Blog

06/25/2017 - Former Fed Advisor Danielle DiMartino Booth On Why The Fed Is Bad For America

06/25/2017 - Former Fed Advisor Danielle DiMartino Booth On Why The Fed Is Bad For America

06/25/2017 - Danielle Park: Central Banks Are Architects Of Global Stagnation And Insolvency

“For the past 20 years, the world has careened from one greater and greater insolvency shock to another. Each time, central banks have been summoned to the ‘rescue’ deploying increasingly more aggressive monetary magic. But after 9 years at near zero rates and trillions in asset buying to extend and pretend the appearance of economic prosperity, reality is dawning once more as the global economy slows and liquidity retreats to reveal even larger debt and sustainability problems.”

Central banks are architects of global stagnation and insolvency

06/25/2017 - Dr. Marc Faber: Massive Wealth Taxation Or Asset Deflation Is Coming

06/25/2017 - The Roundtable Insight: Charles Hugh Smith On Central Bank Buying Of Equities

FRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Charles Hugh Smith, America’s philosopher. He’s a leading global finance blogger and author. He’s the author of nine books on our economy and society including A Radically Beneficial World: Automation, Technology and Creating Jobs for All. Resistance, Revolution, Liberation: A Model for Positive Change, and The Nearly Free University and the Emerging Economy. His blog, http://www.oftwominds.com has logged over 55 million page views and is #7 on CNBC’s top alternative finance sites. Welcome, Charles.

Charles Hugh Smith: Thank you, Richard. That makes me seem larger than I actually am in real life.

FRA: You’ve got a great blog, I mean I read it avidly. A wide range of topics from a very philosophical perspective

Charles Hugh Smith: Well thank you. Yeah, we’re living in extremely interesting times and it’s a struggle to contextualize all the information and news that we read you know? Like how does this fit together? And that’s one of the topics that we’re going to discuss today, how does this all fit into our era and the global economy?

FRA: Yeah so I thought today we might take a look at Central Bank buying of private assets, in particular equities. But there’s also buying of corporate bonds as well. What exactly is the extent of that and potential implications to the economy, to our overall economic system, moral hazard issues in terms of what that means philosophically?

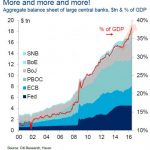

Charles Hugh Smith: Right, right. I think we all know that Central Banks have been buying just immense sums for like over 8 years now of sovereign bonds, corporate bonds, and more recently corporate equities either directly in specific companies like the Swiss Central Banks been buying Apple and Amazon I know. And then the Bank of Japan has been making huge purchases of ETFs, you know exchange traded funds which are basically index funds, pools of corporate equities. But nonetheless, enormous purchases of private sector equities which is unprecedented in a non-crisis situation.

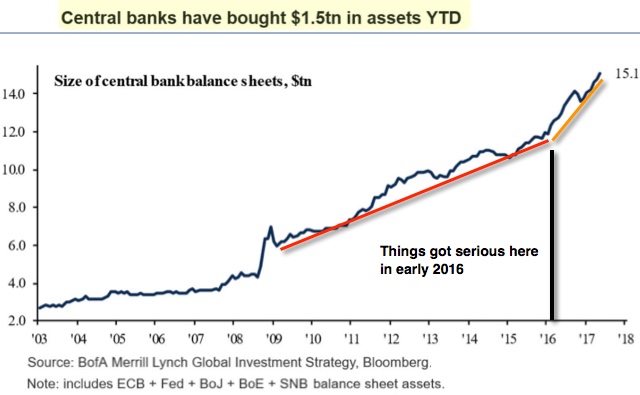

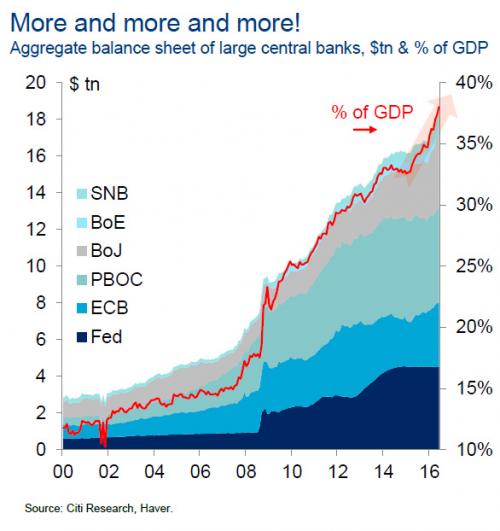

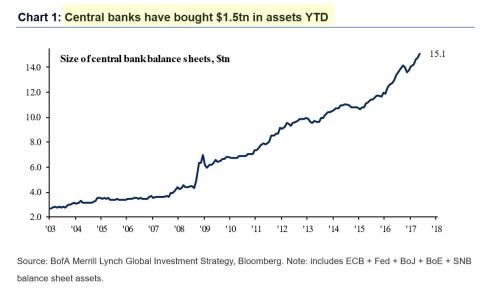

FRA: Yeah, they’re some statistics out there that indicate this year alone there’s been so far somewhere between one and two trillion of financial assets purchased by Central Banks, especially the European Central Bank and the Bank of Japan.

And a certain subset of that includes the buying of equities. And it’s not just those Central Banks, its Central Banks such as the Swiss National Bank as well. So those are major buyers of equities and the ECB is focused on corporate debts, so specific company bonds.

Charles Hugh Smith: Right, and let’s discuss that a bit. So to explain as I understand it, and I’m not an expert, but as I understand it when Central Banks go to buy corporate bonds, they can go to the marketplace. They might be buying bonds that were issued a year or two or three years before by the corporation right? It’s the open market for corporate bonds. Or recently it appears they’ve been buying directly from the issuer, from the corporation. And this is quite a bit different because they’re basically funding corporations by snapping up their bond issuance without even going to the marketplace where they’d have to compete with other buyers and sellers and the market would price the risk factor in that bond. And so they’re really overstepping the market by buying directly from corporations. Do I have that basically right?

FRA: Yeah, I mean there’s all kinds of risks that come from this. I mean you can think of the distortions to the market in terms of valuations, price discovery, risk, the price of risk if you will. And then overall the associated issue philosophically is does it make sense for governments to buy specific company assets? Are they not then picking and choosing particular companies over above other companies? You know favouring certain companies by buying their stocks, by buying their bonds and not others, versus others.

Charles Hugh Smith: Right, and I think before we started recording you used the phrase “picking winners” right? And of course, all the stocks their buying are winners as long as their buying.

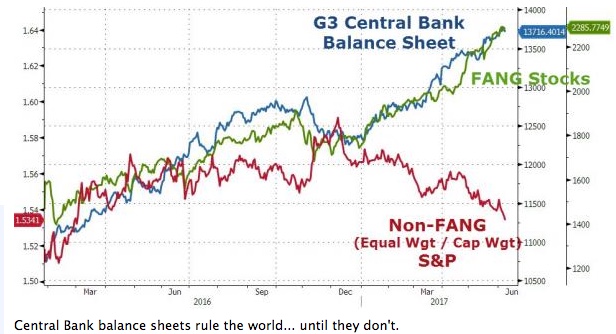

And I’m looking right now at a chart that showed the Central Bank balance sheet for the last say about 9 months and then the FANG stocks, you know the Facebook, Apple, Netflix, and Google. And they’re extremely correlated, extremely correlated.

So it suggests that Central Banks are buying these hot very large cap tech stocks and in a way, picking them as winners. Because if there’s steady buying by Central Banks in the hundreds of billions of dollars, then you basically created a floor under all these stocks that the Central Bank has picked as winners and that’s distorting the market. I recently wrote a piece that tried to describe a fairly subtle, at least to me, dynamic which is the markets are based on transparent information being available to all participants, right? And so when insiders say have an information asymmetry, like they know something the rest of us don’t, then of course that’s considered illegal because they can then benefit from that asymmetric knowledge. And so the market requires a free flow of information if it’s going to have the necessary foundation for price discover, risk assessment, pricing of risk and so on. So when Central Banks are setting a floor under the stocks they’ve picked as winners, they’ve actually deprived the market of essential information. And so my view is when you rob the market of information, then you’ve crippled all the participant’s ability to make a realistic assessment. And this may be part of the reason why we see stocks just lofting ever higher is there’s no information that would suggest risk might be rising beneath the surface because of all this Central Bank buying. So they’re basically stripping out the essential information from the market. And that’s making the market kind of beneath the surface much more fragile and much more unstable because the buying and selling is not an open market, it’s intentionally favouring a few large kept stocks. So we have to ask, what happens if Central Banks ever stop buying for whatever reason? What happens if the market starts falling? The Central Banks will sell, are they going to be bag holders or they’ll hold forever and buy more? I mean all these issues are unprecedented, right? Because in the past, Central Banks would famously buy the market in crisis. You know like when the market was crashing or going through a severe downturn they would institute the plunge protection team, right? Which would go in and buy enough equities or bonds to seize up the market and stop the crash and reverse that. And then all the computer programs would recognize the reversal and jump in and start buying. And so that kind of plunge protection team buying is one thing, but here we are eight and a half years into a supposed recovery, and they’re still buying a trillion and a half dollars in five months? I mean that’s unprecedented.

FRA: Yeah, and in terms of being able to get out, that’s a good question but maybe they cannot get out or they don’t want to get out. I mean you got issues of the baby boomers retiring, they may be looking to sell their stocks. So who is going to be the buyer in that case if there’s a large selling by the baby boomers? Pension funds as well, if there were to be a large selloff in the markets that would negatively severely affect the pension funds insurance companies. And the governments don’t want to have to bail those guys out like they had to bailout the banks back in the first financial crisis. Your thoughts?

Charles Hugh Smith: Right, well Richard we recently spoke about the millennial generation and some of the issues connected with it. And you’re absolutely right, as sort of a generalization, it’s fairly clear that the millennials income is lagging from previous generations and they have much higher student loan debt. So they’re not going to be able to fund their IRAs and 401Ks to the same degree as previous generations because even if they’re frugal they’re having to devote a lot of their income to pay down their student debt. And so that suggests there’s not going to be any secular movement generationally to buy equities because millennials simply don’t have enough money to buy a lot of equities to counterbalance the tremendous selling that will be going on over the next ten years as baby boomers retire and start drawing on pension funds which as you say have been invested in equities and will now have to be unloading them in order to fund their retirees. So if the Central Banks are going to replace an entire generation and all the pension funds globally, then they’re going to be owning a significant percentage of the entire bond stock market. And I’ve read numbers and I don’t know if they’re accurate or not, but apparently the bank of Japan owns roughly 30% of the entire Japanese equity market already. I mean that’s a significant percentage. And so what happens when that goes up to 50% or higher? And as you said before we started recording you used the term “financial alchemy” and there is an element, isn’t there, of what I call perpetual motion machine. The Central Banks just create money out of nothing, then they buy equities and bonds, and they can continue to do that with apparently no friction. There’s no risk and no friction, but is that really true?

FRA: Yeah, that’s a good question. I mean from the perspective of the Central Banks, if we look at the Swiss National Bank SNB, their driving factor of doing this, buying equity’s is a tool in the Central Bank policy tool chest in terms of trying to maintain their currency. So there’s a tendency for the Swiss Franc to get stronger. So by buying in particular U.S. equities you’re essentially buying the U.S. dollar thereby decreasing the strength or the value of the Swiss Franc. So what is essentially happening is a sort of financial alchemy. Whereby the Swiss National Bank is printing money out of thin air and then using that to buy real assets, stakes in real companies. I mean this can go on ad infinitum until they own all companies that are publicly listed.

Charles Hugh Smith: Right, right and then that’s an interesting point you raised about the sessity of Central Banks to maintain their currencies or in many cases attempt to devalue their currencies to keep their exports up. And so that’s certainly a driver for purchases of U.S. dollar based bonds and stocks. And of course, that also offers the benefit to other Central Banks of great liquidity, right? Like you can buy quite a bit of U.S. treasuries and unload them without pushing the market around much.

And the same is true of huge large kept stocks like Apple or Google and so on. So it’s interesting how stocks, equities, and bonds have become tools of currency manipulation. But the currency market is so much larger than bonds and equities, and of course, bonds are larger than equities. And so we see this sort of pyramid where when you’re going to play around with currencies you’re dealing with several trillion dollars moving around every day and then you move up to the bonds and it’s smaller and the equities are considerably smaller. I think that again it’s raising the risk in the equities market because the amount of capital that could be moving into stocks and bonds from Central Banks is unprecedented in size. And so we have to ask, what is the consequence of that in a crisis situation? Will Central Banks then have to buy another $5 trillion worth to stem the market crash? Or how are they going to respond? If they start selling then that alone can trigger a serious decline because they have now become buyers of size.

FRA: Yeah, we have several charts that we’ll put up on our write-up showing a very strong correlation between the level of Central Bank buying and the associated markets, it’s quite correlated.

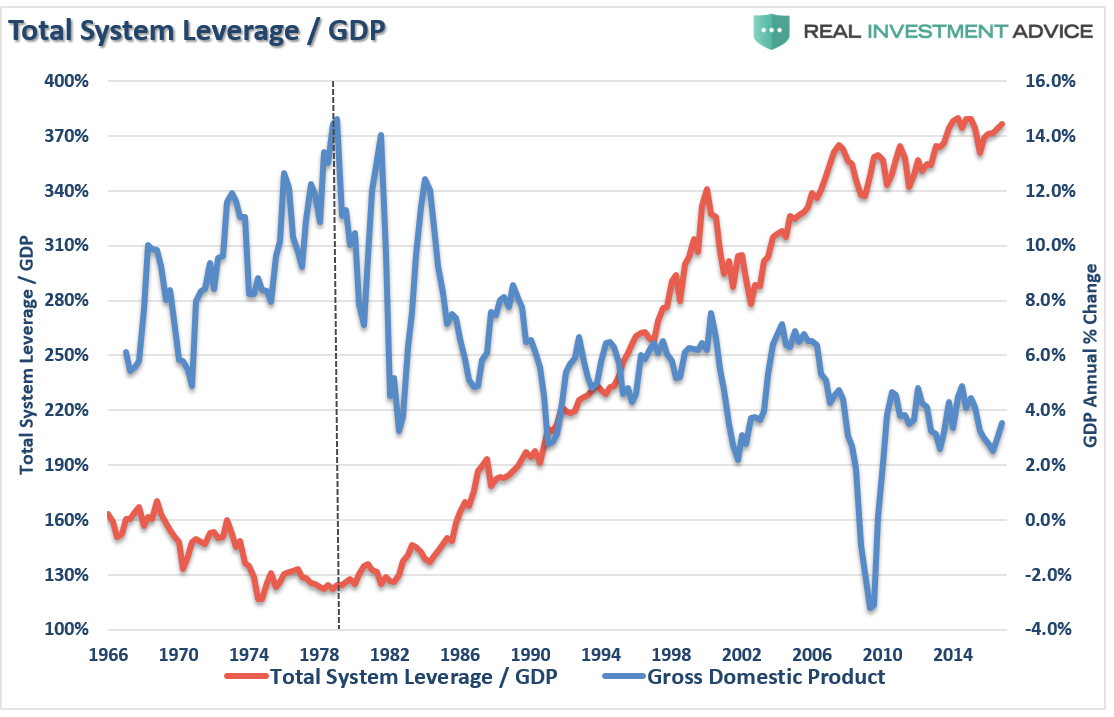

Charles Hugh Smith: Right, and if we look there’s a chart that I submitted, it’s called total system leverage, it’s from Real Investment Advice. Total system leverage which is really a proxy for liquidity provided by Central Banks and then GDP.

And we see that Central Banks have generated a tremendous increase in total financial system leverage, you know credit and liquidity. And yet GDP has been in a secular downtrend since the 80s. And so we’re also in a situation where the Central Banks are taking these unprecedented actions of interventions and manipulations in the market and yet actual growth is still declining. So we’re seemed to be getting less actual growth for the buck, right? For the Central Banks, there’s a definite element of diminishing returns in their purchases of private equities and bonds.

FRA: And there’s also another interesting study that was put into the Wall Street Journal EBSCO, they have some interesting results whereby what they did as a pole and they came up with a figure of 80% of Central Banks plan to buy more stocks. So this came out earlier at the beginning of the year. And then they did some survey on asking what areas equities, corporate bonds, government bonds, deposits with Central Banks and so on in terms of asset classes. They looked at the net percentage points of Central Banks saying whether they will increase or decrease future allocations in each asset class. And equities came right up at the top, plus 80. Corporate bonds number two at plus 43. So those are the two asset classes where there’s a focus by the Central Banks. And then after those two asset classes are government bonds, so that’s quite interesting. On the decrease side are deposits with Central Banks and deposits with commercial banks, so that’s quite interesting results.

Charles Hugh Smith: Yeah Richard that is extremely interesting. And it obviously speaks to the current uptrend shall we say in global stocks. And so clearly if Central Banks have prioritized buying equities, that’s very likely a driver of the current reflation as it’s called. And so what do we do in that kind of situation? Well, the easy thing to do it just go long equities and ride the thing higher, right? But how long can that go? And that of course is an open question.

FRA: Yeah that’s the big question, where is this all leading to? Does it end? Or due to the need to implement their monetary policies will Central Banks even perhaps accelerate their buying of equities? Not so much for trying to get ownership of companies but just as a tool in their policy chest of implementing policies. So if there’s sort of more currency devaluation, competitive currency devaluations in the world going on and the need for quantitative easing for monetizing debt. I mean this whole process can accelerate I think.

Charles Hugh Smith: In my view what the Central Banks are doing is creating a widening divide between the actual real economy of sales, profits, and productivity that once drove equity valuations. And so now the more it’s based on Central Bank buying then there’s a gulf that’s widening between the real economy and the stock market. And Central Banks view the stock market as a singling device, that’s part of the reason for this purchasing as you say, it’s to support equity valuations held by pensions but it’s also to signal to everyone that the economy is healthy because the stock market keeps going up. And so as the real economy stagnates and falters and the stock market keeps rising, then the stock market starts losing its signaling capacity because people will eventually catch on that the stock markets rising from Central Bank purchases but the real economy is stagnating or in decline. And so there’s a certain element of trust in this whole idea that a market is an open transparent market. And if you lose that trust and people think that it’s just being manipulated as a signaling device, then the Central Banks may lose that whole belief of the general public that the stock market actually does reflect the real economy. And so once that trust or faith has been lost, then the stock market is no longer a reliable signaling device and the Central Banks will kind of have been revealed as the power behind the curtain.

FRA: Yeah, exactly. Okay, that’s great insight Charles thank you very much. How can our listeners learn more about your work?

Charles Hugh Smith: Please visit me at http://www.oftwominds.com and you can read free chapters of my books and take a look at my archives and see what I’m coming up with in terms of solutions.

FRA: Excellent, excellent great insight and we’ll be having another discussion in about a month.

Charles Hugh Smith: Yes, look forward to it Richard, thank you very much.

Transcript written by Jake Dougherty <jdougherty@ryerson.ca>

06/22/2017 - The Roundtable Insight: Uli Kortsch On The Monetary Trust Initiative – Why/How It Could Address The Underlying Problems With The Financial System

FRA is joined by Uli Kortsch in a discussion of the Monetary Trust Initiative and the underlying problems with the monetary system that lead to its creation.

Uli Kortsch is the Founder of both the Monetary Trust Initiative (MTI) and Global Partners Investments (GPI). Currently most of his time is spent on MTI whose mission is to bring transparency and authentic principles to our monetary system. As President of Global Partners Investments and other ventures, he has worked in over 50 countries, written a bill for Congress, and conferred with approximately 15 national presidents, ministers of finance, and ministers of commerce. He has served on numerous corporate boards with both for-profit and not-for-profit organizations.

HOW MONEY IS CREATED

Almost everyone thinks it’s the Fed that creates money, but it’s not. It’s the commercial, normal banks around the corner from which you borrow money. Almost everyone thinks that money came from a prior saver; it didn’t.

Let’s say you want to buy a Ford for $30,000. You walk in and the banker lends you the money. When you sign the contract that’s an asset to the bank, and let’s assume we now do an intermediation process. The bank takes that $30,000 from a prior saver and moves it into your account. This doesn’t happen, but it’s what most people think. Where did that $30,000 come from? It came from a man who saved the money. But who is that man? It happened to be a man that’s working for Ford and Ford paid the money to the employee, who saved the $30,000 which you now have. What do you do? You give your dealer the $30,000 so you can get the car, and the dealer gives that money to Ford, which gives it to the worker, which gives it to the bank, which gives it to you and—It’s one big circle. The money hasn’t come from anywhere. People don’t think about this. We’re not intermediating money from the previous saver, because the previous saver didn’t exist. Where did they get the money from? The same place you did: the bank.

Then most people think the money came from the Fed, who printed approximately $3T of money over a period of a year and a half, and we run a fractional reserve banking system. Well, no. Those are reserves, and reserves never hit the street. None of us have ever gotten a penny of that. So where does the money come from? Let’s go back to the Ford.

You sign your contract for $30,000 and the bank, out of nothing, creates that $30,000 deposit. That is true in the aggregate and the overall system how it works. In the bank’s bookkeeping, it looks different, but that’s in effect what happens. Let’s reverse the whole process and say the bank charges you 10% interest. You have a really good year and haven’t made any payment. At the end of the year, you pay your whole loan off: you owe the $30,000 loan plus $3,000 in interest. That’s a total of $33,000. What happens with that money? The $3,000 is income to the bank from the money it created out of nothing, the $30,000 that you have now payed off ends up as nothing. The bank, in its bookkeeping, in its aggregate, destroys the $30,000.

We’ve got several things here that are now obvious: 100% of our money is created by debt. It’s what we call bank money verses cash. Almost everything is based on bank money; there’s very little cash out there. There are a few implications to this. We must have an ever increasing level of debt in order to have price stability. In order to have price stability, if GDP grows by 2%, then the monetary aggregates have to grow by 2%. We have to have an ever increasing level of debt, but a lot of economists say one person’s debt is another person’s asset. No, debt creates saving, not the other way around. You have to turn the whole thing on its head: if there was no debt, there’d be no savings.

We know the $30,000 was created by the bank, but where did the $3,000 come from? We’re always short. There is never enough because we always create debt but not interest. The first users of money are always the greatest beneficiaries. In this case, it’s the banks or the people wealthy enough to borrow these funds at ridiculously low interest rates.

INEQUALITIES

Back to reserves, it’s a dual cycle system where two cycles run simultaneously and do not interact. When the Fed creates $3T, we run a fractional reserve banking system at about at 10% reserve ratio. In theory, if it were the Fed creating money through their reserve system, $3T would be the equivalent of $30T on the street. Well, that didn’t happen. What happens is that the FOMC create this “money” on their balance sheets and go out and buy paper – Treasuries and agencies – and goes to the bank because they have to buy from a primary dealer. The bank hands over the Treasury for $1000. Where does that money go? It goes nowhere because it’s an accounting entry that goes from an asset to the Fed to an asset to the bank, but it stays as a reserve.

The effect of inequalities is unbelievable. Agencies are houses and Treasuries are bonds. What we’ve done is forced the market into higher risk and the people who own those assets have gone through the roof. The top 1/10th of 1% is almost the exclusive beneficiary of these trillions of Dollars that have been created. The banking system favors assets. It does not favor labor. It preserves assets and preserves their value. The way to solve this is to change our whole system for greater equality.

These are the biggest issues, and what do we do about it? The question really comes down to money creation. We can get into arguments with the Austrian economists about gold standards or methods of limiting the amount of money production, but that’s secondary.

There are two separate issues: how money is created and how we control that.

You cannot have the second issue without solving the first issue. The first issue, how money is created, we have to take out of the hands of private banks. It is an extraordinary privilege they have: they’re allowed to create money, and they’re allowed to merge their funds with their customer’s funds. No one else is allowed to do that and this is why we have bank runs.

How do we then create money? Some minor examples historically were through sovereign money, the power of the state to create money. The control level is actually much better, because currently we’re printing money and bankers are trying to maximize loans. The only reason they do not issue loans is when they don’t trust the customer or economy. So you have these huge ups and downs in the business cycle as a result of this kind of system. If you get away from banks creating money, you stabilize the system. How do you distribute it? You can do it directly through the government. In theory, the government represents everyone, so if you want to equally hand the money to everyone you give it to the government. Then banks become true intermediaries and depositors. It creates stability in the system because when you have a decreasing economic situation, the government can create the amount of distribution and pull it back later on.

This happened during the American Revolution, when they created Greenbacks to pay for the Civil War and to rebuild the country’s infrastructure after. We could do the same today for infrastructure and not create inflation. It has to be done carefully, and if it does you can stop it or sterilize the funds. We would not be left indebted.

CHALLENGES AND BOTTLENECKS – THE NEXT STEP

The bottlenecks are the smaller banks. Since Dodd-Frank was enacted, about 2000 community banks had gone bust or been forced to merge, because the regulatory expenses are so burdensome that they can’t handle it. Dodd-Frank is not needed under a system of sovereign money, so you don’t need a regulatory oversight like we have now because the system is internally stable. Lawyers and the employees involved in the regulatory system are opposed to this, along with the large banks that disproportionately gain. It’s regulatory capture.

What’s interesting politically is that people who are fairly strongly on the left or right are in favor of this. It’s the people in the middle who aren’t a whole lot that don’t care much socially, who need to be persuaded. There’s a rising level of interest as people start to understand that in effect, we’ve been lied to for the last hundred years about how the system really works. People are starting to get angry.

MONETARY TRUST INITIATIVE

The Monetary Trust Initiative’s goal has been to create a model. Four years ago the plan was Puerto Rico, now it’s New Zealand and some other small places whereby there is monetary autonomy and we can change the system such that it’s a demonstrable model that can be studied. All the attention is going toward that.

It is not currently operational there.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

LINK HERE to download the MP3 Podcast

06/20/2017 - The Roundtable Insight: Brett Rentmeester On Cryptocurrencies In An Era Of Financial Repression

FRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Brett Rentmeester, he is the president and Chief Investment Officer of WindRock Wealth Management. He founded WindRock Wealth Management to bring tailored investment solutions to investors seeking an edge in an increasingly uncertain world, he’s a veteran in the industry. He was a founding partner of Altair Advisers, a $3 billion investment firm and he served on the Investment Committee with a specialty in alternative investments opportunities. Prior to that, he was a manager at Arthur Andersen, helping to build their Investment Advisory and Private Client Services practice. He’s a CFA and also earned a Chartered Alternative Investment Analyst designation and he has an MBA from Northwestern University’s Kellogg Graduate School of Management. He also has activities as a philanthropic donor in areas of serving as the founding Board Member of the Northwestern Center for Integrative Medicine and a member of the Major Gifts Committee of the Edward Hospital Foundation in Naperville. Welcome, Brett.

Brett Rentmeester: Hey thanks for having me, Richard.

FRA: Great, today we would like to discuss with you a topic that you have keenly on your mind and that is in the area of cryptocurrencies. First, before we begin would you like to give a disclaimer?

Brett Rentmeester: Yeah, I think it’s important to just mention that we’re going to be talking about the theme cryptocurrencies in general, and in no way should this be considered investment advice in that people are always encouraged to talk to their investment advisors. The interviewee personally owns cryptocurrencies including bitcoin and ethereum.

FRA: Great, thank you. And so yeah, we’d like to go over a number of developments in the cryptocurrencies space. What’s happening and the technology behind that, the blockchain technology, what are the advantages of the technology, the power, the features that it is bringing to the economy? And what are merging applications that you see coming about? Also, we can go into a bit on the actual cryptocurrencies, your thoughts on Bitcoin, Ethereum, and others.

Brett Rentmeester: Sounds great.

FRA: So I guess to begin with can you give us an overview of cryptocurrencies in terms of the history and evolution?

Brett Rentmeester: Yeah, and it’s a great place to start because what we find is there’s a lot of misunderstanding. And as you and I were talking earlier, Richard, it is quite analogous to the early days of the internet. And when you think back to the perception in say 1994, if you said the word internet, most people had heard that word but probably associated it with this idea of some online college chat room. And then a couple years later they realized that it was a great place to find information and now they’ve realized that it’s changed the whole world and most business models along with it. So we think cryptocurrencies are really at that same stage, that the first reaction is people have heard of Bitcoin but associate it either with criminal activity or maybe think of it as internet monopoly money. But then they dig deeper and they find there is something to Bitcoin which is pretty unique which we’ll talk about, and then as they get past Bitcoin they realize Bitcoin is really just the beginning of this whole wave of cryptocurrencies and blockchain technology that’s going to change a lot of how businesses operate globally. So when we go back in the story of Bitcoin which was the first cryptocurrency, it dates back to 2008, and we think of it most easily as a sort of virtual money and payment system. So if you think of payment systems like PayPal or Western Union, you know it’s got some of those elements. And it was started by a mysterious founder that nobody really knows named Satoshi Nakamoto. And by owning Bitcoin you’re essentially owning a piece of the system, which again some people associate with a store of value, but at its core, it’s a payment system globally. But the real key behind Bitcoin and all these cryptocurrencies is the technology which is referred to as blockchain. And what’s really interesting if you think of Bitcoin is, compared to a bank, if you go to a bank and try to get your money, we’re long past the days where they go to the vault and pull out real physical money. It’s really a private accounting ledger, that the bank has, and they’re the middleman and they have to give you access to your money. Well, Bitcoin has taken that and made it a public accounting ledger. Something that’s transparent that gives you control of your own money where instead of having a bank as a middleman, it’s really a system that’s peer to peer. So the system’s maintained by all of these users and a group of people referred to as miners that help audit the system. So every transaction is seen in the light of day and it takes a number of people almost auditing it to confirm a transaction. So you get rid of the bank and the middleman. And what this really creates and has created in Bitcoin is this idea of a trustless system. The idea that for you and I to transact, I don’t really need to know who you are or trust who you are as a person, do my background check, all I need to know is I need to trust the Bitcoin system itself that if I’m receiving a payment from you that the payments been received, or I’ve sent the payment to you. So in this way it’s really revolutionized money and payment systems because now I don’t need a bank, I don’t need a middleman standing between me and my money. So as I mentioned earlier we’ll go into some of the tenants of blockchain in more detail. This movement is really much bigger than Bitcoin. Bitcoin is kind of the beginning, the application of a payment system and maybe a store of value. The next big wave in the development was really the founding of Ethereum in 2014. Which in layman terms I’d call kind of a technology protocol or open source systems where developers can actually build applications or so-called smart contracts that are using blockchain technology in different business applications to get rid of the middleman. So this time not in banking and money transfer, but in other industries where we’ve long relied on a middleman or gatekeeper in the middle that’s taking a fee. So it’s almost like a Microsoft operating system for blockchain applications, and that’s given way now to really a rush of new companies in almost every industry.

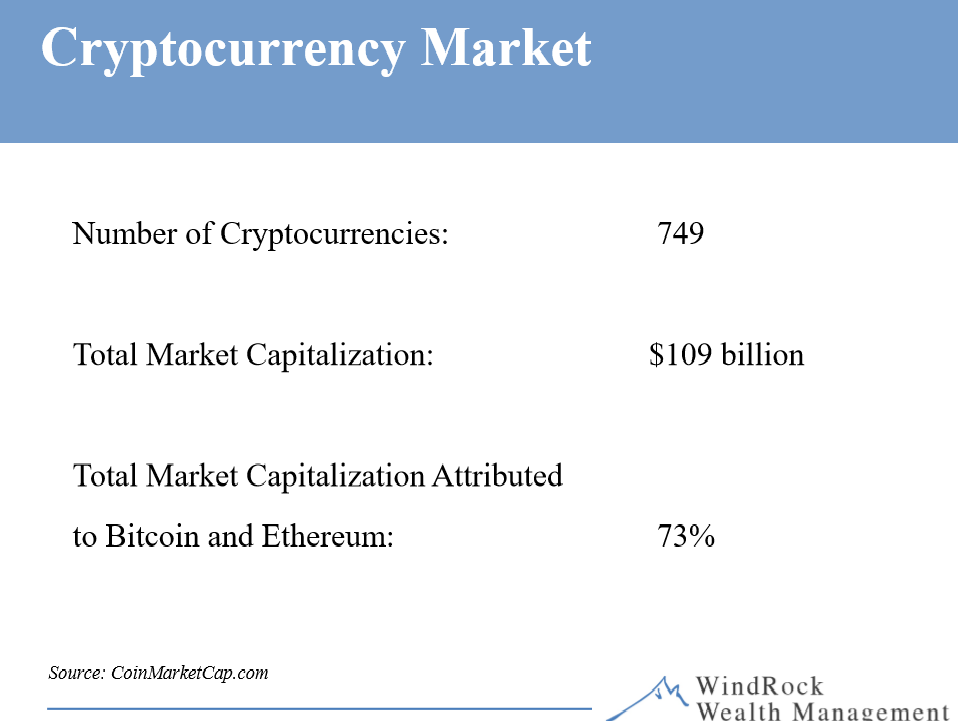

FRA: And you’ve kindly provided a couple of interesting charts which we’ll make available in the write-up, the transcript to this interview discussion on Bitcoin and Ethereum very interesting fact that you have there is that the total market capitalization attributed to Bitcoin and Ethereum is 73% out of a total number of cryptocurrencies of over 700, that’s quite fascinating.

Brett Rentmeester: Yes, yes absolutely. And yet the entire space is only about $100 Billion which although a big number, pales in comparison to some public companies out there. So it’s really in its early innings.

FRA: And so, what is exactly blockchain if someone was to ask, inquire. What is the nature of that technology? Is it sort of like a secure spreadsheet? Like an Excel spreadsheet that’s secure in some way?

Brett Rentmeester: Yeah, well I’m not a programmer but conceptually I think it’s an accounting ledger. It’s a record keeping mechanism, a program, an algorithm that’s keeping record of all transactions. So if I send Bitcoin to you it’s transacting that I used to be the owner of that block on the chain or node and now you are. So it’s a way to make something where you used to need a middleman keeping tally of all of that to allowing a computer program to do it. But really the genius behind it is empowering the users to verify transactions. So if you and I have a transaction, before it can complete it takes a certain number of users that are active and supporting the network, those are referred to as miners, almost like gold miners in a gold analogy, to actually audit and confirm that transaction. So it’s almost like I can feel secure in the fact that we made a transaction in Bitcoin and I got my money because a dozen people did an audit on it before it could go through. So the chance of them all colluding or something happening is pretty low. That’s the best way I can describe it to someone who’s not a programmer.

FRA: And what are some of the emerging blockchain applications that are currently out there and that are coming out in the near future?

Brett Rentmeester: Yeah, well I guess to give a little perspective to that, maybe just back to the internet analogy for a minute can kind of give the framework of what’s coming out because obviously the internet is probably the most sweeping technology of our time, and it did liberalize information sharing and collaboration. But it had two primary problems that blockchain helped solve. The first was, even though it’s the system we all use, it’s still controlled by big corporate users. Meaning if you’re on YouTube, YouTube gets most advertising revenue, not the posters of content or the active users. Same thing with Facebook, most of the economics go to Facebook the company, not the most value add users and active users. We’ll talk about how blockchain solves that, but the second thing with the internet is everything went digital in the world, but we still don’t have a way to feel great about the security of data. So cybersecurity is still a huge issue. So what the blockchain has allowed and where these businesses are popping up are in a couple of areas, but blockchain has allowed: 1 the power to come back to the hands of the people as we’ve talked about. So, instead of Facebook getting all the economic benefit, there are models out there now where the users get the most economic benefit. If you post a video or an article and it has a huge amount of hits, you’re actually going to be rewarded in the token or currency of that system. And if you’re a contributor and you make value added comments you’re going to get a reward; it’s not going to go to a platform provider like YouTube or Facebook. So I think that key concept of it being peer to peer has a real power to it, because fundamentally it cuts out the middleman, and we’ll talk in a minute about other areas, but I think social media is ripe for this. The idea of these are peer to peer social networks, why are all the economics going to be companies? So again, this is as you and I talked from a financial repression perspective, this is a very empowering concept because it’s putting control back in the hands of individuals and really away from governments and big companies because they’re not needed as the middleman. The second big problem of security, we think the blockchain helps solve. I don’t want to say it’s an unhackable technology, but let’s call it virtually unhackable. Meaning there’s no corporation, no CEO, no central server that can be hacked. It’s literally a web of users, a whole ecosystem where the blockchain is copied and replicated on all the user computers such that if one or two computers or one server is infected with a virus, it’ll be identified by the remainder of the network. So it’s possible to be hacked, but it would be much harder than today where people are hacking into single servers. So when you start going one step deeper on what are the applications coming out, we talked about some of the social media ones, and they go by names like Steemit and LBRY credits and SingularDTV – I mean there’s all these upstart ones that are replicating YouTube and Facebook and other things. And again incenting the users and the content providers. There’s also people out there in the esteem of giving power back to the people of allowing you to earn money on things you have to lease out. One of the more interesting ones is Golem where if you have extra computing power you can basically lease it out and somebody can garner all the world’s computing power into probably the biggest supercomputer in the world. And you, the person lending out your CPU power in getting incentive for it in Golems coin or token. So you’ve got some really innovative things, you’ve got gaming coins coming out, the idea that maybe fantasy sports, maybe normal gaming will start rewarding winners and users using their own coins. So you have this whole element of peer to peer coins and things that we’ve already got natural networks. On the other side though, back to the cybersecurity, we talked about the issues of sensitive data and all these hacks and cybersecurity issues we’re finding. And so I really believe any sensitive data in the future is going to run through some sort of blockchain technology. Now that may be blockchain technology developed by private corporations for their own company, maybe some of these other applications. But you’ve now got companies out there trying to use blockchain to make healthcare records unhackable, you’ve got companies out there like Storj coin (note: I keep say companies but I’m really referring to coins or tokens) where their trying to create an unhackable cloud storage service. So if you’re backing stuff up, personal information, pictures, things to the cloud, that can’t be easily hacked in the way it can today. Those are two things that I think solve the issues you talked about, but this idea of a trustless system in eliminating the middleman goes even further and can disrupt almost any industry with a middleman. So think of industries like real estate where you’ve got escrow companies and title companies, all these people in the middle of a transaction just to make sure you’re both good parties and both parties makes good on their promises. Blockchain technologies could end up eliminating all of those middlemen in the future. Or even things as common as stock exchanges today, I mean why can’t there be a global network of peer to peer users trading Apple stock where there’s no middle centralized exchange taking a fee from every transaction. Now, I think you might have a couple of thoughts with the regulatory issues with that, but conceptually this idea of getting rid of the middleman. Instead of seeing all these IPOs on Wall Street where Wall Street takes a huge fee, we’re starting to see this new phenomenon referred to as Initial Coin Offerings (ICOs) which are these businesses coming out and not paying fees to Wall Street, but coming out and issuing a coin, almost like a crowdfunding where people that put money in get a coin which inherently is a piece of the system. So the value in the coin is you own a piece of the platform. And interestingly enough, Richard, this year alone the initial coin offering market has raised $327 million whereas the venture space has invested $295 million in these technologies (source: Coindesk). So you’re starting to see this initial coin offering market take off and maybe that’s the future of fundraising. Again, unless there are regulatory issues that pop up but they haven’t thus far.

FRA: That’s all fascinating. So this represents potentially incredible opportunities in a number of areas?

Brett Rentmeester: Yes absolutely. And it’s really just beginning so you know irrespective as to whether somebody wants to be an investor in this space I think you can step back and think about our economy today and look at industries that are likely to be disrupted and think critically about what to do about it if you work in one of those industries. Or it could be an opportunity for entrepreneurs to disrupt many industries.

FRA: And a key point on these blockchain applications is that a number of cryptocurrencies can be applied to each application, we’re not mandated to use Bitcoin or fixed upon one cryptocurrency. It’s all likely to be interoperable, your thoughts on that?

Brett Rentmeester: Yeah well that’s right, I mean that’s what makes it so exciting, it’s true entrepreneurial spirit at its best. Bitcoin right now is, by market cap, the largest payment store value system, but this is technology so it doesn’t have to stay that way. Just like Myspace disappeared and Facebook came out of second or third place or wherever it was, it is uncertain who will be the winner. But because these are not corporations and centrally controlled enterprises these platforms as I’ll call them evolve themselves meaning Bitcoin today and Bitcoin five years from now could be very different things. And it’s really up to the Bitcoin user base and again these more active miners who are maintaining the system and collectively kind of voting to make changes to see what things evolve. So if there’s an upstart coin that’s competing with Bitcoin, Bitcoin itself could decide to change to be more competitive. So it really is this amazing free market experiment right now that’s a little bit like the Wild West. And I mean that’s part of the caution because you’ve got a lot of ideas being funded that are simply ideas. And you’ve got other businesses that might be great ideas but are at the very beginning. Now again if we were critical and went back and looked at the first week of YouTube being out there and the early days of Facebook, I’m sure it would leave a lot to be desired too from where they’re at today. But it is an area that’s highly volatile and very exciting, but it’s definitely the Wild West.

FRA: So if we focused down on the actual cryptocurrency landscape, what does that look like today in terms of the types of cryptocurrencies, what they are, and what their potential is?

Brett Rentmeester: Right now by most counts there are about 750 cryptocurrencies, so more than anybody probably thinks there are. But collectively, it’s only about $100 billion of value. So again, imagine if you could have gone back in the early days and someone told you all Internet stocks together are $100 billion, it may seem like a big number but now that we sit here today in 2017, if you could have bought the internet for $100 billion you would have done it. So I think there are a lot of companies, there’s only a handful with scale right now, and that’s why when you cited earlier Richard that Bitcoin and Ethereum together are over 73% of that market capitalization they’re the big ones, but the space is just beginning. I mean a lot of these coins a lot of these ideas I’ve referenced are things that have just come out in the last six months. So this is brand new. So just like YouTube started with a couple million dollars invested and it’s now probably a $10 billion plus enterprise within Google, you know some of these things will likely be big disrupters. Now that’s not to say that the entrenched powers won’t evolve and try to engrain blockchain technology in their systems as well, but I think what makes this exciting and so disruptive is that the whole concept is peer to peer. That means users and content providers should get paid, and not just the corporations. So I think it’s a fundamental shift we’re seeing. You know, we’re seeing a lot of people really interested in blockchain and not quite sure how to navigate the space as they look into it because it is brand new.

FRA: And what is the potential evolution? Do you see governments getting into this in terms of establishing cashless societies based on cryptocurrencies by using government based cryptocurrencies? And will governments allow the use of non-government cryptocurrencies like Bitcoin or BitGold, other types of cryptocurrencies, do you see that happening?

Brett Rentmeester: Yeah, I mean you’re right. The risks out there, the primary risk is what governments do because there is no telling how far they can go to stop it. But I use the same analogy back to the internet, even if they wanted to stop the internet, could they have? I don’t know. And would they have shot themselves in the foot so much by giving up that economic benefit? So it’s tough to say, I mean the central banks andgovernments we know want control. On the other hand, right now you’re starting to see more and more countries kind of throw the towel in and say we can’t control this because it’s not a central entity it’s not just something local, it’s a global market. So if we shut it down in America and everybody else adopts it, they have a huge technological lead over us. And so you’ve seen some really interesting developments, you saw Russia go from very adverse to all these cryptocurrencies to being very open about it. In fact Putin just met with Vitalik Buterin, the founder of Ethereum I think last week, so that’s an interesting sign. Japan just on April 1st made Bitcoin legal tender, you know as good as the yen in the country, so think of that impact. So if you’re a Japanese investor under that system and burdened with that debt with negative interest rates, you’d think everybody would put a piece of their money in something like that. And you’ve even got countries like Australia slated this summer to make Bitcoin and other cryptocurrencies legal tender. So I don’t know, you would think it’s one of two things. Either governments are letting this happen to allow people to become used to a cashless thing and then might come in and try to enforce their own system, or they’ve conceded they can’t control it. I don’t know, do you have a point of view on that?

FRA: I think that it’s likely that the cryptocurrencies which are based or regulated within the financial system and perhaps privatized would likely be allowed to coexist with government based cryptocurrencies. So if you have a cryptocurrency like BitGold which provides compliance to regulations within the financial system, even though it is outside of the banking system, it does comply with the banking type of regulations for deposits. So I would say in that case the governments would allow those types of cryptocurrencies to coexist. And in that sense, it’s better to have or to be into cryptocurrencies which are either backed by some type of commodity like gold or perhaps just private based relative to government fiat based cryptocurrencies.

Brett Rentmeester: Right, but it does bring up a good fact. I mean given that the fractional reserve banking system is so over-levered, globally, but just thinking about the U.S. for a minute if everybody put 5%-10% of their money in Bitcoin or some other cryptocurrencies, the whole banking system implodes on itself. So you’re right, it’s really unknown forces ahead. But right now, even in the U.S. there hasn’t been a big move to crack down on it. I mean even though it’s not treated as currency and tax-free, it is given capital gain treatment for long-term holding which is more beneficial than some other assets. So I don’t know, again I’m back to it’s a global world, so a country that chooses to really crack down on it faces a big technological disadvantage relative to other countries that are endorsing it. And so I think you’re going to have a race for countries wanting to endorse it. But maybe the risk is a big global clampdown at some point, it’s hard to say. But for right now the future looks really bright from a technological point of view.

FRA: What are your thoughts on these cryptocurrencies as being stores of value? Do you see them as more of payment systems? Are they deriving a lot of their value from the ability to move money around? Like many have pointed out the use of Bitcoin by Chinese and China looking to diversify outside of China in terms of their asset holdings? So perhaps some of the value has been derived from that utility value, being able to move money around. What are your thoughts on that? Is it a real store of value?

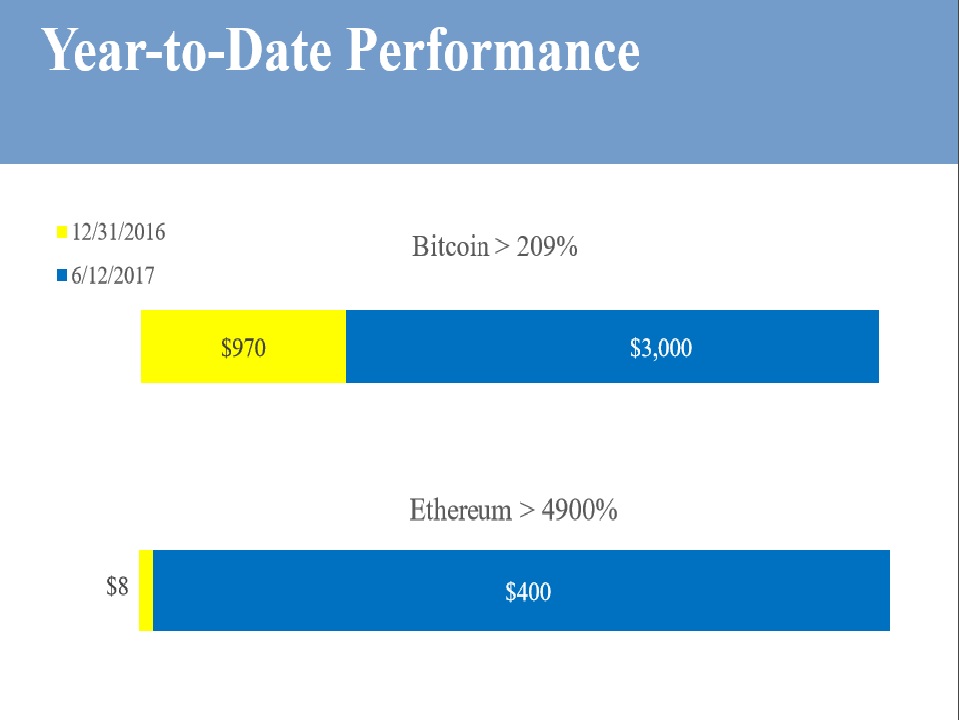

Brett Rentmeester: Yeah, well it’s an excellent question because I think one of the biggest questions most people new to this space have is why do these things have any value? Explain to me why Bitcoin is worth what it is, or Ethereum. And so when you step back, I guess the way I view it is owning a coin, a Bitcoin or an Ethereum token, is essentially owning a piece of the platform they’ve created. So it’s not that different then if Facebook, instead of being a public stock had Facebook coin. And if you owned 10% of the Facebook coin it was like you own 10% of Facebook. So I view it very analogous to owning equity. It’s almost like you own a piece of the system. So if the system is Bitcoin and you believe it’s a valuable payment system and more people will come on board, that in of itself is a form of store value. Now, that may be different than owning gold and other things, I don’t think we have to say they’re the same, they’re not, but just say it’s a payment system for a moment. The current market capitalization or size of Bitcoin is about $43 billion, so it’s grown a lot, it’s done tremendously well. But the market capitalization of PayPal, another payment system is $61 billion. Visa is $211 billion. So I step back and say, okay is the value assigned to all of Bitcoin reasonable? It sure seems like it to me, because I would imagine Bitcoin’s got the potential to be much much bigger than PayPal, and probably surpass a lot of these credit card valuations over time. So I look at it that way, but it is a hard thing to assess. Same thing with Ethereum, I don’t have the number in front of me I think there may be $34 billion, but you compare that $500 billion for Microsoft, you know could they be the next “operating system for blockchain applications” they could be, they may or may not be. But you know I think you have to look at value on a relative basis and acknowledge that what you’re really owning when you own a coin is a piece of the system. I think once you get to that level of understanding, it’s a little easier to think about how value works and why people are assigning value to these tokens or coins.

FRA: So is it in a bubble or is it just volatile just like the other currencies?

Brett Rentmeester: Yeah, I think it’s just inherently volatile because it’s unregulated and it’s the Wild West and it’s got a trajectory that’s going to happen quicker than the tech boom did. So if technology stocks started surfacing around 1994-1995 and ran to 2000, so five to six years, maybe this is a tighter cycle. I think we’re going to see a bubble perhaps, but I don’t think we’re there yet. And I say that because in all the anecdotal evidence we get we find that still, most people don’t really understand this space. In polling people almost nobody’s an investor even in Bitcoin and Ethereum. If you really ask 1,000 friends that are pretty well to do with money, very few people actually have money in. So I think the space from an investor point of view has been dominated by kind of techies. People that knew the technology and got involved early and get it. Or some traders. And it’s a difficult space to navigate, it’s not as easy as just going to your Fidelity account at least today, or Schwab and just buying the stock, you have to navigate these private exchanges, you have to hold it in these things called private wallets, there’s a lot of security issues you’ve got to be aware of. So it’s a pretty treacherous thing, it’s taken us a long time as investors to get up to speed on how you navigate it. So I think given how rough the landscape is of doing it, it just seems to me like the demand side is just beginning. That if the door starts opening for easier ways for people and institutions to put money in, you’re going to see the demand side grow and you’re also going to see the supply side grow as these disruptive businesses shake up other industries. So I think again the analogy’s pretty good with the internet boom, you’re going to see probably a big boom ahead. And somewhere down the road, you’re going to see a washout of a lot of the ideas that should have never been funded or really had no use. So like the modern day Pets.com, some of that. But out of those ashes will come the Facebooks, the Googles, the Amazons and everybody else. So, it’s going to be a highly volatile area, but I think for people that are looking for the next growth engine in the world, there’s no more exciting place than this. I think the blockchain tsunami has really just begun to sweep over the world.

FRA: Yes, and as you mentioned, we are in the second inning only. And also you mentioned this technology will revolutionize almost every business.

Brett Rentmeester: Yeah, it’s pretty remarkable. The more time I spend on it the more excited I get about the prospects for blockchain and in all the applications in the future. So I think for those people that aren’t taking the time to really understand it, they’re missing something arguably as big as the internet revolution where they can take the time and understand it today they will have such an edge ahead.

FRA: Well great, thank you very much for your insight, Brett. How can our listeners learn more about your work?

Brett Rentmeester: Yeah, they can go to https://windrockwealth.com/ that’s our wealth management company, we have a research and analysis section. Or they can reach out, I’ve got a long email but it might be in the reposting. I’ll leave my phone number which is 312-650-9593. We’re investors in this space and we spend a lot of time understanding the structure of the space, and it’s very unstructured, like we said it’s the Wild West. So anybody dabbling in it needs to be very careful, but by the same token, it’s a very exciting space to be part of.

FRA: Excellent, great, thank you very much Brett.

Brett Rentmeester: Thank you Richard.

Transcript written by Jake Dougherty jdougherty@ryerson.ca>

06/16/2017 - Charles Hugh Smith: Debt-Asset Bubbles Implode Either Via Inflationary Collapse Or Via Deflationary Collapse

“When debt-asset bubbles expand at rates far above the expansion of earnings and real-world productive wealth, their collapse is inevitable. The Supernova model of financial collapse is one way to understand this .. Financial supernova collapse has two pathways which we call deflationary and inflationary .. In a deflationary supernova, defaults–and the avoidance of additional debt–are the gravity that overwhelms the forces of expanding debt. Once the losses and risk are visible to all participants, the herd psychology changes, and participants no longer believe that central banks ‘are now the ultimate power in the Universe.’ .. The other pathway to implosion is to print currency with sufficient abandon that debtors have enough money to service their debts. Emitting sufficient new free money to re-set all the unpayable debt destroys the purchasing power of the currency–a supernova implosion that is little different than the deflationary implosion. The inflationary pathway results in the destruction of the currency, impoverishing everyone holding the currency.”

06/16/2017 - Satyajit Das: Policy Makers Are Using Financial Engineering In An Attempt To Maintain Economic Growth

“Rather than reducing high borrowing levels, policy makers use financial engineering, such as quantitative easing and ultra-low or negative interest rates, to maintain them, hoping that a return to growth and just the right amount of inflation will lead to a recovery and allow the debt to be reduced. Rather than acknowledging that the planet simply can’t support more than 10 billion people all aspiring to American or European lifestyles, they have made only limited efforts to reduce resource intensity. Even modest attempts to deal with environmental damage are resisted, as evidenced by the recent fracas over the Paris climate agreement. Short-term gains are pursued at the expense of costs which aren’t evident immediately but will emerge later.”

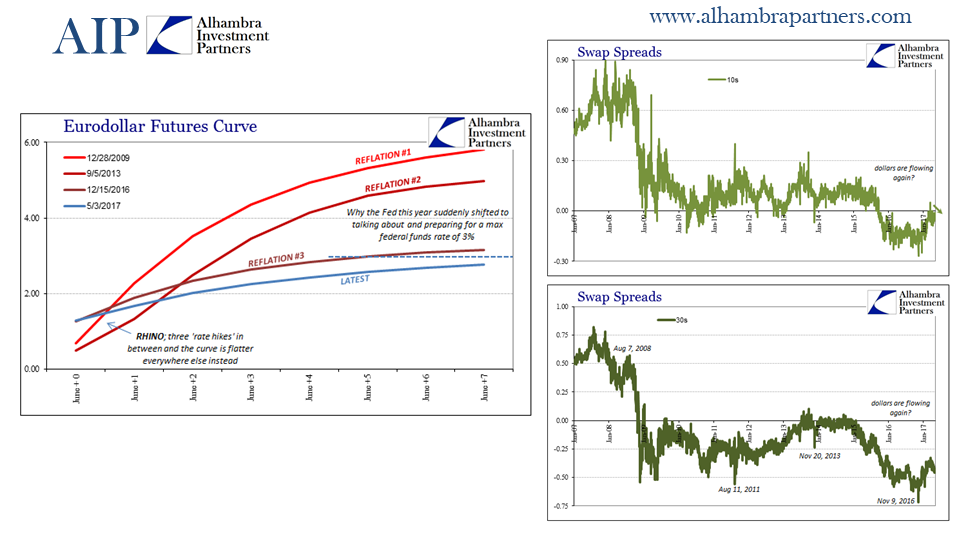

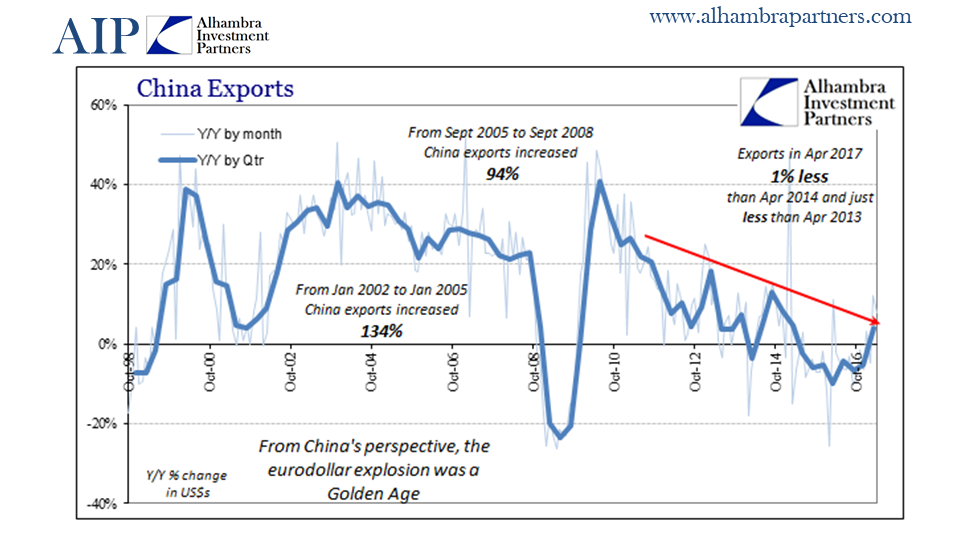

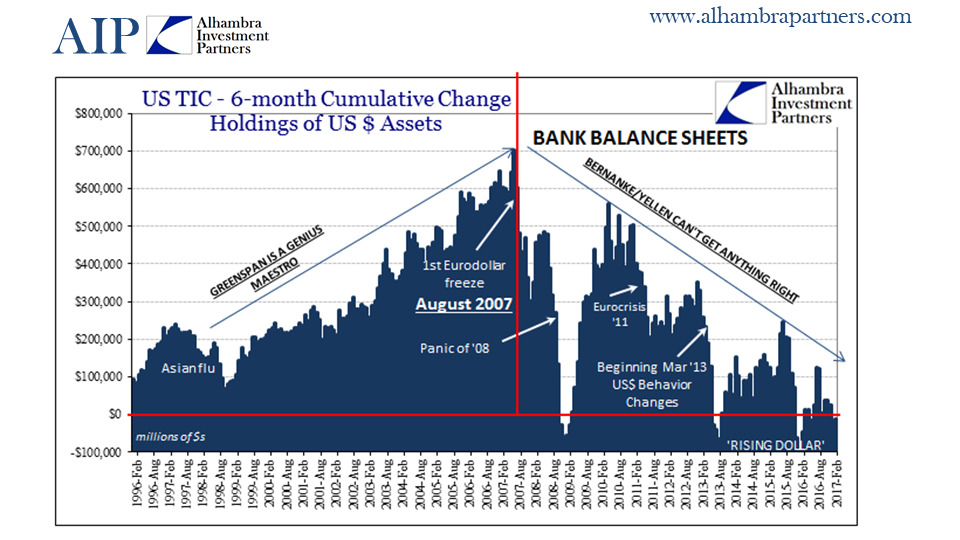

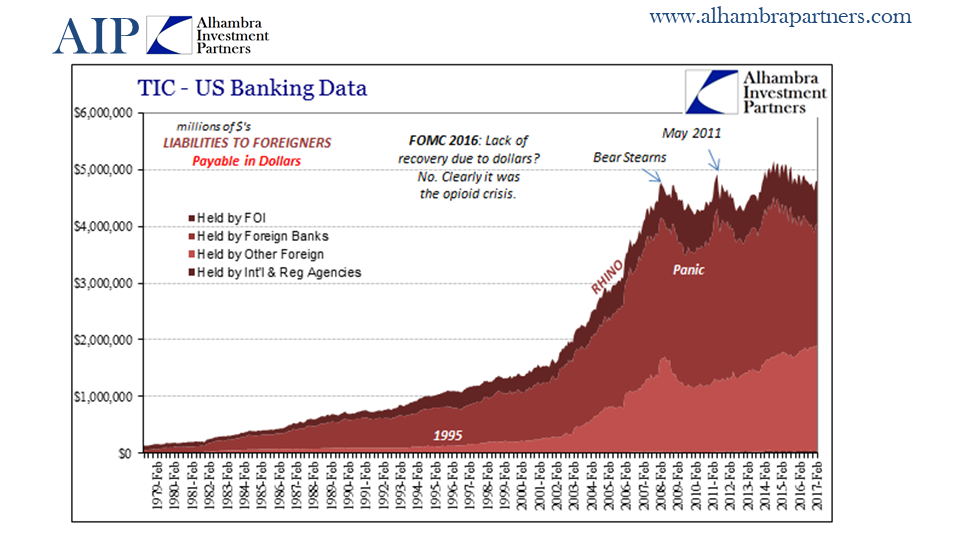

06/15/2017 - The Roundtable Insight: Jeff Snider – We Have A Shadow Money Driven Economic Depression

FRA is joined by Jeff Snider to discuss the shadow banking system and monetary policy.

As Head of Global Investment Research for Alhambra Investment Partners, Jeff spearheads the investment research efforts while providing close contact to Alhambra’s client base. In the nearly year and a half run-up to the panic in 2008, Jeff analyzed and reported on the deteriorating state of the economy and markets. In early 2009, while conventional wisdom focused on near-perpetual gloom, his next series of reports provided insight into the formative ending process of the economic contraction and a comprehensive review of factors that were leading to the market’s resurrection.

In 2012, after the merger between ACM and Alhambra Investment Partners, Jeff came on board Alhambra as Head of Global Investment Research. Currently, Jeff is published nationally at RealClearMarkets, ZeroHedge, Minyanville and Yahoo!Finance. Jeff holds a FINRA Series 65 Investment Advisor License.

FRA: So we have a real special treat. You’ve provided some slides that will be made available on the website and also in the body of our write-up. They provide some great insight into monetary policy evolution over the last couple of decades and what we’re going to be talking today is monetary policy in 2017: h the Federal Reserve is raising interest rates, why they’re doing that, and how the whole evolution over a long period of time, the last couple of decades, especially since the 1990s, has led to bubbles and overall economic chaos. So with that, if you want to start an overview of what you’d like to talk about and start getting into the slides?

SNIDER: We have a bit of a contradiction here because the Federal Reserve in 2017 wants to raise interest rates. I think they’ve made that very clear that’s what they’ve wanted to do all along for the last couple of years. Yet most people have an intuitive sense that the economy hasn’t ever recovered from the Great Recession. So we have this disconnect between what they’re doing and the way the world actually seems to be, and there doesn’t seem to be a good explanation for why all this has occurred the way it has. The reason for it is because the monetary system and the banking system have been drastically changed over the last few decades, especially during the 1990s, the all-important years that led monetary policy along a different path than the economy and the markets. So to understand what the Federal Reserve is doing today, you really have to review how monetary policy evolved as the banking and monetary system evolved.

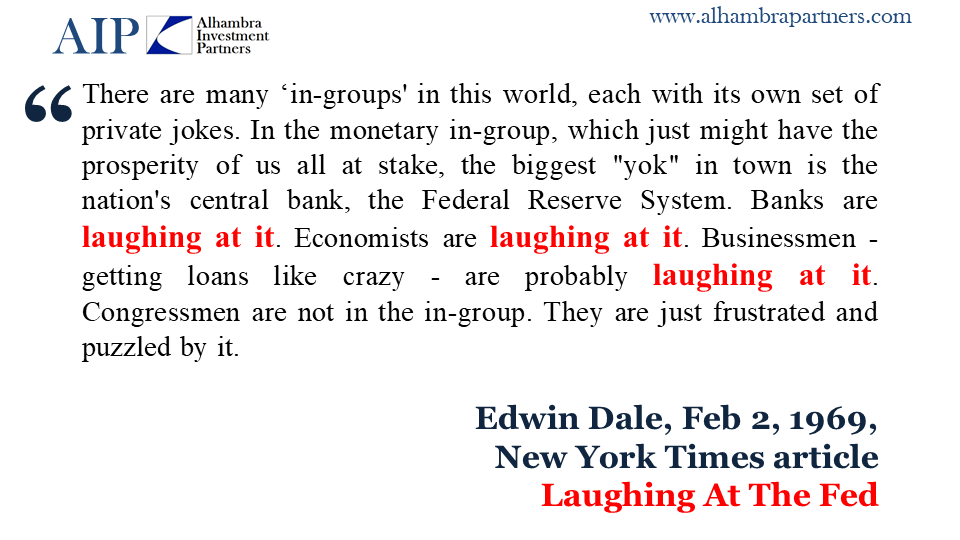

FRA: And to begin with, on the first few slides you’ve got a quote from 1969?

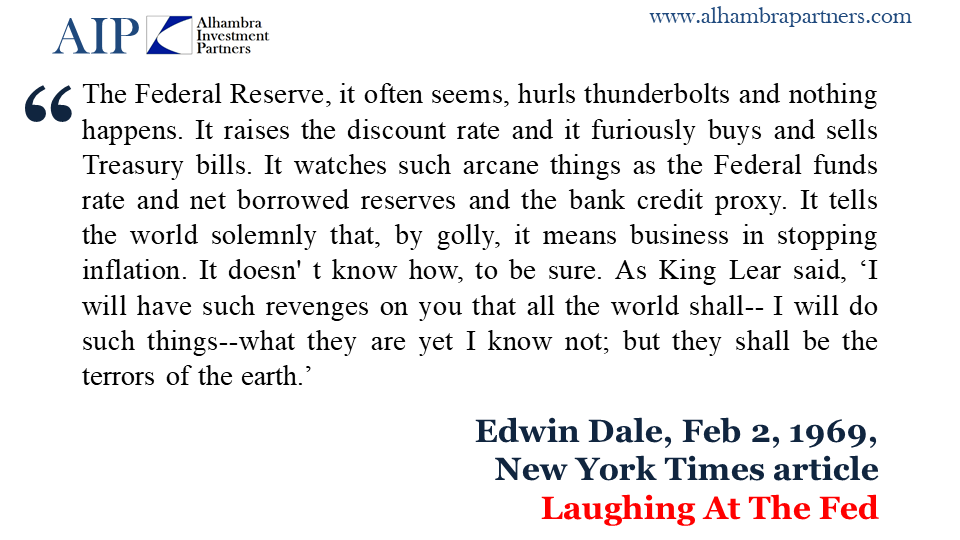

SNIDER: Edwin Dale was a reporter for the New York Times. In early February 1969 he wrote an article that was called ‘Laughing At The Fed’. It was a fairly typical article for Edwin Dale, and Edwin Dale wasn’t a typical beat reporter for the New York Times, he was very well known, very astute observer of economics and monetary policy. The article had such an effect that two days after it was published, it was actually discussed in the FOMC meeting that followed just after. In fact, the best part of the story is that Frank Morris, who was the president of the Boston branch of the Federal Reserve, actually took it upon himself upon reading Edwin Dale’s article, and asked various banks in his bank district whether or not they were actually laughing at the Fed. Which, I think, is a pretty good starting point to tell you about the timeless nature of policy makers, how they can typically be thin-skinned and often probably too self-assured. And, furthermore, how none of the banks actually answered back that they were laughing at him when in fact you could be sure that as soon as they hung up the phone with Mr. Morris that they actually were laughing.

That was kind of the period in 1969; just on the cusp of what would become the Great Inflation. And it became the Great Inflation because Edward Dale was essentially right. The Federal Reserve had no idea what it was doing, even though it sounded like it was in command of every little minute detail. It’s almost a perfect mirrored start between then and now because nowadays things are very similar: the Federal Reserve makes a bunch of claims, does a bunch of things, and nothing ever seems to work. But that’s not the way it was. In 1969 when people were supposedly laughing at the Fed, to 1999, things had changed very drastically.

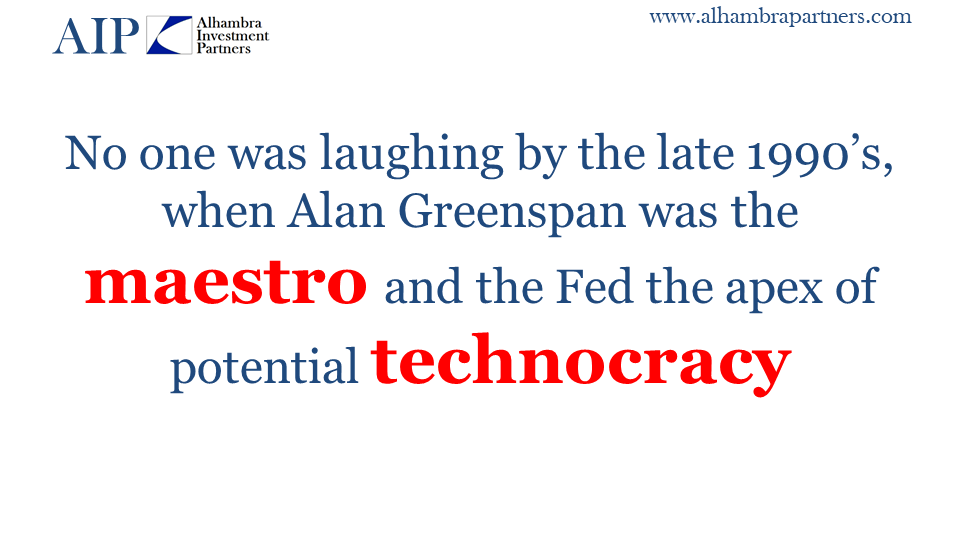

In 1999, Alan Greenspan was considered the maestro. He was essentially the most admired central banker in history. So we have to understand how it got that way, how the Fed in 1969 go from being a joke to, by 1999, being the apex of technocrats?

FRA: As you mentioned, no one was laughing by the late 1990s when Alan Greenspan was the maestro.

SNIDER: If you go back to that time period, if you’re old enough to remember the Dot Com era, Alan Greenspan was, on Wall Street at least, a god; even with the mainstream media he was something of a celebrity. I remember that his briefcase even had its own page on CNN.com when the internet was relatively young, because it was believed that you could tell whether or not the Fed was going to raise rates by what hand he was holding the briefcase. It got to be that kind of almost cultish behaviour because of his reputation and the reputation that people believed was based on actual condition.

FRA: So what really happened in the 1990s? Can you elaborate?

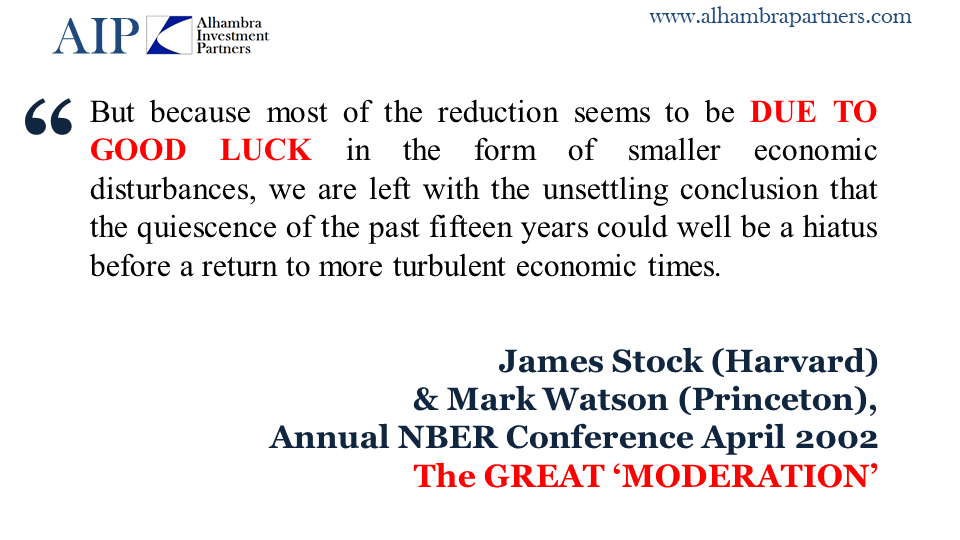

SNIDER: There was a lot of disagreement over what happened. If you were a stock investor, Alan Greenspan was the chief; even in the academic circles of mainstream orthodox economics, there was quite a bit of doubt. In 2002 for example, James Stock of Harvard and Mark Watson of Princeton delivered a presentation at the annual NBER conference that coined the phrase ‘the Great Moderation’. And what they were doing was try to figure out where this oasis of low volatility economy actually came from. They assigned several reasons for it, and one of the most intriguing and most relevant answers they came up with was what they called just pure good luck. What they meant by that was during the 15 years leading up to that point, during that decade and a half of what seemed to be a Great Moderation, there weren’t any of the usual kind of global monetary abnormalities that had plagued economic systems throughout history. From their position inside orthodoxy economics, especially in the academic side, that seemed to be just good fortune. When, in fact, there were other explanations for it that explained a lot more than just passable luck.

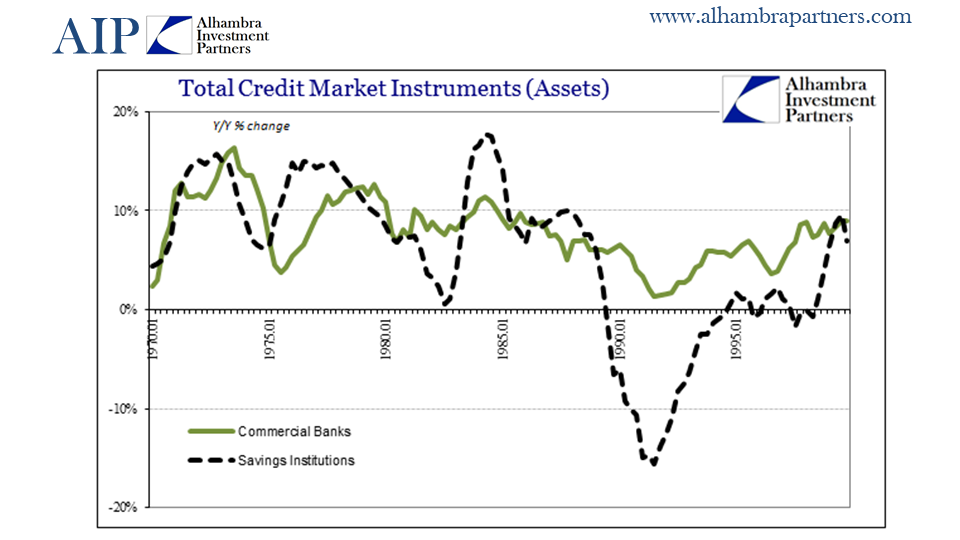

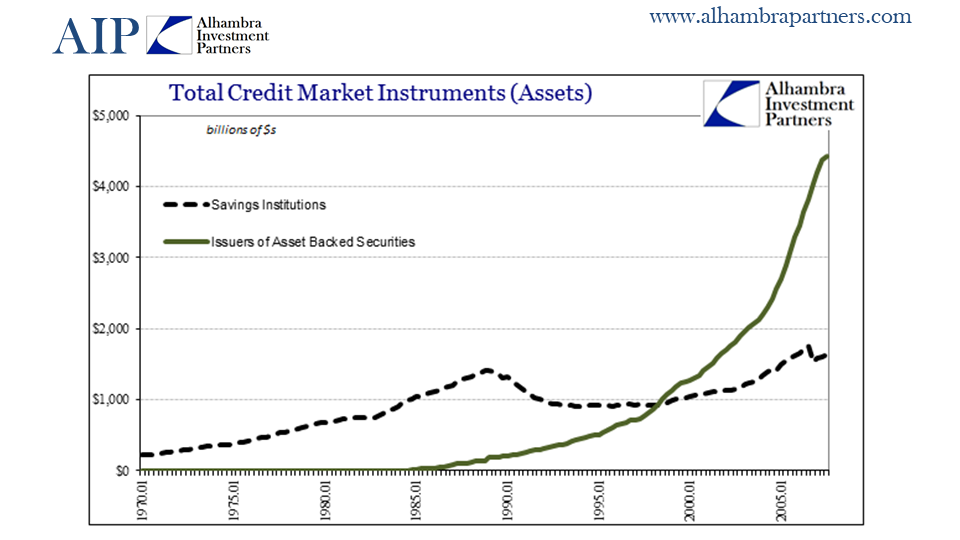

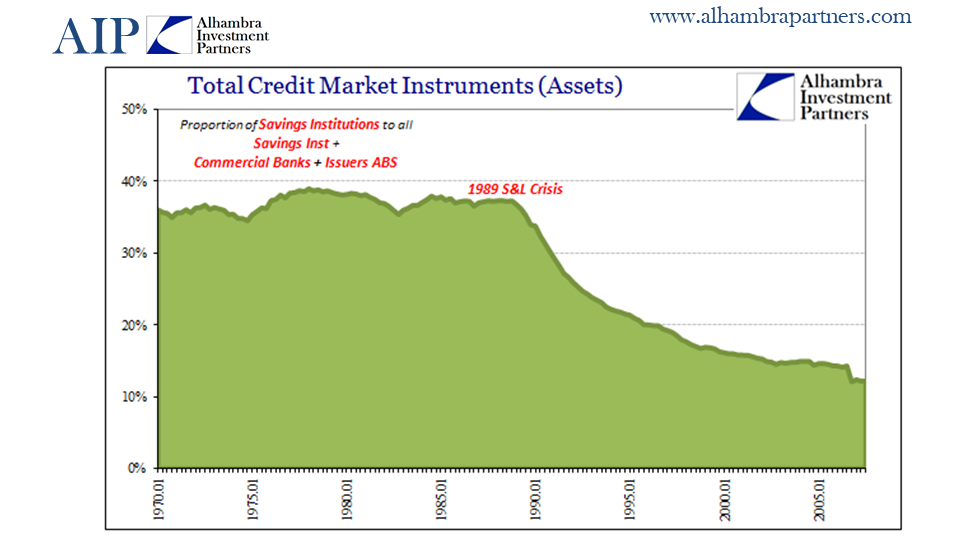

FRA: So take us through some of these initial slides here. You’ve got total credit market assets and how does the story develop over the last two decades?

SNIDER: Policymakers themselves, again going back to the 1969 Edward Dale article, were very interested in taking credit for the Great Moderation. They wanted everyone to believe, as many people did, that they were in control of the economy. That by increasing or decreasing the Federal Funds Rate a quarter point at a time, they could engineer the so called ‘Great Moderation’. Ben Bernanke actually gave a speech in 2004 where he actually made that claim: that monetary policy, under interest rate targeting, actually deserved the credit for the Great Moderation. It was a view that many people came to adopt, including many in the official academic circles, as well as people inside the Fed, where it was almost a given that monetary policy was perhaps the most powerful thing on Earth and that by controlling the Federal Funds Rate, the Federal Reserve could make everything go. But if you actually go back into the 1990s and review what happened, what you’d find is that, again, a radical transformation.

The S&L crisis that developed in the late 1980s pertained to what we all think of when we think of a bank: the bank as in taking in reserves of either cash or hard money, then the money multiplier taking that into levels of loans and deposits. The actual, traditional banking system. That wasn’t the only part of the banking system at the time, of course, but after 1990, after the S&L crisis, the traditional bank model essentially ended. By the mid-1990s, these new forms of banking and monetary advance had increased and grown so rapidly that they had surpassed the traditional model in every way, shape, and form.

I presented here just one of those possible avenues, which is the issuers of Asset-Bank Securities, the type of off-balance sheet arrangements that no one really became aware of until 2007 when it was too late. These were wholesale, modern vehicles for not just banking but securities, all sorts of money dealing activities… basically the whole range of what used to be done under the traditional banking banner were being done more and more under this brand new system that did not operate in the same way as a traditional bank. By 2007, the traditional banking system was a fraction of what it had been, even in 1990. So there was an enormous evolution of banking and even money because the way these things were funded over the 1990s.

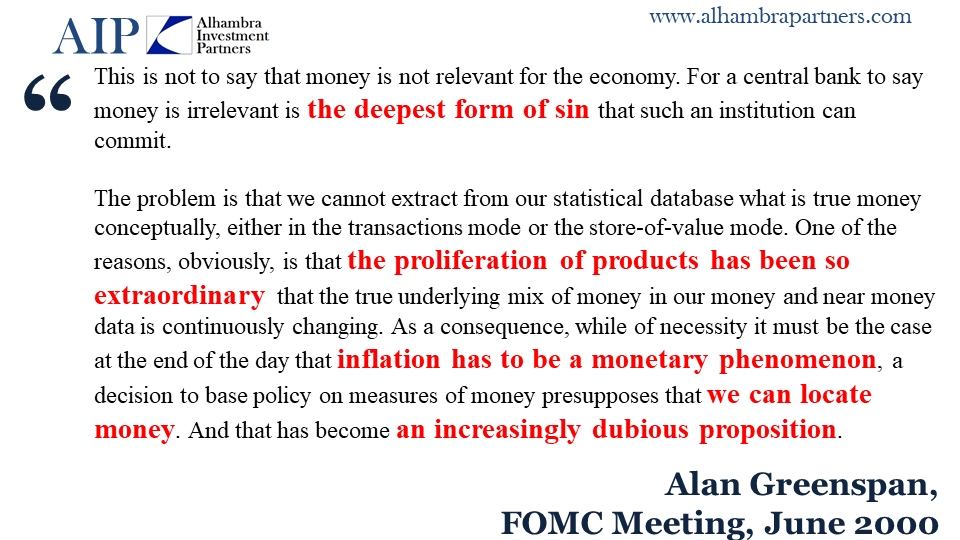

In fact, it was Alan Greenspan himself who noticed these kinds of things and mentioned them throughout the 1990s. I’m sure most people remember in December 1996, Greenspan’s irrational exuberance. But they remember it for all the wrong reasons. They think about the Dot Com Bubble and what they think of as a warning. But what he was really saying, if you read the speech before he got to irrational exuberance, what he was really saying is that the monetary correlation – the correlation between money growth and various money aggregates in the economy – had gone way off course during the 1980s. He was confident that by targeting just the Federal Funds Rate, that wouldn’t matter. In other words, he knew that monetary evolution was taking place. However, he felt that because the Federal Funds Rate was such a hugely powerful control mechanism, it wouldn’t matter that the Federal Reserve couldn’t even define money.

Any normal person in that situation, especially tasked with being head of the central bank, probably would be unnerved by it. But his reputation was such at the time and the conditions of how people perceived the economy, especially in 1990. It was a disconnect between what everybody thought he was able to do with the Federal Reserve and what he was actually able to do. And so proven through monetary policy there may be changes in the Federal Funds Rate, especially in the decade of 2000. You see this very big difference between what is supposed to happen and what does happen.

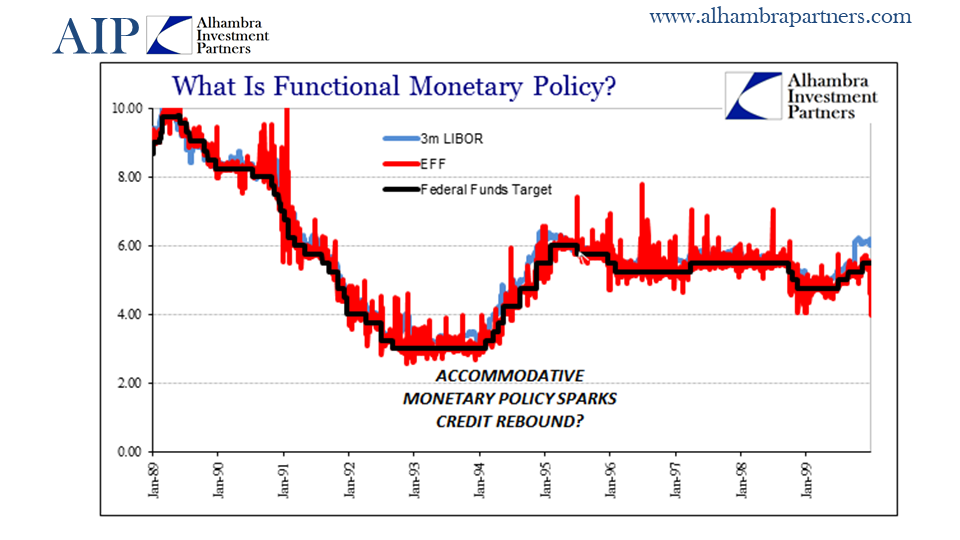

FRA: And that brings us to the concept of the functional monetary policy. We have a chart that sort of begins around 1989 and then goes into the 1990s that depicts accommodative monetary policy sparks credit rebound.

SNIDER: That’s what people conceive out of what the maestro was doing in the 1990s. He was moving the Federal Funds Rate around, either stimulating or tightening: the famous 1994 bond massacre when he tightened rates and engineered supposedly the soft landing for the middle 1990s. And there were other minor adjustments in the latter part of the decade. There was a 75 basis point rate cut around 1997-1998 related to the Asian flu, but overall what happened throughout the 1990s was that people got the idea that there was a correlation between what the Federal Reserve did with nothing more than the Federal Funds Rate, and this relatively calm period of economy where it expanded for a decade without any recession. Then 2001, the recession that did come was a very mild one, despite the fact that the Dot Com bust was an enormous event. So it really did seem like, on the surface, the monetary policy was a powerful instrument wielded by the best and brightest that we had to offer. Of course that really started to go awry with the housing bubble.

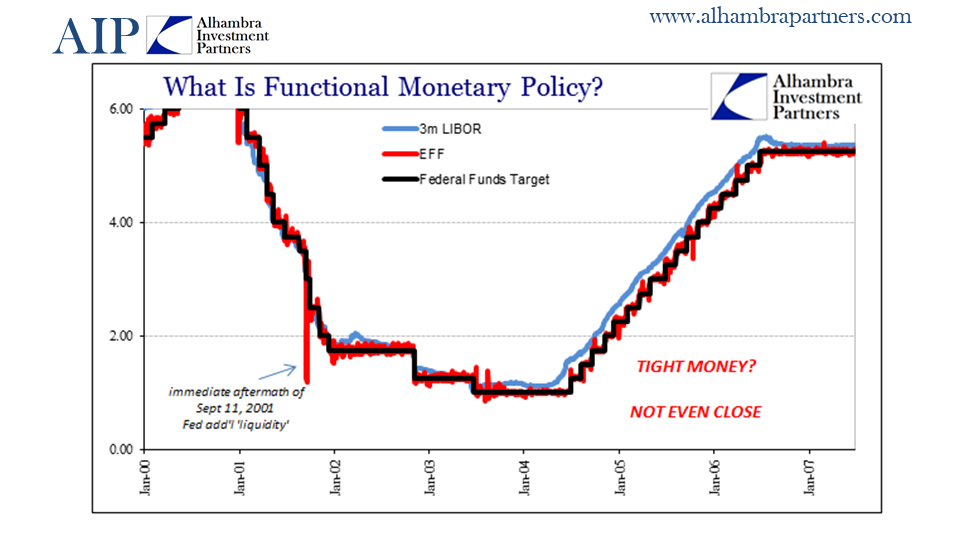

Really, the housing bubble goes back to 1995, and what we can see of the housing bubble conventionally is the housing mania portion, which is 2003 forward. During that period, we really start to see how monetary policy wasn’t what people thought it was. In fact, Greenspan’s Fed started to raise the Federal Funds Rate in lieu of 2004. He kept at it for 17 straight rate cuts, so that by June of 2006 the Federal Funds Rate had gone from 1.5% to 5.25%. Which sounds, on the surface, like a tremendous amount of monetary policy tightening, yet when you look around at that time and look through all the various statistic monetary economics, there was almost no detectable effect from that policy cut. In fact, conditions overall, especially monetarily outside of the traditional monetary statistics, it was actually the opposite. Greenspan intended to tighten but it was as if the banking system had simply gone insane in the opposite direction. It was expanding at an exponential, parabolic rate in almost every wholesale-shadowed capacity.

FRA: Moving past that into 2007-2008, as you show on the next slide, the interest rate going down and you question if this is accommodative money, not even close.

SNIDER: It’s funny. It’s almost an exact mirror image of the rate hike. During the hiking regime of 2004-2006, the Greenspan Fed raised the Federal Funds Rate from 1% to 5.25%, and then starting in September 2007 the Bernanke Fed just reversed it – it went from 5.25% back to 1%. During that period where this is supposed to be a hugely accommodative interest rate cut or a series of interest rate cuts, you cannot classify that period as accommodative in any way, shape or form. In fact, it ended up in the first global financial panic since the 1930s.

So what are we witnessing here with the Federal Funds Rate? It isn’t stimulus when they cut the Federal Funds Rate, just as it wasn’t tightening when they raised it. So what is actual, functional monetary policy? What we find is that it ties directly to the evolution of banking and money primarily through the 1990s, how banking had changed from the traditional banking model to this wholesale model which at the time in 2008 people had started to refer to as ‘shadow banking’. The reason we call it ‘shadow banks’ is because the central bank, the Federal Reserve and its cousins throughout the globe, simply dropped the ball. They stopped caring about actual functional money because they thought the Federal Funds was all they needed to control.

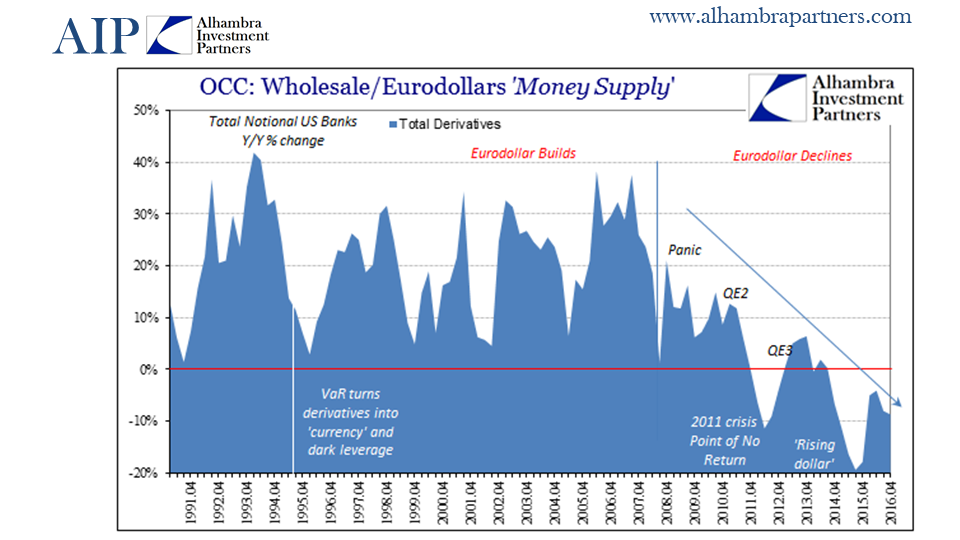

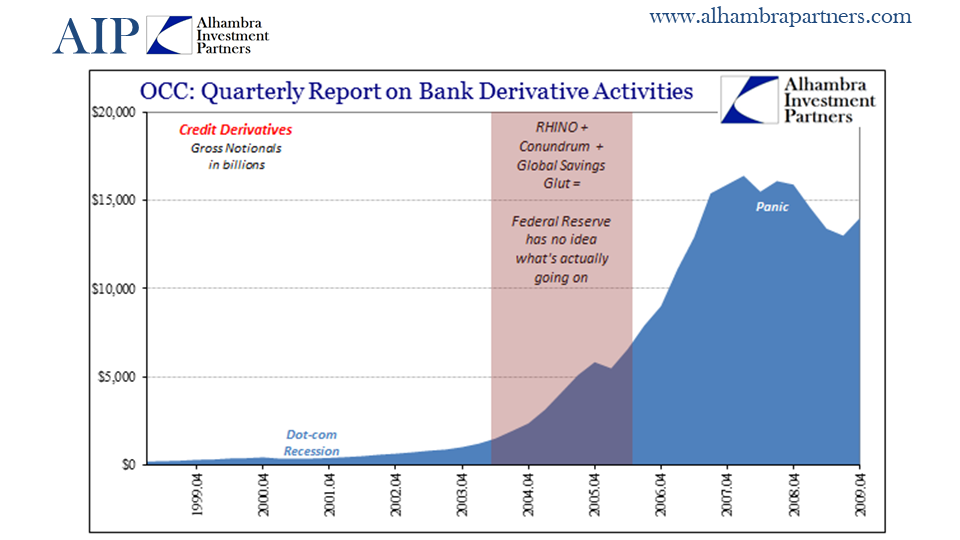

FRA: And the next two slides, if you can provide some elaboration from the office of the controller currency, getting into derivatives and how value at risk turns derivatives into ‘currency’ and dark leverage?

SNIDER: These are the other balance sheet factors that have, at various points in time, acted very much like money themselves. They’re very currency-like at times, especially the thing about interest rate swaps and credit default swaps. Credit default swaps, people probably remember from AIG, and the relation to subprime mortgages, but in fact the use of our credit default swaps was primarily related to balance sheet capital efficiency. In fact, most of the credit default swaps were primarily for primarily European banks to expand their balance sheet without having to raise additional cash. So what these derivative balance sheet factors tell us is, in general terms, bank behaviors. Whether they’re expanding, not necessarily how they’re expanding but how quickly they want to expand, and from that we can infer the global monetary system as it actually was, was expanding. Credit default swaps in particular, you look at during the period where Alan Greenspan was raising rates in the mid-2000s, the credit default swap market or at least the total gross notional written standing paid absolutely no attention to the Federal Reserve whatsoever. In fact, they increased geometrically throughout that period and into the period after it until the panic period started in 2007. So the banks that were off in this other shadow world were expanding rapidly all throughout the 1980s and 1990s and early 2000s. So we have to consider, was that this so-called good luck impetus that allowed the so-called Great Moderation to develop? Was it instead how banking was evolving and growing during that period rather than Alan Greenspan and his 25 basis point rate cuts and rate hikes in the Federal Funds Rate, which was in many ways an irrelevant marker.

FRA: What happened in 2016 from the financial crisis that caused the Federal Reserve to quietly surrender, as you quote?

SNIDER: Well, the fact that the economy never recovered, to put it bluntly and blatantly, despite all expectation. To be fair, Federal Reserve officials like Ben Bernanke from the very start said that the recovery would be long sell. And he did so because they expected the banking irregularities and the bank panic and all of that would act as a drag on recovery rather than be a rapid event like there had been in typical recessions. They fully expected that it would be drawn out a little bit longer than maybe people were comfortable with. That, in the end, it would be a full recovery. Yet time and again we find that it wasn’t ever a recovery. Every time the economy was supposed to kick into high gear, something even close to recovery, it just never did. By 2016, the Fed was forced to admit defeat. They had tried four different QEs that had no success. It didn’t create the inflation they thought it would, and therefore there was no inflation and no wage gain and no recovery, so they had to admit what most other people had finally figured out many years before, that there was never going to be a recovery.

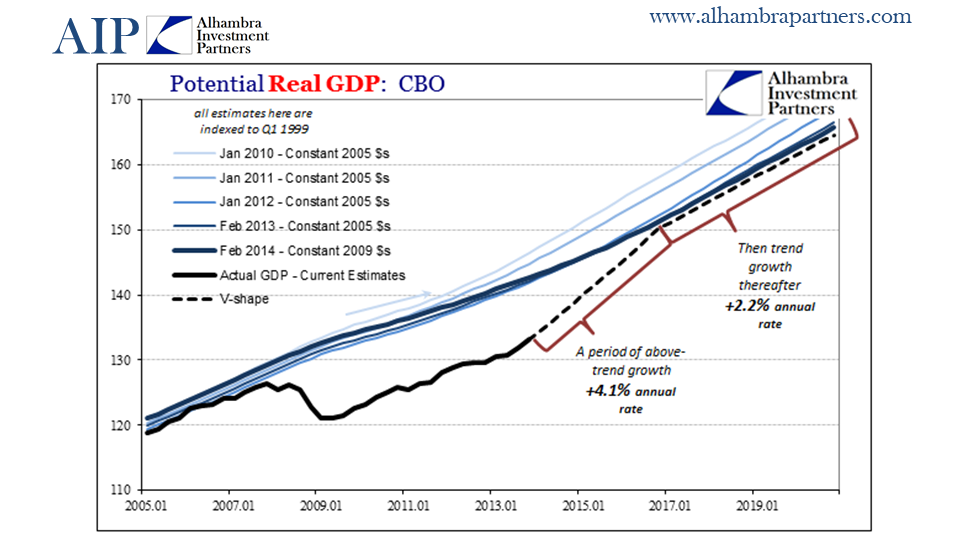

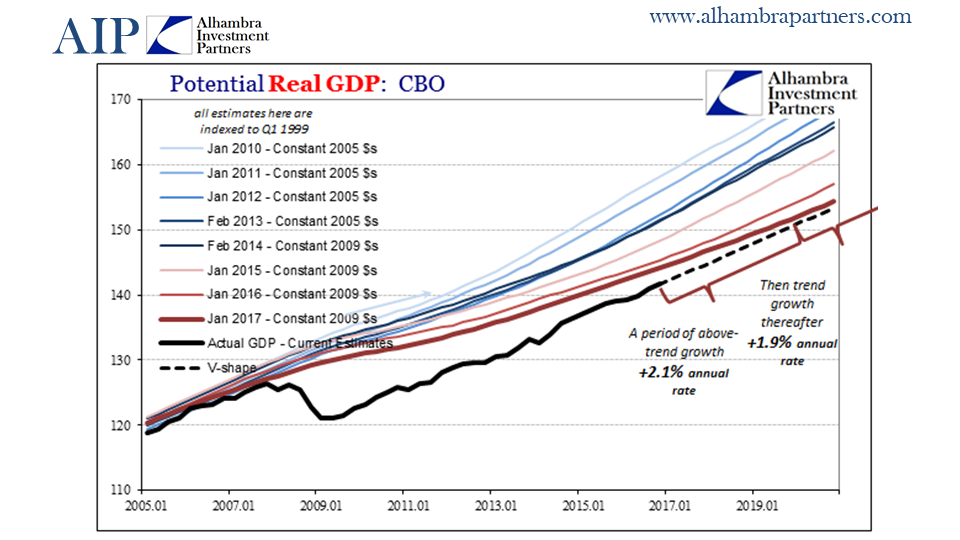

FRA: The next few slides illustrate how the Fed was in fact destroying potential rather than initiating recovery.

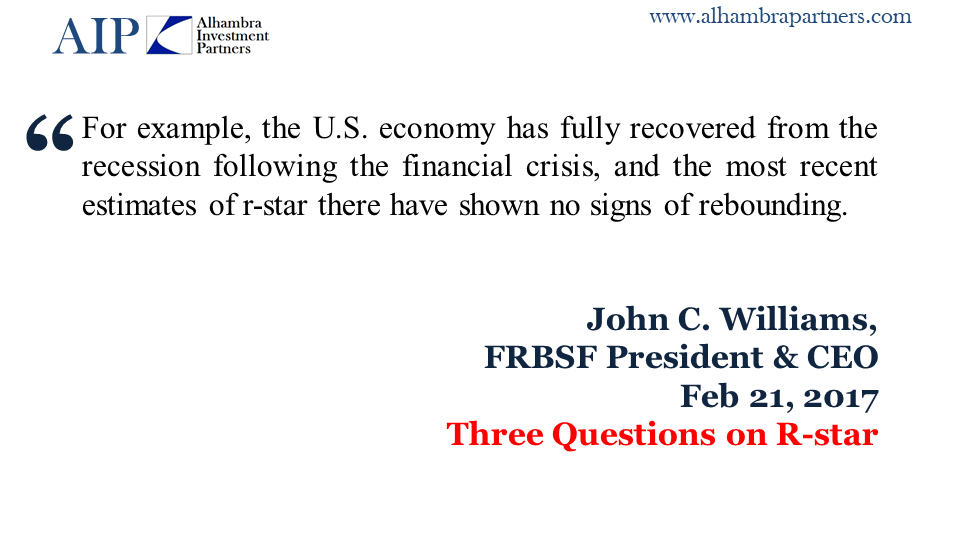

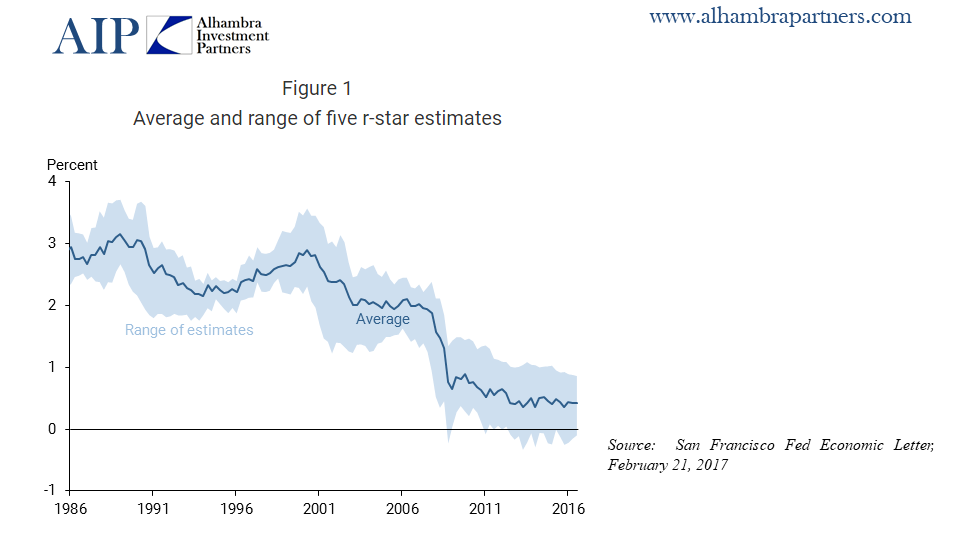

SNIDER: I don’t know if I would say the Fed was destroying potential so much as they were calculating the destroyed potential as a consequence of what they still think of as unknown. One of the primary ways that they arrive at that conclusion is what’s called R* or the natural rate of interest. The natural rate of interest is something that a Swedish economist had developed in the late 19th century, but lay dormant until the late 1990s when academics at Princeton and other place resurrected it. The natural rate of interest is supposed to be useful to monetary policy because it supposedly tells us where employment and inflation balances. In other words, what is the rate on money that won’t either spin the economy off into overheating or depress it too much into a depression. It’s not something that’s directly observed, so it has to be calculated through various mediums; there’s no actual agreement on what R* is. But what economists and policy makers have come to realize is that their calculation of R* since the panic in 2008 has basically arrived at that conclusion: that there basically is no recovery. And furthermore, there isn’t one coming. When you get to that point in terms of monetary policy, what that means is that there’s nothing left for you to do.

The FOMC discusses things like the output gap because that is supposed to tell them where they are in relation to this R* rate where risks of inflation and deflation are perfectly balanced, where unemployment can be the lowest without risking inflation overheating. What you find is that as the so called recovery developed, time and again they expected to get this burst of recovery-like growth to occur. When it didn’t happen, they’re forced to mark down their estimate of potential GDP and potential output to match the fact that it never happened. Over time, year after year, the level of potential just sank and sank and sank so that by 2016 there was very little distance left between potential and where GDP actually was. To the Federal Reserve policy makers, what that said was there was no output gap, or very little left. And if there was very little output gap left, there’s absolutely nothing for monetary policy left to do. At a situation where output and the level of potential are the same or nearly the same, stimulus is a waste of time.

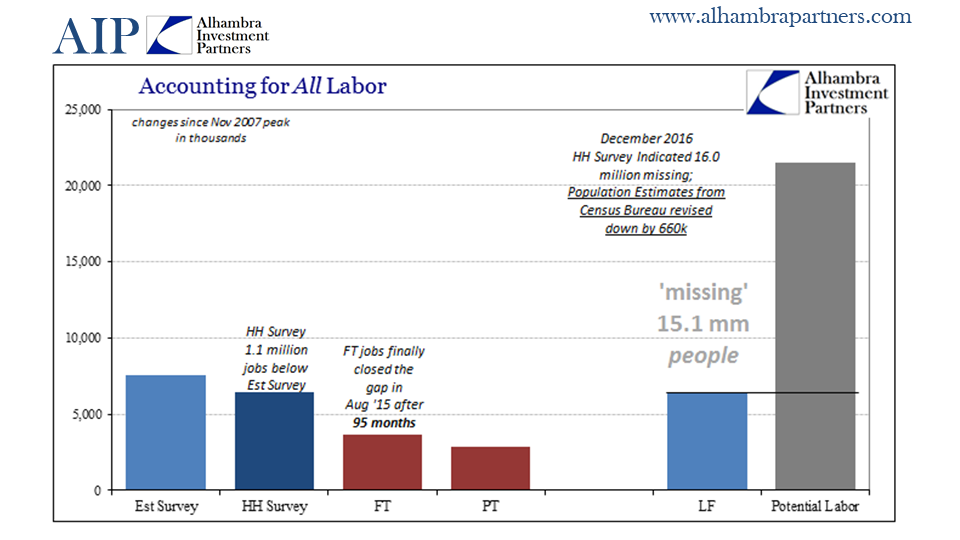

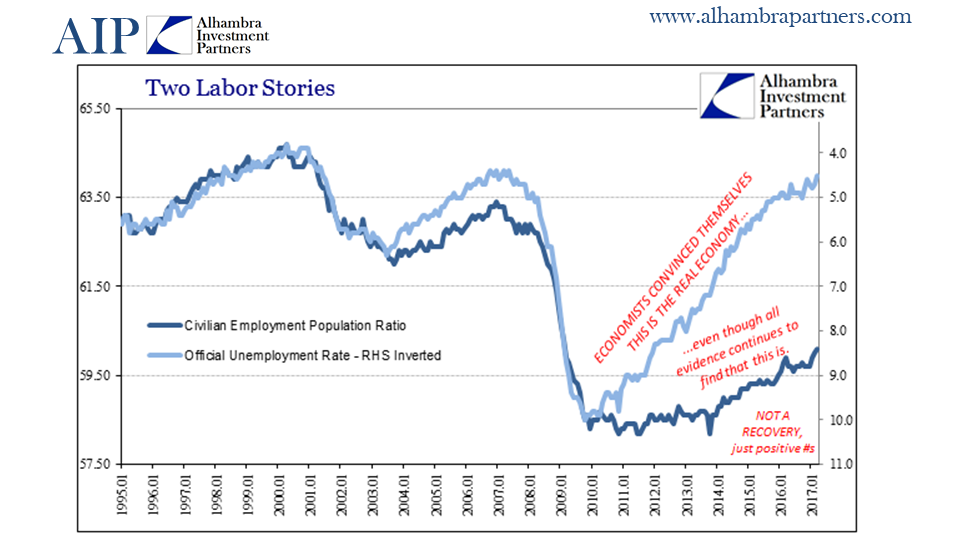

FRA: If we look at labor, one of your charts there, what happened to cause a divergence from 2010 up to today in terms of two labour stories?

SNIDER: That gets back to, essentially, the mystery of where did the recovery go? For monetary policy makers, this is a global phenomenon, not just a US one. Specifically with the US, the participation problem is that for whatever reasons, a huge chunk of the potential labour force has never re-entered the labor market. They have either never entered during the recovery period, or those that were out of work in 2008 never went back. The size of that pool of missing labor is immense, perhaps 15 million or more.