The lower limit ultimately depends on costs associated with holding cash. Before this happens, however, it is possible that frictions will occur which reduce the impact of cutting the repo rate further. In addition, risks to the financial system will increase the lower the rate goes. One important factor that is difficult to assess is also whether negative policy rates change the behavior of households and companies.

Rogoff: Costs and benefits to phasing out paper currency

This paper explores the costs and benefits to phasing out paper currency, beginning with large-denomination notes, later extending to all but small coins and bills, and eventually those as well. It is hardly a simple issue; paper currency is deeply ingrained in the public’s image of government and country, and any attempt to change long-standing monetary conventions raises a host of complex issues.

Fed (New York): If Interest Rates Go Negative . . . Or, Be Careful What You Wish For

We suggest that significantly negative rates—that is, rates below -50 basis points—may spawn a variety of financial innovations, such as special-purpose banks and the use of certified bank checks in large-value transactions, and novel preferences, such as a preference for making early and/or excess payments to creditworthy counterparties and a preference for receiving payments in forms that facilitate deferred collection.

Fed (Richmond): Overcoming the Zero Bound on Interest Rate Policy

The paper proposes three options for overcoming the zero bound on interest rate policy: a carry tax on money, open market operations in long bonds, and monetary transfers. A variable carry tax on electronic bank reserves could enable a central bank to target negative nominal interest rates. A carry tax could be imposed on currency to create more leeway to make interest rates negative. Quantitative policy–monetary transfers and open market purchases of long bonds–could stimulate the economy by creating liquidity broadly defined. A central bank needs more fiscal support than usual from the Treasury to pursue quantitative policy at the interest rate floor.

…central banks may then need to think imaginatively about how to deal on a more durable basis with the technological constraint imposed by the zero lower bound on interest rates. That may require a rethink, a fairly fundamental one, of a number of current central bank practices.

What Lower Bound? Monetary Policy with Negative Interest Rates

…gains from negative rates depend inversely on the level and elasticity of currency demand. Credible commitment by the central bank is essential to implementing optimal policy, which backloads the most negative rates. My results imply that the option to set negative nominal rates lowers the optimal long-run inflation target, and that abolishing paper currency is only optimal when currency demand is highly elastic.

BoC: The International Experience with Negative Policy Rates

A key issue in the renewal of the inflation-control agreement is the question of the appropriate level of the inflation target. Many observers have raised concerns that with the reduction in the neutral rate, and the experience of the recent financial crisis, the effective lower bound (ELB) is more likely to be binding in the future if inflation targets remain at 2 per cent. This has led some to argue that the inflation target should be raised to reduce the incidence of ELB episodes. Much of this debate has assumed that the ELB is close to, but not below, zero. Recently, however, a number of central banks have introduced negative policy interest rates. This paper outlines the concerns associated with negative interest rates, provides an overview of the international experience so far with negative policy rates and sets out some general observations based on this experience. It then discusses how low policy interest rates might be able to go in these economies, and offers some considerations for the renewal of the inflation-control agreement.

OVERCOMING THE ZERO BOUND WITH NEGATIVE INTEREST RATE POLICY

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/04/2016 - Bill Gross: Central Banks’ Low Yields And Financial Repression Is Not Helping The Real Economy

“Central banks all seem to believe that there is an interest rate SO LOW that resultant financial market wealth will ultimately spill over into the real economy. I have long argued against that logic and won’t reiterate the negative aspects of low yields and financial repression in this Outlook. What I will commonsensically ask is ‘How successful have they been so far?’ Why after several decades of 0% rates has the Japanese economy failed to respond? Why has the U.S. only averaged 2% real growth since the end of the Great Recession? ‘How’s it workin’ for ya?’ – would be a curt, logical summary of the impotency of low interest rates to generate acceptable economic growth worldwide. The fact is that global markets and individual economies are increasingly ‘addled’ and distorted .. What I do know is that our finance-based global economy is transitioning due to the impotence of monetary policy which has always, and is now increasingly focused on the elixir of low/negative interest rates.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/03/2016 - Amin Rajan: HOW PENSION PLANS ARE RESPONDING TO FINANCIAL REPRESSION

Chief Executive of CREATE-Research, Amin Rajan discusses investing in the age of financial repression as well as key points for risk mitigation with FRA Co-founder Gordon T. Long. CREATE-Research is a a network of prominent researchers undertaking high level advisory assignments for governments, global banks, fund managers, multinational companies and international bodies such as the EU, OECD and ILO. In 1998 Amin was awarded the Aspen Institute’s Prize in leadership. It is a subject on which he has done extensive research involving some of today’s outstanding business leaders. In two resulting publications, he has developed a close link between leadership and the emerging business models.

As well as appearing on radio and television regularly, he has contributed feature articles to The Financial Times, The Guardian, The Sunday Times, and The London Evening Standard and IPE. He has published reports and articles on leadership, business cultures, strategic change, globalisation, new technologies, and new business models. He has presented the results of his work at over 100 major events in the USA, UK and Asia-Pacific in the last five years. His expertise covers, amongst others, leadership and new business models in financial services. As an economist, he has held significant positions, including, Secretary; Economic Group, Cabinet Office, providing weekly briefs to the Prime Minister. And as a Forecaster; UK Treasury’s Econometric Model, producing forecasts of key macro indicators.

“Financial repression results from a combination of low interest rates and rising inflation. Authorities are keeping interest rates low so they can manage their huge debt and furthermore they’re attempting to spike up inflation as a means to eliminate this debt. This combination of low interest rates and rising inflation results in an arbitrary redistribution of wealth from investors to borrowers.”

PENSION PLANS AND SMARTER ASSET ALLOCATION

Risk in equity markets are currently at their all time high. We have a lot of conviction-less trade which means people are taking high amounts of risk because they have no other choice. Under this new approach to asset allocation, a number of things are happening:

They are taking much more risk in order to get higher return.

Trying to look for uncorrelated assets

Having a very broad diversification which covers different geographies, different asset classes etc…

Practising dynamic investing

In today’s markets lucrative opportunities do appear but they vanish as soon as they appear which results in a tendency to capture value as soon as value appears. Pensioners have been pushed up the risk curve and as a result their main view is they ought to be as opportunistic as possible and get out at the first sign of concern. What they are essentially doing is rebalancing their portfolios much more now than they have ever done before.

Dynamic investing has become the norm in that you have to be very vigilant from where your returns are coming from, how quickly they’re materializing and how nimble can you be in ensuring you are capitalizing on those returns. As a result of difficulties in seeking non-correlated assets, institutional investors are moving towards risk factor diversification. They are identifying various risks and are identifying various assets which allows them to compensate for that risk.

“Authorities are looking at all the factors which contribute to portfolio risk and undoubtedly the biggest risk at the moment is policy errors on the part of the Federal Reserve.”

There are many risks lurking in the background, risks such as QE. The challenge is to construct a portfolio which factors in such risks. In the past there was tendency to go for stop-loss mechanisms or to go for options contracts, in order to protect the downsides. What we are finding now is there has been so much volatility in the market that many of these stop-loss mechanisms get activated from the wrong information.

IDIOSYNCRATIC RISK

“Idiosyncratic risk Deals with the fact correlation between asset classes is very difficult to avoid which essentially makes diversification seemingly ineffective.”

We find that all asset classes are highly inflated in values simply because of central bank action. We find that the real returns come from finding individual opportunities at the most micro level. Idiosyncratic risk is about looking at very specific investment opportunities, assessing their risk parameters and making a decion to act upon it or not. These broad brush approach ways in investing just do not work; you have to be much more specific. It is about understanding the risk parameters about specific investment opportunities and understanding what are the inherent risk and opportunities and figuring out how to minimize the risks while maximizing the returns.

“Growth is what everybody is looking for and it is truly what keeps people awake at night.”

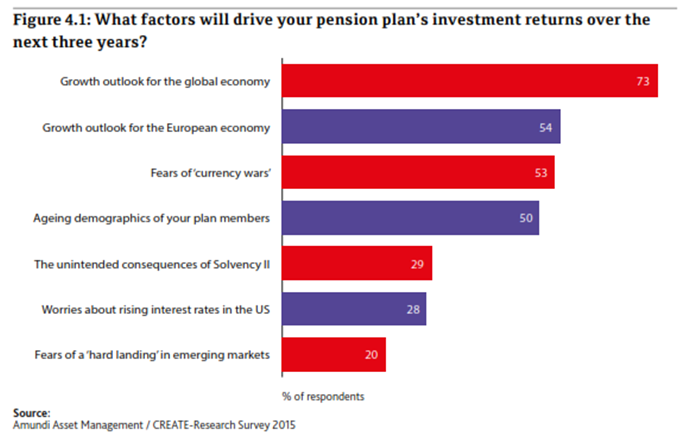

In regards to figure 4.1, what we try to do before asking investors about their asset allocation approaches, we try to find out what they think will be driving the markets over the next 3 or so years. The most common response we got was growth in global outlook and growth in the European economy. There are worries about currency wars, since the beginning of last year we have had 25 nations around the world that have devalued their currencies. Things like aging demographics are having major effects on pension plans because due to the baby boomer generation a mass influx of people will be coming into retirement, and this will dramatically change the asset allocation of pension plans or of individuals who are managing their own funds.

QE programs inflated asset values for both equities and bonds and that saved the day. Now we are in a situation where these asset values are not sustainable in light of economic performance from the last two years or so. We hope that growth will resume, we hope that the situation in China and Japan improves and so on. But if these conditions do not happen we will be in a situation where the current valuation will be very hard to sustain and we could be looking at another major correction.

“Growth has slowed down everywhere. In Europe and Japan we are talking about another round of QE. The biggest worry in all this is that this drug of QE worked in the beginning but for it to work again we have to come out with bigger and bigger doses.”

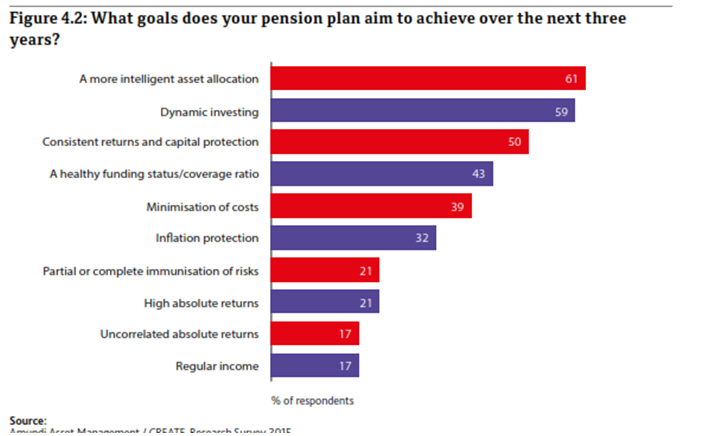

THE GOALS OF PENSION PLANS

“They key is to try and be a smart investor, don’t continue old trends because that is a recipe for disaster.”

Four key ideas that pension plans have is:

Don’t follow the herd: Have an intelligent asset allocation. Engage in asset allocation which firmly addresses your long term liabilities.

In so far as long as good returns will come from idiosyncratic forces try to engage in dynamic investing. Identify opportunities, identify value traps, know the difference between the two and take advantage whenever opportunities arise.

Go for consistent returns and capital protection: If pension plans experience big losses now, it will take a very long time to reconcile those losses. Because of the fact we are in a low return environment you cannot afford to take big hits.

Healthy funding levels: At the moment the funding levels are not good in any part of the world except for Canada. In the US every funding level in the private sector is about 78 and numbers do not vary much in the UK, Japan and other markets.

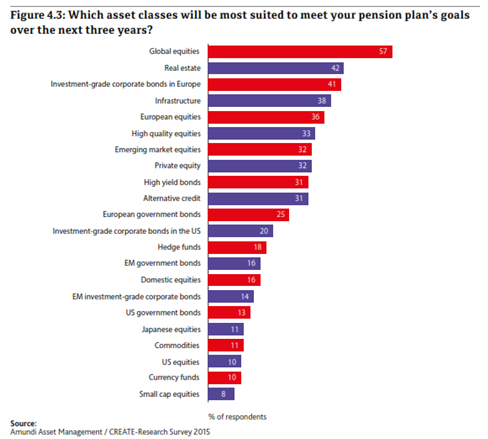

MACRO RISKS TO IDIOSYNCRATIC RISKS

What we did was analyze amongst these asset classes which ones are people most likely to fear. And sure enough at the top came out global equities and real estate. Secondly, within these asset classes are people going to use them the same way they have in the past? For example, to think that as long as you’re invested in global equities you will be okay or are you going to be much more selective? We concluded that being selective is definitely the way to go, to be very selective in the way we invest in global equities, real estate etc.

It used to be a belief that fixed asset allocation in numbers would follow as well as that 90% of returns come from doing the right asset allocation. Now this is outdated and nobody holds on to those beliefs anymore. If we believe in this we will only think that some 50% of returns come from correct asset allocation and the other 50% comes from making the right choices of specific securities.

THE AIMS OF ASSET MANAGERS

“There is a rampant feeling that we are entering a long period of low returns. QE isn’t going to work second time around in the way that it worked the first time. It has lost its potency.”

What asset managers need to do is having their business models change in four fundamental ways:

Asset managers need to get much closer to their clients. Understand their clients risk profiles, identify if clients are being provided service that they need and so on. Client focus is paramount.

Investment Capabilities: What makes an investment professional at a time when markets are so distorted? It is a tough question to answer but I believe an investment professional should know the difference between value traps and value opportunities. The fact that markets are falling in emerging markets does not necessarily mean that it is a great buying opportunity. A smart investor knows that emerging markets have very strong price momentum. Prices in these markets have tendency to be falling for much longer.

Understanding correlations under different phases of market cycles: Yes, correlations are rising but what we also find is that there are different regimes emerging. Under certain regimes correlations are higher and under others they are lower. Learn to understand what those different regimes are and then devise your portfolio accordingly.

Alignment of interest: Asset managers need to have a strong financial alignment of interest. It can be from having things such as performance related fees or making sure they are not a part of a structure which basically says, heads I win and tails you lose. Innovation processes that asset managers have need to be rethought. Products need to be tested and tried before being released.

A link to Amin Rajans’ full report, Investing in the Age of Financial Repression can be downloaded at

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

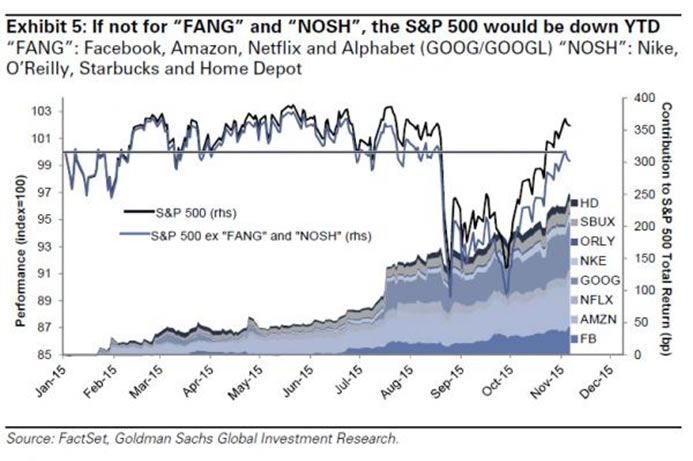

02/03/2016 - RISK MITIGATION: FRA Warns to Beware of the FANTAsy of ETFs

The rise of index ETFs and mutual funds which all depend on the FANTAsy stocks, has never accounted for this much of the market before. The rapid emergence of Index ETFs accounted for nearly 30 percent of the trading in the U.S. equities market last summer. FANTAsy weakness will magnify, or even potentially cause flash crashes if they break critical support levels. This is an untested $1 trillion stock bubble problem! The FRA examines the problems and where FANTAsy may be headed.

FANG & NOSH

As we entered Q4 earnings season and the economic news continued to deteriorate, it was clearly evident that we had eight stocks called “FANG & NOSH” holding up the US equity markets. Market breadth had collapsed but not the indexes – yet!

“FANG” STOCKS

Facebook,

Amazon,

Netflix and

Google

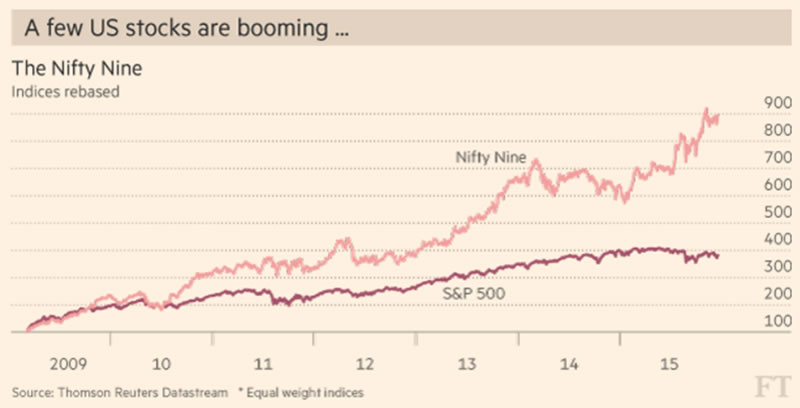

THESE EIGHT BECAME THE “NIFTY NINE”

While the S&P languishes unchanged in 2015, these small groups of overwhelmingly propagandized stocks were up on average over 60%, but with a collective P/E of 45, they were not cheap.

Ned Davis Research identified the NIFTY NINE in December, which added the following to the four FANGs:

Priceline,

Ebay,

Starbucks,

Microsoft and

Salesforce. (Note that Apple appears on neither list which until recently was THE MARKET and accounted for 20% of the underlying Margin Expansion since 2010.)

WE HAD FALSE EUPHORIA CENTERED ON 9 STOCKS

This was very similar to what we have witnessed at all bubble tops.

Only the names change (the 4 Horsemen in the Dotcom Bubble run-up: Cisco, Intel, Microsoft & Qualcomm) and the rationalization hype (2000: “new economic paradigm”)

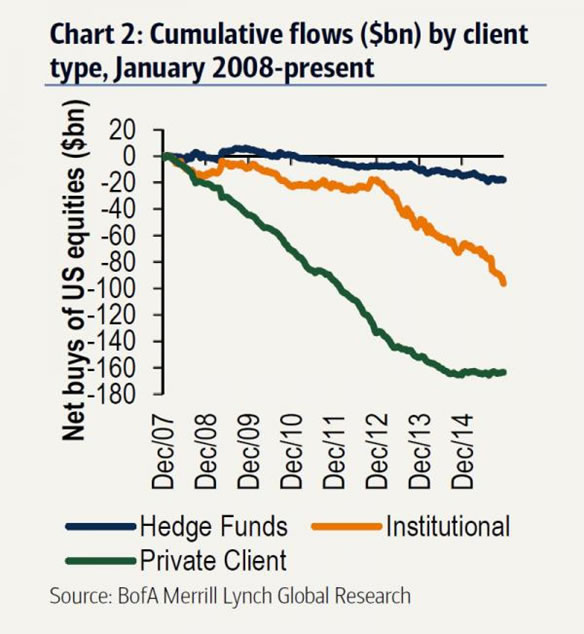

“NIFTY9” HID THE FACT THAT INSTITUTIONS HAD LEFT THE PARTY

Institutions were seeing the following Sales Growth was no longer there,

Earnings were steadily falling,

Companies were spending more on Buybacks and Dividends than they were actaully earning:

Almost 60 percent of the 3,297 publicly traded non-financial U.S. have bought back their shares since 2010.

In fiscal 2014, spending on buybacks and dividends surpassed the companies’ combined net income for the first time outside of a recessionary period, and continued to climb for the 613 companies that have already reported for fiscal 2015.

In the most recent reporting year, share purchases reached a record $520 billion. Throw in the most recent year’s $365 billion in dividends, and the total amount returned to shareholders reaches $885 billion, more than the companies’ combined net income of $847 billion.

Spending on buybacks and dividends has surged relative to investment in the business. Among the 1,900 companies that have repurchased their shares since 2010, buybacks and dividends amounted to 113 percent of their capital spending, compared with 60 percent in 2000 and 38 percent in 1990.

Among approximately 1,000 firms that buy back shares and report R&D spending, the proportion of net income spent on innovation has averaged less than 50 percent since 2009, increasing to 56 percent only in the most recent year as net income fell. It had been over 60 percent during the 1990s.

FANTAsy – FAN + Tesla + Alphabet

At the end just before the markets began collapsing at year beginning 2016, we had the FANTAsy stocks. This included the core FAN plus Tesla and Alphabet (Google).

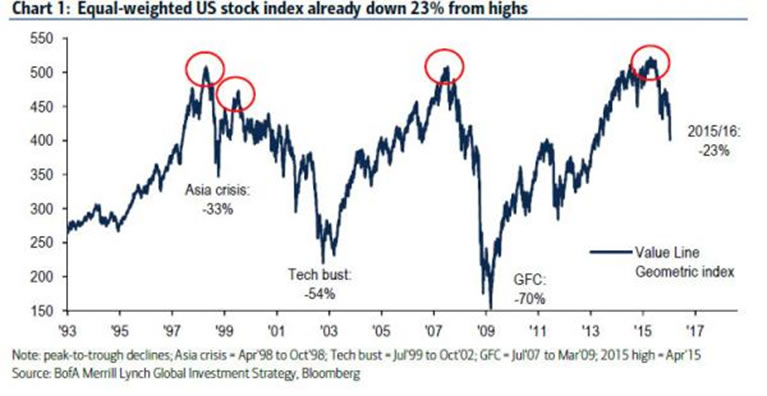

By considering an Equal-Weighted Stock Index which removes the FANTAsy distortions from the market many technicians were able to identify clearly what was occurring.

“FAN” HAS BROKEN DOWN – Possible Near Term Support and Then Another Drop??

CONCLUSIONS

A technical view of the equal-weighted US stock index may help resolve the support question.

It appears to suggest the market has further to fall in Q1 2016!

Caution is advised, as it has been since we first identified the FANGs in the market,

which could really bite the unsuspecting!

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/01/2016 - Leo Kolivakis: Are Negative Interest Rates The New Normal?

“Japan’s big bang smacks of desperation and this is where things get tricky and potentially dangerous. Why? Because we saw what happened last year following China’s Big Bang, .. and the risks of a full-blown emerging markets crisis are rising and this will have ripple effects throughout the world .. The greenback’s strength will only reinforce commodity and asset deflation, lower import prices and inflation expectations, and in my opinion, it will force the Fed to reverse course fast .. Be very careful here. The big bet is that as central banks pump more liquidity into the system using all sorts of unconventional monetary policy tools, those funds playing the global recovery theme will come out ahead, but for me this is nothing more than another short-covering countertrend rally that will fizzle as global deflation becomes more entrenched. That’s what the bond market is telling us .. And if global deflation becomes more entrenched, you can bet the Bank of Canada will regret its recent decision to stay put and that negative interest rates are coming to Canada too .. Right now, central banks are the only game in town and they’re desperately trying to save the world from a deflationary slump that will likely last for decades. Unlike what some market gurus claim, the Martingale casinos aren’t about to go bust, but clearly central banks cannot fight the global deflation tsunami and the world desperately needs a new macroeconomic paradigm to fight secular stagnation .. But my fear is that the fiscal response to world’s economic woes is lacking, either because of politics or high debt levels constraining public finances, and this means central banks will go it alone and negative interest rates will be the new normal.”

– Leo Kolivakis, Economist & Senior Pension Fund Consultant, Author of Pension Pulse

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

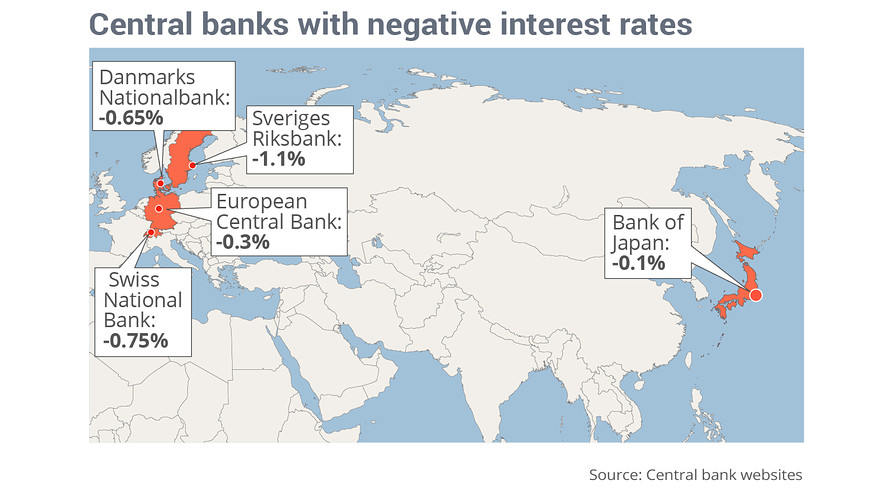

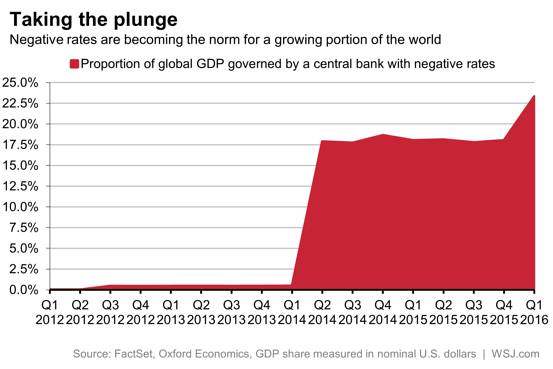

01/31/2016 - Negative Interest Rates Show Desperation By The Central Banks Of Heavily Indebted Countries

Commentary on Japan’s decision to join countries such as Denmark, Switzerland, Sweden & others on imposing negative interest rates .. more than a 1/5th of the world’s GDP is now covered by a central bank with negative interest rates .. the BBC writes: “The country is desperate to increase spending and investment.” .. commentary: “Japan has been desperate to boost consumer spending for years. At one point it even issued shopping vouchers to stimulate demand.” .. The New York Times writes: “Moving to negative rates reflects a measure of desperation on the part of central banks. Their traditional tools have been largely exhausted, as most countries’ interest rates have been pushed to almost nothing.” .. commentary: Negative rates will eventually come to America. Central bankers are implementing negative interest rates to force savers to buy assets … so as to artificially stimulate the economy.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

Dr. Lacy Hunt joins FRA Co-Founder Gordon T. Long in an in-depth discussion on the current debt dilemma and the decisions of the Federal Reserve. Dr. Lacy H. Hunt, an internationally known economist, is Executive Vice President of Hoisington Investment Management Company, a firm that manages over $5 billion for pension funds, endowments, insurance companies and others. He is the author of two books, and numerous articles in leading magazines, periodicals and scholarly journals. Included among the publishers of his articles are. Barron’s, The Wall Street Journal, The New York Times, The Christian Science Monitor, the Journal of Finance, the Financial Analysts Journal and the Journal of Portfolio Management.

Previously, he was Chief U.S. Economist for the HSBC Group, one of the world’s largest banks, Executive Vice President and Chief Economist at Fidelity Bank and Vice President for Monetary Economics at Chase Econometrics Associates, Inc. A native of Texas, Dr. Hunt has served as Senior Economist for the Federal Reserve Bank of Dallas. Dr. Hunt received his Ph.D. in Economics from the Fox School of Business and Management of Temple University. Furthermore Dr. Hunt served on the Board of Trustees of Temple University from 1987 to 2010 and is now an honorary life trustee. He received the Abramson Award from the National Association for Business Economics for “outstanding contributions in the field of business economics.” He is a life member of the American Finance Association. He was a member of the Economic Advisory Board of the American Bankers Association and Chairman of the Economic Advisory Board of the Pennsylvania Bankers Association. He served on the Monetary and Fiscal Policy Affairs Committee of the National Chamber of Commerce.

TACTICS OF THE FED

“Debt only works if it generates an income to repay principle and interest.”

Research indicates that when public and private debt rises above 250% of GDP it has very serious effects on economic growth. There is no bit of evidence that indicates an indebtedness problem can be solved by taking on further debt.

One of the objectives of QE was to boost the stock market, on theory that an improved stock market will increase wealth and ultimately consumer spending. The other mechanism was that somehow by buying Government securities the Fed was in a position to cause the stock market to rise. But when the Fed buys government securities the process ends there. They can buy government securities and cause the banks to surrender one type of government asset for another government asset. There was no mechanism to explain why QE should boost the stock market, yet we saw that it did. The Fed gave a signal to decision makers that they were going to protect financial assets, in other words they incentivized decision makers to view financial assets as more valuable than real assets. So effectively these decision makers transferred funds that would have gone into the real economy into the financial economy, as a result the rate of growth was considerably smaller than expected.

“In essence the way in which it worked was by signaling that real assets were inferior to financial assets. The Fed, by going into an untested program of QE effectively ended up making things worse off.”

THE FLATTENING YIELD CURVE

“Monetary policies currently are asymmetric. If the Fed tried to do another round of QE and/or negative interest rates, the evidence is overwhelming that will not make things better. However if the Fed wishes to constrain economic activity, to tighten monetary conditions as they did in December; those mechanisms are still in place.”

They are more effective because the domestic and global economy is more heavily indebted than normal. The fact we are carrying abnormally high debt levels is the reason why small increases in interest rate channels through the economy more quickly.

If the Fed wishes to tighten which they did in December then sticking to the old traditional and tested methods is best. They contracted the monetary base which ultimately puts downward pressure on money and credit growth. As the Fed was telegraphing that they were going to raise the federal funds rate it had the effect of raising the intermediate yield but not the long term yields which caused the yield curve to flatten. It is a signal from the market place that the market believes the outlook is lower growth and lower inflation. When the Fed tightens it has a quick impact and when the Fed eases it has a negative impact.

The critical factor for the long bond is the inflationary environment. Last year was a disappointing year for the economy, moreover the economy ended on a very low note. There are outward manifestations of the weakening in economy activity. One impartial measure is what happened to commodity prices, which are of course influenced by supply and demand factors. But when there are broad declines in all the major indices it is an indication of a lack of demand. The Fed tightened monetary conditions into a weakening domestic global economy, in other words they hit it when it was already receding, which tends to further weaken the almost non-existent inflationary forces and for an investor increases the value.

FAILURE OF QUANTITATIVE EASING

“If you do not have pricing power, it is an indication of rough times which is exactly what we have.”

The fact that the Fed made an ill-conceived move in December should not be surprising to economists. A detailed study was done of the Fed’s 4 yearly forecasts which they have been making since 2007. They have missed every single year.

The Fed begins the year with the high forecast and ts declines each forecast after that and by December it isn’t much of a forecast because you already have 11 months of data. An empirical indication that QE has failed is the fact that their models have relied on them to be indications and the models were wrong which means the policies have also been a failure.

CRIPPLING NEGATIVES

“Another risk which may very well lead to a worse result is the Fed going to negative interest rates. First we must consider if the Fed can engineer negative interest rates and it is very likely they do have that capability. There will be severe consequences which we will not even be able to anticipate.”

There is a trend that in weak economic times the fed will continue untested experiments. Even though QE 1, 2 and 3 have failed, in dire times they will implement QE 4. But if the Fed resorted to negative interest rates it will have an adverse impact on bank earnings, particularly small banks and greatly harm savers who have already been hurt. Negative interest rates will simply penalize people to a far greater degree. It will have devastating consequences to the money market mutual funds; difficult to see how they would operate at all.

Pushing interest rates in a negative territory will greatly increase the unfunded liabilities of the corporate pension plans. Pension plans will either be dropped or for those already covered it will explode the liabilities causing them to cut expenditures in the real economy to fund the pension liabilities.

“If the Fed went into negative interest rates they would ultimately be required to call in the currency and force people to use their bank deposits.”

We are no closer to solving our indebtedness problem in 2016 as we were in 2009.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/29/2016 - Financial Repression In Japan – Negative Interest Rates – Currency Wars To Intensify

8 Days Ago – the Bank of Japan governor Haruhiko Kuroda, said No Plan to Adopt Negative Rates Now

Today: the Bank of Japan adopts Negative Interest Rates!

“The BoJ actions should lead to further intensification of global currency wars with central banks around the world trying to engineer sustained competitive devaluation against the background of slowing global trade and growth as well as persistent commodity price disinflation. With its latest measures the BoJ will allow Japan to borrow more growth from its trading partners and limit the severity of the imported disinflation .. Almost 60% of the households’ financial assets are held in deposits. If indeed, the Japanese banks pass on some of the costs from the BoJ’s penalty rate to their depositors, this will result in a negative wealth effect, reducing the purchasing power of the Japanese consumers. Domestic demand should suffer and Japan’s contribution to global growth could decrease further. The BoJ’s measures thus should result in more currency wars and continuing slowdown in global trade and growth.” – Credit Agricole’s Valentin Marinov

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/28/2016 - Dr. Joseph Salerno: The War On Cash In Norway

Mises Institute’s Dr. Joseph Salerno highlights the developments in Norway in the war on cash .. Norway’s largest bank, DNB, has joined the campaign by governments & big banks the world over to abolish cash .. the first step the bank suggests is to get rid of the 1000 kroner note – “The aim of progressively withdrawing larger denomination notes from circulation is, of course, to make cash payments less convenient and to habituate the public to paying for even small transactions electronically.” .. Salerno asks what is the real reason for this war on cash – he quotes Zero Hedge: “The answer appears to be that the banks and government authorities are anticipating bail-ins, steeply negative interest rates and hefty fees on cash, and they want to close any opening regular depositors might have to escape .. The escape mechanism from bail-ins and fees on cash deposits is physical cash, and hence the sudden flurry of calls to eliminate cash as a relic of a bygone age — that is, an age when commoners had some way to safeguard their money from bail-ins and bankers’ control.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/27/2016 - Yra Harris: Japan Seeks Chinese Capital Controls

“The most important news item of yesterday was buried on page 6 of theFinancial Times: BOJ KURODA SEEKS CHINESE CAPITAL CONTROLS. This is significant for a Governor of a major central bank to openly suggest the imposition of ‘stringent capital controls to help stem massive outflows of hot money from China and stabilize hot money’ .. Governor Kuroda seems concerned that if the Chinese YUAN continues to weaken it will cause problems for the Eastern Asian economies and put pressure on other central banks to pursue policies of currency weakness. Japan would have to embark on more QE to deal with Asian depreciation and it appears that Kuroda-san is reticent about buying more JGBs. It seems Kuroda wants the Abe administration to continue its structural reforms, which have fallen far short of its stated goal. It seems many central bankers have tired of more QE as it appears that the vast monetary purchases have had limited success.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/27/2016 - Investing Techniques In Financial Repression: Profiting When Stock Markets Fall

With increasing signs of a global recession, stock markets throughout the world have experienced one of the worst annual starts in history.

Many investors fear 2016 will bring another stock market downturn similar to 2000 and 2008. While investors can protect themselves by selling equities or even shorting the stock market, both of these approaches involve potential problems. An options strategy offers a third alternative with the potential for sizeable profits.

WindRock interviews Ed Walczak, Senior Portfolio Manager of the Catalyst Hedged Futures Fund, about the use of an S&P 500 options strategy.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/26/2016 - PwC: Financial Repression Of Savers and Retirees In The New Normal

With bond yields going lower, PwC’s Andrew Sentance discusses financial repression & its unintended consequences to savers & retirees .. 4 minutes

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/24/2016 - Your Gold Is Only As Good As Where You Store It

International Man’s Jeff Thomas advises the following principle: “Keep your bullion in a place where you maximize your control over your ownership of it, whilst minimizing the control others (such as banks and governments) have over it.” .. mentions the coming cash controls by indebted governments – these developments may affect where you store your gold, it’s financial repression .. identifies many investors are moving into real estate & precious metals for protection .. points to what Sprott is doing – offering services to store precious metals in “safer jurisdictions” like Switzerland, Singapore & the Cayman Islands.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/24/2016 - Norway Joins In On The Worldwide War On Cash

Norway now appears to be joining in on the worldwide war on cash .. with estimates of only 6% of Norwegians using cash on a daily basis & with many of those being elderly people, Norway’s Ministry of Finance is opposed for now to the proposal .. nonetheless in the meantime, the big 2 banks in Norway have already stopped using cash in their branch offices. And the movement toward a goal of no cash has been going on for a while. The Norwegian Hospitality Association pushed to eliminate consumers’ right to pay cash at all stores & restaurants in 2013 .. many have emphasizes the trend is a big move away from privacy, with the government (state) now increasingly knowing what, how, when & perhaps even why you spend your money on .. Zero Hedge: “If allowed to continue, state wealth control will exist. And thus, as we concluded previously, if you can’t withdraw your money as cash, you have two choices: You can deal with negative interest rates…or you can spend your money. Ultimately, that’s what our Keynesian central planners want. They are using negative interest rates and the War on Cash to force you to spend and ‘stimulate’ the economy. If you ask us, these radical and insane measures are a sign of desperation. The War on Cash and negative interest rates are huge threats to your financial security. Central planners are playing with fire and inviting a currency catastrophe.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/22/2016 - YRA HARRIS: “There is No Wizard Behind the Curtain!”

FRA Co-Founder Gordon T. Long discusses with Global Macro CME Floor Trader Yra Harris, the difficulties of investing in the currently suppressed global market. Yra has been a member of the CME since 1977 and is a well-known global macro trader. Yra currently works with Vine Street trading.

YIELD CURVE

Yra distinguishes the 5/30 UST as much more of speculators curve, and the 2/10 UST, an investors curve, meaning people with a longer term horizon.

Regarding the flattening of the yield curve line: Yra references Paul Samuelson saying the stock marketing having predicted the past 9 of the 5 recessions, however the same cannot be said for the yield curve.

“When the yield curve starts to flatten, to ultimately invert, trouble looms”.

Yra believes that central banks eventually error one way or another, and ultimately cause the curve to flatten.

2016 PREDICTIONS

The market anticipates slowing growth, if not negative growth resulting in recession. The last time this was seen was 2006-2007. When the Fed was raising rates, driving the rate to 5.5% on the federal fund rate, the yield curve was flattening, and within 6-9 months later, the curve had inverted.

Yra combats the notion that the yield curve is a bad indicator by saying, “It is only a bad indicator because I cannot time for you, what the market’s reaction to it will be”

Yra mentions Stanley fisher saying that going to negative yields in the United states would be very difficult because of their money market funds.

“If the Federal Reserve of the United states went to negative yields it would be a catastrophic statement that they had panicked, indicating they have nothing left.”

Yra brings up Stanley Fisher saying the four rate increases are a probability.

“I’m going to watch what the metals market is doing. If the gold rallies while the curve flattens, it will be telling me that the market is getting fearful…meaning the central banks are losing control”

“The optimal control function is a myth. Economic analysis is not rocket science. Good science is the ability to continuously replicate an experiment and get the same results, this is not the case.”

Yra believes that central banks are not concerned about inflation, because banks have learned they can slay inflation, by raising rates high enough to stop it, which will and has caused the yield curve to invert in the past. Systems built on borrowing, such as China, would rather endure periods of inflation than deflation, deflation is 30% unemployment, everything stops. “run inflation hotter, because that’s the greatest thing to remove the overhang of debt”

“If you can’t restructure, and if you can’t write it off, because you’re worried about the banks, you have to create some inflation, and their fear is that they’ve been unable to.”

GEO POLITICAL TENSION — OIL & CHINESE MARKETS

Demand is contracting because the world economies are slowing down. The Saudis have built their structure based on that they felt comfortable that the United States and the six fleet would always be there to support them.

“Saudis are sending a message that they’re upset with the United states about a shift of policy, as they see it. We are at a critical junction, and I think oil is all part of it. All of a sudden the Saudis are going to do an IPO of Aramco, which will bring significant implications, they’ve never gone that route, why now?”

There is word that they’re short of capital, however it’s cheaper to raise capital in an equity capital than a bond market. Saudi reserves are not the collateral for those bonds. This is all tied into the price of crude oil.

“China is a great story, from an academic sense, but from a market sense I don’t trust anything that I read out of China”

Yra’s tongue and cheek example is Google not being allowed to be used freely, restricting the free flow of information.

“It’s amazing to me that this country, that does not allow free flow of information and data, can meet market projections at so many of their data releases. I don’t trust the (Chinese) data enough to trade.”

One thing that has always scared the Chinese authorities is losing control of the employment situation. Michael Pettis has talked about how the Chinese leadership has financially repressed the middle class, because they’ve kept the Yuan too cheap in order to build a vast pool of reserves. When a country wants to buy imports, they have to pay a greater price but the goal was to drive the export engine. When trying to make the shift from export oriented to a more domestic oriented economy, then a stronger Yuan is more desirable, which would make for cheaper imports. Yra states,

“If you’re really trying to empower your citizenry, let the currency go higher.”

“China is still a totalitarian government, and they can inspire fear, which is what a totalitarian regime operates on”

THE FOCUS FOR INVESTORS

“We don’t have the play out of fundamentals that we used to. They will eventually play out because fundamentals will ultimately drive the market, they have to.”

Yra says that the equity markets are so linked and tell a global story, but believes that linkage is a false correlation.

“Monetary policy and financial acumen is still not rocket science” – It brings with it much uncertainty.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/22/2016 - Financial Repression In Canada

Article emphasizes how Canada’s deepening recession is likely to prompt the Bank of Canada (BoC) to go down into negative interest rates like parts of Europe are already .. the BOC has already hinted that Europe’s not-so-grand experiment in the Keynesian Twilight Zone known as NIRP (negative interest rate policy) may be about to cross the pond – “The effective lower bound for policy rates is around -0.5%,” central bank governor Stephen Poloz said in December, setting the stage for negative rates in Canada .. IceCap Asset Management sees the following scenario:

1. Canadian economy to be in recession in 2016

2. Bank of Canada will be at 0% interest rates in 2016

3. Bank of Canada will be at NEGATIVE interest rates in later 2016

4. Bank of Canada will be PRINTING MONEY in later 2016

Barclays says: “The BoC would need to cut at least 50bp this year to partially counteract the continued slide in crude oil prices .. the BoC would need to cut policy rates by at least 50bp in 2016.” .. The BoC itself estimates that the effective lower bound for Canada could be around -50bp, giving room for further cuts if needed.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/22/2016 - China Accelerates The War On Cash

The central bank of China is targeting an early rollout of China’s own digital currency to boost its control of money in the country .. this is another development in the worldwide war on cash – how governments are limiting the use of cash or abolishing it outright .. it’s all about capital controls & financial repression .. governments are now anticipating bank bailins & negative interest rates, & by limiting or abolishing cash, this will minimize or prevent the possibility of bank depositors from withdrawing their cash from their bank ahead of or during a bank bailin .. People’s Bank of China statement: “To enhance the central bank’s money supply and currency in circulation control.” .. Zero Hedge commentary: “There are three enormous flaws with the war on cash: “One is that households and businesses have cash to hoard. The reality is the bottom 90% of households have less income now than they did fifteen years ago, which means their spending has declined not from hoarding but from declining income .. The second flaw is that hoarding cash is the only rational, prudent response in an era of financial repression and economic insecurity. What central banks are demanding — that we spend every penny of our earnings rather than save some for investments we control or emergencies — is counter to our best interests. This leads to the third flaw: capital — which begins its life as savings — is the foundation of capitalism. If you attack savings as a scourge, you are attacking capitalism and upward mobility, for only those who save capital can invest it to build wealth. By attacking cash, the central banks and governments are attacking capital and upward mobility .. When the dust has settled who ultimately benefits by this war on cash – government and the central banks, pure and simple.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/20/2016 - Eric Sprott: “Think About How to Mitigate Your Losses!”

FRA Co-Founder Gordon T. Long deliberates with Eric Sprott about the outlook for the global economy in 2016. Eric Sprott is a Canadian hedge fund manager and founder of Sprott Asset Management. He became a billionaire on paper with the initial public offering of Sprott Inc, the parent of his Sprott Asset Management firm. In August 2011, Sprott was acknowledged by Bloomberg as a ‘hidden billionaire.’ The publication estimated Sprott’s worth at $1.3 billion, largely based on his publicly disclosed holdings in Sprott Inc. and Sprott Physical Gold Trust. Sprott started his career as an analyst at Merrill Lynch covering everything but commodities. He eventually became known as a natural-resources and energy investor.

In 1981, Eric Sprott founded Sprott Securities Ltd. (now Cormark Securities Inc.), an institutional brokerage firm focused on small-to-mid capitalization companies, servicing Canadian corporate and institutional investors. In the year 2000, Eric Sprott made the decision to focus solely on the investment management business. Accordingly, the “investment management division” of Sprott Securities Inc which became one of Canada’s largest independently owned institutional brokerage firms. In 2000, Eric divested his entire ownership of SSI to its employees and chose to focus his sole attention on the investment management business and he formed Sprott Asset Management. In 2006, Eric was awarded the Ernst & Young Entrepreneur of the Year Award for Ontario.

In late 2009, Sprott published a well circulated white paper titled, “Is it all just a Ponzi scheme?” The document dug into who was actually purchasing recent Federal Reserve U.S. Treasury auctions and concluded that the biggest new buyer versus the previous year was the U.S. government.

Eric’s approach to philanthropy is straightforward. He wants to help society change for the better. He is also constantly studying how to best serve his community through the foundation’s philanthropic donations. He believes that “the world needs true leadership to deal with unrecognized problems.”

2016: WHAT LIES AHEAD

“There is nothing constructive to say about the financial ponzi we have gone through since QE and negative interest rates were initiated.”

By knocking interest rates down to zero and in some cases they’re negative, savers are getting crucified. They get no return on their money. They have to buy the slimiest of assets, US bonds receiving 2%.

QE, printing of money will not do anything for the economy. We saw this with japan for the last 30 years. QE was only in place to inflate assets prices and we are all going to pay the consequences for that. It’s shocking that the market has held up as long as it has, and even more shocking is that during this whole process policies are so irresponsible that precious metals are not getting enough attention. I feel like a lone wolf believing that people should be in precious metals to protect themselves against this recession.

THE FOCUS FOR INVESTORS

“The most important thing is that roughly 97% of stocks are in bear markets throughout the world.”

Originally only a few stocks in the US were holding things up, and now they’re all getting crushed. In 3 months it would be no surprise to see every stock in the world being in a bear market. Furthermore it’s unbelievable to think you have a stable economy when oil prices are under 30. There are so many areas of falling prices; hitting or nearing all-time record lows.

“I do not have much hope for the economy right now; the stock markets are reflective of that.”

The whole issue of medical care in the US is being swept under the carpet; there are significant expenses for too many people. We need to be very careful about equity and bond investments. If you begin with the premise that the US is broke, you have $85 trillion of unfunded liabilities and a GDP of 18 trillion that says enough right there; it’s a joke.

This is why I preach to own precious metals because they will survive a financial meltdown. Risk mitigation is critical, but you have to understand all the elements of risk. It is phenomenal the risk that you will be taking in turn for the yield you’re expecting.

PRECIOUS METALS

Not to put a number on it, but I believe for the last 15 years the demand for gold has been well above supply and central banks have superficially provided the extra supply. The physical gold market may overwhelm the paper market, if or when it does you can imagine a recession or depression or even a currency crisis which is happening throughout the world.

BLACK GOLD

For oil, when you ask questions about markets that are dominated by paper and the influence of central planners it is difficult to give an answer that makes much sense. Ultimately oil should be going back up; very few entities can produce at $30/barrel. Sooner or later we will see shutdowns, and once that happens it will be highly unlikely for a restart until prices are at a profitable amount.

CANADIAN DOLLAR

“Government revenues are going to plunge coupled with stocks falling; 2016 is not looking very bright.”

It is a very tough situation because of oil prices are so devastating for everyone but particularly devastating for US and Canada. People are going to take all sorts of losses and reclaiming former capital. It is a dark hole where weaknesses are being amplified unless there is an outside influence to turn things around.

CLOSING STATEMENTS

“Seeing all the previous crisis happening from the Dot.com to the 2008 crisis you can see what is likely to happen here; it has just been postponed. But I suspect it will be worse, it will be global and it will not be as easy to fix as it was in 2008 because now it will have to be coordinated.”

It is a question of whether people believe or don’t believe in the market. Everyone realizes after what has happened is that there is a vulnerability in the market that people didn’t expect. Hopefully we will see signs of precious metals going up that will indicate the importance of focusing on the real issue in the financial system is today.

“All indicators are telling you that there is no recovery happening here anytime soon. It may just keep going down and potentially get violent. In the midst of all this the key thing is to focus on mitigating your losses.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/20/2016 - Charles Hugh Smith: The Unintended Consequences Of Financial Repression On Retirees

“On the devastating long-term impact of the Federal Reserve’s zero-interest rate policy (ZIRP): with the real (i.e. adjusted for inflation) return on savings near zero (or even negative, for those who have to pay soaring rents, healthcare insurance premiums, college tuition, etc.), those saving for retirement are losing the Red Queen’s Race: no matter how much they save, the income will be too paltry to support retirement. This has three extremely negative consequences. Those seeking a return above zero are forced to put their savings at risk in boom-and-bust markets that tend to reward only those who get into the bubble expansion early and exit early. These boom-and-bust markets tend to savage the assets of the middle class when they blow up, but do little to rebuild these assets in the bubble expansion phase, as prudent investors who were burned in the previous bubble bust shun risk assets. The second negative consequence is the structural pressure on spending as those saving for retirement must sacrifice current spending to pile up capital to spend during retirement. No wonder the velocity of money is in free-fall–everyone hoping to retire on more than cat food has to set aside more of their earnings because they cannot count on any future earnings on capital. The third consequence is the destruction of middle class retirement. When a $500,000 nestegg earns a miserable $15,000 a year (3% annual yield), saving enough to generate a middle class income in retirement is beyond the reach of what’s left of the middle class.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

“Retiring overseas is becoming increasingly common: Some 373,224 retired workers received Social Security checks overseas in 2013, the latest data available, up from 306,906 in 2008 and 246,890 in 2003.”

LOCK IN YOUR LIVING ACCOMMODATIONS NOW

“Today, soon-to-be retirees have more reason than ever to think that dream can become reality, thanks to the strong dollar. As of January 15, $100 would buy 92 euros, up from 83 euros at the beginning of 2015. That same dollar amount would now buy roughly 1,827 Mexican pesos, compared to 1,474 on Jan. 1, 2015. The Colombian peso is up roughly 33 percent from a year earlier.

All of that means buying a home or any other assets overseas is easier than it has been in some time, said Kathleen Peddicord, publisher of “Live and Invest Overseas.”

“If you have a fixed income in U.S. dollars, right now the U.S. dollar is super strong,” she said. “What I recommend as a strategy is, find a place you want to live where the dollar is very strong right now, and buy your residence. Once you do that, buying at today’s strong dollar value, you can buy at a good price and you have taken the cost of housing off the table.”

BARRIERS COMING DOWN

Previously issues like health coverage may have been an issue but today “In some countries the care is extremely inexpensive and high quality. In others, you may want to obtain global health insurance from a company like Bupa or Cigna.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/04/2016 - Collection Of Articles On Negative Interest Rates

02/04/2016 - Collection Of Articles On Negative Interest Rates