11/04/2014 - STRANGE THINGS ARE HAPPENING IN THE BOND MARKET!

11/04/2014 - STRANGE THINGS ARE HAPPENING IN THE BOND MARKET!

“There is a very simple lesson that when the markets finally break through the manipulation they move to price in deflation and not inflation. This is key because it means financial repression has failed.”Analyst Russell Napier

The Economist’s Buttonwood column described it as:

“Letting go of Daddy’s hand,” and cautioned, “[W]e may indeed get to see QE4 rolled out. Daddy might have let go of the market’s hand for the moment but he’s still close by.”

“That coinage nicely speaks to the juvenilisation to which markets have been reduced during six long years of:

-

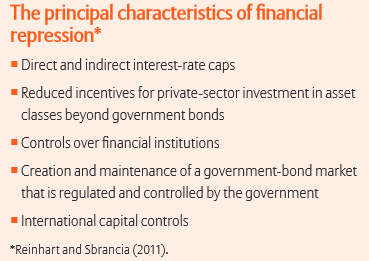

Financial Repression,

-

Interest Rate Manipulation, and

-

The Unprecedented Expansion of central bank balance sheets.

Only the asset purchases have abated (for now): the Financial Repression, one way or another, will go on. Whether the asset purchases have really disappeared or merely been suspended will be a function of how risk markets behave over the coming months and years.

And

“Although our crystal ball is no more polished than anyone else’s, we would not be surprised to see petulant markets rewarded with yet more infusions of sweets. Our fundamental views are clear:

- Bonds are already grotesquely expensive, yet may become even more (we’re not investing in “the usual suspects” so we don’t much care).

- Most stock markets are pricey – but in a world beset by QE (and prospects for more, in Europe and Asia) which prices can we really trust ?“

LINK HERE to the source article

Hong Kong-based Fung Global Institute essay gives tribute to Ronald McKinnon who died earlier this month & who is author of the 1973 bookMoney and Capital in Economic Development .. a treatise on how governments that engage in financial repression hamper financial development .. they highlight how McKinnon was working on a related concept – a dollar-renminbi standard which was being designed to help alleviate the financial repression & fragmentation undermining global financial stability & growth .. “The notion that the dollar’s global dominance is contributing to financial repression represents a significant historical shift .. Speculative inflows of ‘hot’ money have weakened China’s macroeconomic tools and fueled ever more financial repression .. The world needs its two largest economies to work together to bolster global monetary stability. Together, China and the U.S. can alleviate financial repression, avert protectionist tendencies, and help maintain a strong foundation for global stability .. It is time for U.S. leaders to recognize that what former French Finance Minister Valéry Giscard d’Estaing called the ‘exorbitant privilege’ that the dollar’s global dominance affords America also entails considerable responsibility. Global monetary stability is, after all, a public good.”

Hong Kong-based Fung Global Institute essay gives tribute to Ronald McKinnon who died earlier this month & who is author of the 1973 bookMoney and Capital in Economic Development .. a treatise on how governments that engage in financial repression hamper financial development .. they highlight how McKinnon was working on a related concept – a dollar-renminbi standard which was being designed to help alleviate the financial repression & fragmentation undermining global financial stability & growth .. “The notion that the dollar’s global dominance is contributing to financial repression represents a significant historical shift .. Speculative inflows of ‘hot’ money have weakened China’s macroeconomic tools and fueled ever more financial repression .. The world needs its two largest economies to work together to bolster global monetary stability. Together, China and the U.S. can alleviate financial repression, avert protectionist tendencies, and help maintain a strong foundation for global stability .. It is time for U.S. leaders to recognize that what former French Finance Minister Valéry Giscard d’Estaing called the ‘exorbitant privilege’ that the dollar’s global dominance affords America also entails considerable responsibility. Global monetary stability is, after all, a public good.”

Scotiabank’s Guy Haselmann thinks asset prices must adjust downward to meet new economic expectations for lower growth & inflation .. the problem is this recalibration is occurring quickly in an asset environment characterized by low liquidity – it is like the financial markets will overshoot to the downside .. “the process has just begun .. the unwind process has far to go” .. on quantitative easing & very low interest rates:

Scotiabank’s Guy Haselmann thinks asset prices must adjust downward to meet new economic expectations for lower growth & inflation .. the problem is this recalibration is occurring quickly in an asset environment characterized by low liquidity – it is like the financial markets will overshoot to the downside .. “the process has just begun .. the unwind process has far to go” .. on quantitative easing & very low interest rates: