05/07/2017 - Central Banks Injected A Record $1 Trillion In 2017 – “It’s Not Enough”?!

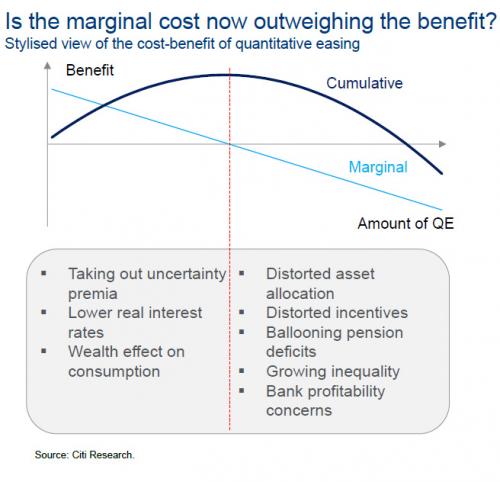

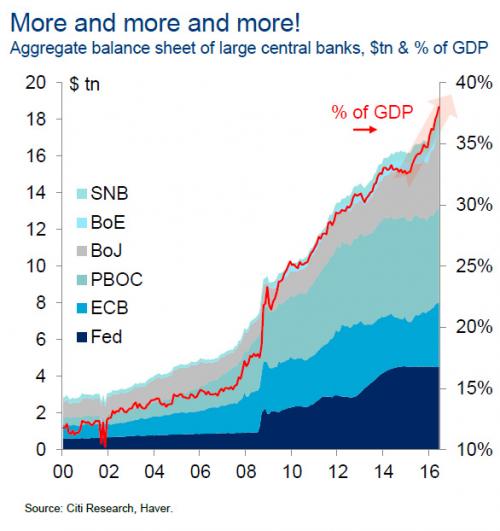

“The latest weekly report by Deutsche’s Credit Strategist Dominic Konstam finds something even more troubling: $1 trillion in central bank liquidity YTD – or roughly $250 billion per month – is not enough .. Konstam’s conclusion is that there are two outcomes: either asset prices drops, or central banks will ultimately be forced to inject even more liquidity .. The bottom line, however, boils down to the following chart first shown by Citi last September, demonstrating that the marginal cost of central bank liquidity injection is now negative…

… and is located in the lower right quadrant, something both markets and policy makers realize.

Which means that when stocks realize just how insufficient the record $1 trillion in central bank liquidity has become, central banks – which have stepped into every single market correction over the past 7 years with some ‘liquidity supernova’ – will, for the first time since the financial crisis – be out of tools… something Janet Yellen appears to have realized some time ago.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/06/2017 - The Roundtable Insight: Yra Harris On The Bond, Currency, Equity and Commodity Markets

FRA is joined by Yra Harris to discuss the current state of bond, currency, equity, and commodity markets.

Yra Harris is a recognized Trader with over 40 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through a combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC.

Yra highly recommends reading The Rotten Heart of Europe – send an email to rottenheartofeurope@gmail.com to order

BOND AND CURRENCY MARKETS

We’re just coming off a Fed meeting in which they called the first quarter transitory, which means they’re not worried about it, yet they made no change to the current policy of maintaining the Fed balance sheet. The $4T will remain at $4T, and whatever expires will be renewed by the purchasing of whatever duration expires by the new instrument. With the Fed raising rates, even though GDP turned out to be low, there are other elements that are slowing down. Right now, if the Fed was looking to start unwinding its balance sheet, which would mean a dynamic act of actually starting to sell some of their assets, the first move would be for the curve to start to steepen. A lot of potential buyers would step back, and market would say ‘show me what you’re going to be doing’. You’re going to have others trying to front run the Fed, because the Fed model says there should be no problem. But what the Fed doesn’t model is the effect on the marketplace, and they’re hoping the marketplace allows them to do this. What the Fed is worried about is whether the market will be cooperative with what they want to do. It’s why they don’t want to acknowledge any pre-program. It’s the same problem the ECB has. A lot of people front run the ECB, and the market tries to rush ahead of it.

If the Fed tries to unwind by an aggressive type of action, which is selling the debt to unwind in a quicker way, the long end of the curve will go up higher than the short end in the immediate period, because the market will race ahead of them. We don’t know how the curve ought to be steepening in that environment. With the Fed doing nothing but raising rates, the curve has actually flattened quite a bit.

It’s interesting how the US 2-10 curve, the ‘investor’s curve’, just mirrors the German 2-10 despite negative rates in Germany. These two just continuously mirror each other. Ultimately, if the Fed is too aggressive in unwinding the balance sheet, that’ll tip us into a very flattening curve, which will fly in the face of what we think should happen. There’s going to be all sorts of things here because the market is going to set the tone. If the Fed were to actually embark upon an unwinding, the market will then set the tone unlike QE. Right now the curves are telling us that the Fed is a little too aggressive, and that’s why it’s flattening.

Everything is ‘transitory’. The Fed is not going to do this in a vacuum. If Marine Le Pen wins the election and throws the entire financial system into turmoil, the Fed has to change their perspective too. So we have a lot of things in play here. Yellen will be very reticent to raise rates too quickly; they want to see more from Trump and Congress before they get more aggressive.

OTHER FACTORS THAT COULD INFLUENCE USD AND BOND MARKETS

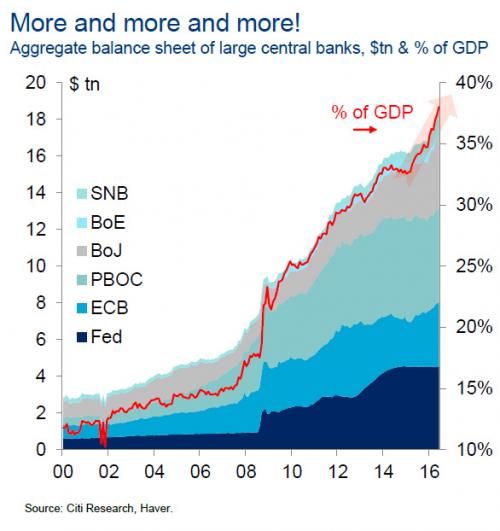

In the first quarter, central bank buying totaled a trillion Dollars in assets. The amount of liquidity is huge. The Dollar and all currency markets are all relative value plays. Even if everyone is moderately up, some are doing better and offering a higher return, but the US equity market is close to what we may discern as full value based on historical metrics. In a fairly stable world, the US is not where we should be chasing assets right now. The Mexican Peso and stock market is probably the most undervalued asset class in the world. People are pushing India as a great place to invest, but India has a lot of enormous infrastructural and political problems that they’re trying to work on.

The best place for investment right now is Germany. If the Germans agreed to do whatever it takes to hold the EU project together, you’ll experience some inflation in Germany but the currency will be weak. On the other hand, if things got so bad that the whole EU project fell apart, you’re buying Germany with a low currency. If it were to pull out for some reason, German assets would convert to Deutschmarks. Germany could be bullish on assets, and you get the use of a weak currency. We get a cheaper currency with a much stronger economy. This is not an easy world to invest in. The political risks are phenomenally great; Italy is still a massive problem for Europe, Greece has not gone away, and there’s no trade in Japan’s JJB.

When you look at how central banks have single handedly destroyed the bond market, you don’t have to look very far. The Fed may be too self-confident, but their models have no respect for market reaction and they still think they can extract themselves with very little pain. If they deem to shrink their balance sheet, they’re going to find out the pent up power of the market and its ability to cause them a lot of pain.

THE GLOBAL MINSKY MOMENT

At the end of the day, interest rates aren’t high enough to attract people into leaving the comfort zone. They won’t let interest rates go high enough to ease some of this burden, so people take comfort in the equity market. Minsky must be spinning in his grave that we’ve gotten to this point and it’s so controlled by the central bank. The central banks have created a global Minsky moment because everyone is complacent. It’s everything approaching the Minsky moment because where are you going to go? There is a cost to everything; just because you don’t see it today doesn’t mean it won’t pop up tomorrow. This is all the outcome of central banks not knowing when enough is enough. QE1 in the US was absolutely needed to prevent a mass liquidation of US assets, but after that it stopped making sense. QE2 and QE3 were totally unnecessary and has created this mess that we are now in.

SILVER-COPPER RATIO TO EQUITY MARKET

Gold has depreciated against silver significantly over the last few weeks, while the equity markets have been holding up pretty strong. Usually silver tends to outperform because it also has industrial usage. Copper has a tendency to outperform the other metals when the equity markets are doing well, because people correlate it to the economy. Copper has been dramatically outperforming silver over the same period, which is highly unusual when the equity markets are holding.

The Chinese have gigantic warehouses full of commodities, which wreaks havoc on that market. You do hear some bad things about what’s happening in the Chinese economy. If that’s the case, commodity prices may come under pressure as some of the lenders call the collateral and start pushing it on the market to raise some cash to secure loans.

INVESTMENT POTENTIAL OF COMMODITY ASSET CLASS

The agricultural sector is a good sector to be in. We have massive crops around the world and prices are relatively strong historically. We’ve had a bit of a rally in the agricultural products in the last few weeks, but it’s something to pay attention to. You should take a look and see if there’s an opportunity for you. The one thing that we’re sure of is that China and India need grain, end of story. As their income levels move up, agricultural products and higher protein products are in demand.

The great thing about the commodity market, unlike the commodity markets which are manipulated, is that farmers and miners react to price. The markets do work.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/05/2017 - Dr. Thorsten Polleit: The Fed Is Causing A Recurrence Of Boom And Bust

“It is Fed that is causing a recurrence of boom and bust. It initiates a boom through its easy money policy. In an attempt to reign in the excess it has created, the Fed at some point turns the boom into bust. To fight the bust it returns to an excessive monetary policy. The result is not only a volatile economy, but also an unsustainable build-up of ever greater amounts of debt on the part of government, consumers and corporates — making the final bust extremely costly .. The takeaway from the Austrian monetary business cycle theory is this: Either the boom goes on, and interest rates continue to remain at very low levels. Or interest rates move back to normal, and the boom turns into bust. An ongoing boom, accompanied with a return to normal interest rates, however, is the least likely scenario. If the Fed has learned from its most recent past, it wouldn’t be surprising if US interest rates will remain lower for longer.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/05/2017 - Chris Whalen: Investment World Is Skewed By The Latest Round Of Monetary Policy Experimentation By The Fed

“We live in an age of asset bubbles rather than true economic growth. The investment world is skewed by the latest round of monetary policy experimentation by the Fed, including years of artificially low interest rates and trillions of dollars in ‘massive asset purchases,’ to paraphrase former Fed Chairman Ben Bernanke .. These bubbles are caused and magnified by supply constraints, not an abundance of credit. Whether you look at US stocks, residential homes in San Francisco or the dollar, the picture that emerges is a market that has risen sharply, far more than the underlying rate of economic growth, due to a constraint in the supply of assets and a relative torrent of cash chasing the available opportunities .. Likewise with the dollar, the image of the financial markets is one of constraints rather than policy ease. Since the middle of 2014, the value of the dollar against major currencies has risen sharply, suggesting a shortage of liquidity or at least a relative preference for dollars vs other fiat currencies .. Regards the prospect of a dollar drop, Megan Greene tells us on Twitter that ‘Only way I see it in the short-run is if everyone else gets in trouble and the Fed opens swap lines w other CBs to supply QE #unlikely’ .. We hear all of that, but can’t help but ask the question. All things do come to an end, including the seeming ability of the FOMC to painlessly levitate the fortunes of heavily indebted nations on a sea of easy dollar credit. This works really well when the dollar is strong, otherwise not so much.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/04/2017 - Kyle Bass: “All Hell Is About To Break Loose” In China

Danielle Park: “Advised and led by their US trained finance types, China has followed the same hide-your-debts-playbook that brought down Enron, Worldcom and global financial markets in 2001-03, as well as Bear Stearns, Lehman and global markets again in 2007-09. The difference this time is the unprecedented scope and scale: China is a whole country, the world’s largest population and the second largest economy. The main benefactor of credit-fueled cash flows from the west over the past 15 years, China forgot that credit expansion is a finite cycle and spent like a drunken sailor throughout. Now it’s left holding a leverage on leverage bomb of unprecedented proportions, with sketchy debts oozing out of every crack and crevice .. We should expect that the liquidity and solvency problems there will be felt though highly connected world markets. This is a necessary part of the great cleanse and reset so needed to reboot asset prices and the economy. So, long-run positive, but short to medium term dangerous for capital.”

Kyle Bass: “Some of the longer-term assets aren’t doing very well .. As soon as liabilities have problems – meaning the depositors decide to not roll their holdings – all hell breaks loose.” .. The wealth management products, or WMPs, have swelled to $4 trillion in assets in the last few years, he says., on a $34 trillion banking system .. “Think about this – in the US, our asset-liability mismatch at the peak of our subprime greatness was around 2%! … China’s mismatch is more than 10% of the system.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/03/2017 - The Roundtable Insight: Megan Greene On The Current Status Of The European Economy

Tonight’s podcast includes some insight on Europe’s current economic and political states, and how it translates into current economic trends. We have seen the rise of the anti-European and anti-EU mindset all across Europe. This movement not only impacts European politics, but the entire state of the European economy as well, and has direct influence over Western economics in terms of trade agreements, investments in the European market, and the value of our currencies.

Megan Greene, an accomplished economist with a specialty in European economics, explores what Europe needs at the moment and what is most likely coming up in the European economy.

FRA: Hi, welcome to FRA’s Roundtable Insight. Today we have Megan Greene. She is [the] Managing Director and Chief Economist of Manulife Asset Management. She’s responsible for forecasting global macroeconomic and financial trends, and analyzing the potential opportunities and impacts to support the firm’s investment teams around the world. Formally, she was with Roubini Global Economics, where she had a focus on the Eurozone, and she also holds a Masters [degree] in European politics from Oxford University. So, quite a focus on Europe and we would like to explore Megan’s thoughts on Europe. Welcome, Megan.

Megan Greene: Thanks for having me.

FRA: What are your thoughts, what’s happening in Europe? The political situation there, the rise of anti-Europe parties, how that all affects what’s happening as far as the economics and the financial situation of the Eurozone and the European central bank?

Megan: Sure. So I would say, first of all, that the far greatest risk coming out of Europe for this year, probably the next year (too) is the political risk. Europe has an incredibly busy election schedule over the next year-the next election coming up is actually in France. It’s coming up quite soon; their two-round presidential election. It seemed at first very likely that it would be a runoff in the second round between the right-wing populist national front’s candidate, Marine Le Pen, and the independent candidate Emmanuel Macron. But more recently, actually, two other candidates had a lot of momentum and those are the right candidate Fillon, and the communist candidate Melenchon. This matters in large part because Le Pen and Melenchon both are running on a platform that’s very anti-European, very populist, and both have said in some form that they would like to renegotiate France’s relationship with the Eurozone, and potentially hold a referendum to see if France might want to leave the Eurozone. There is a chance that the second round of that election could be a “Le Pen, Melenchon” runoff, and that would be a market event for sure; it would be dramatic. More likely is still a “Le Pen, Macron” runoff, and it does seem most likely that Macron will end up winning. Even if Le Pen, the most anti-European candidate won, there’s a parliamentary election at the end of this year, and it seems very unlikely that her party would do well in those elections. It does seem that parliament would still be controlled, in which case it might be very difficult for Le Pen to actually have a referendum on France’s membership in the Eurozone. Even if they had a referendum, actually, the most recent opinion polls suggest that the French would vote to keep France in the Euro(zone). I don’t think that it’s very likely that, first of all, Le Pen would win, but secondly, that even if she did, that France would go ahead and exit the Eurozone. It’s a very low probability event, but such a high impact event-it’s something worth looking at.

The much bigger risk of a Le Pen win isn’t actually exiting the Eurozone, it’s just a series of bank runs starting in France but maybe spreading a bit wider. That would obviously have implications on the markets. Even bigger as a risk for the Eurozone than the French elections, I think, are the Italian elections which are due to be held by March of next year. It’s possible they might be held early…but probably not before the fourth quarter of this year. In any case, according to most opinion polls, the populist, anti-European five star movement isn’t in the top slot. It’s unlikely in an Italian election that the five star movement would actually win in absolute majority. They would have to find coalition partners and that won’t be easy given their ideology and the ideologies of the other political parties in Italy that might want to form a coalition with them. So even if the five star movement were to win the Italian elections, it’s not totally clear if they would make it into government. But if they did make it into government, they said that they too would like to have a referendum on Italy’s membership of the Euro(zone). Unlike in France, Europe is much less popular in Italy so it does seem plausible that if there were a referendum in Italy that Italy could end up choosing to leave the Euro(zone), and that would be dramatic-to have Europe’s third-largest country leaving the European project, that could really pose an existential challenge for the Eurozone. So those are two countries that could end up following in the footsteps of the UK in terms of leaving the European project.

Scotland is another country that could end up, actually, leaving the EU in its attempt to leave the UK. Its hopes given, of course, how pro-European Scotland is would be to rejoin the EU but they might end up having to get in the back of the line. That’s one concern. And then of course one issue that has been at the forefront of European risks since the beginning of the crisis, the global financial crisis, is Greece. Greece hasn’t been solved by any stretch of the imagination, it’s just garnering a lot less attention from the markets these days. Whereas before, the real concern was that there would be a stand-off between Greece and its creditors, and Greece would end up leaving the Eurozone almost by accident. Now, it’s very different. It’s very clear that the Greek government will just end up caving every time its creditors ask new reforms of this government, and just recently they came up with a deal for another round of funding to ensure the government is signed up to what the creditors demanded. The problem now is that creditors themselves can’t agree on what they want, so the IMF would really like to see Greece have debt relief, which is necessary in my view. The other creditors, particularly Germany, don’t want to commit to debt relief now, particularly not in advance of the German elections coming up. If they don’t come up with a solution, the IMF could end up leaving the bailout program in which case there is a real risk that Germany, and more recently the Netherlands, has said that they wouldn’t participate without the participation of the IMF. If these countries don’t participate, then the bailout program would fall apart. Greece would have no means for funding, and could end up leaving the Eurozone, not because it was specific strategy on the part of the government or even on the part of the creditors, but again, almost by accident. There is a risk that you could have some EU and Eurozone breakup, even though the risk isn’t as high as it once was.

In terms of the actual economy in the Eurozone, in aggregate, I think that the Eurozone is roughly a 1.5% growth economy, but again that’s in aggregate so it masks the big divisions between the core countries like Germany and the weaker countries like Greece and Portugal, and Italy as well. Data has been looking better; much as in the US, much of the confidence data has looked good, a lot of the soft data, the PMI data for example, has been really improving. It’s the hard data that’s not looking as great so things like industrial production, new factory orders, that hasn’t really come in yet. Lending is actually expanding, so we might expect some improvement of the hard data such that there is a sustainable economic recovery in the Eurozone. That recovery can only really be so strong as long as the approach remains that if all the weaker countries doing all the adjusting and all the core countries just carrying along as they always had. Evidence in that is Germany’s current account surplus which continues to hit new record highs every month. Germany and other core countries aren’t adjusting at all and the weaker countries continue to cut their wages and pensions. In Greece’s case at least, we haven’t seen much wager-pinching growth, and they continue to try to increase their national savings as a percentage of their GDP to match Germany’s again, and that just means there’s not a lot of consumption or investment happening in the weaker parts of the Eurozone. That really cuts off any avenue towards domestic demand, it means that most of the Eurozone is relying on exports for growth. There is an economic recovery happening in the Eurozone, it’s just muted by the fact that it’s all the weaker countries doing all the adjusting and none of the stronger ones. I think that we can expect that to continue in the absence of any major policy change, so I think the Eurozone in aggregate will continue to be a 2% growth economy.

In terms of what the ECB is doing, the ECB would love to normalize monetary policy but it’s just taking them a while because the recovery is so weak and because inflation isn’t coming in. I think that the ECB will probably announce a tapering of their QE program at the end of this year, and at the end of next year, they might have to wait until the beginning of the following year. The ECB is very much going in the footsteps of the US in trying to very, very gradually normalize monetary policy. I think that if some of these political risks I mentioned materialize, then it’ll be incredibly difficult for the ECB to hike rates in to that for sure. There are other risks, in the banking sector for example, particularly in Italy, that might make it really difficult for the ECB to tighten monetary policy.

FRA: You mentioned earlier on bank runs, could those be initiated from a catalyst of something other than one of the countries pulling out, like Italy or France, pulling out of the European monetary union? Would it be other factors potentially, in terms of the bank runs?

Megan: Yeah, you could see bank runs happening as a result of financial instability in in of itself. Particularly in Italy, there are a lot of banks that are still requiring recapitalization, non-performing loans in Italian banks. Portuguese, Irish, Greek, even French banks are really elevated and it used to be that they would work at their non-performing loans by creating bad banks because they can’t create the same bad bank that they used to be able to. That’s no longer a solution which means that none of these countries really know what to do with the massive heap of MPL’s that are sitting on their balance sheets, and so if you see those non-performing loans start to be realized and turned into defaults you could end up having a real scare.

The Eurozone has made some progress on institutional change in terms of creating a banking union, but they haven’t gotten all the way there yet so rather than saying they have a banking union I’d say they have a loose banking federation. There’s still no risk sharing in terms of banks in Europe so that means that not only is there not a common deposit guarantee in Europe, but I do think that if any country that has a big bank that really needs to be wound down. Now, governments aren’t allowed to step in and bail them out, and I think that wounding down a big bank is absolutely politically toxic for any leader so faced with that choice, most leaders would just break the rules and completely undermine the banking union and that in itself could spark off bank runs as well.

FRA: Do you see the potential for a move towards a fiscal union in terms of creating an actual European bond or just conducting fiscal policy across the entire Eurozone?

Megan: I think part of a fiscal union is needed, though I don’t think we need, for example, a common fiscal authority. I think we do need to see asset class in Europe that is liquid and deep enough to withstand any sudden stops, so I do think they need to create mutualized debt like a Eurobond. But then actually I think that the private sector can go ahead and step in rather than having a fiscal authority. If we had a capital markets union, I think that that could go a long way towards achieving what a public fiscal union could achieve and I think that’s necessary because I just don’t think that there’s any political will either in the core or in the periphery to actually have a fiscal authority and have everyone sign up to the same rules. So I think that it’s unlikely and would be a waste of political capital to try to create a fiscal authority.

One way of explaining what I think that the Eurozone needs is a mutualized debt so a Eurobond, but then in terms of the private markets governing cross border investments and exposure, it’s a bit like our credit card companies like VISA and MasterCard, that’s mutualized debt with no real central authority to manage it. There is some precedent for, I think it’s possible, but I don’t think it’s possible to see a full fiscal union with a single fiscal authority. Unfortunately, Eurobonds aren’t at all on the agenda now. It would require several more acute crises, and existential crises in the Eurozone to get the core members and the peripheral members to sign up for it, but particularly Germany because Germany doesn’t really see why they should accept other countries’ risk, and they’re worries about creating a moral hazard by going ahead and mutualizing bonds. So I think it’s very unlikely, but I do think that we need Eurobonds eventually for the European project to stay together.

FRA: And actually just recently this week US president Donald Trump made some comments on the dollar that it was too strong and so there was some movement on the dollar going lower; pushing the euro higher. Could that be a trend, and if that were to happen, if the euro would strengthen, could that cause global havoc and the countries’ struggle on their economy and debt burden?

Megan: Well, I think that’s its really unlikely that the general trend will be that the dollar weakens, I think that it’s much more likely that the dollar ends up a bit stronger even though the US president is trying to talk down the dollar at the moment. It’s really hard to conceive of a situation in which it’s in the US government’s best interest to see the dollar depreciate. The only scenario I can really think of is if there were huge problems in other economies, and the US fed opened up slop lines with other central banks to essentially fund their QE program so the Bank of Japan and the ECB, and the Bank of England. I think that’s really unlikely. We have seen the dollar weaken a little bit but the general trend is for the dollar to strengthen and that’s relative to a basket of currencies but that includes the Euro. I think generally the Euro will be weaker. Also, we will have movements, depends on your time frame of course, but I think if the French election results in Macron at the helm of government, then I think that the Euro could strengthen off the back of that. But if Le Pen were to win for example, I think the Euro would weaken off the back if that, so it will depend to some degree of political developments and in the long term, I do think that the Euro will probably weaken relative to the dollar. Not so much necessarily because of the factors that mean the Euro should be weak but in large part because of what the US and the fed are doing.

FRA: Given these political developments, do you see Germany continuing to bear the debt of the rest of Europe in terms of transferring its current account surplus to the less fortunate states of the union…or could it be that Germany considers on leaving the Eurozone?

Megan: I think that Germany has really been taking on risk through the target to balance this at the ECB, so the target to imbalances is now at record high, or higher than they were back in 2012, when there were much greater concerns about countries leaving the Eurozone. That’s largely because of Italy, actually, so it’s largely because of German investors pulling out of Italy. Now that only becomes a problem if a country actually leaves the Eurozone and that seems unlikely, I think. It’s certainly not my base case scenario over the next couple of years. Otherwise, Germany isn’t really funding everybody else’s debt, but I do think that there is a discussion about whether it’s really in Germany’s best interests to stay in this project. I think that it definitely is. Germany benefits from an artificially weak currency because it is connected to so many weaker countries, and that’s been really helpful for Germany given that their growth model has been pretty reliant on exports for the past several years so the domestic demand now stand for a slightly larger percentage of GDP than it has in the past, but its only really slightly larger. Germany is still dependent on exports for growth. If Germany were to go ahead and leave the Eurozone, it would probably see its currency appreciate massively and that would completely undermine its entire growth model so it would have to come up with an entire new model and that’s not really in Germany’s best interests so I do think it’s in Germany’s best interests to stick in the Eurozone.

I will say that I’ve spent a lot of time talking to the EU governments and my argument with them has always been that Germany always had a very high national savings rate, and so they’ve had a really low national investment rate, which hasn’t really served them well. I mean they’ve invested in Greek government bonds, and Portuguese retail, and Irish property, which (those investments) turned out to be really bad investments. It also means that German investment domestically has been really low, so Germany suffers from chronic underinvestment and as a result their roads are in bad shape, their bridges are in bad shape, so my argument has always been that maybe the German government should encourage domestic investment and that would boost Germany’s growth, and that would also trickle out and help the growth of the rest of the Eurozone. The German government’s response to me every time is to ask me why they should care about growth, which as an economist you can imagine, seems like a weird question but according to them, they don’t have incredibly high growth but they have a really high standard of living and very low unemployment. In their view, growth is kind of an Anglo-Saxon obsession and they’re doing just fine. So this approach to growth in Germany, and this approach in the entire region whereby Germany does the same as its always done and everybody else tries to look more like Germany, I think that’s here to stay for a number of years.

FRA: Interesting. And what are your thoughts on the UK and Brexit, how that’s playing out, and could there be any changes between now and the next two years after they receive their Article 50 notice like a few weeks ago?

Megan: I think there are still some that are hoping that the UK will take back triggering Article 50. I spoke with the guy who wrote Article 50, John Kerr, and he says you can and he intentionally left wiggle room in it. I think it’s very unlikely that the government will do that given that they’re acting on a mandate that was given to them by the people. Also if they were to go ahead and revoke it, they probably would have already damaged their relations with the rest of the EU given that they’re negotiating to leave.

I did a lot of consulting on Brexit and testified in the House of Lords, and before Brexit I would’ve said that the worst possible option was the UK going for a so-called “hard Brexit”, which means leaving the single market all together. Now, I think that’s no longer the worst option, I actually think it’s the most likely option. The prime minister has said that’s what they’ll pursue. I think there’s a worse option out there which is that after two years of negotiating, both their divorce from the EU and their new relationship with the EU, they actually don’t have any agreement on what their new relationship with the EU should be, at which point the UK would just kind of stumble out of the EU. They would have to rely on the WTO for their trade relationships. The problem with that is that right now the WTO has relatively robust rules and some credibility, but in two years from now it actually might not, so, you could conceive for example the US government trying to implement a border adjustment tax which is most likely illegal according to WTO rules. Having the WTO turn around and say, “Well, that’s illegal you can’t do that” and the US administration could just reply by saying well, “We don’t care anyhow”. That would completely declaw the WTO. That’s just one example and there are a number of potential trade policies coming out of the US in particular that could really undermine the WTO, so the UK’s plan is to actually rely on WTO rules so that at the end of two years the WTO might be severely undermined by then, in which case, that’s a terrible plan for the UK. I think that’s the worst scenario.

The only way, I think, that the UK could actually have a deal at the end of two years is if they cut and paste it from somewhere else. Two years is not a lot of time to negotiate their divorce from the EU first, and of course not much will get done before the French elections, and then the German elections in September, and then the Italian elections in March, so, there will have to be breaks in negotiations. They’ll have to negotiate the divorce and then they’ll have to negotiate an entirely new relationship-that’s a lot to do in two years. If they can cut and paste a new relationship from somewhere else, they might be able to pull it off. One way to do that is to copy the deal that Canada and the EU struck: the Ceta deal. The problem with that is that it doesn’t include anything on services and more than half of the UK’s economy is services so they’d have to write an entire new chapter to cover services, and that in itself could take two years. That’s problematic. There’s one other option that’s currently being discussed behind closed doors in the UK and that’s to copy the deal that the EU just struck with the Ukraine which does include services so that is really feasible. It is mainly being talked about behind closed doors because the UK doesn’t want anyone to realize that they’re trying to follow the Ukraine as a model. That is one option but it’s too early to say whether really is possible or not but it’s something that they’re looking at.

FRA: Finally, just wondering your thoughts on the investment environment, what this all means, not mentioning any specific companies or securities, any thoughts on asset classes or types of investments that could make sense in Europe given all the scenarios, assuming there could be some investments that could make sense regardless of all the different scenarios like whether Germany stays, whether they pull out and different countries leaving, the effect of political parties getting elected. And would it make sense for Europe in general now from a contrarian perspective? Perhaps like German corporations or German real estate, if they were to pull out their currency would appreciate, but if they stay in there could be more inflation generated to ease to burden of debt across the Eurozone. Your thoughts?

Megan: German real estate certainly is one potential opportunity but generally I would say given even all the risks that I’ve highlighted particularly the political risks, I think that the most likely scenario over the next year or two is that we go through all these elections and actually in the end we just have the status quo, which would be market-positive. I’m hesitant to get too excited about that because I do think that there are real restraints on the economic recovery in Europe because of the politics as they currently stand, so the status quo means that would continue. Still, I think that would be a risk on development in which case given that you have the ECB continuing to ease now and I think that they’ll continue to maintain accommodative monetary policy going forward, and you have the fed in the US tightening actually, that does means that there might be opportunities and equities in Europe generally so I do think that that is one place that investors could look. In terms of banks in Europe, there are some real problems in terms of the health of bank balance sheets particularly in Italy, Portugal, even France, but banks are incredibly cheap so there might be some valuable investments there. Generally I do think that the valuations for companies in Europe will go up so I would say that European equities are probably a good opportunity now.

FRA: Great. Great insight. How can our listeners learn more about your work?

Megan: You can follow me on twitter, its @economistmeg to not only see what I write myself but to also see my commentary on the latest, greatest in Europe and the rest of the world.

FRA: Great, thank you very much for being on the show and again, thank you.

Megan: Pleasure, thanks for having me.

Abstract by Tatiana Paskovataia, tatiana-p28@hotmail.com

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/01/2017 - Former Federal Reserve Chairman Alan Greenspan: What Is Trump Going To Do When Inflation Hits

Greenspan thinks U.S. President Donald Trump has a math problem with his budget .. Greenspan says that interest rates will have to rise because of very large budget deficits if big programs are not cut .. Interest rates and inflation will go up right along with it.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/01/2017 - Frank Shostak: Central Bank Policies Are Leading To Economic Instability

“Increases in money supply lead to a redistribution of real wealth from later recipients, or non-recipients of money to the earlier recipients. Obviously this shift in real wealth alters individuals demands for goods and services and in turn alters the relative prices of goods and services .. Central bank policy amounts to the tampering with relative prices, which leads to the disruption of the efficient allocation of resources.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/30/2017 - Hedge Fund CIO Eric Peters: What Central Banks Have Done Is “Stunning, Unprecedented”

“Since 1955 we’ve experienced uninterrupted annual inflation. It’s a stunning fact, unprecedented. To an economist in 1955, the coming 60yr inflation would have appeared less probable than a catastrophic meteor impact .. We created history’s greatest volatility-suppressing machine, and it delivered breathtaking stability .. Minsky taught us that stability begets instability. And it stands to reason that our volatility-selling machine will break one day. We saw a glimpse of this in 2008-09 .. But volatility suppression at the lows is much easier in many ways than at the highs. In a crisis, our central banks simply go full-throttle. At the highs though, they seek the unattainable, which is perfect economic balance in a world that is inherently unstable – they attempt to crystallize the entire ecosystem. Which is as arrogant as it is impossible.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2017 - David Rosenberg: The Bond Market Is Reacting To The Facts On The Ground

The stock market is at a critical juncture, and it may be time reduce risk, strategist David Rosenberg says .. He predicts economic growth will slow even more as the Federal Reserve resumes its tightening policy.

“The reckoning will be which market has the story right: Is it the stock market that is de facto pricing in double-digit earnings growth or is it the Treasury market with the 10-year yield at 2.3 percent? .. The bond market is really pricing in a completely different nominal GDP growth world .. The bond market is actually reacting to the facts on the ground. The facts on the ground are this: Year-over-year growth on a nominal GDP cycle already peaked at 4.9 percent. We have never before in the post-World War II period ever have seen year over year nominal GDP growth peak below 5 percent. That happened two years ago.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2017 - Governments Keep Spending, Now Addicted To Cheap Interest Rates

“This is a confidence game .. Back in 2007, the Fed only had to worry about its policy and the contracting economy. The problem they created is that government just keeps going like the Energizer Pink Bunny – it never stops spending regardless of the level of interest rates .. The Fed cannot neutralize the fiscal spending of government .. Government has become addicted to cheap interest rates. If rates go back just to 5%, we are looking at a fiscal deficit explosion the Fed cannot overcome.. The crisis has to hit before a politician would ever act. Once the crisis begins, you cannot restore confidence. The whole thing will have to play out. Moreover, the crisis in Europe helped to send capital to the USA easing the economic pressure here. This is why the USA is holding up the entire world economy right now and a stiff wind will blow over the European banking system. I seriously doubt that anyone can stop the next crisis and whatever they do will then be seen as a failure.” – Martin Armstrong

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2017 - Incrementum Advisory Board Meeting Minutes: Central Bankers Cannot Afford To Let Risk Assets Decline

Heinz Blasnik:

“If I may add a quick point, I’m not actually as long-term bearish on gold as Frank. I’m just saying that many of the short-term macro economic drivers for gold do not look supportive, but the gold price is strong anyway. And I believe that these macro economic factors will probably become supportive in the not too distant future and that the market is already discounting this view. So I’m actually quite positive on the gold price in the medium to long-term. And I’m not even negative in the short term because the demand is there and the price is holding up. There is one more aspect to this, the assets that are most vulnerable to a sharp slowdown in credit and money supply growth are stocks and junk bonds because these assets have become the most expensive on the back of the expanding money supply. And if there is upheaval in these risk assets we will have problems in the banking system and regardless of what the money supply is doing people will look to gold because it’s the one asset that is not dependent on promises and is an effective hedge against trouble in the banking system.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/28/2017 - Dr. Albert Friedberg: Bullish On Risk Assets, Federal Reserve Will Only Shrink Its Balance Sheet When It Sees Accelerating Inflation

“In sum, we see a global expansion gathering strength and being liberally financed by politicians, politically influenced bankers and academics with little feel for reality. It is these academics who are now floating the idea of raising the inflation target to 4% from 2% on the pretext that it will be easier to achieve negative real rates without having to breach the zero-interestrate bound — the next time they are called on to save the world!

There is good reason to believe, then, that we are still early, that the bull is proceeding as it always has, confounding the great majority of experts, defying the well-armed but uncritical skeptics and taking its sweet time. So what is needed is patience (don’t switch lanes — you will always regret it), blindness and deafness (to experts’ concern about valuations, presumed political gridlock, Brexit, etc.) and discrimination (persist with active managers, for their time has come).”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/27/2017 - Macquarie’s Research Team: Financial Repression Is Here To Stay As Governments Run Out Of Options

“Today’s financial repression is set to last for decades (and possibly forever) as policymakers are seeking to keep government funding costs low .. – that’s according to a new report from Macquarie’s economics research team. Since the financial crisis, central banks around the world have embarked on an unprecedented monetary policy experiment. Interest rates have been pushed down to artificially low levels in an attempt to stimulate economic growth and stave off a deep financial depression. Unfortunately, while these policies have worked to some degree, they have also punished savers. This is the very definition of financial repression .. Macquarie argues that governments have made an implicit fiscal policy choice by pursuing this strategy .. Artificially low-interest rates have imposed a tax on savings while at the same time keeping funding costs low, allowing for more borrowing on favorable terms. With this being the case, the analysts argue that rather than signaling a global slump, low bond yields reflect a conscious policy choice to minimize public debt funding costs .. As Macquarie’s analysts point out, financial repression is a headwind to real GDP growth as it involves a transfer of wealth from savers to debtors (in this case the government). Japan is a real-life example of how ineffective this policy really is. Savers have responded to financial repression by increasing the household savings ratio, which has resulted in weekly consumption growth and anemic economic growth.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/26/2017 - Dr. Marc Faber: Indebted Western World Economies Are More Fragile Than Ever Before

Marc Faber thinks there will be 20 – 40% pull back in the markets, we are still in the Trump euphoria stage. He goes on to say that Trump will beg Janet Yellen not to raise interest rates and to keep on printing. Tax reform will not really help the U.S. The U.S. and western economies are terminally sick. The Debt loads are huge and the economic conditions are more fragile than ever before.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/26/2017 - The Roundtable Insight: Richard Duncan On A Recipe For Disaster

Richard Duncan is the Chief Economist at Blackhorse Asset Management in Singapore. He is the author of numerous books including, The New Depression: The Breakdown of the Paper Money Economy, andThe Dollar Crisis: Causes, Consequences, Cures, an international bestseller that predicted the current global economic disaster with extraordinary accuracy. Since beginning his career as an equities analyst in Hong Kong in 1986, Richard has served as global head of investment strategy at ABN AMRO Asset Management in London, worked as a financial sector specialist for the World Bank in Washington D.C., and headed equity research departments for James Capel Securities and Salomon Brothers in Bangkok. He also worked as a consultant for the IMF in Thailand during the Asia Crisis.

Richard has appeared frequently on CNBC, CNN, BBC and Bloomberg Television, as well as on BBC World Service Radio. He has published articles in The Financial Times, The Far East Economic Review, FinanceAsia and CFO Asia. He is also a well-known speaker whose audiences have included The World Economic Forum’s East Asia Economic Summit in Singapore, The EuroFinance Conference in Copenhagen, The Chief Financial Officers’ Roundtable in Shanghai, and The World Knowledge Forum in Seoul. He runs a blog called https://www.richardduncaneconomics.com/ where he has a video newsletter service called Macro Watch, which is available to our listeners at a 50% discount using the code word: authority

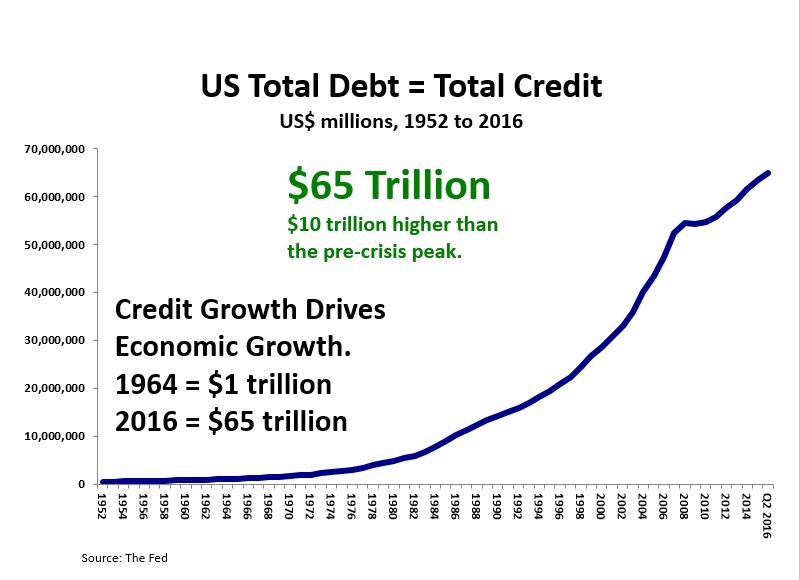

I coined the term ‘Creditism’ to describe an economic system driven by credit creation and consumption, in contrast to Capitalism, which was driven by investment and savings. Creditism replaced Capitalism when money ceased to be backed by gold nearly five decades ago. But Creditism requires Credit growth to survive. The evidence presented in this video suggests that Creditism is in crisis globally because Credit is no longer increasing fast enough to drive global growth, even with record low interest rates. It is not possible to understand the global economic crisis without taking account of the exhaustion of Creditism.” – Richard Duncan

Current Creditism trends:

Once we stopped backing money with gold in 1968, the nature of our economic system changed very profoundly. Credit growth became the driver of economic growth. When we were still on a gold standard, there were constraints as to how much credit could be created, but after we stopped backing money with gold, all those constraints were removed and credit absolutely exploded. Total credit or total debt in the United States first went through one trillion dollars in 1964, and now it’s 66 trillion.

So it’s expanded 66 times in just over 50 years. This extraordinary explosion of credit in the US has completely transformed the global economy. It ushered in the age of globalization, it allowed countries like China to be revolutionized from a very poor, developing country, to the second largest economy in the world. What I’ve seen is even adjusted for inflation, every time credit has risen by less than 2% in the US going back to 1950, the US goes into a recession. And the recession doesn’t end until we get another big surge of credit expansion. So it’s crucial to be able to forecast credit growth if you want to be able to understand what’s going to happen in terms of economic growth. And it’s been very weak since 2008; we’ve now hit the point now where the private sector, the households, are so heavily in debt that they just can’t continue taking on new or additional debt to make credit expand enough to drive the economy.

So this is the real point: once credit started to contract in 2008, the global economy began to spiral into a new great depression. And it was only the expansion of government debt that prevented that from occurring. US government debt has more or less doubled since 2008, it is roughly $19 trillion now. It was the expansion of government debt that kept total credit expanding, and that prevented the world from collapsing into a depression.

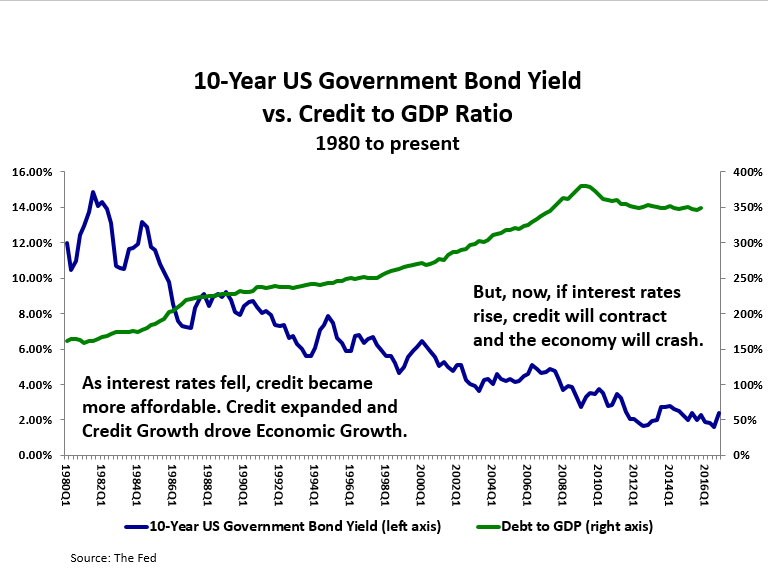

The key as to what is going to happen next to the US economy and the global economy is interest rates. Interest rates are crucial to the future of Creditism as I call it. Going back to 1980, interest rates in the United States have gone down very steadily.

The 10-Year US Government Bond Yield in the early 80s was as high as 15% and now it’s gone down to around 2.2% today. And as the interest rate fell, this made borrowing more affordable, so the Americans were able to afford more debt. They became increasingly indebted, and we can see this by looking at the ratio of total debt to GDP in the United States. Now when I talk about total debt or total credit, I mean all the debt in the country. The government debt, the household sector debt, the corporate debt, financial sector debt, all debt. In 1980, it was only around 150% total debt to GDP, now it’s about 350%. So as credit expanded, the credit growth drove the economic growth in the United States. And as the US economy expanded, US imports from other countries grew, and that drove the global economy.

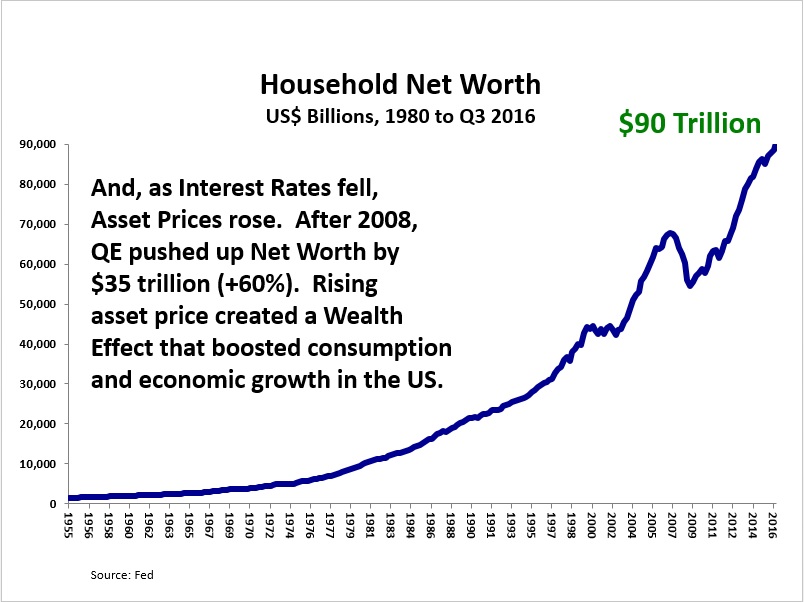

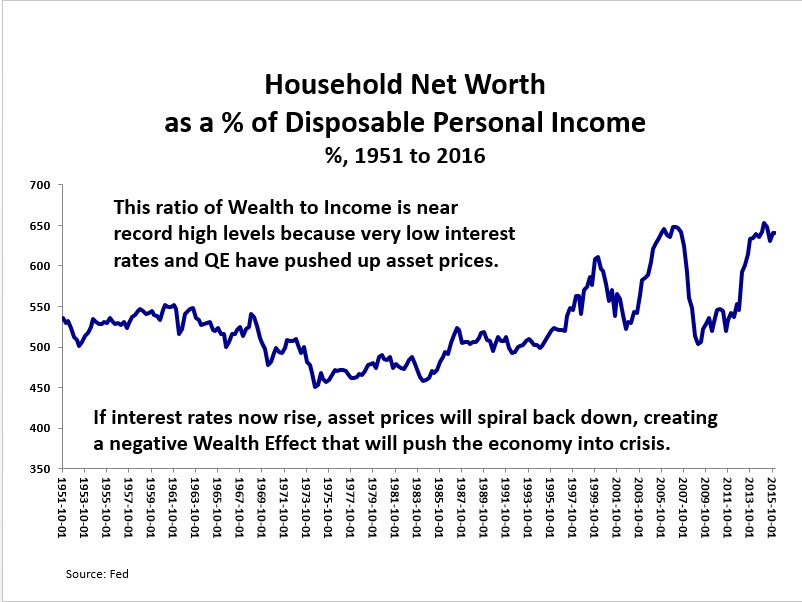

As interest rates have fallen, Asset prices have gone up. The stock market, property market, bond prices, they’ve all gone higher as interest rates have gone lower. The best measure of total wealth in the United States is household sector net worth.

Household net worth is now $90 trillion, it’s gone up by 60% since the post-crisis low in 2009. The reason this wealth has expanded is that the government and the fed took very aggressive action to reflate the global economy after 2008. The fed and the central banks around the world had interest rates to near 0% and reflated the global economy.

Going back to 1950, the ratio of wealth to income has averaged about 525%. During the property bubble, this ratio went up to about 650%, and of course, the property bubble blew up, and the ratio went back down to its normal level of about 525%. But now this ratio has once again expanded and is now at its back at its all-time peak level at 650% once again. And this is telling us that asset prices are very high, and the stock market is very expensive, property prices are expensive. And that means interest rates now begin to move higher, then asset prices are very likely to fall. So we’re seeing a situation now where interest rates are the key, because if interest rates move higher then credit is going to contract. That’s going to throw the economy into a severe recession, and on top of that asset prices would have a very significant correction or crash, that would cause a negative wealth effect, and that would also cause a US economy and the global economy to go back into severe recession, or worse.

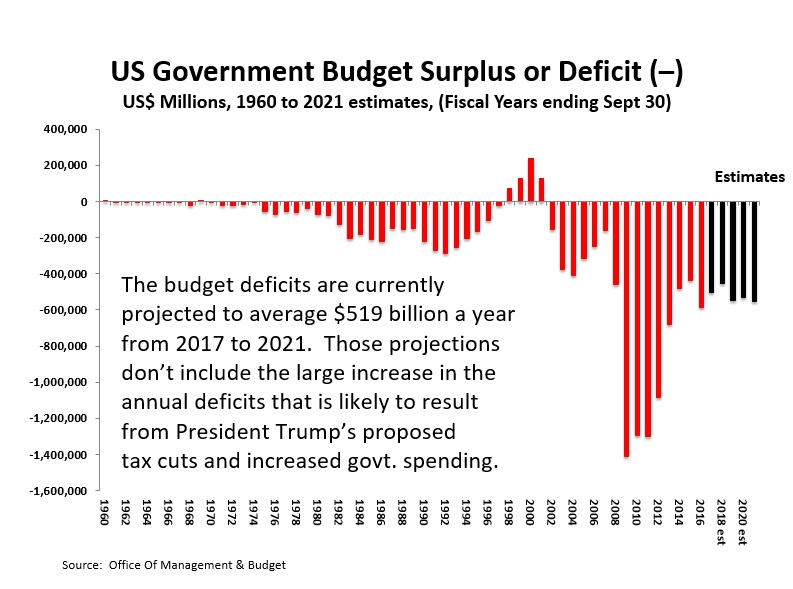

The US budget deficit

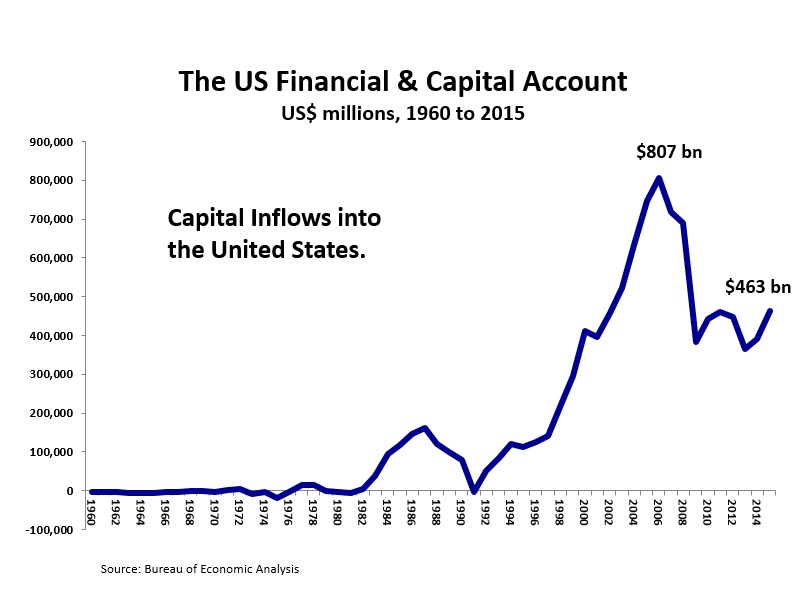

When the government borrows money it tends to push up interest rates. For instance, if the government doesn’t borrow anything then there’s less demand for money and interest rates will be lower. But if the government were suddenly to borrow $3 trillion, then that would suck up all the money available in the economy and that would push interest rates to very high levels. So when the government borrows more, it tends to push up interest rates. This is assuming all else is unchanged, but over the last many decades, something very important has changed. Once the Bretton Woods system broke down in 1971, the United States discovered they could run very large trade deficits with the rest of the world. This is important because it means the US will have very large capital inflows. When the US has a large trade deficit, it will have an equally large amount of capital inflows coming into the country to finance that trade deficit. The larger the capital inflows are, the easier it is to finance the government’s budget deficit at low interest rates.

In 2006 we had about $800 billion in capital inflow, and that was enough to finance the entire government budget deficit that year a few times over. So these inflows are very important financing the budget deficit at low interest rates. If Trump is successful in his promises to cut taxes and increase government spending, then it’s going to make their budget deficit considerably larger.

The Capital Inflows are the mirror image of the Current Account deficit. When the Current Account Deficit grows larger, the Capital Inflows also grow larger, making it easier to finance the budget deficit. But, when the Current Account Deficit shrinks, Capital Inflows also shrink, making it more difficult to finance the budget deficit at low interest rates.

President Trump’s plans to force US companies to bring their factories back to the US, to renegotiate trade deals and/or to impose trade tariffs on China and Mexico would all cause the US Current Account deficit to shrink. A smaller Current Account deficit would cause the capital inflows into the United States to shrink, too. Less capital inflows would mean less demand for US government bonds. That would push up interest rates and pop the asset price bubble. So, we must keep a close eye on the US Current Account Deficit because it will determine the size of the capital inflows.

What Could Cause Inflation to Rise?

Inflation has fallen since the early 1980s because increasing trade with low wage countries has pushed down US wages and the price of consumer goods. Now, however, if the US imports less from low wage countries, the price of manufactured goods will rise, US wages will rise, and inflation will rise. Forcing companies to bring their factories back to the United States or imposing trade tariffs on imported goods would cause inflation to increase. Increased government spending could also cause inflation to pick up.

The Undesirable Consequences of Eliminating the Trade Deficit

If the US reduces its imports, the global economy will shrink. If the US eliminates its $1 billion a day trade deficit with China, China’s economy could collapse into a depression that would severely impact all of China’s trading partners, and potentially lead to social instability within China and to military conflict between China, its neighbors, and the US. Additionally, if the US Current Account deficit returns to balance, the global economy will suffer from insufficient Dollar liquidity, which could cause economic stagnation or worse. A reduction of imports from low wage countries would cause US inflation to rise, which would push up US interest rates. The elimination of the Current Account deficit would cause a sharp reduction in capital inflows into the US, which would also cause US interest rates to rise. Higher interest rates would cause credit to contract and a sharp fall in US asset prices, which could cause the economy to go into recession. It could also cause a wave of credit defaults in the US and around the world, potentially leading to a new systemic financial sector crisis.

Moving Forward

The US could stimulate the economy “the old fashion way” by increasing military spending and starting a war, or they could invest in 21st century industries and technologies. We could invest a trillion dollars over the next 10 years in developing renewable, green, solar energy. And if we did that, we could then re-structure the entire US economy, and induce a new technological revolution that would be so profitable, that we would pay off these investments many times over. We could grow out of this crisis, rather than collapsing into a new great depression.

Conclusions

The proposals outlined thus far by President Trump suggest that:

The budget deficit would grow larger (due to tax cuts and increase government spending);

The current account deficit would shrink (due to renegotiating trade deals, bringing US factory jobs back to the US and possibly trade tariffs);

And inflation would pick up (due to increased government spending, higher US wages, pressure on China to push up the RMB and, possibly, tariffs).

More about Macro Watch

Macro Watch is a video newsletter published by Richard Duncan. Every two weeks a new video is uploaded describing something important going on in the global economy, and how that’s likely to impact asset prices. Macro Watch monitors and forecasts credit growth and liquidity to measure and anticipate economic growth. You can subscribe to Macro Watch at https://www.richardduncaneconomics.com/ where you can save 50% with the discount code: authority

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/24/2017 - John Mauldin On The Pension Fund Crisis

“Many, perhaps most, current city and state workers simply aren’t going to get anything like the pension

benefits they have been led to expect” .. Fred Sheehan: ‘We are promised… is the haphazard refrain often encountered when the reduction of pension claims is mentioned. Promised or not, one distinguishing feature of non-federal government spending commitments stands out: only the United States has a printing press. States cannot print money. They can earn returns on their pensions’ invested assets, they can sell city hall, lay off the public works department, and tax, but an underfunded pension plan can only pay claims with dollars that exist.’ .. This list of options is actually too generous. Sell city hall? That presumes someone will buy it. Lay off the public works department? Not good for property values. Raise taxes? Right, on all the people in those houses without sewage service .. Repeat Sheehan’s last line and burn it into your brain: ‘An underfunded pension plan can only pay claims with dollars that exist.’ No one gets anything if the money isn’t there, and in a disturbing number of places it isn’t.

We know that pension plans typically have only 40–50% of their assets in equities, something like 40% in bonds, and the rest in real estate and alternative asset classes. How do you get 8% from that mix? Keeping 40% in bonds at 3% (if you’re lucky) means everything else has to make 15%. Marc Faber, who is even better at scaring people than I am, points out something that should be obvious but apparently is not: Pension plan funding ratios have been declining even as financial markets have posted impressive gains: ‘I find the deteriorating funding levels of pension funds remarkable because post-March 2009 (S&P 500 at 666) stocks around the world rebounded strongly and many markets (including the US stock market) made new highs. Furthermore, government bonds were rallying strongly after 2006 as interest rates continued to decline sharply.’

Like state and local pension obligations, US federal government pension obligations are also basically unfunded. They are expected to come from future tax revenues. Those obligations are the bulk of the over $100 trillion in unfunded liabilities that show up in the estimates of how much the United States is really in debt. That money is going to have to come from somewhere. But just as the United States will never default on its actual debt, I truly don’t believe we will default on US government pension obligations.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/23/2017 - Central Banks Have Bought A Record $1 Trillion In Assets In 2017

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/23/2017 - Accommodative Monetary Policy Is Encroaching On Fiscal Policy

“We believe that the ECB is presently using monetary policy in effect to conduct fiscal, as well as monetary policy. Elected politicians should be up in arms; that they are not would imply either that they do not understand this or that they simply accept it. This may provide an interesting pointer as to the future of the EU itself .. Private-asset QE purchases by the ECB is a big deal, because the selection and execution of these asset purchases benefits some elements of the private sector at the expense of others .. The absence of any objection from the vast majority of eurozone governments implies acceptance of this usurpation of power by the ECB. Perhaps this portends a pathway to federalization among those countries (unlikely to include Germany) who have chosen happily to acquiesce.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

04/23/2017 - Allianz’ Mohamed El-Erian On Financial Repression

Mohamed El-Erian, chief economic adviser at Allianz SE and a Bloomberg View columnist, discusses global economic risks with Tom Keene and Francine Lacqua at the IMF and World Bank meetings. (Source: Bloomberg)

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/07/2017 - Central Banks Injected A Record $1 Trillion In 2017 – “It’s Not Enough”?!

05/07/2017 - Central Banks Injected A Record $1 Trillion In 2017 – “It’s Not Enough”?!