Pension "Peril & Poverty"

Global Investing "FATCA"

- FATCA

- PFIC

- Citizenship Taxation (including the absurdity of 1986 Tax Legislation for "Mars"??)

- Unofficial Capital Controls Now in Place

- US 2008 "Exit Tax" (for citizens and green card holders on unrealized gains)

- Inheritance IRS tax grabs

- The new Ex-patriot Act

- Investing Abroad

- The rate of Acceleration of restrictive foreign choices for Americans

- The growing movement towards second citizenship protection

- Why the legal abolishment of cash is coming

Global Investing "Internalizing"

Inflation / Deflation

Store of Value Challenges

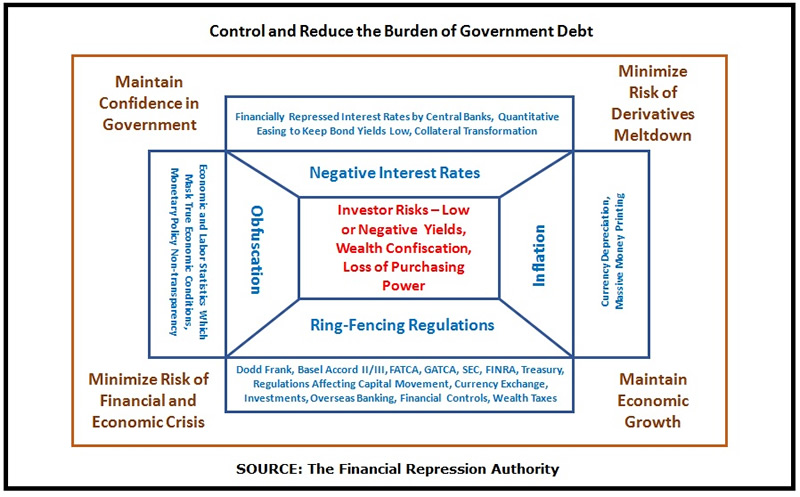

Policy Controls

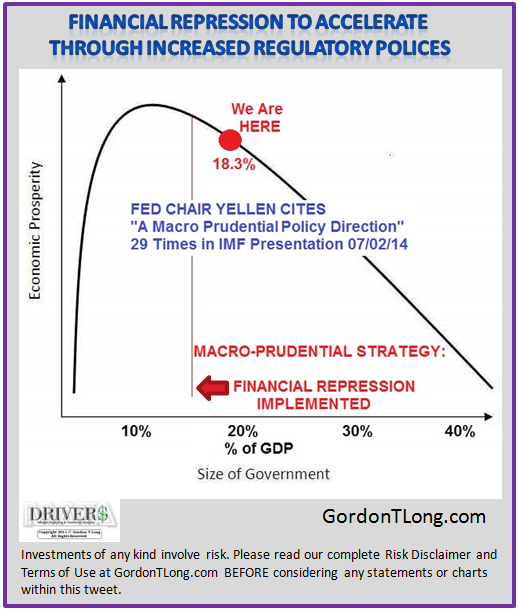

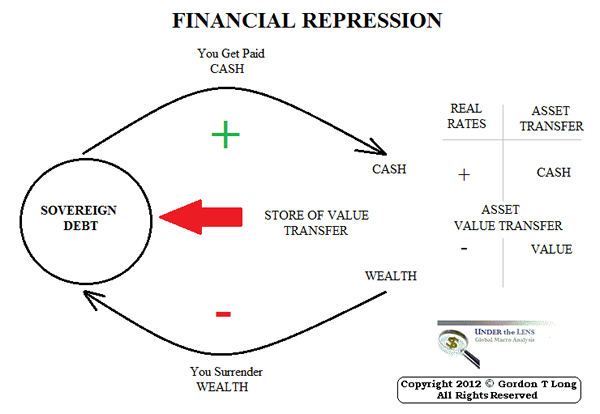

- January 2015 Financial Repression - New IMF Paper on The Liquidation of Government Debt

New IMF paper by Carmen Reinhart & M. Belen Sbrancia .. presents how public debt is often reduced through the use of financial repression - a tax on bondholders & savers via negative or below market real interest rates .. from abstract:High public debt often produces the drama of default and restructuring. But debt is also reduced through financial repression, a tax on bondholders and savers via negative or below-market real interest rates. After WWII, capital controls and regulatory restrictions created a captive audience for government debt .. Financial repression is most successful in liquidating debt when accompanied by inflation. For the advanced economies, real interest rates were ne gative ½ of the time during 1945–1980. Average annual interest expense savings for a 12—country sample range from about 1 to 5% of GDP for the full 1945–1980 period. We suggest that, once again, financial repression may be part of the toolkit deployed to cope with the most recent surge in public debt in advanced economies." - October 2014 - Financial Repression is Very Low Interest Rates for a Very Long Time

The 16th annual Geneva Report by the International Centre for Monetary and Banking Studies & written by senior economists including 3 former senior central bankers, predicts interest rates across the world will have to stay low for a "very, very long" time to enable households, companies, & governments to service their debts and avoid another crash .. The report's authors expect interest rates to stay lower than market expectations because the rise in debt means that borrowers would be unable to withstand faster rate rises .. "Global debt-to-GDP is still growing, breaking new highs .. At the same time, in a poisonous combination, world growth and inflation are also lower than previously expected, also – though not only – as a legacy of the past crisis. Deleveraging and slower nominal growth are in many cases interacting in a vicious loop, with the latter making the deleveraging process harder and the former exacerbating the economic slowdown. Moreover, the global capacity to take on debt has been reduced through the combination of slower expansion in real output and lower inflation." - October 2014 - Financial Repression is the likely approach for Governments to pay down debt

Great insightful article on financial repression by Daniel Amerman .. questions how the U.S. federal government can pay down its enormous debt .. sees 4 primary options that the government can take: 1) Decades of austerity with higher taxes and lower government spending. 2) Defaulting on government debts. 3) Inflating away the value of the debt through rapidly slashing the value of the currency. 4) Using "Financial Repression", a process that is complex enough that the average voter never understands how it works, thus allowing governments to use this potent but subtle method of taking vast sums of private wealth, year after year, decade after decade, with almost no political consequences. The essay reminds readers the 4th option is the likely approach, points out the world took this approach in the 1940s through the 1970s to pay down government debt .. "Because of the sheer size of the problem – most of the population must be made to participate, year after year. Financial Repression therefore uses an assortment of carrots and sticks to ensure that investors have little choice but to participate – on a playing field that has been rigged against them as a matter of design – even if they are among the small minority who are aware of what is being done to them."The essay covers 4 areas of financial repression: 1) Inflation (Shearing #1) 2) Negative Real Interest Rates (Shearing #2) 3) Funding By Financial Institutions (Fence #1). 4) Capital Controls (Fence #2). - September 2014 - Governments Implementing Financial Repression

International Man article on how western world indebted governments need money, how they will protect the big banks at the expense of the citizens with financial repression .. The International Monetary Fund (IMF) published a horrifying paper, called The Fund’s Lending Framework and Sovereign Debt. That paper in turn was based on one from December 2013, called Financial and Sovereign Debt Crises: Some Lessons Learned and Those Forgotten .. The December 2013 document, right at the start, says that financial repression is necessary: "The claim is that advanced countries do not need to resort to the standard toolkit of emerging markets, including debt restructurings and conversions, higher inflation, capital controls and other forms of financial repression .. As we document, this claim is at odds with the historical track record of most advanced economies, where debt restructuring or conversions, financial repression, and a tolerance for higher inflation, or a combination of these were an integral part of the resolution of significant past debt overhangs." .. The IMF report goes on to say: "Governments can stuff debt into local pension funds and insurance companies, forcing them through regulation to accept far lower rates of return than they might otherwise demand .. Domestic defaults, restructurings, or conversions are particularly difficult to document and can sometimes be disguised as 'voluntary' .. The Fund would be able to provide exceptional access on the basis of a debt operation that involves an extension of maturities .. That means that 30-day notes can be instantly turned into 30-year bonds." - this last sentence means the ability to change 30-day notes into 30-year bonds, effectively holding the money captive for a much longer period of time - Monetary Policy & Financial Repression in Britain, 1951 - 59

New book coming out by William Allen on Monetary Policy and Financial Repression in Britain, 1951 - 59 .. this book explores the politics of formulating monetary policy in the 1950s, the tools implementing it & discusses the parallels between the present monetary policy & that of 1951 .. "Drawing on official archives, this study describes how monetary policy was decided on, implemented and communicated at a time when the government was struggling with massive post-war debts while maintaining welfare and military spending and cutting taxes. It discusses the roles of the Governor of the Bank of England, Cameron Cobbold, and of successive Chancellors R.A. Butler, Harold Macmillan, Peter Thorneycroft and Derick Heathcoat Amory, and Macmillan's continued dominance of monetary policy after he became Prime Minister. It explains the intimate relationships between monetary policy, government debt management and fiscal policy, and the use of 'financial repression'." - Low Interest Rates & Inflation To Address Financial Repression

Article points out the worse things get on the European financial/economic crisis, the more pressure there is on the European Central Bank (ECB) to print money - stocks will likely go up as this happens on the anticipation that the ECB will given in & start money printing .. "The ECB would print money and use it to buy eurozone government bonds, in order to prop up the region’s banking sector, and to encourage more risk-taking by lenders and investors. Of course, any hint of more money-printing always cheers the market, and European stocks reacted well to the news." .. the article points to how U.S. & UK stocks have similarly reacted positively on all the money printing .. whether all this money is good for the economy or whether it even benefits the economy in any positive way is another question .. the article emphasizes the approach of financial repression taken by the U.S. & UK in keeping interest rates down & allowing inflation to rise in order to pay off some government debt via inflation, rather than by defaulting or cutting back spending .. most western world governments are in this bind, so that "we could see interest rates staying lower than markets expect for some time. And in the longer run, we could see a lot more inflation than we’ve been used to as well" .. in terms of investing, the article suggests sticking with countries that are looking to do more money printing & that have relatively inexpensive stock markets, such as Europe or Japan. - This Is Going To Destabilize The Entire World Financial System

Ronald-Peter Stoferle, Incrementum AG "Bond prices in practically all industrialized nations are near all-time highs. Never before have interest rates been this low on a global basis. If one examines these events more closely, it becomes clear that the underlying problems cannot be solved by global zero interest rate policy, but that the natural selection process of the market is instead being undermined .. Interest rates are the heart, soul and life of the free enterprise system .. This truth is however veiled and distorted at the moment. Governments, financial institutions, entrepreneurs and consumers that are acting in an uneconomic manner are thus kept artificially afloat. As a result, instead of them being punished for their errors, these errors are perpetuated. Protraction of this process of selection leads to a structural weakening of the economy, and a concomitant increase in the system's fragility .. Declining interest rate levels make a gradual increase in public indebtedness possible, while the interest burden (as a share of government spending) does not grow .. Without negative real interest rates, the steadily growing mountains of debt would long ago have ceased to be sustainable. Central banks are increasingly prisoners of the policy of over-indebtedness .. Central banks and governments are currently trying to create an increase in prosperity out of nothing. Such a monetary perpetuum mobile would be quite desirable for humankind, however, historically such attempts have at best led to a brief sugar high followed by a major hangover. - Alasdair Macleod On The Markets: Keep Calm & Carry On

"Investment is now all about the trend and little else. You never have to value anything properly any more: just measure confidence. This approach to investing resonates with post-Keynesian economics and government planning. The expectations of the crowd, or its animal spirits, are now there to be managed. No longer is there the seemingly irrational behaviour of unfettered markets dominated by independent thinkers. Forward guidance is just the latest manifestation of this policy. It represents the triumph of economic management over the markets .. Doubtless there is a growing band of central bankers who believe that with this control they have finally discovered Keynes’s Holy Grail: the euthanasia of the rentier and his replacement by the state as the primary source of business capital. This being the case, last month’s dip in the markets will turn out to be just that, because intervention will simply continue and if necessary be ramped up .. But in the process, all market risk is being transferred from bonds, equities and all other financial assets into currencies themselves; and it is the outcome of their purchasing power that will prove to be the final judgement in the debate of markets versus economic planning." - The Fed's Financial Repression At Work: How Big Blue Was Turned Into A Wall Street Slush Fund

David Stockman -- "IBM is a poster child for the ill-effects of the Fed’s financial repression. In effect, the Fed’s zero interest rate policies are telling big companies to issue truckloads of debt and use the proceeds to buyback shares hand-over-fist. That way fast money speculators on Wall Street are appeased by the resulting share price lift, and top executives collect bigger winnings on their stock options." - Time For Regime Change At The Eccles Building: Interest Rate Pegging Is Destroying Capitalism

07-13-14 David Stockman - BoJ To Engage In 'Financial Repression'; We Stay Long USD/JPY - BNPP

07-11-14 eFX News "Japan now has one of the highest inflation rates in the G10. Our economists expect the BoJ to engage in ‘financial repression’ to restrain the rise in JGB yields that results from Japan’s fiscal dynamics," BNPP says as a rationale behind this view. "A larger overshoot in Japan’s inflation rate would also see the yen weaken. If inflation gets out of hand, we could, our economists suggest, see an ‘operation twist’ policy in Japan – similar to that witnessed in the US. This would entail aggressive purchases of JGBs coupled with interest rate hikes to stave off inflation. The resultant inversion in the yield curve, along with the upside shock to inflation, is a risk scenario for Japan and the ensuing adverse growth-inflation paradigm would necessarily entail a weaker yen," BNPP argues. "In addition, a re-allocation in the government pension investment fund (GPIF) and a likely pick-up in Japanese outflows will mean JPY weakens," BNPP adds. - Expropriation Is Back - Is Christine Lagarde The Most Dangerous Woman In The World?

Zero Hedge - Norway Sovereign Wealth Fund Unveils "New Strategy" - Buy 5% Of Every European Stock

06-24-14 - Boston Consulting Group Study

September 2011 - Financial and Sovereign Debt Crises: Some Lessons Learned and Those Forgotten

December 2013 IMF - Extending Maturities on Bonds

05-22-14 IMF

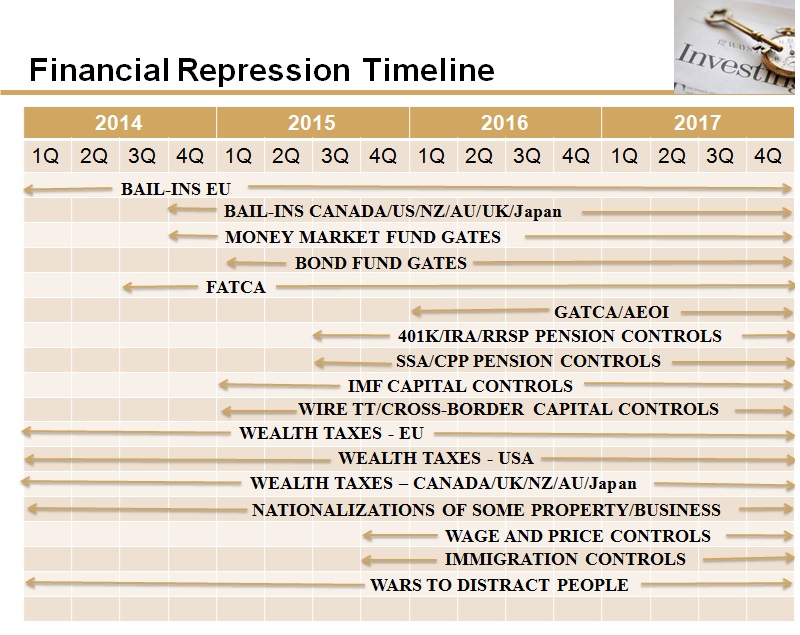

Regulations and Legal/Political Challenges

- U.S. Pushing Banks On Dodd-Frank Act To Make It Easier For Government To FREEZE YOUR MONEY - Financial Repression Via Regulations

"The U.S. wants big banks to simplify their Dodd-Frank Act resolution plans so it's easier for government to freeze your money." .. Bloomberg reports on the progress made by Wall Street banks developing their "living wills" as part of the Dodd-Frank Act legislation attempting to minimize "too big to fail" banks .. Bloomberg: "The Federal Reserve and Federal Deposit Insurance Corp. told 11 of the largest U.S. and foreign banks, including JP Morgan Chase & Co. (JPM) and Goldman Sachs Group Inc. (GS), that they botched their so-called living wills. The agencies ordered the banks to simplify their legal structures and revise some practices to make sure they can collapse without damaging the wider financial system." Jim Rickards - Fischer worries about macroprudential policy

07-10-14 FT Mr Fischer’s most interesting remarks relate to his experience with macroprudential policy in Israel. Israel’s bank supervisor used a range of tools to restrict mortgage lending and try to avert a housing bubble. Mr Fischer draws three lessons: - Prohibiting Banks From Paying Interest On Demand Deposits

Regulation Q - Basel Accord II and III

05-16-14 Cliff Küle - The Level Of Economic Freedom In The United States Is At An All-Time Low

- **FRA POST: Central-Planners Herd Money Market Funds Into Government Financing

- **FRA POST: Fund managers now have the Legal Right to 'suspend redemptions' by the you on your Money Market Funds

- “Redemption Gates” for Money Market Funds

Acting Man --"The adoption of 'redemption gates' effectively means that money market fund boards will be able to suspend the property rights of their customers. Once again, this creates a big disadvantage for the money market fund industry in favor of banks, since demand deposits will continue to lack such 'redemption gates', in spite of the fact that banks are de facto unable to actually pay out all demand deposits, or even a large portion of them, 'on demand'. It is an interesting detail that retail customers are to be exempt from this regulation based on the idea that they are basically too addled to react to crisis conditions. Why are such regulations held to be required at all? Are regulators implying that the system has not been 'made safe' by adopting several telephone book-sized tomes of additional regulations?" - SEC Votes Through Money Market Exit Gates

Zero Hedge -- the SEC has adopted the news rules designed to curb the risk of money market investor runs .. "Among the changes, funds will have to switch to a floating share price instead of the current $1/share (hence the term breaking the buck). But the key part: 'The SEC's rule will require prime money market funds to move from a stable $1 per share net asset value, to a floating NAV. It also will let fund boards lower redemption 'gates' and fees in times of market stress." .. suggests this may send money market investor rushing out & into other asset classes - the SEC, the Federal Reserve & the U.S. Treasury hope that asset class is stocks to keep the stock market rising .. "Clearly, everyone understand that the only purpose behind implementing 'gates' is to redirect the herd. And with some $2.6 trillion in assets, money markets can serve as a convenient source of 'forced buying' now that QE is tapering if only for the time being. The only question is whether the herd will agree to this latest massive behavioral experiment by the Fed, and allocate their funds to a stock market which is now trading at a higher P/E multiple than during the last market peak." - ALERT: Pull Your Money From Money Markets Now!

Economic Policy Journal - U.S. SEC poised to adopt reforms for money market funds

Reuters - Fund managers on alert over money market shake-up

FT -The SEC is looking to drive money market funds to only government securities, especially institutional money market funds - this means money market funds will be helping to pay for the government debt .. The SEC is also planning to allow fees and restrictions on redemptions in times of stress, but it is not clear how widely these will be applied across the money markets - FT: "Any restrictions on redemptions may not be severe at first, but the regulations will only become more restrictive over time. Don't waste time thinking you are going to monitor the situation and get out later. Get out now, when the getting is easy." - GATCA and FATCA

02-22-15 Haydon Perryman - Capital Controls Rolling Into High Gear Under FATCA

05-28-14 Dollar Vigilante - Interest On Bank Deposits & Federal Reserve Excess Deposits

11-27-14 Cliff Küle - First HSBC Halts Large Withdrawals, Now Lloyds ATMs Stop Working

- Martin Armstrong Warns Europeans Of The Coming Expropriation Of 10% Of Everyone's Accounts Zero Hedge

- Chart Of The Day This Is What Generational Theft Looks Like

- Poland Confiscates Half Of Private Pension Funds To -Cut- Sovereign Debt Load

- Europe Considers Wholesale Savings Confiscation, Enforced Redistribution

- When the Defaults Come, So Will the Wealth Grab

07-04-04

Obfuscation: Government Statistics and Economic Reporting

- Charting The Death Of The Saver

- September 2014 - Financial Repression Through Shrinkflation

Financial Repression Using Shrinkflation: "As ‘shrinkflation’ becomes no longer viable, it will soon reveal itself in the form of higher consumer prices. And with central banks around the world creating inflation as a policy measure so as to inflate away the world’s massive debt pile, the question remains as to whether the central banks will be able to control this deliberately induced inflation in an environment where ‘shrinkflation’ no longer works." - Feeling poorer through the power of inflation

MyBudget360

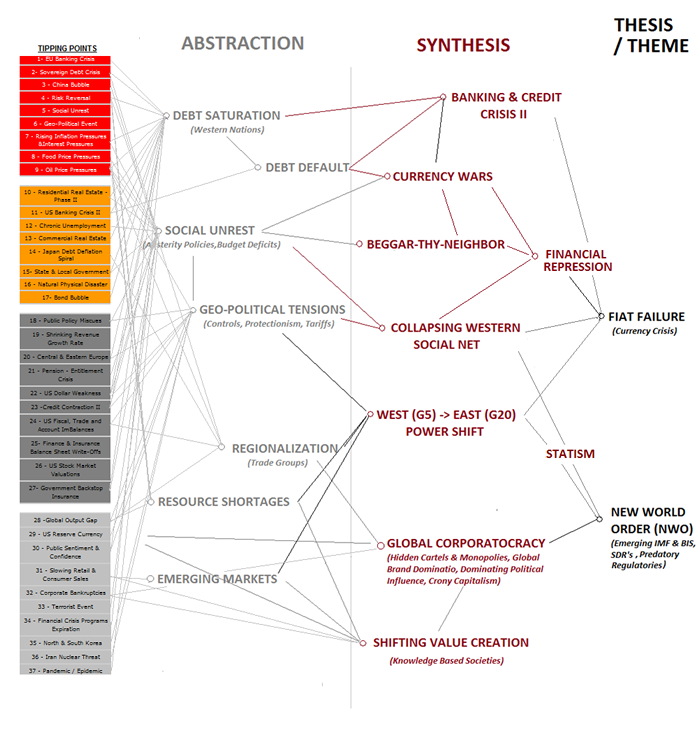

Thesis Paper

Abstract

Through the Process of Abstraction the 2012 Thesis outlines how the Global Macro is presently on a well defined path towards a global Fiat Currency Failure and the emergence of a New World Order.

2012 will be highlighted by social unrest during a period of heightened conflict and tension. As economic growth declines and chronic unemployment becomes even more broad based on the world stage, Macro Prudential Policies of Financial Repression will accelerate.

Increasing centralized planning and control by sovereign government will further push advanced societies towards collectism and statism.

Abstraction