08/31/2015 - Chris Casey Talks Financial Repression & the Myth of Money Velocity

Special Guest: Chris Casey – Managing Director, WindRock Wealth Management

CHRIS CASEY DISCUSSES TYPES OF FINANCIAL REPRESSION, THE MYTH OF MONETARY VELOCITY, AND WHAT IT MEANS FOR INVESTORS.

FRA Co-Founder Gordon T. Long interviewed Chris Casey of Windrock Wealth Management on the monetary policy aspects of financial repression. Mr. Casey, an Austrian economist, is a frequent speaker and writer on macroeconomic topics and their related investment implications.

TYPES OF FINANCIAL REPRESSION

“Financial repression can best be described as government intervention in the financial markets which causes distortions not only within financial markets, but throughout the economy.”

According to Mr. Casey, financial repression can take direct and indirect forms. The most damaging form of indirect financial repression is the expansion of the money supply decreases interest rates. The artificially lowered interest rate structure causes widespread malinvestment within an economy.

All of this would perhaps be tolerable if monetary policy actually stimulated the economy, but Mr. Casey states that even Federal Reserve economists have recognized the ineffectiveness of the multiple quantitative easing programs.

THE MYTH OF MONETARY VELOCITY

Mainstream economists believe inflation is currently mitigated by today’s historically low monetary velocity (“the number of times one dollar is spent to buy goods and services per unit of time”), so the money supply can be expanded without the damaging effects of inflation. Chris Casey takes issue with this as well as the very concept of velocity.

“Velocity has no impact whatsoever, in fact it is a meaningless statistic.”

Worse, the theoretical construct from which the concept of velocity derives, the Fisher Equation of Exchange, is equally faulty. This equation attempts to explain the price level within an economy, but while it includes the supply of money, it ignores the demand for money which renders it useless. A useless theory in the wrong hands can create disastrous policy:

“The real danger is that by looking at velocity, by being focused on velocity, mainstream economists have been focusing on a false measure which creates false decisions which is going to have a very real impact on investors.”

WHAT SHOULD INVESTORS DO?

Where may the faulty policy decisions lead the U.S. economy? Chris Casey believes that “the endgame eventually will be a massive inflationary recession.” Gordon T. Long then asked Mr. Casey:

“What could you suggest to our listeners that they should be doing or thinking about to protect themselves in this environment?”

After recommending investors consider becoming fairly liquid, Chris Casey addressed how to profit from the coming economic environment:

“Build a portfolio of hard assets. You want to look at anything from precious metals to certain types of real estate such as rental residential real estate to farmland. You potentially want to look at foreign currencies to diversify from the U.S. dollar despite the dollar’s strength over the last year.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/31/2015 - Ramiro Larroy – Lessons in Financial Repression from Argentina

Special Guest: Ramiro Larroy – Partner & Director, Integras Capital

RAMIRO LARROY DISCUSSES HIS VIEWS ON WHAT LESSONS THE WORLD CAN LEARN FROM RGENTINA ABOUT INVESTING IN AN ERA OF FINANCIAL REPRESSION

FRA Co-Founder Gordon T. Long interviewed Ramiro Larroy, Partner & Director, Integras Capital in Buenos Aires, Argentina.

FINANCIAL REPRESSION

“Financial Repression globally is basically governments keeping interest rates below the rate of inflation as a way of taxing savers”

Ramiro suggests that in Argentina it is much more direct it its enactment by governments. “We had many experiences throughout the years where depositors in banks were ‘bailed-in’ and forced to take on debt as opposed to their deposits”

“IT IS A TAX! It was applied a little differently in Argentina than how it is being achieved by governments in developed countries.”

THE ARGENTINIAN EXPERIENCE

“When Argentina regained democracy in 1983 we had a government that from an economic standpoint did not do that well. They ran fiscal deficits and prices of exports were poor. By the end of this government in 1989 the country was heavily in debt with inflation. At the same time they paid high interest rates on deposits so people kept deposits in the bank. With these deposits the banks were able to buy government debt. In 1990 enacted (like at midnight!) a program where everyone that had deposits received a bond.” Literally, overnight with no recourse.

“Maybe people were able to earn a rate higher than inflation before, but all of a sudden they lost everything!” The government did not have the money to pay the money owed on the bonds it had issued. This was a way to reset and issue a new long term bond.” Argentinians have experience in their bank deposits being taken from them.

CHANGED INVESTMENT SENTIMENT

“These banking actions resulted in a huge change in the mind set of investors! It is now very difficult for a family to have a substantial part of their assets to be held locally or exclusively in the banking sector. Though rates may be ‘ok’ in the banks, people are not comfortable with the risks they are taking! Pretty well everyone has developed OTHER WAYS OF STORING WEALTH, from Real Estate, to buying Gold to buying physical US Dollars.”

“The more wealthy individuals and families have their wealth outside of Argentina as a way of protecting those assets. It is not about higher returns, but rather not wanting to lose the wealth.”

STORE OF VALUE STRATEGIES

“Store of Value Strategies are so prevalent that on this day we are talking, in the morning paper of one of the largest newspapers in Argentina, the major story is “8 Strategies Not to Lose Your Wealth in the Upcoming Depreciation! Need I say more!”

.. there are many lessons to be learned in this broad 35 minute interview discussion. Maybe the most important is that Argentina is 15-20 years ahead in regard to Financial Repression investor strategies. Government actions are very predictable when debt becomes too large for officials to handle.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

Special Guest: Danielle DiMartino Booth – Former Federal Reserve Advisor, Chief Market Strategist, The Lisco Report

Having done lots of fishing this summer at Camp Kotok in northern Maine, Danielle DiMartino Booth is here interviewed by FRA Co-Founder Gordon T Long. Danielle is a former Dallas Federal Reserve Bank Advisor and now the Chief Market Strategist of The Liscio Report. She takes an Austrian School of Economics viewpoint on economic and financial matters.

Danielle emphasizes how she understands financial repression “in her bones” because she worked in “The Financial Repression Factory”, referring to the Federal Reserve. She understands the level of malinvestment, mispricing and lack of price discovery as the unintended consequences of repressive and obfuscating monetary policies of central banks. She thinks the Federal Reserve “does not have a deep enough appreciation of malinvestment .. as if Ludwig von Mises never walked the planet.”

She is angered by the considerable level of savings which has been foregone thanks to the quantitative easing (QE) policies of the Federal Reserve. Gone are the days of retiring on a Certificate of Deposit paying a decent level of interest income, due to the virtually 0% interest rates.

Danielle says there must be a renewed emphasis on education and innovation in America for it create jobs and jobs that are higher-paying generally than is currently the case.

Check out her recent speech – subscribe to our Mailing and Alert System and we will email you the PDF or view the Scribd below:

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/25/2015 - Peter Schiff Talks Gold Backed Debit Cards

Special Guest: Peter Schiff – CEO & Chief Global Strategist, Euro Pacific Capital Inc.

PETER SCHIFF TALKS FINANCIAL REPRESSION, CRYPTOCURRENCIES AND MORE.

Continuing with our series on financial repression, today we have Peter Schiff here with us who is being interviewed by FRA’s Gordon T long. Peter Schiff in his own words has been in the industry his whole life. He is also one of the few people to predict the financial crisis and was vocal about it in 2008.

FINANCIAL REPRESSION.

According to Peter one of the ways in which the government represses its citizens financially is through the banking system. He talks about the lack of privacy that arises from the opening of a bank account.

“In America today, if you have a bank account you have no privacy anymore. Your banker is basically an unpaid spy working for the government trying to monitor your activities for anything suspicious so they can turn you in to the government!”

Other ways include inflation, which erodes the value of one’s assets over time and government taxation in its many forms.

BAIL-INS AND CASHLESS SOCIETY.

“Bail-ins are a function of government deposit schemes which really don’t work!”.

He goes on further to explain that the reason they don’t work is due to the safety nets which these schemes provide. A situation is created where the banks “know that the depositors couldn’t care less how risky the bank is”. He alternatively suggests that market forces be allowed to reign in the banks so that banks compete on the basis of how much risk they can mitigate.

“People are looking for an alternative to the fiat currency created by governments”.

He mentions is one of the basis on which bitcoin was formed, although he doesn’t believe in its longevity going as far as likening it to a Ponzi scheme. The flaw in bitcoin according to peter Schiff is its lack of intrinsic value, unlike gold.

EURO PACIFIC BANK

“How do I spend my gold?”

Peter Schiff asserts this is a problem faced by consumers around the world and his bank Euro Pacific provides a solution to this problem. Customers are provided with gold and silver backed accounts with which they can access their gold 24/7. This works by using a 2-step process in which the customers have to open their account and sell off gold before they can swipe their card. Ultimately, he plans on streamlining this 2-step process into a 1-step process. This will work by converting gold in real time at the market value when customers swipe their debit cards.

Peter Schiff mentions how the real benefit from this system will be the ability of customers to save their gold since it holds on to its value and spend their fiat currencies. He goes on to compare his system and that of bitgold saying that the concept of giving out free gold which bitgold uses is not a viable business plan.

Check out his interview with Gordon T Long which covers much more of this.

Abstract written by Chukwuma Uwaga – chuwaga@gmail.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/22/2015 - The Unintended Consequences of Financial Repression: “The Impossibility of Meeting Return Targets”

Greenwich Associates conducted a study on German institutions .. some quotes from the study:

“The low interest rate environment makes it impossible to meet return targets. We have not yet found a solution.” — German Public Pension Fund.

“Low interest rates are a problem. As a reaction, we have globalized our investments and invested in higher risk asset classes.” — German Foundation

“Primary challenge is the low interest rates. The only chance to avoid this is to do things you didn’t do before.” — German Insurer.

For many institutions in Germany, “doing things they didn’t do before” means investing significant amounts of assets in something other than domestic & government bonds.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/22/2015 - The Unseen Consequences of Zero Interest Rate Policy

Incrementum’s Ronald-Peter Stöferle explains how central banks with a zero interest rate policy (ZIRP) in place are creating unintenddd consequences & associated adverse risks to investors & retirees .. it’s financial repression .. “With artificial stimulus like ZIRP, we only end up with a situation in which governments, financial institutions, entrepreneurs, and consumers who should actually be declared insolvent all remain on artificial life support.” .. with the unintended consequences being:

1. Conservative investors by nature come under increasing pressure with respect to their investments & take on excessive risks in light of the prospect that interest rates will remain low in the long term. This leads to capital misallocation & the emergence of bubbles.

2. The sweet poison of low interest rates leads to massive asset price inflation (stocks, bonds, works of art, real estate).

3. Structurally too low interest rates in industrialized nations due to carry trades lead to the emergence of asset price bubbles & contagion effects in emerging markets.

4. Changes in human behavior patterns occur, due to continually declining purchasing power.

5. As a result of the structurally too low level of interest rates, a ‘culture of instant gratification’ is created, which is among other things characterized by the fact that consumption is financed with credit instead of savings.

6. The medium of exchange and unit of account function of money increases in importance, while its role as a store of value declines.

7. Incentives for fiscal discipline decline.

8. Zombie banks are created: Low interest rates prevent the healthy process of creative destruction. 9. Banks are enabled to roll over potentially non-performing loans practically indefinitely & can thus lower their write-off requirements.

9. Newly created money is neither uniformly nor simultaneously distributed amongst the population

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/01/2015 - Financial Repression Will Intensify as Central Bank/Government Policy Options Become Limited

Economist Satyajit Das sees increasing methods of financial repression being employed by governments as policy options become limited .. Introduced in 1973 by economists Edward Shaw & Ronald McKinnon, the term refers to measures implemented by governments to channel savings & funds to finance the public sector, lower its borrowing costs & liquidate debt .. Das sees new taxes, means testing, user pay surcharges all coming .. “Entitlement liabilities, such as retirement benefits, will be managed by increasing the allowable minimum retirement age, reducing benefit levels, linking to actual contribution by individuals over their working life, and eliminating inflation indexation. Many of these policies will be packaged as socially and ethically progressive initiatives, belying the financial imperatives.” .. points out in a 2013 study, the McKinsey Global Institute found that between 2007 & 2012, interest rate & quantitative easing (QE) policies resulted in a net transfer to governments in the United States, Britain & the eurozone of $1.6 trillion (£1.03 trillion), through reduced debt-service costs & increased central bank profits – “The losses were borne by households, pension funds, insurers and foreign investors. Households in these countries together lost $630bn in net interest income, with the major losses being borne by older households with significant interest-bearing assets. Non-financial corporations in these countries also benefited by $710bn through lower debt service costs.” .. Das also sees deliberate devaluation as another financial repression mechanism .. regulations are another mechanism: “Governments can legislate minimum mandatory holdings of government securities for banks, pension funds and insurance companies. New liquidity regulations already require increased holdings of government bonds by banks and insurers.” .. wealth confiscation is yet another mechanism – seizing savings or pension fund assets like in 2013 when Spain drew €5bn (£3.5bn) from the state’s Social Security Reserve Fund, designed to guarantee pension payments in times of hardship .. nationalizations are yet another mechanism .. “Debt monetization and the resultant loss of purchasing power effectively represent a tax on holders of money and sovereign debt. They redistribute real resources from savers to borrowers and the issuer of the currency, resulting in diminution of wealth over time. This highlights the reliance on financial repression, explicitly seeking to reduce the value of savings. Ultimately, the policies being used to manage the crisis punish frugality and thrift, instead rewarding borrowing, profligacy, excess and waste.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/01/2015 - The Disappearing Retirement Fund

International Man’s Jeff Thomas points to the unprecedented financial & economic challenges & crises in the indebted developed world .. Thomas is very pessimistic about the retirement situation for Americans, Canadians, Europeans .. he thinks their investments in their pension funds will diminish dramatically in value or disappear .. for example, on U.S. social security, “Ergo, each year, those working will need to be taxed more heavily if the system is to continue. Unfortunately, at some point, we reach the tipping point and the concept itself is no longer viable. After that point, benefits will be reduced and, possibly, eliminated altogether.” .. in regard to private pension funds like 401Ks, Thomas sees the risks of a stock market crash as bringing down the value of these funds, even if the funds are so-called “diversified” .. but there’s more – there are now new risks from governments desperately in search of funds to keep their operations & public pensions going .. “When governments find themselves on the verge of insolvency, they invariably react the same way: go back to the cash cow for a final milking. Each of the jurisdictions that is in trouble at present, has, in its playbook, the same collection of milking techniques. One of those will have a major impact on pensions: the requirement that pension plans must contain a percentage of government Treasuries .. Legislation will be created to ensure that a percentage be in Treasuries, which are ‘guaranteed’ .. Sounds good. And people will be grateful. Unfortunately, the body that is providing the guarantee is the same body that has created the economic crisis. And if the government is insolvent, the ‘guarantee’ will become just one more empty promise. Recently, the U.S. Supreme Court ruled that employers have a duty to protect workers invested in their 401(k) plans from mutual funds that perform poorly or are too expensive. By passing this ruling, the US government has the power to seize private pension funds “to protect pensioners”. It also has the authority to dictate how funds may be invested. The way is now paved for the requirement that 401(k)s be invested heavily in US Treasuries.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

A Mexican Economist, Guillermo Barba never heard of the Austrian school of economics until after graduating. Mexican University teaching still focuses on Marxist philosophy and Keynesian thinking. His subsequent exposure to the Austrian school of Economics was an eye opener which started him on a road which he hopes to help others in Mexico and Latin American become exposed to. He believes that the socialist thinking which South American universities are still oriented towards is one of the cancers in the world and hurting economic development.

“I became a real economist after I met the Austrian School of Economics!”

“The Austrian School has a framework to explain the current ‘economic mess’ in the world today!”

Barba’s popular Mexican blog is focused on financial intelligence because he felt the truth was not being told and it needed to be.

FINANCIAL REPRESSION

“Mexicans know perfectly what Financial Repression means! Living in Mexico means living in the neighborhood of the United States of America. That is a lot of financial repression!”

“The entire world is suffering from Financial Repression because there are Financial Repressors. That is the problem. Who are those financial repressors? As Hugo Salinas Price told him, the entire world is controlled by a group of about 1000 people and a smaller core group control most of the decisions. Most of them are bankers”

Barba believes that t he global reserve system which is based on the US dollar “is basically a scam”. According to Barba, to keep the whole system working the powers to be must get people into debt. Debt must grow exponentially.

IMPORTANCE OF SAVINGS

“Pushing people to spend and taken on debt versus savings is insane! Savings is the base and the cornerstone of development. Savings are the cornerstone of capital! The world needs capital accumulation, not debt accumulation!

“Debt accumulation is not sustainable. Capital accumulation is sustainable!”

Guillermo Barba believes the powers to be simply don’t know what to do other than just ‘print more money’. He also sees the US dollar getting much, much stronger as people generally won’t know what to do to protect their wealth. This will offer opportunities to use inflated US dollars to buy real estates at attractive prices.

….. there is much more in this interview on the Mexican and South American economies.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/17/2015 - David Morgan Talks Silver

Special Guest: David Morgan – Silver Expert, Publisher: Morgan Report, Silver-Investor.com

An Aeronautical Engineer by training, David brings these analytic skills to his analysis of financial and commodities markets. He believes the inability of the majority of people to properly understand the significance of mathematical science such as the exponential curve is one such important example. A “hockey stick” of debt growth is simply and fundamentally unsustainable!

FINANCIAL REPRESSION

Keeping interest rates low is central to debt ridden governments surviving. Acording to David Morgan the government must keep rates low as long as possible but believes a reset of some sore is inevitable. David sees the mechanics and policies of keep rates repressed as fundamentally defining Financial Repression.

Financial Repression is like a big coffee press, pressing everything down and has suppressed the ability for us to have a free market and thereby enjoy the fruits of our intellect, labor, creativity and purpose as humans.”

POTENTIAL RISING INTEREST RATES

Many believe that rising interest rates will hurt gold. David fully expects the Fed to increase rates but sees it as being nothing more that “showmanship”. David suggests that:

“his experience shows that it is when REAL RATES get positive that you COULD see gold impacted from an increase in interest rates”

“What you really need to know is what are the real rates versus nominal rates which you see iin the newspapers.”

GOLD-SILVER RATIO

The current gold-silver ratio implies to David Morgan is that silver is presently undervalued relative to gold.

According to Morgan the Gold-Silver Ratio is telling us something else that is important.

“If you have a real economy with sound money you get a deflationary trend. This means your money is worth more over time. It is beneficial to almost everybody. Silver is the best inflation edge and not the best deflation hedge. Gold is the best deflation hedge. Silver anticipated this huge inflationary environment back when QE2 was announced and moved from $26/OZ to $48/OZ. What happened was all that anticipated inflation didn’t get into the market place because all the increased debt only resulted in re-liquifying the banks. They forced the money into the banking system and not out into the public sector.”

David believes silver is currently a better buy than gold. He still believes silver will outperform gold.

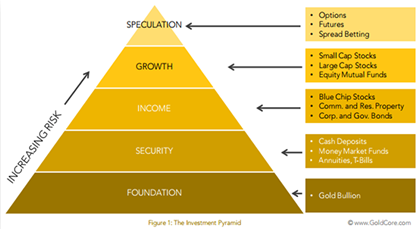

“We are not out of the woods. There is a place for precious metals in your portfolio. 20% for “metal bugs” and 10% for the average public.”

There is much, much more in this 32 minute interview with this well respected precious metals and silver expert.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/17/2015 - Jeff Berwick talks Crypto-Currencies

Special Guest: Jeff Berwick

Jeff Berwick, based in Acapulco, Mexico, has formerly been interviewed in this series (https://www.youtube.com/watch?v=O20n_oDUx54 ). He founded the StockHouse Media Corporation in 1994 and was its CEO until 2002. He is publisher of the dollar vigilante website (https://www.dollarvigilante.com/ ), which went online in 2010. Back then, he predicted the complete collapse of the US Dollar and the world financial system within the next five to ten years. He thinks that we are a lot closer now. He recently predicted a massive breakdown for September 2015 based on the seven year “Shemitah cycle“ (http://surviveshemitah.com/ ).

Jeff is concerned about the dependence of governments and financial market institutions on extremely low interest rates, even negative interest rates, which he calls “complete Keynesian insanity”. What is happening in Greece right now is just the beginning. It will eventually happen in other eurozone countries like Spain, Portugal, Italy, France and in countries all around the world, including the US.

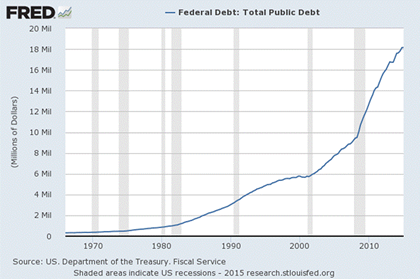

Government debt in most countries has become so high that minor increases in the interest rate would lead to immediate default. The explicit US debt is above $18.3 trillion, as shown in the figure below. This however does not include implicit debt and liabilities that the US government has accumulated over the years, for example in the form of social security. Total debt and liabilities according to Jeff amount to $95 trillion.

“All it takes is, for example, for the Federal Reserve to raise interest rates by .25 per cent and they can bankrupt the entire financial system. This is where we are now. It’s been complete insanity. They tried to fix the 2008 crisis by printing money and going into more debt, which is why they got into that problem in the first place. And we are starting to see the next wave of major collapses and crises.”

As a response to the ongoing war on cash, Jeff suggests to go out of large cash holdings as soon as possible. He sees one potential solution in BitGold and even more so in Bitcoin, as a completely decentralized money and payment system. The price of bitcoin has been rising during the recent Greek crisis, whereas gold and silver have fallen. However, Jeff points out that the prices for gold and silver are systematically distorted on a “very manipulated market.”

“There is no Bitcoin office, there is no BItcoin servers. So no matter what the government does, unless they turn off the internet entirely, they can’t stop Bitcoin. That’s the beauty of Bitcoin.”

Although Mexico is often portrayed as a dangerous third world country, Jeff can tell from personal experience that it is in many respects a better place than the US, as there is far less government involvement in private and business affairs. Mexico will nonetheless face serious problems, because of their close economic ties to the US. The collapse of the American economy will inevitably spill over to Mexico.

“But I think people here [in Mexico] are more used to it. So, for example, they had their peso collapse in the 90s and people lived through it. But Americans aren’t ready for what’s coming. They haven’t seen it in their lifetime. And as you know, half the people in the US are on government assistance now, and a lot of those are on welfare and food stamps. When those EBT cards get shut down, I wouldn’t want to be anywhere near any major population center in the US.”

Jeff generally sees potential in other Latin and South American countries like Columbia, Chile and even Nicaragua, as well as some Asian countries, but definitely not in North America, Europe, Japan or Australia, which all share the same problem: the biggest cohorts of their populations looking for unsustainable entitlement payments in the near future.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/16/2015 - James Turk on Financial Repression

Special Guest: James Turk – Founder & Managing Director, GoldMoney.com

With a career in International Banking, including managing the Abe Dubai Investment Authority’s Commodities Portfolio, James Turk is an experienced professional whose insights should be thoughtfully considered. He feels strongly that the US needs to return to the sound money principles the framers of the US Constitution outlined and which the US has unfortunately and perilously veered away from.

FINANCIAL REPRESSION

“Financial Repression is government intervention in the market system which distorts the market’s signals. …. Government intervention not only distorts the markets but in fact is counter-productive because many times it is government policies which the market are reacting to!”

Instead of changing the policies, governments try and convince the markets (through intervention) that the policies they are following are the correct ones, when in fact they are not.

James feels strongly that governments need to be outside the markets and be primarily focused on maintaining the ‘rule of law’ and ensuring there is a level playing field for competitive capitalism to operate on. Government intervention results in distorting that playing field to the advantage of themselves and their special interests.

“(Governments & Central Banks) are following policies that basically are not sustainable!”

“The government’s ‘make believe’ is that they are creating wealth through creating currency and distributing it through their various programs. That is not creating wealth, but rather debasing the currency. When you debase the currency this is the worst type of financial repression because you are essentially destroying people’s ability to interact entirely voluntarily within the market place, as we fulfill our needs and wants.”

UNDERSTANDING WEALTH

There is only so much wealth in world. It needs to come from somewhere if it is to be distributed in a meaningful way. James Turk believes wealth fundamentally comes in two forms: Tangible Wealth and Financial Wealth.

Financial Wealth comes with counter-party risk and the exposure to insufficient cash-flows required to support the leverage that inevitably comes with pyramiding and the interconnection of financial wealth.

James Turk believes we are presently destroying wealth. Financial Wealth gets destroyed because of the eventuality of insufficient cash-flows (Free DCF) to support the over financialization of the economy.

…. there is much, much more in this fact filled 24 minute Video.

WAR ON CASH & BAIL-INS

The Holy Alliance

Perpetuating the Welfare State

Why we can’t trust the banking sytem anymore.

How banks have become Hedge Funds versus lending institutions,

Why we need to separate the banks function of being a payments system versus being investment fund managers.

CRYPTO CURRENCIES

What is the real purpose is of money,

How the current environment is a historical aberration. We have moved away from a sound money system as the constitution framed.

Why we need to return to the wisdom of the framers of the US constitution,

Why Gold and Silver’s proven historical track record is important.

GoldMoney & BitGold MERGER

Why GoldMoney and BitGold Merged,

What James sees the future to be for the merger.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/10/2015 - Joseph Salerno on Bail-Ins & “The-War-on-Cash”

Special Guest: Joseph Salerno – Austrian Economist, Professor of Economics, PACE University, VP Academic MISES Institute

Professor Joseph Salerno is a noted Austrian Economist who spoke with the Financial Repression Authority on Financial Repression and his growing concerns with what is referred to as “the War-On-Cash”, which he sees leading America and other developed countries in the wrong direction. He sees it as presently gaining momentum in senior policy levels around the world as global debt problems become more acute.

FINANCIAL REPRESSION

“A combination of Deliberate Inflation and very low Interest Rates. Interest rates which are kept low by a variety of what are called “Unconventional Monetary Policies“.

“There is talk now of having:

Negative Nominal Rates,

Governments taking over Pension Funds,

Varies ‘privileging’ of government debt as part of bank capital.

..so it (Financial Repression) is a series of interferences in the financial markets by government with the end being to push interest rate lowers so they can inflate away their debt! They do that by having interest rates even lower than the rate of inflation.”

“What Financial Repression does is transfer surreptitiously resources and coming wealth from savers and retirees to the government and its crony banks. I think it exists, it is dangerous and I think many people are being hurt by it!”

WAR-ON-CASH – GETTING TO NEGATIVE NOMINAL BOND RATES

Professor Salerno believes the government wants Negative Nominal Rates but as he points out: “The only way they can do that is to lock peoples deposits into the banking system – that is where the War-on-Cash comes in! They would love to restrict or even abolish the use of cash within the United States if they could. That means they would have to use deposits.”

“This is another way of propping up a very unsound and dangerously flawed banking system!”

Professor Salerno has spoken out extensively on this subject, most recently at the Mises Circle event in Stamford, Connecticut

Governments, at least modern western governments, have always hated cash transactions. Cash is private, and cash is hard to tax. So politicians trump up phony reasons like drug trafficking and money laundering to win support for bad laws like the Bank Secrecy Act of 1970, which makes even small cash transactions potentially reportable to the Feds.

Today cash is under attack like never before. Ultra low interest rates are the norm for commercial bank accounts. In Europe, as the ECB ventures into negative nominal interest rates, certain banks threaten to charge customers for depositing cash. Meanwhile, certain European bonds now pay negative yields, effectively turning them into insurance products rather than financial assets. And some economists now call for the outright abolition of cash, which shows just how far some will go in their crazed belief that economic prosperity can be commanded by forcing us to spend rather than save.

The War on Cash is real, and it will intensify.

PUBLIC FOREIFEITURE

Both bank deposits and withdrawals of cash are now carefully scrutinized by banks and police agencies across America. Safety deposit boxes are seeing increasing restrictions on what can be held in them in the way of cash. People depositing cash often find themselves facing public asset forfeitures and seizures by the police. In some cases when cleared as being innocent then have serious difficulty in getting their seized assets returned. Professor Salerno expounds on this and other troubling new developments in America.

….there is much, much more in this fact filled 29 minute Video.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/04/2015 - The Head of India’s Central Bank: Financial Repression Policy of Devaluation Is Being Used to Hide a Worldwide Depression

The Indian central bank chief who saw the financial crisis coming thinks the world is now facing Great Depression-era problems .. Raghuram Rajan*: “Are we now moving into the territory of trying to produce growth out of nowhere? We are in fact shifting growth from each other, rather than creating growth. Of course, there is past history of this during the Great Depression when we got into competitive devaluation .. We have to become more aware of the spill-over effects of our actions and the rules of the game that we have — of what is allowed and what is not allowed — needs to be revisited.” .. it’s financial repression ..

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/01/2015 - Mark O’Byrne on Bank Bail-Ins & the Potential Deceptive Defrauding of Depositors

Special Guests: Mark O’Byrne – Founder & Research Director, Goldcore

Mark O’Byrne feels that holding a Degree in Greek and Roman Civilization with a focus on their economic and monetary history. This gives O’Byrne insights into the cyclical nature of societies that few other writers have. It is these insights that Mark shares in this 35 minute video. Bank Bail-Ins are only a modern day indicator of financially collapsing societies. “Unfortunately, we don’t learn the lessons of history to our own downfall!”

FINANCIAL REPRESSION

“Given the large amount of debt in the world today we are seeing almost ‘anti-free market philosophies’ whereby the governments don’t like price signals and the pricing mechanism, so they are trying to repress this to repress interest rates.”

“By artificially suppressing the pricing mechanism, similar to forcing an inflated beach ball under the water, it will shoot up in another direction and can go in the opposite direction to what is initially intended!”

BANK BAIL-INS

“We are told Bail-Ins are to protect the taxpayer from the government having to bail-out the banks. But the depositors are the tax payers? Bail-Ins are just to protect the Senior Secured Debt holders!”

This is wrongful deception as people belief their money is safe in the bank It is intended to protect the assets of the Senior Secured Creditors within the banks capital structure. Private individuals and depositors are not holders of Senior Secured Credit to the banks which is strictly the realm of select international banks.

CONFISCATING DEPOSITORS FUNDS MEANS DEFLATION

“If you confiscate depositors funds (in a Bail-In) you will cause deflation like you would not believe!”

If you follow Mark O’Byrne’s analysis you quickly realize that Bail-Ins are both economically very dangerous and basically nothing more than regulations to protect elements of the bank financial structure. The question may be: are regulations today to protect tax payers from the banks or to protect the banks from taxpayers (depositors)?

“Maybe today we need to come to the obvious realization that the government is no longer regulating the banks, but rather the banks are regulating the government!” Gordon T Long

INTERNATIONAL DIVERSIFICATION IS THE ANSWER – While the Doors are Still Partially Open

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/27/2015 - Entire Discussion Now Available for FREE – Real Vision TV – THE RESET Watch Raoul Pal & Grant Williams Talk Financial Repression

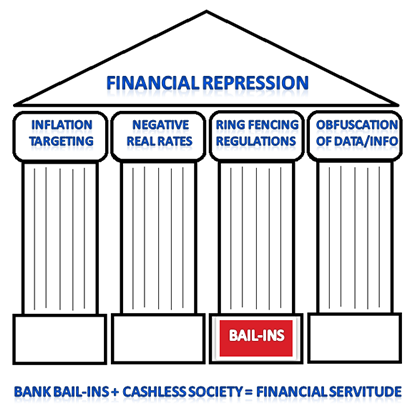

Global Macro Investor’s Raoul Pal and Vulpes Investment Management’s Grant Williams discuss essentially what we have classified as the 4 pillars of financial repression: repressed interest rates, forced inflation, obfuscation and ring-fencing regulations. The terms they use are a bit different, but the basic concepts are the same.

They discuss the systemic risks to the financial system including the loss of faith in money itself. They explain how massive money printing has distorted financial markets and prices worldwide, especially through the suppression of bond yields by central bank policies.

They also discuss their suggested solutions to investing in this environment – physical gold held outside of the financial system, cryptocurrencies, assets held outside of the concentration of risk in the financial system, investments in the monsoon regions of the world.

This is a fascinating must-watch discussion which will help you understand what is currently happening in the financial markets, the banking system, the investment world and the global economy.

If you want to subscribe within the podcast – Apply Our Discount Code – we are partnered with Real Vision TV and we offer the maximum discount you can get anywhere .. Our Discount Code is as follows: FRA-RV

FREE REALVISIONTV PROGRAM SHOW DISCUSSION BETWEEN RAOUL PAL AND GRANT WILLIAMS ON FINANCIAL REPRESSION – NOW AVAILABLE AT NO COST – SIMPLY CLICK THE PODCAST LINK BELOW.

CLICK HERE Subscribe to REAL VISION TV at the lowest possible price:Real Vision was launched to combat the dumbed-down approach to finance in traditional media. It is the world’s first on-demand video channel for finance and our driving ambition is to deliver the highest quality economic, financial, and geopolitical content available. This obsession affords us access to the world’s finest financial minds. Want to see it? See THE RESET by linking here.

If you want to subscribe – Apply Our Discount Code – we are partnered with Real Vision TV and we offer the maximum discount you can get anywhere .. Our Discount Code is as follows: FRA-RV

25% Discount off of $400/Year Subscription = $300/Year

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/24/2015 - Ronald-Peter Stoeferle – “In GOLD we TRUST” Report

Today, the 2015 edition of the gold report “In Gold We Trust” was launched. It is the 9th edition (read the 2013 and 2014 edition). With a global reach of some 1 million readers, it is probably the most read gold report worldwide. The In Gold We Trust 2015 is written by Ronald Stoeferle. He is the managing partner of a global fund at Incrementum AG in Liechtenstein, focused on the principles of the Austrian school of Economics.

2015 EDITION: “IN GOLD WE TRUST”

The gold price has stabilized in 2014, after its collapse in April and June of 2013. Investors’ interest in the yellow metal is los. Hence, market sentiment vis-à-vis gold is standing at a multi-year low, maybe even a multi-decade low. History learns that extreme underperformance usually lasts for one year. If history is any guide, than there should be a recovery in the gold price in the foreseeable future. Even with the severe underperformance since 2013, gold is up approximately 9% per year since it started to trade freely in 1971. As seen on the next chart, depending on the currency in which it trades, the average yearly performance is excellent for investors with a long term horizon. In other words, gold does what is always has done throughout history: preserve value and purchasing power.

Preservation of wealth is the primary reason why one should hold gold nowadays. Monetary policies of central banks are extremely unusual. The U.S. Fed could be talking about “normalization,” but with 7 years at zero percent interest rates we are nowhere near “normal” conditions. The most extreme monetary conditions, today, are being seen in Japan. It is really no coincidence that the gold price in Yen is near its all time highs. The gold price in Yen is simply reacting on the extreme expansion of the monetary base by the Japanese central bank. As the next chart shows, the balance sheet of the Bank Of Japan (BOJ) is approximately 65% of the country’s GDP. In other words, the assets that the BOJ is holding nears 2/3 of the total economic output of the country. When compared to other regions, it is clear that is a monstrous amount. It seems that Japan is near its endgame.

One of the “reasons” gold has gotten so little attention in the last two years is that investors have been focused on stock markets around the world. The U.S. stock market has seen a huge rally since October of 2012, European stocks catapulted higher when the European version of QE was announced earlier this year, Japan keeps on making multi-year highs in the wake of an ever expanding monetary policy. Meantime, however, stocks are not cheap anymore. On a historic basis, when expressed in a price/earnings ratio according to the Shiller method, the stock market in the U.S. sits at relatively high levels (although no extremes). Although it is not given that the stock market is about to go south, there always is a possibility that the top is set in which case gold should see positive returns. As the next chart shows, during periods of the worst performance of the S&P 500, stocks and commodities have lost significant value while gold remained steady.

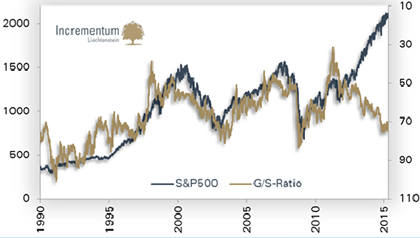

A correction in the stock market is certainly in the cards. Why? Because traditionally the gold/silver ratio is mostly negatively correlated with the S&P 500. In other words, as the gold/silver ratio goes down which means there is a disinflationary environment, stocks come down as well. Over the last 25 years, that correlation has held very well, but started to diverge strongly 3 years ago.

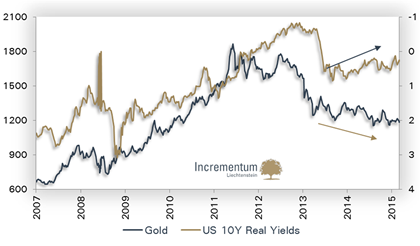

Gold is underperforming in a disinflationary environment. That has been one of the key observations in the last In Gold We Trust reports. There was enough evidence in the datapoints so far, but the most up-to-date chart says it all (see below). While the real rates were standing at -4% in 2011, they have gone up steadily since then, and are again in positive territory this year. The gold price has moved in the opposite direction in that same time period. The In Gold We Trust Report 2015 focuses, among many other things, on the correlation between the gold price and inflation expectations. Gold is an inflation sensitive asset. The U.S. 10-Year real yields provide an indication of inflation expectations. As readers can see, a strong divergence is in place since 2013, arguing for a strong revaluation of the gold price as inflation expectations are in an uptrend since then.

Suppose, however, that inflation expectations will change their trend … would that be bad for precious metals? The answer to that question is to be found in the last chart. During deflationary periods, like the ones starting in 1814 or 1864, the Great Depression of the 30ies or the financial crisis of 2008, gold did remarkably well. It is during those periods of “financial stress” that gold shows its real value, i.e. preserve wealth and provide protection against other assets.

The themes in this years 2015 “In Gold Trust Report” are the real value of gold as a financial asset and the end of gold’s underperformance.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

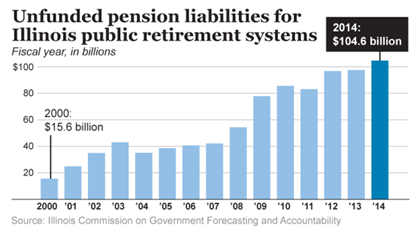

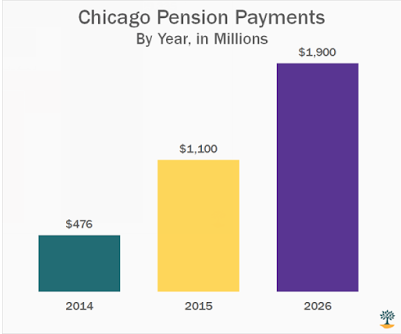

06/21/2015 - Mike “Mish” Shedlock – What Do the State of Illinois, Chicago, Public Pensions and Greece Have in Common?

Special Guest: Mike “Mish” Shedlock, MICH’S Global Economic Trend Analysis

MISH SHEDLOCK COMES OUT SWINGING ON: State of Illinois, Public Pensions and Greece

STATE OF ILLINOIS & CITY OF CHICAGO –Never Ending Financial Obfuscation

From Seven Illinois cities, to the City of Chicago, to the State of Illinois, Public Pensions are bringing the proud ‘Land of Lincoln’ to its “financial knees”!

Decades of politically expedient l promises and over generous Public Pension concessions to appease powerful public unions have left all levels of government with few financial alternatives. Many are now be forced to consider bankruptcy.

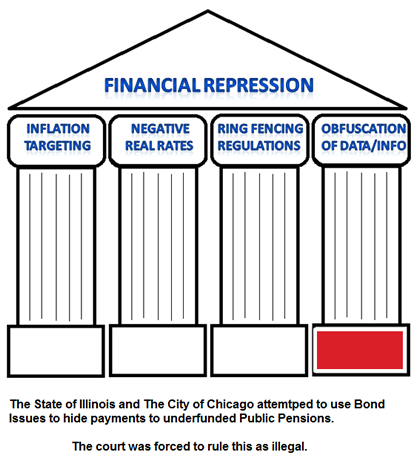

The Fourth Financial Repression Pillar of “Obfuscation” has been the practiced tactic for some time which has camouflaged this cancer. This obfuscation involved many clever accounting games which according to Mish Shedlock:

“Illinois’ Pension Plans are funded on average something like 39% and of course that creates a conflict of interest after judges have ruled on Pension Plans. The courts ruled that a bill Governor Rauner signed is unconstitutional and now sends things back to the drawing board. That (the bill) was supposed to save Illinois about $2B per year. Judges were in on it, Actuaries were in on it, the Rating Agencies – everyone was in on it.”

“Moody’s cut Chicago’s rating to junk. The City of Chicago promptly removed Moody’s from rating its bonds and instead hired another third party to rate its bonds. This is “rate shop whoring” and that is what I call it! The same process goes on with “actuarial whoring” because no city wants to admit that their pensions are as underfunded as they are!”

“Many of the pensions allow workers to retire at 50 after putting in 20 years of service, or whatever the requirement was. What do they do? They retire, collect their pension and then go to work for another government agencies and accrue benefits for yet another pension! – The whole system is untenable!”

“The taxpayers in Cook County are paying 50% of the tax revenues – not for services – instead it goes towards interest and pension obligations!”

… and IT’S STEADILY GETTING WORSE!

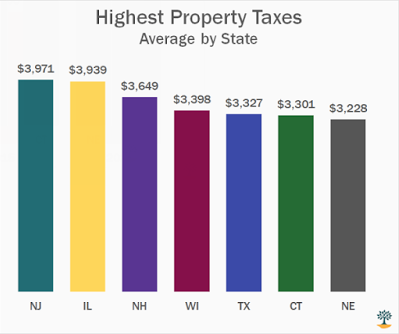

SOARING STATE TAXES – Sacrosanct Public Pensions Are Forcing Increased State Taxes

LOCAL PROPERTY TAX INCREASES

“To shore up Chicago’s Pension System they would have to hike Illinois property taxes by approximately 50%. – My (Mish’s) property taxes are already $14K/year!”

City, Local & Town Taxes in America are about Property Taxes. We can expect to see and explosion going forward in property taxes to pay unfunded public pensions.

Could this be a potential Death Knell For Real Estate Prices?

Could this trigger a collapse in ‘Tax Free’ Muni Bond Values?

GREEK CRISIS HAS COME TO A HEAD – Public Service Pensions A Major Sticking Point

“You have to actually wonder if the Greek Government is giving Greeks time to get their money out of the banks – only the dumb money is now left?”

….and much, much more in this fast paced 30 minute Video

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/21/2015 - Paul Brodsky Talks Financial Repression

Special Guest: Paul Brodsky – Investment Strategist, Wall Street Veteran

Paul Brodsky introduced himself as a presenter at the Park Plaza Hotel (NYC, NY) to 200 of the world’s largest Institutional Investors from large Sovereign Wealth Funds, Pensions Funds, Endowments and Foundations …. “I’m Paul Brodsky, I’m a Gold Bug!” This not only took guts but serious credibility in front of an audience that doesn’t consider gold in their portfolio allocation decisions. So why would he do this?

Paul had been asked to present the “Case for Gold”. It was 2010 and Gold had just had a run. Though Gold had been the elephant in the room for previous 9 years , Paul surmised the organizers simply felt gold needed some sort of obligatory representation. His presentation focused on the Global Monetary System and sheepishly admits he actually never mentioned the world Gold again! This summarizes the thinking within the community of Global Managers of serious money.

Paul says he felt he got the invitation because of the thrust and struggle of QB Asset Management, the hedge fund he co-founded. It showed in Paul’s writings to QB’s clients while seeking the truth. He sought an understanding of Price and Value (which are often quite different) in addition to Alpha generation for clients.

FINANCIAL REPRESSION

“Its easy to think there is a grand conspiracy out there is terms of the banking system, the policy makers and politicians in the political dimension. It is very easy to draw lines between all these groups connecting them. I think what we have is a natural set of incentives that are drawn together by how the system works. For example, Politicians usually like to spend money they don’t have and the banking system can let them do that! So it is a very symbiotic relationship – one feeds the other – there is little need that a word be said! There is no back room, smoke filled discussions going on.”

“After the 1971 Nixon Shock, for the first time ever we had a global monetary system where there wasn’t one currency that was ‘hard’ – that is, backed by anything scarce. What that did was make everything relative. It made currencies relative and it made financial assets relative. Ultimately it made performance relative!”

“When everything becomes relative it makes thing very easy for authorities to manage the system because there is no governor on them to bring things back into balance!”

“What was once “the role of the Fed to take away the punch bowl when the party got going”, it was now the Fed that was ‘spiking’ the punch bowl.”

FRACTIONAL RESERVE BANKING

“The system as it is constructed using fractional reserve lending and fractional reserve banking is the real ‘bugaboo’!” Paul is quick to point out there are two sides to this argument. “Yes, the hard money crowd is correct – it has allowed us to spend money beyond what may be considered sound, but also this “funny money” for example helped defeat communism and helped fund the dotcom frenzy which left a technology footprint that may not have occurred as quickly without it.”

“It has been a terrible flowering of baseless credit, debt that has never been extinguished. It may all come down in a Minsky like debt deflation that is ugly – or it may force the Fed and other central banks around the world to create much more base money through QE and other lines of credit that diminishes the value of not only our currency but all others – that gets us back again to relative value and performance!”

“The central banks are devaluing their currencies and devaluing against themselves in a ‘tag team’ manner. They are also devaluing against Production. There used to be only four ways you could get a dollar. You could produce something, you could borrow it, you could reinvest what you had already earned or you could steal it. Now banks can make money out of thin air without any discipline. There is nothing on the other side. Debt is created through the loan process and it never has to be extinquished if the monetary authority doesn’t demand that.”

“We have gone through this great leveraging over the last 35 years. It has been encouraged by Monetary Authorities in the US and elsewhere. Now we are at zero interest rates we can’t refinance ourselves to another round of leveraging. We have to find a new outlet for credit or there is going to be some sort of reconciliation. When you ask about Financial Repression, I think it has been forced on Monetary Authorities (though its their own doing). It had to happen. It is a consequence of the past 35 years.”

“I think they are boxed, as is everyone else (like the IMF) that is involved”

WHO IS GOING TO STAND UP TO THIS?

“It is also in China and Russia’s interest to have a baseless currency and even fractional reserve banks. What it does is centralize power to decide what wealth looks like in their nations and economies.”

“My sense is we have to accept that this is the reality. That for the first time ever …. I think there is going to be increasing coordination amongst all sorts of Monetary Authorities and the net loser is going to be the saver or pensioner in real terms. It is not necessarily a negative on equities, real estate or anything that relies on credit. It may be bullish on nominal pricing but bearish on real pricing and value. That is what Financial Repression is bring us.”

…. there is much, much more in this broad ranging 46 minute interview with a very thoughtful and experienced Wall Street insider telling it the way it really is:

Why the death of the infamous Bond Vigilantes occurred and how they got trampled by the Fed,

Why we have had a slow migration from Capital producing economies to Credit producing economies or Financialism,

Why a policy of unsound money has allowed China and Russia to transition to modern societies without becoming militaristic,

Why the global over supply is driving pricing pressures and deflation,

The eermergence of China’s new private mercantilism system,

The political dimension of the $555T global SWAPS market exposure.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

06/20/2015 - How Financial Repression is Making it Difficult to Retire

Charles Hugh Smith & Gordon T Long discuss the unsustainability of pension funds for U.S. public employees, the challenges of ordinary retirees to be able to retire given the financial repression on interest rates & low yields .. while everyone is beginning to agree that most people will not be able to retire, but must keep working, many do not realize that there are already “means-testing” in place for the U.S. social security benefits because if you & your spouse keep working & make at least $44,000 per year, your U.S. social security retirement benefits will be reduced by 85%! .. 26 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/31/2015 - Chris Casey Talks Financial Repression & the Myth of Money Velocity

08/31/2015 - Chris Casey Talks Financial Repression & the Myth of Money Velocity