12/22/2017 - Nomi Prins: How Central Banks Are Influencing The Financial Markets

“The ‘dark money’ comes from central banks. In essence, central banks ‘print’ money or electronically fabricate money by buying bonds or stocks. They use other tools like adjusting interest rate policy and currency agreements with other central banks to pump liquidity into the financial system.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/15/2017 - Stan Druckenmiller: Central Banks Are Financial World’s “Darth Vader”, Creating Exploding Asset Bubbles

“If I was ‘Darth Vader’ of the financial world and decided I’m going to do this nasty thing and create deflation, I would do exactly what the central banks are doing now” the billionaire told CNBC Tuesday.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/15/2017 - The Roundtable Insight: Dr. Lacy Hunt On The Unintended Consequences Of Federal Reserve Policies

FRA: Hi, welcome to FRA’s Roundtable Insight ..

Today, we have Dr. Lacy Hunt. He’s an internationally recognized economist and the Executive V.P. and Chief Economist of Hoisington Investment Management Company, a firm that manages over $4.5 billion USD and specializing in the management of fixed income accounts for large institutional clients. He also served in the past as Senior Economist for the Federal Reserve Bank of Dallas, where he was a member of the Federal Reserve System Committee on Financial Analysis. Welcome. Dr. Hunt.

Dr. Lacy Hunt: Nice to be with you, Richard.

FRA: Great. I thought we’d have a discussion on a variety of topics relating to the economy and the financial markets. You recently mentioned that you thought this was the worst economic expansion recovery in U.S. history since 1790. Wow. Can you elaborate?

Dr. Lacy Hunt: If you calculate the average growth rate in the expansions since 1790, this is a long-running expansion, but it’s the slowest and in the last 10 years the household sector lagged very, very badly. The rate of growth in real disposable household income per capita is only 0.9 percent per year. And in the last 12 months, we’re up only 0.6 percent per year. So it’s a long-running expansion, but it’s been a poor expansion. There are certainly problems with some of the earlier data, but this appears to be the slowest expansion since the turn of the 18th Century and our households are the main problem for the growth rate lag.

FRA: And do you point a finger for this cause as primarily on the Federal Reserve or do you see structural changes happening to the economy?

Dr. Lacy Hunt: I think that the main element suppressing growth is the heavily leveraged U.S. economy. We have too much public and private debt, and this debt does not generate an income stream for the aggregate economy. As a result of the prolonged indebtedness, which is on the verge of going much higher because of problems in the governmental sector, the economy is now experiencing very poor demographics. We have a baby bust, a household formation bust, and the lowest birth rate since 1937. These demographics are exacerbating the problems because we have too much of the wrong type of debt and thus the velocity of money has been falling since 1997. Velocity this year is only 1.43 percent, which is the lowest since 1949. Furthermore, the debt creates a situation where monetary policy capabilities are asymmetric. In other words, a lot of action is needed to provoke even a muted impact on the economy, whereas the slightest monetary tightening goes a long way in depressing economic activity. So the root cause of this underperformance is extreme indebtedness.

FRA: And what about the Federal Reserve? How has it undermined the economy’s ability to grow?

Dr. Lacy Hunt: The Fed’s most serious mistake was made in the 1990s up until 2006 during which they allowed the private sector to become extremely over-indebted with the wrong type of debt. And, in essence, I think that quantitative easing, through the push for higher stock prices, created more problems than it has solved for the economy. QT caused the corporate executives to switch funds from real capital investments into financial investments through the paying of higher dividends, buying shares of their own companies, and buying back their shares from others. While this type of action does produce a higher stock market; it doesn’t generate a higher standard of living. And so, Federal Reserve policy has not improved the economy, although it certainly has well served components of the economy.

FRA: And due to that do you think that there’s been too much financial investment versus real economy investment in terms of diverting the economic financial resources away from the real economy?

Dr. Lacy Hunt: I think that’s the principal problem. Business debt last year reached a record high relative to GDP. As I said earlier, Fed policies have created a higher stock market but have not generated an improved standard of living. When the Reserve undertook quantitative easing, it was a signal to the corporate executives that the Fed preferred and would protect financial investments. But that meant financial assets were preferred over real side investments. And so QT is intermingling with the growth-depressing effects of too much debt. And the debt levels are getting ready to move substantially higher in our governmental sector. Government debt is already approaching 106 percent of GDP, a record high with the exception of a brief period during World War II. And by 2030, federal debt will be approximately 125 percent of GDP. For a long time, we’ve known about the issues that would inflate the entitlements — such as the prior-mentioned demographic problems — but there is an increasing likelihood that new federal programs with expenditure increases will further accelerate the growth in federal debt. I think there is clear evidence that increases in federal debt at these high levels relative to GDP over any measurable length of time, reduces economic activity. Thus, the multiplier is not a positive but negative figure, or otherwise exactly what economist David Ricardo hypothesized in his 1821 work. I have looked at the relationship between per capita changes in real GDP and government debt per capita and the relationship is negative, not positive. And so, we’re trying to solve an indebtedness problem by taking on more debt. You can get intermittent spurts of economic activity and inflation, but ultimately the debt is a millstone around the economy’s neck.

FRA: So would you say that we have migrated to a sort of financial economy?

Dr. Lacy Hunt: Let me give you a couple of examples. There’s so much liquidity in the financial markets, particularly the stock market, that a lot of the economic news is constructively interpreted even when it’s unconstructive. Virtually the world believes that the United States is experiencing large job gains and the idea that such productivity may be incorrect is hardly considered. But the rate of growth in payroll employment on a 12-month basis peaked at 2.4 percent in early 2015 and for the last 12 months, has sunk to 1.4 percent. What is even more critical — if you look at just the expansions and don’t include the recessions since 1968 – is that the average growth in employment in an expansion year was 1.9 percent. And in the last 12 months, we are half a percentage point under that figure. Yet, given these numbers, there is an erroneous perception that the employment gains are strong. And this view undermines the improvement in the standard of living. And because of the liquidity and the need of some investors to fully participate in the rising stock market, investors tend to overlook other important developments. If we go back to the 12 months ending November of 2015, real average hourly earnings were up about 2.5 percent. And in the latest 12 months, real average hourly earnings gained a miniscule 0.2 percent. The liquidity tends to push the focus away from the more realistic interpretation of the economy for certain types of assets.

However, the weak performance overall and the deceleration in some of the indicators that I just referred to is not unnoticed by the bond market. So, we have a dichotomy in which the stock market is strongly up but the long-term bond yields are down. Now, the short-term yields are up because they are under the control or heavy influence of the Federal Reserve. The Federal Reserve is in the process of raising the short-term rates and winding down their portfolio. They sold 20 billion dollars of government agency securities in October and November, pushing up the short-term rates. Erstwhile, the long-term rates — which look at some of the more important economic fundamentals — are actually declining.

Another element not in the public understanding, since the Federal Reserve no longer produces this sort of monetary analysis, is a very sharp slowdown in the money supply’s rate of growth, bank loans, and within important credit aggregates. Last year, the M2 money supply was up 7 percent. In the latest 12 months, it decelerated to less than 4.5 percent. The rate of growth in bank loans and commercial paper, which topped out on a 12- month basis about 9 percent, is now under 4 percent. So the Fed is raising the short-term rates, reducing the monetary base, and causing a tightening in the financial side of the economy. Some investors understand what is happening and yet it’s not in the general psyche because such monetary analysis is increasingly rare.

However, another more public indicator is the very dramatic flattening of the yield curve. And when the yield curve flattens in such a way, first of all, it’s a symptom that monetary restraint is beginning to bite. Now, the slowdown in money supply growth and the bank credit flattening of the yield curve will occur well before there is any noticeable impact on a broad array of economic indicators or long lags in monetary policy. But when the yield curve starts flattening, that intensifies the effect of the monetary tightening because it takes away or, at the very least, greatly reduces the profitability of the banks and all those that act like banks. Banks make a profit by borrowing short and lending long. When those spreads recede, bank profitability is hurt, particularly for the higher, riskier types of bank loans since not enough spread exists to cover the risk premium. So the banks begin to pull back, further intensifying the restraint pressing on economic growth. To the vast majority of investors, we have an economy that is apparently doing well, but in fact there are elements right beneath the surface that strongly suggest to me that the outlook for 2018 is considerably more guarded than conventional wisdom implies.

FRA: And do you see the potential for an inverted yield curve in the near future?

Dr. Lacy Hunt: I’m not sure that we will have to invert because the economy is so heavily indebted and the velocity of money is its lowest since 1949. Now, a number of people have pointed out that we typically invert before a recession and historically such inversions have been the case most of the time — but not always if you go back far enough in time — and you should since this is not a normal economy. For example, money supply growth since 1900 has averaged about 7 percent per annum, whereas, currently, the rate of growth in M2 is about 36 percent below the long-term average, indicating a very weak growth rate. And the velocity of money is lower than all of the years since 1942 — with the exception of 7 years — and the economy has never been this heavily indebted. And so the yield curve could possibly approach inversion, but it may or may not occur or stay there very long because at that stage of the game, the flattening of the yield curve will greatly intensify all the other effects — the reduction in the reserve, monetary, and credit aggregates, as well as the weakness in velocity. And when this reduction becomes apparent, the Federal Reserve will not be able to reverse gears quickly enough to ameliorate the impact produced upon future economic growth.

FRA: So do you still see a secular low in bond yields on the long into the yield curve remaining in the future sometime?

Dr. Lacy Hunt: The lows have not been seen. The path there will remain extremely volatile. We will have episodes in which the long yields rise. My attitude is that the long yields can go up over the short run for any number of causes. While many elements work out of the system in the long end, yields cannot stay up. When yields go up — especially now that the yield curve is flattening — this intensifies monetary restraint, which puts downward pressure on commodities. This puts upward pressure on the value of the dollar and cuts back on the lending operations. Something I think has been somewhat overlooked in general euphoria over the strength of economic indicators, is the that commercial and industrial loans for all of the banks in the United States are now only up one-tenth of one percent in the last 12 months. There are forward-looking elements that have historically been very important for signaling that change is ahead. They don’t tell us the timing — timing is always difficult — but they are flashing signals that should be observed.

FRA: And as this plays out, do you see monetary policy and fiscal policy is changing, like will we get fiscal policy stimulus? Will there be a change in monetary policy and how will that look like?

Dr. Lacy Hunt: Here’s my attitude: the new federal initiatives, whether tax cuts or infrastructure or otherwise will not provide a boost to the economy if they are funded with increases in debt — that’s where we’re at. And by the way, it’s been that way for some time. If you go back to 2009, we had a one-trillion-dollar stimulus package that was said to be inflationary and was going to boost economic growth, but yet we still had this very poor expansion and little inflation except for intermittent bouts here and there, largely from highly-priced inelastic goods. All the while, the inflation rate has trended lower.

For example, when President Reagan cut taxes, government debt was 31 percent of GDP and now that’s 106 percent on its way to 120-125 percent. And so if you go back and if you read Ricardo’s great article in 1821, he was asked whether it made a difference as to whether the Napoleonic wars were financed by taxes or by borrowing. Ricardo said that, theoretically, either way private sector activity was going to be suppressed. Now we have a lot of evidence, including some that I produced, that the government multiplier is negative, not positive, over a three-year period. Thus, the tax cuts may work for a very short while, but not on balance. And if the tax cuts were revenue-neutral and financed by reductions in government expenditures that would be a positive since the evidence shows tax multipliers are more favorable than expenditure multipliers. Such a theoretical proposal would provide greater efficiency for private sector spending and government spending. There’s also evidence that you would lower the cost of capital, but that’s not what we’re talking about is it? We’re talking about a debt-financed tax cut and we’re not talking about a revenue-neutral infrastructure plan, just as we were not talking about a revenue-neutral stimulus package in 2009. We’re talking about the debt-financed variety of tax cuts and at this stage of the game, this will make us more vulnerable, except for a few fleeting instances.

I will say this: when you have a debt-financed infrastructure program or tax cut, there will be pockets within the economy that will benefit, but the aggregate economic performance will not benefit and so fiscal policy, as I see it, is not really going to be helpful. The risk is that the debt buildup will add to the problems. There is extensive academic research indicating that when government debt rises above 90 percent of GDP for more than five years, this trend will reduce the economy’s growth rate by a third. Remember, we’re at 106 percent debt to GDP and there’s evidence these higher levels of debt have a non-linear effect. In other words, we use up growth at a faster pace. And there’s a lot of evidence from the available data that we’re even losing a half of our growth rate from the trend. For example, GDP has risen at 2.1 percent per capita since 1790. The latest 10 years produced a reduction to 1.0 percent. And so we should have lost only seven-tenths or come down at 1.3 over 1 but we didn’t and this is a consequence that we have to deal with. We’re not in a position to ignore the debt levels. Fiscal policy can be talked about, we can debate about it, and we can proclaim its benefits, but I don’t see them in the current environment just as I didn’t see them in 2009. I would change my tune if they were revenue-neutral, but that’s not the issue here.

To me, inflation is a money-price-wage spiral not a wage-price spiral as with the Phillips curve. The way inflations begin is by money supply growth acceleration not being offset by weakness in velocity, which shifts the aggregate demand curve inward. Remember, the aggregate demand curve is equal to money times the velocity by algebraic substitution as evidenced in all the leading textbooks on macroeconomics. So you have declines in the money supply and velocity, which will make the aggregate demand curve shift inward over time. This shift gives you a lower price level and a lower level of real GDP. It doesn’t happen every quarter or even every year, but it’s the basic trend. Thus, monetary policy is in the process not of decelerating money supply growth and by a significant amount. If the Fed adheres to their schedule of quantitative tightening, I calculate M2 will grow by the end of the first quarter – it’s currently running around four and a half percent – and the year over year growth rate will be down to less than 3 percent. And so monetary policy is taking steps to lower the reserve monetary and credit aggregates, and these actions will further flatten the curve because they can press the short rates upward. But I think the long-term investors will understand that the inflationary prospects on a fundamental basis are weakening not strengthening.

FRA: And do you see these trends as being exacerbated on the emerging government pension fund crisis? Could there be more debt used to solve that like for bailouts? Do you see that potentially happening?

Dr. Lacy Hunt: Well the main problem with government debt is that we’re going to have approximately one million folks a year reach age 70 in the next 14 to 15 years and we’ve known that this was coming, but we didn’t prepare for it. We’ve made a lot of promises under Social Security Medicare and the Affordable Care Act and government debt will have to be used to fund the entitlement benefits — I don’t see any other way around it. Another overlooked problem is that the actual federal fiscal situation is much worse than these surface numbers. For example, in the last three years, the budget deficit worsened each year. If you sum the budget deficits for 2015, 2016 and 2017, the sum is 1.2 trillion, but a lot of what was previously called “outlays” have been moved off budget — we call them investments (such as student loans) and there are other examples. The actual increase in federal debt in the last three years is 3.2 trillion. So the budget deficit is actually greatly understating what is happening to the level of federal debt which wasn’t always the case. Furthermore, the deficit was made worse by a 2015 bipartisan deal between Congress and the White House. And while neither party is blameless — they both agreed on the deal — yet it doesn’t change the fact that the federal situation is deteriorating and at a much worse rate than the deficit numbers themselves indicate.

FRA: And what about for state and local jurisdiction locales, in terms of their government pension funds? Could there be federal level bailouts at that level?

Dr. Lacy Hunt: Again, what are they going to bail them out with? You’re going to have to sell Federal Securities. And one of the multipliers on new sales of Federal debt is negative, not positive. Forget what was taught you in your macroeconomic class 30, 20, or even 15 years ago. When I was in graduate school, I was taught that the government multiplier was somewhere between four and five percent. Now, it looks like the multiplier is at best zero and even possibly slightly negative.

FRA: Great insight as always. How can our listeners learn more about your work, Dr. Hunt?

Dr. Lacy Hunt: We put out a quarterly letter as a public service. Write to us at hoisingtonmgt.com and we’ll put your name on the subscription list. We don’t spam you with marketing so please go ahead and subscribe.

FRA: Okay, great. Thank you very much for being on the Program, Dr. Hunt. Thank you.

Dr. Lacy Hunt: My pleasure Richard. Nice to be with you.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/15/2017 - The Roundtable Insight: Yra Harris Sees The Swiss Franc As The Oldest Cryptocurrency

FRA: Hi, welcome to FRA’s Roundtable Insight .. Today we have Yra Harris. He is an independent floor trader, successful hedge fund manager, a global macro consultant trading foreign currencies, bonds, commodities and equities for over 40 years. He was also the CME director from 1997-2003.

Welcome Yra.

YRA HARRIS: Thank you Richard. It’s good to be back with you – It’s been a while.

FRA: Great. I thought today we would start off our discussion with Janet Yellen’s presentation and her statements – Your thoughts?

YRA HARRIS: Well, the conference went just as I thought it would be. Of course, as usual, she handled herself well. She discussed some certain issues, but didn’t give much away. And more importantly she didn’t trap her successor, Jay Powell, to any type of situation. She has been gracious and thoughtful and so she continued in that vein. She didn’t really tell us much. Again, she was struggling to understand the lack of inflation and that will continue to plague her because they just don’t truly understand where the inflation is as the Fed measures it. That’s all we have to go in is the way they measure it. How any of the rest of us measure it at this point in time really is meaningless because we’re not driving the markets in that regard.

FRA: Did she set any expectations for future interest rate hikes?

YRA HARRIS: I’m not sure, maybe a couple, she was kind of reticent. I heard one of the media economists talking about it today saying that Greenspan understood with the technological innovation, going back to 1996, that he thought it was going to have an impact on supply-enhanced growth period so he was reticent to raise interest rates and that was a good thing. But every Austrian economist I know worth their weight and those who are not in the Neo-Keynesian new model will tell you that that was exactly what caused all the problems, was that Greenspan was reticent to raise all the rates even though the return on capital was rising significantly. And that’s when you need to start raising rates because then you head off any type of excess capacity developments which of course we saw by 1997-1998, we had a massive overcapacity situation which started the Asian Contagion. She is kind of settled with this too because she talked about that with the tax cut and the fiscal policy today which was good, not in any type of derogatory way, but she is worried about maybe the increase in debt, but she’s hoping that if this tax cut is stimulative it will be supply-side leaning and we will get greater productivity growth which she said would be the good type of growth that she wants.

So we will see.

FRA: What about the U.S. yield curve? Do you see continued flattening of the yield curve or potential inversion going into next year?

YRA HARRIS: Well again, they tried to pin her on that new version. People have to be specific. I am using the 2-10 yield curve. When the 2-10 inverts, there is danger ahead for a lot of asset classes. People will say, “Well, not so fast”, but I will be the first one to tell you because I’ve looked at this for 35 years as part of my trading paradigm that I developed for myself and I can’t time it. I have a study here that was done in 2003, it is right here I keep it in my drawer and it’s exactly on this. It was done by an intern of mine who is very highly qualified and it was written in July of 2004 titled, An Investigation into the Relationship between Changes in Yield Curve and the Performance of Stock Indices. So we’ve looked at this. It is so difficult to time. I can’t tell you when the results going to be, but I’m going to tell you just like in 2007 when then yield curve inverted, it was only by 6 basis points, we know what followed. In 2000, the yield curve inverted, we know what happened then. In 1979-1981, of course that was a forced inversion by Volcker as he was ringing inflation out of the system, but we know what happened then. This time, I can’t tell you. We’ve discussed this, you and I, for quite a while. We’ve been right in many ways about it and I’ve warned with what the central banks are doing that this is a wild card. I can’t tell you what the impact is going to be. It was interesting when Yellen discussed the yield curve today. She didn’t talk about the effects from other central banks and I think that’s a huge part of the flattening that is going on.

FRA: Yes. And about that…Do you see the ECB, Bank of England and Bank of Japan having their yield curves affected?

YRA HARRIS: Well for the Bank of Japan, Kuroda tried to give us a different spin on it thinking that maybe they were going to put an end to it, but as soon as the dollar/Yen softened off of that, I forget what the exact phrase was, it was from a speech in Switzerland in mid-November where he used certain language that spooked the market, but then he walked it back of course. You see that the dollar/Yen got weak today and then dollar really fell off after the Fed’s action. Tomorrow (Thursday, December 14th, 2017) we have an ECB meeting, an SNB meeting, Bank of England meeting and the Bank of Mexico – They are all in play here. I think Kuroda’s term that he used in November was reversal rate. It was a new term. We hadn’t heard it and myself included. I thought maybe they are thinking about ways that they can finally start to get out of this, but then he walked that back. They’re not going anywhere. And as I was talking with Rick Santelli the other day, I wasn’t on T.V. with him, but I had a tea and he had a cup of coffee and we were just talking about that and it’s different, unlike the U.S., when the U.S. started down the path of tapering when Bernanke stopped being afraid of his own shadow and stopped being plagued by the Taper tantrum and they actually announced how they were going to do it, it was a monthly reduction in the amount of what they were going to purchase and they were going to end it over in less than a year. They went from $85 billion to zero, where they weren’t purchasing any new stuff, in a fairly quick period, but the market new what they were going to do. The ECB is totally different. We know that they are cutting from $60 billion to 30 billion starting January 1st, but they’re not reducing it after that. So Draghi is going to be buying $30 billion instead of 60 billion, but he has already told us he is extending it out to September. So we know we are going to get $270 billion new buying with whatever else they are buying in Europe all of next year. And the Bank of Japan does have some latitude there because of the yield curve control. There is not change coming. I think Draghi has a very grave problem on his hands. You saw it today where the Italian bonds actually got hit even with whatever they are buying because now we know there is going to be an Italian election on March 4th and this is going to be a very contentious election because right now the polls have the Lega Nord and Five Star Movement leading. So this market knows there is an election coming. But more importantly for Draghi is Merkel, And Richard you and I have talked about this before the election that she is not going to be as strong – And she’s not. She is very weakened right now and the German elites, the nomenclature or the thinkers, are so afraid of a new election, but meanwhile it is 3 months’ time from the election and no new governments have been formed yet. It’s a caretaker government. And Merkel offered, because she was pressured to do so, the SPD (Social Democratic Party of Germany), who swore that they weren’t going to go into coalition and now they’re negotiating for coalition, but she’s phenomenally weakened. This is a very important thing for Draghi because she has been his bodyguard. Whatever he wanted to do, Merkel was willing to deflect criticism. Now that she’s in such a weakened state with the Italian elections, he’s in no position to do anymore tightening or hawkish statements. I’m looking for tomorrow to be excessively dovish.

FRA: Any updates on the gold currency cross exchange rate you’ve written about recently that gold is being restrained from positive real yields?

YRA HARRIS: Right now, the 2 year yields dropped a little bit today, so we’ve about neutral right now using the 2 year on inflation. Real yields are probably about zero, but global real yields are exceedingly negative. That’s why I said gold will perform well against all currencies because global short-term real yields are very negative. In the U.S. they are neutral, but the interesting thing is the dollar is not getting a bit. This defies most things that anybody has looked at this and traded on it and analyzed it. The United States dollar should be screaming right now based on what we saw during the Reagan years because you’re getting a fiscal stimulus package via tax reform and rising interest rates. These are two variables that are very positive for currency and yet nothing. This is really starting to get interesting and forcing me to think because something is wrong here.

FRA: And today Yellen made some statements about Bitcoin, everybody is talking about Bitcoin. She mentions it is not legal tender – Your thoughts?

YRA HARRIS: Well it’s not legal tender, but it definitely should be legal tender. We have talked about Bitcoin before and again I’m far more interested and I’m on record for over a year saying that I’m more interested in the blockchain technology and the concept of it buying Bitcoin, to my own detriment, but I’m with guys like Druckenmiller – I can only trade what I understand. I went through the dot-com bubble and I couldn’t understand them. I didn’t understand when people were talking about burn rates of money and my common response was that I’m a child of middleclass parents – We don’t burn money…You’re going to have to help me better than this. So I’m watching it and it’s intriguing. I wonder whether it’s going to affect gold. Some people think it affects gold because it moves potential gold buyers into another alternative, but as I wrote last week, hell has frozen over when I find myself in agreement with Alan Greenspan. Greenspan just didn’t understand and you cannot create value out of nothing. I know tech people tell me that it’s not nothing and that there is a process here that we can probably find in David Ricardo’s labour theory of value. You have to mine it so there is some value, but I agree with Greenspan about that where you just cannot create value out of nothing although I would’ve asked him the question…Then that would make the Swiss Franc the oldest cryptocurrency in the world because it’s so secretive, so if that’s the definition of crypto is being secretive and basically finding it under the radar. They’ve been doing this for a long time and we’ve watched them for 3 years create value out of nothing by printing Swiss Francs so I’m voting the Swiss Franc as the cryptocurrency of the year. If you actually look at the SNB stock price, it almost mirrors that of Bitcoin – It’s such a dramatic rise this year.

FRA: Do you think that a government-based digital currency or cryptocurrency, if we can call it that, will allow private-based cryptocurrencies like Bitcoin and others to coexist?

YRA HARRIS: I really can’t answer that. Janet Yellen was very good in her answer when somebody asked her if the Feds are looking into it and she said, “Other central banks are. When we said we are looking at it, are people doing research? Yes. But we are looking at digitized money, not cryptocurrencies and there’s a big difference.” And she was very good at explaining that difference. I think that we are going to get digitized currencies…Why? Because people like Larry Summers, Kenneth Rogoff and others have wanted to get electronic money because then they would have greater control over what you and I do. So when you go to financial repression rather than us pulling our money out of the system and hoarding it, they would force us to use an electronic currency which they can control. Then they would hope they can restore velocity to the money which is why Larry Summers said to get rid of the $100 bill because it’s much harder to hoard currencies with smaller denominations because if you’re hiding them under your mattress, it doesn’t take that much money to give you sleepless nights. You can only hold so much currency in smaller denominations.

FRA: And to allow for easier implementation of negative interest rates through monetary policy.

YRA HARRIS: Yeah. Marvin Goodfriend, who has written very extensionally on negative interest rates, that’s right because that’s the whole thing. I’m going to go to negative interest rates and I’m going to force you to keep your money in the system rather than anyone with a brain says, “Negative interest rates? I’m going to pull my money out of the bank.” Because if you have negative interest rates for 10 years and we’re at -2%, I’m going to lose 20% of the value of my currency. Then people pull it out of the bank and do other things with it such as investing in gold and other things. It gets very interesting.

FRA: Exactly. And finally, I’m just wondering about your thoughts on the geopolitical scene in terms of Saudi Arabia and Russia with what’s happening in Saudi Arabia and any new developments on meetings and more discussions between Saudi Arabia and Russia.

YRA HARRIS: I have looked at this for quite a while and I stated the last time around that there was major event that took place on October 4th and that’s when the Saudi King, not the crowned prince, Mohammad Bin Salman, the king himself went to Russia for the first time ever. I’m always interested in the events that are first-time-evers because there is always a reason for it. Dixon going to China was amazing event. So the king went to Russia. On those two days he was there, oil traded down to about 49 dollars and then over the next 8 weeks it went all the way up to about 60 dollars. Is this happenstance? No, I don’t think so. I think that major shifts are taking place in the world. You’re seeing it in the mid-east, and Russia is very involved with this because the Obama administration leaped them into a bigger role in Syria which has now given them the primary role. So there are all types of things that are taking place. There are shifting sands, no pun intended, and we have to pay attention.

FRA: Great insight Yra as always. How can our listeners learn more about your work?

YRA HARRIS: You can go to YraGHarris.com and Notes from Underground, which is where I blog, will pop up. They can follow me and register to receive it for the very expensive price of free. And again I don’t talk trades to people, I try to explain to you where I think the next opportunities are going to be from a trader’s perspective because I always have to wear two hats: as a trader and as an investor. And they are radically different.

FRA: Great. Thank you very much Yra for being on the program show again. Thank you.

YRA HARRIS: Well Richard, at this time we’re in I hope I was able to “shed some light”.

Transcript written by: Daniel Valentin <daniel.valentin@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/11/2017 - Russia & Other Oil Producers To Create Oil-Backed Government Cryptocurrencies?

“The gradual acceptance of digital currencies, with major exchanges about to launch bitcoin futures trading, may prompt some oil producing nations to ditch the US dollar in crude trade in favor of cryptocurrencies, an oil analyst says.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/11/2017 - Forbes: What Is Financial Repression?

“Stanford economists Edward S. Shaw and Ronald I. McKinnon coined this term. In short, it means governments essentially use the private sector to service debt ..

Financial repression is also useful for governments to control capital and have its citizens consume the bulk of domestic government debt.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/07/2017 - Bill Gross: When Credit Risks Increase, Creditors Increase Preference For Classical Money And The Financial System Can Be At Risk

“High-quality credit can at times take the place of money when its liquidity, perceived return, and safety of principal allow for its substitution.

When the possibility of default increases and/or the real return on credit or liquidity decreases and persuades creditors to hold classical ‘money’ (cash, gold, bitcoin), then the financial system as we know it can be at risk (insurance companies, banks, mutual funds, etc.) as credit shrinks and ‘money’ increases, creating liquidity concerns.

Someone asked me recently what would happen if the Fed could just tell the Treasury that they ripped up their $4 trillion of T-bonds and mortgages.

Just Fugetaboutit! I responded that that is what they are effectively doing. “Just pay us the interest”, the Fed says, “and oh, by the way, we’ll remit all of that interest to you at the end of the year”.

Money for nothing – The Treasury issuing debt for free. No need to pay down debt unless it creates inflation. For now, it is not. Probably later.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/06/2017 - Martin Armstrong: Bitcoin To Be Declared A Financial Institution To Avoid Currency Competition With Government Currency and Government Cryptocurrency

“Now comes Bitcoin. The Judiciary Committee of the United States Senate is currently working on Bill S.1241 that aims to criminalize deliberate concealment of property or the control of a financial account. The bill was submitted in June, and the law would change the definition of ‘financial account’ and ‘financial institution,’ and thus also cover digital currencies and digital exchanges. Who is pushing it? None other than California’s Senator Dianne Feinstein, who maintains that the bill is needed to update existing money laundering laws because of terrorists.

This means that the miners of Bitcoin will become a ‘bank,’ .. .

.. They can shut down Bitcoin in the blink of an eye by simply defining anyone who is a miner to be a financial institution.

The bill will change the definition of “financial institution” in Section 53412 (a) of Title 31 , United States Code. The text will read:

“An exhibitor, a redeemer or a cashier of prepaid access devices, digital currency or a digital exchanger or a digital currency.”

The regulation will remove the anonymity of Bitcoin and other cryptocurrencies defeating this idea that there is an alternative-financial-universe separate from government.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/04/2017 - India, Turkey, South Korea, Netherlands, France, UK, U.S. Governments Begin To Crack Down On Bitcoin And Cryptocurrencies

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/04/2017 - Danielle DiMartino Booth: Governments Will Not Allow Private-based Cryptocurrencies To Co-Exist Alongside Government-based Cryptocurrencies

FRA: But would governments necessarily allow private-based cryptocurrencies to coexist with government-based cryptocurrencies?

Danielle DiMartino Booth: I would have to say no. What we have seen with the parabolic thousand point increase, and we are at a thousand points at 8:26pm EST on November 29th, Bitcoin crossed the $10,000 mark and it didn’t even take it 12 hours to go across the $11,000 dollar mark. What we are witnessing is clearly a bubble that is going to implode on its own weight. I think that we can all hopefully agree on that; we are all adults in the room. But I think that central bankers know good and well that once these cryptocurrency bubbles burst, laying in their wake will be a very refined technology that allows central bank cryptocurrencies to rise up where they have left off. To your question, do I think that they will be allowed to coexist? – I think not.

FRA: So you see a phasing out or an abolishing of Bitcoin and other types of private-based cryptocurrencies?

Danielle DiMartino Booth: I hate to inflammatory words like abolishing, but you could certainly see a sequence of events whereby if the Bitcoin bubble ends up bleeding into other overvalued asset classes that then bleed into an economic contraction leading to recession, and then causing the central banks of the world, starting with the Fed, to go back to the zero-bounded interest rates. Once we get to that point, and I hope we don’t, I hope that our new chairman, Jay Powell, is going to say, “You know what, zero-interest rates didn’t work. We are not going to go back there.” But if we get to the point where we are back to zero-interest rates or worse, negative interest rates, the next logical step for central bankers is the eradication of cash and controlling our buying which can only really be done electronically with this emerging cryptocurrency technology.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/04/2017 - Charles Hugh Smith: “The Fear By A Lot Of People Is Governments Issue Their Own Cryptocurrencies Or Governments Try To Ban Existing Cryptocurrencies”

“The fear on a lot of people’s part is that the central banks and central governments are not going to just stand still. They’re either going to issue their own blockchain currency and require their citizens to use only that Cryptocurrency or that they will try to ban or outlaw the existing Cryptocurrencies as an extension of the financial repression.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/04/2017 - The UK Will Regulate Bitcoin And Other Cryptocurrencies

“The UK Treasury has now said it intends to begin regulating the virtual currency, which has a total value of £145 billion, to bring it in line with rules on anti-money laundering and counter-terrorism financial legislation.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/04/2017 - The Federal Reserve Warns Private-based Cryptocurrencies Could “Pose Serious Financial Stability Issues”

The Federal Reserve’s Vice Chariman of supervision, Randy Quarles, warns that digital currencies like Bitcoin pose “serious financial stability issues” as they grow… “Today, the vast majority of our payments by volume and value are processed by regulated financial institutions. In the U.S. payment system, digital currencies are a niche product that sometimes garners large headlines. While these digital currencies may not pose major concerns at their current levels of use, more serious financial stability issues may result if they achieve wide-scale usage.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/02/2017 - The Roundtable Insight: Charles Hugh Smith Insights On Bitcoin and Cryptocurrencies

FRA: Hi welcome to FRA’s Roundtable Insight .. Today we have Charles Hugh Smith. He’s author, leading global finance blogger and America’s Philosopher. He’s the author of nine books on our economy and society including a Radically Beneficial World Automation Technology and Creating Jobs for All .. Resistance Revolution Liberation, A Model For Positive Change .. and The Nearly Free University & The Emerging Economy. His blog oftwominds.com has logged over 55 million page views in his number seven and CNBC top alternative fine sites. Welcome, Charles.

Charles Hugh Smith: Thank you, Richard. I don’t know if I can live up to that .. but I’m very excited about our topic today.

FRA: Oh yeah. You always do. Always live up. And today we’re talking about Cryptocurrencies. You’ve written a lot about that on your blog, including today as we speak with the potential Bitcoin price as you suggest going to the $17,000 level.

Charles Hugh Smith: Yeah that was my sort of back of the envelope forecast a year or so ago and last summer. You know I want to start out Richard by saying that you know there’s a lot of people have an emotional connection to this topic of Cryptocurrency. A lot of people are extremely skeptical or feel like it’s really not worth anything and certainly not worth you know $10000 per bitcoin and other people are kind of evangelistic about it and super excited about the Blockchain, you know disrupting all of the intermediaries in our financial system. And so I think what we’re going to try to do in our program is to be skeptical of the whole Cryptocurrency movement and be open to the potential benefits that it offers, but not like we’re not going to accept anything just uncritically. We’re going to look at everything .. We’re not going to put our belief structure in either camp either anti-Bitcoin or pro-Bitcoin. we’re just going to look at it as coolly and rationally and as we can and try to understand the value if there is value here.

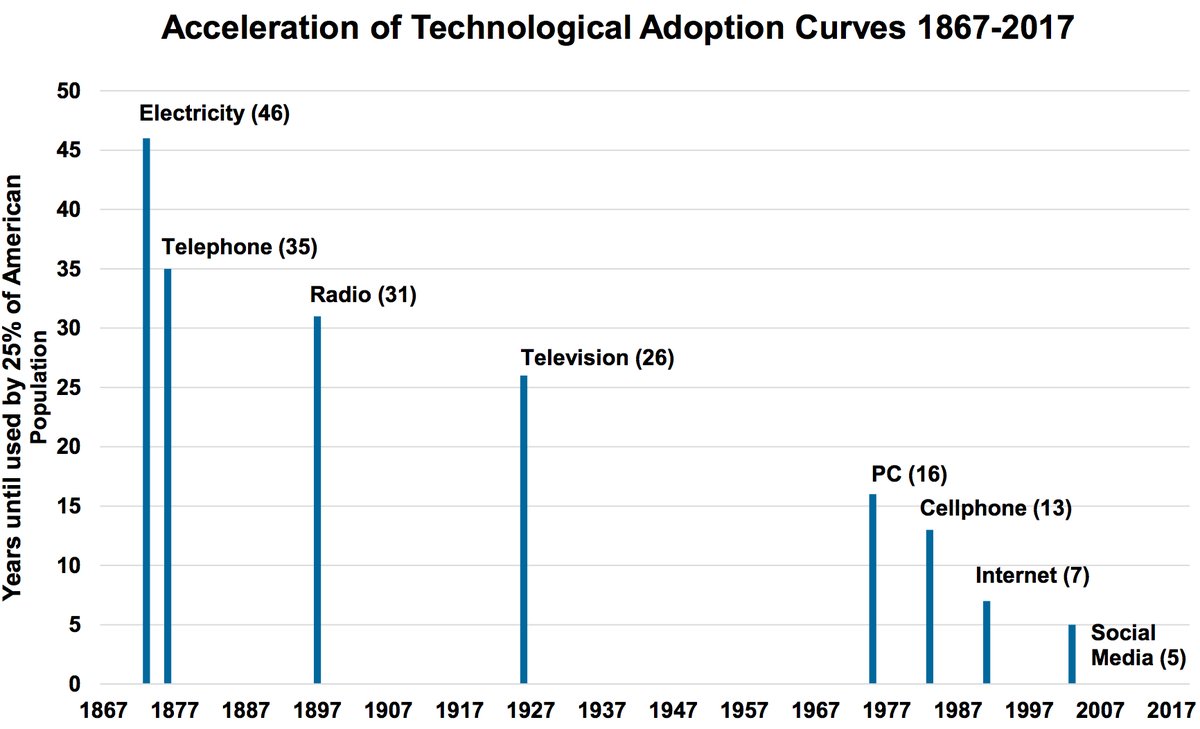

FRA: Excellent. And you’ve provided some charts that we will make available on the website .. maybe we can begin there with the technology adoption curve.

Charles Hugh Smith: Right. And you know it’s it’s almost unbelievable when you think about it, at least it is to me. That the whole Cryptocurrency space is only eight years old. I mean that Bitcoin protocol was released in 2009 and it really didn’t do anything for quite a while, it was kind of a hobby of certain people and Bitcoin trading under a dollar for quite a while and then under $10 for quite a while and then it kind of made a splash in 2013 with the Cyprus bailin .. which was at least one of the triggers that caused Bitcoin to suddenly come out of nowhere and go to about a thousand dollars .. and then various hacks into Bitcoin exchanges caused a complete selloff that drove the price back down into the $200 you know so there was a massive sell off.

But my point is this space is developing very quickly in a lot of different directions that are hard for us amateurs to track. In other words, there’s a proliferation of Cryptocurrencies, but there’s also a lot of development going on .. And then there’s a lot of development of trying to make the transaction rate of Bitcoin faster. You know for instance Bitcoin cash raised a block size from one megabyte to eight megabytes. And this .. was supposed to add a layer on top of Bitcoin that would process transactions much faster. Well that didn’t go because it was withdrawn because of technical difficulties. But you know it’s going to be very difficult to predict where the Cryptocurrency space will be in eight more years. That’s all I’m saying is that there’s a lot of development and innovation going on. And most of it we know will fail or drop away just as the Internet itself proved. But what we’re trying to do is ascertain the core value here. So that whether there will be some winners that will need to develop as as time goes on to meet the needs of people in our financial system .. That’s basically if it meets a need it will it will survive if it doesn’t really meet it. I mean if it doesn’t really have utility then it will fade in and become a novelty.

FRA: Yeah I agree very much with those observations. I mean you have the growth of the block chain based economy that is just massive potential. And then the use of Cryptocurrencies as a payment mechanism for Blockchain based applications and services. Right now there’s about twelve hundred Cryptocurrencies in the universe. And we can see lots of mergers and acquisitions just like what happened in the Internet.com era. Many of those Cryptocurrency is either going out of existence or many of them merging, some acquiring others, so that space could then dwindle down to a very small number of you know of Cryptocurrencies.

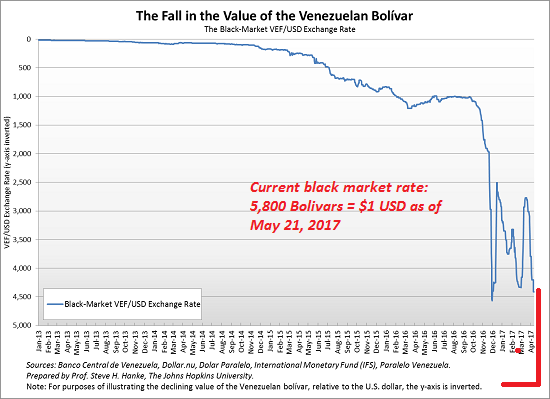

Charles Hugh Smith: Right and one of the other charts I proposed using for our program was a chart of the Venezuelan Bolivar, the national currency of Venezuela. And of course as we all know it used to trade about 10 to 1, in terms of the Bolivar to the U.S. dollar. And now last time I checked which was a few months ago it was trading around 6000 Bolivar to the dollar on the black market. So this currency is as experienced what we call, you know you can call it hyperinflation or a tremendous loss of purchasing power. That’s just basically destroyed the wealth of everybody holding Bolivar right. And so this is what we’re all concerned about with Fiat currencies. You know currencies that are created by Central Banks or national governments and that can be created without any restraints. And so this is what I think part of what’s driving the interest in Bitcoin and the Cryptocurrencies is what other financial mechanism is available to people who are trying to preserve their capital when their own national currencies are in free-fall.

FRA: Yeah exactly. Just recently there’s been a couple of quotes. One from Mike Novogratz on Bitcoin and one from Danielle DiMartino Booth on Bitcoin. And I would just like to read you that that. Mike says “this whole revolution came out of a breakdown of trust. It came out of the ’08 financial crisis when people said we no longer trust financial institutions, we don’t trust governments and in parts of the world today still. If you’re in Venezuela, it’s really hard to trust a Central Bank or in Zimbabwe. So the de-centralized revolution was Bitcoin is really the poster child of a response to the breakdown in trust.” And Danielle DiMartino Booth who is a former Federal Reserve Adviser to the Dallas Federal Reserve President, she mentions that “Bitcoin is a reflection of panic. It’s a reflection of people trying to get into a safe place knowing the major governments of the developed world have got their printing presses running 24 by 7. It’s a reflection of anxiety and fiat currencies and the fact it’s not practical to go back to a gold standard. What scares me most about Bitcoin, if the central bankers are studying it to figure out how the blockchain works. They are going to be controlling our spending with blockchain technology that is being perfected in the Cryptocurrency universe.” Comments?

Charles Hugh Smith: Wow. Yeah I think that those two, you chose quotes very wisely because those express very widely held views that you know we’ve all seen expressed by a number of commentators and observers over the last few years, which is Cryptocurrencies are one of the few avenues that an average person might have to escape the kind of financial repression that you know that you’ve covered in so many programs. In terms of capital controls, bail-ins, expropriations, and massive devaluation of the currencies. You know all these different tricks of financial repression, the elimination of cash. And that’s one of the driving factors, but then the fear on a lot of people’s part is that the central banks and central governments are not going to just stand still. They’re either going to issue their own blockchain currency and require their citizens to use only that Cryptocurrency or that they will try to ban or outlaw the existing Cryptocurrencies as an extension of the financial repression.

FRA: And everybody these days is talking about the price of Bitcoin where is that going .. you mentioned Venezuela on that chart – If we look at the history of the price of Bitcoin .. Going up to sort of the 1000 to 2000-dollar level. A lot of that seems to have coincided with Venezuelans in Venezuela and also Chinese in China looking to get money out of their countries – you know capital outflows and then from there, it seemed to have critical mass taking off to where it is today slightly over $10000 as we speak. Comments on that.

Charles Hugh Smith: Right. Well you know before we started recording you were speaking about the costs of mining Bitcoin and as being one factor in that we could use in its evaluation. And so let’s try to contextualize the discussion about the value of Bitcoin and you know a lot of people feel it should be zero because it’s not backed by anything. And of course then proponents say well there’s nothing backing all these national currencies either, there’s nothing backing the Dollar, the Yuan, the Yen or the Euro either. Which is technically true. And so let’s move on to valuation. One factor that’s in a lot of people refer to Bitcoin in particular as having a big impact on its evaluation is, it’s a scarce entity. In other words, there’s only 21 million Bitcoins that will ever be mined. And beyond that beyond that amount then there will be a fee structure to support the blockchain right. Because currently the whole blockchain is maintained, it’s basically paid for by the issuance of the admittance of new Bitcoins. And I think you had some numbers that you found on the estimates of how much that cost in terms of electricity and computing power to mine one Bitcoin.

FRA: Yeah you know with approximately $1000 US to perhaps $1200 US to mine one bitcoin. And that represents the cost of electricity and computing resources .. It’s similar in the gold world where it costs approximately $500 to $800 per ounce to mine one ounce of gold today. So on that basis, if we look at the value of gold being thirteen hundred dollars today relative to the cost of mining .. Bitcoin could approximately be valued at something like $1500 to $2500 dollars US relative to its mining cost.

Charles Hugh Smith: Right .. And so in that analysis it’s overvalued you know by a factor of four then. Alternatively, we can say in a world where national currencies and central bank currencies are no longer trustworthy because they’ve been created in vast sums and continue to be created to the tune of like $300 billion a month or more. That may be what’s really happening is gold is lagging and this has of course been frustrating to a lot of people who feel that maybe gold should be $5000 an ounce if Bitcoin is $10000, then gold shouldn’t be $1300 it should be $5000 an ounce. And so it may be that gold is lagging and to where it should be. But you know let’s look at the utility value of some of these alternative currencies and I’m including precious metals are the historical safe haven because they have intrinsic value and in the case of silver they have utility value as well. I mean that we all know that silver is not only pretty and a nice thing to make art out of, it’s also a an industrial metal with you know that it’s widely consumed. So we understand the utility value in the store of value of precious metals and then Bitcoin is obviously it’s a different animal because it’s a digital thing and it has no physical presence and no physical utility, but it is quite handy in terms of transferring capital around the world. And I myself have used it to pay editors and translators in other countries and you know there’s no fooling around with bank fees and you don’t have to fill out any of the capital control forms required by the Federal government. And this is of course why a lot of people feel that Bitcoin you know it’s all about money laundering and drug money. But I am just a little regular person here doing my running my little business and I used it to pay other people doing you know legitimate services for me. I file my tax return you know what little gain I made on my Bitcoin transactions .. So you know I think there’s a legitimate utility to the Bitcoin and the Cryptocurrency phase in terms of regular people transacting business globally.

FRA: Yeah sort of the mobility utility factor. And as mentioned earlier that seemed to what happened to propel the price to go from $1 up to $1000-$2000 dollars per Bitcoin. Especially from Venezuelans and Chinese using it .. Now there is a development just in the last month or two that I’d like to mention. That has to do with the Internet protocol of Bitcoin. So most if not all of the Cryptocurrencies are operating over the Internet, over the IP Internet Protocol space and there are technologies coming out now that are able to detect Bitcoin transactions, Bitcoin traffic, even if the traffic is encrypted. This is quite new. As that develops, this will actually make it possible for banks to look at bringing into regulatory oversight the Cryptocurrencies, the traffic that’s coming to and from the banks .. and even governments as well for Bitcoin traffic into and out of countries. So this mobility advantage initially may not hold as much you know, given this technological development. The government of China has long been looking at this on how to do it .. this technology can be used by banks and by governments.

Charles Hugh Smith: Right. And that’s an excellent topic and observation. I wasn’t aware of this technology, but I think what it raises for me is the regulation of the Cryptocurrency space is inevitable in developed economies. You know in other words like this is a normal trend. And frankly I think it’s a good trend in the sense that if you want to legitimize a new form of money it has to be regulated to some degree so that people won’t get ripped off by fraud, like people selling Bitcoin they don’t actually own or you know this kind of thing. And I also think that you know if people are fortunate enough to make you know a million dollars trading Cryptocurrencies, then why shouldn’t they pay the same taxes somebody that was fortunate enough to make a million dollars trading stocks or bonds or future contracts. So I think the advent of regulation is a positive development. And the reason why I say that also is some countries are embracing the Cryptocurrency space and I mentioned Japan which has legalized Bitcoin I mean fully. Right. And of course this is the third largest economy in the world. And South Koreans have basically given a pass. So they’re not going to ban it which is taken as a form of approval .. the U.S. itself has deemed Bitcoin and Cryptocurrencies as commodities. So in other words they are viewed as, if you’re trading Bitcoin – it’s viewed as equivalent to trading pork bellies or something. Right, it’s a commodity. So I think once a country like Japan, with a huge capital market and a vast economy now that it’s legalized the Cryptocurrencies it’s very difficult for other economies to say oh no we’re going to ban this. And I think we have to draw a distinction between common sense regulation of the Cryptocurrency space, like legalizing it and regulating it and taxing it right, as opposed to banning it. And I’m not so sure that banning it is going to work anymore. Because like I’ve explained on my blog a couple of times, if for instance the United States decided to ban Cryptocurrencies Well I could take my Bitcoin and you know my one Bitcoin or whatever and I could put it on a thumb drive or a so-called hard wallet. And then I could take it with me to Japan or I could mail it in a package with some other stuff. And then I could have an associate or friend in Japan you know upload it and deal with it in a legal country. Where they are legal in a legal setting for Cryptocurrencies and then transfer it into yen or dollars in that country where it’s legal to do so and then transfer it back to the U.S. And so you know if I can figure out a really simple workaround. Pretty much anybody can. So I think where a lot of people fear this tracking of Bitcoin and other Cryptocurrencies and then regulating it, is a bad thing. It doesn’t have to be a bad thing. I think it could be a positive development actually.

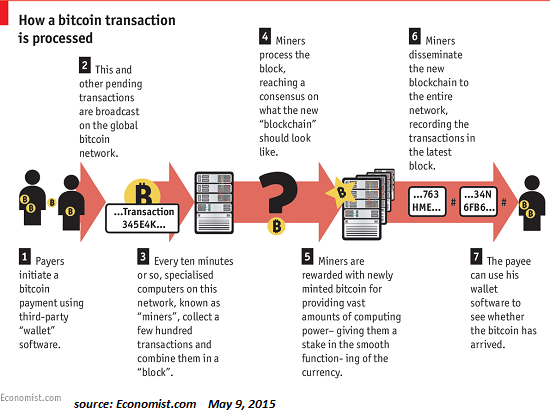

FRA: Yeah and it will accompany the growth in Blockchain services as the economy develops around those based services you know. The concept of an encrypted Excel spreadsheet type of ledger that Blockchain is.

Charles Hugh Smith: That’s right. And I’m glad you described it so succinctly. Because a lot of people are confused by it and that’s really what it is. It’s basically a ledger that’s public so everybody gets to see what’s been entered. And so that’s the utility value. Well you know let’s also talk about, go back to the financial repression part because one thing I’ve started to write about and other people have also started to write about is the possibility that we finally get some inflation. We all know that unofficial inflation, real world inflation, is running a lot hotter than official inflation, but so far the central banks of the world have created you know trillions upon trillions upon trillions of new currency and they’ve injected that into the financial sector. And there’s been only asset inflation. Right. In other words, stock markets have doubled and tripled. And you know bonds have risen in value and real estates gone back up to bubble levels but there hasn’t been a lot of real world inflation and certainly no wage inflation. So if we started to get inflation that’s going to create a real problem for the central banks because they won’t be able to emit in the quantities of currency they’ve been emitting because that will fuel inflation and inflation of course destroys capital, it destroys the savings, it destroys the purchasing power of wages and people actually have less money to spend, less purchasing power. You know also that’s I think another driver for the whole Cryptocurrency space is that if Cryptocurrency is perceived as something that is a store of value based on scarcity, then it becomes an attractive hedge against inflation.

FRA: Exactly that’s a good observation. So where do we go from here. Like what will happen? How do you see the Cryptocurrency space evolving? You know I guess we have private based Cryptocurrency. And then they’ll also be government based Cryptocurrency.

Charles Hugh Smith: Right. Right. And my sense is the value of of Cryptocurrencies like Ethereum and Dash and Bitcoin, in other words, we can call these the leading Cryptocurrencies. The value is that they’re non-state, non-central bank, non-government right. And so I don’t see a Cryptocurrency issued by the Bank of China or the Federal Reserve as having any value because the the control of how much of that Cryptocurrency is emitted, is created, is of course still in the hands of the bank and so on. I think the fear of anybody that is at all skeptical of how government and central banks work, as the central bank and say oh well there’s only going to be 21 million of these coins issued and then the next morning they say Oh well actually we’re going to issue $300 billion and then it’s $300 billion. And then that currency has no value at all. And so I think that we have to kind of specify that the value of Bitcoin is that being decentralized, you can’t change the protocol. No one person or agency can say no we’ve decided to issue $210 billion of Bitcoin. Now it doesn’t work like that. And even if somebody claimed that we’re going to do this to the Bitcoin protocol the miners and everybody, the participants in the Bitcoin ecosystem, they would have to follow along and support that. And if they didn’t support it, then that fork would die and others would just vanish. And so if I declare, hey I’m going to start a new version of Bitcoin that there’s a billion coins and nobody comes along to mind that. In other words, maintain the Blockchain, then my version just dies it goes to zero because there’s nobody to support the Blockchain. So there is a rough and ready very free market kind of democracy, if you will, and a lot of people have criticized Bitcoin because it major miners obviously have a lot more influence than people who are mining as a hobby and so on. And so there are blocks of self-interested people who can dominate these Cryptocurrencies. And that’s a danger for sure. But it’s a lot different than having nine people meet in a room and decide to add a zero to the money. Yeah. And so I think that government and central bank versions of Cryptocurrency are going to go nowhere because they’re not again for the elements you described earlier in the program. There’s really no reason to trust them.

FRA: I mean they may be mandated by governments to use just like you know currencies today of the countries of the world. But I guess with the coexistence with private based Cryptocurrencies, the ones that make sense will be ones that are you know operating within the financial system. Even if they’re outside of the banking system, if you will, but still within the financial system. And the ones that are based on sound money, so that they have limited numbers that they can be printed or perhaps they’re based on a commodity like gold.

Charles Hugh Smith: Right. Right. And I think that you raise an excellent point that what people are seeking is sound money and sound money that has utility. In other words, it’s not just a store of value, but it’s a means of exchange and so there’s certainly a role for the precious metals. And that’s why a lot of people are saying if you’re going to go in terms of recommending a hedge that you should have both precious metals and some Cryptocurrency, you know exposure, even if it’s you know one percent or something. But I think you know I would say we’re sort of an equivalent of the Internet or the the world wide web around 1995. You know so we have it back when the first browser emerges. Right. And Mozilla and all that and all the assumptions that we would have drawn that have all turned out differently. Right now there is like Yahoo was the first for the most asked and and and then Yahoo faded and lost all of its advantages. And so we you know to say where will Bitcoin be in eight years. Gosh I would hate to even say. I mean it could it could be surpassed by a new Cryptocurrency or an entirely new Cryptocurrency protocol and then it becomes a legacy system. That’s definitely a possibility right. Something comes in that’s faster better cheaper and it’s going to it’s going to take all the market space away from the existing Cryptocurrencies you know. And that’s what we want. We want innovation, we want faster better cheaper. And that’s part of what we like about the Cryptocurrency space is it’s still open to that kind of thing compared to so much of the developed economies are controlled by monopolies, cartels, central banks, governments, which are only self-serving. You know they only choose policies and enforce policies that protect the few at the expense of the many. On the other hand Bitcoin could transition into being something that’s slow and secure. It’s never going to work in terms of buying a coffee at Starbucks with Bitcoin and that’s just a dead duck. It’s a transaction rate it’s just too small, but it might be useful in interbank transfers or large financial transfers. Maybe Bitcoin will find a home in that space. While other Cryptocurrencies will arise to take care of the the transactions on the level of consumer goods. You know we don’t know.

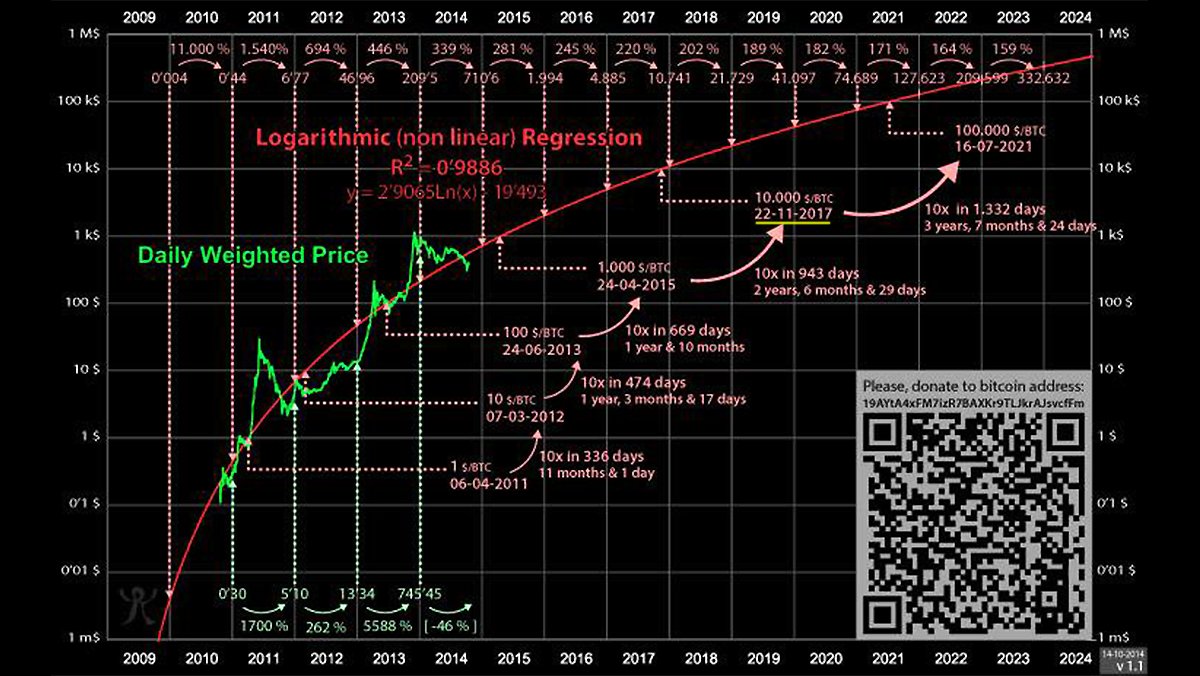

FRA: You had a chart that shows if Bitcoin replaces or becomes part of reserve currency. We could see prices in the $500000-dollar range:

Charles Hugh Smith: I know and it’s so funny because you know I’ve been following Bitcoin, but I never bought any and I was just kind of an interested observer until I needed it. As for its utility value, in other words, I needed to get some to buy some Bitcoin in order to pay the translators I had in Venezuela because that was the only form of currency that they could they could access right. That made sense. And if you think that the world economy is going to enter a time of instability where a lot of things start falling apart then of course we can say that Bitcoin or other Cryptocurrencies will well maintain their utility value for that reason. In other words, if people can access it and and pay their debts and buy stuff with it or buy other currencies with it, then its going to have utility value.

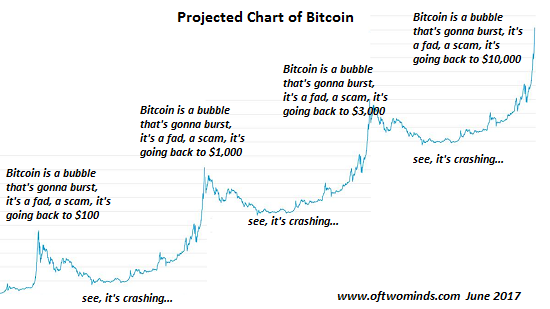

Charles Hugh Smith: I have another chart here the logarithmic progression of Bitcoin and its obviously kind of a rough guess, but this chart suggests that there is a logarithmic function to the number of days that it takes for Bitcoin to advance tenfold. In other words to go up by ten times and so it was kind of like how long did it take to go from a dollar to 100 an hour to a $10 then to $100 in $2000 and then to ten thousand. And so of course we can play these kind of games and you know those of us who like charts you know we love like tracking charts and projections and stuff, but it certainly we don’t know.

FRABut actually your logarithmic regression chart does seem to be fairly accurate. The November 22 date for $10000 is pretty much on track.

Charles Hugh Smith: Yeah it is. And this was I think the projection was made in late 2014. So by this chart, if we follow if that regression kind of goes continues as charted, then we would be at $100000 Bitcoin in 2021. So while we have to wait a whole four years. Yeah and of course I’m laughing because this is all speculation right, but we really don’t know what’s going to happen and what I like to say is this is the way markets should operate. They shouldn’t be manipulated by central authorities. So they always go higher and there’s never any retrace, there’s no volatility. You know volatility has been destroyed in a stock market, it’s been erased. And so there’s no real price discovery because there’s no volatility, there’s no price discovery. So Bitcoin is extremely volatile and to me, part of that is number one it has a very low float you know that of the 70 million Bitcoin. Several million, at least several million, are estimated to have been lost and in hard drive crashes and things like that. So the founders have about a million Bitcoin that they’ve never touched and never moved. For whatever reason and a lot of people are pursuing the idea of hold on for dear life, otherwise known as HDOL. And so the actual tradable float of Bitcoin is probably a relatively small percentage of that 17 million or 18 billion Bitcoin that are out there. So you got a very small float and like a small float in stocks, you get big volatility when there’s a small float and then if the more open the market is the more volatility you have. Right because you’re exposed to human emotions and there’s more surges of euphoria and panic and all the things that drive volatility, so I don’t see volatility going away.

FRA: Well that’s excellent insight for a balanced view. How can our listeners learn more about your work?

Charles Hugh Smith: Please visit me at oftwominds.com.

FRA: Great thank you very much Charles for being on the show. We’ll do it again.

Charles Hugh Smith: Yeah. Thank you so much Richard. My pleasure. Great topic.

Submitted by Boheira Manochehrzadeh <bmanoche@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/02/2017 - James Grant Interviews Alan Fournier: “Pension Funds Are So Desperate For Yield, They’re Systemically Selling Vol…”

“The central banks have succeeded in pushing people out on the risk curve. They’re taking people that are managing the pensions of state pensioners and they have them in negative earning sovereign instruments. And now they have them– they’re so desperate for some yield, they’re systemically selling volatility, which is remarkable.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/01/2017 - Nobel Prize Economist Joseph Stiglitz: “Bitcoin Ought To Be Outlawed .. It Is Successful Because Of Its Lack Of Oversight”

Stiglitz: “Bitcoin is successful only because of its potential for circumvention, lack of oversight .. So it seems to me it ought to be outlawed .. It’s a bubble that’s going to give a lot of people a lot of exciting times as it rides up and then goes down.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

12/01/2017 - The Roundtable Insight: Former Fed Advisor Danielle DiMartino Booth On Bitcoin and Cryptocurrencies

FRA: Hi – Welcome to FRA’s Roundtable Insight .. Today we have Danielle DiMartino Booth. She is a global thought leader on monetary policy and economics. She is the author of Fed Up: An Insider’s Take on Why the Federal Reserve is Bad for America. Her book rose to number 22 on Amazon’s Best Seller List. She founded Money Strong LLC in 2015 which is an economic consultancy firm with a great insightful newsletter. She is also a full-time columnist at Bloomberg View, a business speaker and a commentator frequently featured on CNBC Bloomberg Radio, Fox News, Fox Business News and other major media outlets. Prior to Money Strong she served as Advisor to the Dallas Federal Reserve President Richard Fisher.

Welcome Danielle.

Danielle DiMartino Booth: So happy to be here.

FRA: Great..I’d thought we would begin with your book. Having worked with the Federal Reserve, the title appears to be very strong; An Insider’s Take on Why the Federal Reserve is Bad for America. Your thoughts on that? Why is it bad for America?

Danielle DiMartino Booth: It’s not so much that I think the Federal Reserve has to go away. I just think that in its current form, or at least the form it’s been in since August 11th, 1987 when Alan Greenspan took office, has ended up being very bad for our country. We have ended up on a series of booms and busts and I, for one, am tired of being on this rollercoaster and think that it is high time we reinvent the Fed, take it down to the studs, and build it from the ground up and make it an institution that is good for America.

FRA: You recently commented on the Federal Reserve in terms of their biggest fear. Could you elaborate on that?

Danielle DiMartino Booth: There is a fallacy here. We have not just come through an era of deleveraging. If you look back at 2007, there was 150 trillion dollars of credit globally in the market. Today, we have over 220 trillion dollars of debt globally in the credit markets. So what we have actually seen is a very aggressive releveraging, overleveraging, of the global debt markets in order to eke out the economic growth that we have seen. I lay the blame for that at the world’s central bankers printing money to kingdom come, trying to create enough debt to spur economic growth, but the question I have is, at what price? I don’t think the central bankers want to answer that question. I think the 70 trillion dollars in debt build that we’ve seen since the outbreak of the great financial crisis is their greatest fear – It keeps them up at night.

FRA: Do you think central bankers have boxed themselves in a corner – Is there any way out? Can they actually implement quantitative tightening?

Danielle DiMartino Booth: I think that that remains to be seen. I laugh every time I hear that the quantitative tightening, the shrinking of the Fed’s balance sheet, is going to appear on autopilot. They are deluding themselves if they don’t think that this is a form of tightening when on Day 1, headed into this experiment of unravelling and shrinking of the balance sheet, the Fed owned 33% of all mortgage-backed securities in the country – They are deluding themselves. It remains to be seen if the Fed is going to remain agnostic to all data and continue shrinking the balance sheet while they continue to increase interest rates at the same time. It is double tightening if you think about it.

FRA: What about other central banks. What are your thoughts on what they are thinking and potentially doing?

Danielle DiMartino Booth: I’m very dear friends with a regular guest of yours, Peter Boockvar, and he lays out some very simple math. If you add together what the Federal Reserve says it’s going to be shrinking its balance sheet by around 400-some-odd billion dollars, run rate, this time, next year, and what Mario Draghi has committed to doing with the ECB in terms of tapering the ECB’s purchases, at this time as we are looking towards the holidays in 2018, we could theoretically have a trillion dollars less of global quantitative easing liquidity propping up these financial markets. It’s a big number and I think we have to take into context where that’s going to put these markets from the starting point of unprecedented historic overvaluation.

FRA: Is there any connection with the emergence and rise of valuations of cryptocurrencies, such as Bitcoin, to what the central banks have been doing?