08/08/2017 - Peter Boockvar On How The Monetary Boom Ends

“The ‘crisis’ (or ‘credit crunch’) arrives when the consumers come to reestablish their desired allocation of saving and consumption at prevailing interest rates. The ‘recession’ or ‘depression’ is actually the process by which the economy adjusts to the wastes and errors of the monetary boom, and reestablishes efficient service of sustainable consumer desires … Continually expanding bank credit can keep the artificial credit-fueled boom alive (with the help of successively lower interest rates from the central bank). This postpones the ‘day of reckoning’ and defers the collapse of unsustainably inflated asset prices … The monetary boom ends when bank credit expansion finally stops – when no further investments can be found which provide adequate returns for speculative borrowers at prevailing interest rates. The longer the ‘false’ monetary boom goes on, the bigger and more speculative the borrowing, the more wasteful the errors committed and the longer and more severe will be the necessary bankruptcies, foreclosures, and depression readjustment.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/08/2017 - The Roundtable Insight: Dan Habib On The U.S. Real Estate Market And Interest Rates

FRA: Hi welcome to FRA’s Roundtable Insight .. Today we have Dan Habib. He’s been involved in the mortgage industry for over 15 years. He was an integral part of mortgage market guide where he created and managed the sales team and helped grow their subscriber base. Dan later worked for Morgan Stanley as a financial adviser where he was a member of the number one ranked Barens financial advisory team in New Jersey. He’s held his serious 763 65 31 and life and health insurance licenses. He’s also one of the founders of NBS highway and has been instrumental in its significant growth during the past four years as a senior market analyst. Welcome Dan.

Dan: Hey thanks for having me Richard.

FRA: Yeah, I just was wondering, could you give us some background on NBS highway and mortgage market guide. What they are? What type of services you offer?

Dan: Yeah of course, so mortgage market guide was kind of the original company that my father Barry and myself had started. We had sold that company and we are now running NBS highway air which we created about four years ago. But a similar principle. Really it’s a service for mortgage professionals where we try to help educate them each and every day, help them close more opportunities that they’re given and also gain and protect new and current referral relationships. We do that by really breaking down what’s happening in the market for them each day, breaking down the economic reports and as that pertains to the mortgage industry and interest rates. We also really help them with timing of blocking and floating their loans to avoid costly reprices or get better interest rates for their customers. We have a bunch of proprietary tools on the site and some really great real estate data that I think really helps our customers showcase and quantify the opportunity that exists in homeownership today. We really try to help (really kind of) give some insights and combat a lot of the negativity that you see in the media especially as it pertains to you know the health of the housing market, and you know some of these economic reports that come out. You know it’s our view that we think the media really just doesn’t really understand it. And you know you see all these reports and all these articles on CNBC all the time about how you know it’s more expensive to buy than rent in every state in the United States. And you know you have guys like Greg Carrdon, who was just on a video on CNBC and said that you have no business owning a home unless you have 20 million dollars in the bank and different things like that which you know ultimately our customers are viewing and seeing and you know in a marketplace where you have really tight inventory. Our customer’s customers are saying individual looking to buy a home and you know in a marketplace we have really tight inventory you know across most of the country and you know these customers aren’t getting a lot of bargains because of that. Now a lot of the time that come in at full asking price or maybe several thousand dollars above and they watch this negative media it’s no wonder why it’s easy for them to maybe flake out and maybe go out and rent. But ultimately it may not be the best decision for them. So we help them to really kind of get to the truth and meet behind the strength in the housing market and help explain that to our customers so they can explain it to theirs.

FRA: Can you help us provide insight into that? So you mentioned the mainstream media doesn’t have that sort of more accurate view of what’s happening. What is the current state in the U.S. housing markets?

Dan: So we think the housing market is strong you know a lot of times people have concerns. We’ve seen some good appreciation, are we in bubble like conditions? Well you know if you look at the facts we look back you know during the housing bubble years those 6 years. So we had an oversupply in the market, we had nearly doubled the amount of inventory levels that we have currently. So certainly not seeing an oversupply in the market from that dynamic. When you look at the demand side, the main demand remains extremely strong. You know one of the kind of metrics that we look at, we like to look at demographics and you know one of the most famous guys, if you look at demographics was Lee Iacocca you know and he was very famous. He worked for Ford and he saw that all these baby boomers were getting older and they needed to have a kind of stylish car and he turned up creating the Mustang, and ended up being the most popular car for Ford at the time and it was their most profitable. So it’s important to look at demographics. When we look at the demographics, Zillow says that the median age for first time home buyer is thirty three years old. So if we take a look at the birth tables and we go back 33 years ago, we can see where the birth rates were and that was in about 1984 or so. And then you can see what’s happened the next nine years. There was a huge surge in births each year greater than the previous year. So what that’s telling us is that over the next eight years you’re going to see a greater and greater and greater crop of individuals turning 33 in either coming into the housing market to either buy or rent. So we’re going to see strong demand I think for the next eight years and it doesn’t fall off the cliff after that, it plateaus at some of the highest levels since the baby boomers. So we think that we’re going to see some really strong demand, supply is tight. Obviously the first law of economics you learn as you know, tight supply and strong demand, it’s going to be supportive of home prices. But also we think that the kind of dynamics that we’re seeing in place are going to persist because builders have a lot of challenges out there right now. They’re highly regulated, they’re having a hard time finding labor and you know lenders just aren’t lending to them on spec like they used to. You know they used to be like build it and they will come, but you know they got burned in the past. So we think that the dynamics are going to stay in place. You’re going to have some tight supply, you’re going to have some really strong demand. And you know the media really I think focuses on the amount of sales. Now obviously if we look at the most recent reports that just came out we had existing home sales and new home sales. And you know both of those were decent reports of course we’re not seeing the amount of sales that we saw you know 10 years ago but we’re still seeing sales of new homes so that were we’re up like nine point one percent in the year over year basis and that’s with really tight supply. So you know if there was more inventory out there I think there’d be more sales. But I think that the dynamics are still in place are very strong and healthy housing market.

FRA: And is it localized like do you see differences between what’s happening in Miami New York versus perhaps less volatile markets. You know that I’ve appreciated in the Midwest.

Dan: Yeah. Well sure it certainly is localized. Overall if we were looking at you know as a whole in the U.S. appreciation you know depending on which report you’re looking at it’s been about six and a half to like 6.9 percent over the past year and forecast there for it to be above 5.2 to 5.5 percent depending on where you’re looking at of the nation for the year going forward. Of course you know that can vary in different markets. You know what’s funny is that it seems like the new markets that are doing the best are the ones that have legalized marijuana, you know in Portland and Seattle and Colorado, Denver those are actually leading in the way with depreciation over the last year. So they’ve been pretty hot.

FRA: Is there like a generational change or what about the millennials? We hear stories where they just want to rant or I mean do they want to buy houses at some point maybe because they’re strapped with debt initially but do they have the intention and the desire?

Dan: I believe they do. You know if you take a look// I think obviously the millennials are a different generation. But you know if we look at kind of like a normal life cycle right I mean if we look many years ago it was pretty normal for an individual to kind of get out of high school get married and start a family and have kids and buy a home. And that happened much earlier, you know people were getting married in the 20s, having kids and now it’s just kind of move back. You know obviously life expectancy got a little bit longer too, but millennials are taking longer to do things you know they’re not going to be like you know the guys in Stepbrothers, 40 years old living in their parents basement. I think they still do have they want to buy a home. But I think that you know they’re just taking a little bit longer to do something. So I think there’s some pent up demand there for sure.

FRA: What about the effect of interest rates on the housing market. How do you see that?

Dan: I think right now is a great time to buy a home. Interest rates I think are you know still really attractive you know interest rates on a 30 year fixed you know anywhere probably between about a quarter point a half percent right now. You now its funny, someone might say oh its high. You know I think all of you know the average interest rate will last like 45 years in the quarter. So we’re still at really attractive levels. And I think now’s the time to buy because you know if we take a look at the Fed. We know from the Fed’s latest meetings and their statements that they want to start where Peter Book likes to call “quantitative tightening” where they’re going to start unraveling their balance sheet and they’re going to do it in a measured pace where they’re going to let you know four billion or more in bonds and 6 billion in Treasuries kind of roll up their balance sheet each month and then kind of revisit each corner and I think increase it by those same amounts and once they do that you know I mean the fed’s the biggest buyer of mortgage bonds and treasuries so once you have the biggest buyers start to back out a little bit I think that rates are eventually going to have to start to move up towards the end of the year. If they start doing this in September and out in September. So you know I don’t think rates are going to go crazy because they go up half a percent or so once the Fed starts doing this. Yeah. So I think I think now is really a good time to buy a home.

FRA: As you see the rates going higher would that have a dampening or a negative effect on the housing markets?

Dan: I don’t think it’s going to affect purchase business too much to be honest with you. But obviously refinances of course you know, what’s interesting is if you look at the most recent mortgage application data that we got just actually this morning, it shows that refinances just rates are up about half a percent from the 50 basis points from this time last year and refinances are down 41 percent. So obviously it has a big impact on refinancing interface. They have a percent in of course that’s going to have an impact further on revise. But I think the purchase market’s very strong.

FRA: And in terms of Fed policy, the Federal Reserve on interest rates. How do you see that playing out? What point do they stop raising rates is the big question?

Dan: I think that the Fed wants to get one more hike in December. I think in September, I see them starting the announcer they’re pointed in on their balance sheet a bit and I think it has to. So long as you know we see things remain the way they are now. I think it was over in December and then I think they’ll probably pause a bit until maybe mid next year. Everything is going to depend on the data. Obviously I mean the jobs data I think has been sufficient for what they want to do. I think that inflation has been obviously a little bit stubbornly low. You know if you look at the most recent data from this morning or yesterday was with the personal consumption expenditures came out and that’s the FEDs favourite measure of inflation and that core rate showed only one and a half percent. Obviously below the 2 percent that they’re looking for we think that the Consumer Price Index is a better measure because it has a heavier weighting towards the cost to put a roof over your head as well as out-of-pocket medical expenses. So I think it shows you know true inflation a lot better. But you know for whatever reason it is the Fed likes to focus on the PCE for that has been stubbornly low. And I also think that the Fed expecting to see the labor market tightening, they’re expecting to see some wage pressure at inflation which we haven’t really seen yet either but maybe we’ll start to see that coming. You know on Friday we’re going to be getting the jobs report which is obviously going to be very important for the stock and bond markets, certainly could have a big impact depending on how that comes out. Know we did get the ADP report today which is about in line with expectations. I believe it was about like about a hundred and seventy eight thousand jobs were created last month. So a decent number. I think a strong enough number for the FED. But we’ll have to see how that BLS report comes out. And really I want to be paying close attention to that average hourly earnings numbers see if we’re seeing any wage pressure inflation there but like I said I think the FED is going to try to get one more hike in this year and then kind of see some of the data that comes out from there.

FRA: Do you think there’s a look at the Federal Reserve policy from the perspective of raising interest rates up to a point where it doesn’t go higher than a 10 year Treasury bond yield because that’s some point that could turn the yield curve into an inverted yield curve you know potential recession type of thing.

Dan; Yeah of course, you know the tend to spread is something that we actually have on our site for our subscribers as a good recession indicator. You know it’s been pretty accurate one. You know I think that FEDs going to be careful I think that you know they’ve obviously done this whole QE experiment for many years and I don’t think they’re going to want to raise rates too quickly to you know send the economy into a tailspin.

FRA: And what about the actual purchasing power of a home. Just what are your thoughts on that? A lot of our commentators have mentioned a distinction between nominal terms and real terms so that if you take the price of a house today and divide by you know how many cups of coffee you can buy today versus how many cups of coffee can buy in the future. You know some measure of inflation. Do you see the actual purchasing power of a home as increasing nominally and in real terms or just perhaps nominally?

Dan: I think I see an increasing in real terms. I think that inflation, you know remains pretty low. I’m not too worried about it getting too out of hand. And any of the reports, you know we’re looking at a we have some great real estate data for every kind of a metro area in the country and you know what I’m seeing out there are some really strong appreciation forecasts. You know I think that it’s going to some really strong power.

FRA: And just your thoughts on the political situation in the USA. How is that affecting the housing market interest rates and the overall financial markets?

Dan: Well I think that initially the financial markets obviously got a really nice push from the new administration and you know we’ve seen the stock market has been on some tear. It’s been unbelievable. You know now and 22000 today. And you know even though the administration has been unsuccessful and you know ….and you see how we do on taxes. You know I guess some would argue that you know markets are moving higher. Maybe not so much based on Trump anymore on the strength of the stock and the earnings that we’ve been seeing in some of the fundamentals. But you know I would love to see some of the stuff from Dodd-Frank. You know kind of get loosened up a little bit and I think that can have a good impact on the housing market. But you know again, its been a little disappointing to see really nothing pass through, you know so far.

FRA: Just overall, your view of the housing market for the next 5 to 10 years?

Dan: Like I said before, I think the housing market’s going to remain very strong. I think we’re going to see some really strong appreciation levels. I think that you know one of the things that has been encouraging is that if you look over the last several years we’ve seen some really good levels of appreciation and you know the media has been negative on the housing market the last five six years or you would have missed a great opportunity. But you know one of the things I think the media gets wrong is the affordability. You know we have great affordability data for every measure for every country and what I’ve seen is that for most markets affordability has remained pretty level. I think the media makes the mistake of thinking that if a home price goes up automatically affordability has to go down. But obviously there’s a couple of other things that go into that number obviously it’s the home price but it’s also interest rates, it’s also wages and jobs and you know if we were to use the media’s kind of explanation well that would mean that if home prices went down all of a sudden affordability has to go up. But what happens if interest rates skyrocket what happens if you lose your job? Does that home get more or less affordable? Obviously less affordable. So I think we’ve been seeing until homes are still relatively very affordable. I think the dynamics of tight inventory are going to persist. I think demand is going to remain strong. And I think it’s going to be a recipe for a really strong housing market for years to come. Not really seeing any kind of you know conditions that would worry me like any bubble like conditions and you know historically you know even if there were talks of recessions and stuff. If we were to look at the last 10 recessions from World War 2 you know nine out of the last ten of them, housing has actually done really well. And you know obviously the last one, housing prices actually started going down a little bit before the recession and really it was more like the housing bubble I think kind of led us into the recession and not vice versa. So you know I think that housings going to be very strong for the years to come.

FRA: That’s a great insight. Overall the discussion and I appreciate very much having you on the show Dan.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/04/2017 - Alan Greenspan: Interest Rates On Government Bonds At Historic Lows

Former Federal Reserve Chair Alan Greenspan shares his concerns about a bubble brewing in the bond market.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/04/2017 - Mish Shedlock: Central Banks Do Not Count The Inflation That Went Into Asset Bubbles

“Central banks are puzzled because they do not know what inflation is, or how to measure it. For example, instead of using home prices in the CPI, they now use Owners’ Equivalent Rent. In general, asset prices do not count. Bubbles in stocks and bonds do not count. The massive global QE liquidity went to someone, as money always does. The liquidity did not go where the central bankers wanted. It went into asset bubbles .. It’s no mystery why central bankers are mystified: Collectively, they are economically illiterate fools engaged in Keynesian and Monetarist group think.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/03/2017 - Mish Shedlock: The War On Cash Is Moving At Breakneck Speed

“Australia’s Black Economy Taskforce has come up with a list of 35 ‘consumer-focused’ proposals to crack down on cash. The taskforce blames consumers for holding cash and for not getting receipts .. Michael Andrew, the head of the taskforce, proposes nanochips in $50 and $100 notes so the government knows where the cash is. Cash will expire after a designated period of time .. On November 8, 2016, India’s Prime Minister Narendra Modi stunned the country with an announcement that 500-rupee ($7.30) and 1,000-rupee notes, which account for more than 85 percent of the money supply, would cease to be legal tender immediately .. The war on cash is moving at breakneck speed.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/02/2017 - Martin Armstrong: Seizing All Bank Accounts Throughout The EU

“Many financial firms in London claim to be looking to move to Frankfurt or Paris with BREXIT. They are going to have a very rude awakening. The proposition to demand all euro clearing takes place inside the EU will be the death of Europe – not the rebirth. The dominating position in Brussels among the majority is control the financial markets to prevent any free market movement against the designs of the EU Commission. Additionally, this position of draconian absolute dictatorial control over European markets includes a pan-European freezing of all bank accounts in the event of an impending banking crisis. The EU Commission is deeply concerned what happens when the EU stops its life-support for Eurozone government debt. They are actually considering the way in which multi-day cash disbursements can be practically implemented in order to resolve emergency measures for banks. Their plan is looking at a prolonged banking and financial crisis that would be 20 to 30 days in duration. If government debt crashes with rising rates, then the reserves of banks will decline and this could result in a banking crisis unleashed when the EU stops its life-support program. The EU Commission will freeze al bank accounts for one week and up to one month if the crisis continues. When Banco Popular went into crisis in Spain, there was a Bankrun which unfolded as a contagion against other banks in Spain. In Greece, accounts were frozen and cash withdrawals were limited for extended periods. This is an ongoing proposition since not all EU members agree. Some countries already have legislation allowing for a total bank freeze such as Germany. Instead of bailouts, we have now move even beyond bail-ins, and into the realm of just total seizure. It is more likely that such a freeze will not preserve banks, but will result in more bank failures.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/02/2017 - McAlvany Podcast: The Economic System Is Always Changing Faster Than The “Controllers” Can Learn

Richard Bookstaber: People Cannot be Controlled like Automatons thus Crises Repeats

About this week’s show:

-The economic system is always changing faster than the “controllers” can learn

-Fed policy and manipulations today are “so yesterday”!

-Unlike flood insurance, Financial Insurance INCREASES the likelihood of crises

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/02/2017 - The Roundtable Insight: Charles Hugh Smith On Where The Jobs Are

FRA: Hi, welcome to FRA’s Roundtable Insight .. Today we have Charles Hugh Smith. He’s author leading global finance blogger and philosopher, America’s philosopher, we call him. And he’s the author of nine books on our economy and society, including neurotically beneficial world automation technology in creating jobs for all resistant’s revolution liberation, a model for positive change, and nearly free university in emerging economy. So we will talk about those books today and he also has a blog of twominds.com. That blog has logged over 55 million page views and is number 7 CNBC’s top alternative finance sites. Welcome, Charles.

Charles: Thank you, Richard. Well, let’s hope that impressed your resume, I am able to shed some light with you on education jobs and the impact of automation.

FRA: Yeah. No, sure, yeah great background and insight as always. And you’ve been very generous in providing some charts today, which will make available on the website for people to download and to view if they listen to this podcast and so yeah maybe we begin with the big picture. What you think education is? Why there is a problem? Also maybe how financial repression initially has created a lot of debt in student debt market and then take it from there.

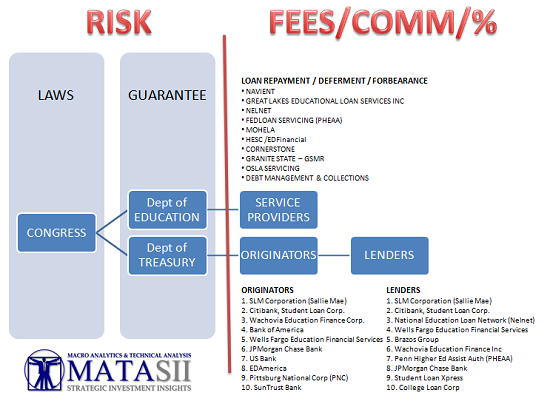

Charles: Ok, well I take a stab at it and you can fill in whatever I miss for which I’m sure will be a lot of changes. You know Richard the thing I concluded and I’m not alone in this, is that higher education throughout most of the developed world and even in fact even in the developing world, like China. It’s a cartel, in another word it functions like a cartel and this is part of the financial repression. aspect there is no competition in the university and college system in the United States. and that every school just boost the tuition based on its peers, and the reason why they have this cartel like pricing power is because they control the credentials. The issuance of credential, diploma, which students have been brainwashed into feeling that they must have or else they are doomed to a life of unfulfilling work and poverty and so this is given in pricing power and that’s completely unconnected to either the value of the credential they are issuing or to their competitive value compared to other universities. And so you’ll have a really pretty nothing special you know state school charging tens and thousands of dollars and not that much less really than Ivy leagues which often give scholarships as well because of their huge fund that they accumulate from you know they’re highly paid graduates. and so this has created a financial repression that focuses solely on the students of higher education.

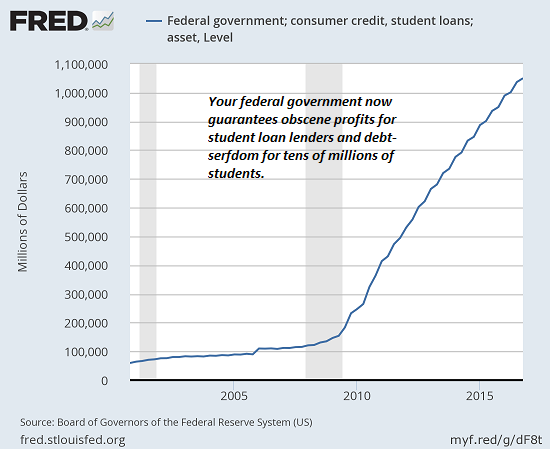

So we can see that student loans have risen from essentially almost nothing to 1.4 trillion and as this is weight more and more heavily on students and they start defaulting right and so the result of this is that cartel has now handed over the funding of its ridiculously over priced service to the federal government, which has now taken on all this student loan debt as an asset if you can believe that. And Gordon Long and I did a program where we drill down and discover that there is an enormous shadow banking system that which has benefited and profited immensely from processing all these you know trillion student loans.

FRA: yeah absolutely.

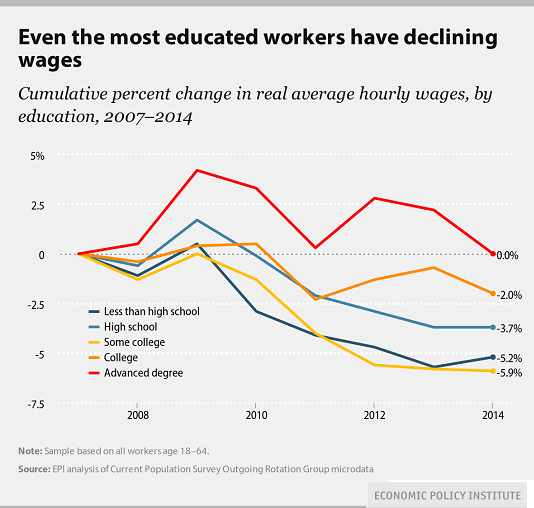

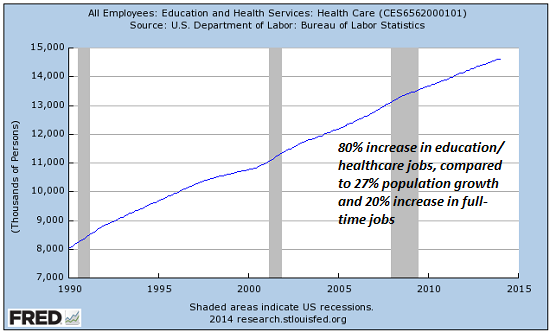

Charles: Yeah now as we seen these enormous costs increase, into like three or four hundred percent increases in tuition while the rest of the economy is more or less flat lined. We find it even the most educated worker has declining wages. And the chart I have submitted was from the 2006 era, you know the era of financial crises. and since then despite this so called recovery, wages of all workers have either stagnated, you know zeroed out or they declined as much as 5 percent.

So even college educated people are not reaping any benefits from this enormously expensive higher education and I have another chart that shows as a percentage of the workforce the number of people with a bachelor’s degree and higher has of course been rising for decades and as a substantial part of the workforce now and so now we’ve been told that getting a bachelor’s degree or higher is like a ticket to you know permanent prosperity and all this and the numbers don’t add up with that.

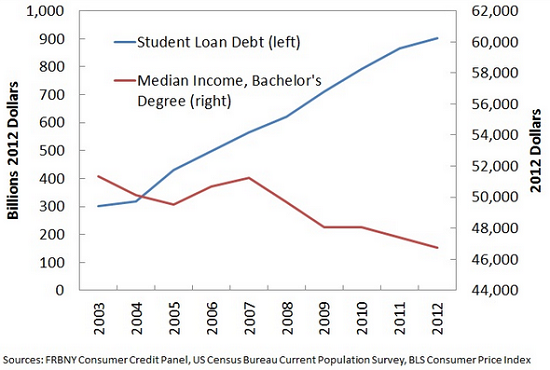

And we also have a chart here that shows student loan debt skyrocketing, but the median income earned by people that have a bachelor’s degree it has been declining. And so there is a mismatch here between the cost of education and the payoff. And people are looking around for answers like why is this? And of course, one reason is that the growth in higher education budgets is largely with results of more administration, more managerial staff being added while the actual teaching staff is not gone up by much.

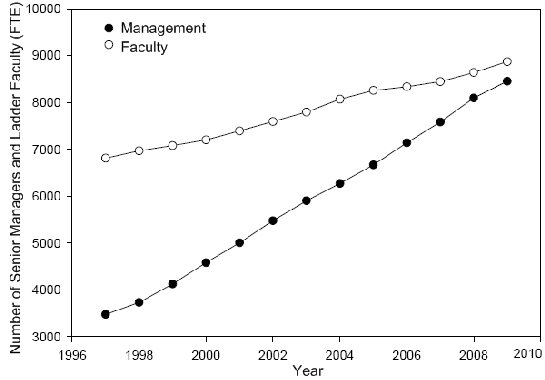

I have a chart here that happens to be to the University of California system. Probably the largest public system in the US, just due to the size of California having 38 million people. And you can see that the number of management staff has skyrocketed while the number of teaching staff has edged slowly higher and they are about the same now. The system has almost as many administrators as it does professors and of course, as you and I were speaking before we started recording, the salaries in higher education are not in competition in the sense of the real world of entrepreneurism or managing in legitimate companies that turn a profit. A lot of these management positions are like they have assistant dead to an assistant associate dean of student affairs and the guy is making quarter million dollars.

It’s a completely out of touch with the private sector in terms of productivity and value of that position, which is really a net negative because the students are paying for all this additional management of their education and yet the quality of the education is clearly not keeping up with what the economy is demanding. Are you seeing the same thing?

FRA: Yeah the same thing in Canada where salaries could be 250 thousand and these are typically government type roles right positions and even though the University of Toronto, it’s also more than that because of the pensions, it could be 80 or 90 percent after they retire, so it’s just huge salaries and its rehashing and repeating the same course of teaching the same thing over and over again and there’s not much you know excitement to that. And you know you have to wonder what is the issue here, is its accreditation. Is that what is driving this you know partly and also the financial repression aspect of it. You know lower interest rates, the ability for the middle class to make loans right at high numbers so the wealthy could essentially pay cash; the poor have potential grants, so the middle class would have to come up with loans. Effects everybody has a virtually unlimited source of money to pay for the tuition and there is a play on the value of having an education, where everybody realizes that, but it’s gone beyond that where they are taking advantage of that value.

Charles: Right, right, and one pernicious aspect of financial repression is suppression of competition and so you know there is no competition really in higher education. The degree, there’s nothing in this whole system that actually measures in quantifies or compares the supposed education that student has gained or the value of the education and compare it to other competing schools. So studies like academic drift, which was a study that came a few years ago found that a huge percentage of university students in the US gained no appreciable knowledge after found years in a university. In other words, they didn’t really learn all that much, that could be identified. And so this has driven a movement away from businesses relying on credentials and grade point averages. For instance Google very famously used to focus on your grade point average and your course work and those kinds of stuff, and they realized it did not connect it didn’t correlate with the productivity and creativity of the worker so they have now moved away from that model and that the third of their hires don’t have bachelors degree or bachelors of science and no college degree at all, and so this is I think what’s what businesses and even government agencies are finding out that the credentials doesn’t say anything about the student which is why in my book in the university I suggested that the solution is a new model in which we are credit the student and not the institution in shirt the student has to prove that he or she has learned stuff and knowledge basis that are of value to the employers so that we would accredit each student and never mind the institution they would be out of it so if they failed to actually educate the student then they would get nothing.

FRA: so is it more of the alignment of the education towards what is being asked for or needed in the economy?

Charles: Yeah, that is right its aligning the education with what is needed in the economy and also aligning it or realigning it with to the cost of education so worthless education should cost almost nothing. if the institution can’t actually help the student or learn what is needed then the institution doesn’t deserve the tuition and that would revolutionize the higher education but Richard I’m just going to shift just a little bit here, and talk about what do we mean by the emerging economy and how are the skills and the knowledge basis that employers need how is that changing and of course we all know the big deal, automation that a lot of human labor can be automated and or replaced by software and robots and following software and many other jobs are now requiring humans to know how to program robotics and program software so that it’s kind of a cooperative effort if you will between me and the forces of automation and the human laborer right? yeah and so that is a higher level of skills thought to be able to reprogram a robot and that sort of thing right? it’s not simple assembly work anymore and so we’re seeing the job market breakdown into these broad categories, of course, the high skill ones like full programmers and people who design software and who can actual engineer actual robotics, of course, there would be jobs for these people who are highly educated engineering types as it’s the middle sector its everybody below that very highly educated engineering math science kind of a sector, that whole thing is, the larger chunk of the economy is vulnerable to automation the larger chunk of the economy is vulnerable to Automation. Of course we’ve seen this and in many fields at starting with like factory work but it’s moving up the food chain to accounting and even legal work and of course in financial tech too right, haven’t you. I’m sure we have all seen the photo in those trading desks at major investment banks that used to have these huge rooms crowded with traders now there’s twelve people in the whole room,

FRA: Most of it can be done through trade processing platforms like calypso and more these are like derivatives trading platforms that can do pretty much everything front office middle office back office altogether in one system.

Charles: Right, right and so another factor here is Michael Spins, he is the economist who won the noble prize in economics for his work on explaining how work is nowadays in the global economy, some of it tradable and some of them not tradable and so that’s a key factor because if tradable work like programming software, that can be done anywhere in the world right? It’s a digital file so that imminently tradeable. Where like giving someone a hair cut or doing the landscaping like on a yard, you can’t outsource them, you can have immigrant laborer and you can try to import labor if you are short on laborer to do that kind of work but yeah, a lot of people are seeing that there is a dichotomy here that we’re going to divide into low skill non-tradable work like landscaping like perhaps even things like food service that, of course, that’s a mixed example because a lot of food services are already being automated as well. And so we have these two pressures, whatever is tradable is under pressure from globalization, in other words, the employers are going to have to ask can this same work be done elsewhere in the world for a lower price so that puts pressure on wages and high cost to develop world economies. And in the low skill nontradable sector such as yard work and taking care of elderly people and that sort of labor then the pressure there is can we automate some of this and so we are hearing from Japan where they’re really pursuing the idea of having some sort of simple basic robots that would provide some basic services to elderly people that are maybe bedridden. So the robot could come in and make sure that they take their medication on time, that sort of thing. And so again because there are facing a labor shortage and here in north America the pressure is the cost of labors just keeps going up, not so much the wage but the cost of labor overhead to pinch us, disability insurance and the health care at least in the U.S., less so in Canada I think. So we sort of seeing that if we combine these sources we can see there seems to be plenty of jobs that are low skill but they’re also going to be low wage and the non-tradable sector, coz there’s going to be a lot more labor that’s able to do that work then there is the abundance on the labor side, not the job side. There’ll be plenty of jobs but there will be even more people who are qualified to do that, but on the higher skill level there’s going to be perhaps a few more jobs but those jobs are often tradable so there is more global competition and pressure on wages even on highly educated highly trained people, you know salary. so

FRS: What is the future pertaining in terms of where the trend is if you had to advise somebody who is going to college and what they should study or should they go to college or how should they prepare for the world of work.

Charles: Right, right, that’s an excellent question and I did write this book: “get a job and build a real career and defy of the wildering economy” and the reason why I characterize the economy as bewildering is it really is bewildering because there are all these big dynamics which we all touch upon whether the work you are trying to get is tradable whether it’s high enough skill can it be automated all of these things factor into jobs of the future. So there is a great Mackenzie report on automation and I think it sort of echoed what I’ve read else where in researching this topic which is what humans are good at and what machines are not good at is combining knowledge basis from various fields. Computers are really good at what is repeatable and can be broken down into definable task, and what they are not so good at is changing or adapting on the fly to changing circumstances, and so that’s the kind of skill set that everybody would benefit from having is try to develop multiple skill set and multiple knowledge bases so you could bring a couple of different sets of experience and knowledge to bear on problems because those are basically impossible to automate, at least in the existing technology, and that can be in a lot of different fields. It doesn’t have to be just in high end, we are not talking about high finance or programming software, it can be something like on the factory floor, with robotic arms and then the work changes because we got a different order, then the skill set that is going to be highly desirable is a worker who knows how to reprogram that robotic arm on the fly, in other words they can change the robot’s tasks and that with accuracy and speed that kind of skill is going to be valuable, so my point here is the whole range of skills from what we might call blue collars like welding and pipe fitting and construction, there’s going to be a lot of changes in those fields too, working with robotics and software and all the way up to health care and higher education itself. Not to mention industrial design, public relation and all the other fields that we think of as upper middle class.

FRA: Yeah, I see the same thing, I mean in terms of multi-disciplinary areas being brought together so like in the consulting world I see that happening with maybe a project involving compliance to a regulation but you know some aspects would have to do with it if you just look at IT itself a lot of that can be outsourced but once you have that, like an IT control, that needs to be put in place for a regulatory compliance this sort of that aspect to it the legal aspects that need to be considered and thought through and how they can be implemented together with the IT control sort of like a multi-disciplinary type of thinking.

Charles: Yeah, that is an excellent example Richard, and then on the global scale, then you can also add cultural knowledge because of the IT and the legal aspect of regulatory compliance then you also have the cultural issues to show up with making sure that the work force in a particular nation, is up to speed culturally, like why do we have to do this and how you educate each particular work force and so. Yeah, that’s a great example of what I am talking about, multi-disciplinary.

FRA: And just in general as you’ve mentioned earlier the ability to adapt quickly sort of the old idea of the adapt sort of the emphasis on the adaptability versus the big dinosaurs.

Charles: Yeah that is right and I think that Charles Darwin himself, famously said, it doesn’t go to the smartest, it goes to the most adaptable. And so one topic I also want to bring up, is that a lot of people in the automation field or in economics they often refer to the idea that well there is just going to be a lot of great opportunities for creative output, we are going to have a lot of people that are poets, making films and all these kind of stuff that. I just want to point out and I’m sorry if I just splash cold water on that but as we all know all the creative output is in super abundance in other words, everything is free now because there’s limitless number of songs and huge quantity of music and films and comics and cartoons and novels and stories and I mean any kind of creative output is in super abundance on the internet and so it’s very difficult to charge any money. You know to get more than 99 cents for an app or song or even an entire book is becoming a challenge. So it’s nice and I’m all for creative output in terms of self-expression and the fun of life, but in terms of making the middle class living my experience is that the number of people who make decent living at being a creator is pretty minimal and so I think the idea here is not to throw cold water on creativity but to say that learn the skills of creativity, which is often mixing and matching the multi-disciplinary skills we are talking about. Bringing a fresh perspective or looking with fresh eyes, but holding those creativity skills, but be able to bring bear on real world problems as opposed to thinking that I am going to be a poet or writer or you know an artist and I am going to make that my career. It is more likely is say for instance if you were super interested in that and had an act for say painting then you might want to get an internship with a curation staff, in other words, learn the ropes of how you would curate a collection and you’d be gaining skills into your interest in painting and your knowledge base, but you’ll be learning some skills that deal with real world and why people would pay you for the knowledge you have.

FRA: So I guess I mean one theme could be if you going into tradable skills that have to be some element of innovation and adaptability innovation, cutting edge if you will, but in the non-tradable that could also mean the job protection by regulations or jurisdiction based licensing, like you know lawyers can practice within certain jurisdiction, does that make sense.

Charles: Yeah that’s good point Richard and I think when we talked about the millennial generation few programs ago, I mean that’s what we both read was that the millennial generation as a generalization is interested in say government employment because it is more secure, but the downside of that is that the economy that we are talking about it has a certain Darwinian element to it, which is you’re going to lean the skills to be part of the disrupter or you’re going to be the disrupted. and so the problem is all these protected industries, which would include health care, higher education, and the government sector itself; these are the low hanging fruit for disruption because they are extremely high cost and tend to be inefficient and they tend to be cartels or self-serving protectorates. you know that makes sure that their wealth funded and never mind if their productivity is actually declining or they’re not really solving any problems anymore.

And so those are the fields that are more likely to be disrupted then the fields that already been constantly disrupted. For instance, the automotive industry. I mean come on the thing is in constant turmoil already, so there’s not much you could disrupt the auto industry with constant and rapidly changing, but if you look at healthcare it’s still stuck in procedures and bureaucratic mindset that no longer require, technology has gone far beyond what we now deliver health care in the US is so annotated and obsolete, it’s laughable and everybody knows this but we haven’t been able to break out of it and innovate, but that will happen because the costs are crushing, the government and private sector. So I would hardly recommend young people not to count on allegory or a health care job or government sector job as being some sort of guarantee going forward, it’s going to be disrupted too.

FRA: Yeah there’s going to be lots of tension, I mean you already see it in Uber and Airbnb, right all these development going on and doing disruption to that type of cartelized industry.

Charles: That’s right, so in higher education is pretty clear that I mean what the model that I proposed and I’m not, again this is not unique to me, I mean we just have to look and say the German model for the way that they funnel students out of high school into apprenticeships or university, and to me the apprenticeship model works well. We can replace the university of curriculum with that kind of approach even in software or philosophy or anything else. That model would be a lot more affective and a lot cheaper than the way we do now where we sit in classrooms.

FRA: Yeah, I think I saw some statistics where Germany does that at a very high rate like seventy percent of apprenticeship programs, compared to only ten percent in the US, something like that.

Charles: That’s right, and it was just an article in foreign affairs about how the US used to have a much more robust system of what we used to call like trade schools, and that’s been allowed to decline any road in favor of everybody getting a bachelor’s degree. This has actually crippled our economy in some way because we’re lacking the skills that the economy needs and yet we’ve turned down lots of people with degrees that don’t really have a lot of value. You know, art history and gender studies and this kind of stuff, and I myself have a degree in philosophy which you know could qualify as worthless. But it did require a certain amount of rigor in thinking things through, and that has served me well. I would argue that philosophy should not be put into the worthless degree category, but it should be connected if at all possible with some engineering skills, or some finance skills or some other more applicable, would be the ideal multi disciplinary approach we’re talking about. Don’t major only in philosophy, major in something else as well and together the two will probably serve you well.

FRA: Actually myself, I’ve got an engineering degree, but a minor degree in the philosophy of science.

Charles: Oh excellent.

FRA: Yeah that’s interesting. What is the path then going forward, I guess you can mention a number of industries but the path is sort of generic, that people should come with a sort of thinking outside the box, look at potentially disruptive industries, you know where things can be improved and then maybe take courses online, or is that what you’re suggesting in terms of trying to get opportunities from that way not necessarily through the traditional bachelor degree or MBA type of approach?

Charles: Right, the ideal pathway that I’m suggesting for people that either don’t have the money or don’t want to waste four years getting a degree that may or may not actually serve them is to seek out the equivalent of an apprenticeship, and this is not going to be a formalized model that you get to join. You’re going to have to make your own apprenticeship, and that would be to seek out a mentor in the industry in which you think you have an interest, whether it be fashion design or you know some sort of art related field or health care. Whatever it is, I would seek out a working professional who would help design your curriculum so that it would actually serve the needs of the working environment that he or she actually understands, and so that might include getting a BA or a BS, but I would get right out of the gate out of high school, and I would be seeking and apprenticeship with work for nine months or a year for somebody who could layout a curriculum and if I could learn all that stuff online then I might not even need a BA or a BS. So that’s what I would do. And if it turns out they say, “look you really got to get this BA or BS”, then you know what your pathway is at least you know that your work will be rewarded, that its essential for what you want to do in life. You’re not just burning four years and getting a hundred thousand dollars in debt and finding out it doesn’t even really serve the economy or your own career path.

FRA: Maybe also thinking outside the box, I know a lot of people that we talk to on the program show have an international perspective. There’s also the idea of looking where high growth areas of the world are, like you know Myanmar, Burma. If you go there now you can basically start a business, whatever has worked in parts of Southeast Asia will likely work there. So you can set up that business, it could be serviced offices or car rental, whatever works elsewhere in Southeast Asia can be replicated there at this time.

Charles: You know Richard that’s an excellent point or super important point that I failed to mention so far, which is really where the value comes in the global economy is filling a scarcity. Where there’s a problem that hasn’t been solved, if you can bring those skills to bear, then you’ve got a guaranteed and a very exciting career. And I think you’re making a really big point here about places like Myanmar, is that there is a huge amount of developing world economies, you know there is so many scarcities that need to be filled there and there’s often a regulatory burden or a lack of infrastructure. I mean there’s often major problems that need to be overcome to get to fill the scarcity, but being part of those can be very rewarding and will require some research. You don’t just blow into some new culture and new nation and it operates by different rules. But again, if we follow the idea of an apprenticeship, if you get hired by somebody who would send you to another nation. Or if you just go there and try to find work and just say “I’m going to give this six months”, then you’ll probably learn a tremendous amount on the job, far more that you can possibly learn by going to school there.

FRA: I can think of my own experience too with the disruption of the internet. I was one of the first users of the internet back in nineteen eighty-three, and I did the whole internationalization of the internet in the nineteen nineties, so all over the world. Setting up internet service providers in different countries. That type of thinking outside of the box, international in scope and just bringing on a new disruption type of technology or process.

Charles: Right, and I guess in a similar vein, we could also say that these sclerotic, stuck in the past kind of sectors like health care and higher education that we’ve mentioned. There’s also huge scarcities in those industries that just aren’t recognized yet. And also as you say geographically, that if you’re the first into a market and with a first solution, and it could be as something as full as bringing a wealth of web related public relations and social media skills to a small town. And if you’re first there, then you can write your own ticket because you’re solving problems and there’s no body else to solve those problems.

FRA: And I think overall with countries in the past pulling financial oppression method of say currency, devaluation, competitive currency devaluations, it’s now moving into a realm, given that all countries are doing it at the same time. Coming down to a differentiator of innovation and how adaptable can your economy be, and how competitive can your economy be, more and more I think I see that globally.

Charles: Right, I would say that cryptocurrency as another example of how financial oppression can cripple an economy is that there’s going to be a huge expansion of block chain technology. So if someone was technically minded I would recommend they really dig in and burrow in, learn how to understand and code block chain technologies because the nations that enable this and encourage block chains are going to succeed far more than those that are trying to supress of repress it.

FRA: Yeah exactly, and that’s a great way to end our program show for today, and that’s great insights as always. Charles, how can our listeners learn more about your work?

Charles: Please visit oftwominds.com and you can read free chapters of my books and look at my archives and see what else I’ve got on tab. Please visit and I welcome your readership.

FRA: Excellent thank you very much Charles.

Charles: Okay thank you Richard, my pleasure.

Transcript by Boheira Manochehrzadeh bmanoche@ryerson.ca

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/31/2017 - Dr. Albert Friedberg: Negative Interest Rates Have Resulted In Malinvestments; Sees Money Continuing To Flow Into Equities Globally

Negative Interest Rates Have Resulted In Malinvestments & Deflation .. Does not see the Federal Reserve increasing interest rates higher than the yield on the U.S. Treasury 10-Year Bond .. Sees money continuing to flow into equities due to their yields being higher than bonds in general .. Sees risk assets doing well globally .. likes Greek banks, Japanese equities, Brazil, U.S. Homebuilders ..

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/31/2017 - John Mauldin: Markets, Trade, Velocity of Money, Pensions Crisis – Sees Long-End Interest Rates Going Lower

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/31/2017 - Chris Whalen: Public Debt Is The Real Driver Behind Central Bank Action

“The indebtedness of the world, especially the public indebtedness of countries, I think is the real driver behind central bank action. The reason is the dropping interest rates has ceased to be an effective way to get economies moving .. I think people have to realize that the weight of debt, and also the posture of all the major central banks, is such that low interest rates are going to be with us for a while. And until you see a change in demand so that treasury auctions are not as successful and yields in fact have to rise to attract investors, I really don’t see that changing.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/30/2017 - Mish Shedlock: It’s Your Money But You Can’t Have It – EU Proposes Account Freezes to Halt Bank Runs

“If there is a run on the bank, any bank in the EU, you better be among the first to get your money out. Although it’s your money, the EU wants to Freeze Accounts to Prevent Runs at Failing Banks .. The entire European banking system is over-leveraged, under-capitalized, and propped up by QE from the ECB. Simply put, the EU banking system is insolvent .. That the EU has to consider such drastic measures proves the point.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/27/2017 - Mish Shedlock Powerpoint Presentation Slides On Misguided Central Bank Policies And Their Consequences

“This ridiculous mix is central bank policies stimulate massive wealth inequality fueled by soaring stock prices.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/27/2017 - Dr. Lacy Hunt: Federal Reserve Actions Will Create Substantially More Volatility In The Financial Markets

“Investors should expect that the Fed’s actions will create substantially more volatility in the financial markets and particularly so over the short-term. Operating with strategic views and multi-year trends, rather than trying to focus on the Fed-generated noise in many monthly and quarterly indicators, may be a preferred method of generating investor returns. Our economic view for 2017 is unchanged and continues to suggest that long-term Treasury bond yields will work irregularly lower. The latest trends in the reserve, monetary and credit aggregates along with the velocity of money point to 2% nominal GDP growth for the full year, down from 3% in 2016. This would be the third consecutive year of decelerating nominal GDP growth and the lowest since the Great Recession. This suggests that the secular low in bond yields remains well in the future.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

07/26/2017 - The Roundtable Insight – George Bragues On How The Financial Markets Are Influenced By Politics

FRA is joined by George Bragues in discussing his book Money, Markets, and Democracy: Politically Skewed Financial Markets and How to Fix Them, along with a thorough overview of the Austrian school of economics.

George Bragues is the Assistant Vice-Provost and Program Head of Business at the University of Guelph-Humber, Canada. His writings have spanned the disciplines of economics, politics, and philosophy. He has published op-ed pieces in Canada’s Financial Post. He has also published a wide variety of scholarly articles and reviews in journals such as The Journal of Business Ethics, Qualitative Research in Financial Markets, The Quarterly Journal of Austrian Economics, The Independent Review, History of Philosophy Quarterly, Episteme, and Business Ethics Quarterly.

FRA: Just thought we’d begin with the book that you have: It’s called Money, Markets, and Democracy: Politically Skewed Financial Markets and How to Fix Them. Can you give us an elaboration on what the basic messages are, the themes of your book?

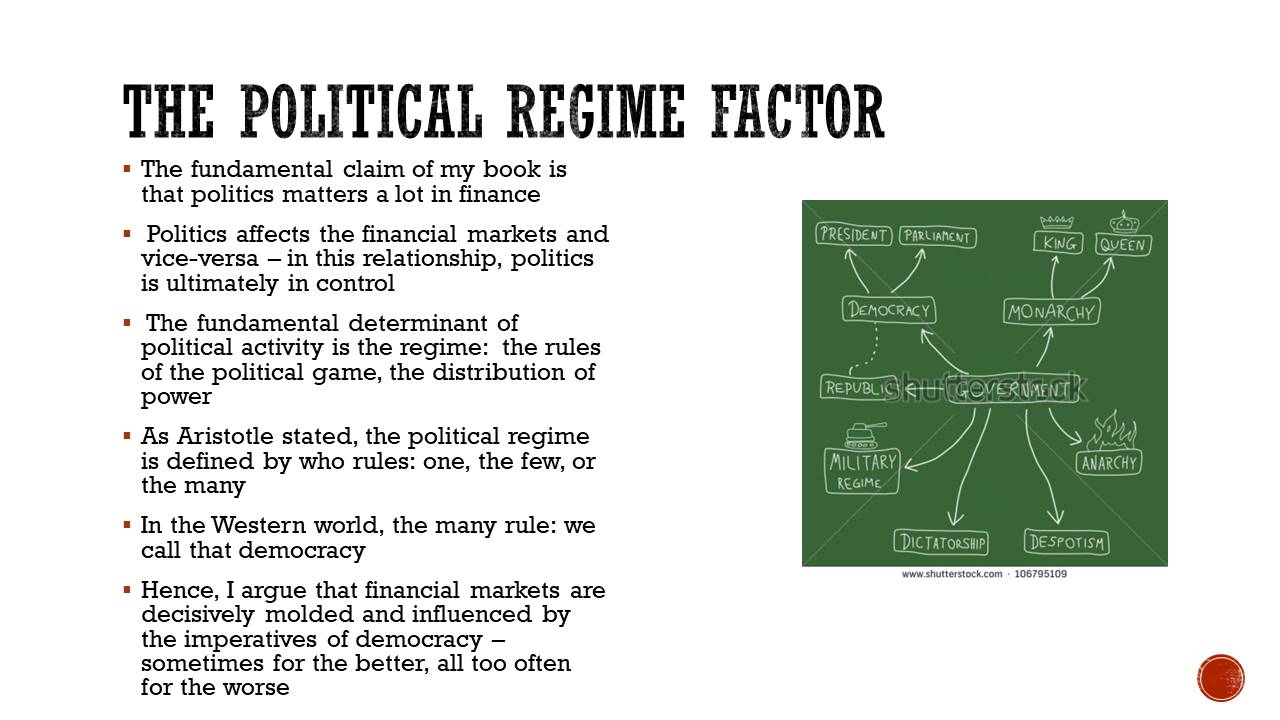

BRAGUES: Sure. The key thing I wanted to get across in my book is the importance of politics for understanding the financial markets. This is something that gets often missed in your typical courses that are taught at the MBA and also the undergraduate level. When a student takes a course in investment finance or financial economics, they don’t get exposed a lot to the political factors that drive prices, that drive trends, that drive decisions of monetary policy and interest rates, as was made abundantly clear with the 2008 financial crisis. Though one could have seen evidence of the role of politics in finance earlier than that, but it became much more obvious after 2008. This is definitely a gap in the way financial markets are taught to students, and the way they’re discussed by economists in general. The book is designed to address the flaw that the economics professor tends to be the only one that studies the financial markets. The dominate it, they practically hold the monopoly in it, and other disciplines, specifically politics, need to be part of the mix.

(click to expand)

As the title suggests, it’s not just politics per say, or politics in general that needs to be considered, but the regime. The regime is defined as the fundamental rules of the political game. This is actually a term that comes from the Ancient Greek philosopher Aristotle. He wrote a book – still very well known, still discussed among political philosophers – called The Politics and he distinguishes regimes into three types. He distinguishes it by who rules: if you want to know what a political system is like, you ask yourself who’s running the show, who’s making the decisions. Three basic different types of regimes that are possible: ruled by the one, which we would call autocracy or sometimes monarchy or dictatorship; there’s ruled by the few, which we would call aristocracy or sometimes oligarchy; and then there’s ruled by many. Democracy would be the example of that.

Financial markets around the world today, with only a few exceptions – China primarily among them – most of the major financial markets today are operating within democratic political contexts. The argument I make in the book is that democracy, because of the political incentives that it imposes on politicians because the values – the types of norms and morality a democracy has, these two factors, the value system and political incentives, what politicians need to do to get elected in a democracy – these fundamentally structure the nature of the financial markets. They don’t do it necessarily on a daily basis, you can’t day trade on this information or even swing trade on this information, but it definitely will illuminate anybody who’s involved in investing on the financial markets to help them better understand the force that drive prices over the long haul.

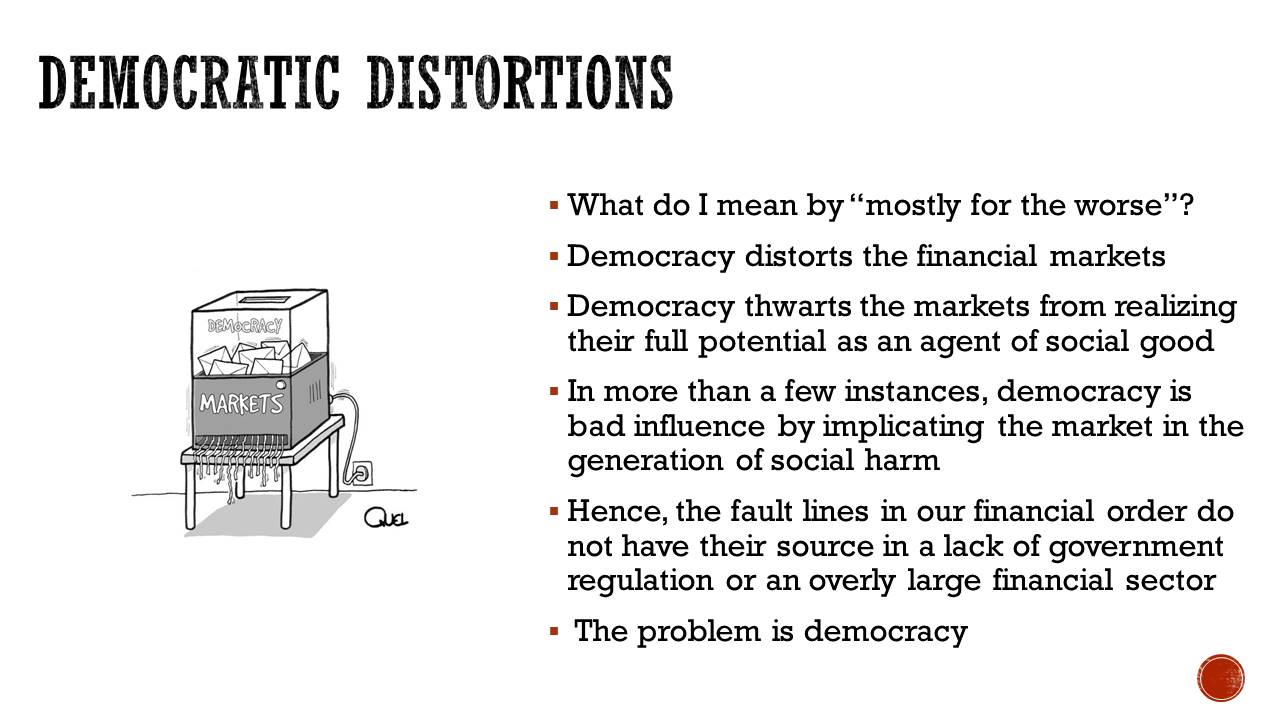

So my thesis is that democracy, while probably the best political system relative to the alternatives, despite it being the best of the available alternatives, it does create problems in the financial markets, it does distort the ability of the financial markets to do social good, and so a lot of the problems that we have are because of the fact that the markets are operating in a democracy.

(click to expand)

FRA: How does that happen? How does democracy distort the financial markets? Could you give some specific examples?

BRAGUES: The big example that I discuss in the book is the money supply. The main argument that I make is that democracies tend to oversupply money into the economy, and that has an impact on the financial system. I distinguish two factors that drive democracy’s overproduction of money, this excess liquidity. One factor is this class conflict between taxpayers and tax consumers. This notion of a class conflict between taxpayers and tax consumers is a notion within Austrian economics and it is meant to replace the Marxist view that the fundamental class divide in society is between bourgeoisie, the capitalists who own property, and the labour working classes who don’t own property. The Austrian view is that the main class division is between those who on net pay more taxes than they receive in services from the government – this group would be the taxpayers – and the tax consumers are those who on net receive more from the government than they pay. In terms of what a tax consumer can receive, this can range to anything from unemployment insurance payments, social assistance payments, favors provided by the government in terms of inhibiting competitors in your industry. The argument is that in a democracy, if a politician wants to get elected, the name of the game is to get 50%+1. Given that the distribution of the income in modern commercial societies tends to be such that there’s a few rich and wealth tend to be a small segment of the population, and the middle class and lower classes tend to be the majority, the best way to get elected is to offer mostly the middle class all sorts of public goods in terms of social programs and so forth, and then have those financed by the well-to-do who would function as the taxpaying class. That way you get your majority and get elected.

(click to expand)

All politicians, whether the left or the right, both sides of the political spectrum do this. Perhaps the left does this with a bit more conviction guiding their efforts, but on both sides of the political spectrum this happens. So politicians engage in this bidding war every time election time comes, trying to offer the majority all these goodies with the idea that they don’t have to pay for it, someone else will. What ends up happening, I argue in the books, is that after a while of this bidding war where politicians offer more and more public goods, someone has to finance this. Eventually you run out of taxpayers or you run into taxpayer resistance. At that point politicians then resort to the bond market and the bond market has proven historically quite eager to lend funds to the government. Government bonds are very attractive investments for a lot of folks because of the safety. This is money that’s backed up by the power of the state, unlike corporate bonds which are not. Corporate bonds are only paid ultimately if the corporation is successful at attracting people to voluntarily buy their goods and services.

I argue in the book that we now have a kind of financial market-government complex, or a bond market-government complex. The bond market has emerged as a kind of handmaiden to the welfare state, this growth of government. At a certain point, even the bond market will say ‘we can’t lend more’ and at that point politicians will appeal to the money press and they will enlist the central bank to print money, essentially, though it’s more complex how liquidity is injected into the economy, but that’s basically what happens. So essentially democracy leads to fiscal profligacy, too much spent relative to the revenues politicians are willing to collect from people. They then have to go to the bond market; public debt rises. And then to increase their options of financing this deficit that is inherent to democracy, they require control over the monetary supply. My argument in the book is that the gold standard, which existed for a good part of the 20th century in one form in another, which ultimately ended in the early 1970s – August 1971 if you want to get exact – that was in a way written in the DNA of democracy; that democracy ultimately is intentioned with a monetary constraint like the gold standard. That’s one of the ways I make this argument that democracies do damage to the financial markets.

(click to expand)

FRA: It sounds like the endgame is either a no bid situation in the bond market, or as you mentioned they could go to the printing presses. The other endgame is the loss of purchasing power in the currency. Either way, I guess that’s likely to be the only way to stop the politicians’ continuous profligate spending.

BRAGUES: Either the bond market has to say no, and historically as mentioned before they’re not very good at saying that. In the book I discuss the historical record of the bond market’s ability to keep governments to account. I remember in the past, I think he’s still around, Ed Yardeni coined the term ‘the bond vigilante’, which was a popular term in the 1990s. The bond vigilante is this creature that’s supposedly watching over governments, closely scrutinizing budgets and if they see any sign that they’re letting public debt out of control these bond vigilantes then start selling off the bonds of the country that’s engaging in this poor fiscal policy. The record, especially with developing economies, is that bond markets only react to excessive public debt very late in the game, when it’s become quite obvious and traders seem very eager to provide money to governments who are spending above their means while the debt is building up. And only when a certain threshold is hit – it’s really hard to find that threshold, Kenneth Rogoff wrote a book a few years ago when he went through the history of it and said, well if it’s a developing country it appears to be about 60% of GDP, that’s when the bond vigilantes come out; developed countries tend to have more tolerance. Even that threshold doesn’t seem to have held, because we now have countries – Japan principally among them – they’re well above 100% GDP and there’s no sign bond markets are growing less willing to finance their debts. The bond markets will have to have a shift in how they approach their investments into bonds.

(click to expand)

The other constraint would be the gold standard, but as I talked about in the book, I don’t totally foreclose the return of the gold standard. I agree that we should try to do as much as possible to bring that back, but democratic politicians don’t want to have the constraints posed by a gold standard because it makes their lives difficult. It means they have to say no to people, it means they can’t win elections by simply promising all sorts of goodies. It’s no surprise to me that the gold standard ultimately disappeared as democracy progressed.

FRA: You’ve included a number of slides, including one slide with a quote from James Grant, editor of Grant’s Interest Rate Observer where he highlights that you not only diagnosed the problem but also proscribed a solution to the problem. As you mentioned on the gold standard, what you’re saying is while not likely to happen, or not likely to come about, you do identify the solution. What is more the endgame: no bid in the bond market or gradual loss of purchasing power in the currency?

(click to expand)

BRAGUES: I would probably say the latter. Especially with the next 20-40 years or so, you have an aging demographic, a greater proportion of people who are older and they will seek safety, and I think that keeps up the bid in the bond market. I would say we have very slow decrease in purchasing power.

The thing is, in part of 1954 inflation was practically nonexistent. You’d have inflation only in certain periods, usually after a war, after substantive crisis, when the government is compelled to appeal to the monetary press to finance conflict. If you look at the data from early 19th century to 1945, I think in Britain for example there was really no change in purchasing power. The Pound was worth around the same in the early 19th century as it was going into the early 20th century. But that’s all changed since 1945. We now live with a situation which we think is normal, but which from a grander scheme of things is not, and people in democracy seems to be willing to live with an inflation rate of around 2% a year. I think governments are going to try to keep that going and if necessary, perhaps tolerate a somewhat higher rate – 3,4,5%. Some economists have talked about that, tolerating a different rate for inflation rate. I think all the incentives are for politicians to continue to take advantage of the bond markets’ generosity, if you want to use that term, and try to finance this via the inflation tax at the highest level of tax that is possible without incurring significant public protest.

FRA: I think we’ve seen figures of if you have inflation at 4% a year for 10 years, it can reduce the burden of debt by one half, something like that.

BRAGUES: Yeah. If you look at history, when we look at how the debt after WWII was dealt with, it was a form of financial repression that took place, where the inflation rate was held higher than the rates that most people be able to gain on deposit. I think they’ll try to appeal to that strategy again.

(click to expand)

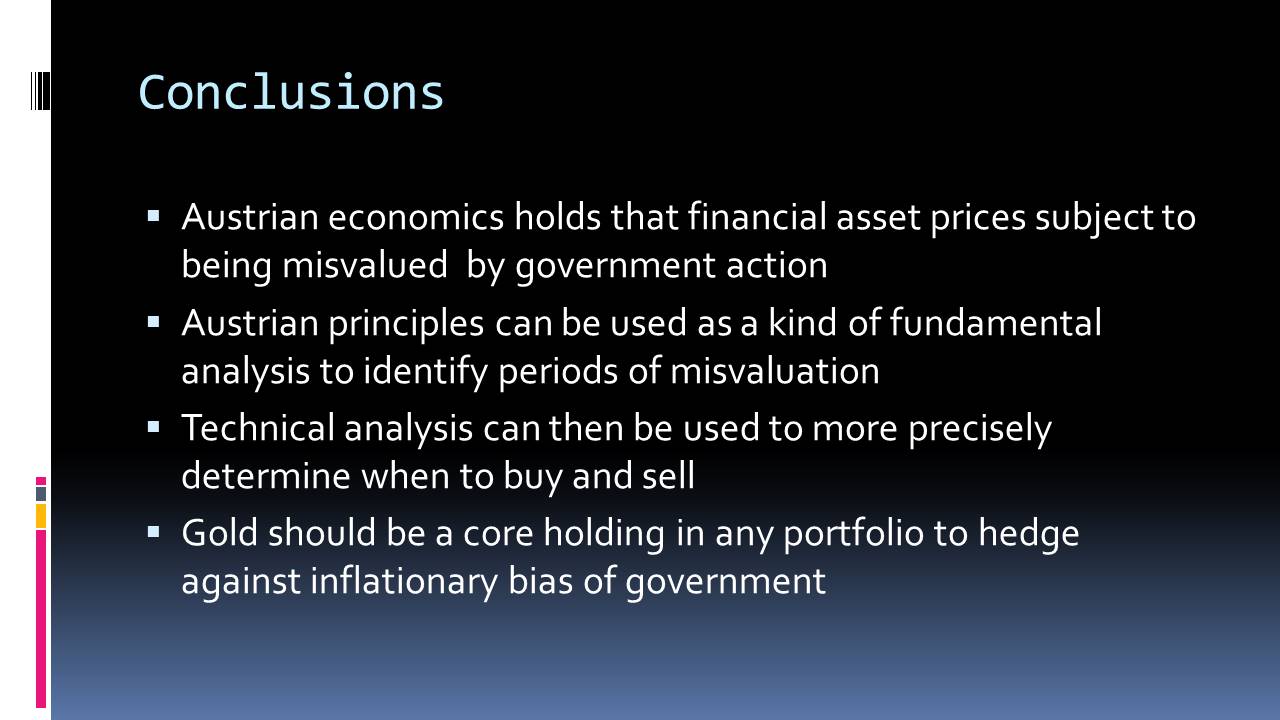

FRA: Yeah, very likely. Just switching gears slightly, we’ve talked about the Austrian school of economics and you’ve also provide a set of slides on the investment potential of Austrian economics in investing. Just wondering if you can give some highlights of those slides and how you see the Austrian school of economics compared to the Keynesian school of economics.

BRAUGES: In terms of Austrian investing, I think it’s a promising approach. In order to succeed in investing, you do need to have an approach that is different from other people because if you’re just doing what everyone else does you’re just going to get at best the average rate of return. You’ll get the same rate of return that you might, say, if passed an investing vehicle like an index fund minus the cost of running your investment, the commissions and so on. Because most people in the financial markets are essentially Keynesians – they may not be conscious fully of their beholden to Keynesian principles, but anyone who follows the markets on a regular basis, specifically on issues of how the Federal Reserve or ECB is expected to react to certain data points, it’s clear that when you see a lot of these analysts get quoted in the Wall Street Journal or the Globe and Mail and so on, that they effectively are operating with a Keynesian worldview. In terms of having a unique point of view that can offer above average returns, I think Austrian economics offers something certainly worth looking at.

In terms of what it boils down to, I’m the first one to admit there’s not set Austrian approach. You can have five Austrians in a room and they’ll have five different approaches, although they’ll come from a common base, that common base being the commitment to certain Austrian economic principles. I say the two biggest ones that are relevant in terms of investing are A: the rejection of the efficient markets hypothesis, which is very common in the academic treatment of finance even though it’s losing some of its support to another field called behavioural finance, which argues that psychology needs to be considered in understanding how markets move. Efficient markets hypothesis still looms large, especially in academia, and it argues that in any point in time prices reflect all available information so that everything that is known or can be known is already in the price. So there’s no point doing any sort of analysis to try and beat the market if you believe in this theory because everyone else has already looked at the financial statements, they’ve already considered the company’s strategy, already looked at the technicals and moving averages and trend lines and all that, it’s already in the price.

(click to expand)

The Austrian view rejects EMH and it’s because of its theory of entrepreneurship. Austrians are very big on the notion that what drives economic activity and specifically economic growth is the activity of entrepreneurs. What entrepreneurs do is they find arbitrage opportunities; they find profit potential that other people aren’t seeing. We can transplant the entrepreneurial function to the financial markets and say that there are similar arbitrage opportunities, similar opportunities that people aren’t seeing, that with good analysis and some work can be grasped. That’s point number one that differentiates the Austrian approach from more mainstream approaches that are taught in academia.