International providers who can help you with taxation planning, non-residency preparation, FATCA compliance, second citizenships, seeting up offshore LLCs in your IRA, or just simply filing your returns.

Retirement solutions for retirees with little or no savings. The environment of financial repression has resulted in low investment yeilds & virtually 0% interest rates, making it difficult to retire on one's savings without using up the savings capital directly. We have low-cost, high-quality solutions which may be of interest.

Wealth Management Firms - scroll down below to view the firms taking an investment management approach based on the principles of the ASE

Investing using ASE: Articles, Books, White Papers, Presentations

Consider investing using the principles of the Austrian School of Economics. This is a growing trend, and we have partner wealth management firms which specialize in this approach. Read our white paper and Incrementum's new book to understand this new investment approach and its advantages and benefits.

A Must Read Book by our solution partner Incrementum Liechtenstein, by Rahim Taghizadegan, Ronald Stöferle, Mark Valek:

Dr. Marc Faber on the Book:

"I am grateful to the authors of this book for not only highlighting the fundamental principles of the Austrian School but also for showing how investors can make practical use of them."

Bearing Fund - Long/Short Hedge Fund using the Principles of the Austrian School of Economics

Bill Laggner and Kevin Duffy manage the Bearing Fund using an Austrian School of Economics lens in terms of identifying boom-bust cycles, value in the market place, bubbles, and distortions created by both fiscal and monetary authorities. Bill is a graduate of the University of Florida (BS in Finance with honors). He began in the investment industry in the late 1980s, initially as a stockbroker and then moved to the buy side at Fidelity Investments. He left Fidelity in late 1998 to manage his own investments. Bill has been featured in Barrons, Reuters, CFA magazine and Business Insider.

Bearing Fund was one of the top performing macro funds during the last bubble implosion in '07-09. Bearing Asset Management created the Bearing Credit Bubble Index (available on the net) which features the various enablers of the last bubble beginning in 2004-05.

Click on the contact button below to fill in the contact form - you will receive Bearing Asset Management's "Stimulus Bubble Opportunities" deck - lots of charts & information!

BEARING SHORT INDEX

December 14, 2015

About 18 months ago we constructed an equal-weighted index of our short selling universe at the time, 53 stocks. The list breaks down according to the following themes:

- Alternative energy (2)

- Asset managers (2)

- Bond insurance (3)

- Canadian banks (2)

- China and commodity-related (6)

- Consumer discretionary (2)

- Cyclicals (2)

- Europe (2)

- European banks (2)

- U.S. financials (4)

- High yield bonds (1)

- Housing (3)

- Luxury goods (4)

- Momentum/tech stocks (6)

- Pharmaceutical roll-ups (3)

- REITs – office (4)

- REITs – retail (5)

From its all-time high set on June 23, the Bearing Short Index is -20.3%. Over the same period, the S&P 500 is -4.8%. Of the 53 stocks in the index, 11 are down over 40% from their 52-week highs while 5 are down over 60%.In other words, the past six months have been ideal for short sellers and miserable for a number of high profile hedge funds which have been long many of these formerly highflying stocks. This underlying damage is being masked by the averages, propped up by the so-called “FANG” stocks: Facebook, Amazon.com, Netflix, and Google. Since June 23, these four stocks are up on average 31.5%.

Such a divergence is typical as an equity bubble is nearing its end, what we refer to as the “casino effect.” Essentially, as betting tables begin turning into losers, the compulsive gamblers refuse to leave the casino, instead gravitating to a smaller and smaller number of winning tables. At that point, the end is fairly predictable: no one leaves with any money in their pocket.

Investors must understand that we are living in an unprecedented period in the history of financial markets. We have entered a condition where we are rapidly moving back and forth between inflationary and deflationary cycles. The reason for this problem stems from decades of excess money supply growth, asset price appreciation and debt accumulation in the developed world economies. To be specific, the total level of U.S. non-financial debt is at an all-time high 250% of GDP. Therefore, a secular period of deflation—which is, in fact, a healthy period of reconciliation--is needed to bring those conditions back to sustainable levels. However, the government and our central bank are fighting that rebalancing with unprecedented measures of borrowing and money printing. Meanwhile, global central banks are actively engaged in yield suppression, causing investors to seek income from companies that pay dividends.

Market forces now demand that a period of selling assets and paying down debt occurs. However, policymakers and the Federal Reserve find it politically untenable for any period of deflation to take place. Deflation is painful to voters and politicians because they are usually thinking more about the next election, than the long-term fiscal health of the nation. So, the US economy swings back and forth between inflation and deflation cycles as the government steps in and out of market manipulation. When the Fed and policymakers intervene we see inflation occur, and when they are not acting, and market forces take over, and we experience deflation. You need to have active management of your money to profit from this dynamic.

Pento Portfolio Strategies uses models to determine the future economic condition we will face by analyzing the Fed’s monetary base, bank lending practices, growth in the monetary aggregates, the primary trend of the U.S dollar, the government’s fiscal condition as well as many other metrics not mentioned in this marketing material. We also determine if we are in a dollar-neutral cycle, in which a bar-belled approach is deployed between the two portfolios. After we determine the economic prevailing condition, a rigorous method of security selection is utilized. That’s because not all asset classes move with the same velocity and in the same direction, so the investment backdrop is not always black and white. For example, during an inflationary cycle, food and energy prices can go up while housing prices fall. The simple reason for this is because those assets that have just exited a bubble may take more than a decade before rebounding. It is vitally important to have your money at a firm with both trust and experience. And it is also crucial that they understand markets and economics. In the most general of terms, here is what our portfolio construction consists of: Our Inflation/Deflation-hedged Portfolio is constructed using primarily precious metals, base metals, energy and agricultural stocks and ETFs during times when inflation is prevalent. During times of deflation, the fund will hold cash and long-USD investments, while shorting growth-related ETFs. Our Global Yield-Enhanced Portfolio owns a basket of globally-diverse ETFs and equities that provide dividends. The fund does not invest in sovereign debt. A covered call strategy is utilized to enhance the stated yield. Pento Portfolio Strategies utilizes a comprehensive risk management strategy to help lock in gains and limit losses in our portfolios. Our risk management employs covered call and long put option strategies. It is our firm’s policy to never use leverage in the management of client's money. When investing your money, you want someone with experience and someone that you can trust. And you want to be treated fairly. Our motto is "Analysis without an Agenda". Please give us a try.

Michael Pento is a well-established specialist in the Austrian School of economics and a regular guest on CNBC, Bloomberg, FOX Business News, CNN and other national media outlets. He is also the author of, "The Coming Bond Market Collapse". His market analysis can also be read in most major financial publications, including the Wall Street Journal. He also acts as a Financial Columnist for Forbes, a contributing writer to TheStreet.com and is a blogger at the Huffington Post.

WindRock Wealth Management is an independent investment management firm founded on the belief that investment success in today’s increasingly uncertain world requires a focus on the macroeconomic “big picture” combined with an entrepreneurial mindset to seize on unique investment opportunities. They serve as the trusted voice to a select group of high net worth individuals, family offices, foundations and retirement plans. Today, in an attempt to offset continued economic weakness, governments are reacting with spending, debt issuance, and intervention in the economy on a scale without precedent in modern history. Although these policies may buy time, they cannot solve the underlying issues. Ultimately, governments will repay debt with their last remaining option – printing more money. As money floods the system, this will drive inflation higher despite continued weakness in the economy. Under these circumstances, the current conventional model of a static bond and stock mix will fail. It will fail investors in realizing reasonable returns. It will fail investors in preserving their purchasing power after inflation. And it will fail investors in protecting their capital and securing their retirement. The conventional experts do not foresee such risks. But these same experts missed the bubbles in technology, real estate, and equities. Today they are missing the bubble in government debt and the ramifications of unbridled money creation. WindRock understands these issues and positions clients to not only minimize their risk associated with these dangers, but to profit from them.

Today the financial community generally adheres to Keynesian economic philosophy - believing that government, through significant regulating, spending, and the printing of money, can steer economies towards prosperity and avoid financial calamities. WindRock disagrees. In subscribing to the free market-based Austrian School of Economics, they understand the inevitable repercussions of government intervention. So why are they “entrepreneurial-minded advisors”? Conventional wisdom associates the word “entrepreneur” with the assumption of risk. While risk can never be fully avoided, what actually makes entrepreneurs unique is their understanding of risk. Their unique insight of the risks posed by governmental interference in the economy serves to protect our clients’ wealth. As entrepreneurial-minded advisors, they emphasize independent and creative thought to boldly seize opportunities while minimizing key risks.

WindRock Wealth Management’s sample of current offerings are listed below. These approaches seek yield through uncorrelated hard assets. View the presentation & the videos below for more insight.

1. Secured Private Lending – Private pools of capital can lend money at high interest rates in areas where traditional lenders cannot participate efficiently. These situations, while attractive to many investors, are difficult to access. WindRock assists clients in participating in these situations.

2. Farmland – Buying a farm today requires a significant upfront investment with illiquidity and farm specific risks. WindRock offers organic or conventional alternatives that overcome these obstacles.

3. Rental Real Estate – Today, most commercial real estate (including multi-family apartment buildings) sell at high valuations in both REITs and private markets. With high valuations come lower rental yields. WindRock offers an alternative that focuses on building rental communities that cater to a growing renter-by-choice demographic (www.nexmetro.com).

Wealth Management Firm - Ty Andros, The Sanctuary Fund

Ty began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Diego, and the University of Miami, majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView of which he is the CEO. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis. Ty prides himself on his personal preparation for the markets as they unfold.

Ty is an expert in applying the indirect exchange method as a principle of the Austrian School of Economics in his investing approach.

Investing using ASE: Interviews

01/07/2026 - Wow watch again Dr. Marc Faber & Yra Harris in May of 2025 – How Prescient!

Summary of the discussion:

The discussion argues that the post‑COVID global economy is structurally weaker than in 2018–2019, with a “two‑tier” system in which asset owners benefited from inflation in financial assets while the middle and lower classes suffer from real income stagnation, higher living costs, and much higher interest burdens on credit cards and mortgages. The speakers contend that official inflation data significantly understate true cost‑of‑living increases, liken tariffs to hidden tax hikes, and criticize current U.S. policy for squeezing households while preserving an asset bubble supported by years of artificially low rates. They see many households effectively already in recession and point to weaker indicators such as disappointing travel bookings and rising homelessness as evidence of declining real prosperity and affordability.

On policy and geopolitics, they argue that U.S. interest rates were held too low for too long, creating excessive debt at both government and household levels, and warn that cutting rates now would risk signaling that the Federal Reserve has abandoned any serious fight against inflation, potentially pushing long‑term yields higher rather than lower. Tariffs and great‑power rivalry are framed as part of a long historical pattern, with current U.S. tariff policy described as economically harmful “taxation,” while China’s Belt and Road Initiative is characterized as a politically motivated but economically constructive alternative to military intervention that improves market access and infrastructure for participating countries. They emphasize China’s long‑term strategy to bypass maritime choke points and reshape Eurasian trade routes, contrasting it with what they see as short‑term, often militarized Western approaches.

In markets, they argue that U.S. equities have likely peaked in real terms and that the dollar is overvalued on economic fundamentals, anticipating a multi‑year environment where non‑U.S. markets and select emerging economies outperform after a decade of underperformance. They highlight value opportunities in markets such as Brazil, Chile, Colombia, and parts of Asia (including Singapore, Malaysia, Indonesia, and Thailand), with particular interest in Asian banks, while noting that all markets remain vulnerable when U.S. equities sell off. They also describe Singapore as an increasingly important wealth‑management hub benefiting from political stability and personal safety, attracting capital from across Asia and serving as a kind of “Switzerland of Asia.”

On precious metals and portfolio construction, they maintain a constructive long‑term view on physical gold due to chronic fiscal deficits, growing debt burdens, and what they expect to be structurally higher inflation culminating in some form of systemic “reset.” However, they stress that investors are generally underweight physical gold and discuss platinum as a particularly attractive store‑of‑value candidate, arguing that platinum is historically very cheap relative to gold and may offer better upside with less downside risk, even as central banks are more likely to concentrate their reserves in gold. Overall, the conversation emphasizes risk control over return maximization, urging investors to think less about beating benchmarks and more about preserving real purchasing power in an over‑leveraged, politically fragile, and financially repressed global environment.

10/04/2024 - The Roundtable Insight – Doug Casey on Geo-Political Risks, Gold and Investing in South America

Become a free subscriber by entering your email address in the form below:

04/18/2024 - Get to Know the CedarOwl

Check out our latest posting – Get to Know the CedarOwl … .. learn about how and why we take an approach based on the Principles of the Austrian School of Economics .. also learn the 4 Principles of Market Environmentalism – what these principles are and how they can be used to identify Positive Ideas to help the environment that make not only environmental sense but also financial sense and economic sense! .. also be sure to read the latest views and thoughts of one of our top 10 Most Admired Advisors (MAA) – Dr. Marc Faber – posting will be published tomorrow Friday Apr 19 at 3pm ET and be available fully free to all subscribers!

04/17/2024 - CedarOwl – Russell Napier. Twenty One Lessons from Financial History for the Way We Live Now.

April 15, 2024

This is a timeless lecture by Russell Napier. It is also applicable to the current economic and investing environment. Russell goes through twenty-one lessons from financial history. Download all the slides – link here.

Spend as much time analyzing supply as you spend analyzing demand – the China impact.

There is no relationship between GDP growth and the return from equities – price is what you pay and value is what you get.

Pepper’s law – estimate how long the unsustainable can be sustained – double it and take off a month.

‘Never, ever think about anything else when you should be thinking about incentives’- Charlie Munger.

Governments like markets only when they deliver the prices they want governments do suspend market prices.

The ratio of corporate profits to GDP ratio must mean revert in a free society- one way to do this is inflation.

In assessing the appropriateness of monetary policy assess both the price of money and the quantity of money – banks make money.

The most dangerous form of speculation is the search for yield- ‘John Bull can stand many things but he cannot stand 2%’ Walter Bagehot.

The real danger for investors from populism depends upon the strength of the constitution and the rule of law.

The countries most likely to default on their debt are those that have defaulted on their debt- institutions count.

High equity valuations fall slowly when the surprise is inflation and quickly when it is deflation – our current repression creates a slow decline.

Never buy emerging market equities if the exchange rate is overvalued- an exchange rate policy is a monetary policy.

Tourism is the best guide to whether an exchange rate is over-valued or under-valued always visit to Rockefeller Center at Christmas.

Always buy equites below 10X CAPE unless the future holds – communism, war or a surrender of monetary independence with an overvalued exchange rate.

Democracy is more suited to the operation of capital controls than the free movement of capital.

When private savings are exhausted monetization of government debt and high inflation/hyperinflation follow – savings are not yet exhausted if conscripted.

Technology never ultimately defeats inflation.

Monetary systems fail about every 30 years – the rules of the old system leave a legacy of bad habits for those in a new system.

Money is almost always in disequilibrium.

Never trust a forecast with a decimal point-especially your own.

Extrapolation is the opiate of the people.

CedarOwl Commentary– Some interesting points and observations:

Russell’s biggest theme is on the risks of financial repression – in many of the lessons he discusses in this presentation, he provides ideas to minimize these risks – jurisdictional-focused investing, diversification in asset classes, holding some gold and certain equities to preserve purchasing power, investing in jurisdictions where the rule of law and respect for property rights is strong and maintained, emphasizing equities versus bonds to minimize capital being forced to fund unsustainable reckless-spending governments.

Thinks best to look for undervalued equities in emerging markets where currencies are not overvalued, instead of holding stagnant developed-world overvalued equities likely to go no where (or even losing purchasing power in real terms) in a manner similar to what happened to equities between 1966 to 1982.

Sees a massive disequilibrium, a result of the monetary change in the world today – will likely result in liquidity going to emerging markets, driving emerging market currencies stronger in general. Advises to look for value-based equities in emerging markets instead of growth equities in the indebted western world.

Observes on the variation of the famous Karl Marx quote of “Religion is the opiate of the people” that extrapolation is really the danger as the opiate of the people. Also known as recent bias. Just because the western world countries have led economic growth and enhancement in the standard of living over the past several decades since World War II – does not mean that this trend will go on forever. The western world countries are now heavily indebted, finding it increasingly difficult to even make the minimum payments on servicing their existing unsustainable government debt levels.

Become a free subscriber by entering your email address in the form below:

04/11/2024 - CedarOwl – Dividend-Paying Companies We Invest In – April 2024 Edition

Become a free subscriber by entering your email address in the form below.

Here are just a few of the crowning qualifications that gave us the green-light to feature today’s pick on the first of our monthly series:

This company currently pays about 15% dividend yields.(from stockcharts.com and investing.com)

In addition to dividend distributions, this company shows a potential for capital appreciation, making them potentially promising for both short and long-term strategies.

This company’s business model is currently based on assets in an underinvested, undervalued jurisdiction.

This company deploys great sustainability programs and initiatives.

This company strives towards international-based environmental certification on their assets.

This company is currently leveraging digitalization technologies for growth and operational efficiencies, supportive of UN SDGs 8, 9 & 16.

This company has over 20 years of proven, stable growth since it started in 1991.

This company is publicly listed on two exchanges for ease of access.

Next up, let’s introduce today’s company pick and explore an up-to-date fundamental and technical analysis on its equity share price. Introducing …

Become a free subscriber by entering your email address in the form below:

04/04/2024 - CedarOwl – Introducing the Most Admired Advisors (MAA) – views and perspective of our Top 10 financial advisors, fund and asset managers

If you’ve been searching for a trustworthy monthly pocketbook of trends and insights on the economy and financial markets, this new, recurring segment is for you.

Introducing ‘Most Admired Advisors’ (MAA) by CedarOwl – a monthly report featuring a global top-10 roster of financial advisors, fund and asset managers. We source and cite a distillation of their current, relevant sentiments on trends in the economy and financial markets as a reliable source of insights for our readers.

Our MAA roster is reassessed monthly and stacked against our values and analysis models so you can enjoy an ever-fresh perspective on our category’s thought leadership.

For each economist or manager, look forward to fulsome summary points and observations on their views and perspective on the economy, the financial markets, and their investment ideas.

All taken from publicly linked sources across the open web, including our partners at FRA Roundtable Insight Podcast.

We do the assessment, research and compilation work as a service to you.

Sign up below to become a free subscriber to CedarOwl:

03/28/2024 - CedarOwl – How We are Investing in Green and Clean Nuclear Fusion Energy

Nuclear Fusion as a solution towards the sustainable, green vision that the world has been striving towards has been severely downplayed and relatively unknown. Yet, key players in the energy sector are advancing nuclear fusion technologies, preparing the world for its commercialization as an energy source, presenting potentially enormous investment opportunities. Link to Bloomberg’s article on Nuclear fusion market could achieve a $40 trillion valuation. Does this make your hair stand on end? It should.

CedarOwl’s goal is to shine a light on innovative and profitable answers to the question: How can our global society transition into a silver-lined, sustainable future through technological advancement, idea sharing and investment?

In today’s posting, we explore the current opportunity presented by the advancements in nuclear fusion as an energy source.

What is nuclear fusion, and why has it been downplayed?

Does nuclear fusion make environmental, financial and economic sense?

What are our nuclear fusion investment strategies that leverage key players advancing the technologies, that can help us attain outperforming return on investment (ROI)?

How Does Nuclear Fusion Energy Stack Up?

Industry experts including Doomberg and Goehring & Rozencwajg Associates have highlighted the challenges of the traditional so-called “green” renewable energies of wind and solar in being able to provide green and clean energy:

Low Energy Return On Investment (EROI) – how much energy is required to generate a unit of usable power output – as wind is generally in the 10-to-1 range and solar is generally in the 5-to-1 range, compared to oil/gas/fossil fuels in generally the 30-to-1 range and nuclear fission in generally the 100-to-1 range

Difficulties in sufficiently scaling to meet demands of current and future energy requirements globally – on required sizes, costs and commodity input availabilities

Rising finance costs on wind and solar projects due to rising interest rates and inflation

Declining abilities by heavily indebted governments looking to finance wind and solar projects, especially in the indebted western world characterized by unsustainable government debt and unfunded liabilities

And then there is also nuclear energy. There are two forms – nuclear fission and nuclear fusion.

Nuclear fission energy is available today, is scalable, has relatively high EROI and can be built economically. A reasonable energy transition strategy – towards lowering carbon emissions and migrating away from fossil fuels – is using a mix of all of the above and other developing energy sources, and has been identified by various industry experts including Doomberg – we fully promote this approach.

What about nuclear fusion? What is nuclear fusion energy, how is it different from nuclear fission energy, and why would it make sense to pursue its commercial development? Can it make financial and economic sense?

“Nuclear fusion—the merging of light atomic nuclei—has the potential to produce energy with near-zero carbon emissions, without creating the dangerous radioactive waste associated with today’s nuclear fission reactors, which split the very heavy nuclei of radioactive elements.”

If nuclear energy is such a great solution, then why have seemingly inferior technologies taken the lead in this race?

Fusion is not Fission. They’re both forms of nuclear energy but one is vastly different than the other. Fission energy power plants of old are the source of attitudes stemming from images of meltdowns, toxic radioactive waste and nuclear bomb material proliferation – even though many of these concerns and risks have been largely mitigated through technology and added-value applications and uses.

This isn’t your daddy’s nuclear energy.

In any case, nuclear fusion energy does not pose these risks to the environment and communities.

Summary of Advantages of Nuclear Fusion Energy

Ian Chapman, CEO of the U.K. Atomic Energy Authority (UKAEA), the British government’s nuclear energy organization says we simply have no other long-term way of getting to net-zero carbon emissions, especially because the global energy demand is projected to triple between 2050 and 2100. “Fusion is essential” to meet that need.

Tony Donné, EUROfusion’s program manager says “I can’t see what else it will be” – renewables such as wind and solar energy definitely have a role to play, but they aren’t likely to be enough.

· Abundant energy: Fusing atoms together in a controlled way releases nearly four million times more energy than a chemical reaction such as the burning of coal, oil or gas and four times as much as nuclear fission reactions (at equal mass). Fusion has the potential to provide the kind of baseload energy needed to provide electricity globally.

· Millions of years: Fusion energy commodity inputs are highly abundant globally.

· No CO₂: Scientists, environmental groups and organizations identify the challenge of lowering carbon emissions resulting from human-generated activities globally. While the science is debatable behind to what extent carbon emissions is affecting climate, everyone agrees that is it is best to minimize or eliminate polluting effluents such as carbon emissions into the environment, whether in the air, land or water. As such, nuclear fusion energy doesn’t emit harmful substances like carbon dioxide or other greenhouse gases into the atmosphere.

· No long-lived radioactive waste: Nuclear fusion reactors produce no high activity, long-lived nuclear waste. The activation of components in a fusion reactor is anticipated to be low enough for the materials to be recycled or reused within 100 years, depending on the materials used in the “first-wall” facing the plasma.

· Limited risk of proliferation: Fusion doesn’t employ fissile materials like uranium and plutonium. There are no enriched materials in a fusion reactor like ITER that could be exploited to make nuclear weapons.

· No risk of meltdown: A Fukushima-type nuclear accident is not possible in a fusion energy device. It is difficult enough to reach and maintain the precise conditions necessary for fusion—if any disturbance occurs, the plasma cools within seconds and the reaction stops. The quantity of fuel present in the vessel at any one time is enough for a few seconds only and there is no risk of a chain reaction.

· Cost: The power output of the kind of fusion reactor would likely be similar to that of a fission reactor (i.e., between 1 and 1.7 gigawatts). As with many new technologies, costs will be more expensive at first, when the technology is new, and gradually less expensive as economies of scale bring the costs down. Some links exploring the costs – link here, link here and link here.

Paul Dabbar, former Under Secretary for Science at the Department of Energy, said fusion does have the potential to one day be an affordable power source.

“The fuel is hydrogen,” said Dabbar. “Hydrogen is the most abundant element in the universe, and also on Earth. You know our ability to use that for energy in theory should be quite cheap.”

At the site of the International Thermonuclear Experimental Reactor (ITER), a poloidal field coil undergoes testing. Six of these ring-shaped magnets will steer plasma within the experiment. Credit: Alastair Philip Wiper

The key consideration we take on investing in nuclear fusion energy is our investment approach.

Our approach to investing is based on the principles of a unique school of thought known as the Austrian School of Economics, emphasizing great, high free cash flowing businesses with little or no debt or manageable debt, elements of scarcity and innovation. Our research team has distilled a set of observable and assessable metrics from these principles – there are several studies indicating these metrics have correlation with equity market outperformance, thus providing us with a statistical edge towards portfolio outperformance, although not necessarily guaranteed.

Further we look to assessing the extent to which the great businesses identified are aligned with the principles of Market Environmentalism, a set of 4 principles emanating from the Austrian School of Economics, which overall provide a market-based approach to helping the environment and promoting the 17 UN Sustainable Development Goals (SDGs). We feel this approach provides a better highway to meeting the SDGs versus approaches based on agenda-based environmentalism or approaches which rely on controlling, taxing or outright restricting human behavior, freedoms or liberties.

Given our investment approach in general, we provide consideration to investing in nuclear fusion with an emphasis on these factors:

· We invest in businesses meeting our metrics-based analysis highlighted above and aligned with the principles of Market Environmentalism – businesses that have relatively low or manageable debt, high free-cash-flows from legacy business units, significant to be able to fund the investment into the development of fusion energy on a large scale, and at the same time targeting equity outperformance as a dual mandate

· We invest in businesses that conduct significant fusion energy development or have ownership in private-based fusion energy development companies

· We invest in businesses that provide engineering and support, commodity inputs or specialized products/services in fusion energy power development and operations

To this end, we have identified several public-exchange traded companies which meet the above set of criteria. Let’s have a look at them here ..

Subscribe and Upgrade to Paid Subscription to read the entire Posting:

Disclaimer: This information and material contained in this post is of a general nature and is intended for educational purposes only. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. This post does not constitute a recommendation or a solicitation or offer of the purchase or sale of securities. Furthermore, this post does not endorse or recommend any tax, legal, or investment related strategy, trading related strategy or model portfolio. The future performance of an investment, trade, strategy or model portfolio cannot be deduced from past performance. As with any investment, trade, strategy or model portfolio, the outcome depends upon many factors including: investment or trading objectives, income, net worth, tax bracket, suitability, risk tolerance, as well as economic and market factors. Economic forecasts set forth may not develop as predicted and there can be no guarantee that investments, trades, strategies or model portfolios will be successful. All information contained in this post has been derived from sources that are deemed to be reliable but not guaranteed.

03/23/2024 - CedarOwl – Introducing a new service – “We Invest in Positive Ideas”

CedarOwl: We are excited to very soon be able to offer you a service which we hope you will find to be of value to you. The service focuses on helping to answer these questions:

What are the interesting trends in the economy and the financial markets?

What are the interesting opportunities we are investing in?

Who are the top 10 economists and asset managers – our Most Admired Advisors (MAA) – we think have the best insightful views and perspective on the economy, the financial markets, and interesting investment ideas? And can we summarize what these economists and asset managers are saying in publicly available articles, essays, reports and podcasts in a brief way, saving you time?

What are interesting investing ideas we are using or considering for getting income and dividends? How are we targeting a portfolio with overall income yields of over 10%?

which make environmental sense, financial sense and economic sense?

which are aligned with the positives of human nature?

which we are investing in?

The service will launch very soon within the next few weeks. You can subscribe today with your email address:

Disclaimer: The information and material provided (“Information”) on the CedarOwl substack is of a general nature and is intended for educational purposes only. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. The Information provided does not constitute a recommendation or a solicitation or offer of the purchase or sale of securities. Furthermore, the Information does not endorse or recommend any tax, legal, or investment related strategy, trading related strategy or model portfolio. The future performance of an investment, trade, strategy or model portfolio cannot be deduced from past performance. As with any investment, trade, strategy or model portfolio, the outcome depends upon many factors including: investment or trading objectives, income, net worth, tax bracket, suitability, risk tolerance, as well as economic and market factors. Economic forecasts set forth may not develop as predicted and there can be no guarantee that investments, trades, strategies or model portfolios will be successful. All Information has been derived from sources that are deemed to be reliable but not guaranteed.

02/26/2024 - Alejandro Tagliavini on Argentina President Milei and the Market Economy that was Not

“There remains the hope that he will return to his speech, not so excellent, but in the right direction and adopt a free market economy, liberating, decreasing the weight of the State over the private sector.”

Some good suggestions and ideas towards the end of the essay .. our thoughts and suggestions, which if anyone is interested in expanding into a document to send to President Milei, please contact us:

* a detailed plan with initial quick wins over 3 to 6 months to show good progress in the right direction

* a regulatory review process to eliminate duplicate or outdated or anti-market regulations will help

* an encouragement of foreign direct investments to get dollars and investment flowing into the country will help .. also tax incentives for entrepreneurs and innovators to setup new businesses and thereby hire new jobs

* a promotion of the Argentine tourism industry

* a setting up of an international university like Hayek College in Brasilia Brazil to educate on Austrian School of Economics to Argentinians and to foreign nationals as recognizing Argentina as a new emerging global leader in this economics

contact email – info@cedarportfolio.com

01/31/2024 - The Vision Series – Dr. Titus Gebel and Charles Hugh Smith on the Opportunities and Benefits of International Cities and Special Administrative Zones

The Four Principles of Market Environmentalism emphasize property rights, voluntary exchange, competition, and entrepreneurship as key pillars for environmental conservation.

Applying these principles to sustainable investing involves supporting businesses that respect private property rights by minimizing negative environmental impacts, promoting voluntary exchange of eco-friendly goods, fostering competition to drive innovation for greener technologies, and investing in entrepreneurial endeavours focused on sustainable solutions.

By aligning investments with these principles, one can encourage the growth of environmentally conscious industries while seeking financial returns in a way that benefits both the economy and the planet.

Educational Webinar by The Cedar Portfoliopresented by Founder Richard Bonugli

01/13/2020 - Spanish – Alejandro A. Tagliavini: Invertir en Argentina : ¿en dólares o… en pesos uruguayos?

“El 23% de las empresas recortaría sus inversiones en 2020 y solo un 25% las incrementaría, cuando en 2017 el 81% proyectaba un aumento, según EY. Los empresarios esperan aire fresco del nuevo Gobierno, pero de momento los números no dan. El 55% cree que sus ventas crecerán en 2020 -debido a la inflación, en términos de volumen no son tan optimistas- el 11% que se mantendrán constantes y el resto que caerán. Y asustan las amenazas, como que aplicarán la ‘ley de góndolas’ si las ganancias ‘son excesivas’.”

07/26/2017 - The Roundtable Insight – George Bragues On How The Financial Markets Are Influenced By Politics

FRA is joined by George Bragues in discussing his book Money, Markets, and Democracy: Politically Skewed Financial Markets and How to Fix Them, along with a thorough overview of the Austrian school of economics.

George Bragues is the Assistant Vice-Provost and Program Head of Business at the University of Guelph-Humber, Canada. His writings have spanned the disciplines of economics, politics, and philosophy. He has published op-ed pieces in Canada’s Financial Post. He has also published a wide variety of scholarly articles and reviews in journals such as The Journal of Business Ethics, Qualitative Research in Financial Markets, The Quarterly Journal of Austrian Economics, The Independent Review, History of Philosophy Quarterly, Episteme, and Business Ethics Quarterly.

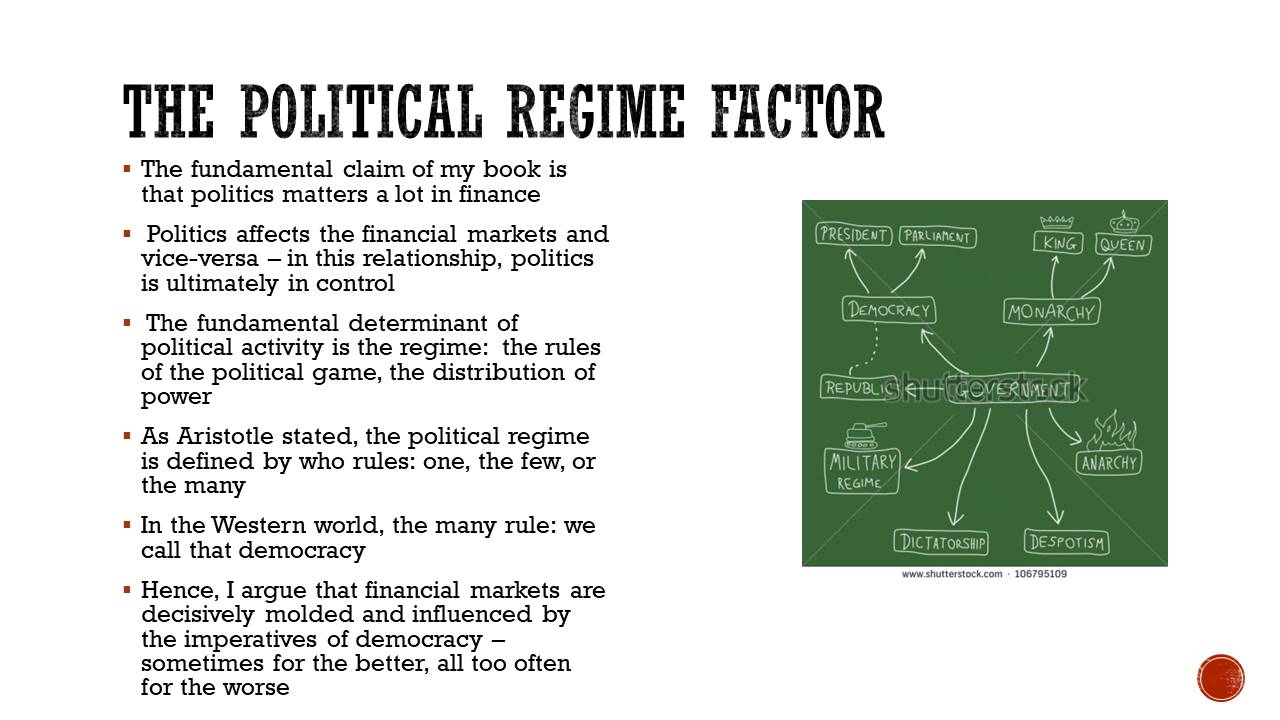

FRA: Just thought we’d begin with the book that you have: It’s called Money, Markets, and Democracy: Politically Skewed Financial Markets and How to Fix Them. Can you give us an elaboration on what the basic messages are, the themes of your book?

BRAGUES: Sure. The key thing I wanted to get across in my book is the importance of politics for understanding the financial markets. This is something that gets often missed in your typical courses that are taught at the MBA and also the undergraduate level. When a student takes a course in investment finance or financial economics, they don’t get exposed a lot to the political factors that drive prices, that drive trends, that drive decisions of monetary policy and interest rates, as was made abundantly clear with the 2008 financial crisis. Though one could have seen evidence of the role of politics in finance earlier than that, but it became much more obvious after 2008. This is definitely a gap in the way financial markets are taught to students, and the way they’re discussed by economists in general. The book is designed to address the flaw that the economics professor tends to be the only one that studies the financial markets. The dominate it, they practically hold the monopoly in it, and other disciplines, specifically politics, need to be part of the mix.

(click to expand)

As the title suggests, it’s not just politics per say, or politics in general that needs to be considered, but the regime. The regime is defined as the fundamental rules of the political game. This is actually a term that comes from the Ancient Greek philosopher Aristotle. He wrote a book – still very well known, still discussed among political philosophers – called The Politics and he distinguishes regimes into three types. He distinguishes it by who rules: if you want to know what a political system is like, you ask yourself who’s running the show, who’s making the decisions. Three basic different types of regimes that are possible: ruled by the one, which we would call autocracy or sometimes monarchy or dictatorship; there’s ruled by the few, which we would call aristocracy or sometimes oligarchy; and then there’s ruled by many. Democracy would be the example of that.

Financial markets around the world today, with only a few exceptions – China primarily among them – most of the major financial markets today are operating within democratic political contexts. The argument I make in the book is that democracy, because of the political incentives that it imposes on politicians because the values – the types of norms and morality a democracy has, these two factors, the value system and political incentives, what politicians need to do to get elected in a democracy – these fundamentally structure the nature of the financial markets. They don’t do it necessarily on a daily basis, you can’t day trade on this information or even swing trade on this information, but it definitely will illuminate anybody who’s involved in investing on the financial markets to help them better understand the force that drive prices over the long haul.

So my thesis is that democracy, while probably the best political system relative to the alternatives, despite it being the best of the available alternatives, it does create problems in the financial markets, it does distort the ability of the financial markets to do social good, and so a lot of the problems that we have are because of the fact that the markets are operating in a democracy.

(click to expand)

FRA: How does that happen? How does democracy distort the financial markets? Could you give some specific examples?

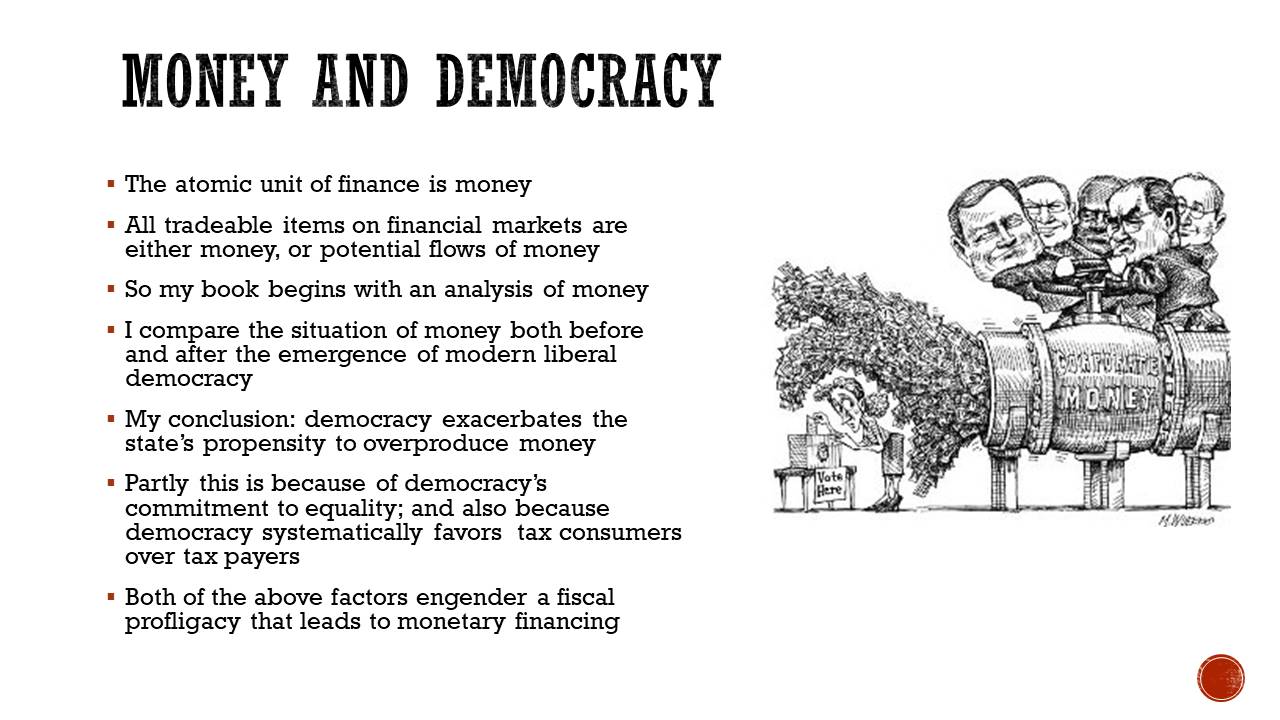

BRAGUES: The big example that I discuss in the book is the money supply. The main argument that I make is that democracies tend to oversupply money into the economy, and that has an impact on the financial system. I distinguish two factors that drive democracy’s overproduction of money, this excess liquidity. One factor is this class conflict between taxpayers and tax consumers. This notion of a class conflict between taxpayers and tax consumers is a notion within Austrian economics and it is meant to replace the Marxist view that the fundamental class divide in society is between bourgeoisie, the capitalists who own property, and the labour working classes who don’t own property. The Austrian view is that the main class division is between those who on net pay more taxes than they receive in services from the government – this group would be the taxpayers – and the tax consumers are those who on net receive more from the government than they pay. In terms of what a tax consumer can receive, this can range to anything from unemployment insurance payments, social assistance payments, favors provided by the government in terms of inhibiting competitors in your industry. The argument is that in a democracy, if a politician wants to get elected, the name of the game is to get 50%+1. Given that the distribution of the income in modern commercial societies tends to be such that there’s a few rich and wealth tend to be a small segment of the population, and the middle class and lower classes tend to be the majority, the best way to get elected is to offer mostly the middle class all sorts of public goods in terms of social programs and so forth, and then have those financed by the well-to-do who would function as the taxpaying class. That way you get your majority and get elected.

(click to expand)

All politicians, whether the left or the right, both sides of the political spectrum do this. Perhaps the left does this with a bit more conviction guiding their efforts, but on both sides of the political spectrum this happens. So politicians engage in this bidding war every time election time comes, trying to offer the majority all these goodies with the idea that they don’t have to pay for it, someone else will. What ends up happening, I argue in the books, is that after a while of this bidding war where politicians offer more and more public goods, someone has to finance this. Eventually you run out of taxpayers or you run into taxpayer resistance. At that point politicians then resort to the bond market and the bond market has proven historically quite eager to lend funds to the government. Government bonds are very attractive investments for a lot of folks because of the safety. This is money that’s backed up by the power of the state, unlike corporate bonds which are not. Corporate bonds are only paid ultimately if the corporation is successful at attracting people to voluntarily buy their goods and services.

I argue in the book that we now have a kind of financial market-government complex, or a bond market-government complex. The bond market has emerged as a kind of handmaiden to the welfare state, this growth of government. At a certain point, even the bond market will say ‘we can’t lend more’ and at that point politicians will appeal to the money press and they will enlist the central bank to print money, essentially, though it’s more complex how liquidity is injected into the economy, but that’s basically what happens. So essentially democracy leads to fiscal profligacy, too much spent relative to the revenues politicians are willing to collect from people. They then have to go to the bond market; public debt rises. And then to increase their options of financing this deficit that is inherent to democracy, they require control over the monetary supply. My argument in the book is that the gold standard, which existed for a good part of the 20th century in one form in another, which ultimately ended in the early 1970s – August 1971 if you want to get exact – that was in a way written in the DNA of democracy; that democracy ultimately is intentioned with a monetary constraint like the gold standard. That’s one of the ways I make this argument that democracies do damage to the financial markets.

(click to expand)

FRA: It sounds like the endgame is either a no bid situation in the bond market, or as you mentioned they could go to the printing presses. The other endgame is the loss of purchasing power in the currency. Either way, I guess that’s likely to be the only way to stop the politicians’ continuous profligate spending.

BRAGUES: Either the bond market has to say no, and historically as mentioned before they’re not very good at saying that. In the book I discuss the historical record of the bond market’s ability to keep governments to account. I remember in the past, I think he’s still around, Ed Yardeni coined the term ‘the bond vigilante’, which was a popular term in the 1990s. The bond vigilante is this creature that’s supposedly watching over governments, closely scrutinizing budgets and if they see any sign that they’re letting public debt out of control these bond vigilantes then start selling off the bonds of the country that’s engaging in this poor fiscal policy. The record, especially with developing economies, is that bond markets only react to excessive public debt very late in the game, when it’s become quite obvious and traders seem very eager to provide money to governments who are spending above their means while the debt is building up. And only when a certain threshold is hit – it’s really hard to find that threshold, Kenneth Rogoff wrote a book a few years ago when he went through the history of it and said, well if it’s a developing country it appears to be about 60% of GDP, that’s when the bond vigilantes come out; developed countries tend to have more tolerance. Even that threshold doesn’t seem to have held, because we now have countries – Japan principally among them – they’re well above 100% GDP and there’s no sign bond markets are growing less willing to finance their debts. The bond markets will have to have a shift in how they approach their investments into bonds.

(click to expand)

The other constraint would be the gold standard, but as I talked about in the book, I don’t totally foreclose the return of the gold standard. I agree that we should try to do as much as possible to bring that back, but democratic politicians don’t want to have the constraints posed by a gold standard because it makes their lives difficult. It means they have to say no to people, it means they can’t win elections by simply promising all sorts of goodies. It’s no surprise to me that the gold standard ultimately disappeared as democracy progressed.

FRA: You’ve included a number of slides, including one slide with a quote from James Grant, editor of Grant’s Interest Rate Observer where he highlights that you not only diagnosed the problem but also proscribed a solution to the problem. As you mentioned on the gold standard, what you’re saying is while not likely to happen, or not likely to come about, you do identify the solution. What is more the endgame: no bid in the bond market or gradual loss of purchasing power in the currency?

(click to expand)

BRAGUES: I would probably say the latter. Especially with the next 20-40 years or so, you have an aging demographic, a greater proportion of people who are older and they will seek safety, and I think that keeps up the bid in the bond market. I would say we have very slow decrease in purchasing power.

The thing is, in part of 1954 inflation was practically nonexistent. You’d have inflation only in certain periods, usually after a war, after substantive crisis, when the government is compelled to appeal to the monetary press to finance conflict. If you look at the data from early 19th century to 1945, I think in Britain for example there was really no change in purchasing power. The Pound was worth around the same in the early 19th century as it was going into the early 20th century. But that’s all changed since 1945. We now live with a situation which we think is normal, but which from a grander scheme of things is not, and people in democracy seems to be willing to live with an inflation rate of around 2% a year. I think governments are going to try to keep that going and if necessary, perhaps tolerate a somewhat higher rate – 3,4,5%. Some economists have talked about that, tolerating a different rate for inflation rate. I think all the incentives are for politicians to continue to take advantage of the bond markets’ generosity, if you want to use that term, and try to finance this via the inflation tax at the highest level of tax that is possible without incurring significant public protest.

FRA: I think we’ve seen figures of if you have inflation at 4% a year for 10 years, it can reduce the burden of debt by one half, something like that.

BRAGUES: Yeah. If you look at history, when we look at how the debt after WWII was dealt with, it was a form of financial repression that took place, where the inflation rate was held higher than the rates that most people be able to gain on deposit. I think they’ll try to appeal to that strategy again.

(click to expand)

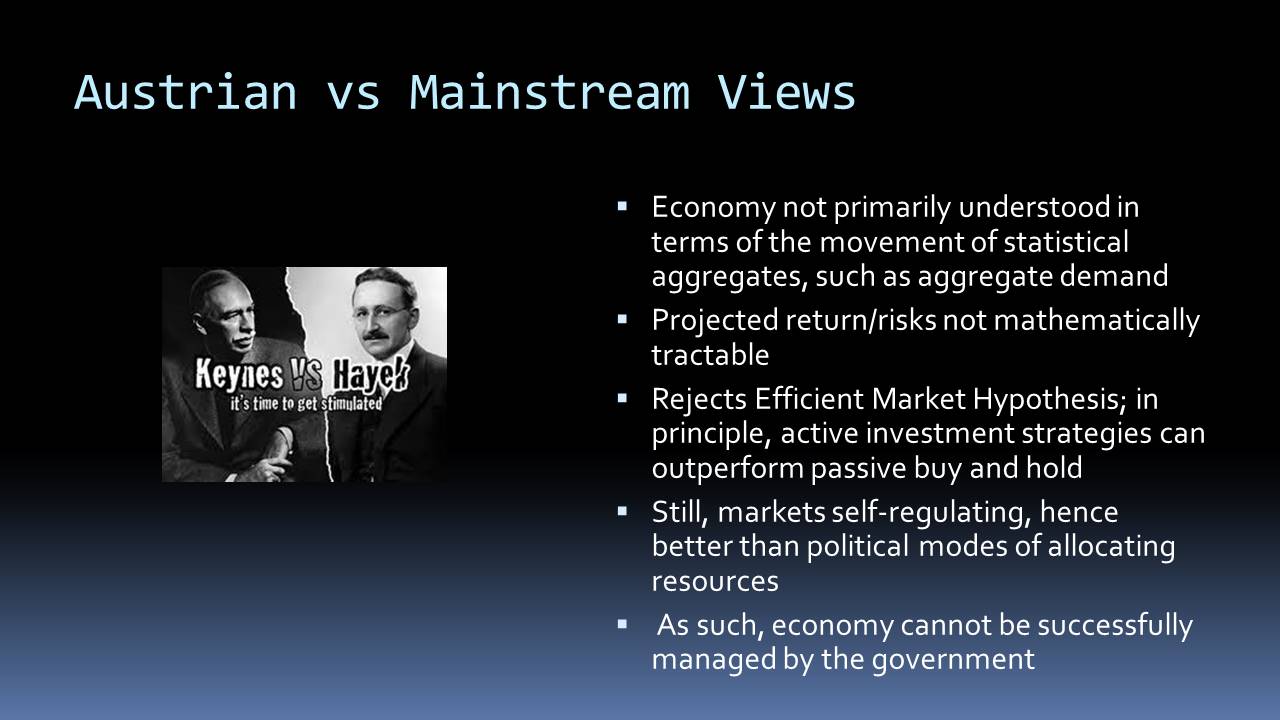

FRA: Yeah, very likely. Just switching gears slightly, we’ve talked about the Austrian school of economics and you’ve also provide a set of slides on the investment potential of Austrian economics in investing. Just wondering if you can give some highlights of those slides and how you see the Austrian school of economics compared to the Keynesian school of economics.

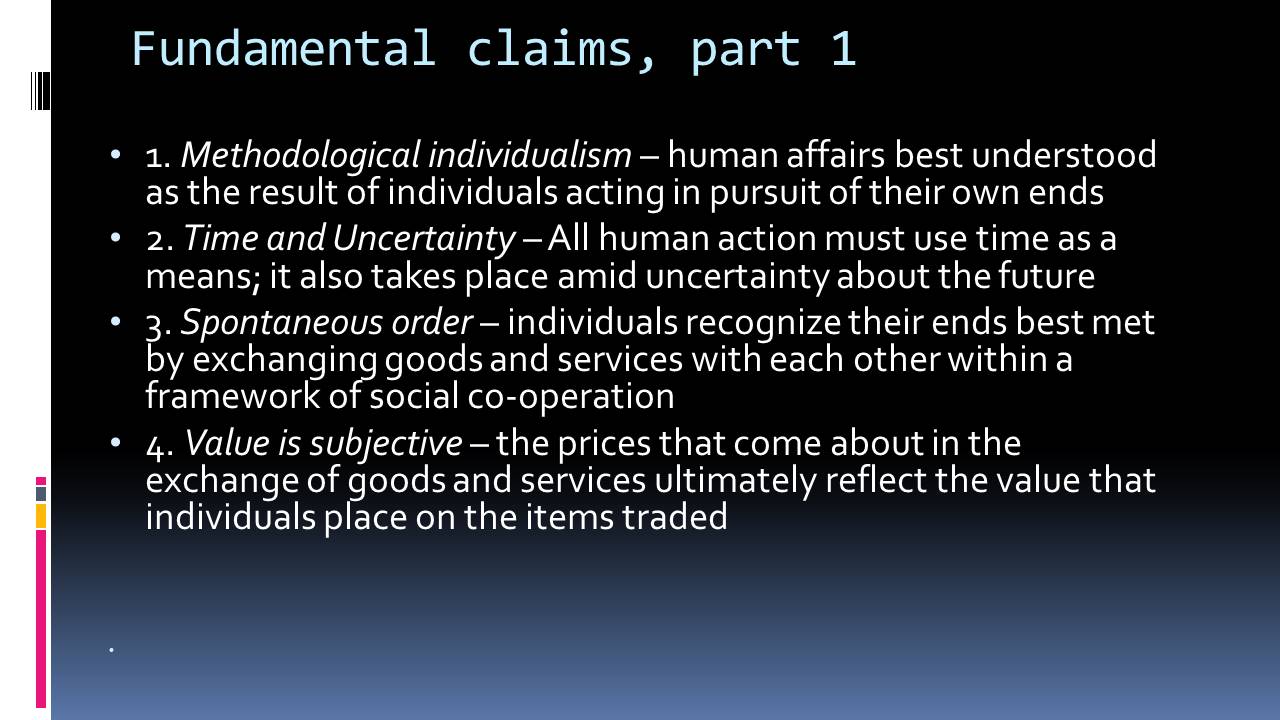

BRAUGES: In terms of Austrian investing, I think it’s a promising approach. In order to succeed in investing, you do need to have an approach that is different from other people because if you’re just doing what everyone else does you’re just going to get at best the average rate of return. You’ll get the same rate of return that you might, say, if passed an investing vehicle like an index fund minus the cost of running your investment, the commissions and so on. Because most people in the financial markets are essentially Keynesians – they may not be conscious fully of their beholden to Keynesian principles, but anyone who follows the markets on a regular basis, specifically on issues of how the Federal Reserve or ECB is expected to react to certain data points, it’s clear that when you see a lot of these analysts get quoted in the Wall Street Journal or the Globe and Mail and so on, that they effectively are operating with a Keynesian worldview. In terms of having a unique point of view that can offer above average returns, I think Austrian economics offers something certainly worth looking at.

In terms of what it boils down to, I’m the first one to admit there’s not set Austrian approach. You can have five Austrians in a room and they’ll have five different approaches, although they’ll come from a common base, that common base being the commitment to certain Austrian economic principles. I say the two biggest ones that are relevant in terms of investing are A: the rejection of the efficient markets hypothesis, which is very common in the academic treatment of finance even though it’s losing some of its support to another field called behavioural finance, which argues that psychology needs to be considered in understanding how markets move. Efficient markets hypothesis still looms large, especially in academia, and it argues that in any point in time prices reflect all available information so that everything that is known or can be known is already in the price. So there’s no point doing any sort of analysis to try and beat the market if you believe in this theory because everyone else has already looked at the financial statements, they’ve already considered the company’s strategy, already looked at the technicals and moving averages and trend lines and all that, it’s already in the price.

(click to expand)

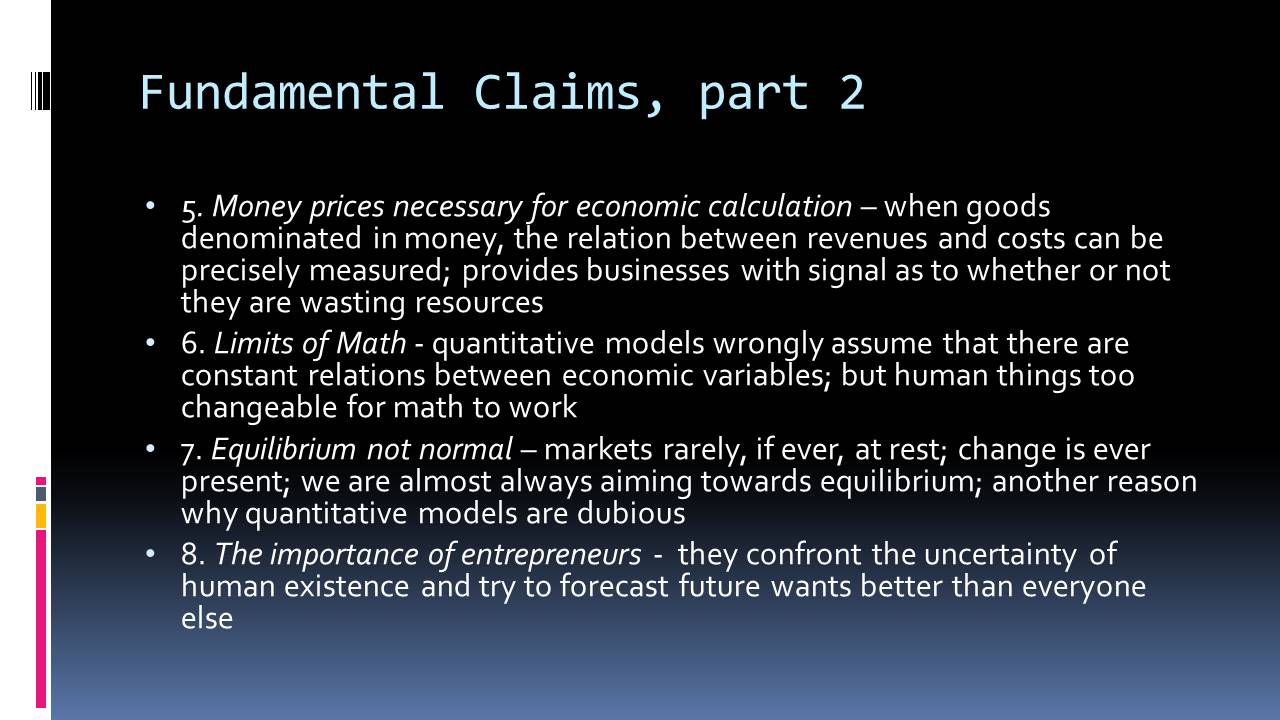

The Austrian view rejects EMH and it’s because of its theory of entrepreneurship. Austrians are very big on the notion that what drives economic activity and specifically economic growth is the activity of entrepreneurs. What entrepreneurs do is they find arbitrage opportunities; they find profit potential that other people aren’t seeing. We can transplant the entrepreneurial function to the financial markets and say that there are similar arbitrage opportunities, similar opportunities that people aren’t seeing, that with good analysis and some work can be grasped. That’s point number one that differentiates the Austrian approach from more mainstream approaches that are taught in academia.

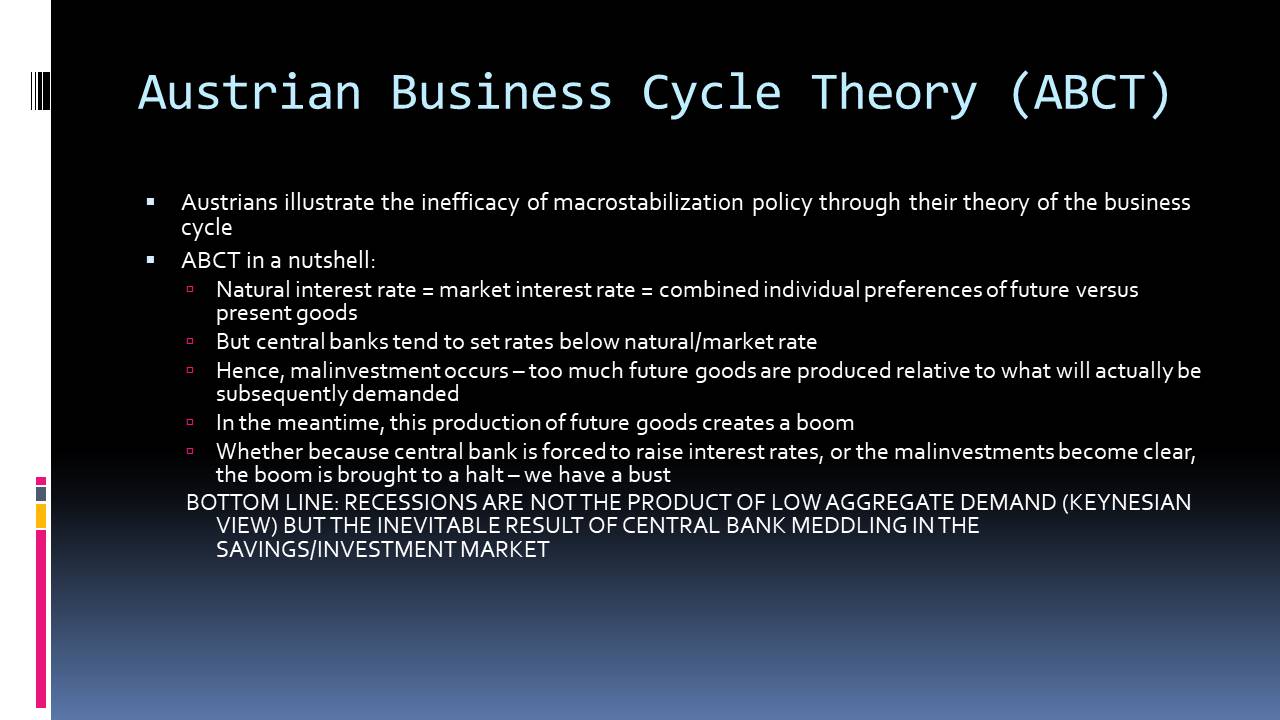

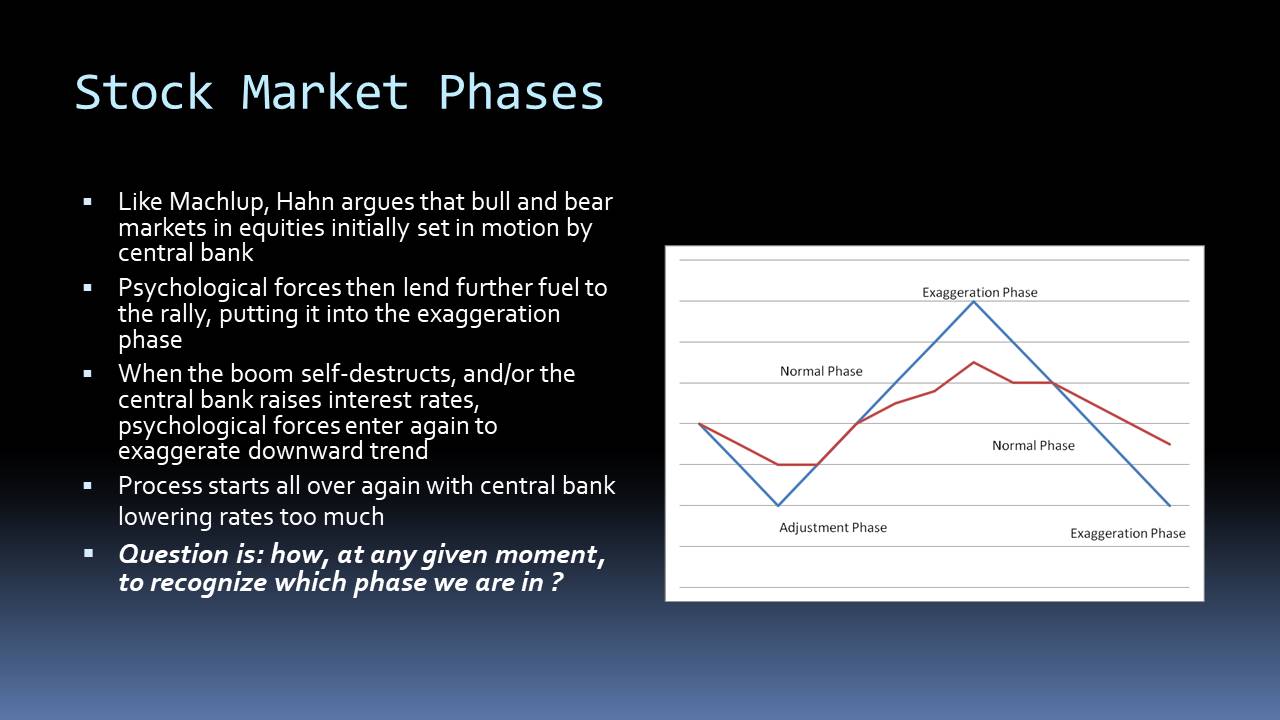

The second component that differentiates the Austrian approach from academic and certainly Keynesian approach, which tends to be dominant among financial market practitioners, is the notion of Austrian Business Cycle Theory (ABCT). This is the argument that central banks, through their policies in terms of money supply and interest rates, artificially induce booms and busts. Booms and busts are not on the Austrian view as simply sort of random events, facts of life of capitalism, or caused as some of the old Keynesians would argue by a lack of aggregate demand. They would argue that the reason we have bull markets and bear markets is large in part because of the actions of central banks. They would argue that central banks have a tendency to run overly loose monetary policies because all of the political incentives are there for that and reinforces that. What happens is that they tend to set the interest rate below what’s called the natural rate. The natural rate would be the rate that the market would set if the interest rate market were free, which it is not when you have a big central bank regularly intervening in the money markets. The argument is that when interest rates go below the natural rate, whenever they’re below what the market would dictate, it gives false signals to investors that future goods, goods with long term – real estate would be the classic example here, but also technology stocks, anything where the payoff is way in the future – those kinds of companies, companies that engage in those products, tend to get overbid. Too much investment tends to flow there and the Austrian view is that this will initially sustain a boom, especially in these areas of the economy, but then at some point one of two things or a combination of both happens: either people realize these investments are not going to work out, that the demand isn’t going to be there, that these future goods everyone’s producing for there isn’t going to be sufficient demand for them so you get a shakeout in that industry. Or two, the central bank decides to tighten monetary policy cause they can sense that things are getting a little too frothy, or a combination of the two. Then you have the bust and the market goes down. The idea is then the central banks will come in while the bust is taking place, aggressively lower interest rates to try to revive things, and the whole cycle starts over again. That’s probably the most important component to the Austrian approach of investment, this acknowledgement that central banks are the ones ultimately behind the longer term ups and downs of the market.

(click to expand)

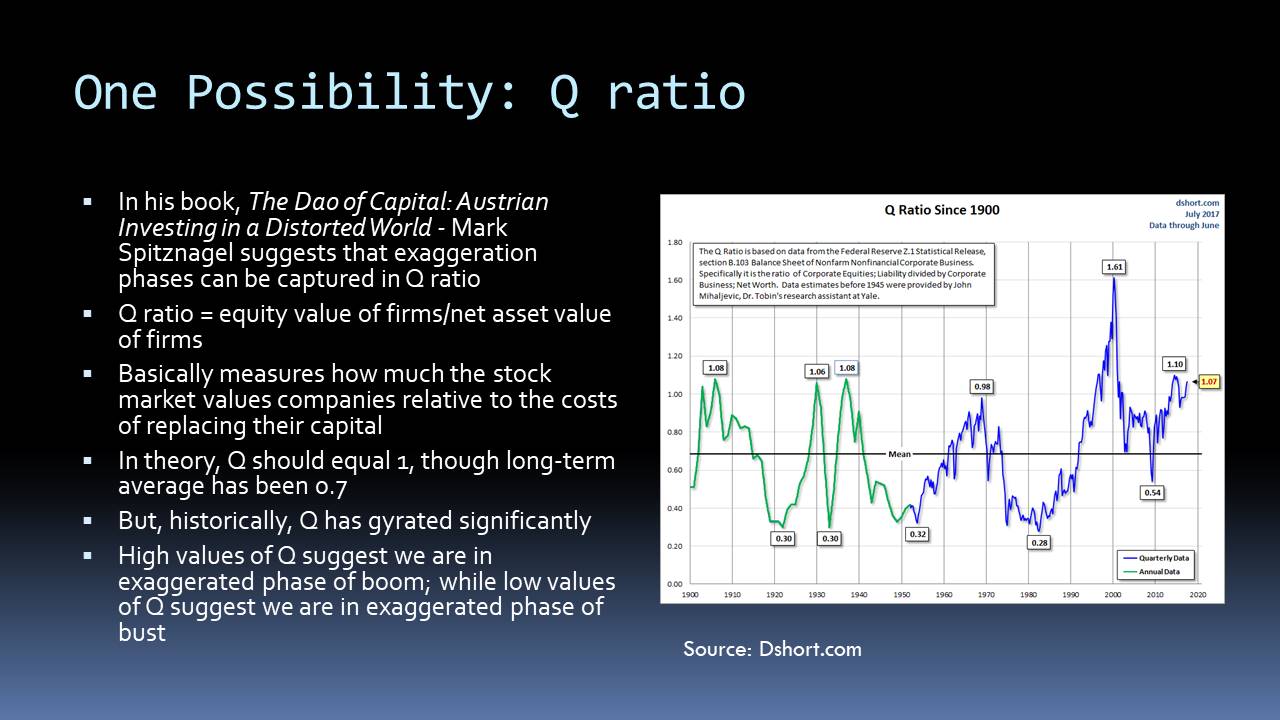

FRA: In terms of other indicators or other aspects of the Austrian school that could help investing, you mentioned a few here like the Q ratio from Mark Spitznagel?

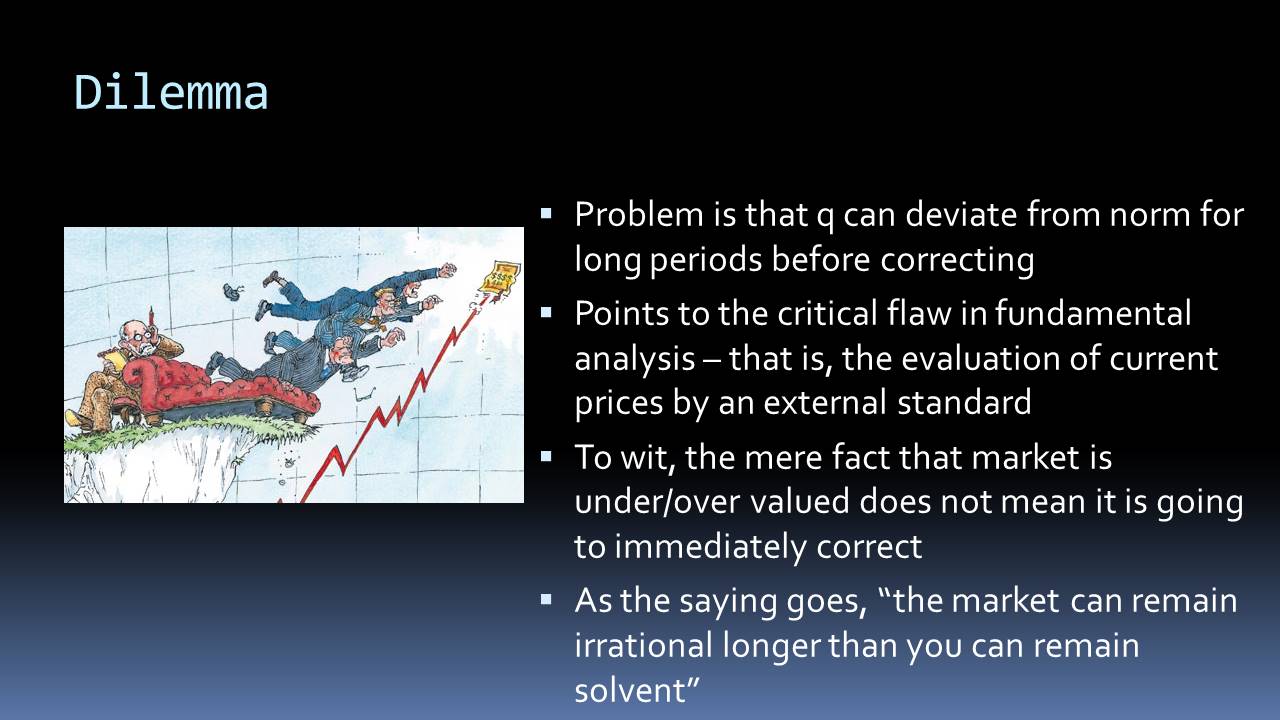

BRAGUES: Because the Austrian school recognizes there are going to be different phases of the stock market where things either get overvalued or undervalued, then the question arises, how do you recognize when we’re in a phase when things are overvalued and where things are undervalued? One approach has been put forward, by Spitznagel as you pointed out – his book is called The Tao of Investing – and he argues that we look at the Q ratio. The Q ratio goes back to James Tobin, a Keynesian economist. Tobin’s Q ratio is based on the numerator being the market value of companies, roughly stock market capitalization, divided by their real asset value, measured by the replacement cost of the assets of the firm. So basically you’re looking at the Q ratio measures how much it would cost to buy all the companies on, say, the S&P500, and you take that number and divide it by what would it cost me if I were to replace all the assets, going out into the real asset market and trying to replace all the assets that are on the balance sheets of S&P500 companies. In theory, it should be 1. That is to say, the market should be valuing the assets at the replacement value. That way you get avoid an arbitrage opportunity. In theory if the market value is higher than the replacement, you can sell stocks and buy the assets. Conversely, if the market value is below the asset value you can buy shares and sell the assets. Historically that ratio has been around 0.7, so Spitznagel suggests we use that as the anchor. If you’re about 0.7, that is suggestive of an overvalued market, and if you’re under 0.7 that would suggest an undervalued market.

Currently I looked at that ratio today and it’s 1.07. It’s not the highest that it’s been historically; it’s been as high as 1.78 in the early 2000s at the height of the Dot Com boom. Currently at the 1.07 level it’s at similar highs at other turning points if we just take the early 2000s out of the picture. If we look at early ‘70s was another high, another high was just before 1929. If you look at the Q ratio that is suggestive that we may be at a key inflection point here. My only concern with the Q ratio, just like I would have any concern with any other fundamental type of metric, whether it’s P ratio or price-to-sales ratio or peg ratio, is that they can show for a long time that an asset is overvalued or undervalued, and if you were to take a position in accordance with that signal it could take a long time for it to actually go in the predicted direction. It’s a notorious problem with these kinds of signals, so I suggest that Austrians can apply technical analysis and the approach here would be you use some sort of long term moving average – this would be just one technique among several that you could use to gauge the long term trend – and you take advantage of the trend and you wait until the trend is broken. If you’re using, say, a 10 month moving average then you wait for the index – here the S&P500 – to close below that average at the end of the month and that would be your signal that, okay, it’s a frothy market but other people are recognizing it, it’s not me with my Austrian analysis and now that the market seems to be coming to realize what’s going on I will get out. And conversely when things are looking undervalued. So an Austrian analysis could tell you things are looking undervalued now, the bust has perhaps gotten a little too far, people have gotten a little too fearful, a little too anxious, but you wouldn’t immediately go in. You would wait until the market went about the 10 month moving average.

(click to expand)

I would argue this would avoid the problem of using something like the Q ratio or some sort of P/E ratio. You could also use the 10 year P/E ratio, which is like Shiller’s – Robert Shiller has that indicator – that you allow the market to tell you when the trend is over, when the frothiness is really done. I’ve done some back-testing on; it seems to work fairly well. There’s also a number of people out there that follow this method, but most people follow the method of just look at the moving average; they don’t come to it with an Austrian understanding of where the market is temperamentally, as it were – whether it’s undervalued or overvalued, just looking at pure trend.

FRA: Another aspect of the Austrian school would be the focus on stores of value. You mentioned you have a slide here about gold, if you want to talk to that a bit in terms of how that can play into a store of value.

BRAGUES: Sure. One thing that Austrians can sometimes fall into the trap of is becoming excessively pessimistic. There are good reasons to be excessively pessimistic when one considers the fiscal state of our governments, and that what central banks have been doing to finance that fiscal profligacy. The reality is that markets seem to do different things that what some Austrians who are really negative would predict. Spitznagel makes this point in his book as well, that Austrians need to be careful of getting a little too pessimistic. That might translate into going into 100% gold; I would not be in favor of that going into 100% gold position. I do believe that it is a good store of value, to use your phrase, and at least some portion of one’s portfolio should be in gold for several reasons:

We really don’t know how this whole thing is going to play out in terms of these highly indebted states and central bank excess liquidity that’s been provided, so we’re not sure how that’s going to play out. It could play out very ugly; my Austrian friends are among those that are very negative and they may turn out to be correct. You want to have a position in your portfolio where you profit from that, or you protect yourself from that. Also two, if as I expect, we’re going to have this continuous slow reduction in purchasing power, whether it’s 2%, 3%, 4%, whatever it is, that does have a long term impact. That does compound and gold has proven able, when looked at form a longer term trajectory, to preserve your purchasing power against that.

(click to expand)

I just did this calculation today, but if you look at the returns of the S&P500 index, total returns assuming you invest all your dividends? From 1971 when the gold standard ended and you compare it to gold, I think there’s only about a—If you put your money in the S&P500 and invested your funds when the gold standard was abandoned in August 1971, you would have made about 10.38% a year, just over 10%. If you had just put it in gold, you would have been at 7.58%. So you’re only looking at about just under 3% differential. That’s not bad. Gold is… You’re not risking your money and businesses, when you invest in gold you really can’t expect that you’re going to earn a risk premium that a firm would typically be expected to earn for assuming risk in the marketplace and offering goods and services. There’d only be about 3% behind, and this is from the current day when gold is relatively low and well off its highs from 2011 and the S&P500 is at near all-time highs. Right now this calculation is very much favoring the S&P500 but over time gold doesn’t do too badly, even though things right now might not look too great in terms of its performance vis a vis the S&P500 index. But looked at it from a longer term? It does trail, but you’d expect that because the S&P500 is a different kind of investment; you’re investing in companies and there’s a risk there. You should be compensated for that.

From a crisis protection point of view, and also from a protection from this continuous reduction in purchasing power, I think that argues for some proportion of portfolio being in gold.

FRA: Excellent comments, excellent view. I guess to close out, if we take the Austrian school of economics and the basic messages and themes of your book on money markets and democracy, how do you see the situation today in terms of perhaps the millennial generation? Where they’re going, where they’re leading politics with respect to economics, finance? What are the millennial views and perspectives on the economy and financial markets currently? How are these views being formed by political, financial, and economic trends?

BRAGUES: The millennials… That’s a pretty slippery term to define; we’ll go with 18-29 year olds. This has been a talking point for the last year or so and it’s certainly became a major point of discussion with the success of the Bernie Sanders campaign – they didn’t win the nomination, he didn’t win that, but he certainly put forward quite a battle to Hilary Clinton. There was a survey done by Harvard University, it came out just over a year ago, which showed that millennials in the United States – so these are young people from 18 to 29 – for the first time since they’ve been doing surveys, that a majority of them no longer supported capitalism. The number was actually 51% no longer supported capitalism, 42% still supported capitalism – I’m not exactly sure with the remainder, I’m assuming they were undecided. Certainly with Bernie Sanders, who is a self-professed socialist or social democratic or ‘democratic socialist’ as he put it, certainly this played out politically. This is a concern though we shouldn’t make too much of it, but it is definitely a concern. I think the reason why we should not overplay it is that traditionally young people have veered more toward the left. If you look at voting patterns, for example Britain, the likelihood of someone who is young voting Conservative – I’m not saying the Conservative Party in Britain are perfect pro-capitalists or pro-markets, but they’re more likely to be pro-market than the Labour Party on the left on the political spectrum. Going back to the end of WWII, younger people were much more likely to vote for Labour or for some other party on the left than for the Conservative Party. As people get older, they tend to veer conservative. There’s this saying that if you’re not Liberal before leaning left when you’re under 30, you have no heart, but if you’re still Liberal after 30 you have no head. It nicely captures out how age affects political and ideological affiliations.

When we consider that, that means we should moderate some of our concern, but it’s still a concern. The question arises, why? I think there are a number of reasons: one is they’re just young, they’re more moved by their passions, morality is very much implicated with their passions or moral sensibilities and young people tend to be quite idealistic. When you look at capitalism, it – at least on the face of it, I wouldn’t say this is the definitive interpretation of it – it looks like it’s driven by selfishness or self-interest. If you’re idealistic that’s not a good motive to have, that’s not a good motive for society to be energized by. That, I think, is a factor that leads the young away from capitalism.

Another factor is just the educational system. Despite all the work that the Milton Friedmans and the Hayeks and the Miseses of the world – which is great work, great books, great arguments – all that effort still hasn’t made its way into the educational system where young minds are formed. I think too there’s certain factors of the way the human mind works against the proponents of capitalism and makes it more difficult for the pro-capitalist side to make its argument. The human mind is structured in such a way that we tend to favor the concrete over the distant, the specific over the vague. Whenever you make a case for capitalism you have to make arguments that are abstract, that tend to emphasize longer term benefits, things that are not immediately evident. That’s a problem that the opposite side, the side that the government is having a greater role in the economy, they don’t have that problem.

My favorite example is, let’s say you think there’s a problem with wages, that some people don’t make enough money. The free marketeer could tell you the story, well if you let wages be free eventually people will acquire skills, will have an incentive to do so, will invest in education or work harder to get promoted, and eventually they’ll get up the income scale. That’s sort of a more longer term view and it can be mentally grasped, but it’s a lot more clear and vivid if you could just tell people, or we could pass a law and we can set a minimum wage at x level where we think people are going to be less poor. And there’s the end of the story. There’s an easier story that the other side has to tell, and I think that plays into this situation with the millennials.

05/31/2017 - Thorsten Polleit: The Fiat Money System Might Be Held Up For Longer Than Some May Fear And Others Might Hope

“The still very low long-term interest rates in the US may, therefore, tell us something important: Investors expect the Fed to keep rates at fairly low levels in what lays ahead; they expect the central bank to refrain from returning yields to levels formerly considered ‘normal.’ Against this backdrop, the latest series of rates increases is merely seen as a cosmetic adjustment .. The US economy, and with it the world economy, is caught between a rock and a hard place. Maybe the Fed’s current rate hiking spree will bring about the bust. Or the Fed refrains from raising rates further and keeps the boom going a little bit longer. Ludwig von Mises put the predicament as follows:

The boom cannot continue indefinitely. There are two alternatives. Either the banks continue the credit expansion without restriction and thus cause constantly mounting price increases and an ever-growing orgy of speculation, which, as in all other cases of unlimited inflation, ends in a “crack-up boom” and in a collapse of the money and credit system. Or the banks stop before this point is reached, voluntarily renounce further credit expansion and thus bring about the crisis. The depression follows in both instances.

Given current bond and stock market valuations, investors seem to be fairly confident that the Fed will succeed in keeping the boom going, that the central bank will not overdo it in terms of raising interest rates. And yes, perhaps central bankers have learned a great deal in recent years, having become true maestros in holding up the make believe world of fiat money. The investor should be aware of the damages caused by fiat money — for instance, boom and bust. At the same time, he should not run for the exit prematurely: The fiat money system might be held up for longer than some may fear and others might hope, so that keeping inflation-resistant assets may be more rewarding than betting on an imminent system crash.”

01/07/2026 - Wow watch again Dr. Marc Faber & Yra Harris in May of 2025 – How Prescient!

01/07/2026 - Wow watch again Dr. Marc Faber & Yra Harris in May of 2025 – How Prescient!