02/04/2017 - Carmen Reinhart: Central Banks Tolerate Higher Inflation To Help Erode Massive Debt In Their Economies

“There may be yet another factor motivating major central banks’ tolerance for higher inflation. But their leaders may be unwilling to acknowledge it openly: as I have argued elsewhere, a steady dose of even moderate inflation will help to erode the mountains of public and private debt advanced economies have built up in the past 15 years or so.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/04/2017 - Charles Hugh Smith: Central Banks Have Failed To Generate Economic Growth

Charles Hugh Smith: “Rather than be seen to be further enriching the rich, I think central banks will start closing the ‘free money for financiers’ spigots .. The Fed’s QE ‘free money for financiers’ never did ‘trickle down’ to the bottom 95%, and the enormous expansion of bank credit is no longer driving corporate profits higher. There are other factors at work, of course; a global slowdown in trade, for example, a rise in energy costs and a stronger US dollar. All of these impact credit, profits and the share of GDP flowing to labor in wages, salaries and benefits. Whatever the causes, the reality is that the positive results of credit expansion have reached the top of the S-curve and are now declining. Expanding credit, via central bank monetary policy or private-sector bank credit, is no longer boosting profits or wages.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/04/2017 - Dr. Marc Faber Likes Agricultural & Precious Metal Commodities

Investors may be in for a “year of disappointments” and precious metals may prove to be a useful hedge, this according to famed contrarian investor Dr. Marc Faber. Known as Dr. Doom for his often pessimistic views, Faber shares his 2017 outlook is no different to his previously negative forecasts. “As we come into 2017, investors seem to be extremely optimistic about U.S. equities and about the U.S. dollar .. I think we can have a year of disappointments.” .. Faber says investors should look to have exposure in commodities, especially platinum, which he dubbed his “favorite precious metal for 2017.” “The individual investor will find it difficult to trade commodities where he has to rollover his position every month or every 3 months, which is very costly .. For the normal investor who wants exposure in commodities, the best is to be in precious metals – gold, silver, platinum.” .. like agricultural commodities.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/03/2017 - Dr. Albert Friedberg: Central Banks Are Lending Against Poor Collateral At Subsidized Rates

Austrian School Economist-based Hedge Fund Manager Dr. Albert Friedberg: “Governments are no longer willing to endure the short-term pain that is necessary to cleanse the economic system of mal-investments and over indebtedness. Lombard Street’s old adage (late 19th century) that central banks should lend freely against good collateral and at prohibitive rates in a financial crisis is no longer the reigning principle. Today, the opposite is true: central banks lend freely against poor collateral at subsidized rates. Andrew Mellon’s austere advice to President Hoover at the onset of the Great Depression to “liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate… it will purge the rottenness out of the system…” — the kind of advice that helped the US recover from the post-WWI depression in record time — was not heeded, and the depression of the ’30s dragged on until the onset of World War II. Today, of course, Mellon’s advice is heresy of the highest order. Increasingly, governments move to abort naturally occurring corrective trends with the result that necessary economic adjustments never occur. The price will one day be paid, but the bearish bet will have expired by then. The practical consequences of this soul-searching examination is to put an important restraint on catastrophic bets, defined as 50% or greater declines in major indices or in systemically important industry sectors like banking that lead to a generalized financial crisis. In short, we will need to exercise extraordinary circumspection before we make bearish bets that hinge on economic and financial upheavals of historic magnitude. These sorts of bets should be considered only when the burden of proof is overwhelming and only if and when limited risk options these conditions not be obtained, a defensive posture, by way of a buildup of cash and near cash instruments, will be adopted.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/01/2017 - Should Cash Be Abolished?

Frank Shostak:

“First, there is the problem that the mandatory switch from physical money to money held as deposits within banks will deprive people of the privacy they may wish in the allocation of their financial resources. Second, once all cash is transferred to the banking system, there is the real risk that control over that money is progressively ceded to that system and to the governments which thrive upon it. Political or consumption activities that are unpopular with government and/or commercial interests — especially in an environment of growing powers of the ‘security state’ — could result in retributive action via restrictions on access to those monetary balances. Third, in a purely digital world it would be impossible to withdraw physical money should people believe that their bank (or the banking system as a whole) was at risk of collapse. This could potentially lock people on board a sinking ship, or at least remove the ability of people to make their own judgments and vote with their monetary feet. The compulsory switch to purely digital cash could well become yet another facet of the growing tendency toward the further centralization of state power and the decline in individual liberty.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/28/2017 - Europe Proposes “Restrictions On Payments In Cash”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/28/2017 - James Grant: It’s A Different Investment World Now

A different investment world. Financial Thought Leader, James Grant, Editor of Grant’s Interest Rate Observerdeclares the 35 year bull market over and sees few opportunities to replace it. WEALTHTRACK broadcast on January 27, 2017.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/28/2017 - The Roundtable Insight – Yra Harris Emphasizes Keeping An Eye On Europe

FRA is joined by Yra Harris to discuss Trump’s effect on the global market, along with Draghi’s influence coming from Europe.

Yra Harris is a recognized Trader with over 32 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has Specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC. He has been interviewed for various articles in Der Spiegel, Japanese television and print media, and is a frequent commentator on Canadian Financial Network, ROB TV.

TRUMP’S EFFECT ON THE MARKETS

This is going to be a slow, grinding process. There’s a lot of things to dislike about Trump, but he’s showing some real leadership in that he’s willing to go out of a lot of boxes. He wants to renegotiate NAFTA so relations with Mexico and Canada would be stronger after it takes place. The Mexican Peso, by all fundamentals, is one of the most undervalued assets in the world. The currency has depreciated 700% since the beginning of NAFTA.

When you look at the value of the Peso, outside of an absolutely closing of the border, you’ll shut down America. The same goes for Canada. The Mexicans have tried to hold their currency, they don’t like the weakness of their currency, but the world has done it. Anyone who has emerging market exposure goes to sell the Peso because it’s the most liquid, but that’s driven it down to 21.28 Pesos to the Dollar. For a currency to devalue that much, it has to be choking on debt or going through phenomenal inflation.

With Canada being a member of NAFTA as well, there’s a strong dependence of Canada on the US economy. The Canadian dollar, weak as it is compared to eight years ago, is still medium.

Trump’s a negotiator, so if went in and spoke to the automobile manufacturers and said “This is what I want from you, what do you want from me?”, they must’ve replied by saying that the Japanese Yen is incredibly weak. It was a cry saying they want relief from this. There’s a lot of short position on the Japanese Yen out there. To couple with that, the Australians approached the Japanese saying they should carry on with PPP regardless, and the Japanese disagreed.

There can’t be a positive course because the world is at odds. United States will move unilaterally to depreciate the Dollar. Trump operates on a give-get basis, and doesn’t hold to international deals like avoiding currency intervention. A lot of Japan’s monetary policy that resulted in financial repression was done to drive currency values lower.

TRADE ARRANGEMENTS

Mexico has a debt on imports, which is basically a surcharge. The US is the opposite because we tax exports for revenue and allow imports. Global supply chains are so deep now. A lot of fields are changing. Trump does want to do a reset on the global order. The entire global order has been a burden on the American middle class especially. It was good for them in the 50s and 60s when the US dominated the world stage, but that was when the US had no competition. It’s harder now because there’s more global competition, but the US is still funding that. And that’s what Trump is saying.

Draghi told the German people that they’ve gotten a lot of benefits from being in the EU, and that may be true but they’re running into the same problem that Clinton and the Democrats had: Trump raised the question of “who’s benefited?” The average German citizen has been repressed to pay for this. They’ve borne the burden. They walked into this; German people do not live on debt, with the lowest home ownership of any developed market because people don’t borrow money to buy things. They’re savers, and whole basis of Financial Repression Authority is talking about people who are financially repressed and the central banks decide to bail out. There’s a momentum to this; this is about what’s going on, and the Germans can’t do anything because they don’t control their currency and they don’t control the bank.

CENTRAL BANK ACTIVITIES AND COORDINATION

Coordination will break down because they’re all in different places. Kuroda’s put the Japanese in a bad spot. What do they do now? The curve has now started to steepen in Japan so they’re on this mission where they’re moving on with QE which weakens the currency. They’re going to have a problem. With the ECB, if Draghi were to pull back the QE, rates would rise dramatically in Italy, Spain, and Portugal. There are some serious issues with this and you can see the Fed going their own way now because they’re looking to fight a battle about exorbitant fiscal stimulus and suddenly they go hawkish. If the Fed were to move aggressively, Trump will respond by intervening on the Dollar.

The effect on the 10 year bond is unknown. If the Dollar rallies, everyone loves America again. If the US intervenes, the 10 year yield will go higher because people will start selling Dollar assets. It’s a very tough question and we’ll have to watch the Fed closely and economic fundamentals, but the curves are steepening all over the world. People are selling in the long run in anticipation of improved global growth.

Gold is good because the central banks have been married to this zero to negative interest rate, and they don’t know what to do. If they’re seeing the panic in any way, that’s what gold is good for. It’s amazing that gold is still up there when equity markets are rallying.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/20/2017 - The Roundtable Insight: Alasdair Macleod & Jayant Bhandari On The Impact Of Trump, China & India

FRA is joined by Alasdair Macleod and Jayant Bhandari on discussing India’s war on cash and the impact of China and Trump on the world.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

Jayant Bhandari is constantly traveling the world looking for investment opportunities, particularly in the natural resource sector. He advises institutional investors about his finds. Earlier, he worked for six years with US Global Investors (San Antonio, Texas), a boutique natural resource investment firm, and for one year with Casey Research. Before emigrating from India, he started and ran Indian subsidiary operations of two European companies. He still travels multiple times a year to India. He is an MBA from Manchester Business School (UK) and B. Engineering from SGSITS (India). He has written on political, economic and cultural issues for the Liberty magazine, the Mises Institute (USA), Mises Institute (Canada), Casey Research, International Man, Mining Journal, Zero Hedge, Lew Rockwell, the Dollar Vigilante, Fraser Institute, Le Québécois Libre, Mauldin Economics, Northern Miner, Mining Markets etc. He is a contributing editor of the Liberty magazine. He runs a yearly seminar in Vancouver titled Capitalism & Morality.

DRIFT INTO FASCISM

Virtually every town and city is covered in cameras and they can literally follow you everywhere. The labour constitution clause was the desire to take into public ownership the means of production – in other words, a communist approach. Everyone’s going that way, not just in the advanced western nations. The central banks basically want to do away with cash. They’re looking forward to the financial technology revolution as means of replacing cash payments. It’s just that India jumped the gun on it. It’s interesting that we’ve had a mini rebellion with Brexit and the election of Trump. The authorities are having difficulties pushing through their plan, but it’s happening.

If you do away with cash, the effect is that people will trust the Rupee less. To an extent this is reflected in reports of unofficial gold prices, showing huge premiums. Which clash with official reports where people have to buy their gold through the market and be charged extra tax. The whole thing is a horrendous mess.

WHAT’S HAPPENING IN INDIA – WAR ON CASH UPDATE

There continue to be problems. India simply cannot work without cash. The banks have taken all the notes back but they have not released new notes to the public. The economy has stagnated; millions of small companies are failing, hundreds of millions of people are losing their jobs, and the economy is in deep trouble. This is a country where about a billion people don’t have internet connection, and people who do find it unreliable. Banks are very unethical and there is no electronic system. The cashless approach will completely fail but it will be very painful.

The IMF came out with a report saying the Indian economy will slow down from 7.6% to 6.6% growth rate, but that’s not true. There is negative growth in the country and everyone is claiming that their business has fallen from 20-80%. The IMF will likely revise that estimate over the next few months. People are avoiding anything other than necessities, but even there hospitals are empty and people are not buying food. Farmers have to dump their food supplies; they’re discontinuing farming, and food prices are down 25-75%. This is a huge gain for the middle class, but if farmers go bankrupt and don’t farm for the next cycle you won’t have food in a few months’ time. This is extremely chaotic for the economy.

There is also the issue of the value of the Rupee compared to the USD. India is among the most expensive of the poor countries, which means the Rupee is overvalued. It will likely lose value, and this will have an additional negative effect on the economy.

THE THREAT OF CURRENCY COLLAPSE

Business being down 20-80% is immensely serious, and we could expect GDP to fall by a third over the next year. There will definitely be a food price inflation, and inflation will follow as the central bank will make sure there is money available and funneled into the market. The people at the bottom of the chain will be impoverished, and the effect is that the Rupee is headed down.

In a cash economy, the rate at which a cash currency loses its purchasing power is largely governed by the availability of cash. As the cash loses purchasing power you need to produce more of it to meet the demand created by the collapsing of purchasing power. This puts a break on the rate at which the purchasing power goes down in a cash economy. If you make it a purely electronic money economy, you can lose that purchasing power overnight because there is no break on the availability of the money through an electronic currency system.

The people who are suffering the most are those that work in the informal economy, and the government doesn’t care about them because they’re below the tax bracket anyway and don’t pay their taxes. It’s very likely that some sort of famine might start in India, and this is something the world doesn’t understand yet.

A MOVE TOWARD CASHLESS SOCIETY?

This is the direction all central banks in Southeast Asia are travelling in. These economies are running on two speeds: the cities, similar to the ones in the west, where people need infrastructure and pay taxes, and then there’s the rest of the country where the poor live. People just use cash because they have no other means of paying for things. From the point of view of the central bank, they see this two speed economy and think that if they can get the economy that isn’t recorded on the books, their economic growth will appear quicker than anyone expects.

The only thing good that might come out of India is that it might make the governments elsewhere think of it before they take similar actions.

STAGFLATION IN NORTH AMERICA

If you look at what’s going on with bank lending, it’s clear that it’s been expanding since 2006. It’s still running over trend, which indicates the US economy is healthy. Trump is going to inject a huge amount of reflation on top of an economy in the stage of the credit cycle where it is already expanding. That will rapidly lead to overheating.

His intended expansion through infrastructure spending and lower taxes comes at a time where China has been stockpiling industrial raw materials so they can discharge their five year plan. China wants to make their economy more technology and service driven, and to bring about an industrial revolution throughout Asia. One way or another, China has cornered a lot of industrial materials and energy to execute their plans. Trump wants to do the same, and the effect on commodity prices is to drive them higher. This is going to bring inflation pressures into American consumer prices, and prices elsewhere.

How far can the Fed raise rates to take control over price inflation? Not very far, because the Fed funds rate of no more than 2.5% will be enough to topple the economy.

There will be a huge amount of investment happening in the US, and China is staying aggressively on the development path. These are very good signs for the future of commodity prices. There is a possibility that Trump will be able to reduce regulations on businesses, which will have deflationary effects on society.

CHINA: BITCOIN AND CREDIT BUBBLE

The authorities don’t like BitCoin. The Americans don’t like it, and the Chinese authorities would rather people use gold as an alternative. But BitCoin seems to be immensely popular with speculators, and is in a speculative bubble right now. BitCoin is too volatile to be practical as money. The only sound alternatives to fiat currencies are gold and silver, which will come back as fiat currencies collapse. The problem with BitCoin is that it has no inherent value. The pricing is based on pure speculation, and is backed by speculative pressures.

We tend to overemphasize the risk of a Chinese credit bubble collapse, because the Chinese government owns the banks and any collapse of that sort gets absorbed by the system. This is a very situation than in the west. While there’s a lot of debt in that economy, the sheer fact that it’s a very productive economy makes it able to go over these humps as time passes.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/18/2017 - McAlvany Commentary: Russell Napier On Financial Repression

Russell Napier: Gold Will Rise With the Dollar

Financial Repression will increase, just ask Carmen Reinhart, Euro & Yen will devalue as Dollar and Gold will rise, Societies that feel a threat to their private property buy gold. You can find Russell’s Book “Anatomy of the Bear: Lessons from Wall Street’s four great bottoms.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/17/2017 - Sprott’s Rick Rule: The U.S. Will Devalue Debt By Devaluing The Dollar

Resource investment expert Rick Rule is asking one very important question about a mountain of U.S. debt? Rule asks, “How on earth are we going to resolve $120 trillion on balance sheet and off balance sheet liabilities before we consider state and local debt and underfunded pensions? .. I think we will have a series of unofficial defaults where we devalue the net present value of the obligations, which is a different way of saying we devalue the . . . currency, gradually like we did in the 1970s. I think that will have the same impact on gold and silver prices.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/17/2017 - From Our Archives: Daniel Amerman Gives A Tutorial On Financial Repression

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/17/2017 - Yra Harris: Financial Repression Is Leveraging The Public Treasury To Maintain The “Animal Spirits” Of Crony Capitalism

Yra Harris: “The conspiracy against the public has been the financial repression of the global middle class in an effort to bail out those who have attached themselves to the public treasury to maintain the ‘animal spirits’ of crony capitalism.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/13/2017 - The Roundtable Insight – Incrementum’s Ronald-Peter Stoeferle On The 2017 Outlook

FRA is joined by Ronald-Peter Stoeferle in discussing his predictions for the next year, along with his thoughts on the state of the global monetary system.

Ronald is a managing partner and investment manager of Incrementum AG. Together with Mark Valek, he manages a global macro fund which is based on the principles of the Austrian School of Economics. Previously he worked seven years for Vienna-based Erste Group Bank where he began writing extensive reports on gold and oil. His benchmark reports called ‘In GOLD we TRUST’ drew international coverage on CNBC, Bloomberg, the Wall Street Journal and the Financial Times. Next to his work at Incrementum he is a lecturing member of the Institute of Value based Economics and lecturer at the Academy of the Vienna Stock Exchange.

GOING INTO THE NEW YEAR

It’s all about politics. We’re seeing quite a lot of drastic changes last year, but in 2017 political uncertainties will most likely come from the Eurozone where we’ve got elections in France, Germany, and the Netherlands. There will be much more surprises coming in, politically. It’s going to be an interesting year, and the interplay between inflation and deflation will be crucial for investors. Inflation numbers and expectations were picking up significantly, while the enormous strength in USD and the major correction in bond markets were very deflationary. There might be some surprises on the deflationary side going forward, though the mainstream is concerned about inflation.

At the end of the zero interest rate trap is going to be inflation. Every fiat money system in history collapsed because of inflation, not deflation, but we can imagine there might be some sort of deflationary shock. And central bankers will act extremely inflationary and this might be the tipping point where people will lose trust in fiat money.

Gold is in the very early stage of of a bull market, and now we’re at the beginning of the public participation phase and gold will rise in purchasing power verses fiat currencies. Already since the beginning of the year, gold is up 3% in dollar terms. The fact that the market became very bearish on gold in the last weeks is a good sign. It’s going to be a great year for gold, but even more bullish on silver.

INFLATION ON THE MONETARY SYSTEM

We all know that at the moment the US dollar is a leading global currency. Normally strength in the USD will affect emerging markets as the weakest links first, and we’re seeing enormous stress in Mexico, Turkey, Brazil and so on, and this will have effects. If the Fed delivered more rate hikes the dollar will go through the roof, and the dollar is the most important driver that one should follow in the market at the moment.

We may be having a transition from very low interest rates to forced inflation. This is going to go hand in hand with social upheaval and more socialist politicians because 4% real inflation is going to hurt the average person the most. The rich don’t care because they’ve diversified their real assets, but for the average person this is going to be a real problem, and this is going to be the point in time where things really get ugly.

The root cause comes from our central banks and the monetary system. Where the money is created first, those regions prosper from. Normally this means financial hubs like London and New York, where people really profit from monetary inflation. This is why in big cities people mostly voted for the status quo while people in rural areas that suffer from monetary inflation voted for change.

Sooner or later in the US there might be a recession.

GLOBAL STAGFLATION

Stagflation is something we should focus on, and is a very realistic scenario. Inflation rates, due to the base effect, may rise 3-4% in the next few months. If economic activity cools off, which is what we’re seeing, then we’re already in stagflation! People should prepare for stagflation, and what works is precious metals.

Stocks in general leave the comfort zone at inflation rates of 3%. Once we get over that level it’s a negative environment for stocks. As a rule, higher inflation rates are not positive for stocks in general.

CHINA’S EFFECT ON THE MACRO VIEW

Perhaps their credit bubble already burst. There’s very aggressive fiscal stimulus in China, and credit growth only came from state owned banks. At the moment capital controls are slowly being put in place, and BitCoin is going crazy because of China, and the RMB is at a seven year low. There’s quite a lot of stress in China, and this will have enormous effects on commodity markets and precious metals.

There are many similarities between BitCoin and gold, but they are competing currencies. There’s so much going on in the crypto-currency space, and a technological revolution will be happening. Our whole world is digitized, so why should that end with money?

It’s not either BitCoin or gold; there’s room for both. The worst financial repression will become, the more people will pile into BitCoin or physical gold.

Companies might stop buying their own stock, and this would have enormous consequences for the equity market. In the corporate world, we’ve been in an earnings recessions for four or five quarters now, and some economic factors already show us that the economy isn’t as well off as people would suggest. Equity markets are overpriced, but for market participants right now greed is much more important than fear. It’s hard to anticipate reasons for such a shift, but it’ll happen very quickly.

GENERIC ASSET CLASSES TO CONSIDER

No one’s talking about business models or valuations anymore; everyone’s only trying to anticipate what central banks might do next. This shows how dependent we are on cheap liquidity and central bank bubble. In this environment you should protect your downside and diversify, and find ways to profit from falling markets.

There’s plenty of opportunities, like in silver and uranium, and if institutional investors start buying into the silver space it’ll have enormous effect as it’s a tiny market. The biggest threat is definitely from China, so one has to be cautious and follow the signs coming out of China, but you should take those signs with a grain of salt.

We’re seeing huge volatilities in emerging market currencies, and this will have global effects. Normally crises start from the periphery. Before every major market crash we’ve actually seen rising rates and rising inflation rates, and we’re seeing both right now. There may not be a crash, but the odds are much higher than the market is seeing.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/12/2017 - China Employing Financial Repression Obfuscation And Secrecy

To “Prevent Public Panic”, Beijing Orders Banks To Keep Capital Controls Secret

Article: “China is so concerned about the ongoing surge in capital outflows that its forex regulator, SAFE, has taken the unprecedented step of ordering banks to keep its instructions about curbing capital outflows secret and also to ensure that research analysts do not publish any negative views about the yuan according to Reuters. According to bankers from local and foreign banks, both demands are seen as an attempt by the authorities to prevent alarm that could trigger further declines in the yuan .. China has implemented full blown capital controls, without wanting its population to know it has done so, which is understandable: fear of the unknown would lead to panic, would lead to more selling, and more panic and so on. But what we find delightfully ironic is that China is cracking down on the internationalization of its currency, just months after the IMF made the Yuan a fully ‘respected’ member of the SDR – a token of how ‘liberalized’ the currency is.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/12/2017 - McAlvany Report: Capital Controls And Financial Repression The New Tools Of Captivity

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/10/2017 - Mish Shedlock On The Fallacy Of Government Free Money Programs

Mish Shedlock: “‘Free Money’ experiments are underway in several places: Canada, California, and Finland .. The alleged studies are all fatally flawed because they do not scale. It’s one thing to give a few hundred people or a few thousand people free money, but it’s another thing to scale the experiment across an entire nation .. Economic illiterates have latched on to the free money scheme. If you pay people to do nothing, there will be masses of people doing nothing and getting paid for doing nothing .. The idea that the government needs to redistribute money to make things affordable is ridiculous in both theory and practice .. Thousands of affordable home programs, tuition programs, and Obamacare prove the ridiculousness of the concept .. If the Fed and governments would just get the hell out of the way, prices would naturally find the right level .. But no! The Fed does not want prices to go down, and when prices go up, economic illiterates scream for ‘living wages’, attacking a symptom of the problem .. The problem is not insufficient wages. The problem is fractional reserve lending coupled with a Fed hell-bent on creating inflation in a technologically deflationary world .. Misguided minimum wages hikes, public unions, and political corruption all exacerbate the problem .. Economically illiterate writers bemoan deflation, as do most economists, central banks, and academia. The final irony in this ridiculous mix is central bank policies stimulate the massive wealth inequality all of the above rail about .. It would behoove ‘living wage’ advocates to consider the possibility the real problem is central bank sponsored inflation, not a failure of government to provide a ‘living wage’ to those doing nothing.” LINK HERE to the commentary

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

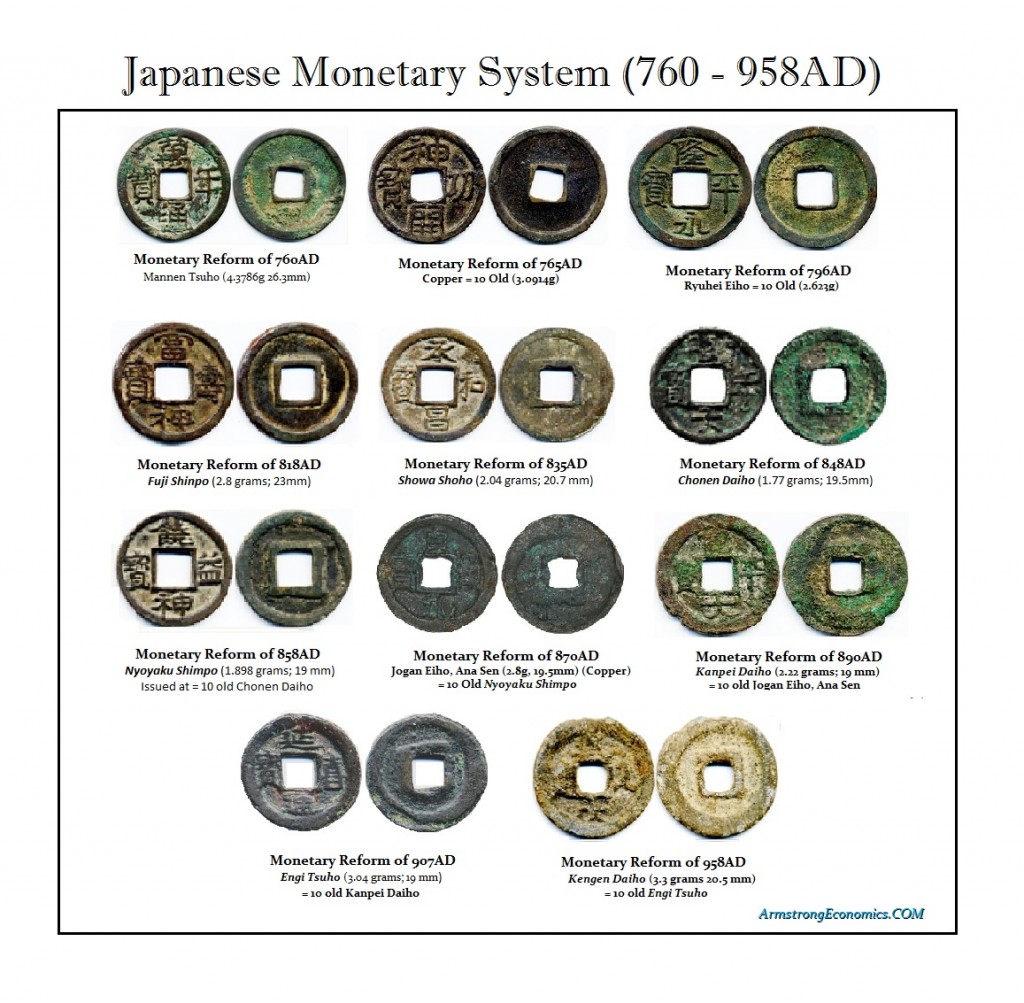

01/10/2017 - Martin Armstrong On Monetary Devaluations & Cancellations – India Is Repeating History

Martin Armstrong: “Since ancient times, many times those in power have cancelled their money supply to make a profit or collect taxes by force .. Three literary passages from antiquity identify the reminting of coinage in ancient Greece that had nothing to do with recycling of worn coinage. The government did what India did, but instead of moving to electronic money, they devalued outstanding coins and recalled them for restriking regardless of their condition, specifically as a means of raising revenue for the state .. Dionysios, we are told ([Arist.] Oec. 1349b27–33), and Leukon (Polyaenus, Strat.6.9.1), recalled in the existing coinage and restruck (or countermarked) it with a new type (character), thereby doubling its original value. This was an effort to cover the expenses of the state by increasing the money supply. Dionysios recalled the coinage and imposed the penalty of death for noncompliance. Leukon followed Hippias and simply demonetized all existing coinage .. Various Japanese emperors engaged in similar tactics but did not recall the existing coinage. Each new emperor just devalued all outstanding coinage to 10% of its value and issued their own coinage for profit. This practice led the population to use Chinese coins and rice. Eventually, nobody would accept a Japanese coin because of this practice. Thus, the end result was that Japan lost the ability to issue coins at all for 600 years after 958 AD. This is why, as we move forward, it will be best to hold assets out of banks and out of currency .. The safest asset may simply be blue chip stocks for they would never make it illegal to own corporations unless you had a full-fledged leftist revolution that seized all private assets as in a communist revolution. That risk would naturally alter everything once again.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/09/2017 - Russell Napier On Financial Repression: “You Are Not Supposed To Know It Is Happening”

Financial Repression – “Put inflation above interest rates and to maintain them there” .. it’s being done by the central banks, and it could be forced by financial institutions upon investors by governments .. it’s all about governments trying to maintain & reduce the burden of government debt .. but now the need to repress is higher than after World War II, since there is also a lot of private debt as well .. “we are at the very early stages of this [financial repression]” ..

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

01/09/2017 - Dr. Marc Faber: Federal Reserve Likely To Launch QE4 In 2017

“Let’s say the Fed realizes that the deficits for the U.S. go up and that interest rates increase and that the economy slows down, do you really think that they will increase the Fed funds rate three times in 2017? Never. What they will aim at, then, is to essentially bring interest rates down, especially if by then the dollar is still strong. And so they will probably launch QE4 in 2017. I think that will be a surprise for many people — not for me, but for many people that will be a surprise.”

Also recommend watching the below video interview: Dr. Marc Faber sees emerging markets as outperforming the U.S., the U.S. Treasury Bond Market likely to correct (go higher) in the short term, & the U.S.$ likely peaking in 2017 .. sees the world’s big central banks – Federal Reserve, Bank of England, ECB and Bank of Japan – as coordinating monetary policies together on a global basis.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

02/04/2017 - Carmen Reinhart: Central Banks Tolerate Higher Inflation To Help Erode Massive Debt In Their Economies

02/04/2017 - Carmen Reinhart: Central Banks Tolerate Higher Inflation To Help Erode Massive Debt In Their Economies