Webinar with Sprott’s John Embry (the Special Guest), Conquer Change’s Robert Ian, Financial Survival Network’s Kerry Lutz, and Financial Repression Authority’s Gordon T Long.

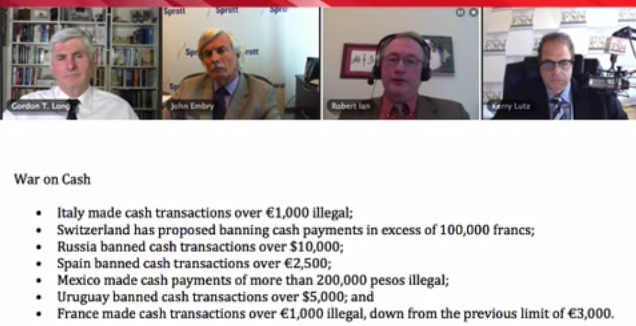

05/24/2015 - Sprott’s John Embry Talks Financial Repression, War on Cash, Gold

05/24/2015 - Sprott’s John Embry Talks Financial Repression, War on Cash, Gold Webinar with Sprott’s John Embry (the Special Guest), Conquer Change’s Robert Ian, Financial Survival Network’s Kerry Lutz, and Financial Repression Authority’s Gordon T Long.

05/24/2015 - Sprott’s Rick Rule Talks Financial Repression, War on Cash, Gold

Webinar with Sprott’s Rick Rule (the Special Guest), Conquer Change’s Robert Ian, Financial Survival Network’s Kerry Lutz, and Financial Repression Authority’s Gordon T Long.

05/23/2015 - Federal Reserve Paper Suggesting a Carry-Tax on Cash

Graham Summers on the war on cash – part of financial repression .. identifies a Federal Reserve paper written back about 15 years ago calling to do away with cash entirely .. the idea proposed was to implement a “carry tax” on physical cash using an expiration date if depositors are not willing to spend the money .. “The idea here is that since it costs relatively little to store physical cash (the cost of buying a safe), the Fed should be permitted to ‘tax’ physical cash to force cash holders to spend it (put it back into the banking system) or invest it .. The way this would work is that the cash would have some kind of magnetic strip that would record the date that it was withdrawn. Whenever the bill was finally deposited in a bank again, the receiving bank would use this data to deduct a certain percentage of the bill’s value as a ‘tax’ for holding it .. The Fed has declared a War on Cash, and a ‘carry tax’ is coming.”

LINK HERE to the Article & Paper

05/23/2015 - European Bank Bail-ins Coming?

– Euro banks no more stable now than in run-up to financial crisis crash

– Banks in France, Spain, Italy are “highly vulnerable to failure”

– Low quality bank equity not sufficient to withstand shock

– Risk to system “enormously underestimated”

– Investor deposits at risk of “bail-ins” – financial repression

05/20/2015 - REGISTER NOW for our Free Webinar with RICK RULE and JOHN EMBRY on The War on Cash, Financial Repression, Solutions to these Risks

FinancialSurvivalNetwork.com and FinancialRepressionAuthority.com present: LIBERTY MASTERMIND LIVE WEBINAR. Join Kerry Lutz,  Gordon Long and Robert Ian (ConquerChange.com) as they interview renowned financial and precious metals experts JOHN EMBRY and RICK RULE. Mr. Embry is Chief Portfolio Strategist at Sprott Asset Management and

Gordon Long and Robert Ian (ConquerChange.com) as they interview renowned financial and precious metals experts JOHN EMBRY and RICK RULE. Mr. Embry is Chief Portfolio Strategist at Sprott Asset Management and

Mr. Rule is Chairman of Sprott U.S. Holdings. This LIVE event will feature up-to-the-minute analysis of the markets with a discussion of current events/trends including the War on Cash, Financial Repression, Gold and Silver, and YOUR QUESTIONS.

This Webinar is presented by the Liberty Mastermind Symposium and is sponsored by:

FinancialRepressionAuthority.com – Macroprudential Policy Advisors – educating investors globally in understanding the challenges of investment and protection in the unfolding Era of Financial Repression.

FinancialSurvivalNetwork.com – Helping you survive and thrive in the new economy.

05/20/2015 - The War on Cash – What You Can Do Now

Mark Nestmann essay focuses on the war on cash, offers helpful suggestions to investors & savers .. Here is Nestmann’s advice:

1. draw down bank reserves & accumulate cash – document the withdrawals to prove the legal origin of the cash in the future

2. make sure you get newly issued bills because more than 95% of circulating bills are tainted with drug residues which under U.S. law allows the cash to be confiscated

3. convert a portion of assets in banks or in cash to gold – store it outside of the banking system

4. keep the assets you maintain in banks which are strong to avoid the coming bail-ins

5. consider putting some assets into electronic-based currencies [like Bitcoin, BitGold etc.]

05/19/2015 - Russell Napier: The War on Cash will cause gold to be used as money again

The war on cash is an unintended consequence of the financial repression macroprudential policy of the zero or negative interest rates .. if your bank is charging you interest on your bank deposit, why not just get your money & leave it under your mattress at 0% (higher) yields? – so governments & central banks are likely to attempt to abolish cash to eliminate this action .. what will be the effect on gold? – Russell Napier: “In such a world, zero-yielding gold would be a high-yielding instrument. If the authorities ever sought to restrict access to banknotes, then gold would suddenly find itself enfranchised as money for the first time in many decades. So, given the scale of these competing forces, it is just too early to say what might happen to the gold price, but the allure of gold will grow the more it becomes clear that central bank fiat has failed and the age of government fiat is dawning .. The time is ever nearer when the price of gold will rise in an era of deflation. In due course, though no time soon, the full force of government fiat will engineer a reflation, albeit one replete with the misallocations of savings and capital so beloved by the bureaucrat. Then the PhD standard, in which the value of money is linked only to the words of the over-educated, will have ended. The gold price will rise even further, ‘And the words that are used for to get the ship confused will not be understood as they’re spoken, for the chains of the sea will have busted in the night’. And that’s ‘The hour when the ship comes in.’”

05/18/2015 - Financial Repression: The War on Cash

International Man’s Nick Giambruno & Mises’ Joe Salerno .. the financial repression of ring-fencing regulations is intensifying in the war on physical cash .. the goal to eliminate the use of hand-to-hand currency, so that governments can document & control every transaction .. one way this war is being fought is by making it illegal to pay in cash above a certain threshold:

Joe Salerno: The War on Cash is the attempt by governments to phase cash out of their economies. Governments hate cash because they hate the financial privacy cash makes possible. And they prefer that you keep your money in a bank to help prop up an unsound fractional reserve banking system .. The War on Cash reflects the desperation of governments .. it really says that they are bankrupt, both literally, in the sense that they can’t pay what they’ve promised, and intellectually.

05/17/2015 - “WAR ON CASH” is a Strategic Requirement to IMPLEMENTING SUSTAINED NEGATIVE INTEREST RATES

We Can’t Rein In the Banks If We Can’t Pull Our Money Out of Them

1- Physical paper money provides the check against negative interest rates, for if they become too great, people will simply withdraw their funds and hoard cash.

2- Furthermore, paper currency allows for bank runs. Eliminate paper currency and what you end up with is the elimination of the ability to demand to withdraw funds from a bank.

Complete abolition of cash threatens our very freedom and rights of citizens in so many areas.

Paper currency is indeed the check against negative interest rates. We need only look to Switzerland to prove that theory. Any attempt to impose say a 5% negative interest rates (tax) would lead to an unimaginably massive flight into cash. This was already demonstrated recently by the example of Swiss pension funds, which withdrew their money from the bank in a big way and now store it in vaults in cash in order to escape the financial repression. People will act in their own self-interest and negative interest rates are likely to reduce the sales of government bonds and set off a bank run as long as paper money exists.

For depositors, this means they really need to grasp what is going on here for unless they are vigilant, there is a serious risk of losing everything. We must understand that these measures will be implemented overnight in the middle of a banking crisis after 2015.75. The balloons have taken off and the discussions are underway. The trend in taxation and reduction of cash seems to be unstoppable. Government is not prepared to reform for that would require a new way of thinking and a loss of power. That is not a consideration. They only see one direction and that is to take us into the new promised-land of economic totalitarianism.

The movement toward electronic money is moving at high speed and this says a lot about the state of the financial system. The track record of the major financial institutions is nearly perfect – they are always caught on the wrong side when a crisis breaks, which requires their bailouts. The fact that we have already seen test runs with theory-balloons flying, the major financial institutions are in no shape to withstand another economic decline.

An official White House panel on spying has implied that the government is manipulating the amount in people’s financial accounts.

If all money becomes digital, it would be much easier for the government to manipulate our accounts.

Indeed, numerous high-level NSA whistleblowers say that NSA spying is about crushing dissent and blackmailing opponents … not stopping terrorism.

This may sound over-the-top … but remember, the government sometimes labels its critics as “terrorists“. If the government claims the power to indefinitely detain – or even assassinate – American citizens at the whim of the executive, don’t you think that government people would be willing to shut down, or withdraw a stiff “penalty” from a dissenter’s bank account?

If society becomes cashless, dissenters can’t hide cash. All of their financial holdings would be vulnerable to an attack by the government.

This would be the ultimate form of control. Because – without access to money – people couldn’t resist, couldn’t hide and couldn’t escape.

Its Happening Everywhere there are Financial Problems – Nowhere Else?

The central banks are … planning drastic restrictions on cash itself. They see moving to electronic money will:

FRANCE

France passed another Draconian new law that from the police parissummer of 2015 it will now impose cash requirements dramatically trying to eliminate cash by force.

French citizens and tourists will then only be allowed a limited amount of physical money. They have financial police searching people on trains just passing through France to see if they are transporting cash, which they will now seize.

Meanwhile, the new French Elite are moving in this very same direction. Piketty wants to just take everyone’s money who has more than he does. Nobody stands on the side of freedom or on restraining the corruption within government. The problem always turns against the people for we are the cause of the fiscal mismanagement of government that never has enough for themselves.

GREECE

In Greece a drastic reduction in cash is also being discussed in light of the economic crisis. Now any bill over €70 should be payable only by check or credit card – it will be illegal to pay in cash. The German Baader Bank founded in Munich expects formally to abolish the cash to enforce negative interest rates on accounts that is really taxation on whatever money you still have left after taxes.

EUROPE

There is a growing assumption that the negative interest rate world (tax on cash) is likely to increase dramatically in Europe in particular since it is socialism that is collapsing. Government in Brussels is unlikely to yield power and their line of thinking cannot lead to any solution. The negative interest rate concept is making its way into the United States at J.P. Morgan where they will charge a fee on excess cash on deposit starting May 1st, 2015. Asset holdings of cash with a tax or a fee in the amount of the negative interest rate seems to be underway even in Switzerland.

People can’t pull cash out of their bank accounts – for political reasons, because they’ve lost confidence in the bank, or because “bail-ins” are enacted – if cash is banned.

The Financial Times argued last year that central banks would be the real winners from a cashless society:

Central bankers, after all, have had an explicit interest in introducing e-money from the moment the global financial crisis began…

The introduction of a cashless society empowers central banks greatly. A cashless society, after all, not only makes things like negative interest rates possible, it transfers absolute control of the money supply to the central bank, mostly by turning it into a universal banker that competes directly with private banks for public deposits. All digital deposits become base money.

05/17/2015 - One of the 4 Pillars of Financial Repression: Data Obfuscation

Dr Pippa Malmgren, a former U.S. Plunge Protection Team member, explains how governments fudge price inflation numbers .. It’s one of the pillars of financial repression – obfuscation.

05/16/2015 - ALLIANZ PRESENTATION SLIDES: Redefining Risk in the Next Phase of Financial Repression

Allianz website to help navigate the risks in the unfolding era of financial repression .. how to find new opportunities & combat new risks in a rising-rate, slow-growth environment.

05/09/2015 - Allianz Global Chief Investment Officer Andreas Utermann on Financial Repression

Allianz Global Investors (Allianz GI) using the following strategies to address investing in the era of financial repression: equity long/short, merger arbitrage, options trading, commodities, volatility, global macro, absolute return bonds, private debt, infrastructure debt & infrastructure equity .. Global Chief Investment Officer & Co-Head at Allianz GI Andreas Utermann: “In an environment of financial repression, characterised by much lower future expected returns from the beta element of all asset classes, these strategies can help investors capture alpha.”

05/08/2015 - IMF Paper on “Capital Flow Management”: Financial Repression – Capital Controls

05/07/2015 - CUSTODIAL RISK QUESTION TO ANSWER: What do you really own when you buy an investment?

In our complex financial world of securities, derivatives, counterparty agreement and rehypothecation of the collateral of assets under management virtually no one has the actual physical share certificates of stocks or other assets held by their custodial financial investment firm.

“Custody Risk is one of the biggest, most important issues to consider if you want to maintain your wealth when the next round of systemic risk hits!” Graham Summers – Phoenix Capital

TWO PROBLEMS

1- CUSTODIANS OFTEN DON’T KNOW WHERE YOUR ASSETS ARE HELD

The SEC recently performed a study of some 400 investment advisor firms. As the SEC itself stated in its report – approximately one-third (140) failed to meet custody rule requirements. What this says is custodians don’t know where their clients funds are! Many didn’t even know they themselves were legal custodians of their clients funds!

2- YOUR ASSETS WILL LIEKLY BE FROZEN WHEN YOU NEED THEM MOST

Even if an appropriate legal framework is in place to eliminate the risk of loss of value of the securities held by the custodian in the event of its failure, it can take weeks or even months to transfer the securities to new custodians. During that time, you cannot close out open positions .. they are effectively frozen.

In the case of MF Global, some investors were locked out of their accounts and couldn’t trade their positions for weeks. As a result many of them incurred massive losses.

05/02/2015 - Financial Repression in Australia Will Likely Lead to Investments in Precious Metals LINK HERE to the Article or view below

05/01/2015 - Obfuscation – One of the 4 Pillars of Financial Repression

Alasdair Macleod points out the obfuscation going on between government economic data & price distortions in the financial markets .. highlights theChapwood Index as a true cost-of-living inflation measure in America – it reports on the actual cost & price fluctuation of the top 500 items on which Americans spend their money on .. as you can see in the above chart, it is much higher than the government reported numbers .. “Understated price inflation fundamentally distorts everything that is macroeconomic, from monetary policy to economic commentary. It misleads central bankers into thinking they are missing their inflation targets when they are in fact exceeding them by a dangerously wide margin. It misleads analysts into thinking we are on the brink of a deflationary slump with prices maybe about to collapse. And most worryingly of all, bond markets have become more mispriced than even hardened bears realise, something that’s very likely to be corrected through a financial shock .. Just think of all those bonds that the banks have acquired as zero risk investments under Basel III rules .. If bond markets discounted, as the Chapwood Index suggests they should, a U.S. inflation rate consistently around 10%, the 10-year U.S. Treasury bond should yield at least that, possibly more. The price would halve to meet those redemption yields, and lesser credit-worthy bonds would fall even more, a development for which all financial markets are wholly unprepared, not to mention the knock-on effects on stocks, derivatives and of course, mortgage rates.”

04/25/2015 - Financial Repression: Negative Interest Rates Now Happening in Australia … 04/24/2015 - Financial Repression is Leading to the Death of Money

04/24/2015 - Financial Repression is Leading to the Death of Money

“Destroying currency amounts to belittling or ending time value, which is a crucial part of gauging and setting risk parameters in the real economy. If there is no time value to money there is essentially no reason to engage in risky behavior. This is what Keynes described as a ‘liquidity preference’, though for different reasons. Instead of individuals holding too much cash, banks will do so because of that same repression. So at the very least, where the central bank is intent on ‘forcing’ spending through negatively manipulating the currency, they are at the same time destroying the financial basis to produce credit – all the while herding financial agents into holding even more ‘currency’ … How do central banks respond to this? … By deciding that currency isn’t dead enough.”

– Jeffrey Snider

04/18/2015 - Financial Repression Explained: It’s about Macro Prudential Policies to Control and Reduce Government Debt

WSJ article highlights how as interest rate benchmarks go negative, banks may be paying borrowers .. “Negative interest rates in Europe have created a previously inconceivable problem for some banks: They may soon have to pay interest to customers who borrow from them .. The novel problem is just one of many challenges caused by negative interest rates. All over Europe, banks are being forced to rebuild computer programs, update legal documents and redo spreadsheets to account for negative rates . Banks, hoping to avoid the expense of having to pay their borrowers, are turning to central banks for guidance. But what they are hearing is less than comforting.” .. it’s financial repression.

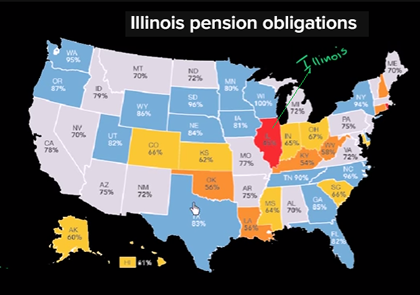

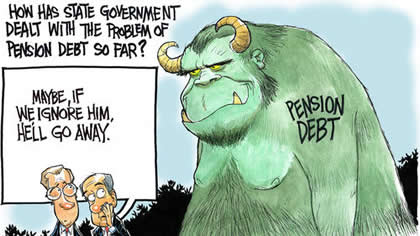

04/18/2015 - MISH SHEDLOCK talks AMERICA’S PENSION PROBLEM

Mish Shedlock talks about the magnitude of the mounting Pension Problem in America and uses his home state of Illinois as a prime example. According to a State Budget Solutions, last year’s state unfunded pensions reached an all-time high of $4.7 trillion. This funding gap state public pension plans are underfunded by $4.7 trillion, up from $4.1 trillion in 2013. Overall, the combined plans’ funded status has dipped three percentage points to 36%. Split among all Americans, the unfunded liability is over $15,000 per person.

ILLINOIS’ PENDING PENSION CRISIS

“Illinois Pension’s in general are 39% funded! This is after this massive rally we have had since 2009 in financial assets. Some of the worst ones are only about 20% funded. I think the Teacher’s Pension Plan is about that and the General Assembly and Judicial Pension Plan are also on the bottom.”

“Various cities in Illinois have problems, Chicago being one of them. The City of Chicago has a huge pension crisis right now. We have things in Illinois like “Home Rule Taxes” where cities can levy their own taxes in addition to the state. That is why we have varying sales tax that range anywhere from 6% to 10%, depending on locality.”

“I believe Chicago is Bankrupt!”

“I have been working with the Illinois Policy Institute. There are a number of cities in Illinois (I am not going to name them), but I am aware of five cities (one of them a major city – not Chicago) that are ready to file bankruptsy – and it is all over the pension issue! The problem is they can’t file bankruptcy because the state doesn’t allow it.”

“The fundamental problem is they have made more promises than they can possibly keep!”

GAMING THE PENSION SYSTEM

The problem is “you have police and fire workers who can retire after 20 years … and collect up to 70% of their earnings based on the 5 highest years salaries. We see a lot of pension spiking in the last few years where for example police work overtime (which counts towards their best five years) so these workers stand to collect far more in retirement (total years in retirement) than they actually ever made while working (total years worked).

“Tax payers are actually funding the employees portion of the pensions by excessive wages and direct contributions “.

“Chicago (has) floated General Obligation Bonds to actually just fund current expenses. That is illegal! We have bonds here in Illinois that are called tax exempt on the basis they are supposed to be funding long term infrastructure expenses that are funding short term needs.”

PROPERTY TAXES THE JURISDICTION OF UNDERFUNDED CITIES & TOWNS

“Taxes in Illinois are are already obscene. A homeowner on a $600,000 home can expect to pay $14-15,000 per year – every year on property taxes. Do you really own your own home in Illinois? On top of tht you have 10% sales tax.”

“Pensions are so underfunded in Illinois that they are going to go bust in the next slowdown. I believe one (a slowdown) is on the way.”

THE NEW, LOOMING PROBLEM FOR STATES, CITIES AND TOWNS

Negative interest rates are sweeping the globe. How will states, cities and towns fund themselves and their pension obligations in an era of potential negative nominal bond rates?

“How will states, cities and towns fund (attract) long term assets with 15 year negative bonds?”

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority