12/19/2015 - Obama Abruptly Waives 1980 Foreign Investment in Real Property Tax Act (FIRPTA)

12/19/2015 - Obama Abruptly Waives 1980 Foreign Investment in Real Property Tax Act (FIRPTA)

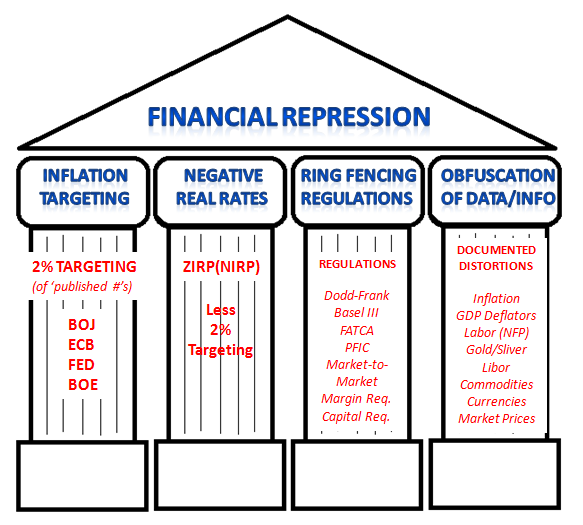

The Financial Repression Authority has consistently shown that Regulatory changes which “Ring Fence” US investors choices is a cornerstone of the Macro-Prudential Policy of “Financial Repression”. Through stealth programs like FATCA and PFIC the US government has steadily and quietly limited Americans ability to take cash out of the country and to invest abroad, other than through profitable public exchange traded products sold by the financial industry. However, it is one thing to shut the doors to American investing abroad but it is quite another to fully open the doors to foreigners! It begs the question why, why now and why the change needed to happen so urgently?

This week, as the BOJ, ECB and PBOC all continued to aggressively expand credit the Federal Reserve was “full ahead” in the process of withdrawing approximately $1 Trillion of liquidity to achieve its December FOMC decision to increase the Fed Funds rate by 0.25%. To counteract this policy initiative and the alarming collapse in the HY & IG bond market, the US government immediately opened the floodgates to easy foreign credit in a major policy reversal. A policy decision which was rushed through congress with almost no time for congressional debate. Obviously what was not lost on the White House was the fact that the now troubled $2.2 Trillion of High Yield bonds peddled to yield starved investors since the financial crisis matches 2/3’s of the $3.5 Trillion increase in the Federal Reserves balance sheet during the same period.

FIRPTA was implemented during a better era for Americans in response to international investors in the late 1980s and early 1990s buying U.S. farmland, as well as the more publicly visible buying of trophy U.S. property by the Japanese. The US government has now expediently waived FIRPTA.

President Barack Obama signed into law a measure easing a 35-year-old tax on foreign investment in U.S. real estate, potentially opening the door to greater purchases by overseas investors, a major source of capital since the financial crisis.

Contained in the $1.1 trillion spending measure that was passed to avoid a government shutdown is a provision that treats foreign pension funds the same as their U.S. counterparts for real estate investments. The provision waives the tax imposed on such investors under the 1980 Foreign Investment in Real Property Tax Act, known as FIRPTA.

“FIRPTA has historically made direct investment in U.S. property a non-starter for trillions of dollars worth of foreign pensions,” said James Corl, a managing director at private equity firm Siguler Guff & Co. “This tax-law modification is a game changer” that could result in hundreds of billions of new capital flows into U.S. real estate.

Foreign investors have flocked to U.S. real estate since the global economic meltdown, drawn by the relative yields and perceived safety of assets from office towers and shopping centers to apartments and warehouses. The demand has helped drive commercial real estate prices to record highs. Many foreign investors structured their purchases to make themselves minority investors and bypass FIRPTA.

REIT Purchases

The new law also allows foreign pensions to buy as much as 10 percent of a U.S. publicly traded real estate investment trust without triggering FIRPTA liability, up from 5 percent previously.

“By breaking down outdated tax barriers to inbound investment, the FIRPTA relief will help mobilize private capital for real estate and infrastructure projects,” Jeffrey DeBoer, president and chief executive officer of the Real Estate Roundtable, an industry lobbying group, said in a statement.

Cross-border investment in U.S. real estate has totaled about $78.4 billion this year, or 16 percent of the total $483 billion investment in U.S. property, according to Real Capital Analytics Inc. Pension funds accounted for about $7.5 billion, or almost 10 percent, of the foreign total, according to the New York-based property research firm.

“Foreign pensions are such a low percentage of foreign investment in U.S. real estate because of FIRPTA,” Corl said.

Investment Surges

Foreign investment has surged from just $4.7 billion in 2009, according to Real Capital. Foreign buying this year as a percentage of total investment in U.S. real estate is about double the 8.1 percent average in the 10 years through 2012.

Despite a perception that FIRPTA was a response to the wave of Japanese buying of trophy U.S. property in the late 1980s and early 1990s, including Rockefeller Center and Pebble Beach, the act was actually passed in 1980 in response to international investors buying U.S. farmland. Under old rules, foreign majority sellers had to pay 10 percent of gross proceeds from the sale of U.S. real estate as well as additional federal, state and local levies that could increase the total tax burden to as much as 60 percent, according to the National Association of Real Estate Investment Trusts.

The change “is a huge deal,” said Jim Fetgatter, chief executive of the Association of Foreign Investors in Real Estate. “There’s no question” it will increase the amount of foreign investment in U.S. property, he said.

WARNING

The FRA predicts that Americans will face significant increases in US property taxes over the next five years starting in 2016. With the change in FIRPTA Americans should additionally expect property values to increase in 2016-2017.

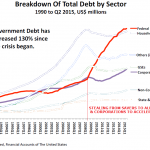

Clearly, foreigners, the “1%” and property owners will all gain from this, but most Americans will simply face significantly increasing property taxes on elevated asset values to fund the ever increasing government debt burden.

Americans owning a house can be expected to initially focus on their net worth being higher, and not that they once again will have even less disposable income. Some will learn painfully why the number one killer of small business is cash flow, not profits..

Gordon T Long

Co-Founder,

The Financial Repression Authority