Link here to the MP3 Voice Podcast

07/16/2026 - The Roundtable Insight – Charles Hugh Smith on the Risks, Costs and Uses of AI

07/16/2026 - The Roundtable Insight – Charles Hugh Smith on the Risks, Costs and Uses of AI

Link here to the MP3 Voice Podcast

05/01/2026 - The Roundtable Insight – Charles Hugh Smith on what it will take to become BullishDownload the Podcast in MP3 for Voice Only

03/11/2026 - The Roundtable Insight – Charles Hugh Smith on the Current Waves and Cycles – Energy, Commodities, InflationDownload the podcast in voice mp3 format link here

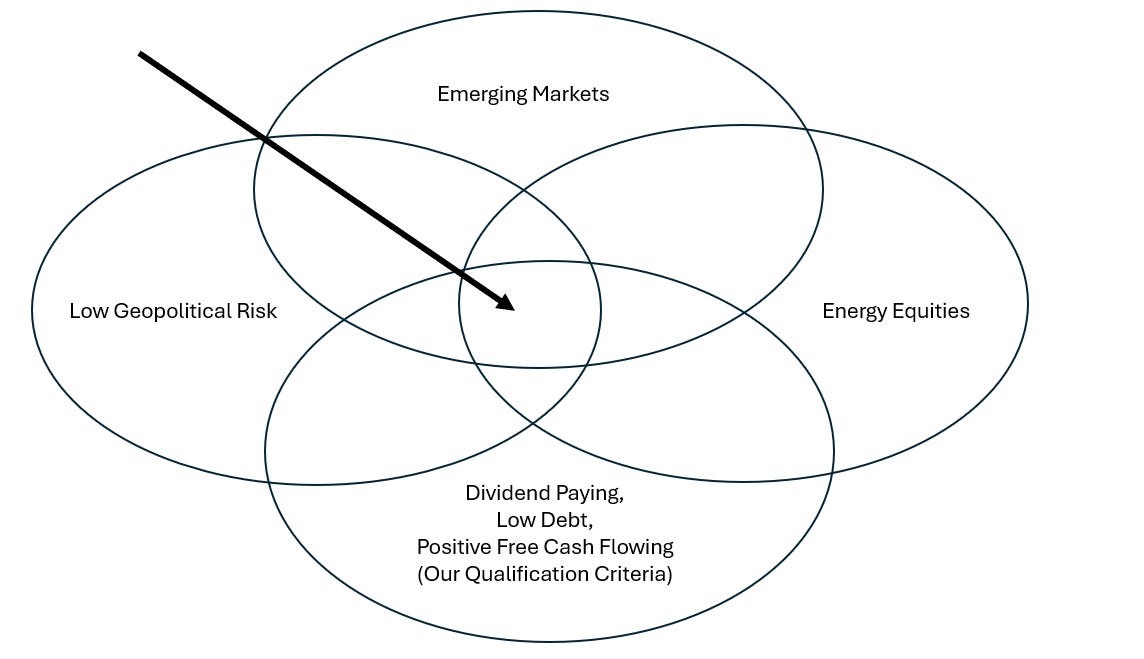

to view the venn diagram discussed in the podcast, cedarowl.substack.com – link here:

03/09/2026 - The Roundtable Insight – Trader Ferg on Emerging Market and Dividend-paying OpportunitiesDownload the Podcast in MP3

Substack Link => cedarowl.substack.com

02/19/2026 - The Roundtable Insight: Dr. Marc Faber & Yra Harris on Precious Metals & Where the Financial Markets are HeadingDownload the Podcast in MP3 Format

02/12/2026 - The Roundtable Insight – Louis-Vincent Gave & Yra Harris on Opportunities in Emerging Markets and Asian Currencies

01/13/2026 - The Roundtable Insight – Daniel Lacalle and Yra Harris on Gold and the Intensifying Sovereign Debt CrisisDownload the podcast in MP3 voice here

12/18/2025 - The Roundtable Insight – Charles Hugh Smith on Insane Financial Imbalances and a Social RevolutionDownload the Podcast in MP3 Voice

12/12/2025 - The Roundtable Insight – Peter Boockvar & Yra Harris on the Trends in Yields, Currencies and Investment Ideas

12/03/2025 - The Roundtable Insight – Luke Gromen & Yra Harris on Escalating Liquidity, Debt and Market RisksDownload the Podcast in MP3 Here

11/14/2025 - The Roundtable Insight – Fed Guy Joseph Wang and Yra Harris on the Trends in Liquidity, Repo Markets and Stimulus

11/05/2025 - The Roundtable Insight – Clive Thompson & Yra Harris on Gold and Value Investing Ideas, with Charts from Judd Hirschberg

10/28/2025 - The Roundtable Insight – David Woo and Yra Harris

10/09/2025 - The Roundtable Insight – Judd Hirschberg on Gold, Silver, Platinum and the Financial MarketsPodcast to be posted shortly ..

09/12/2025 - The Roundtable Insight – Rudy Havenstein & Yra Harris on Gold, Inflation and Financial Repression

08/26/2025 - The Roundtable Insight – Charles Hugh Smith on AI – the Hype, the Great Positives and the Dystopian Negatives

07/25/2025 - The Roundtable Insight – Rob Arnott & Yra Harris on the Long-Term Trends in the Markets

07/09/2025 - The Roundtable Insight – Kevin Duffy and Yra Harris on Tariffs, Debt, and “Following the Puck” to Investment Themespodcast to be posted shortly

07/08/2025 - The Roundtable Insight – Charles Hugh Smith on the Challenges of Debt, Currency, Interest Rates and Productivity in the G7 Worldpodcast to be posted shortly …

07/02/2025 - The Roundtable Insight – George Magnus and Yra Harris on Trends in Trade, Tariffs, USD Reserve Status and the Global EconomyDownload the Podcast in MP3 voice only

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority