim that today’s interest rates are low enough to be causing economic problems.”

Despite already low interest rates, economic growth around the world has been relatively low. Barnes states, “Economies should be booming with current interest rates but they’re not, we are living in a world that I would argue needs lower interest rates.”

“The by-product is financial distortion which has powerful implications for certain groups of people such as people trying to live off of fixed incomes. But you can’t push interest rates up to protect the interest of those people if the global economy is screaming for even lower rates. We cannot have a level of interest rates that will have everyone happy.”

THE PENSION FUND DILEMMA

A major mistake with the development of pension funds is that governments did not increase the pension age with the increase life expectancy.

“In a world of low returns, and people living much longer, the promises that were made a long time ago can no longer be kept. Everyone needs to understand that at some point those promises have to change, either by raising retirement age or increasing contribution rates. The logic behind these pensions is unsustainable and therefore it must change.”

SITUATION IN CANADA

In the midst of falling commodity prices, devalued currency and the housing market bubble, Barnes states the Canadian economic situation

“…is not disastrous; just like so many other economies, we are stuck in low growth. Exports are battling against moderate global growth and world trade. The big drop in the Canadian dollar has not lead to a big pick up in exports as we would have hoped. We are very tightly linked with the US economy and they are slowly growing so that is a positive.”

“Housing by every standard is incredibly overdone, especially in Toronto and Vancouver, it’s hard to get away from the fact that house prices are extraordinarily high here and it will likely erode.”

“China is moving away from its commodity oriented growth to a more service oriented model. The world is moving away from its commodity dependence which is not great for Canada, but we’ll adjust to that.”

Check out his interview with Gordon T Long which covers this and much more.

Abstract written by Karan Singh

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/11/2015 - David Berson – The Fed’s Plan for Interest Rates

Special Guest: David Berson – Senior Vice President & Chief Economist, Nationwide Mutual

David Berson is the senior vice president of Nationwide Mutual. Before now, he has worked as a College professor, at the Fed and for 20 years he was the chief economist at Sallie Mae. He has also worked at Nationwide Mutual insurance for the past three and a half years.

To David depending on where you are in the financial system financial repression will mean different things to you. According to him,

“Financial repression is holding interest rates below the level where they would naturally go.”

He explains that there are two sides to holding down the interest rate, a positive and a negative side. The positive with reducing the interest rate and applying quantitative easing include the addition of liquidity to the economy. According to him, most of the models used by macroeconomists indicate that monetary expansion helps the economy a bit at first but only a period of time. David says the expansion policy helped boost the economy out of recession and is responsible for the modest growth we see now. But the downside to it all is that keeping rates lower than it should naturally be results in savers being hurt due to the extremely low interest rates. At the same time borrowers are at an advantage. It also makes it difficult for investors to have a reasonable return. David agrees that low interest rates push investors to riskier assets but also insists that it is one of the points of having an expansionary monetary policy. He further reiterates that the upside to the artificial reduction in rates is the increased liquidity, which moves the economy a bit upwards.

“They need to concentrate on what’s happening in the domestic economy, they are the US central bank, they are not the central bank of emerging market countries even if those countries are greatly affected by what we do”

According to David, what’s happening in terms of the fall in commodity prices is not directly as a result of what the Fed does. He believes it is as a direct result of the rapid growth in china’s economy as they move to become an industrialized economy. He explains that the primary force driving the fall of commodity prices is the slowing down of the Chinese economy that is occurring now.

On what the Fed will do, David thinks the Fed will tighten this September although he also mentions that with the recent market volatility, the chances of that happening is less than 50%. He believes the Fed should tighten this September as he believes that such an action will help the economy.

On the disappointing recovery of the economy, David explains that there is an excess of government oversight on the economy, which has further contributed to the slowing down of the economy. If you look at what he calls the core GDP, which includes private sales and private purchases minus volatile inventory, trade and government, he is convinced that growth has picked up better than the overall GDP suggests and much closer to historical averages.

“One of the reasons why economic growth has been weaker in this expansion than others is a lack of government spending now I think that in the short-term negative in the long run I think a move in resources from the government sector to the private sector is positive but it takes a while for that to manifest itself in stronger overall GDP growth”.

Check out his interview with Gordon T Long which covers this and much more.

Abstract written by Chukwuma Uwaga – chuwaga@gmail.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/08/2015 - James Bianco – The Fed’s Plan for Interest Rates

Special Guest: James Bianco – President, Bianco Research LLC

Bianco research started in 1998 and is affiliated with Arbor research and training. It is an independent research company with James Bianco as its president. Bianco research specializes in macro, fixed income and equity research.

James views financial repression in light of what Ben Bernake said in his November 12 op-ed in the Washington post:

”the purpose of QE2 is the fed buys bonds, force down interest rates, that would make them relatively unattractive for most bond investors, seeking alternatives they would move further out the risk curve and they would not buy .They would push up those assets prices, create a wealth effect expecting a cycle in which the wealth effect creates economic growth to justify those higher prices”.

The forced down interest rate will not bode well for individuals who need certain rates of return to guarantee things like pension and retirement. You end up taking more risk by buying riskier assets which pushes up its price causing you to feel wealthier. He explains that when a government body in this case the CBN steps in and sets price at levels where they would not ordinarily go by themselves, they are repressing the price of interest rate, inflating the price of risk assets. They argue it is a greater good because of the wealth effect that comes from that.

James doesn’t think that the wealth effect occurs as a result of that. According to him, Milton Friedman in 1915 developed the permanent income hypothesis which states that if an asset goes up in price for example a house, you treat it as another form of permanent income. One the other hand, if your stock portfolio goes up, you perceive as temporary due to what you read in the paper.

“That’s why we obsess over the fed because we think all this stuff is temporary and we want to find out how temporary it is, because when the fed raises rates… I guess to mix my metaphors a little bit with the old warren buffets’ old line that we find out that we are swimming naked when the tide goes out”.

That’s why a rate hike is such a big deal in the financial markets. What will the Feds do?

“There are two things to keep in mind concerning what the feds will do. There’s the economic data and the market pricing of it”.

He says that based on the economic data, the fed has set up some parameters for itself and from a data dependent point of view, they have everything they need, but James believes that what will hold back the feds will be market instability. Currently, there is a great deal of volatility and uncertainty in the Chinese and emerging markets. He believes the instability in these markets will cause the feds will to maintain interest rates because they are hoping that things would calm down enough by Dec. He mentions that part of the reason for the unstable markets is due to the Feds insistence on raising rates.

EU

On his view of the EU, James Bianco has this to say:

“The history of the Europe is for the last thousand years is every generation they try to kill each other and the last one was in World War 2”.

Then they decided to get closer in order to prevent more wars. This led them to create the euro. According to him, the problem with the euro, is that you have 17 different countries in different cycles using the same currencies. He says that Draghi’s plan is to get interest rates to below zero and continue trying to stimulate the economy. He goes further to explain that the current refugee crisis that the EU is facing will have a huge negative impact on their economy. He doesn’t think Draghi’s plan will work because people think it’s temporal and as long as they think that, the permanent income hypothesis will take effect.

Check out his interview with Gordon T Long which covers this and much more.

Abstract written by Chukwuma Uwaga – chuwaga@gmail.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

09/05/2015 - Is Financial Repression Here to Stay?

The First Chairman of the UK’s Financial Services Authority Howard Davies writes an essay on financial repression .. “Maybe it is unreasonable for investors to expect positive rates on safe assets in the future. Perhaps we should expect to pay central banks and governments to keep our money safe, with positive returns offered only in return for some element of risk.” .. Davies worries about the consequences of financial repression on the economy .. he sees distortions from the prudential regulation adopted in reaction to the financial crisis – “The question for regulators is whether, in responding to the financial crisis, they have created perverse incentives that are working against a recovery in long-term private-sector investment.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

10/10/2015 - Financial Repression In China: Capital Controls

10/10/2015 - Financial Repression In China: Capital Controls

{kind=link}