Interviews

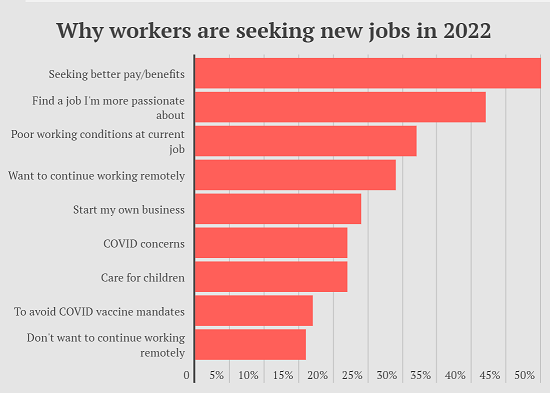

01/26/2022 - The Roundtable Insight – Charles Hugh Smith on Why Many are Resigning From Their Jobs

01/26/2022 - The Roundtable Insight – Charles Hugh Smith on Why Many are Resigning From Their Jobs

01/13/2022 - The Roundtable Insight: Bernard Connolly and Yra Harris on Europe and Risks to the Global Economy and Financial System

01/05/2022 - The Roundtable Insight – Doug Casey on the Economy, the Financial Markets, Migration and Freedom

12/14/2021 - The Roundtable Insight – Michael Pettis and Yra Harris on China

12/10/2021 - The Roundtable Insight – Charles Hugh Smith on a Grand Strategy to address the Global Crisis

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

12/07/2021 - The Roundtable Insight – Shehzad Qazi on What the Data on China is Indicating

See also this related article – Link Here, based on the data from the China Beige Book:

“A paradigm shift has taken place in how Beijing approaches its economic priorities and management. Many China watchers have missed it because they are relying on a series of misperceptions and flawed forecasts based on China’s old growth playbook ..

With the Beijing Olympics in early 2022 and the critical 20th Party Congress following next fall, Beijing will almost certainly find it useful at some point to ease monetary conditions. But these will be political considerations based on a political calendar. For now, stimulus is less urgent, and medium-term growth will be far more subdued, than the Wall Street consensus is expecting. “

11/23/2021 - The Roundtable Insight – Jim Bianco and Yra Harris on the Economy and the Financial Markets – LIVE recording

11/16/2021 - The Roundtable Insight – Kevin Duffy and Yra Harris on Key Investment Themes

11/09/2021 - The Roundtable Insight – Judd Hirschberg on Technical Analysis of the Financial Markets

10/26/2021 - The Roundtable Insight – Peter Boockvar and Yra Harris on Inflation, Currencies, Interest Rates and Commodities

10/19/2021 - The Roundtable Insight: Democracy, Economics and Entrepreneurship in the Future of Spain and Latin America

10/13/2021 - The Roundtable Insight – Prof. Barry Eichengreen and Yra Harris on Debt, the Dollar and Inflation

10/11/2021 - The Roundtable Insight – The Future of Argentina, Spain, Latin America and Europe (in Spanish)

Podcast in YouTube and MP3 Download – See Below:

10/08/2021 - The Roundtable Insight – Charles Hugh Smith on the Failure of the Federal Reserve and Rising Secular Inflation

09/07/2021 - The Roundtable Insight – Sustainability in Sports

08/26/2021 - The Roundtable Insight – Harley Bassman, Brian Pellegrini and Yra Harris on the Economy and the Financial Markets

podcast to be posted shortly ..