09/11/2015 - David Berson – The Fed’s Plan for Interest Rates

09/11/2015 - David Berson – The Fed’s Plan for Interest Rates

Special Guest: David Berson – Senior Vice President & Chief Economist, Nationwide Mutual

David Berson is the senior vice president of Nationwide Mutual. Before now, he has worked as a College professor, at the Fed and for 20 years he was the chief economist at Sallie Mae. He has also worked at Nationwide Mutual insurance for the past three and a half years.

To David depending on where you are in the financial system financial repression will mean different things to you. According to him,

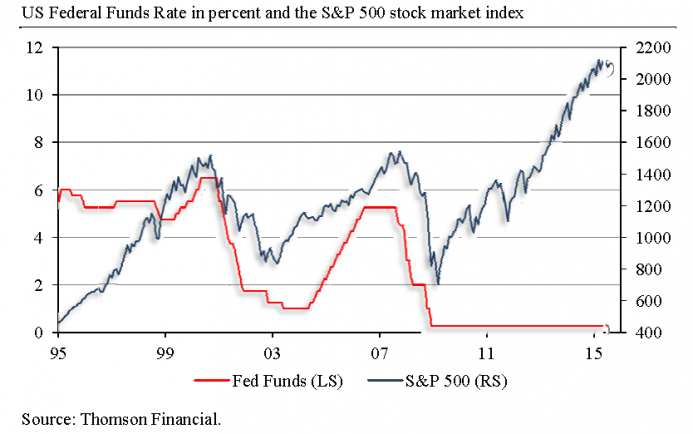

“Financial repression is holding interest rates below the level where they would naturally go.”

He explains that there are two sides to holding down the interest rate, a positive and a negative side. The positive with reducing the interest rate and applying quantitative easing include the addition of liquidity to the economy. According to him, most of the models used by macroeconomists indicate that monetary expansion helps the economy a bit at first but only a period of time. David says the expansion policy helped boost the economy out of recession and is responsible for the modest growth we see now. But the downside to it all is that keeping rates lower than it should naturally be results in savers being hurt due to the extremely low interest rates. At the same time borrowers are at an advantage. It also makes it difficult for investors to have a reasonable return. David agrees that low interest rates push investors to riskier assets but also insists that it is one of the points of having an expansionary monetary policy. He further reiterates that the upside to the artificial reduction in rates is the increased liquidity, which moves the economy a bit upwards.

“They need to concentrate on what’s happening in the domestic economy, they are the US central bank, they are not the central bank of emerging market countries even if those countries are greatly affected by what we do”

According to David, what’s happening in terms of the fall in commodity prices is not directly as a result of what the Fed does. He believes it is as a direct result of the rapid growth in china’s economy as they move to become an industrialized economy. He explains that the primary force driving the fall of commodity prices is the slowing down of the Chinese economy that is occurring now.

On what the Fed will do, David thinks the Fed will tighten this September although he also mentions that with the recent market volatility, the chances of that happening is less than 50%. He believes the Fed should tighten this September as he believes that such an action will help the economy.

On the disappointing recovery of the economy, David explains that there is an excess of government oversight on the economy, which has further contributed to the slowing down of the economy. If you look at what he calls the core GDP, which includes private sales and private purchases minus volatile inventory, trade and government, he is convinced that growth has picked up better than the overall GDP suggests and much closer to historical averages.

“One of the reasons why economic growth has been weaker in this expansion than others is a lack of government spending now I think that in the short-term negative in the long run I think a move in resources from the government sector to the private sector is positive but it takes a while for that to manifest itself in stronger overall GDP growth”.

Check out his interview with Gordon T Long which covers this and much more.

Abstract written by Chukwuma Uwaga – chuwaga@gmail.com