Jay Taylor Interview ..

09/07/2017 - Jeff Deist And Dr. Mark Thornton: Central Bankers Are Responsible For Boom And Bust Cycles

09/07/2017 - Jeff Deist And Dr. Mark Thornton: Central Bankers Are Responsible For Boom And Bust Cycles Jay Taylor Interview ..

09/07/2017 - Paul Brodsky: Nominal Asset Prices Could Rise – But In Purchasing Power Terms?

“Central bank purchases and government investment have been fabricating output growth and asset gains. Central banks now hold about $19 trillion in assets on their balance sheets, up from almost zero in 2008, and are now 20 percent owners of global assets. There is also about $20 trillion in US federal debt, up from $9 trillion in 2008 .. The current imbalance separating credit (claims on money) from money itself suggests a doubling, tripling or even quadrupling of the money supply in float (yes, 100, 200 or 300 percent monetary inflation directed towards financial markets). This implies nominal asset prices could rise, but not nearly as much as the purchasing power value of the currency they are denominated in would fall.”

09/07/2017 - Daniel Lacalle: Are Central Banks Nationalizing The Economy?

“The FT recently ran an article that states that ‘leading central banks now own a fifth of their governments’ total debt.’

The figures are staggering.

•Without any recession or crisis, major central banks are purchasing more than $200 billion a month in government and private debt, led by the ECB and the Bank of Japan.

•The Federal Reserve owns more than 14% of the US total public debt.

•The ECB and BOJ balance sheets exceed 35% and 70% of their GDP.

•The Bank of Japan is now a top 10 shareholder in 90% of the Nikkei.

•The ECB owns 9.2% of the European corporate bond market and more than 10% of the main European countries’ total sovereign debt.

•The Bank of England owns between 25% and 30% of the UK’s sovereign debt.

The Bank of Japan, with its ultra-expansionary policy, which only expands its balance sheet, is on course to become the largest shareholder of the Nikkei 225’s largest companies. In fact, the Japanese central bank already accounts for 60% of the ETFs market (Exchange traded funds) in Japan.

…

The central bank can ‘print’ all the money it wants and the government benefits from it, but the ones that suffer financial repression are the rest. By generating subsequent financial crises through loose monetary policies and always being the main beneficiary of the boom, and the bust, the public sector comes out from these crises more powerful and more indebted, while the private sector suffers the crowding-out effect in crisis times, and the taxation and wealth confiscation effect in expansion times.

…

It is a clever Machiavellian system to end free markets and disproportionately benefit governments through the most unfair of competitions: having unlimited access to money and credit and none of the risks. And passing the bill to everyone else. If you think it does not work because the government does not do a lot more, you are simply dreaming.”

09/05/2017 - Alasdair Macleod: Normalizing Interest Rates Would Threaten The Whole Western Financial System

“Where do the Fed and the ECB respectively think America and the Eurozone are in the central bank induced credit cycle, and therefore, what are the Fed and the ECB going to do with interest rates? And why is it still appropriate for the ECB to be injecting raw money into the Eurozone banks to the tune of $60bn per month, if the great financial crisis is over? .. Normalizing interest rates would spring the debt trap firmly shut. The whole Western financial system would be threatened by a combination of defaults and collapsing asset values, starting from the weakest point in the global financial system. With debt of today’s magnitude, it will take nominal interest rate rises of only one or two per cent to set off the crisis Ms Yellen believes will never happen again. It is a repeating credit cycle endemic to the fractional reserve monetary system and central banking’s monetary intervention. And when the crisis hits, yet again for the umpteenth time, central banks will flood the system with ever larger quantities of cash.”

08/31/2017 - Dr. Thorsten Polleit: Central Bankers Are Debasing Currency

“Sound economics tells us that central bankers do not pursue the greater good. They debase the currency; slyly redistribute income and wealth; benefit some groups at the expense of others; help the state to expand, to become a deep state at the expense of individual freedom; make people run into ever greater indebtedness.”

08/31/2017 - Nomi Prins: Ongoing G7 Central Bank Monetary Policy Collusion, 0% Interest Rates Globally, Unlimited QE Potential, Major Asset Bubbles

“As we approach the ninth anniversary of the collapse of one of my former employers, Lehman Brothers, and the 10th anniversary of the beginning of central bank collusion into the financial crisis, there has been – no change – in global G7 central bank monetary policy .. Take the composite of all that and what are you left with? Ongoing G7 central bank monetary policy collusion, zero percent interest rates globally, unlimited QE potential, and major asset bubbles.”

08/29/2017 - This Is Not Capitalism – Overregulation, Corporate Bailouts, Manic Money Printing, Artificially Low Interest Rates

“Today, we’re continually reminded that we live under a capitalist system and that it hasn’t worked. The middle class is disappearing, and the cost of goods has become too high to be affordable. There are far more losers than winners, and the greed of big business is destroying the economy. This is what we repeatedly hear from left-leaning people and, in fact, they are correct. They then go on to label these troubles as byproducts of capitalism and use this assumption to argue that capitalism should give way to socialism. In this, however, they are decidedly wrong. These are the byproducts of an increasing level of collectivism and fascism in the economy. In actual fact, few, if any, of these people have ever lived in a capitalist (free-market) society, as it has been legislated out of existence in the former ‘free’ world over the last century .. Years of overregulation, corporate bail outs, manic money printing, and artificially low interest rates, have bloated and warped the economy.” – Jeff Thomas

08/29/2017 - Yra Harris: The Exit From QE Programs Will Be Far More Difficult Than Central Bank Models Have Predicted

“The SWISS FRANC has certainly been involved in currency intervention as it has increased its foreign reserves over the last seven years from roughly 100 billion Swiss to a now 715 billion, which most of the accumulation having occurred over the last three years.

My argument has been and continues–as the SNB PRINTS BILLIONS of SWISS FRANC to sell in order to prevent the dramatically rising I WONDER WHAT ENTITIES HAVE BEEN ACCUMULATING SO MANY FRANCS DEFYING THE WILL OF THE SNB. Yes, the SNB have performed the greatest alchemy in financial history as it exchanges newly printed fiat currency for real corporate assets (i.e. APPLE STOCK.)

At a time when the SNB has actually managed to weaken the Swiss franc versus the EURO SNB President Thomas Jordan OUGHT to be buying back some of the francs and selling its EUROS. Unwinding its massive foreign reserve portfolio. But as Peter Boockvar discussed in an FRA PODCAST, the SNB is trapped because any hint of SNB buying of Swiss francs would lead to a sizable rally. The EXIT from QE programs will be far more difficult than their beloved models have predicted.”

Notes From Underground: Arthur’s Song, Lost Between the Moon and New York City

08/28/2017 - The Roundtable Insight – Morten Arisson On A Unique Investing Method Based On The Austrian School Of EconomicsFRA: Hi, welcome to FRA’s Roundtable Insight .. Today we have a very special guest. He’s Morten Arisson. He’s a Canadian economist, whose work in interest focuses on portfolio management, investing history, probability and mathematics. He has worked in strategy consulting, private equity and credit portfolio management. He’s written a book called Investing in the Age of Democracy. In that book he explains how democracy, beginning with the American and French revolutions, shaped the way we currently invest in the 21st century. He proposes an alternative approach to investing based on 4 key features that are unique to the Austrian School of economics: class probability, the role of entrepreneurship and institutions, and the notion of inter-temporal exchange. Followed by ultimate consequences, these define a unique investing method. So what he has done is structured the book in 10 lessons where history, math, law and economics mix to provide the reader with a rich perspective that stretches from ancient Rome’s first investment vehicles to high frequency trading in the 21st century. So we’re going to explore that today with Morten. Welcome Morten.

MORTEN ARISSON: Hi, thanks for having me Richard – a pleasure.

FRA: Great – so I just want to mention that you were kind enough to put some notes together that we will put into an overall transcript once this podcast is published so we’ll have a transcript plus a podcast that people can either read or listen to the podcast or both. Just wondering a little bit about your background on economics – how you came to look at the world through an Austrian School of economics perspective.

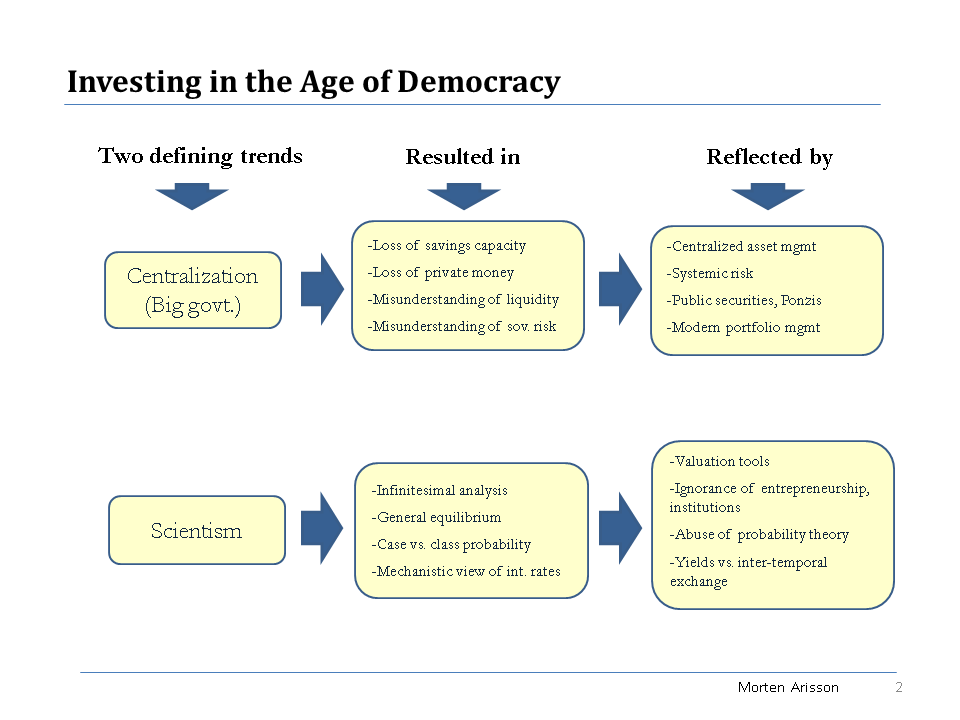

MORTEN ARISSON: Okay – I was educated in Economics. I have a bachelor’s degree in Economics, but it was only recently, a few years ago, that I became very interested in Austrian economics and I went to the conference at the Mises Institute, in Auburn in 2011 – And I did further research and I really liked the work of a gentleman from Spain, Huerta de Soto. He has written extensively about the issues of dynamics, coordination in markets, probability and so forth. And you know, being familiar with the Austrian school, I often heard that it is not clear whether one can say that there is a unique investing method that would define Austrian Economics, in an applied way. This book was a challenge for me. I was going through some pillars, some defining characteristics of the school of thought, and I think that if you follow them to the last consequence you can actually organize a very rigorous structure, a consistent investment method that will be unique. The book obviously asks why, if that is the case, market forces would have not led us there. I argue that we would have been there had it not been for interventions which are of political nature and have a lot to do with the political developments that we have seen since the French and American revolutions. So, broadly speaking, there were two trends: one was centralization – also sometimes understood as big governments – it has been increasingly growing since then, and at the same time Scientism, which is a term that was brought forward by Hayek, if I’m not mistaken, Friedrich Hayek. It mainly describes the abuse of the scientific method; in this case, to humanities. These two have created a lot of situations, gave place to a lot of interventions by governments that in a way ended up taking us apart from this approach to investing.

FRA: And so what you’ve done is you’ve identified 4 elements from the Austrian School of economics that yield a unique investment method if you want to go into some detail on that.

MORTEN ARISSON: Right. Probably, I should expand a little bit more first on what each, centralization and Scientism, do to the way we look at investing today and how the pillars define that method. So, in terms of centralization, we have seen with increasing tax rates that we have experienced a loss in the saving’s capacity, particularly with the establishment a hundred years ago, approximately, even more, of income taxes. And that’s something that began in a few countries and now it’s widespread all over the world. Then, in parallel to that, we have suffered the loss of private money – also called gold – which was also a very slow process which began in 1913 with the creation of a Federal Reserve and then in 1933 with the expropriation of gold in the United States, we’ve had a system – the gold exchange standard that lasted until 1971. From then on, we have been basically on fiat currency. That also led to a misunderstanding of the concept of liquidity. I think this is important. I’m going to put a few minutes here.

FRA: Sure.

MORTEN ARISSON: The way people look at liquidity today is as if it was an intrinsic characteristic of an asset. So, people can say: “Well this bond is liquid or this stock is liquid.” If you look at the way we used to see it – even until 1936 John Maynard Keynes, who was obviously not an Austrian… – He referred to the concept of liquidity preference. So, we all do have a liquidity preference, which is the preference to be liquid and to own money, which is an asset that sort of protects us from uncertainty. At the same time, the concept that liquidity is characteristic to an asset unfortunately was suggested by Carl Menger, who was an Austrian. He called that, in his words, “Marktgängigkeit” which was sort of “marketability”. And from then on, it was corrupted, and today we understand liquidity as the capacity of an asset to be traded with credit. If we say that a market is liquid, what we are saying today is that there is enough credit in that market to trade an asset, even though as a counterpart we don’t have true savings supporting that. And that is very important, because then, that creates a distortion that shouldn’t be. I mean, if you want to be liquid, Austrians would say, just own money that is the instrument that you need to be liquid. Then, from then on, if you want to invest, invest in capital assets. But the corruption of the concept of liquidity led us to mix everything – money and capital, and create degrees of liquidity in them, and forces to think in terms of paying for risk premiums when in fact there’s an asset available to us at every time, which is money. That too, because money began to be created by the expansion of fiscal deficits which led us to the misunderstanding of sovereign risk as well, – and it is something I discuss in the book. But all of that together created a distortion in favour of public securities versus private securities, the creation of Ponzis, and with central banks, systemic risk. At the private level the rationalization of all that under modern portfolio management – the theory of modern portfolio management. And all of this is a product of that movement in centralization that we have experienced, our big government that we have experienced since 1780s. In terms of Scientism, which can be described as the abuse of the scientific method applied to humanities, you can see that particularly after the 1870s with Walras, you have seen infinitesimal analysis, general equilibrium and the use of probability and the mechanistic view of interest rates that Austrians considered as inter-temporal exchange rates rather than as productivity rates, applied to the valuation of securities which are actually property titles on entrepreneurial processes. So all of that together takes us to where we are today.

However, I think we can make a pause here and think in terms of the 4 pillars of the Austrian School of economics. One of them I think is the most important is entrepreneurship – the role of entrepreneurship. It is completely ignored in mainstream economics; there’s no place for that because, mainly, it cannot be formalized, and that is seen as a disadvantage rather than being considered on a factual basis. There is no reason to believe it is better or not to mathematize entrepreneurship. And somebody, a few years ago, published an article on a Spanish magazine – Procesos de Mercado, edited by Jesús Huerta de Soto, proposing a way to establish whether or not entrepreneurship could be formalized. He concluded that it cannot, – because it’s non-recursive, it cannot. And so why did I bring this up? Because if you establish that human action cannot be mathematized, entrepreneurship cannot be mathematized, then there is no point in saying that you can value equity, which is a property title on said entrepreneurship. And that has profound consequences, because if you cannot value that, if it’s up to the risk management of the entrepreneur, the immediate direct consequence of that is to say that if you’re going to invest in equity you should invest in private equity because it’s something that you can manage. It’s a risk that you can manage. It’s an uncertainty in which you have certain control. And that is not the case solely with public equity. And one of the things I bring up in the book is that at the time of Adam Smith, with the beginning of the concept of limited liability, there was an enormous debate on whether it was advantageous or not for investing. One of the distortions that took us out from the field of private equity that was predominant, I would say, since the fall of the Roman Empire to the times of the trading companies in Holland, was private equity. And it was in the beginning of the trading expansion of Holland that lawyers like [Hugo] Grotius bought up the issue of changing the status quo and establishing the concept of limited liability. There was a lot of reaction against that at the time, and it had to be imposed. And because it was imposed and was properly seen as a privilege, the monarch that did that charged a fee on that privilege. And I would say it stayed that way until the mid-19th, century when increasingly in the United States it was seen as necessary to fund more ventures. But, like I say – it’s something very, very recent and it has created a distortion in terms of favouring public equity versus private. And at the same time, if you add the other intervention, which is the banning of insider trading, which takes the signal out of the market, it creates the illusion that there is no such thing as insider information –,… It also unlevels the field of private equity versus public equities.

So this would be one of the first pillars – the idea of entrepreneurship, that if you think the Austrian way, literally you think that the best case for you as an investor is always to go for private equity. The other one is the concept of probability. I think it’s a key characteristic of the Austrian School of economics to distinguish between case and class probability. The concept of class probability was actually the mainstream concept of probability up until the 1920’s. And I’m going to try and be brief here, but it basically was the probability that – you can think of in terms of when you roll the dice [here are limited spaces and you know the outcomes. Richard Von Mises, who was the brother of Ludwig Von Mises, wrote a book called “Probability, Statistics and Truth” that I think was published in 1928, and he made the case that that is the only time when one can speak of probability correctly – properly. And that means that, in order to do so, you have to identify a collective, a group of elements or, in this case companies, if you want. And they have to behave in a homogeneous way and converge to a number that you may be looking at, let’s say a return or a ratio. And most importantly, whenever you take different time frames to see that convergence take place, regardless of which time frame you take, you still see that trend taking place. And if you apply that to investing, you will realize that since entrepreneurship is unique – there are unique markets, there are unique companies with unique management, unique capital structures, it’s impossible to apply probabilities here, because, – I mean you can speak of a asset class called equity versus an asset class called debt and I guess you could say that the convergence of the net returns is positive otherwise there would be no entrepreneurs – otherwise they would be always bankrupt. But besides that, I can’t think of any other case. And the proof of that is that rating agencies show every month updated tables on, for instance, migration in risk ratings. I mean, if you could apply probabilities here regardless of which timeframe you see, probabilities of default for, let’s say companies with similar debt-to-equity or similar net debt-to-ebitda ratios, it should not change, – but the fact is that they do change… I’m not surprised. And it’s just, you know, with that scientist approach, with that search for perfect information, you run into the illusion that we can use it.

But it was a movement that began with Keynes in the 1920’s in a book called “The Theory of Probability” and it has really shaped the way we look at portfolio management today. If you use a Bloomberg terminal and you try to value any security that would be a derivative or any structured product, you would immediately see that probability is used without thinking, without a pause. It’s just something very direct. If you use the other concept, the Austrian concept of class probability you realize that unless you actually have control over that security that you want to own for your investment purposes, there is no point in trying to forecast the probability of something happening, because effectively you have no control. I mean you’re running into a tautology where you tell yourself: if such and such a thing happens, I would get this outcome. But I mean, that adds no insights – no further information. So, I don’t know if you have any questions or, if you want, I can go to the 2 other pillars of…

FRA: Yeah, sure. So we’ve covered so far entrepreneurship and sort of the correct theory of probability and we have two more institutions, money, capital and interest rate. Go ahead on those two.

MORTEN ARISSON: In terms of the institutions, I think that the Austrians have an advantage because they can understand the institutional context in which investing takes place. I mean, there are very important institutions like a deposit and a loan that the Austrians can distinguish. They understand that a deposit is not a loan, and that fractional reserve banking corrupts that concept today. They understand what is money and what it’s not, and the qualities that money has to have and that gold is money, so to speak, because it has all those qualities. If you look at, for instance, virtual currencies, I believe that virtual currencies lack two qualities that are quite necessary – I mean fundamental to money. One of them is fungibility. Since Bitcoin by definition is a ledger, a distributed ledger, it will never be fungible.

FRA: Sorry, just to clarify, the virtual currencies you’re meaning the cryptocurrencies right? Such as Bitcoin and –

MORTEN ARISSON: Right, right.

FRA: Okay. Just to be clear.

MORTEN ARISSON: Yeah. So those cryptocurrencies are distributed ledgers. There’s a reason why that happens, because they are not redeemable. So, the two characteristics that define money – I mean that are more but these are fundamental to money: these are fungibility and redeemability. And by definition virtual currencies or cryptocurrencies are not redeemable. You cannot redeem them into any… – you can change them, you can use them as an indirect medium of exchange, but you can never redeem them themselves. Fiat currencies you can do, you get the physical paper bill. Gold you can do, you get the metal. But that’s not the case [with cryptocurrencies] and because possession is not there to show ownership –, Ownership has to be established via the distributed ledger. And that institution [distributed ledgers], if you want, because it has been a spontaneous creation of the market, cannot benefit from fungibility, by definition, because at any point you know what belongs to whom.

FRA: Yeah.

MORTEN ARISSON: So, there can never an established capital market in that sense. And as far as I know, at least to date, the only inter-temporal exchange is peer-to-peer, right? Which some savings are – you know exchanged from one participant to the other, but not to a central institution that collects and then distributes. And I mean that is intrinsic to virtual currencies precisely because .. my understanding that those who created them, actually wanted to avoid that centralization, – But banking has a role, right? I mean, there’s a lot of information to be discovered about those saving and those demanding those savings, and it has value. And banking itself is an institution that has been documented at least since the time of ancient Greece. So, without fungibility you can never have capital markets in cryptocurrencies. And at the same time without the redeemability if there ever is any sort of expansion via credit multiplier, it will have to be unchecked by definition too, because there will be never any run on any Bitcoin banks, for example. And eventually Bitcoin or any cryptocurrency that advances to that stage would devalue. You know, defeating its own purpose, right? Because the credit multiplier would affect an expansion that was not thought of by the traders of the cryptocurrency. So, if you want, you know, in a way you can say that Austrian investing is institutional arbitrage, because you’re always understanding loopholes, interventions on market-driven creations, institutions and arbitrage and sell the bad ones to buy the good ones. You could say the same about structured investments, you could say the same within the space of currencies” you’re arbitraging certain features. Usually scarcity being one of them, we arbitrage scarcity when you see that a currency expands more than another, you’re arbitraging scarcity. If you need to take capital out of a jurisdiction that is pretty restricted, you are arbitraging redeemability. And that’s where Bitcoin gets its value [from], because it’s less redeemable and at the same time less sizable by the authorities.

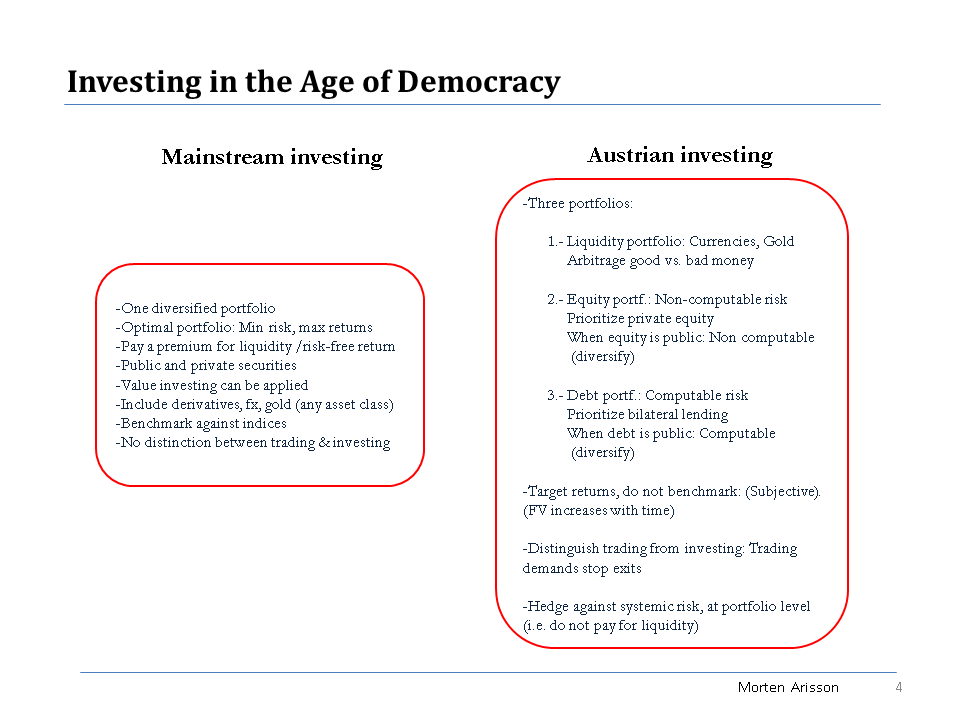

There is also the issue of public institutions where you recognize, if you are into the Austrian School of economics, you recognize failures in public institutions. One of them is the Eurozone, where mainstream economists took last year’s crisis as a liquidity crisis, while lots of other economists understood that it was an institutional problem and that it was the fact that there’s not a unified bond market in the Eurozone. And the last but not least important of all the pillars is the understanding of what is money and what is capital that is lacking in mainstream Economics. And that interest rate is actually an institution too, whose function is to allow the inter-temporal exchange of resources between people. And the direct consequence of understanding that is that it allows you to differentiate when you invest and when you trade. When you invest is when you exchange your money for capital assets. And so with derivatives that are not used for hedging, for instance, or commodities or fiat currencies, you’re not investing, they don’t yield any produce and that’s the same case for gold. So an Austrian would say that you do not invest in gold, you exchange a fiat currency: one currency for another one. There is also another direct consequence of understanding what an interest rate is, which is that asset allocation is nothing else but inter-temporal preference. So, there’s a direct connection between your inter-temporal preference and the way you allocate your assets, whether you want growth or not. If you want growth you need, like I said, to invest in equity, in entrepreneurial projects. If not, if you want yield, obviously you will go for another part of the capital structure – for debt. And any subjective exchange – I mean any, inter-temporal exchange is completely subjective. There’s no point in trying to benchmark yourself against indices in terms of returns. You have to target your absolute returns, the ones you are comfortable with and the ones that are consistent with your liquidity preference and I’m going back to the concept of liquidity. So that when you put all these four pillars together: the correct understanding of the theory of probability, the correct understanding of the role of entrepreneurs, the correct understanding of the role of institutions, and the correct distinction between money and capital, and understanding of interest rates, then you come up with a particular method that would say to you: Well, you need to think of investing not in the terms you have seen until now, where you have one big diversified portfolio that tries to be optimized in terms of risk and returns, minimizing risk and maximizing return.

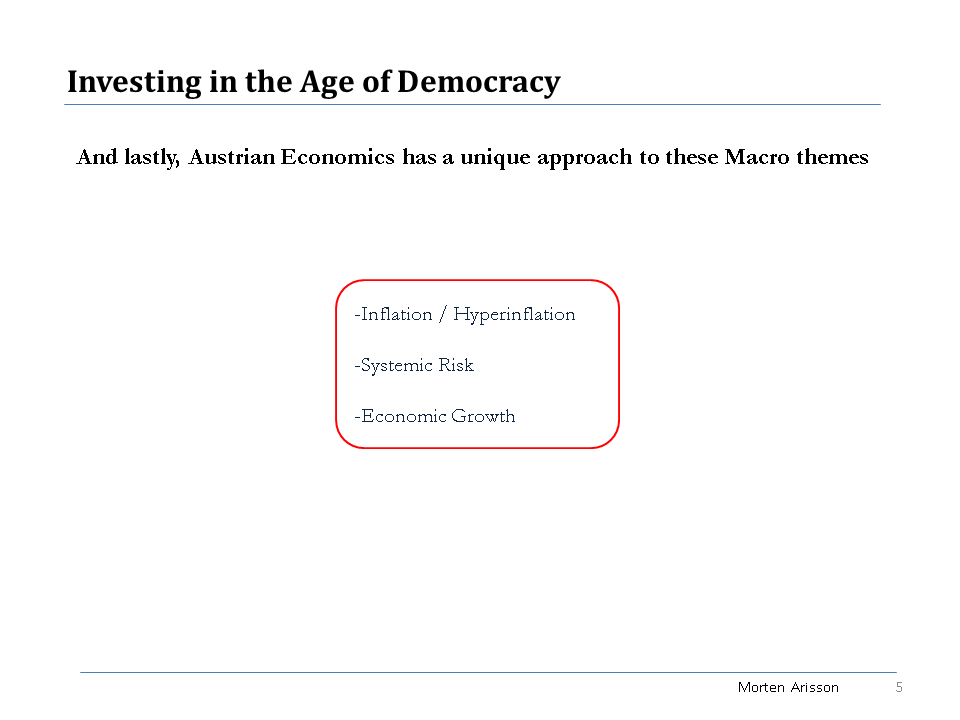

You shouldn’t be paying a premium for liquidity. You shouldn’t mix private and public securities. You shouldn’t even try to do any value investing because it’s a tautology. You will never be able to really know the value of any entrepreneurial project unless you have a control of it. And then, the first thing you should do is define your liquidity needs, so your liquidity preferences and separate that into a liquidity portfolio. Then, the second one is, once you establish your inter-temporal preference, you look for a certain component of growth and a certain component of yield and that growth will be represented by equity. But you have to prioritize private equity and in terms of that the same happens once you prioritize bilateral loans. But again the book goes to explain all the distortions that we have suffered that have made the use of bilateral loans, such as lending to someone directly via mortgage, – that took us away from that. We are left with public securities, public equity and public bonds, and we are constantly benchmarking the indices. There is another interesting thing; if you recognize the fact that final value increases with time and the direct consequence of that is that – most of the time with mainstream investing theory – the recommendation comes that when you’re young you should try to go for as much equity as you can for as much growth as you can with your investments, because only after when you’re established you need a stable cash flow. But when you think of that, you are putting yourself through an enormous amount of risk, uncertainty in securities over which you have no control and you lose an enormous amount of compounding value. So, I think that when you go through all this thinking in terms of how to approach investing, one conclusion is that the longer your term horizon, that means, the younger you are, the less you have to invest in equity and the more you have to invest in computable risk that can compound – that you can manage. There were a lot of institutions that we had created before this big increase in government. One of them was the annuity business by the insurance companies. It was a legitimate market-driven, spontaneous invention, but today we don’t have that and with distortion in interest rates it’s pretty expensive if you try to go that way. So, again, the younger you are the more you have to allow for that compounding to work for you. Only when you’re getting older and you see that you don’t get to your target in terms of savings, then you can start risking something, which is completely counterintuitive versus what common knowledge says. So, and after all, yes I devote one third of the book, the last third of the book, to discuss the proper macro themes in Austrian economics. But, as you can see, we just discussed very specific things and I haven’t gone properly into discussing any macro themes. And one of them, I think is most important, is systemic risk, in the chapter where I go to show that there is no such thing as systemic risk. It [systemic risk] is just the natural outcome of the interventions in the market by central banks. The fact that we don’t know when it’s going to happen doesn’t mean it is risk. It is there, and we know it causes, and we know how the process works, the coupling between central banks works, which I describe in a chapter, via cross currency swaps. And I recommend that after you have established your three portfolios, liquidity, equity and debt portfolios, one can think in terms of an aggregate hedge against that systemic risk at the portfolio level. That could sort of address the mainstream view that you have to pay a premium for liquidity. An alternative could be that you do not, again, you separate whatever liquidity you need under your liquidity portfolio. Then once you have established your investing portfolios you put a hedge against systemic risk for them, to protect them.

FRA: And how do you do that exactly in terms of applying a hedge?

MORTEN ARISSON: This is just my own opinion, in the case of Canada that the hedge was the exchange rate between the U.S. dollar and the Canadian dollar. As you see, increasing systemic risk in these particular times, in this particular moment, through the increase in risk from the real estate market, I think that will be translated into sovereign risk and it would push the monetary authorities to devalue the Canadian dollar. So, if you can be long an instrument that would capture that and would have some convexity properties in that sense, then you’re doing exactly that [hedging systemic risk].

FRA: And just a couple questions. You mentioned on the equity portfolio that you should prioritize private equity. How do you go about doing that in terms of the prioritization process?

MORTEN ARISSON: I think the simplest way to do that, which is accessible to everybody, is to buy a property today. But that has been completely intervened today by the government. There is this push from the government to take you away from any safe haven assets. When you buy a property for investment purposes, obviously you are first avoiding fractional reserve or re-hypothecation of the assets, because there cannot be two similar assets on the same location, because you’re buying location. Then you are free to manage – you have a lot of latitude in terms of managing, and in terms of having control over that. But for real capital assets, I have a chapter devoted to them, but I think the conclusion in the book is that there is never a definitive answer to that. And that is very intrinsic to Austrian Economics: the notion that there is never equilibrium; that you’re always in danger, that you always have to look out for opportunities and for future problems. Like I said, there might be multiple real capital assets. You can have property, cattle, wine, forestry, and farmland. And all of them they serve a purpose at a specific time within a crisis. For instance, in terms of farmland, it’s not a hedge against crisis forever. It will be your equity investment, but to a certain extent if things go really bad, you will be stuck with an immovable asset, a very easily taxable asset. So again, even as I provide examples of ways in which you can invest into private equity, there is never a safe haven asset.

FRA: And in terms of public equity, is your suggestion to diversify due to the non-computable risk?

MORTEN ARISSON: Yes and no. If you say that then anybody could argue well you’re just saying the same as mainstream economics. And here’s the thing: in Mainstream Economics, the exercise of diversification is against the…they have what they call systemic risk component that they claim to be able to measure from observations on what they call risk-free assets, such as sovereign bonds. That diversification comes from the measurement of the sigma, the volatility of all their assets and their correlation and so on. Which again, they go into a circularity because they assume that past performance will be something that you can project into the future and you have to make a lot of assumptions that just revolve around themselves. What I am saying is, yes you have to diversify, but only because you know nothing. You absolutely know nothing and the shot can come from anywhere. If you tell yourself that you need 20 securities to be diversified, well you’re kidding yourself, that is not the case. If these are subject to a currency zone and they are denominated in a currency that because of institutional problems, because the central bank is too weak or prone to suffer from devaluation – there is no remedy to that. So, the diversification comes only as a consequence of the recognition of our ignorance, but only that. I cannot provide you with a specific number [of securities to diversify]. Obviously, the general idea is that all things equal, the more assets you have, the better. But that is not necessarily true and that [diversification] is a very subjective exercise.

FRA: The last question is on – you mentioned these three macro themes and how Austrian Economics has a unique approach to these three macro themes. Can you briefly touch on the inflation/hyperinflation macro theme?

MORTEN ARISSON: Yeah, sure. Obviously the general notion of inflation within mainstream economists is that you have something that is observable, that is a vector which they call an index of prices and that inflation is neutral, that never goes up or down in terms of monetary expansions or reductions. But as an Austrian you recognize two things. First, that it is not neutral, absolutely not. The reason that money expansion is not neutral is precisely what motivates monetary authorities to create, inflation. The second thing is that there is this notion that hyperinflation is simply an arbitrary high number in terms of inflation, and that is not the case. Hyperinflation is not quantitative – that is my point. Hyperinflation is a qualitative phenomenon and it is one in which the central bank finds itself defenseless, in a circularity where they are obligated, they are forced to issue an interest-paying liability. The interest that they pay on the liability is higher than any interest they receive on their assets so that [resulting] deficit, which is called quasi-fiscal deficit, can only be covered by monetizing and by printing money to pay that net interest. Then again, in order to take that money that the central bank just put into circulation, what they have to do is increase the rate, they have to sterilize that money that they have just printed, at a higher rate, which simply enhances that circularity. Today, right now as we speak, there is one country that is suffering from that – Argentina. With an instrument called Lebacs, the central bank began paying something like 38% a year ago and it’s around the high 20’s now. And, unless they have the fiscal deficit in control in Argentina, that will spiral out of control. So, even though you don’t see inflation in the 100’s like you used to in the 80’s maybe, the fact is right now that that central bank is out of control, and they’re in the early stages of a hyperinflationary process. What about us in the first world? Well, what matters here is the relation between the interest income received by the central bank in excess and what they have to pay. It doesn’t have to be too high. What if there was a sovereign problem in the Eurozone and all of a sudden the central bank had to replace sovereign bonds with their own liabilities? Right now what they do is they collateralize, but, what if they actually had to replace it with their own liability, but with an interest-paying liability? On the one hand they have, like any central bank, money supply which bears no interest and then they have to pay 25 bps. Those 25 bps will have to be monetized. So, right there, you have hyperinflation, and I think one has to pay close attention to that, and only if you understand that you will see how, in my opinion, we are at the early stages of a hyperinflationary period. But again, you have to understand that it is a loss of control by the central bank [what causes hyperinflation] and not the inflation rate on its own.

FRA: Wow Morten, great insight on Economics and investing. How can our listeners learn more about getting access to your book “Investing in the Age of Democracy”?

MORTEN ARISSON: The book is already on available now on Amazon. It is under the title “Investing in the Age of Democracy”. And soon, I intend to put it on a digital format for Kindle.

FRA: Great, we look forward to that. Thank you very much Morten for being on our show.

MORTEN ARISSON: You’re very welcome.

Transcript by: Daniel Valentin <daniel.valentin@ryerson.ca>

LINK HERE to get the podcast in MP3

08/23/2017 - Dr. Marc Faber: “Compared To Assets, Money Has Lost A Tremendous Amount Of Purchasing Power.”

Central bankers, Bitcoin, and why he’s buying physical gold every month

Hard Assets Alliance, Released on 8/15/17

“It’s good to have a diversified asset outside of the banking system.”

08/23/2017 - Yra Harris: “Low Volatility Priced With So Much Uncertainty Will Provide Dangerous Outcomes.” “‘It’s time to stop wasting our money and recognise the high priests for what they really are: gifted social scientists who excel at producing mathematical explanations of economies,but who fail,like astrologers before them, at prophecy.’ …. The juxtaposition of Jackson Hole with the SOLAR ECLIPSE is perfect for understanding the FED‘s deficiencies. The ROCKET SCIENTISTS at NASA were able to provide exactitude for monitoring the path of the eclipse, knowing to the minute when locales spread over a 3,000-mile path would be viewing the commencement of this rare astronomical event. We were told to don certain GLASSES to view the full eclipse so as not to harm our eyes .. The FED has provided a once-in-a-lifetime experiment to promote a resolution to a severe financial dislocation, but the progenitors of a massive liquidity cannot provide a sense of certainty to the path out of the financial experiment. And, they have no sense of how it ends. The FED, like NASA, bases its outcomes on sophisticated models but in following its theoretical construct we also need glasses: ROSE-COLORED GLASSES. The FED, ECB and BOJ will allude to exit strategies but they do not ensure the certain path of predicting TOTALITY that concludes in South Carolina. Low volatility priced with so much uncertainty will provide dangerous outcomes. When? I don’t know and I say that with great certainty.”

Notes From Underground: Can Jackson Hole Foster a “Dynamic Global Economy”?

08/18/2017 - Jim Rickards: Next Financial Crisis Could Cascade Into Frozen Funds, Banks, Markets

“If regulators freeze money market funds in a crisis, depositors will take money from banks. The regulators will then close the banks, but investors will sell stocks and force the exchanges to close and so on.”

08/18/2017 - China’s Epic Default Cycle Accelerating

Former Fitch credit analyst Charlene Chu believes that bad debt in China is some $6.8tn above these official figures as the government has propped up the appearance of growth and allowed underlying problems to go unchecked.

08/18/2017 - Nomi Prins Speech On Global Monetary Policies: Central Banks In The U.S., Europe & Japan Hold Assets Equivalent To 17% Of Global GDP “Central banks around the world are now pursuing a coordinated zero percent money policy and increasing their assets. The big three central banks in the United States, Europe and Japan now hold assets equivalent to about 17% of global GDP.”

08/11/2017 - The Roundtable Insight: Yra Harris And Peter Boockvar On The “Pottery Barn” Global Bond Market And The Insanity Of Central Bank PoliciesIn this week’s episode we are joined by both Peter Boockvar and Yra Harris. Peter is the Chief Market Analyst with The Lindsey Group and the Co-Chief Investment Officer for Bookmark Advisors. He runs an economic newsletter product called The Boock Report which offers great macroeconomic insight and important updates on economic indicators. Yra is an independent trader, a successful hedge fund manager, a global macroeconomic consultant and has been trading foreign currencies, bonds commodities and equities for over 40 years. He was also the CME Group Director from 1997-2003.

FRA: Today we would like to talk about a few things, perhaps starting with quantitative tightening. Peter is the first to come up with that term. You’ve written recently about that, Yra, in terms of the relationship of that to steepening curves, the 2-10 spread on the yield curve. Also with the possibility of buying bank stocks; there was a question from a reader. If you want to talk about that?

YRA HARRIS: In following Peter’s line – everything I’ve read from Peter and what he’s talked about – is that the next move by the Fed will be the commencement of quantitative ease before we get the next Fed Funds increase. The dynamic will be very interesting to watch. I know what Peter talks about hinges on that, and now everyone else is talking about Draghi and his upcoming appearance at Jackson Hole. I know Peter’s probably more prone to think that he’s going to lay something out to the market, but I’m not quite there yet. I view the ECB and what their final destination is different from the Fed’s destination.

It was interesting on July 26 when everybody was talking about the five year anniversary of Draghi’s famous ‘Whatever It Takes’ speech. When he said it which was actually July 25, I was on CNBC with 5:30 Chicago time, I’ll never forget it, and Steve Liesman was interviewing me, and I said, “They’re going to have a very big problem in Europe” because all the 2-10 curves, the two year yields on the peripheral bonds were 7% and the curves had flattened dramatically from over a hundred-some odd basis points down to 70, and I said it was all coming because of the pressure. They couldn’t fund anything even in the 2-year market. So it was a bear selloff in two year debt across all of sovereign Europe. I said, they got a problem, and while we were on talking about this, Draghi announces his ‘Whatever It’ll Take’, no taboos. So I find that interesting, but when they quote that speech he said, the mandate was also the preservation of the Euro.

I hang a lot on that; I think Draghi hides behind the veil of inflation now, even though inflation targets for whatever they’re worth – and how they came up with the 2%, that’s a whole other show, I’m sure. But that discussion means he’s got something else. The thing we’ve kind of talked about is that he wants to pile on as much assets onto the ECB balance sheet. I think his end game is that he’s going to do what the EU finance ministers and leaders don’t have the strength to do, and create a Eurozone bond. I think that’s what his plan is, and I’m more reticent to thinking he’s going to give us a wink and a nod to some type of Boockvar QT. That’s what I’m looking at.

Going back to the steepening, if the Fed embarks on this we ought to see a steepening. If the ECB doesn’t pull back and the BOJ doesn’t pull back, then as Peter’s talked about, markets are broken so we’ll never get a real signal. The signaling mechanism truly has been broken by central banks. I tongue-in-cheek use Colin Powell’s phrase that ‘it’s a pottery barn bond market now’ cause central banks have broken it so therefore they own it. That’s where we lie, but we should see a steepening.

FRA: Peter, your thoughts? You were the first to identify that term and what could happen by the Fed QT – quantitative tightening.

PETER BOOCKVAR: I think that long term treasuries are caught in this tug-o-war between the downward dragging yields because of the moderation and inflation and mediocre growth at the same time the Fed’s raising interest rates and there’s a natural inclination to flatten the curve. You have that one hand, and speaking of a mediocre economy we have the very interest rate sensitive auto sector that’s essentially in a recession. On the other hand you have this potential pull upwards as QT begins and maybe Draghi starts buying less bonds on a monthly basis. We’ve seen some days some relationships, some days not, of a move in overseas yields dragging or suppressing upwards downwards US yields.

So if all of a sudden Draghi does say, ‘you know what, starting January we’re trimming our purchases from 60B to 40B Euros, and then three months later it’s gone to 20B, and by the middle of next year it’s gone to 0, we’ll still reinvest but it’ll be over by the middle of next year’, then I don’t think the 10 year German bund yield is going to be 42 basis points. I don’t think that the Italian 10 year is going to be sitting around 200 basis points. I think that the European bond market is tinder for a major selloff if Draghi actually follows through with the 2018 tapering plan that takes him down to near nothing. I can’t imagine the US Treasury yield, regardless of what inflation and growth stat is going to sit there, also 225, if the German 10 year is all of a sudden 1%.

If we rewind the tape back to 2015, over a two month period the German 10 year bund yield went from 7 basis points to 100 basis points in two months. It definitely helped to drag up US interest rates. There is going to be that push and pull back and forth, and we saw when Draghi hinted at the tapering last month, and we saw in eight trading days, the German 10 year yield went from 25 basis points to 54 basis points and it helped to drag up US rates. How this plays out in terms of process obviously remains to be seen, but I’m more worried about US yields based on what the ECB is going to do rather than what Fed QT is going to do.

A combination of them both could be dangerous for longer end bonds, but I think the ECB may be more of a dominant lever in determining that.

YRA HARRIS: I agree with that wholeheartedly. If the ECB were to announce quantitative tightening of any sort, I agree with that. That’ll happen. I’m just not expecting Draghi to go that route yet, but if he does I think we’ll have a tremendously volatile move in the long end of the curve especially. When the Fed talked about ending QE, when they first started QE everyone said, ‘oh these curves, they’re going to flatten it’, and then when they were going to end it the initial thing was to steepen. And people were going, ‘yeah, you’re removing a buyer from the markets’, which everybody who’s been sitting there it’s almost like Greenspan putting it to the stock market. If you pull away the reaction is going to be dramatic because so much risk has been put on for very little premium. Risk premiums are ridiculously low across the board. When Greenspan comes out and talks about his bubble, first off all I don’t give much credibility to it because he might be right, but if I wait for it I’ll probably be broke. It’s a famous Keynes line.

If Draghi ejects all, I will be pinned. I haven’t wanted to be. You’d like to take a European in August, but that becomes so critical if he does deliver that. I think we’ll see a tumultuous move, I agree with Peter, on the long end of the curve. Across the board, and it’ll be led by the Europeans. I know that Gundlach was out talking about, oh, German debt is mispriced, but I would argue that French debt is more mispriced, being only 25 basis points richer than the Germans. At least the Germans have a bid to it automatically because of the repo market. It’s the most desirous high-quality liquid asset, so you always have a little bit of a bid. The French, it doesn’t serve as great a purpose. And certainly not the Italian and certainly not the Spanish. It would really cause some interesting moves in the debt market. From a trader’s point of view, I hope he delivers it. When I analyze it and think about his endgame, possibly which is the creation of a Eurozone bond, I’d be surprised to hear that from him. But if he does deliver that, I agree with Peter. We will have a wild ride in the global bond market.

PETER BOOCKVAR: Central banks generally – and certainly the ECB – believe in what they’re doing. They really believe that negative interest rates has been a good thing. They really believe that essentially nationalizing the European corporate bond market and the region’s bond is a good thing. As long as they continue to believe in what they’re doing, they’ll continue to do it to the greatest extent. Draghi is running up against some logistical challenges where it’s some sort of taper is the default rather than by his choice. It’ll be an interesting hoop that he jumps through.

The program is scheduled to end in December so they have no choice but to lay out a game plan for 2018 for the purpose that the current one is going to expire so they’ve got to renew it in some way and in some fashion. By doing it in September, we’re laying groundwork in August, he’s at least giving the market enough time to say, ‘now we know what the 2018 plan is.’ Basically what Yra is saying is that the plan can continue as is. Instead of saying, ‘we’re just going to extend it a year’, which is very possible, they have to tell us something because it’s supposed to end anyway, even though we know it’s not.

YRA HARRIS: Someone ran a very good article yesterday, talking about the amount by just rolling over. Even if they ended QE, but didn’t start shrinking the balance sheet, it’s still a huge amount of money cause of the duration they have on, when they really started buying this stuff. There is a shortage, and they’re already in violation of every rule that was written about this, because the capital key which is supposed to be sacrosanct? They can’t meet it because there’s just not enough German paper. They could not ever meet that number. It was a design flaw to begin with. Typically in the EU, they circumvent whatever rule there is anyway because the European Court of Justice already determined that the primary thing is the preservation of the entire EU project, which means whatever makes it sustain itself. That seems to be their legal binding principle from the European Court of Justice. So even though in Germany when some of the more stalwart money people had brought cases, they’ve lost in at the German high court because they seem to follow that same principle.

We are getting to crunch time. You can keep pushing and kicking the can down the road but as Peter rightly says, we’re getting to crunch time. They’re going to have to tell us what they’re going to do. I think the biggest surprise is – I’m sure Peter will agree with this – if they said, and this will be a huge surprise, that they were going to start following the rule with the BOJ and start buying actual equities. That would really rock the market; we’d probably see the Euro drop 5-6%. Then they know there’s no end to this and they have no end plan and they’ll keep searching for assets to keep pumping money into the system.

PETER BOOCKVAR: That would uncharted territory. That, I think we’re not going to do because that is a logistical nightmare, that is a political nightmare. At least when you’re buying sovereign bonds you should get paid back, but you start buying equities? I can’t imagine the Bundesbank crossing that line.

YRA HARRIS: Like I said, that would be the greatest surprise there is, especially in August before the German elections. You might hear that in October but you won’t hear it until Merkel is comfortably enthroned upon the Chancellorship of Germany. That would really rock the system.

FRA: But isn’t that what the Swiss National Bank has been doing in terms of financial alchemy buying international bonds and equities?

PETER BOOCKVAR: It’s been extraordinary, and even before they got there they cut short term deposit rates down to minus 70 basis points. Just to emphasize, negative interest rates are just a tax, and someone has to eat it. Whether it’s the bank that eats it or they pass it onto a consumer, it’s confiscating wealth. I call it a weapon of mass confiscation. That’s all it is. So you layer on the Swiss National Bank becoming its own hedge fund, that becomes dangerous. Now the Swiss Franc, outside of today’s rally, has been weakening.

Let’s take this a step further. Let’s say Draghi lays the groundwork for tapering and follows through when the Euro goes north of 120. Well the Swiss Franc will weaken further, reducing the need for the Swiss National Bank to be so aggressive, and maybe that leads to some time in 2018 either reversing negative interest rates or manipulating their currency less and you could see where global monetary policy is potentially heading. At the same time the Bank of Japan is in a subtle taper, they’re only on track by 50T Yen instead of 80T because they’re focussing on yield curve control and we know Kuroda is leaving in April and maybe whoever replaces him is going to change tact. We heard from an ex-deputy Bank of Japan member a few days ago – Owada – who even talked about 10 year yield curve is stupid, because you’re destroying the yield curve for banks, let’s just out the 5 year and give them some steepness of the curve. Well you see a sharp selloff in 10 year, 20 year, 40 year Japanese paper, it’s not going to just be in Japan, it’s going to filter through interest rates throughout the world. I guess we’re sort of paining a scenario where you can get a long term rise in interest rates globally and not for a good reason. It’s for the reasons of the reversal of extreme monetary policy that’s sort of blowing up and central banks are losing control of interest rates on the longer end, which is probably their biggest fear.

FRA: We were under the impression that the Swiss National Bank was doing this for the reason of lowering the currency rate, especially in the Euro-Swiss cross in terms of what that is, but in July that cross rate was making 30 month highs and even then the Swiss National Bank was still buying. Are there any other reasons that they might be continuing to do this?

YRA HARRIS: I just think that they don’t have an action plan. This has been going on and going on because if I’m running the bank, they don’t have to announce it, they’re not under the same mandates as the Fed. I would argue that when I do a weighted average of what they spent to buy in Euros, because the biggest intervention was buying Euros because that’s what they purportedly wanted to do to control the cross rate from appreciating too much in favor of the Swiss, but their average price for all the interventions that they’ve done? They have to be making money on their Euro end, which is unbelievable. You would think that they’d start entering the market. It is interesting that we saw last Friday a substantial move corrective in the Swiss. I thought, hmm, maybe the bank is in. But it didn’t have any staying power. I thought maybe they were coming in and selling their Euros to buy some Swiss back, but now we’re seeing it today – the cross has moved a big way. We’ve gone overnight from 114.5 down to 112.5. It’s a sizable move, but that has to do with the “safe haven” status of the Swiss in the time of Tweetmania from the president and chief, which is ramped up global tensions. So you saw some move there.

We’ll see what that does, but the Swiss… it begs the question, do any of these central banks really have an end to this? It’s really interesting that the Fed went that route, but of course Yellen gave us the ‘relatively soon’ comment in the FOMC in the last statement. ‘Relatively soon’, I’m not sure what that ‘relatively soon’ means. Peter, I have to agree with him, it’ll probably be in September, that’s what relatively soon means. I was hoping it’d be August just so that from a trader’s standpoint I could see some of the action, but markets are too thin and it’s probably right to hold off. This is what the Swiss are telling me. What do you want? This is what your objective was. Now you’ve gotten there. Even though as we learned, the Swiss did intervene with 20B Swiss of new purchases in July, that just came out on Monday morning. We got to see that. That helped push it, but that wasn’t an astronomical amount cause they’ve done that much, but the movement of 4-5% in that cross rate over the last 2-3 months has been very severe and you would think that if they really had an exit strategy they’d be using it at this time. If everybody wants to buy Euros, then sell them Euros. You’ve got them to go and you can unwind some of this position. But they don’t seem to be doing that, so it really causes the question, what is the real objective?

PETER BOOCKVAR: The analogy I give is, to make war analogy, this is like Vietnam for these central banks. Rewind to the mid-60s when the war first started, it was gung ho and we’re going to win and cutting rates and QE and all this, and all of a sudden they realize they’re not really hitting their objectives. Inflation is below their target, growth is not accelerating, let’s just do some more, let’s just send in more troops. And that’s wasn’t enough so let’s send in more troops. And all of a sudden they realize that the war is being lost and they’ve got a full army but they can’t just pull out because the place will collapse. So Nixon wins the presidency in 1968 on okay, we’re going to get out of this war, and the war didn’t end until 1975. It seems like this is sort of what they’ve gotten into.

Just to add on what Yra said, let’s just say they all achieved their objectives. Let’s just say the Eurozone CPI goes to 1.5-2% and the BOJ is successful in generating higher interest rates. Well then what next? You can be sure bond yields won’t be where they are right now; they’d be much higher. The central banks have to get out of what they’ve done. If they create the next recession, if they create the next bond market implosion, was it really all worth it? They’re only good at getting in, and I can’t imagine what will happen if they reach their objectives or now try to get out. There’s no foresight. If you’re a company executive, if these central bankers were company executives, they would’ve been fired ages ago. No director would allow a CEO to remain in place, doing the same thing year after year after year with no results. As any government official, since there’s not really much accountability, they unfortunately get to do what they want, with the consequences to be felt later.

YRA HARRIS: It’s such a great analogy, and fits so well with David Halberstam’s great book of that period, The Best and the Brightest. When you listen to financial media all day and read the papers, they view that every central banker is the best and the brightest. Well, we saw the mess that they’ve got us into, the best and the brightest so to speak, with their models. Of course, those were also rational actor models, the same we’re seeing today in North Korea because the post-WWII period has been built on rational models. We won’t have a nuclear catastrophe because the actors are rational. Which is what economics is based on, and their economic theories and the modelling is based on rational responses. Those are the assumptions that all these models make, that consumers investors savers, everyone do things rationally. We certainly learned that in 2007. Peter’s allegory with the Vietnam War is right, we’re doing more, more, more because they don’t know. Of course the fallback for policy makers, as Peter points out, is counterfactual. I can’t argue with counterfactual, but you’ll be gone when everybody has to unwind this. It’s like Jack Welch running GE – it was great until the classes he built to withstand the 2007-2007 got tested and we see the outcome of GE today. It’s a stagnant, do nothing stock that’s a stagnant investment.

There’s so much yet to play out. That’s why the Swiss model is very interesting. If anyone should be extricating themselves, it should be the Swiss. They’ve purportedly done whatever they needed to do, they’ve been successful, and they’ve made nothing but profits and the world has accepted it. We’ve talked about it on this show plenty of times, it still boggles my mind because I’m still trying to figure out who in their right mind purchases Swiss Francs. Who’s the buyer?

PETER BOOCKVAR: Imagine what happens with them is, they sit around their table at their office at the Swiss National Bank and say it’s time to start backing away, and then all of a sudden you see the Swiss Franc rally and then what do they do? Then it becomes, forget about Vietnam, it becomes Afghanistan. Pull out and the bad guys are going to fill the vacuum, and then we’ve got to get back in again. They’re just trapped; they’re all trapped and they’ve trapped themselves.

YRA HARRIS: I agree with that 100%. And their language is the same – when you listen to Draghi, it’s like he’s just quoting from the FOMC statement. And the Japanese? It’s longer but it’s the same sell. And now Peter talks about it too: this yield curve control, this YCC, has been an absolute disaster because it was meant to steepen the curve. The Japanese curve is at 16 basis points, far from steep, it’s very flat. They’ve failed on every metric, and the currency really hasn’t done anything because of turmoil in the world and of course huge Japanese repatriation of money whenever they so desire because they have so much. They’re like Britain in the 1800s; they’ve got so much money invested all over the world that any time they decide to bring it home it boosts the Yen up.

PETER BOOCKVAR: You have the Japanese Bank TOPIX index, which if the banks were the transmission mechanism for monetary policy, and it’s up to the banks to increase lending and jumps start the economy, well the Japanese Bank stock index is 20% below its peak of 2015.

YRA HARRIS: I know, because I own the individual ones. Between the dividends, it’s been okay; it was a parking spot for me. They’ve had a few ups here and there, but there’s no way that’s a success because those bank stocks would be extraordinarily higher. If you look at the 20 year chart you would gag. If you look at it over 30 years you’re not close to even, and there’s nothing in sight. You look at everything the Bank of Japan has done – disaster. The JJB market is the second largest debt market in the world after the US, and there’s days it doesn’t trade. Imagine that; it does not trade.

PETER BOOCKVAR: There was an article the other day that the Japanese 10 year JJB trades at about 900M a day. The US around 7-11 year traded at 80B a day.

YRA HARRIS: They’ve trapped everyone with them. Now they own so much stock. It was interesting, I was listening to Jamie Dimon talk about how he buys Japanese stocks because the government pension and investment fund, cause they kind of follow their lead because they’re doing all this work behind quality companies, but they’re in a race with the BOJ. The BOJ is buying so much equity that in 4-5 years they would own 70% of the ETF market. What is that? It is absolute insanity and the Swiss show us there’s no way out. They don’t even know how the end the insanity.

Which leads you to where the trading situation is: the markets are very low, volatile, and people are getting paid to sell their premium and that’s what scares me more than anything. It’s not just risk parity traders like AQR and Bridgewater, it’s everyone that follows them buy, because as their models crush the volatility in the markets, everyone’s forced into a short situation. I think there’s so much more risk out there that if equity markets started to correct for whatever reason, and the bonds went with them. For a while last year we had equity markets dropping with bond yields rising, so that was like death for them. I harken back to long term capital – when everyone thinks they know the risk, it’s far bigger because of all the people who are copycatting and mimicking that trade.

FRA: One last question: if we see balance sheet shrinkage by the Federal Reserve and QT, could that result in increased monetary velocity?

PETER BOOCKVAR: That’s a great question. Considering that QE has resulted in the exact opposite, I think eventually. I don’t think immediately. I think that asset price bubble will be pricked when QT begins, along with maybe future rate hikes, but it won’t be until the expansion after the next recession that we’ll get that. If what Bullard said was any indication, and he’s a non-voting member, is in the next recession the Fed will put themselves back in the same hole. They’ll cut rates back to zero and they’ll start increasing the size of their balance sheet again, hoping and praying for different results. The question is whether next time around, the market tolerates that. You’d think a lot about QE is psychology. And we always hear about, oh I have no place to put my money, this and that, but QE1 QE2 QE3 because a lot of that money went right back to the central bank and excess results, a lot of the market reaction was psychology. If you get reverse psychology because people realize, oh that central bank put is much further out of the money than I thought, you get this decline in asset prices. The US economy in particular, the only thing keeping it out of recession is the consumer. Capital spending is defunct, yes trade has picked up a little bit, but it’s predominantly the consumer. Consumer spending is also dominated by middle to upper end, and if you get a decline in markets for example, that could change psychology and that alone could put us in recession. The velocity story may not be sold again until the next recession, but that alone may be dependent on how the central bank responds to that, and if they just continue with the same old tools, thinking they’re going to get some sort of different results, then maybe it won’t be reviving any time soon.

I think the next rate hike will be determined by how the market responds to quantitative tightening of September. If the market’s very nonchalant with it and doesn’t really respond and we get to that December meeting, I think the Fed’s going to raise interest rates again because they’re going to be looking at the employment situation in terms of labor markets being tight and anecdotal evidence in terms of wages popping up here and there and the difficulty in workers. Regardless of what you think of the Phillips Curve, it doesn’t matter because the Fed believes in it. Now if the market has a hissy fit or a tantrum after QT begins in September, they’ll obviously not be raising in December. The irony is that the market can rally itself into another rate hike, or it can sell itself off away from another rate hike. I guess it’s pick your poison, then.

YRA HARRIS: I think that’s right. And to follow it up, Richard, with your question, I know if you start down that path, and nobody has a timeline for when it’ll happen, you put all that money back to work into the collateralized repo market, this may fall right in your face and for all the inflation that everyone said wouldn’t be taking place? You might get some real velocity to this money you haven’t had before because it’s been sitting tart. Again, it’s theoretical and we’ve never been here. There’s a lot of theoretics to it and I want to see. I’m with Peter. That’s why I can’t wait for them to start shrinking it just so we can start to test it. Anybody who’s a scientist, you gotta put these theories to work. Let’s find out what’s going to happen. What scares me about the central banks is that they’re so afraid of going down some exit strategy that that’s what’s probably the most unnerving for me now.

Transcript by: Annie Zhou <a2zhou@ryerson.ca>

LINK HERE to download the podcast in MP3

Summary

Today’s Topics Covered:

• The relationship between Quantitative Tightening (QT) and steepening bond yield curves

• Possible volatility moves in the European bond curve if the European Central Bank (ECB) intends on announcing a QT policy

• The Swiss National Bank’s (SNB) purchases of international bonds and equities and the possible consequences of doing so

• The state of the Bank of Japan (BoJ) and the possible consequences of their current economic strategies

• How the Japanese Government Bond market is fairing in comparison to the United States

• The possibility of a balance sheet shrinkage by the Federal Reserve (FR) and what positive or negative outcomes may arise

Quantitative tightening, a term first identified by Peter Boockvar, is a policy in which the Federal Reserve uses to minimize bonds and shrink their balance sheet. Peter and Yra shed light on the relationship between QT and 10 year bond yield curves. Peter explains that long term treasuries are caught in a tug of war between the downward drag in yields because of natural inclinations to flatten the curve and the potential pull upwards as QT begins and bonds are bought less frequently. If the ECB announces QT then there will be a volatile move in the curve. Peter explains that there is a direction central banks are following in which there will be a rise in global long-term interest rates because of the reversal of extreme monetary policy. This outcome will gradually make the central banks lose control of interest rates.

They then discuss the questionable strategies of the Swiss National Bank to control the EUR/Swiss Franc cross rate. At first it was assumed that the SNB was using aggressive monetary policies in order to lower the EUR/Swiss Franc cross rate, but in July that cross rate was making a 30 month high while the SNB was continuing to buy. Yra went as far to question the actual existence of an exit strategy by the Swiss, “..but the Swiss… it begs the question, do any of these central banks really have an end to this?”. He argues that the SNB initially started off by trying to control the cross rate, but now they do not know what they want to do next or how to do it. He also makes an interesting point on how they should be making money on the euros they purchased and that they should be entering markets. Peter agrees with Yra and adds that central banks seem to only be good at getting towards their objectives, but they are not great at planning exit strategies. He explains that a Director for a commercial bank would be let go if he did not produce any results, but a government official does not face the same consequences. A government official can do as he pleases and not worry about detrimental future consequences. Yra states, “When you listen to financial media all day and read the papers, they view that every central banker is the best and the brightest. Well, we saw the mess that they’ve got us into, the best and the brightest so to speak, with their models.”

“Negative interest rates are just a tax, and someone has to eat it. Whether it’s the bank that eats it or they pass it onto a consumer, it’s confiscating wealth. I call it a weapon of mass confiscation. That’s all it is.” – Peter Boockvar

Peter also gave an insightful analogy comparing the SNB with the U.S. government during the Vietnam War. He explains that when the war started in the mid-60s, the U.S. government was overzealous in their pursuit to defeat the North Vietnam armies. In relation to the SNB, they too felt overconfident in their strategies and began cutting rates and using quantitative easing tactics. During the Vietnam War, the U.S. government realized that they were not progressing and decided to send in more troops. Just like the U.S. government, the SNB was not hitting their inflation target and growth was not accelerating and so they were increasing their amount of purchases. The U.S. Army continued to ramp up their reinforcements to Vietnam and eventually realized that the war was being lost and that they could not pull out of Vietnam because the place would collapse. He notes then noted that after Nixon won the presidency in 1968, the Vietnam War still did not end until 1975. He explains that the SNB has gotten themselves into a similar situation where they have already done so much damage to themselves that it cannot be so easily undone.

Peter also makes a great insight on how the SNB trapped themselves in a potentially disastrous situation. He describes a possible scenario where the SNB begins to back away from their tactics, but the Swiss Franc begins to rally. In regard to this scenario he states, “what do they do? Then it becomes, forget about Vietnam, it becomes Afghanistan. Pull out and the bad guys are going to fill the vacuum, and then we’ve got to get back in again. They’re just trapped; they’re all trapped and they’ve trapped themselves.”

They continue by discussing the poor state of the Bank of Japan and the Japanese Bond Market. Yra states that everything the JCB has done is a disaster and now the Japanese government bond market is the 2nd largest debt market next to the United States. He adds that there are days where the Japanese government bond market does not trade. Peter also adds that the Japanese 10 year government bonds are trading $900 million a day while the U.S. market is trading somewhere around $80 billon each day. They both agree that Japan and Switzerland need to figure out better policies and strategies to combat against potential recessions in both economies.

“The BOJ is buying so much equity that in 4-5 years they would own 70% of the ETF market. What is that? It is absolute insanity..” – Yra Harris

Lastly they discuss the possibility of an increase in monetary velocity if the FR is able to shrink their balance sheet through the use of QT. Peter believes that QT will eventually allow for the FR to shrink their balance sheet and the current asset price bubble will pop along with possible future rate hikes. He speculates that this will not happen until the expansion after the next recession. When asked if the market would thereafter tolerate quantitative easing he argues that the market reaction to QE is revolved around the psychology of the U.S. public. Depending on what tools the FR uses this time around will decide how the people react which affects the effectiveness of QE. Peter emphasizes his belief by stating, “If what Bullard said was any indication, and he’s a non-voting member, is in the next recession the Fed will put themselves back in the same hole. They’ll cut rates back to zero and they’ll start increasing the size of their balance sheet again, hoping and praying for different results. The question is whether next time around, the market tolerates that.”

Summary by Daniel Valentin, email address Daniel.Valentin@Ryerson.ca

08/10/2017 - McAlvany Podcast: Is A Cashless Society At The Doorstep? Look To Asia For The Answer

-Is a cashless society at the doorstep? – Look to Asia for the answer

-A dynamic approach to compounding the amount of ounces you own

-Dow at all-time highs…Echo of 1987, 2000 and 2008