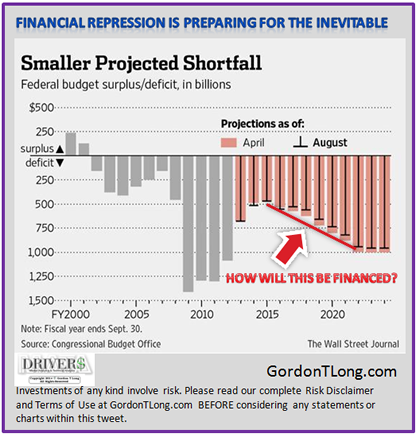

FINANCIAL REPRESSION IS

THE ONLY SOLUTION

(FROM THE GOVERNMENT’S PERSPECTIVE)

How will these deficits be financed when the present budget debates causes such Congressional wrangling & gridlock?

09/02/2014 - Financial Repression is in preparation for the inevitable that is now clearly visible.

09/02/2014 - Financial Repression is in preparation for the inevitable that is now clearly visible.

FINANCIAL REPRESSION IS

THE ONLY SOLUTION

(FROM THE GOVERNMENT’S PERSPECTIVE)

How will these deficits be financed when the present budget debates causes such Congressional wrangling & gridlock?

09/01/2014 - Surviving The Age of Financial Repression

Mark Yusko, founder and CEO of Morgan Creek Capital Management, shares his perspective on how institutional investors make money during gloomy economic times at Thomson Reuters‘ PartnerConnect East conference– conference last year, but principles still applicable .. If you invested $10 million in U.S. Treasuries seven years ago, you could expect an annual return of $480,000, but today you see a return of just $24,000 a year, Yusko points out .. “In this age of financial repression, we have to think differently about how we invest .. Surving the Age of Financial Repression.”

08/31/2014 - Federal Reserve Vice Chairman Says U.S. Preparing Bank Bailins

“The Great Recession is a near-worldwide phenomenon, with the consequences of which many advanced economies continue to struggle. Its depth and breadth appear to have changed the economic environment in many ways and to have left the road ahead unclear .. Work on the use of the resolution mechanisms set out in the Dodd-Frank Act, based on the principle of a single point of entry–though less advanced than the work on capital and liquidity ratios–holds the promise of making it possible to resolve banks in difficulty at no direct cost to the government .. As part of this approach, the United States is preparing a proposal to require systemically important banks to issue bail-inable long-term debt that will enable insolvent banks to recapitalize themselves in resolution without calling on government funding–this cushion is known as a ‘gone concern’ buffer.”

– Federal Reserve Vice Chair Stanley Fischer

LINK HERE to the article

08/30/2014 - Renunciation of U.S. Citizenship About To Get More Expensive: From $450 to $2350 America’s Corralito Tightens

With an exponentially increasing number of Americans & U.S.-based companies renouncing their citizenship, the U.S. State Department is now looking to raise the cost of renunciation from U.S.$450 to U.S.$2350on individuals .. [Cliff Note: Expect similar regulations or rule changes soon to keep U.S. corporations from renouncing their citizenship through overseas corporate inversions, like what Burger King is doing now .. America’s corralito tightens .. ]

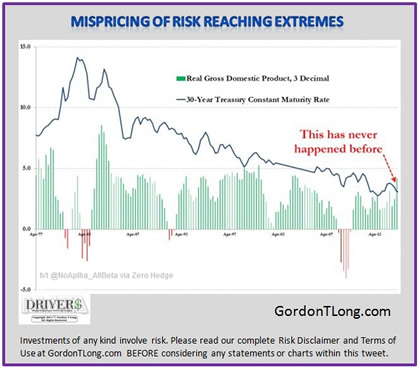

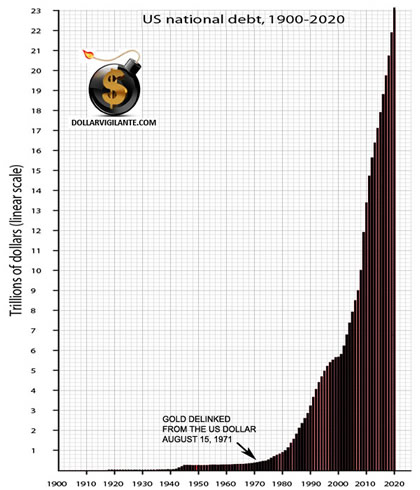

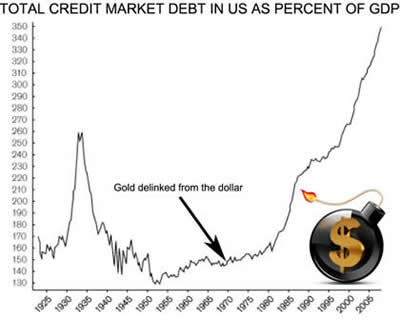

08/29/2014 - For the first time in history, (based on FRED data), the 30Y constant maturity yield is below the real GDP growth level.

FINANCIAL REPRESSION IS

COMPLETELY DISTORTING

THE PRICING OF BOND RISK

(The RISK is in FIAT US$ CURRENCY)

08/29/2014 - Jeff Berwick – Financial Repression

The founder of the well recognized Canadian web site Stockhouse Media Corporation and CEO until 2002, Jeff Berwick says “around 2003 I woke up and started studying and learning (and I am still doing that to this day) and the more you learn the deeper this ‘rabbit hole’ gets! We are living under a financial system that is completely not real! People are going to find this out pretty soon!”

Berwick defines Capitalism as “the free voluntary transactions of human beings where every transaction improves the lives of eveyone. They (government) have been portraying capitalism as evil.”

Berwick defines Capitalism as “the free voluntary transactions of human beings where every transaction improves the lives of eveyone. They (government) have been portraying capitalism as evil.”

Because of this the future suggests to Berwick that ” whoever loses the least over the next decade, will win the most! It is going to be a game of not losing everything.”

“We are going to go through the ‘Great Transition’ in the not to distant future which the internet will facilitate and which could potentially be the saviour of humanity. The real issue over the next few years is trying to get enough people to understand what is wrong about this world and what could be right about it. Then let the people decide”

His recommendation for Americans who he believes ‘are the most asleep people in the world (from his perspective living outside America), is to “put your assets into hard assets that Janet Yellen can’t counterfeit into obscurity.”

FINANCIAL REPRESSION in Jeff Berwicks words:

“Financial Repression all started in 1913 with the foundation of the third central bank of the US, the Federal Reserve. Income tax came into existance with the same act which people should find interesting! …. The Repression as you call it (Oppresssion as I call it) of the Central Banking, Communist System has been hidden from people because of a tremendous amount of productivity…. the government and bankers tell people things are good because of them – in actuality things are worse because of them – a lot worse. Hardly anyone sees this…. they have taken away from the true human potential.”

The answer is that “we need an awakening where people begin to realize what is going on and move beyond this really horrible system of statist, communists, central bankers, fiat currencies and go to a solid money (like precious metals and bitcoin) and allow the markets to make decisions”.

The answer is that “we need an awakening where people begin to realize what is going on and move beyond this really horrible system of statist, communists, central bankers, fiat currencies and go to a solid money (like precious metals and bitcoin) and allow the markets to make decisions”.

“People need to wake up, turn off their TV (it is literally ‘programming’) and start listening to real information. People need to break free from these chains. If they don’t, unfortunately they will get hurt in this coming “Great Transition”. As in life someone always has to pay for mistakes and some people are ging to pay more than others. We are unfortunately all going to have to pay. It is going to be a dramatic period and incredibly stressfull…. America is going to be ground zero for this transition “

“There is going to be a great evolution in everything we know today in the next decade. It is going to be biblical in proportion. The sooner you start to look into these things (whether gold, silver, real estatre, bitcoin) the better”

08/28/2014 - WHAT WEALTH CONFISCATION MAY LOOK LIKE FOR AMERICANS

“Would the U.S. government really turn to a 1933-style gold grab again? .. I would argue that they wouldn’t, but that doesn’t mean the threat to your gold has diminished .. If the government is looking to confiscate wealth, they’ll likely go for the low-hanging fruit like financial accounts, which can be plundered with a few mouse clicks. Or they’ll continue to ramp up the inflationary money printing, which is a way to confiscate from savers .. If and when an executive order is issued to convert a portion of your retirement savings into unwanted Treasury securities, it will likely apply only to the most susceptible retirement assets — those being accounts with the large, traditional IRA custodians. These assets are soft targets for the government. They could be frozen, confiscated, or nationalized at the flip of a switch.”

– Nick Giambruno, Senior Editor InternationalMan

LINK HERE to the article

08/27/2014 - FINANCIAL REPRESSION REQUIRED TO PAY GOVERNMENT DEBTS & UNFUNDED OBLIGATIONS

MONEYWEEK.COM article points out the worse things get on the European financial/economic crisis, the more pressure there is on the European Central Bank (ECB) to print money

– stocks will likely go up as this happens on the anticipation that the ECB will given in & start money printing

.. “TheECB would print money and use it to buy eurozone government bonds, in order to prop up the region’s banking sector, and to encourage more risk-taking by lenders and investors. Of course, any hint of more money-printing always cheers the market, and European stocks reacted well to the news.”

.. the article points to how U.S. & UK stocks have similarly reacted positively on all the money printing

.. whether all this money is good for the economy or whether it even benefits the economy in any positive way is another question

.. in terms of investing, the article suggests sticking with countries that are looking to do more money printing & that have relatively inexpensive stock markets, such as Europe or Japan

.. the article emphasizes the approach of financial repression taken by the U.S. & UK in keeping interest rates down & allowing inflation to rise in order to pay off some government debt via inflation, rather than by defaulting or cutting back spending

.. most western world governments are in this bind, so that “we could see interest rates staying lower than markets expect for some time. And in the longer run, we could see a lot more inflation than we’ve been used to as well”

08/26/2014 - Emerging Pattern of Wealth Confiscation – Russia Confiscates Private Retirement Savings Businessweek reports that earlier this month, the Russian government seized its citizens’ pension contributions – 6% of Russians’ salaries is invested in financial markets, earmarked for their retirement, but this year that $8 billion in contributions will finance Russian spending instead .. “Russia is not the first country to confiscate pension assets to pay its bills, and it probably won’t be the last .. For governments facing financial pressure, billions of dollars of pension assets proved too tempting to resist.” .. Argentina recently “nationalized” $30 billion of pension assets & Hungary, Poland, Portugal, & Bulgaria have done the same ..

LINK HERE to the article

“In most countries, it’s extremely unlikely that the government will outright seize pensions. In America, it’s nearly impossible to change Social Security or Medicare benefits, and the idea of the U.S. government confiscating everyone’s 401(k) is unimaginable to all but the most ardent conspiracy theorists.

However, it’s not unrealistic to think that the American government could take a bigger bite out of individuals’ 401(k) assets with higher tax rates: Income taxes are at historic lows, and if the American government needs to raise revenue in the future, taxes on 401(k) withdrawals may be higher (along with taxes on everything else).

08/25/2014 - Emerging Pattern of Wealth Confiscation – Is Portugal Next?

Casey Research’s Nick Giambruno sees an emerging pattern of wealth confiscation globally, identifies Portugal as a likely next country candidate in this regard .. “It starts out with government officials telling you everything is all right—when clearly everything is not all right.” .. here is a summary of the pattern:

1. COUNTRY GETS INTO SERIOUS FINANCIAL TROUBLE

2. OFFICIAL GOVERNMENT DENIALS

3. SURPRISE BANK HOLIDAY/CAPITAL CONTROLS

4. CONFISCATION

Portugal is clearly at the first stage in the pattern—serious financial trouble .. recommends taking your money out of Portuguese banks while you can .. “When it comes to protecting yourself from confiscations, capital controls, bank holidays, and other desperate measures of an out-of-control government, it’s absolutely essential to take action before it’s too late .. While the window is still open for those in the U.S. to protect themselves, the warning signs are clearly there. And the writing is on the wall.” .. another example of financial repression.

08/24/2014 - A New Confiscation To Worry About? “‘Since the financial crisis, the world’s central banks have collectively put more than $10 trillion into the financial system. This kind of money printing is literally unheard of in modern history. And it has set the stage for a roaring wave of inflation.’ — Graham Summers, analyst .. With the world in a deflationary recession, I now doubt we’ll see new highs in the D-J Averages. But with enough QE, it might be possible .. With deflation enveloping the world, investors have been racing to buy Treasury bonds, whose yields have sunk to record lows. My survival choice in investments continues to be silver and gold .. Today it finally happened: I received an advertisement from a firm featuring a scare I’ve been waiting for. There are two ways for the government to handle its outrageous debts. The first is reneging, as per Argentina, but this is unthinkable. The second way is via inflation — inflate enough and your debts appear to shrink. Ah, but there’s a third way, and it’s confiscation of wealth. Don’t think this is impossible, because governments will do whatever they have to to remain in power. How about confiscating all individual wealth above $200,000, for which the government will give you stubs which will say IOU. This will be a switch on the 1933 confiscation of gold. This time it may be confiscation of cash. Finally, something new to worry about.” .. it’s default or financial repression, take your pick.

– Richard Russell*

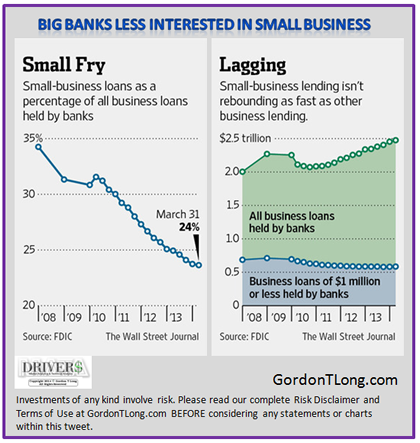

08/21/2014 - FINANCIAL REPRESSION INCENTS BANKS INTO..

NOT THE RETAILING OPERATIONS OF MAKING (EXPENSIVE) SMALL BUSINESS LOANS!

Small Business has historically been the life blood of America.

It no longer is for a consolidated banking industry.

THE BANKING INDUSTRY

IS NO LONGER EFFECTIVELY

SERVING AMERICA!

08/20/2014 - PRIOR TO FINANCIAL REPRESSION IN AMERICA

Government Policy was about:

“positively incenting & directing actions”

Government Policy is now about:

“negatively forcing & impeading actions”

READ: Treasury Officials Prepare Options to Address Inversions 08-19-14 WSJ

Treasury Department officials are assembling a list of administrative options for Secretary Jacob Lew to consider for ways to deter or prevent U.S. companies from reorganizing overseas primarily to avoid paying federal taxes

Some Democrats in Congress believe lawmakers should pass a stopgap measure to deter companies from pursuing the deals, while some Republicans have said the only way to stop inversions is through an overhaul of the tax code.

others believe the White House has ample flexibility to step in and have raised different ideas for administrative actions, including

FINANCIAL REPRESSION IS ABOUTREGULATIONS

FORCING BEHAVIOUR

versus

REWARDING BEHAVIOUR

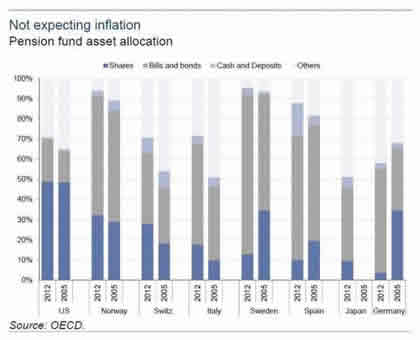

08/19/2014 - BEFORE Financial Repression BONDS were “for Widows, Orphans and Pensioners” For those who couldn’t and SHOULDN’T take risk

Now the government is forcing Public Pensions into Stocks

Some 50% of all US pension fund assets are invested in stocks and only 20% in Treasurys

UNDERSTAND

“SHORTING” & “PUT DERIVATIVES”

to know how

THE GREATEST WEALTH TRANSFER IN HISTORY

IS BEING SET-UP TO EVENTUALLY BE EXECUTED

08/18/2014 - “When a Government Doesn’t Own its Own Currency this Eventually Happens”

Its Called FINANCIAL REPRESSION

When an Unelected, Private Institution (The Federal Reserve), Owned by the Banks, Controls the Money Supply & Interest Rates this occurs

“Permit me to issue the money of a nation, and I care not who makes it laws”

Mayer Amschel Rothchild, Banker 1790

08/18/2014 - Indebted Governments Will Resort To Capital Controls

Daily Reckoning commentary on how indebted, western-world governments will likely begin instituting draconian controls & regulations on restricting the movement of money, all with the goal of keeping itself alive & not going into default on its debt while at the same time maintaining a relatively strong currency

Daily Reckoning commentary on how indebted, western-world governments will likely begin instituting draconian controls & regulations on restricting the movement of money, all with the goal of keeping itself alive & not going into default on its debt while at the same time maintaining a relatively strong currency

.. “The U.S. government, along with other Western countries and innumerable banking institutions, is starting to make it very difficult for regular citizens — you, me and the nice lady next door — to move money

.. In essence, capital controls enable governments to limit the flow of money coming in and out of their country in the hopes of manufacturing conditions that protect the value of their currency. As we reach a fiscal tipping point, we could very well see our government revert to making use of capital controls.”

.. it’s another example of financial repression.

READ: 4 Ways the Government Is Set to Take Your Money

08/17/2014 - ECB TAKES ON INCREASED POWERS THE “SUPERVISION FRAMEWORK”

CENTRAL PLANNING & CONTROL

A EURO BOND IS COMING

&

THE UNIVERSAL TAXATION TO SUPPORT

ITS DEBT

Bloomberg Brief Reports:

“A new supervision framework is required to revive the euro area’s single financial market with the assurance that it will yield more benefits than costs. So far, balkanization of banking rules among assorted national supervisors has been a barrier for cross-border lending. This will be lifted with the ECB taking the role of a new single supervisor on Nov. 4.

As Draghi pointed out, “There will no longer be a distinction between home and host supervisors for cross-border banks. Instead, there will be a single supervisory model and eventually a single supervisory culture, rather than one per country.”

As a result, banks could see a reduction in compliance costs and an increase in opportunities for economies of scale, even if taxes will still differ according to member states’ fiscal policies. For the longer term, the authority given to the single supervisor may also improve the monitoring of systemically relevant banks, helping to curb sector excesses and risk.

The transfer of power to a single European bank supervisor should be a game changer.

The transfer of power to a single European bank supervisor should be a game changer.

The ECB is hoping to do more than simply strengthen financial stability. It also envisions unified authority as a tool to repair the broken channels of monetary policy transmission, prompting banks to make their comeback at the periphery and improve credit conditions there. The central bank timidly expressed this wish in its latest financial integration report, stating that “the banking union is expected to contribute indirectly to the return of cross border credit flows.”

When Dead Beat Peripherals Can no Longer Pay there is only one solution.

Tax The Entire Union

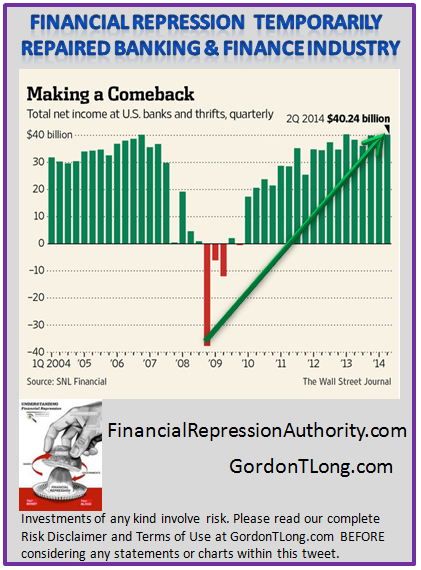

08/16/2014 - FINANCIAL REPRESSION SAVED THE BANKS

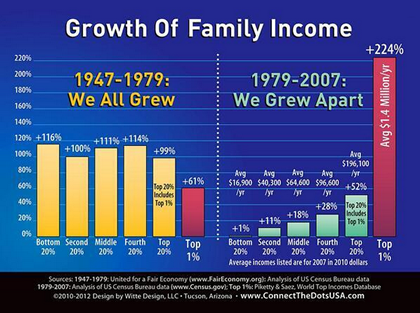

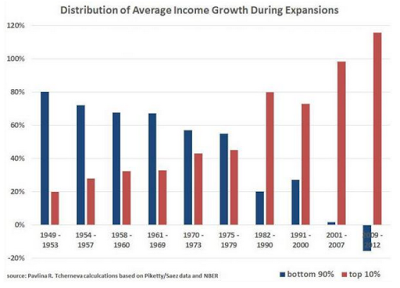

BUT DESTROYED THE US MIDDLE CLASS

FINANCIAL REPRESSION

Accelerated the Decline of America

AMERICA Now A Two Class Society

“Haves & Have Nots”

& Maybe More Concerning

A Culture of

“SOCIAL DEPENDENCY”

08/11/2014 - Federal Reserve & Congress Talk “ENHANCED PRUDENTIAL STANDARDS”

CENTRAL PLANNING & CONTROL

Moving towards Control of YOUR Pensions

through Control of Insurance Industry

Other non-banks to face ‘designation’ as “systemic risks to the financial system”

The Fed has insisted that the Dodd-Frank financial reform bill forced it to apply bank capital standards to non-banks. In response, the Senate recently passed a bill that would give the Fed the room to apply capital standards that are tailored for the insurance industry

Life insurer MetLife is waiting to see if it will be designated this year, while its smaller rival

Prudential Financial was deemed a systemic risk last September.

LARGEST ASSET MANAGERS: On July 31, FSOC decided for now to lift the threat of systemic risk designations for the largest asset managers, but said it would focus on the industry’s products and activities.

PRIVATE EQUITY & HEDGE FUNDS: The review of asset managers came after an FSOC-commissioned report on the industry, which also said it was reviewing private equity and hedge funds, prompting predictions that those sectors could be next on the council’s agenda.

Fed gives preview of future non-bank scrutiny 08-11-14 FT

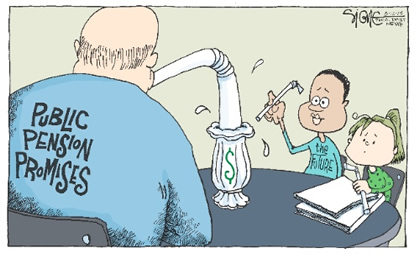

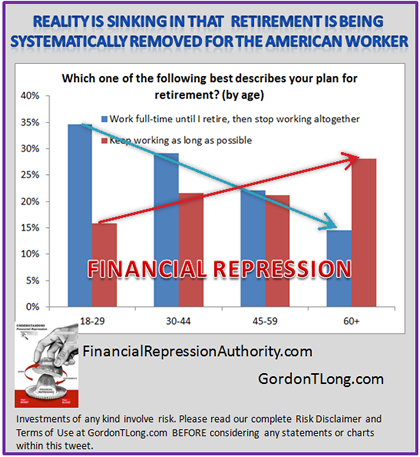

08/10/2014 - DON’T EXPECT SOCIAL SECURITY TO BE THERE TO SAVE YOU!

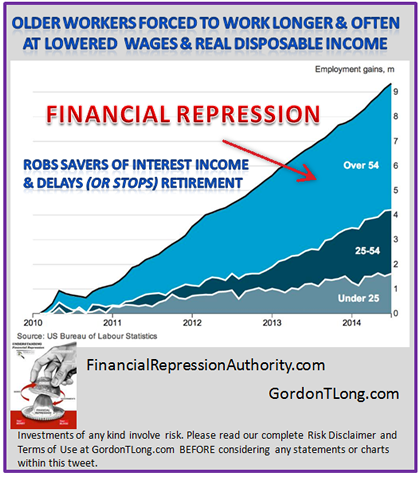

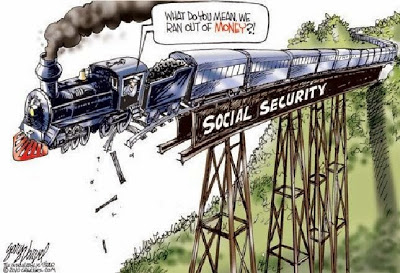

THERE ARE

$84T OF UNFUNDED RETIREMENT ENTITLEMENTS

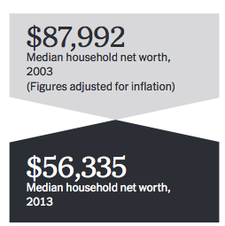

US is Bankrupt: $89.5 Trillion in US Liabilities vs. $82 Trillion in Household Net Worth & The Gap is Growing. We Now Await the Nature of the Cramdown 08-04-14 Chris Hamilton via Charles Biderman TrimTabs’ blog, via ZH

America’s Hidden Credit Card Bill Laurence Kotlikoff: The Government Should Report Its ‘Fiscal Gap,’ Not Just Official Debts LAURENCE J. KOTLIKOFF

The Financial Repression Authority (FRA) educates investors, funds and retirees on the adverse risks resulting from good-intentioned macroprudential central bank policies, government fiscal policies and financial regulations focused on controlling excessive government debt, attempting to stimulate economic growth, and minimizing the potential for financial and economic crises. FRA provides consulting services, lead generation services and retirement solutions.

(*: indicates required .. Click on "Contact Us" once and your email will be sent to us. We will reply to you ASAP.)

Terms of Use and Disclaimer © 2015-2023 - Financial Repression Authority

{kind=link}

{kind=link}