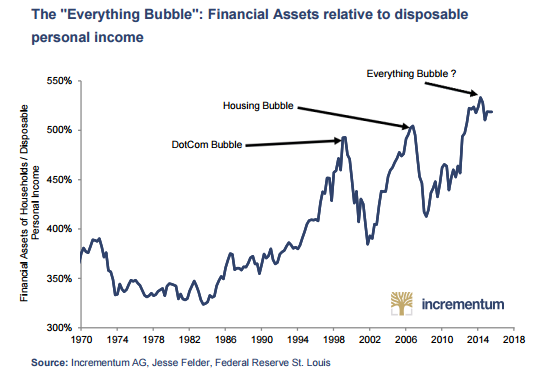

06/05/2017 - “Everything Bubble Chart” From Incrementum’s New Report

06/05/2017 - “Everything Bubble Chart” From Incrementum’s New Report

06/05/2017 - Gordon T Long: Global Central Banks Won’t Ever Decrease Balance Sheets?

Jason Burack of Wall St for Main St interviews Gordon T Long .. discussion on if Janet Yellen and the Federal Reserve can continue to raise interest rates? .. Gordon says that the Fed could possibly do 2 more 25 basis point interest rate increases in the near future before something in the real economy or markets breaks, but that the Federal Reserve and other major global central banks cannot ever reduce their balance sheets without collapsing markets and the real economy .. Gordon highlights how the ECB now has a balance sheet over $4 trillion and so does Japan’s central bank, the Bank of Japan. Balance sheets for the PBOC and Bank of England are also massive .. Gordon thinks the Federal Reserve will have to start rapidly expanding its balance sheet in the near future rather than reducing their balance sheet .. Gordon also discusses shorting opportunities he is positioning his clients for.

06/05/2017 - Hot Off The Press – Incrementum’s In Gold We Trust Report Incrementum is out with their latest annual “In Gold we Trust” report. As always, they try to deliver a holistic analysis of gold and financial markets in general, of course from a very Austrian perspective ..

Key topics and takeaways of the report:

• High expectations of Trump’s growth policy dampened the gold price increase in 2016 – Still up 8.5% in 2016 and 10.2% since Jan. 2017

• The further development of the normalization of monetary policy in the US will be the litmus test for the US economy.

• Bitcoin: Digital gold or fool’s gold?

• White, Gray and Black Swans and their consequences for the gold price

• Exclusive Interview with Dr. Judy Shelton (Economic advisor to Donald Trump) about a possible remonetisation of gold

• 5 Reasons why the gold bull market will continue

06/04/2017 - Central Banks Now Own A Third Of The Entire $54 Trillion Global Bond Market

“While the point is critical, what we would like to highlight in the chart below is the staggering amount of debt instruments owned by central banks: as of the latest data, central banks own just over a third of the global tradable bond universe of $54 trillion, or roughly $18 trillion. How this amount of debt on bank balance sheets is ever unwound, i.e. sold – even with central banks’ best intentions – without crashing the bond market, we don’t know.”

06/04/2017 - Peak Prosperity’s Adam Taggart On Financial Repression: The Currency End-Game Of Too Much Debt

“The Federal Reserve .. has chosen to sacrifice the many — the savers and those dependent on a fixed income — to benefit an elite few. Rock-bottom interest rates are greatly helpful to the banks, as well as the financial assets that the bankers and their wealthy clients own .. And just to add to the outrage factor here, when your local TBTF bank stores its own money at the Fed, the Fed pays it a full 1% in interest — nearly 20 times what your bank is paying you. Your bank simply pockets the rest as pure risk-free profit .. The data clearly shows that this suppression of interest rates, combined with the central banking cartel’s Herculean efforts to flood the world with liquidity (to the tune of $1 trillion so far in 2017), accrues benefits in a grossly lopsided and unfair manner to those at the top of the wealth pyramid .. This is a situation societies have found themselves in before. In fact, it has happened so often throughout history that there’s actually a playbook (for the government) when you get to this stage. It’s called financial repression .. While financial repression extends the lifetime of an over-indebted economic system, it does not avoid the consequences of Too Much Debt. It merely serves to shift the worst of the inevitable losses from the government onto the public.

As von Mises’ guarantees:

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion, or later as a final or total catastrophe of the currency system involved.

~ Ludwig von Mises

Negative interest rates are a milestone down the slippery slope of the latter: currency destruction. The central banks are intentionally devaluing their currencies, but betting that they can do so at a controlled pace.

But as von Mises warns and as history has shown again and again, currency regimes burdened by too much debt eventually reach a critical failure point where a uncontrollable cascading collapse becomes inevitable.”

06/04/2017 - The Roundtable Insight: Jayant Bhandari On The Economic Effects Of Going CashlessFRA: Hi, welcome to FRA’s roundtable insight today we have Jayant Bhandari. Jayant is a specialist in the natural resources sector, he travels the world looking for investment opportunities in this sector. He advises institutional investors about his findings and he worked for 6 years with U.S. Global Investors, a boutique natural resource investment firm, and also for one year with Casey Research. Welcome, Jayant.

Jayant Bhandari: Thanks very much for having me, Richard.

FRA: Great, so I thought we’d start with an update on the situation in India, as you know we’re trying to keep an eye on this as what’s happening there could affect other locations or could evolve in a similar way in terms of what’s happening to physical cash and the currency there. Any updates from your end?

Jayant Bhandari: Sure, though Richard, as I have talked with you in the past, on the 8th of November 2016 Indian Prime Minister demonetized 86% of monetary value of cash in circulation. The result was that the economy started to stagnate, this was my experience and this has been my experience in the last 6-7 months. The World Bank, the IMF, and the Indian government continued to claim that Indian economy was actually starting to do better. Now, yesterday they came out with new numbers and they now accept that the economy is starting to show signs of the stagnation. Instead of the economy growing at 7.5% according to them, it is now growing at only 6.1%, again according to them. In my view, the growth is negative not even positive. I see, as I have repeatedly said on your show, India is actually becoming a police state. And this police state is going to be a horribly chaotic place because Indians are very chaotic people. Trying to propose a totalitarian system on this country will lead to a disaster in India.

FRA: And you see the Totalitarian approach as being indicative from the developments on physical cash, is that directly related to that? And in turn is that what is causing the slowdown in the economy?

Jayant Bhandari: Well, that is one part of the story in a country where 95% of consumer transactions are cash based transactions. You cannot really impose internet and banking on these people, this led to a massive slowdown in the economy. Now Richard, one funny example I want to tell you about and that will give you a glimpse of what is actually happening; I bought a New Delhi to London plane ticket two months back, I paid for it using my debit card, not my credit card because I refuse to have a credit card in India. The money left my bank account, I got no ticket. And no one knows where my money is today two months after the event.

FRA: Wow.

Jayant Bhandari: Now in a society like this, you can’t really impose digitalization and banking because Indians are not capable of, and it’s totally not structured for high-tech movement of cash, they have to have physical cash to do transactions, physical cash invariably will come back into existence. But in the meantime, Indian government will have destroyed the economy, lives of hundreds of millions of people, old people are going hungry in my opinion because food prices continue to be half as much priced as they should be.

FRA: So what are the trends at this point or recently in the areas of the inflation-deflation situation in terms of inflation on food prices or consumer prices in general? And also the trend in the currency strength or value as well, like what is it relative say to the U.S. dollar, any trend you are seeing there?

Jayant Bhandari: Sure, so what has been happening with inflation is that this has because of demonetization it has created a deflationary environment. People are simply not buying anything. Now, deflation is a good thing as long as it happens because of excess supply. The reality with India is that deflation is happening because of significant reduction in demand. People are simply not buying anything that they don’t need right now. But that also includes food now, so this deflation is a horrible deflation which is destroying businesses and the economy. And I keep meeting the small businesses who tell me that they are shutting down, not just because of the cash crunch, which is a major part of course, but regulations have increased, the rapaciousness the corruption of the bureaucrats has increased very significantly. Now the other side of this story is the Indian stock market is booming and Indian currency has gained a lot of value in the few months. Now firstly talking about the stock market, the stock market is not necessarily correlated with the growth of the economy which a lot of people erroneously believe. Now the thing with the stock market is that people’s cash is stuck with the bank, so they have really no option but to buy stock. At the same time there is an increased bullishness about India in the Western countries which is completely wrong, these people will eventually lose a lot of their money but because they have continued to send more money into India, Indian currency has improved and the Indian stock market has improved but as I said, Indian economy is stagnating and in my view, passing through a negative growth rate right now.

FRA: And what about inflation? Do you see consumer price inflation happening? Any trends there?

Jayant Bhandari: Well it will eventually happen because once they have destroyed the economy, once businesses are shut down, the supply won’t be there anymore. So inflation has to happen, and also the cost structure of creating everything has gone up because of the rapaciousness of the government, the bureaucracy and the regulation and the enforcement of digitalized cash on people. Which people are incompetent to use if at all the system works which has increased to cost of doing business, eventually it will lead to huge inflation in my view, but for the moment its deflation but this is only in the transitionary time, and that is mostly because the mint has been destroyed, it’s a horrible sign for the future of the economy in my view.

FRA I see, and what about elsewhere in Asia? Any trends there in terms of an economic slowdown or inflation-deflation, other parts of Asia?

Jayant Bhandari: I see the same thing in the rest of the Asian countries; Sri Lanka, Thailand, Myanmar Pakistan, Bangladesh, Nepal, they are all starting to stagnate, the East is blowing up. So I think that the economic future of these countries is not good at all, the only place where I see optimism and actual growth happening that’s in China, Korea, Singapore, and Hong Kong.

FRA: In what areas is that growth happening?

Jayant Bhandari: In China I see growth happening everywhere, in the infrastructure the investment continues to exist. I think the cities the manufacturing continues to grow, consumption of commodities continue to grow in China. Now the reality is that the perception among resource investors is that China is slowing down and Chinese demand for these commodities is falling, which is actually not true. What is happening is Chinese consumption of commodities continues to grow, the problem is that we have increased supply more than the demand has increased in commodities, hence the destruction of pricing of commodities. But the Chinese continue to buy a lot of commodities, and maybe they have reduced the chasing of iron ore, but that’s only because recycled steel is now coming back to the market which means that iron ore needs might have fallen off a bit, but that is not a result of a fall in economic growth, it’s just a result of increased recycling.

FRA: From that perspective, what opportunities are you seeing in the natural resources sector, are there opportunities in Asia or elsewhere in the world?

Jayant Bhandari: Again, China is still heading growth around the world in my view. And in both cases, in the case of precious metals and in terms of commodities. Commodities because they continue to grow, China is putting into place this one road, one belt road. Which is the Chinese attempt to link countries in Asia and Africa economically which I think will be a great thing for these countries because China is the only country in my view which has the capability for leadership among the third world. So commodity consumption I think will continue, I just hope natural resource investors do not pump up the supply more than the demand goes up. At the same time, in my view precious metals consumption will continue to grow in China, not actually because of volatility partially because of increased political risk, but mostly because the Chinese need to diversify. These people are diversifying their world for the very first time really. I mean, China was a completely closed economy 30 years back, it’s only in the last 10-15 years the Chinese are internationalizing themselves. It’s not necessarily a bad sign in my view, neither is it a sign of their increased fear about China, but they are merely diversifying. If you and I become rich, we want to diversify.

FRA: And will this leadership by China still be maintained given their current challenges with lots of government and corporate based debt? You know the shadow banking system, the non-banking sector has a lot of non-performing loans, and then overall there’s a problem with the wealth management products in terms of a potential bubble there from sort of a Ponzi nature of WMP products. Any thoughts there? Like will China still be able to maintain their development on the Silk Road?

Jayant Bhandari: I think that China will continue to grow. And the reason is that the rest of the emerging markets are in much much worse shape. Look at what’s happening in Venezuela, Brazil, which actually comprises almost half of South America, more than half of South America probably. Yes, there are problems with China. There’s a shadow banking system, there’s a problem with corruption in China, there’s a problem with overcentralized politics of China. But really, China has continued to grow for the last 30 years and this must mean that overheating must have happened in parts of the economy and parts of the society and politics. Corrections will happen, but again it’s a centrally managed system. I don’t think they will have a major crisis anytime soon. They will be able to deal with some of these smaller issues, they do have to deal with too much credit given to state government-run companies, and all those kind of things. But I think China has the capabilities and the resources to deal with the short-term crisis. In the long term, certainly, but who has seen the long term? In the long term maybe there will be more problems.

FRA: And in terms of investment opportunities, which countries in Asia, Southeast Asia, East Asia do you see as offering opportunities in different areas?

Jayant Bhandari: I love China. I love China I invest in China, I invest in China via Hong Kong. Hong Kong is a great place, Singapore in my view continues to be a great place. Singapore and Hong Kong continue to be places where the wealth goes to for protection. I also like Australia and New Zealand, I think both these countries despite that they are very socialistic in their orientation, have done a lot of good work in their countries and their societies are relatively stable societies far from the problems of the world, problems of the western world, problems of Europe and huge problems of the emerging markets in my view.

FRA: And are the opportunities in areas of industrial commodities or agricultural commodities or other sectors of the economy?

Jayant Bhandari: In Australia and New Zealand, yes. Australia continues to grow big at providing a huge amount of commodities. Iron ore, coal, gold and the rest actually to China and the rest of the world. And these commodities have been extremely helpful to Australia in terms of the growth in their economy. They have also been able to attract a lot of wealthy, good investors and migrants into Australia where it might not have been the case with Europe. So yes, I think natural resources continue to be a big part of Australian economy today.

FRA: Moving to North America, we were talking just before our discussion began today on what’s happening politically and the ramifications of that on the economy. Can you bring us up to speed? What’s recently happened politically in British Columbia, Canada?

Jayant Bhandari: Sure, Richard. I’m currently in Vancouver and it’s very sad to see that as much as 17% of the votes in the recent provincial elections went to the green party. Now the vote green probably made the party very attractive to a lot of people, 17% which is a massive increase from less than 1% that they used to get in the past. And it is twice as many votes than what they got in the last elections. So there’s a huge shift towards the left in British Columbia from what I see. Now, the results will be that the next government will very likely be a leftist government, a combination of the Green party and NDP which is left to the center party. Now, these people have already promised in their election manifesto that they would want to kill Kingdom Morgan gas pipeline which is going to be a pipeline from British Columbia to Alberta. Now, this is supposed to be a $7.5 billion pipeline and they want to destroy construction of this pipeline despite that most of the permits have already been issued. They also want to destroy a hydroelectric project in British Columbia, they want to increase minimum wages to $15.00 per hour in British Columbia, and they want to impose massive taxes on foreign buys of properties in British Columbia. So far there’s a 15% tax on foreign buyers just in Vancouver, now they want to make it 30% and they want to impose it across the province. These are not good news in my view for the future of British Columbia.

FRA: Wow, 30%. In Ontario, the percentage has gone to 15 like they have there now. Is this having any effect on the Canadian housing market? Is there any indications it’s slowing down or prices are falling?

Jayant Bhandari: Well from what I have seen in the media, no the prices aren’t necessarily falling, they did stagnate for a while when they imposed the taxes, but from what I see, the prices continue to go up. So no, it hasn’t really made any real impact onto the housing market.

FRA: And coming back to our point on the movement to the left in British Columbia, do you see this as a trend overall in North America, a sort of backlash if you will against the recent elections in the U.S. with U.S. President Donald Trump, we are apolitical, we don’t take sides but just what are your thoughts on that? Do you see as we mentioned on other shows a potential for a movement to the far left in the sense of socialism perhaps led by the millennial generation?

Jayant Bhandari: I think that’s actually happening Richard. And it seems to me from whatever number I see that most of the leftist votes tend to come from relatively educated urban people. Richard such an irony because educated people should know better that socialism does not work and it is the free market that has given us all these nice things that we enjoy in our lives. But I guess urban environment and schooling system has a dyadic effect on people’s minds, it makes them simplistic in their thinking, they start to forget about second order consequences. And the problem is, when I wake up in Vancouver and when I switch on my light, they always switch on. And so life becomes so predictable in rich technologically advanced countries, particularly in urban centers, but people tend to become simplistic because they don’t really have to deal with chaos on a day to day basis. I don’t know how you can change that, but simplistic thinking also leads to leftists, because the promises of leftists are simplistic promises, and they look attractive to simplistic people.

FRA: And what would be the effects of this on the economy, economic development, and the financial markets in North America?

Jayant Bhandari: Well I am, Richard, optimistic about Trump, I think he’s trying to change a few things. I am increasingly pessimistic about Canada. We have to remember Canadian currency has fallen about 30%-35% or even more in the last four or five years. This has seriously hurt the Canadian economy I guess, now that of course has made Canada more attractive to foreigners, foreign tourists, foreign investments, and foreigners who want to buy housing in Canada. But despite just the short term gain for Canada economically, it might come at a huge cost in the future. Given that now we have leftist governments in many provinces, many important provinces like Alberta, British Columbia, and of course in the federal government with Justin Trudeau, who in my view has no understanding of economics or pretty much anything actually.

FRA: And what about just overall like in the U.S. North America? Do you see this as a trend and a negative effect on the economy, slowing it down?

Jayant Bhandari: I think so, yes. I think people in the western world are becoming increasingly leftist, and we also have to accept that most of the migrants who have come to the Western society tend to predominately vote for the left, the left in any governments, and they want to covert the Western governments into many governments. And that means that our politics is increasingly becoming leftist and you go to the government offices, government offices are over-represented, have a higher proportion of migrants working in government offices then the proportion of migrants in the society. So I think there’s a clear trend in the society in all of the west to become increasingly leftist, and this will have a harmful effect on our society going forward.

FRA: And how would the emerging pension prices, government in particular government pensions, especially in the U.S. initially before Canada, although it’s likely to affect Canada as well. Is this all going to be exacerbated by that in terms of these trends happening and an overall slowdown? There’s been some recent reports like the wealthy are now leaving Connecticut due to the pension crisis already, so do you see that happening?

Jayant Bhandari: Well from what I read it does not look like as if people are really going to have access to their pensions 10-15 years from now, and maybe much sooner than that. So, people who are hoping to benefit from their pensions in the future, it’s probably not going to happen. Particularly when unemployment is increasing hugely in the west, peoples need for welfare from the government is increasing. So government really does not have the resources to continue to give money to people when the tax revenues might actually start to fall at a certain point in time given mostly stagnant economies in the western society.

FRA: Great insight, wow that’s great as always Jayant, how can our listeners learn more about your work?

Jayant Bhandari: Richard, I have a website, www.jayantbhandari.com/ and everything I do is on that website.

FRA: Great, thank you very much once again, thank you Jayant.

Jayant Bhandari: Thanks very much for the opportunity Richard.

FRA: Yup, we’ll do it again, thank you, take care.

LINK HERE to download the MP3 Podcast

06/01/2017 - Danielle DiMartino Booth: The Demographic Divide: A Police State Of Mind

“It comes down to the demographic divide that’s opened up since President Ford was in office. In the 1970s, the typical public pension’s active employees outnumbered retirees by a factor of four-to-five times; today that ratio is 1.5-to-1 and continues to fall as Boomers retire in droves and Millennials fail to fill the yawning gap.

After a grisly year that ended with a tally of 4,000 homicides, Chicago has begun to coordinate with federal authorities to control a crime wave driven by gangs’ unencumbered access to firearms. The last thing the city can withstand is further cuts to public service funding. By the same token, taxpayers have already begun to vote with their feet as rising taxes and foundering pensions promise to beget more tax hikes to come.

It’s plain that the last thing any of us want to see is a Police State of any kind. But the growing risk is that the next recession and deflating asset prices could well alter the rules of engagement between federal and state authorities on more levels than any of us care to envision.”

06/01/2017 - Dr. Marc Faber: We Have A Bubble In Everything

“We have global debts as a percent of global GDP that is 30 to 40 percent higher than it was in 2007 .. All of us and I also own lots of assets, we’re going to lose 50 percent. Either the government will to take it through taxation or expropriation or there’ll be a deflation in asset prices that is surprising most people on the downside.”

05/31/2017 - Thorsten Polleit: The Fiat Money System Might Be Held Up For Longer Than Some May Fear And Others Might Hope

“The still very low long-term interest rates in the US may, therefore, tell us something important: Investors expect the Fed to keep rates at fairly low levels in what lays ahead; they expect the central bank to refrain from returning yields to levels formerly considered ‘normal.’ Against this backdrop, the latest series of rates increases is merely seen as a cosmetic adjustment .. The US economy, and with it the world economy, is caught between a rock and a hard place. Maybe the Fed’s current rate hiking spree will bring about the bust. Or the Fed refrains from raising rates further and keeps the boom going a little bit longer. Ludwig von Mises put the predicament as follows:

The boom cannot continue indefinitely. There are two alternatives. Either the banks continue the credit expansion without restriction and thus cause constantly mounting price increases and an ever-growing orgy of speculation, which, as in all other cases of unlimited inflation, ends in a “crack-up boom” and in a collapse of the money and credit system. Or the banks stop before this point is reached, voluntarily renounce further credit expansion and thus bring about the crisis. The depression follows in both instances.

Given current bond and stock market valuations, investors seem to be fairly confident that the Fed will succeed in keeping the boom going, that the central bank will not overdo it in terms of raising interest rates. And yes, perhaps central bankers have learned a great deal in recent years, having become true maestros in holding up the make believe world of fiat money. The investor should be aware of the damages caused by fiat money — for instance, boom and bust. At the same time, he should not run for the exit prematurely: The fiat money system might be held up for longer than some may fear and others might hope, so that keeping inflation-resistant assets may be more rewarding than betting on an imminent system crash.”

05/31/2017 - McAlvany Commentary: U.S. GDP Growth Is Matching The 1930s Depression Decade

This week’s show:

-Normally Understated Gold Expert Jeff Christian Now Sees $1,900+ Gold Price

-Russian Ruse Being Played Politically In The U.S. To Distract From Real Issues

-U.S. GDP Growth 1.33% (10 Year Average) – Identical Match To The 1930s Depression Decade

05/31/2017 - Jim Rickards: China’s Economy Fueled By Debt & Ponzi-based Investment Instruments

“China is in the greatest financial bubble in history. Yet, calling China a bubble does not do justice to the situation. This story has been touched on periodically over the last year .. China has multiple bubbles, and they’re all getting ready to burst .. The first and most obvious bubble is credit. The combined Chinese government and corporate debt-to-equity ratio is over 300-to-1 after hidden liabilities, such as provincial guarantees and shadow banking system liabilities, are taken into account .. Paying off that debt requires growth, but the growth itself is fueled by more debt. China is now at the point where enormous new debt is required to achieve only modest new growth. This is clearly non-sustainable .. The next bubble is in investment instruments called Wealth Management Products, or WMPs .. In the past ten years, bank customers have chosen almost $12 trillion of WMPs. That might be fine if WMPs were like high-quality corporate or municipal bonds. They’re not. They’re more like the biggest Ponzi scheme in history .. Here’s how they work. Proceeds from sales of WMPs are loaned to speculative real estate developers and unprofitable state owned enterprises (SOEs) at attractive yields in the form of notes .. So, WMPs resemble collateralized debt obligations, CDOs, the same product that sank Lehman Brothers in the panic of 2008 .. The problem is that the borrowers behind the WMPs can’t pay their debts. They’re relying on further bubbles in real estate or easy credit from the government to meet their interest obligations .. Finally, there is an infrastructure bubble .. About half of China’s investment in the past ten years has been wasted on ‘ghost cities,’ white elephant transportation facilities, and prestige projects that look good superficially, but that don’t produce enough revenue or efficiencies to pay for themselves .. Much of this investment was financed with debt. If the project itself is not revenue producing then the associated debt cannot be repaid, and will go into default .. The toxic combination of government debt, corporate debt, WMPs, and unrealistic growth expectations have set up China for the greatest market crash in history.”

05/31/2017 - Mauldin Economics Patrick Watson: How To Retire On 2% Returns

“We shouldn’t assume 7% real returns will continue .. keep your expectations conservative. Better to be surprised by a windfall than a shortfall .. Specifically, you can start by tempering your retirement lifestyle plans. That could mean pushing back your planned retirement age, living in a less expensive home, or renting out part of your house to lower expenses .. You could also save more aggressively for retirement, which might require reducing your current spending plans. You’ll be glad you did later .. Finally, reconsider your investment strategy .. You‘ll notice in the BCA forecast that they expect the highest future returns to come from emerging-market (EM) equities.”

05/30/2017 - Martin Armstrong: Wealth Migration Is Intensifying The Government Pension Crisis, Causing Wealth Migration To Intensify

“Municipal Bonds are in trouble in Europe as well as the United States. The local level cannot print money, nor are they ever capable of managing their economies. The general view is when short, just raise taxes. Everything comes to an end and we are looking at the end of a Muni-Bond Bubble. The strongest possible recommendation is get out before it is too late. Sure, not every municipality or state/province is in trouble – YET! Once the muni bond bubble bursts, there will be a contagion so even the ones that are not yet insolvent .. it is the government employee pensions that are blowing everything apart at the seams .. Hedge fund managers are permanently relocating to Florida have been leaving New Jersey and Connecticut. When you count on taxing the rich, then one man can move out of and put the entire state budget at risk. Taxing the rich has its limits .. The motto of make the rich pay doesn’t work when the rich pick up and leave. You do not want to be the one still sitting. This game works opposite of the musical chairs game as a kid. This time, the one still sitting will have to pay the taxes for everyone who left. Then they will be unable to sell their house and leave because nobody wants to buy it because of the taxes.”

05/30/2017 - Government Pensions Are Consuming State & Local Budgets

“Most state and local governments in the United States offer retirement benefits to their

employees in the form of guaranteed pensions. To fund these promises, the governments

contribute taxpayer money to public systems. Even under states’ own disclosures and

optimistic assumptions about future investment returns, assets in the pension systems will

be insufficient to pay for the pensions of current public employees and retirees.”

http://www.hoover.org/sites/default/files/research/docs/rauh_debtdeficits_36pp_final_digital_v2revised4-11.pdf

05/30/2017 - Dr. Lacy Hunt: Indebtedness Cannot Be Solved By Taking On More Debt

Erik Townsend Interviews Dr. Lacy Hunt

Dr. Lacy Hunt: Dr. Hunt explains, the US debt load will continue to climb and velocity will continue to slow – unless, of couse, “we get lucky.”

Hunt points to an excellent summary was published in 2010 by McKinsey Global Institute…

“They looked at 24 advanced economies that became extremely over-indebted. The indebtedness brought on a panic year, such as 1929, 1873, 2008, and they followed the process through to completion.

It’s a very long process, and what it shows is that an indebtedness problem cannot be solved by taking on additional debt.

McKinsey says specifically that multi-year sustained rise in the savings rate, what they term austerity, is needed to solve the problem, and of course, as we all know, in modern democracies, that option doesn’t seem to exist.

So, we try to continue to use what has failed, and while we get transitory improvement in economic activity, the longer-term trend is to weaker and weaker economic performance.”

05/28/2017 - Chris Martenson: Non-U.S. Banks Are Being Paid By The U.S. Central Bank

“The Fed is now paying interest on so-called ‘excess reserves’ held at the Fed. Those ‘excess reserves’ include a huge chunk of money held there by foreign banks who are only too happy to receive 1% on their holdings from the Fed given that their own central banks are paying 0%, or even negative rates. The money that the Fed pays these foreign banks is deducted from the amount remitted to the US Treasury at the end of each fiscal year. It’s this simple: foreign banks are being paid billions .. not one single person in the US got to vote for or approve of that action. Let me repeat that: billions and billions .. are being sent to boost the profits of foreign banks. And there’s not a single thing a voting citizen can do about it .. The decision to do this has been made unilaterally by unelected people for reasons they are under no obligation to either share or even have audited by the public. I wonder if Detroit wouldn’t mind getting several billion dollars to use however it wishes, courtesy of the Federal Reserve? Or the permaculture movement? Or jobs training programs?”

05/26/2017 - The Roundtable Insight – Yra Harris On Currencies – Central Banks Can Promote Crypto/Electronic Currencies To Help Implement Negative Interest RatesFRA is joined by Yra Harris to discuss the current state of currencies – crypto currencies, USD, Yen, and Euro.

Yra Harris is a recognized Trader with over 40 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through a combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has specific achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC.

Yra highly recommends reading The Rotten Heart of Europe – send an email to rottenheartofeurope@gmail.com to order

RECENT RUN-UP OF CRYPTO CURRENCIES

It seems to have caught on for people who are trading gold and treat it like a haven. It’s difficult to understand how the crypto currency market works and why we can be secure that it will hold value when it seems to just move around in huge gyrations. We saw the movement of when it had a fall of almost 50% a few months ago when it appeared that the guys from Facebook were behind the push for creating a Bitcoin ETF; when it looked like it wouldn’t get approved, the currency dropped significantly in value. In some way, central banks would love to go to a crypto currency or an electronic currency, because then they can control what people do with their money when they need to go to negative interest rates. There’s a lot to understand and learn here and too many uncertainties here. If you’re looking to secure your money, you should stick with precious metals.

The concept of crypto currencies in the form of Bitcoin and Ethereum don’t appear to be based on anything in terms of either a commodity like gold or precious metals or the faith and credit in a government, so it’s a bit of a wonder how it’s getting its value.

Governments don’t like competition. If the Chinese wanted to shut this down they could shut it down whenever they wanted; they still have tendencies toward repression. If there was a movement by governments to get into crypto currencies, then it would make more preferable sense to have some type of crypto currency that would be backed by a commodity, preferably gold, verses nothing like Bitcoin or Ethereum. Otherwise you would need to use a government-based crypto currency – which would be another form of fiat currency. In other words, it would be preferable to use a crypto currency based on a commodity instead, as long as that commodity-based crypto currency is still regulated by the financial system.

In a fiat currency dominated world, central banks have not acted in the best interests of holders of the currency – that has forced people to reconsider things. Shariah-compliant crypto gold is a potentially interesting movement.

RECENT CURRENCY SHIFTS

Yra offers his perspective on the US Dollar (USD) currency, offering his counterarguments relative to recent observations by Russell Napier who takes a bullish view on the USD:

Russell points out that Japan is running out of savings so there’s an insufficient private savings level to fund its government. The counterargument to insufficient savings rate is the fact that Japan traditionally has a tremendously high savings rate and phenomenal investment all around the world. They run current account surpluses not just because of trade balances, but from investment income. If their savings are drawn down, the Yen won’t collapse even though the underlying fundamentals are terrible in other ways. When the Japanese get nervous about the world, they bring money home, and they have huge amounts to bring home.

Russell also points out how China for a weaker Chinese currency (and relatively stronger USD) for export competitiveness. Yra points out that if the Chinese are going to move to a more domestic-based economy, it will not be in their interest to depreciate their currency. Will the currency go down because China has troubles? Maybe, but it’s already depreciated over the last 18 months in anticipation of a lot of those troubles. It depends on how much the Chinese move toward enhancing themselves in a domestic-based economy instead of on exports – from that view, the Yuan will likely appreciate.

Yra points out the Yuan-Peso currency exchange rate is a much more interesting relationship because Mexico stands to be a real competitor to China for the US economy, whatever way NAFTA is treated. The Yuan needs to not appreciate against the Peso.

INTERNATIONAL USD DENOMINATED DEBT

Russell thinks the USD will strengthen also because of the high levels of USD denominated debt held internationally outside of the US, saying that at some point in the event of a recession, there could be higher demand for USD to pay back USD denominated debt.

Yra asks will the global recession cause a run in the Dollar? If the US equity market is a flows argument, and global flows are headed there, the Dollar hasn’t performed that well over the last 4-5 months. That one’s not going to play out and if the world gets into that type of financial difficulty because of the debt, some of the old true relationships are going to break down dramatically. That’s really when you want to start buying gold – if that’s the case, the Dollar isn’t going to be bullish, and you just load up on precious metals instead of any currency.

We know the US President can lower the value of the Dollar, but it’s not an easy task when everyone wants a weaker currency. What can the US President do? He has to explain to his friends and trading partners why he wants a lower Dollar and get them to sign off on it as what’s best for the global financial system. That’s what we’re discussing here. He could do it by having bad policies.

ON THE EURO CURRENCY

After the French elections are over, we can probably look for the Euro to rally. The Euro is too weak for where the Germans are at. The question for the EU is “whose Euro is it”. France, Italy, and Spain don’t need a stronger Euro, but will it go up? Maybe. As Germany now presses onto this election, the discussion seems to change a little bit. With all the problems the US has, it’s scary what the discussion is. But the equity market continues rallying so no one cares. The fact that the Dollar cannot gain any type of strength with everything else that’s going on in the world and other geopolitical problems, that is a warning sign that things are not good here and the Euro can go higher.

Draghi isn’t going to announce any tapering of the QE plan, and he needs to keep building the ECB balance sheet because that’s what’s going to pave the path for a Eurozone bond. That’s the real game and it’s capturing the Germans. That’s where they’re going and it won’t be easy. They’ll bail out Greece because they don’t want this to be an issue in the German elections because it’ll undermine Merkel a bit. The stronger she gets, the better it’ll be for her after the election.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

LINK HERE to download the MP3 Podcast

05/25/2017 - David Rosenberg: The Fourth Industrial Revolution Is Having A Profound Impact On Worker Anxiety

“The yield curve is flat enough that if the Fed raises rates four more times, that’s all it takes. We probably will have a recession next year .. Politics, to me, unless it has a substantive impact on the earnings outlook or the economy, is just short-term noise .. What’s happening in terms of artificial, robotic intelligence and the shared economy… Right now, we’re going through the fourth Industrial Revolution, and it’s having a profound impact on worker anxiety .. How is it that we have 23 million Americans between 25 and 54, in their prime working age, that are out of the labor force? .. There’s some real structural things happening here that really transcend the need to cut taxes or what’s happening in terms of immigration policy.”

05/25/2017 - Danielle DiMartino Booth: Beware Of Central Bankers Bearing Gifts “The bottom line is we still have too much debt and precious little to show for it.

It’s critical to note that Corporate America is also drowning in record levels of debt – nonfinancial corporate debt within a hair of $6 trillion. And though it was nary mentioned in the campaign by either party, at $20 trillion, Uncle Sam himself is up to his eyeballs in hock.

Hopefully you can see Trump’s once in a century chance to reshape the warped thinking inside the Fed. He has the tremendous power to redirect the meme by draining the debt swamp that makes our government beholden to foreign lenders, our corporations less competitive on the global stage and our households seething at their inhibited upward mobility. Talk about Making America Great Again, for ALL Americans.

Without a doubt, this will be one of Trump’s toughest tests, and yes, the Fed can easily take down the stock market in retaliation; they could even follow through on threats to shrink the balance sheet. It would be as if someone flipped a switch and we veered from Quantitative Pleasing to Quantitative Plaguing.

And what politician in their right mind wants plague visited upon their economy on their watch? Ask any of Trump’s predecessors and they’ll shoot you straight. Passing legislation with ultra-easy monetary policy and fluffy stock prices on your side sure as heck beats the alternative.

But in the end, it just buys time, not Greatness.

Artificially low interest rates might be as alluring as that Trojan Horse was to the people of Troy. But let’s put their experience to better use and not dismiss Laocoön’s words as the tragic Trojans did. Let us all Beware of Central Bankers Bearing Gifts.”

05/24/2017 - Charles Hugh Smith On The Ongoing Permanent Keynesian Stimulus To The Economy – The Failure Of The Keynesian Coloring-Book Plan

“What do we call a status quo in which ’emergency measures’ have become permanent props? A failure. The ’emergency’ responses to the Global Financial Meltdown of 2008-09 are, eight years on, permanent fixtures. Everyone knows what would happen if the deficit spending, money-printing, zero interest rates, shadow banking, asset purchases by central banks and all the rest of the Keynesian Cult’s program stopped: the status quo falls apart .. Nothing has worked as the Keynesians expected. Instead, state/central bank measures that were supposed to be temporary are now permanent, and the expansion of private-sector debt has failed to ‘trickle down’ to earnings .. The Keynesian solution—borrowing from future earnings to ‘bring consumption forward’—has expanded consumption at the cost of enormous increases in debt throughout the economy, which has exacerbated income-wealth inequality and declining real incomes .. Can we finally admit that eight years of following the Keynesian coloring-book plan have not just failed, but failed spectacularly, and not just failed spectacularly, but made the economy even more vulnerable and fragile, as more and more future income must be devoted to service the skyrocketing debts? .. Isn’t it obvious that there are deeply structural problems in the economy that inflating yet another credit/asset bubble won’t fix? .. Clearly, the real-world economy does not function like the simplistic Keynesian coloring-book model.”

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority