Blog

06/07/2018 - The Roundtable Insight: Ronald-Peter Stoeferle And Yra Harris On Gold And The Emerging Chaos In Europe

06/07/2018 - The Roundtable Insight: Ronald-Peter Stoeferle And Yra Harris On Gold And The Emerging Chaos In Europe

06/07/2018 - Emerging Markets Are Begging The Federal Reserve To Stop Shrinking Its Balance Sheet

Central Bank of Indonesia Governor:

“We know every country must decide their policy based on domestic circumstances but look, you have to take account of your actions and the impact of your actions to other countries, especially the emerging markets.

There are three global players that impact the future of interest rates and exchange rates. Now it’s only the U.S. .. That’s why the U.S. and the dollar are king. But next year if Europe starts normalizing, Japan starts normalizing, then I don’t think the U.S. or the dollar will be the only king.”

06/06/2018 - The Roundtable Insight – Jayant Bhandari On The Risks Of A Stronger U.S.$ And Rising Rates On Emerging Markets

FRA: Hi welcome to FRA’s Round Table Insight .. Today, we have Jayant Bhandari. He is constantly travelling the world to look for investment opportunities. Particularly, in the natural resource sector. He advises institutional investors about his findings. He also worked for six years with US global investors in San Antonio, Texas, a boutique natural resource investment firm and, for one year, with KC Resource. He writes a lot of a number of publications including liberty magazine, the MC Institute, KC Research, Acting Man, International Man, Mining Journal, Zero Hedge, Little Rockwell, Frasier Institute and many others. He is contributing editor of the Liberty Magazine. Welcome Jayant.

JAYANT: Thank you very much for having me, Richard.

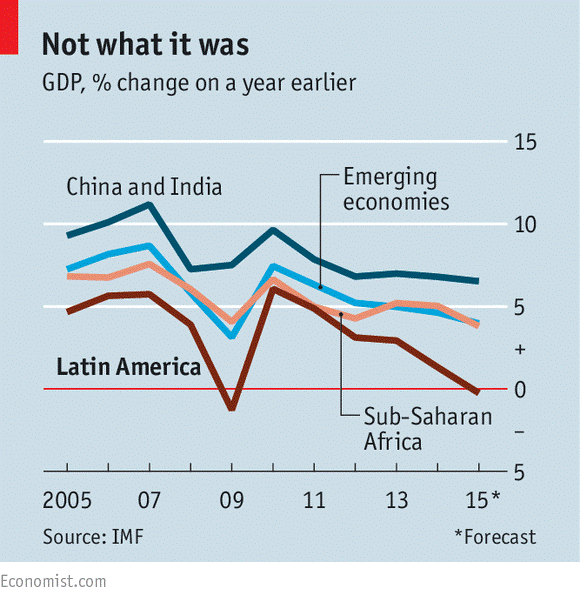

FRA: Great. I thought today we’d do a focus on the plight of the emerging markets, and you have graciously come up with a number of charts that can help form the basis of the discussion. We’ll make these charts available through the link on the website. But, yeah, I wanted to focus on what’s happening in the emerging markets considering the trends in oil prices, in the US dollar, interest rates and what they have done in terms of investing in energy in particular, what they have not done is probably a better way to put it. Just wondering your initial thoughts on that to get the discussion going.

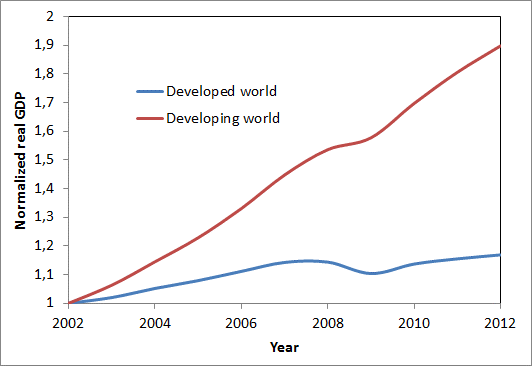

JAYANT: What happened, Richard, was that from 1995 onwards for almost 20 years, emerging … What are now known as emerging markets did grow very nicely. They have grown by about 100% between 2002 and 2012 according to one of the charts that I sent you. While this growth was an extremely good growth for the emerging markets, from the base that they were starting at, the problem is that the growth rates of the emerging markets have been falling consistently for the last 10 years. Now, if you pay closer attention to what’s happening in sub-Saharan Africa, the growth rate has fallen to only 1.4%. Now, when growth rate … Economic growth rate is only 1.4% and population growth rate is 2.8%, you actually now suddenly end up with a negative growth rate which is -1.4% per capital for sub-Saharan African.

Growth rates in the third world are falling and in case of sub-Saharan Africa it is negative now—while there is still 1.4% GDP growth rate, population growth rate is 2.8%. The net effect is negative growth rate on per capita basis.

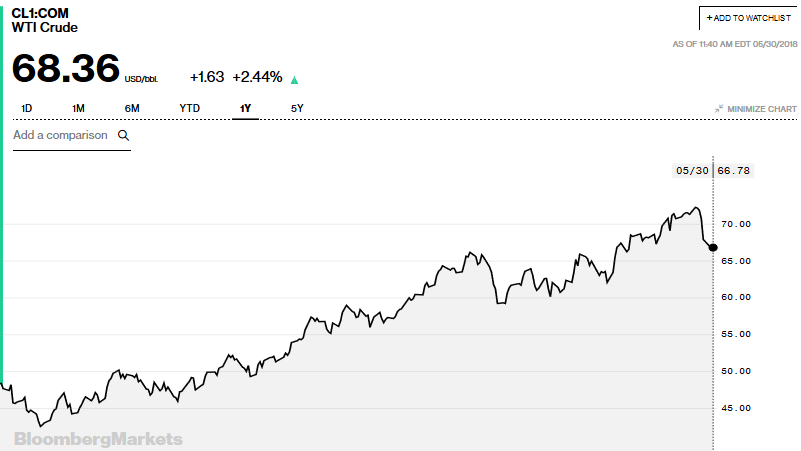

Today, US 10-year treasury yields are inching towards around 3%. WTI crude has gone up from US$48 a barrel to US$68 today.

JAYANT: What also happened in the last 10 years was that, a decade back, the western countries adopted very easy money policies which meant that money managers sitting in London and New York suddenly found it very attractive to invest in the third world countries, which were now known as emerging markets despite the fact that the risks of emerging markets were extremely high. They invested a huge amount of money in Africa; particularly money managers sitting in London did that. This money, while superficially was going to generate good returns for them, they did not really take into account the risks associated with investing in sub-Saharan Africa. These people gave a lot of money in US dollar denominated bonds of African countries. They got a much higher interest rate from these countries, but the problem is that Africa suddenly finds itself hugely indebtness. African was indebted by only about 30% in 2005 and now it is more than 50%. The reason it was only 30% 15 years back was that multilateral agencies forgave a lot of debt that African countries owned, and these people have then, again, taken a lot of debt in the last 10, 15 years, and they’re now hugely indebted. What you also find is that a lot of this debt money that African countries raise did not go into investing in capital. A lot of that money went to deal with budgetary deficits. Then, if you pay closer attention to the investments they made in capital, you also see that a lot of that money was not invested properly which means that now that yields on American dollar is starting to increase the currency values of these third world countries are starting to suffer rather badly, and as a result, their stock markets are falling, their currencies are falling and these countries will face problems paying their debts again.

In 2005 the WB, IMF and ADB forgave debts of the heavily indebted poor countries, 30 of which were in Africa. These countries were growing very nicely during the same time. There was actually synchronous growth happening in the third world.

By early this decade, sub-Saharan Africa’s debt to GDP was 30%. This has now gone up to 50%. Given the past failures to pay, African countries pay higher interest rates. Then commodity prices started to suffer, there wasn’t enough revenue to service debts and the pace of borrowing picked up. Interest rates in the West were very low, which made it possible for increased flow of money from the West to Africa.

Fund Managers in Europe invested hugely in Africa, particularly in their bonds those denominated in US$.

Alas, this money went in to deal with budget deficits rather than in capital investment or in infrastructural investments. When money did go into capital investments, it was often squandered.

FRA: You mentioned the money managers in London didn’t look at the risks at that time, what were those risks at that time in terms of the emerging market risks?

JAYANT: The third world has a history of not honoring their debt payments, but every time there is a euphoria about third world countries, money managers in New York and London start thinking that the past is gone and the future is going to be different. Unfortunately, the future continues to be the repetition of the past which means that they keep giving money to countries like Argentina, Venezuela and countries in sub-Saharan Africa, and then the money refuses to return back to the western countries. These people including people in the World Bank, IMF and development banks around the world continue to lose money by giving too much easy money to these third world countries.

FRA: So, you’re saying the loans made during the last 10 years did not go into capital investment or infrastructure investments. It just went to pay yearly budget deficits?

JAYANT: Most of it, yes. If at all that money went into investing in infrastructure, it actually was mal-invested. There was a very interesting case of Mozambique in which a couple of billion dollars of money that was supposedly have gone through invest in government companies actually got mis-invested in good living of people in those companies. Yes, even the capital money that was invested in capital was mal-invested in many of these countries.

FRA: Given how the US dollar trend has been strengthening recently, as you mentioned, these emerging market currencies have been weakening, and so it makes it more difficult to come up with the money, with the dollars to pay US dollar denominated debt, is that what you’re saying?

JAYANT: Absolutely, and not only US dollar is improving, the problem is oil price has also been improving, so some of these countries that do not produce enough oil, actually not only have higher interest to pay on their debt, they also have to pay more money for their oil imports that they’re doing, which means that their currencies are suffering hugely.

The above means that along with falling growth rates, the third world is facing increased interest rates on dollar-denominated borrowings and are also having to pay more for oil, which can be among the biggest imports of the third world. This is happening exactly when the governments and people of the third world were expecting continual improvements in their economies.

JAYANT: I sent you some charts before our conversation started; Indian currency has fallen by more than 5% in the last few months.

The result: Oil importing India’s currency has fallen by 5% y-to-y. As the recent result of increasing yields of US$, foreign institutional investors have been net sellers of Indian stocks and bonds. This will continue exiting going forward as the days of easy money are now gone.

JAYANT: Turkish currency is in a free fall. It has fallen by 33% in the last one year.

Turkish Lira has fallen by 33% y-o-y.

JAYANT: Even Russian Ruble which has fallen fair bit despite that fact that Russia is a net exporter of oil and gas and Brazilian currency, which again, is a country that exports oil and gas fallen about 13% in the last one year. In fact, Brazil is currently facing a huge amount of problems in the country. My Brazilian friend who I was talking with yesterday was telling that his stores do not have supplies anymore, she cannot find gas anymore, she is not driving anymore in the last two weeks because they don’t really have gas at the gas station.

Brazil has lost 13% value of its currency despite that it is an oil exporting country. It is currently facing an emergency situation with truckers on strike. The stores have gone empty, vital supplies are not available, and gas stations have run out of fuel. As we speak Petrobras workers have gone on strike. Michel Temer, the centre-right President is failing to put things right.

Angola and Venezuela are failing to benefit from increase in oil price, as their exports suffer. Angola has aging fields.

As you can see in the currency graphs above, the fall in Argentinean peso, Indian Rupee, Turkish Lira and Brazilian Real has been most significant over the last few weeks exactly when US$ yields have creeped up.

Even the oil-exporting oil countries (Chad, Venezuela, the Middle East, Angola, etc.) can no longer expect oil price to continue to increase, particularly in the long term. They must restructure their economies.

FRA: Wow.

JAYANT: The hospitals have run out of supplies because truckers are on strike which means that nothing really is moving much in the country, and there is a fear psychosis that has gone into the minds of these people despite that this friend of mine is living in gated community in a nice part of Brazil. Now remember, Brazil is an oil exporting country. Despite all that, these countries, in the third world, are continuing to face problems because they did not really invest properly when the oil prices were low. Remember, they were very dependent on oil revenue, so when oil prices fell down, they did not really have money to invest back into the fields. They actually used up the profit of oil companies for other purposes; for their budgetary purposes, and now that the oil prices have gone up, the problem is that oil prices have gone up but they can’t really produce enough to generate the good cash that they were generating when oil prices were higher in the last decade. For example, Angola was producing about 1.5 million barrels of oil every day and now it has fallen quite a bit from that level. I think it’s close to 1.5 million barrels per day or even less than that today.

FRA: We essentially have a double win in terms of the oil price rising and the US dollar currency strengthening. I’ve read estimates there’s as much as 9 or 10 trillion in the corporate based US dollar denominated debt outside of the US. Is that your understanding and what will happen to this? What is the outcome or how do you see it play out?

JAYANT: Well, I don’t have the exact number with me, but the problem with corporate debt is that, if the US dollar continues to be strong and the money continues to leave the stock market of these third world countries, how are these corporate going to actually pay the debt that they owe the western countries? It will become increasingly difficult, and with oil prices increasing, inflation in the third world countries, particularly those third world countries that do not produce oil that actually import oil, inflation will kick in and the profitabilities of these corporations in the third world will suffer. The end result will be that, in my view, a lot of this money is actually not going to return back to the first world. Also, at the same time, and at least I know data of India, foreign institutional investors were huge. Net investor in the Indian stock market between 2017 and 2018, but in the last three months they have pulled out a significant amount of money out of India and the reason is exactly the same. The reason is that now is much nicer for them to invest in US dollar in North America so they’re pulling their money out of India. The consequence is not just that the stock market is losing money in India, but at the same time because India is losing US dollars, Indian currency is falling as well, and as you can see in the chart, it has fallen quite a bit in the last few months.

FRA: How are they going to address their budget deficits? It seems like it’s going to get worse, especially now with interest rates rising? The dollar rising more difficult to make loans.

JAYANT: Absolutely. I don’t know how they’re going to sort out these problems, but this is a traditional problem of the third world countries. They do not plan for tomorrow. They take as much debt as possible today and they use it up without actually worrying about tomorrow, and the western countries all consistently give the third world countries too much money without really understanding the risks involved in giving all that money. The end result is that the first world does not get its money back and the third world countries continue to suffer the problems they have historically suffered.

FRA: Now, recently Argentina ran into that similar problems and they received some guarantees or a bail out by the IMF, I think, of about $30 billion, if I’m not mistaken. Do you see that as the outcome in other emerging markets?

JAYANT: Well, look at Argentinean peso, it has fallen 40% in the last one year despite that fact that their new president is a pro-free market president, and he has been unable to control inflation in the country. He has been unable to control fall in the value of the local currency. You see the same in Brazil, the president of Brazil is a relatively low pro-market president, and the society has gone against him because he has been trying to implement relatively pro-market policies, so yes, you can actually give them a buffer again. The problem is that these societies are relatively socialistic societies; they’re culturally socialistic societies, which means that they have a tendency to always go back to normal, which is, situations in which they cannot actually pay back their debts.

Argentina continues to suffer despite the seemingly pro-freemarket President, Mauricio Macri. Its currency has fallen by 40% y-to-y.

FRA: What about the situation on the energy? You mentioned the money borrowed over the last 10 years could have gone into infrastructure improvements, especially focused on energy but wasn’t. If you can elaborate on that, how is the situation worsening with some of these, particularly oil exporting nations?

JAYANT: Well, look at Chad and Angola; they are two very interesting cases. Both of these countries have been facing fall in the export of their oil, and the reason is that when oil prices fell in the last decade from $150 to $50 per barrel, these countries because they had created government institutions large enough based on higher prices of oil, were unable to sustain the bureaucracy they had created with when the oil prices fell, the end result was that these people were no longer able to invest capital back into the fields that required capital that they must have invested in the oil fields, which means that they cannot actually increase their oil production now that the oil prices have gone up. But at the same time, oil prices are not going to go back to $150 anymore, and these people are structured to live on the basis of $100 per barrel of oil or higher, and the end result is also what you see in the Middle East, a lot of countries in the Middle East, look at Saudi Arabia, they are now in deficit situation consistently because the current price of oil despite being higher than what it was a year back, is unable to give them enough revenue to the government to deal with, to meet the requirements of the government, and they’re having to use up the money that they have saved over the last many years before the oil price fell.

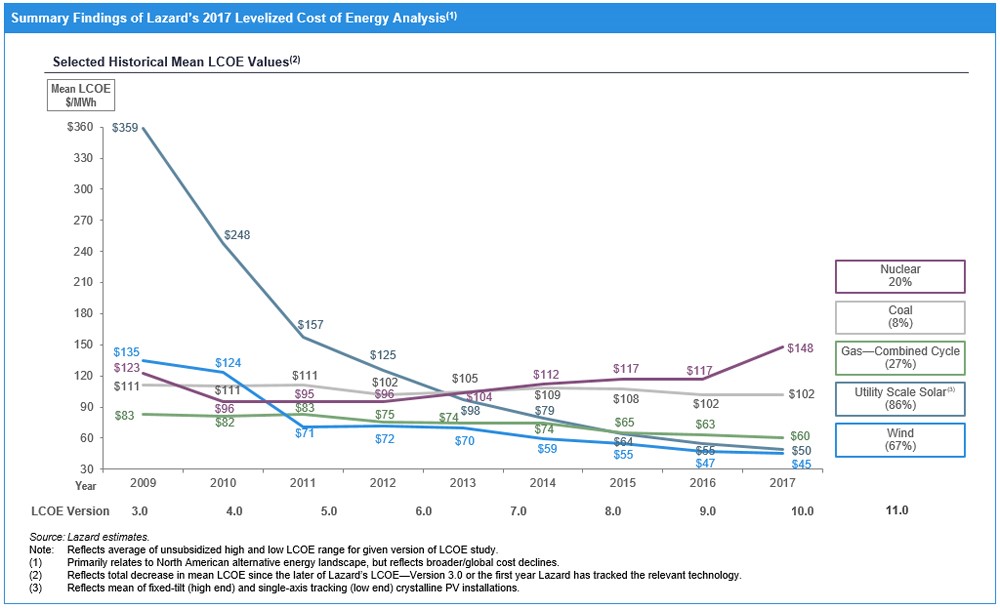

As you can see while costs of wind and solar energy were the highest ten years back, on relative basis they have become cheapest sources of energy.

FRA: Could commodity prices in general go higher considering that oil is at the apex of the commodity stack, if you will? Could that happen even with the rising US dollar?

JAYANT: Absolutely. Commodity prices can certainly rise higher, but commodity exporting countries have basically … Is still not have to feel confident about being able to benefit from higher commodity prices because when commodity prices go up, the cost of producing commodities tend to go up as well because some of the costs of making commodities are costs like oil and other commodities. But also, if you look at what’s been happening in most of Africa, while commodity prices might have gone up, they have actually increased their taxes and they have made it extremely difficult for mining companies to profit from investing in Africa. I’m talking about virtually every country in Africa. The end result is that African countries have become very difficult countries to invest for mining. You see problems in Ghana, you have always seen problems in Zimbabwe, you have increasing problems in South Africa. Unfortunately, even if commodity prices increase, these countries are very likely not going to benefit from that.

FRA: Could we get a situation where with the rise in the interest rates in the US dollar, could we see a potential situation given the plight of the emerging markets whereby there’s an inflow or international capital flows from the emerging markets to the US equity markets in particular given rising interest rates not being good for the bond market. Could we see that similar to what happened in 1927 and 1929 where interest rates also went up and the US stock market also went up? This has been pointed out observers like Martin Armstrong, for example?

JAYANT: I’m not sure what influence it will have on the US equity market, but I certainly see, before our conversation, I was looking at the increase in yields, and it seems to me that part of the reason why US yields have gone up is because the yields have also gone up in the US, which to me is a signal and a symbol that US economy is likely becoming more competitive, and I can see the reasons why it is becoming competitive; regulations are going down in the US, the tax structure and as a result I would not be surprised if equity prices in the US actually continue to improve. If American companies can bring in money from outside the US; if regulations go down and the corporate tax continue to reduce and the filing of tax requirements continue to become less stringent.

FRA: Finally, what are your thoughts on where can investors protect themselves in this environment, or what makes sense in terms of generic asset class for investors?

JAYANT: Richard, I continue to like East Asia: China, Hong Kong, Taiwan, Singapore, Korea, Japan. These are very good stable countries that continue to grow, and there are places where a stock market tend to be rather cheap. I like these countries to invest in. I like gold because the third world countries across the border are suffering and wealthy people in the third world will continue to invest their money in gold. The end result of which is that gold prices will perform going forward. Remember, gold prices have done very well in the last 10 or 15 year timeframe in the last 10 years in US dollar terms, gold has gone up by more than 100%. I continue to feel reasonably good about what’s happening in the US right now.

FRA: Well, great. That’s awesome insight JAYANT, and thank you very much for the charts. How can our listeners learn more about your work?

JAYANT: Everything I do goes on my website, which is Giantbhandari.com.

FRA: Thank you very much Jayant.

JAYANT: Thank you very much for the opportunity, Richard.

05/20/2018 - The Roundtable Insight – Charles Hugh Smith On The Intensifying Pension Crisis

FRA: Hi. Welcome to FRA’s RoundTable Insight .. Today we have Charles Hugh Smith. He is an author and leading global finance blogger and America’s philosopher – we call him. He’s the author of nine books on our Economy and Society including A Radically Beneficial World; Automation, Technology and Creating Jobs for All, Resistance, Revolution, Liberation: A Model for Positive Change and the Nearly Free University in the Emerging Economy. His blog oftwominds.com has logged over 55 million page views and number 7 on CNBC’s top alternative finance sites. Welcome, Charles!

Smith: Thank you, Richard! Always a pleasure to join your program.

FRA: Great. I thought today that we’d do a discussion on what you actually wrote about recently: the tension between the public sector and the private sector. In particular, between public pensioners and the population that pays for that – mainly in the form of property taxes and other fees. This is happening all over North America – this growing tension. Likely to result in a growing pension crisis across the continent and also globally too. This is a global problem as well and just wondering about your thoughts initially on that from your recent writings.

Smith: Right. Thank you, Richard. I think it has been a topic that has that has been suppressed by the mainstream media because there is no easy solution. In other words, the authorities in charge of the pension funds have tended to down-play it by claiming they’re going to make it up from very high returns on capital and other kinds of peen less means but the reality that is now becoming visible is that the public pensions have to be funded at rates that require the cutting of public services. So, there is a seesaw here – that the more money that is put in to the public pension funds to build up their capital to minimum levels then the less money there is available for public services. It is a win-lose situation or a zero-sum game. You can’t find money for both. As the asset bubble economy that we’ve been living in for decade normalizes, or perhaps even declines, then this is really going to be a case where many municipalities and counties are going to be proverbial as time goes out and we’re going to see who is naked.

FRA: Yeah. I mean many of them have built-in assumptions of trying to get 7% to 8% yields in order to make stakeholder obligations but, as you know in financial repression, the repression of interest rates to low values has made it difficult to get yields. A big part of their holdings has been bonds. So, as yields have gone down, it has been made really difficult for the pension funds to meet their yield goals.

Smith: Right. And what has been their response? If you’re one of the fund managers, then you’re piling in to the FANG (Four High-Performing Technology Stocks) stocks, right? Piling into Apple, Facebook, Google and Netflix as the only way to get those kinds of huge returns that are required to keep the funds solvent. We know what happens. These FANG stocks are a tech-bubble that we’ve seen before in 2008. These pension funds are exposing themselves tremendous risks that are way above that of buying a 30-year treasuries or AAA rated corporate bonds, which is as you say, the normal haven for their safe positive return. They’re exposed to a lot more risk so they could end up suffering tremendous draw downs if bond yields continue to rise as we know the value of the existing portfolio on bonds declines accordingly. If the FANG stocks rollover and decline, then that’s going to hit a lot of these pension funds have counted no technology companies to make up for the low yields that you have described.

FRA: Yeah. There are already warnings on that in terms of what could happen otherwise or what could be their response. For example, the Ontario Municipal Employees Retirement System (OMERS), which is actually Canada’s largest defined benefit pension plan with about $95B in net assets. They actually put on their website that deficits will be funded through a combination of contribution rate increases and benefit reductions. They’re already warning that either they’ll be likely much higher property taxes or a cut in benefits to the actual pensioners.

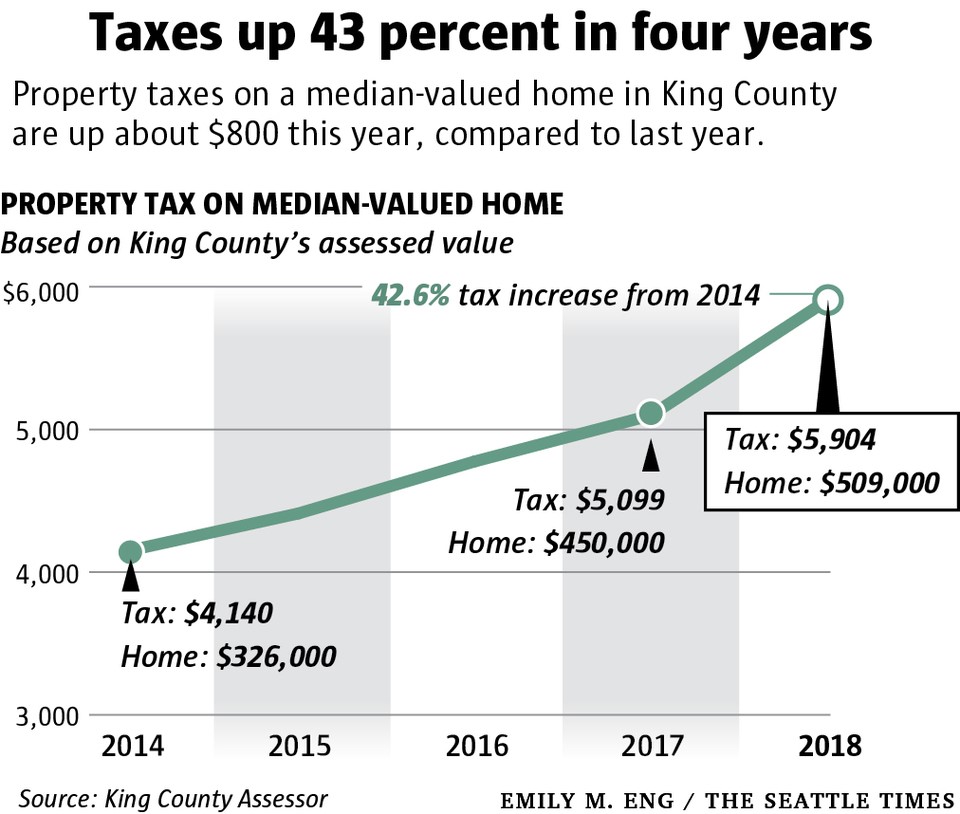

Smith: Right. And maybe we can put some numbers behind these statistics and dynamics that we have been discussing. I have a couple of charts here that I submitted to you before we started recording and the first one shows that the taxpayer contributions into government pensions and that means public sector pensions has more or less doubled in a decade from $60B annually to over $121B and that is skyrocketing. The rate of increase is far above the rate of growth of the economy. In consequence to raise these sums, then municipalities, states and cities are raising property taxes and I have a chart here of King County which is in the Seattle Municipal area.

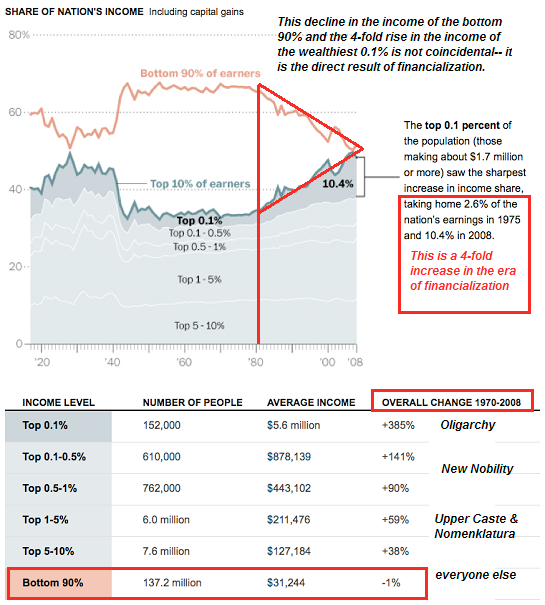

The property taxes there are up 43% in four years. Anecdotally, I just heard someone report their taxes in the Seattle area went up 26% in one year. That may have been local taxes on top of the other property taxes but 43% in four years, that’s more than 10% annual gain there. Most people’s wages have gone nowhere and I have a chart here that is dated a few years but nothing really has changed and it shows that the bottom of 90% when adjusted for inflation, the bottom 137 million households in the U.S. have lost income when adjusted for inflation.

So, the vast majority of households that are property owners are not making more net income here. They’re having to cut their other spending in order to pay skyrocketing property taxes.

FRA: Yeah. Exactly. You also have some other charts in here as well on how, on the other side of the fence, the government pensioners have been paying themselves very lavish pensions – awarding themselves which actually only makes the whole problem worse.

Smith: Right. This was a chart from a Sacramento article regarding the Sacramento area’s fire department’s highest paid pensioners and a number of these people are earning over $200 000 a year in pensions. A $200 000 income will put you in the top 5% of American households.

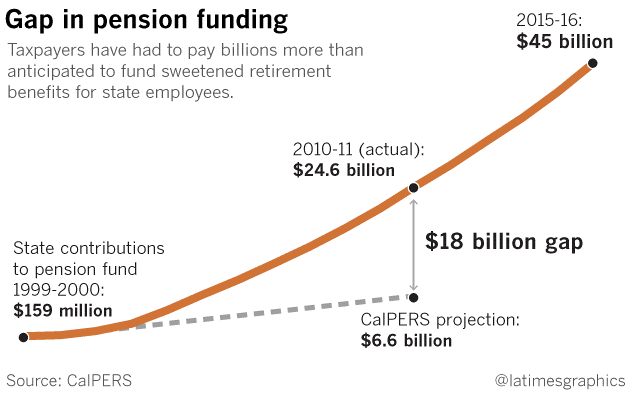

In other words, this is an extraordinarily high income and the number of pensioners in the state of California that earn over $100 000 in pensions annually runs into thousands of people. There is a sense here of great injustice. In other words, the majority of people who are paying property taxes have not seen their income soar by these extraordinary increases that these property taxes are going up by nor do they have pensions in a 6-figure range. So, it feels like exploitation to those of us who aren’t looking for $100 000 – $200 000 in guaranteed pensions. What this is doing is creating huge gaps in pension funding. I have a chart that shows an $18B gap in Calpers which is the largest of pension fund in the state of California.

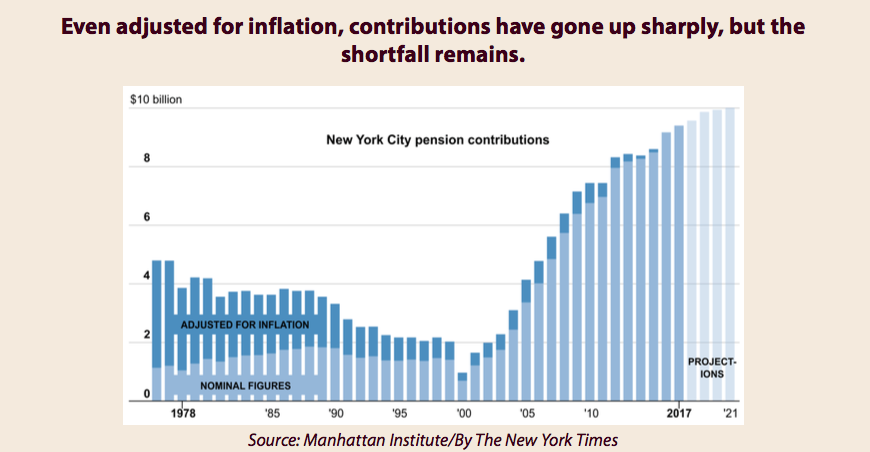

We also see here that we have a chart of New York City pension contributions which soared from about $1B annually around the year 2000 and now it is pushing $10B.

So you’re talking about a tremendous increase and the rate of increase continues. In other words, this isn’t just a one-time bump up and then the pension contributions stabilized. They continue to rise at these rates that are four or five times the growth rate of the economy as a whole and also of wages. Before the program, you mentioned that if we extrapolated these trends, where would we end up?

FRA: Yeah. I mean in your recent writings, you mentioned that the migration to lower tax jurisdictions. Like when somebody is living in Illinois, they may move to Florida. Can you elaborate on that?

Smith: Right. Right. Just to kind of set a context here. The context of what we’re describing is that cities, counties and states are under legal obligations to fund these pensions at the rates that were promised to the pensioners and the only way out of those legal obligations is bankruptcy and many states have unclear laws regarding municipal bankruptcies. In other words, cities and counties in many states do not have a clear pathway to declare bankruptcy and the only way they can raise money to fund the pension plan is to cut public services. You’re hit with the double whammy. In other words, your property taxes and junk fees are rising rapidly. Meanwhile, your library’s hours are being cut, your police departments are being cut and the roads are filled with potholes that can’t be filled unless you pass a special bond. These places that are being crunched by these pension costs – the public is seeing a deterioration in their lifestyle. The local infrastructure is crumbling and there is no money to fund it because all the money has to go to the pensions. I call the people that are stuck in these areas tax donkeys because they’re loaded up with ever higher taxes and it is difficult for them to escape in many cases because of many reasons: kids are in school, family obligations, can’t quit their jobs, etc. So they’re really stuck but there are a very large number of people who tend to be high-income and are mobile. They can leave. They either are childless or their kids have already left home. They work largely in the digital realm so they can work from anywhere. These people are going to migrate and despite the claims of the status quo of politicians in these high-tech states like California, Illinois and New York that people don’t leave. They don’t leave if the services they’re getting keep increasing in quality and quantity every year. In other words, the past is not a good guide to the future because we’ve had an asset bubble based economy for the last decade. So, municipalities have been scoring huge gains in tax revenues which has allowed them to maintain services at a very high level and fund the pensions. Once there is a recession, that goes away then the public services are going to be slashed. So, people like New York City, San Francisco and Seattle but at some point, as homelessness overtakes their neighborhood, homeless encampments show up in their block, crime starts going up, property crime and theft starts going up, and all of that stuff. Good restaurants close because the taxes are too high for them to survive. All these reasons to stay in these high-tech areas vanish. Literally over night. We’re starting to see anecdotally articles from people saying why they’re leaving their cities, for example, Seattle. We’re seeing more and more of these so migration is difficult to track. We know that there is a leakage of population from California and other cities but what is not being captured is the nature of the people who are leaving and I think that if we could dig down those statistics, we’d find that it is the most productive in terms of paying high taxes. It is those people who are leaving because they are the ones caught in the vice. The people who are staying or who are left behind are the less productive or the people who make less money, pay less taxes and absorb more of the government’s services. We can discern a very destructive feedback loops starting now. This feedback loop will only get stronger as we finally get a recession in which the high tax payers are leaving for low tax claims and leaving the people who are depending more and more on the government’s services which are going to be slashed.

FRA: Right. It seems to be an emerging negative feedback loop as you’ve mentioned that is actually non-linear as these more productive citizens leave, then the ones that are left behind are burdened even more to make up for the loss. So it just gets worse in a non-linear way.

Smith: Right. I think that is an excellent observation, Richard. When we think about small-scale entrepreneurs that make cities livable and this includes restaurants, cafes, small theatres and services for the children and elderly and all of these private sector niceties are going to be under tremendous pressure as their customers flee. So they start closing or those people that try to start a new café or restaurant quickly find that they don’t or won’t make enough money to survive as their tax rates go up. I personally am in communication with a lot of people through emails throughout the U.S. where they’re small businesses and they’re noses are just above the waterline. In other words, they’re staying afloat but just barely. There is a huge number of businesses like this that create that non-linear effect that you’re saying. In other words, if property taxes go up another 10% and a recession causes a 5% decline in consumer spending in a city or a county, you’re not going to see a 5% decline in small businesses. You’re going to see a 30-40% decline. That is a huge impact because there are so many people that are right on the borderline. Of course, we can also throw in other factors in which we can be fans of and we can support minimum wage laws and these kinds of things but they’re accumulative. For the small business owner, it is like the property tax, any other junk fees and then the minimum wage increase, and then the higher health care. Each one seems to be something we believe could be absorbed but when you add up 10%, 10% and 10%, then suddenly you’ve got increases of over 40-50% in their fixed expenses and they can’t survive. I think you’re absolutely right that there is going to be an enormous non-linear effects as these feedback loops eke into the class that pays most of the property taxes.

FRA: And the idea that the pension benefits could be cut. What do you think of that? That alone could cause a lot of social unrest, right? – in terms of people not accepting that or not willing to accept those cuts.

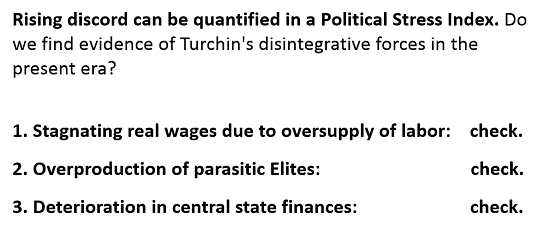

Smith: Right. Well, we’ve seen some examples like the city of Detroit where there was a successful municipal bankruptcy and pensions were cut, what was actually sustainable with the existing pension fund? Of course, that created a lot of unhappiness in the pensioners who felt that they have been promised “X’ and were given half of X. On the other side of the coin, in regions like California, Illinois and New York that are dominated by public unions then the war that is heating up would be first from the public tensions and the public employee’s unions versus the tax payers and in the current arrangement, the taxpayers have very little representation in the local government. They don’t really have a voice. The unions have the political influence so they’re going to fight tooth and nail to keep the pension structure as it is. I think it will require a political crisis, either a tax revolt of some kind or the complete disappearance of all cash where the cities and counties simply no longer have any money. Their accounts have been drained and have zero money to pay people. Until that point comes, then I doubt that the status quo would change. I have a chart here based on Peter Turchin’s work about the disintegrative forces and he identifies integrative eras where people find reasons to work together and disintegrative areas where they find reasons to disagree. He plots this on a political stress index. This is what he calls it. So, what we’re talking about here in the public pension and private sector versus the tax donkeys, we can see the three of the key dynamics that Turchin identified at his work: One of is the stagnating real wages. As I said, for 90% of the workforce that is getting nailed with higher property taxes, wages have not gone up in years and maybe decades. Overproduction of parasitic elites and I think that whether you want to call the parasitic elites public or private, I would lump them all together. People pulling down enormous salaries at the expense of other people – that I think, no matter how you want to describe it, I would call that an overproduction of parasitic elites and the deterioration of state finances. We see that counties and cities have and are struggling now in the second longest economic expansion in history. A tremendous expansion in stock markets and housing values and this is the best of all possible times. If we’re seeing cities and counties struggle with budgets now, then you can imagine what happens when we finally get a real recession. Clearly, we’re seeing point 3 to deterioration in state finances. This dynamic that we’re discussing is definitely increasing the political stress index and it is definitely going to create severe structural, social unrest and social discord.

FRA: Yeah. Exactly. This is very interesting on Turchin’s disintegrative forces. There’s also that idea that as property taxes go higher, we begin to wonder whether you own the property and the concept of property rights comes into question. Is it the government owning the property and you’re just renting the property from the government when property taxes get so high? Your thoughts on that?

Smith: Yeah. I think that’s a great topic, Richard! Before we started recording, you mentioned the model that goes back even to the Roman era when Rome suffered these disintegrative forces that Turchin describes in which people simply abandon their properties. They walk away from it because the taxes are higher than they can afford. The property has lost its value because of this tremendous increase in the tax burden. In my view, places like San Francisco, Seattle and New York (Brooklyn) and a lot of other places, people have tolerated these rapidly rising property taxes because their homes have gone up so much in value. In other words, you’re talking about Seattle – a $500k house a few years ago is now $800k and we see these numbers. So, when you feel like you’ve made $300k in five years or less then you feel like you can afford another five thousand dollars a year in property taxes. But if that $800k house drops to $400k in the next recession, then all of those people are going to suddenly start feeling that it is not so easy anymore to make those taxes. Even more recently than the Roman era, there have been times where cities have gone into decay and this feedback loop that we’ve described and Detroit being a famous example, the value of houses fell to zero. Well, that is an extreme or caused by an extreme depopulation and so on but we have to remember that we’re not talking just about the total value of the home, we’re talking about the home owner’s equity. So, if somebody buys a house for a half million dollar and it drops in value into $400k and their entire equity is forty thousand, they’re now under water by twenty grand. They can walk away and they’ve lost nothing. So, it depends on the debt burden that each of these home owners has taken on. That’s how we could see that even these high value cities start having people jingle mail their mortgage because the property taxes are pushed to fifteen and twenty thousand a year. That’s just a standard in Northern California and many other high value places. As you mentioned before we started recording, there was a news report that one of the branches of the federal reserve suggested a one percent wealth tax on all homes in Illinois to resolve their pension crisis.

FRA: Yes. Exactly. Already I know someone in Illinois paying about 3.3% in property taxes. So something about fifteen thousand dollars per year, over a thousand dollars a month on a house that is approximately $450k in value. To add another one percent on that is a suggestion by the Chicago Federal Reserve to add a proposed one percent on property annually for the next thirty years to cover the pension crisis problem in Illinois. That was just recently proposed by the Chicago Federal Reserve.

Smith: Right. So that one percent – the additional $2500 a year – you can imagine as in a recession, there’s even more as we say in tax revenues start drawing up. The public starts rebelling against the cuts in public services then there’ll be another one percent suggested, then another one percent. This is a dynamic that you’ve mentioned earlier program. We can see the feedback loop here that as tax revenues decline in a recession then they have to raise taxes on those people that are remaining who can’t afford to pay those taxes. Another little dynamic here is that rents in places like Seattle are skyrocketing as well and from the property owner’s point of view, if their property taxes are going up by 10-15%, 20-25% a year, then they feel that there is no option but to raise the rents that they’re charging on their properties. It doesn’t just hit property owners. It eventually bleeds over and hits everybody in a municipality: renters and owners alike.

FRA: It’s interesting when you mentioned how the property values in Detroit went towards zero, this is also been observed by Martin Armstrong who sees Illinois following the exact pattern as the fall of the city of Rome during the Roman Empire era. What he mentions is that more and more people just walked away from their property. There was no bid. Illinois is the number one state that now has a net loss of citizens; people that are fleeing the state. Martin Armstrong writes that there absolutely no hope whatsoever in fixing this problem of a pension crisis in Illinois and every solution like the one from the Chicago Federal Reserve we just discussed will fail in the end. Martin mentions that the state also has colas? (30:24) which insanely increase state employee pensions by an automatic 3% annually regardless of the inflation rate. That’s how crazy things have become. Martin also writes that because Illinois does not have its own currency, it is then bound by the national international value of the dollar. Like Greece, if the dollar rises, Illinois is thrown into deflation. Its institutions are broken and will only be remembered by history. When you plot the actual population of Rome when it emerged, it is very interesting and the stock reality that applies to Illinois is that people could no longer afford to live there. They were forced to just walk away from their homes and the value of real estate went to zero. That’s what Martin writes from the analogy of what happened in history with the city of Rome. One thing to think about in that model is that ultimately, every government or state function, whether it be a city, county, state or federal, the government depends on the private sector to generate the jobs and the income that can be taxed to support the state and its employees. As a general rule, the government in the U.S. is surrounded by 20% of the workforce. It depends on the other 80% of the workforce to generate the taxes to pay the 20% state employees. If you strangle your private sector to where it is impossible to make money, it is almost impossible to start a business that is actually profitable. What happens is that you end depending more on a few large employers. The way that Seattle used to depend on Boeing and now it depends on Microsoft and Amazon. What happens is that these large corporations are also mobile. They are the epitome of mobile capital. They don’t need to stay in these high tax areas. They can leave. They can keep a sort of a façade corporate presence but they can move the 90% of their workforce elsewhere in the U.S. or in the world. Once you become dependent on these very large employers and they move, then your city is absolutely gutted. You go down the Detroit path. Detroit became far too dependent on one industry and a handful of corporations and I see this as extremely likely that Seattle and the San Francisco Bay Area are dependent on these leaders in the tech industry. Once they go away or move elsewhere, then the tax base is going to be cut tremendously because those are the companies that are creating the high income jobs that allow people to buy these over priced homes.

FRA: Ultimately, you see sort of a combination of that with brain drain and wealth drain.

Smith: Right. Exactly. The demographic, we didn’t really talk about this much, but as we know, millennials as a generation are already burdened with tremendous student loan debt and compared to previous generations, their earnings in their 20s and 30s is considerably lower than what was achieved by Generation X and the Baby Boomers. That question comes down to whether the millennials want to marry and have children, unless they’re both brain surgeons or CFOs of a company about to go public or somebody earning extraordinary amounts of money like a quarter million dollars each, that dream is not doable anymore in a lot of places. In other words, they can’t marry and have children, have a decent life and buy a house. Generationally, what we’re going to end up with is that we’re hallowing out these very high cost houses and we’re leaving the baby boomers and people that bought their homes long ago with a lot of equity but we’re putting a lot of incentive for younger families and households to leave because that’s the only way they can afford to buy a house and have a family.

FRA: Wow. That is great insight today from Charles on emerging pension crisis and the growing tension between the public sector and the private sector. Charles, how can our listeners learn more about your work?

Smith: Yeah. Please visit me at oftwominds.com and thank you very much, Richard! Always a pleasure

FRA: Great! Excellent. We’ll end it there and do another one next month.

By Karl De La Cruz

karl.delacruz@ryerson.ca

05/17/2018 - The Roundtable Insight – Yra Harris And Peter Boockvar On How Credit Cycles Are Being Driven By Monetary Policy

05/14/2018 - Illinois Pension Crisis Causing Falling Property Values And Population

“Illinois .. is following the EXACT pattern as the fall of the city of Rome itself .. More and more people just walked away from their property for there was NO BID .. Illinois is the NUMBER ONE state that now has a NET loss of citizens and people are fleeing that state .. There is absolutely no hope whatsoever of fixing this problem of a pension crisis in Illinois and every solution, like the current one from the Chicago Federal Reserve and its proposed 1% on property annually for the next 30 years, will fail in the end. The state has COLAs which insanely increase state employees’ yearly pensions by an automatic 3% annually, regardless of the inflation rate. Because Illinois does not have its own currency, it is then bound by the national value and international value of the dollar. Like Greece, as the dollar rises, Illinois is thrown into deflation. Its institutions are broken, and they will be remembered only by history .. when you plot the actual population of Rome, what emerges is a very interesting and a stark reality that applies to Illinois .. people could no longer afford to live there and they were forced to just walk away from their homes. The value of real estate went to ZERO!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! Beware!!!!!!!!!!!!!!!!!!!! History repeats!!!!!!!!!!!!!!!!!!” – Martin Armstrong

05/11/2018 - Underfunded Big Canadian Pension System – OMERS – Is Planning For Contribution Increases And Benefit Reductions

Danielle Park: “The Ontario Municipal Employees Retirement System (OMERS) is Canada’s largest defined benefit pension plan with $95 billion in net assets (as at December 31, 2017), administering pensions for almost half a million active, deferred and retired employees of nearly 1,000 municipalities, school boards, libraries, police and fire departments, and other local agencies in communities across Ontario.

After losing 15.3% or some $8 billion in value during 2008, the fund recovered over the past 5 years to achieve a top decile average return of 5.9% a year over the last decade. The target return however was 7.3% and so the plan reported a 94% funding ratio (6% capital deficit) in 2017. If the plan was able to achieve its current target return over the next 8 years, OMERS states that it “aims to return the Plan to full funding on a smoothed basis by 2025”.

A 94% funding ratio is robust compared with most other pension plans in the world today. And yet still, 10 years since the last recession and bear market–and the second longest running bull market for financial assets ever in history–OMERS (and other retirement savings plans) are approaching the next bear market still in a capital deficit.

The prospects of netting investment returns of 7.3% a year over the next decade from present price and yield levels, is even less likely than it was over the last decade. So OMERS managers have rightly resolved that the plan must remedy its funding deficit, as laid out on their website:

“Deficits will be funded through a combination of contribution rate increases and benefit reductions.”

Both of these approaches are highly distasteful to members, and increased contributions are anathema to taxpayers, especially since government budgets are already in growing deficit, and most private sector workers today have woefully inadequate retirement savings plans.

After years of kicking the can and pretending that magical markets will make up for insufficient contributions rates, math must be faced, and cutting or reducing annual benefit indexing is generally perceived as the least offensive place to start.

Today, the Civic Institute of Professional Personnel (CIPP) the union representing professionals in the municipal sector in the Ottawa area since 1953, sent this message to its members:

Dear CIPP Members:

OMERS, your pension plan, is currently considering changes to the plan that threaten the financial security of your retirement. Among these changes is the removal of guaranteed indexing of pension benefits. Having an indexed pension means that your retirement benefits are adjusted annually to keep up with the cost of living. Without this guarantee, your retirement income will be eroded by inflation year after year.

To inform you about the proposed changes and what we can do about them, CIPP is organizing an information Town Hall. The proposed date for the Town Hall is Wed, May 23, 2018. Please use the link below before 5:00pm on Monday, May 14th to indicate whether you are interested in attending. Once we know how many members will be attending, we will follow up early next week to confirm the date, time, and location. For those who can’t attend, we will be distributing further information, but this Town Hall will be your chance to ask questions and talk about protecting the financial security of your retirement. We hope to see you there.

On behalf of CIPP’s Board of Directors,

Jamie Dunn, Executive Director, CIPP

Because pension plans have tried for higher returns over the past few years through higher allocations to risky asset classes than ever before, they now face higher drawdown/loss prospects than in past cycles, as we approach the completion of the current one.

This is the tangled web of disappointment woven over the past 20 years in under-saving and over-promising return prospects and benefits/withdrawal rates. Unfortunately, all sides have played a leading role in today’s financial woes and there are no magical ways out.”

05/02/2018 - The Roundtable Insight: David Rosenberg & Yra Harris On Stagflationary Pressures & Volatility In The Economy & Financial Markets

FRA: Welcome to FRA’s The Roundtable Insight .. today we have David Rosenberg and Yra Harris. David is Gluskin Sheff’s chief economist and strategist with a focused on providing a top-down prospective to the firm’s investment process and asset mix committee. He received both a bachelor and Master of Arts degree in economics from the University of Toronto. Prior to joining Gluskin Sheff he was chief North American economist at Merrill Lynch in New York for seven years during which he was consistently ranked in the institutional investor all-star analyst rankings. Prior to that he was chief economist and strategies for Merrill Lynch Canada based out of Toronto. He is the author of Breakfast With Dave a daily of distillation of his economic and financial market insights and I think now there’s espresso with David also that’s out. Yra is an independent trader, a successful hedge fund manager, a global macro consultant trading in foreign currencies, bonds, commodities and equities for over 40 years. He was also CME director from 1997 to 2003. Welcome gentleman.

DAVID: Thank you very much.

YRA: thank you Richard, this is a great honor for me, thanks.

FRA: yeah, it’s a great honor for having David on our show, first time and I thought we’d begin with some of David’s recent thoughts. You recently wrote about how Canadian equity markets go higher even US markets go lower as a hedge against inflationary pressures. Can you give us some insight on that?

DAVID: Well sure, it’s not even an opinion it’s a fact in a sense that it’s happened so many times in the past and most recently in 2007 and in 2008 as the US market went down 20% in the opening months of the … market. The Canadian market was up 20% and of course, then the wheels fell off when it turned into a global near depression after AIG and Lehman collapsed. But it’s because the Canadian market being so exposed to the commodity cycle and energy and there are so many other sector correlations with the resource sector and the resource sector is classically psycho value. The SME of 100 is because the classic growth index, Canada doesn’t have much in the way of healthcare exposure, doesn’t have much way in a technology exposure. These are there groppy aspects of the US market that’s kept it alive and well for so long. Either you’re buying on the premise that we are entering into the late cycle, I think there’s a lot of evidence and if it late cycle then it’s value over growth and then if you’re talking about stylistic investing value over growth you have to understand if you look at North America Canada is deep value in terms of sector representation. The US is much more growth oriented. I look at it not just from historical experience in terms of late cycle investing but just looking at evaluations. The Canadian stock market right now trades at a forward multiple of a 14.7 times the coming year’s earnings estimates. In the United States that number is over 16. I look at some other benchmarks as well in terms of valuation matrix and wherever there’s been a day that the Canadian stock market has been this inexpensive relative to the United States.

FRA: Yra have you seen that type of behavior in the financial markets in in your trading?

YRA: It’s interesting to see David and having read his work for so many years. Mine doesn’t take that type of analysis. I will read that and put that into my thought process but then I have to ask, David, about yesterday when to governor Palu speak and his concerns about that their Canadian personal debt levels were elevated and she’s like the bank of Canada is worried about them. How would that play into that scenario? That’s the question that would arise from the way that I would analyze this. I’d like to hear David speak to that.

DAVID: Right. I think that as far as I know the only central banker that is talking insistently about debt exposures and sensitivities and fragility is the Bank of Canada. I guess that’s partly because there’s no real bubble this time around in US household balance sheet. I would argue that even letting out the cash, we have some sort of a bubble in the US corporate balance sheets. Debt worldwide looking at governments, we all own this debt. We can say this … debt in US household balance sheets but the government debt, if we look at corporate debt, household debt. We’re in a situation now where globally outstanding debt in all levels of society is 164 trillion that’s with a T trillion dollars. We’ve already taken out the previous credit bubble peak of 2007 and half that debt and it might not be households in United State system, this time around. We’re get to a government debt bubble I’m sure looking at the future fiscal situation in United States half that debt is in Japan, China and the US. Basically this is a global situation, we just happened to have an honest central banker in Ottawa talking openly about it. He’s basically saying that this is actually one of the risks for the Canadian economy. We have NAFTA risks, we have really an incoherent energy policy to ship the oil out of Canada at the present time. Hopefully that’s going to change. We have divergent tax policies. All that is true. The Canadian economy even with the community boom is destined to underperform the Unites States economy. Of course we don’t have fiscal stimulus in the tax side that the US has so that goes without saying. You see that’s from my economics perspective and then when you put in a strategy a heart, what do you see? Well you’re on the correlations and you’ll see that the Canadian stock market, the TSX does not have that much of a correlation with the Canadian economy, believe it or not. That’s because most of the companies in Canada are truly global in nature. Even the Canadian banks, so you’d been thinking wow the Canadian banks, how much would be exposed. These are giant multinational corporations. You have banks like the bank in Nova Scotia that had a branch in Latin America before they ever had a bunch in Toronto. Going back a century or more. You go along the whole eastern seaboard in United States all you see are those green comfy couches from the Toronto dominion bank. You see what I’m saying basically is that the Canadian stock market has a much more torque to the global economy than it does to the Canadian economy. It doesn’t mean that there’s some special situations or some consumer cyclicals or consumer discretionary stocks that are relayed back into Canadian domestic demand. I will way suggest to stay away from those. I think the energy stocks here, McTaps are priced very attractively and I have nothing to do with the level of Canadian debt on the household site. You have a lot of Canadian companies you see if the bank of Canada hadn’t been keeping interest rates below the US and right now there’s a big negative interest rate spread. Look at where oil prices are right now. The Canadian dollar should be at 85 cents in quotes, should be but it’s not, it’s closer to 78 cents. Well there’s a lot of Canadian companies that have very high at us dollar revenue streams that we’re going to benefit immensely from this ongoing shall we say surreptitious policy in Ottawa to keep their Canadian dollar depressed. Something that doesn’t manage to make it to Donald Trump’s tweets is where the Canadian dollar is relative to the US dollar but that benefits a lot of Canadian exporters.

YRA: You think that that’s an active policy out of Ottawa that’s extended to central … heavily involved in that. Believe me I believe that … Certain as I can look to see what the Australian … When the RBA issued its statement the other night they all target currency whether they do it in the open but when you talk about the strength of your currency and your reason to keep interest rates on a hold … I understand the G40, I understand the G7 but if these are active policy then of course it gives leverage to the Ross Navarro Lighthouse Group about what countries are doing. So you think that that’s an act of policy approach from Ottawa?

DAVID: Well look there’s nobody that … Especially the central bank that’s going to come out and tell you where they would like to see the Canadian dollar. They’re not going to say directly. I think your comment before is right. I think of Steven Mnuchin’s comments in Davos which I believe he made on January the 24th which was like two days before the stock market peaked. Talking openly about the wonders over having a cheap us dollar. The trade weighted US dollar index is dominated by the euro and in the euro really peel back over the course of the past couple of weeks. I never really understood why I thought about 125 to begin with. The reality is that for Canadians what the Australian dollar does if you’re trading aussie currency you do business in Australia that’s obviously important but for Canada over three-quarters of our exports go to the US so that’s what really matters for the Canadian economy and for Canadian profits is that particular relationship. Maybe it is off the radar screen. You can’t have it both ways. If you’re going to have a situation where Donald Trump’s spray team and his NAFTA team creates this air of uncertainty. Nothing has happened yet and maybe we don’t get this solved until later this year if at all. What it does in Canada is it creates this cloud of uncertainty and when you’re uncertain because don’t forget if you’re setting up shop in Canada you’re not really just setting up shop as a business to service 35 million Canadians, you’re doing it the service 300 million Americans south of the border, that’s where the big market is. If you’re going to create a situation in Washington where you’re going to put this cloud of uncertainty over your chief trading partner called Canada you don’t get business investments. Business investment stays in the sidelines. Without business investment you don’t get a lot of growth, you don’t get a lot of employment. Nothing is zero in Canada but the economy is being held back by this air of trade uncertainty that is something that Canadians have imported from the United States. We didn’t start this whole thing, we got to renegotiate NAFTA. What that does is as the Fed raises rates the bank of Canada just says we’re on hold basically because we are frozen in time here for a variety of reasons. Stephen Poloz has mentioned several times that NAFTA uncertainty is part of it. What’s the … going to say? You’re deliberately keeping interest rates below where they are here and they’re artificially depressing the Canadian dollar. The Canadian government will say we’d rather not do that but because you’re creating this air of uncertainty because Canada is a much more intense export-oriented country than the united states is so NAFTA matters infinitely more for our economy than those in the states so naturally we are going to keep rates below and keep the Canadian dollar artificially below until something changes. We successfully renegotiate NAFTA, then that could all change. There is a method behind the madness whether or not it would ever be openly admitted. It’s funny because in the last policy review, the Bank of Canada just came out and lament about Canadian competitiveness. How our non-energy exports have lacked far behind what their models would say. That is code for we’re comfortable actually from a policy perspective having the Canadian dollar trade at competitive levels to make interest rates… or it should be for an extended through a period of time.

YRA: the amazing this is, and I am long term bullish on the Canadian dollar. First of all because, if we go back to the great financial crisis, for lack of a better word. The Canadian banks were certainly low capitalized. They did not suffer because of their lending risk. Their lending practices were so much better than the US banks probably by design. Number two there’s never been a quantitative easy program in Canada. There’s no quantitative easy program as Peter Boockvar would say. You have to go to quantitative tightening. I mean overall the underlying fundamentals to the Canadian financial system, yes I know they got a little bit of a bubble because they’re achieving rates over than it should be by regular market signaling. I think Canada is very well positioned. Once they work through the points that you just raised.

DAVID: I agree with what you said but, I think that we really do have to complete the analysis in this sense because, there are some fundamental reasons why the Canadian economy is being held back. There’s a fundamental reason why a lot of capital investment has been deflected away from Canada. There’s a reason why the Canadian dollar is trading about seven cents below any semblance of equilibrium value. Still on the other side of the equation, we have … You could say well the United States is blowing its brains out on physical policy. Well that might be true. But for the here now, for the first time in decades, the net effect of corporate tax rates in the United States is lower those is in Canada. In Canada being the junior partner and younger brother, we have to have compelling reasons for companies to want to set up shop here. We have to have lower tax rates here. We’re not a price maker on tax policy globally. We’re a price taker not a price maker. It was disappointing that there was no reference outside of one sentence to any response to what happened in the United States. Vis-à-vis at least the corporate tax situation, and then you layer on the accelerated depreciation analysis. If you’re a North American company right now, you’re incentivized to the taxes from right now to book your revenues in the United States which means that’s where the employment and investment are going to be directed towards at the expense of Canada. We have diverging fiscal policies point number one. We don’t have a coherent energy policy which is a very big problem. Hopefully that could change, but that will take a lot of political will, especially at the federal level. On top of that, we do have the situation where consumer balanced sheets are over extended. How that plays out. Of course you do have overextended housing markets in Toronto and Vancouver, which is not 100% of the national market, but it’s still 35% of the national market, and that’s not exactly trivial. I would say that there are some constraints. There’s all this sort of things that is on the bank of Canada’s radar screen, they’ve talked about it. There’s still some I would have to say, you could argue that there are unresolved issues in the United States as well. There’s at least as many if not more can at the current time.

FRA: What do you think of the rising US dollar as a recent trend? Is that going to take place for a longer period of time or … Is it related to the nine trillion and overseas US dollar the nominated corporate then?

DAVID: Well I think that it’s … It’s this classic economics 101. It’s the country that is tightening monetary policy, and the country that is using fiscal policy is usually the country that has the stronger exchange rate. That generally comes through in relative industry differentials. To me the big surprise for the past year, up until the trade weighted dollar starts to really turn around, it’s Back to where it was the first week in January. There was a time where if you looked at the yearly trend in the US dollar, just in the opening months of the year was down roughly 10%. That was really what would go against any macroeconomic textbook would tell you where the currency should be going. Then there was the other side of the argument which is that we have this band of trade protectionist in Washington. You have a president who his whole professional life and now carries it inputs his political life has always made [unintelligible] the current account deficit is his modus operandi. There’s another side, another side to the equation that well, if United States is going to ever want a really balance its deficit, well it’s going to have depreciate it’s currency 10% which is exactly what happened. I think that as this comes down to the old market refrain that you typically get the currency that your president wants. It was no secret that president Trump, would have preferred to have a weak currency that boots exports. I think what’s happening now is this realization. The Fed futures contracts are pricing in more fed. You’re seeing in the UK Mark [unintelligible] is peeled back. The ECB has more less gone quiet. The BOJ is not going to be doing anything. The Bank of Canada the view the beginning of the year was that they were going to raise rates several times. The only central bank it seems right now that’s in play in terms of raising rates is the Fed. I think that’s been part of it. You’ve also seen … Although the data flow in the United States has not been very impressive. I can’t do summersaults over 2.3% GDP growth the same quarter that we got. The fiscal stimulus. Be that as it may it’s the old saying about, in the land of blind the one eyed man is king. I suppose the US with 2% growth is the king, because the data in the UK have been very weak. The data in the Euro zone in particular has been extremely soft over the course of the past few months. I think there is this view on a relative basis that these interest rates differentials are going to work in the US dollars favor. Even more than people thought a couple of months ago. I think that’s a starting to finally come through in the currency markets.

FRA: Yra your thoughts.

YRA: Well, being a currency trader for over 40 years, and I’ve written about it for the last year. … The dollar, there’s fiscal stimulus coupled with interest rates differentials, and how the central bank is raised their rates when nobody else is, sure as David directly says. There’s always been the backup to a stronger currency and where was it. I of course … I agree with it because, I go back to that when Trump was having all the manufacturing, CEOs at the White House back in January February 2017, and Mark Fields who was then the CEO of Ford comes out and immediately calls the currency manipulation the mother of all trade barriers. Well that’s evidently what got discussed at the White house, and that Trump [unintelligible] the euro moved from 106 pretty much history line all the way up to 125, 126. Which bothers one mind because … I’m not one who accepts the European growth story willy-nilly. I think that’s a lot of nonsense to me, I say that for many reasons. The missing dollar really has caused a lot angst to the market, a lot of large hedge funds had miserable years trying to make that trade. I stone cold agree with that. I think now that we’re getting a little more maturity and some more negotiating tactics, there’s no question in my mind that guys like Robert … and Ross Mnuchin, I’m not sure what to make of … Certainly the Navarro they will use the currency as leverage. Trump especially accepts that. It’s interesting David say that the president gets the currency that he wants eventually. I think that’s is true and now I think the market is just … It’s just liquidated in some of the short dollar positions and trying to work through their way through this, this understanding with the dollar differential, the interest rate differentials. Certainly favors the United States and now we saw … with a phenomenally devilish press conference last Thursday. I think the ECB would relish nothing more than the weaker euro. That gets a question I … My favorite train would probably be long gold and short all the fiat currencies, not necessarily the dollar expression because interest rates to the US of course are now … We can argue what are, but they’ve at least going to a real yield. I don’t think there’s anywhere else in the world of the main developed nations where you get a real yield, on your short of interest rates. I think at least the dollar will hold here barring any type of any misstep by the US administration.

DAVID: I’ll just add further that. Look at where the two year note is trading right now at two and a half percent. Then take a look and see where a two year German bond is trading at -0.6. You have over a 300 basis point gap. Not even taking out any real duration risk. Like coming to the front end of the US seal curve compared to we’re in Germany. That spread is widened out, you asked me what’s changed. If that spread is widened out in Americas favor to the tune of 40 basis points just in the past three months. I think that’s really what caught the raider screen a lot of FX traders and why the US dollar starting to come back to life there.

YRA: I agree and plus, in saying that because I know a lot of traders who … They would buy, well when you thought the Euro was going higher, they would do these as unhedged decisions because there wasn’t enough in it. Because if you put your hedges on, by the time you do it wasn’t worth doing. Now, there’s enough meat on that bone to do those things and still being able to hedge a position who wanted to generate a much greater return than you could have as David talks about. That 40% rise in the differential I significant to attract people’s attention.

FRA: In terms of volatility David why do you think markets have been more volatile this year versus last year?