05/22/2017 - Russell Napier Fears The Dark Ages Of Government Allocating Resources And Capital To Run The Financial System

“The central banks try to manipulate markets to deliver growth, that’s effectively what they do by manipulating the price of money. If it doesn’t work, then what? Well, it’s pretty straightforward. Well, people the demand the politicians do something, people demand political action. But political action for those people who invest in financial markets means in some way reducing the par of financial markets, reducing the par of price. And yeah, I’ve speak to a lot of people about this. People fear inflation, they fear deflation. I fear something much bigger than that, that the political reaction to this is effectively to go through one of those periods again, what we’ll called ‘dark ages’, where we basically- the politicians can make it and then they run the financial system, or they begin to get directly involved with the allocation of resources and capital and credit and we go back into that, let’s call it the 1950s, 1960s, certainly a in a European context, that type of world is a world that the population demands because they look at central banks and say ‘well you haven’t been able to do this using so-called market forces, so let us use non-market forces.’So, we’re really dealing with something very existential, here, that this will be a shock to the face and the ability of the market to deliver, not only in the ability of central bankers, but in the ability of the market to deliver in a decided move towards intervention in markets.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/19/2017 - The Roundtable Insight: Peter Boockvar and Alasdair Macleod On The Risks Of Central Bank Policies To The Financial Markets

FRA is joined by Alasdair Macleod and Peter Boockvar in a discussion of geopolitics, central bank monetary trends, and their impact on the global economy and markets.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

Prior to joining The Lindsey Group, Peter spent a brief time at Omega Advisors, a New York based hedge fund, as a macro analyst and portfolio manager. Before this, he was an employee and partner at Miller Tabak + Co for 18 years where he was recently the equity strategist and a portfolio manager with Miller Tabak Advisors. He joined Donaldson, Lufkin and Jenrette in 1992 in their corporate bond research department as a junior analyst. He is also president of OCLI, LLC and OCLI2, LLC, farmland real estate investment funds. He is a CNBC contributor and appears regularly on their network. Peter graduated Magna Cum Laude with a B.B.A. in Finance from George Washington University. Check out Peter’s new newsletter service at www.boockreport.com.

THE TRUMP FACTOR

Up until recently, the market was laser focused on tax reform, health reform, and policies. But Trump’s behavior in his tweets crossed a line that the market couldn’t ignore it any longer. The market knows that he needs all the credibility and stature in order to get the tax reform that the market has been anticipating. The market has been solely focused on tax reform and not paying attention to central banks pulling back and the issues with the US economy and mediocre growth. It’s all been chips on the table of ‘Trump’s going to make things great with tax reform and I don’t care about anything else’, and this is a gigantic wake-up call that the belief that everything is going to go smoothly was incredibly naïve.

This is much more than a one-day event. Now you have a dark cloud over the Trump agenda. You take that away at the same time the Fed is raising interest rates, the US economy is mediocre at best, and the yield curve keeps flattening? There’s no room for error in terms of valuations, and it’s that kind of cocktail that gives us a sell-off like we’re having today.

Trump’s problem is that there’s a turf war raging in the White House. On one side you’ve got established security and on the other you’ve got Trump and his men. The central point about this is that you’ve got the McCain type faction hell bent on continuing to wage a cold war against Russia and China, and you’ve got Trump coming in as a peacenik. He’s turned into someone who’s started quite a few actions around the world. What’s interesting is that President Shi came over, and the result now is that there’s a dialogue between him and Trump. Trump wants to do the same with Putin, but he’s being prevented because there’s so many leaks accusing him of leaking things to Russia, or appointing someone who’s said the wrong things to Russia, etc. The unfortunate thing about it is that it’s moved away from that into the public domain, and now it’s become an issue and they’re talking about impeachment. The fallout from the turf war is starting to destabilize things, and it’s likely that Trump has lines of communication with Shi and Putin, which in the final analysis is going to be very good for all of us. Continuing with the cold war is fundamentally a mistake.

THE EFFECTS ON INTEREST RATE POLICIES

Rate hike odds have gone down, but at the end of the day the Fed is still going to focus on the numbers that they see, and in their eyes they’ve reached their ‘mandates’ in terms of employment and inflation and they’re going to raise interest rates. It’s going to be interesting to see how they manage the political landscape verses what they should be doing on the economy because even if Trump gets impeached, Mike Pence will just carry out what Trump did. The Fed should not be focssed on politics and focus more on what policies will come this year and next. Even so, the Fed seems intent on raising a few more times and shrinking their balance sheet.

The possibility of impeachment does throw into the air when tax reform and health care reform is going to be done. The policy people working on tax and health care reform are going to do that regardless of what shows up in the newspaper and on TV. As Trump is losing credibility, everyone has to ask the question of what moral suasion is he going to have on this process to get something passed. If he doesn’t get this passed and it bleeds into next year, that’s going to have economic implications because corporate CEOs and CFOs are going to freeze some decision making on capital spending or anything else. That’s what the market is questioning; they couldn’t care less about whether Trump is president, they’re just worried about what happens to his agenda.

The basic job of the Fed is to try and manage monetary policy in the context of what the economy is actually doing. Having driven interest rates down to zero, there comes a point where the Fed should try and normalize. Unemployment and employment statistics have come back to target, and that means interest rates should be normalized. The problem the Fed has is that there’s so much debt in the US economy that to raise interest rates very much would destabilize the situation. This is why they’re being very cautious about the rate at which they increase interest rates. If they raise the Fed fund’s rate to 2.5%, they could bring on the next credit crisis. The Fed is very much aware of the debt situation and they don’t want to raise rates like they did in 2006/2007. Assuming that people in the Fed have a sort of inkling, that’s as far as they’re willing to go.

NORTH AMERICA’S EFFECT ON EUROPE

They’ve been beating to a different drummer. While we have political challenges with Trump, their political situation has actually gotten cleaned up with the elections in Austria, the Netherlands, and France. Then we have Italy next year, but the political worries that were becoming widespread have calmed down. We’re seeing better economic activity, and at the same time there’s a growing pressure on Mario Draghi to further taper. Europe is enjoying some calm, but it’s going to be the European central bank and Draghi that completely disrupts that sometime this year and certainly into next year.

There is growing antagonism in Europe about the whole of the EU project. The real problem the ECB has is that it has completely mispriced the bond markets. The prices are way overinflated, but under Basel II and Basel III, these debts are risk free as far as the regulators are concerned. They’re not risk free. The problem now is that as things begin to normalize in the EU, what’s going to happen is that substantial losses are going to appear in the bond market. This could be better absorbed in the US banking system, but not the European banking system. The banks are horribly weak: their balance sheets are rubbish, dressed up to look good for regulators. If you dig down, most of those banks are barely solvent and they cannot afford to take the losses on the bond market which accompany an economic recovery. That is going to be the big, big problem.

Moving on, we’ve got the Brexit negations and the general election. There’s little doubt that Theresa May will have a strong mandate to negotiate as she sees fit with the EU. The EU does want to get a settlement done because they’ve got other problems. The potential Brexit offers the UK is absolutely enormous. If interest rates start rising in the US, there is going to be a tendency for the Euro to be weak. Sterling could also recover against the Dollar are people begin to understand that Britain’s position in negotiating Brexit is actually pretty good, and an agreement is going to be achieved.

The only other currency that needs to be considered in this context is the Yen. Japan is beginning to move, joining the Asian Infrastructure Investment Bank for example, which indicates that business in Japan is starting to drive the government in a different direction from the pockets of the US. There’s lots of change going on, but the big danger is raising interest rates in the EU, which is going to be difficult to do without casualties in the banking sector.

The Fed is going to create policies here irrespective of what goes on overseas. They’re not going to run out of things to buy, but you run into restraints where you start to break the market. The Bank of Japan has certainly broken the JGB market, and the more ETFs they’re going to buy the more they break the stock market. You do reach a natural wall, and that’s not even talking about the limits they reached in terms of the inflation they’re creating and the goals that they’ve met. The level of central bank activity for the sole reason of 2% inflation is a scorched earth monetary policy, and now they have to live with the consequence that they can’t reverse themselves. It’s going to be a nightmare to get out; look at the Fed: here we are in the ninth year of the expansion and the balance sheet hasn’t shrunk one Dollar after raising three times.

OVERALL EFFECTS ON GOLD AND LONG END OF BOND MARKET

The Dollar Index has given back the entire Trump trade; it’s gone back to where it was on Election Day. Now you have the yield curve below where it was on Election Day. Half of that is the Fed raising interest rates and people worried about the economic implications, but at the same time we’re seeing a drop in long yields because they were worried about US growth and the Trump reform not happening. The only real outlier here is the stock market, that’s really on a different planet in terms of its perception of the macro economy and what Trump can do.

The reason that the stock market is so overvalued is that no one is valuing anything in the stock market anymore. The vast majority of investors today are just buying ETFs. It sort of insulates them from reality, but at some stage the market will turn and you’re going to get an awful lot of liquidation. You can’t say the stock market is overvalued; it’s just not valued.

China has tried to take a lot of speculation out of the wealth management products because they’ve been frontrunning the Chinese government’s purchases of commodities. Everyone in China knows the government is stockpiling commodities for its plan to industrialize the whole of Asia. She’s easing down her US Treasuries in order to buy commodities. Basically China’s shaken this out and that process is coming to an end. This is an important signal in gold and silver today. This year so far, silver has risen less than gold, likely because of China unwinding these wealth management products. If you put together the thought that this liquidation in the commodity holdings in the wealth management products, plus the weakness in the Dollar, the potential for gold to rise is pretty good. Base metals and precious metals will move up from there, possibly extended to mid-year. The background for gold and other precious metals is looking pretty good.

The Dollar’s been nothing like a safe haven, so people have found a different save haven. The whole thing with geopolitics is that usually it has a very short impact on markets. It still comes down to what affects markets over a longer period time than currencies, commodities, and fixed income: monetary policy and economic growth. That’s what people should focus on the most.

The Dollar will continue to weaken in the short term, because the rallies we’ve seen in both the Euro and Sterling aren’t over yet. Measuring the Dollar against a basket of commodities, you get a different situation: the Dollar is fundamentally weak against the major commodities and raw materials. Energy is interesting because it refuses to weaken, the purchasing power of the Dollar measured in oil will tend to go down.

FINAL THOUGHTS

This is the first year that all five central banks are either raising rates, ending QE, shrinking their balance sheet, or tightening liquidity. The only reason this market is trading is because of central bank policy. The second concern is what Trump is going to be able to pass, assuming he remains in office, because obsession with tax reform and regulatory relief has blinded people to other growing risks. These are the two things people should focus on the most, instead of geopolitics. People have to understand that we have credit cycles, not business cycles. If central banks didn’t exist, we wouldn’t have these cycles at all! We’re getting quite close to the crisis phase in the cycle, and this time around this crisis could even be bigger than the great financial crisis 8-9 years ago.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/19/2017 - Charles Hugh Smith: Central Planning Based On Central-Bank Inflated Debt-Asset Bubbles Works Until It Doesn’t

“A media mini-industry touts Scandinavia’s ‘happiness’ as the result of its high-tax, generous welfare state-capitalism .. The high-tax, generous welfare model is just as dependent on unsustainable credit bubbles as every other version of state-capitalism .. Take away these unsustainable bubbles, and how ‘happy’ will these economies (or their suddenly impoverished residents) be? Central planning based on central-bank inflated debt-asset bubbles works until it doesn’t. The day of reckoning draws ever nearer in every economy that’s created the illusion of solvency with debt/asset bubbles and export-dependent economies.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/19/2017 - Peter Boockvar: All 5 Major Central Banks Are Going To Turn Off Liquidity

“Some have disagreed with me but I’ve remained steadfast that the post election stock market rally was mostly due to hopes for tax reform and regulatory relief (the Trump put I’ve heard from some) and the positive impact that would have on earnings. I’ve also repeated, likely to your annoyance, that the elephant in the market room in 2017 is that this will be the first year that all 5 major central banks will in some fashion turn off some of the liquidity lights at this party. Thus, the lack of tax and regulatory reform or a watered down version and the tightening of monetary policy would be the two main risks to stocks.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/18/2017 - Jeremy Grantham: Could High Stock Prices Be Here To Stay

“In conclusion, there are two important things to carry in your mind: First, the market now and in the

past acts as if it believes the current higher levels of profitability are permanent; and second, a regular

bear market of 15% to 20% can always occur for any one of many reasons. What I am interested in

here is quite different: a more or less permanent move back to, or at least close to, the pre-1997 trends

of profitability, interest rates, and pricing. And for that it seems likely that we will have a longer wait

than any value manager would like (including me).”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/18/2017 - HSBC: Cashless Society Is Coming, It Is Just A Matter Of When

“Pomeroy thinks that a cashless society puts another important weapon in the central banker’s toolbox, one that could take negative interest rates to a new dimension. ‘With the removal of cash, the zero-yielding asset, rates could in theory be cut more negatively without some of the limitations that have previously been in place.'”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/18/2017 - The World’s Central Banks Are Frozen With Fear

“2016 was supposed to be the year that the Federal Reserve ‘normalized’ its policies. As much as two years ago — after years of a near-zero target rate — the Fed was swearing that it would begin to raise rates back to ‘normal’ levels and cut its balance sheet. That never happened .. Looking at the central banks of Australia, the EU, Canada, Japan, China, and the UK, we find no tightening at all. Since 2012, with the exception of the Fed, it’s been nothing but cuts in the target rate. Excluding the Fed, the last time we saw central banks move was when the Australian central bank and the Bank of England lowered their target rates in August 2016. Meanwhile, the European Central Bank and the Bank of Japan continue to sit in negative territory .. The cumulative effect of all of this is to drive home, yet again, that the central banks are simply too frozen with fear about the true state of the economy to take any hawkish action on interest rates .. the world’s central banks are driving home yet again that we’re in a race to the bottom. Yes, the US is in the midst of an inflationary regime, but the ECB, BOJ, and others appear to have no qualms about keeping their own money spigots wide open.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/16/2017 - David Rosenberg: Investing Around The Latest Trump News? Don’t

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/16/2017 - Michael Pento: Central Banks Are Trapped – Central Bank Crisis Ahead (July 2016)

“As arduous as the path to interest rate normalization will be to the Fed, it will be far more chaotic for the BOJ and ECB to even hint at rate hikes .. By waiting until inflation is well entrenched in the mindset of investors and after pushing sovereign bond yields well into negative territory; the ECB and BOJ have unwittingly backed their sovereign debt markets into death traps. Therefore, even suggesting that it is time to gradually pull back from bond purchases will cause a colossal stampede out of Japanese Government Bonds and European Sovereign Debt .. Traders that have habitually been front-running the central banks’ bids will try to dump their holdings of negative yielding debt as bond prices plunge in response to a 2%–and rising—inflation rate. Throw in debt to GDP ratios that have absolutely soared since the Great Recession of 2008 and the result will be complete chaos in bond markets.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/16/2017 - Capital Controls – The New QE?

“Given the rise of inward-looking and panicked politicians around the globe and the monetary policy extremes after the 2008 crisis, a financial repression via blanket capital control regime could be the policy response to the next crisis. In this process, the global financial system would be totally fragmented, while wealth would be transferred from the private sector to the government. Investors could be caught by surprise; liquidity would evaporate in an instance, with devastating effects for asset prices. In this new paradigm shift, capital mobility will become a thing of the past.”

Jason Manolopoulos is the co-founder of Dromeus Capital and author of Greece’s ‘Odious’ Debt

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/16/2017 - The Roundtable Insight: Charles Hugh Smith On How Financial Repression Is Affecting Millennial Generation Values

Charles Hugh Smith is an author, leading global finance blogger, and America’s philosopher we call him. The author of nine books on our economy and society including A Radically Beneficial World: Automation, Technology and Creating Jobs for All, Resistance, Revolution, Liberation: A Model for Positive Change, and The Nearly Free University and the Emerging Economy. His blog, http://www.oftwominds.com has logged over 55 million page views, probably more by now, and is #7 on CNBC’s top finance sites.

Last time we talked about the commercial real estate bubble and we thought today we’d do a special focus on the millennial generation and how financial repression through repressed interest rates and quantitative easing has resulted in asset bubbles that ultimately have affected the millennial generation in terms of their values, how they look at the economy and life and the way they’re conducting themselves in the economy: what they’re facing in terms of the housing market and the job situation.

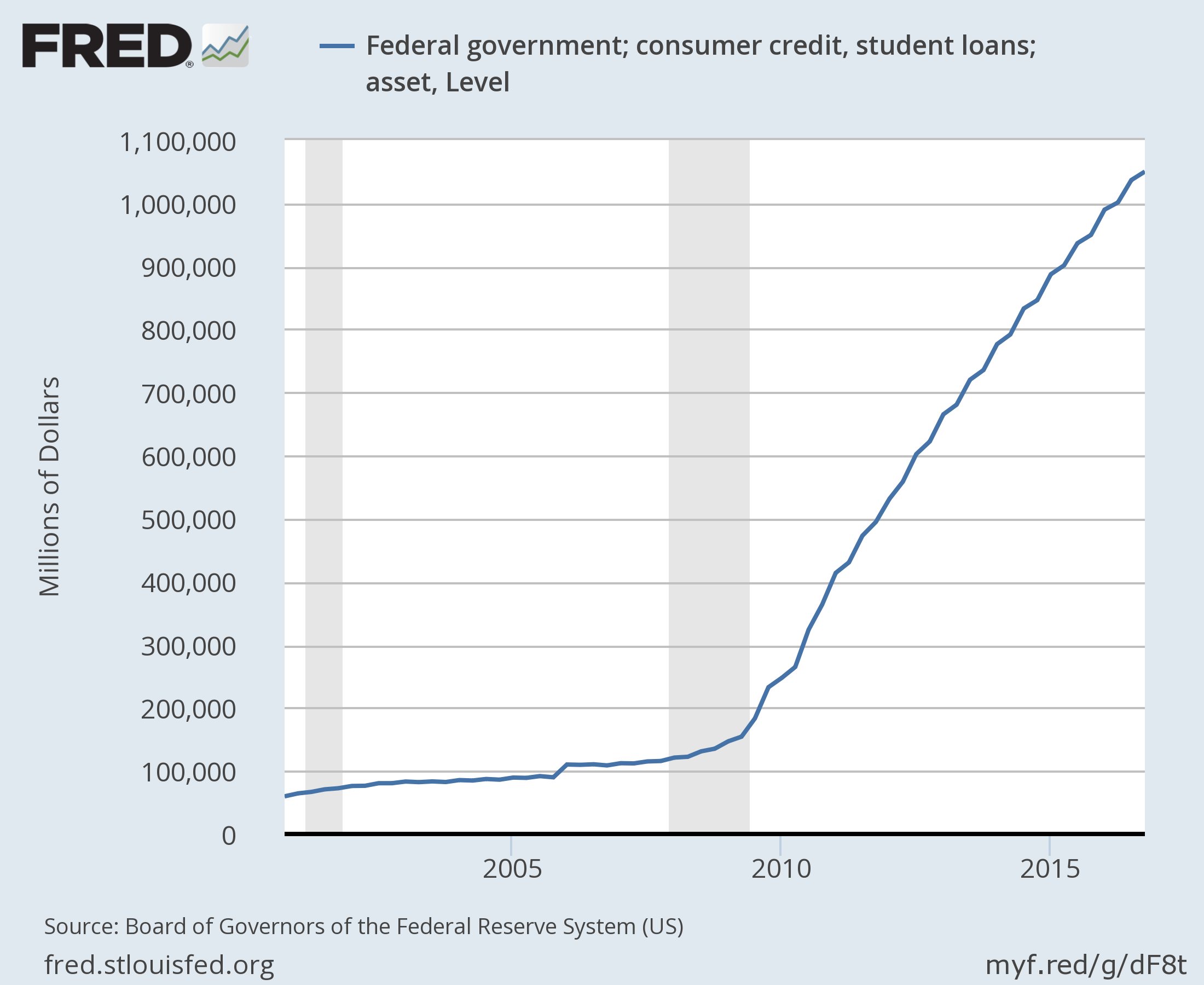

Many millennials are carrying student loan debt, nowadays a small student loan debt is $25,000-$30,000. If someone can escape with a bachelor’s diploma and onlyhave $30,000 in debt, they’re considered to have done quite well. But in reality, that’s a pretty large debt for somebody who doesn’t even have a full-time job yet.

In cases where the central state guarantees any sort of lending and the lender can’t lose money because the government will step in and cover any losses, there’s a huge incentive to lend out to marginal borrowers and to really push every loan you can. And that’s exactly what we have with student loans: anybody that is breathing can get a student loan in an immense amount, and these are non-recourse loans right? Talk about financial repression, you can’t take them to bankruptcy court or reduce them in any way short of a few government programs. The interest rates on student loans are not that low, sometimes they’re as high as 7.5%-8.5%, so millennials have that burden on them right from the start.

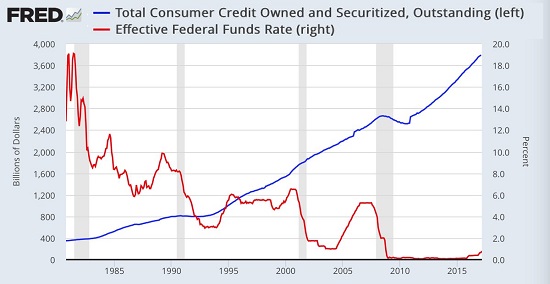

Many of the millennials grew up seeing their parents under a lot of financial stress mostly due to the bubble pop global financial meltdown in 2008-2009. So this has made them very wary of debt. And consumer debt still continues to climb. The total consumer credit owned and securitized chart shows a minor dip in the 2009 time frame, but has since rocketed even higher by another 1.2 trillion.

Marc Faber explores the concept that the millennial generation is much more risk adverse. We can see why, they’ve observed the damage and the stress and the losses that can result from taking on way too much debt and not having enough income or collateral to support it. So, they’re very cautious about taking on gigantic mortgages that their parents did and buying new cars and adding debt on top of debt on top of debt. And so as a generalization, they’re less willing to take the risk of taking on a gigantic mortgage, and I mean by that in the $700,000-$800,000 range, right? That risk aversion, it carries several potential consequences. One that was being discussed in the essay was that there’s less entrepreneurial activity for the same reason: why risk everything on a business that might fail?

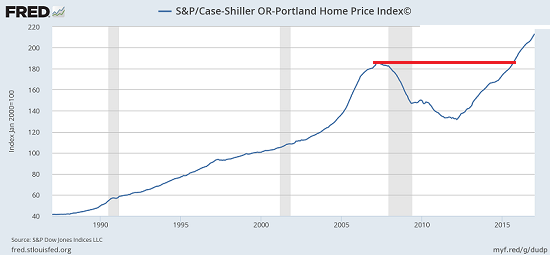

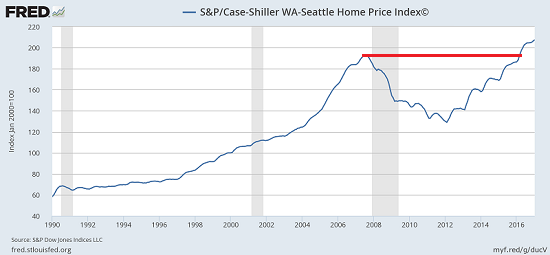

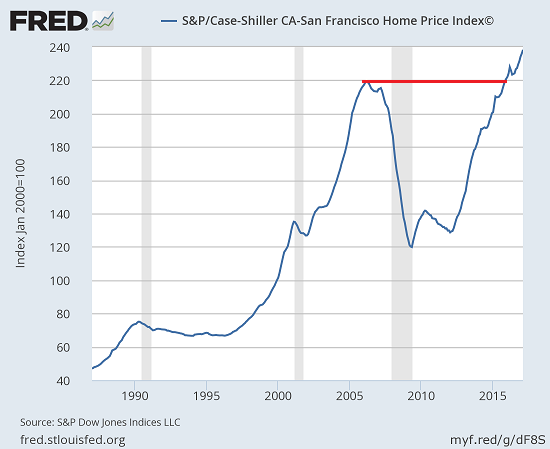

Seattle and Portland top the list of where students would like to move after college, based on various surveys. And according to the Case-Shiller home price index, these two cities now have exceeded the 2007 bubble in terms of housing valuation.

And many other favoured cities that are attractive to millennials like the San Francisco Bay area is also exhibiting this enormous home valuation bubbles or expansions. So then that raises the question, what are the millennials going to do? I don’t think there’s any evidence at this point to presume that the millennials are going to suddenly in some magical point in the future start making a lot more money and be able to afford overvalued housing. There’s no evidence for that, all the trends are the opposite: stagnating incomes and a millennial income trend that will stay sub-par, below that of previous incomes for decades to come.

Joel Kotkin, who studies demographics and the economy, thinks millennials do want to buy and own homes, but they’re only willing to do so if they can afford them. So the opportunities could lie within some of the smaller cities. For example, a house in Columbus Ohio, which is a classic college town in the upper Midwest can sell for less than $50,000.

It will also more difficult for the millennial generation to inherit their parents’ home, because the cost of retirement is so high, and most of their parents are forced to sell their homes instead of just giving it to their children. Housing is becoming increasingly expensive to build due to government fees and regulations on building in most cities, and government programs merely subsidize this process at a cost to the taxpayers; and rent control has been a disaster because that immediately kills off any new construction and reduces the incentive for land owners and landlords to maintain their property because their income is fixed.

Because of this, we’re seeing many innovative alternative housing solutions such as the tiny house movement and retro-fitting dying malls, using them used for housing instead. In addition, there’s an increasing trend of millennials moving towards smaller cities and working at home, telecommuting, and utilizing internet online based businesses. Because of this, local governments that are willing to accept innovations and ease building regulations are the ones who are more likely to prosper.

Richard: Today we have Charles Hugh Smith. He’s an author, leading global finance blogger, and America’s philosopher we call him. The author of nine books on our economy and society including A Radically Beneficial World: Automation, Technology and Creating Jobs for All, Resistance, Revolution, Liberation: A Model for Positive Change, and The Nearly Free University and the Emerging Economy. His blog, http://www.oftwominds.com has logged over 55 million page views, probably more by now, and is #7 on CNBC’s top finance sites. Welcome, Charles.

Charles: Thank you, Richard. That’s an introduction that’s going to be hard to live up to. I’m a beginner here, we’re just exploring interesting topics okay? I don’t have all the answers but we have some interesting topics.

Richard: Great insight as always, and last time we talked about the commercial real estate bubble and we thought today we’d do a special focus on the millennial generation and how financial repression through repressed interest rates and quantitative easing has resulted in asset bubbles that ultimately have affected the millennial generation in terms of their values, how they look at the economy and life and the way they’re conducting themselves in the economy: what they’re facing in terms of the housing market and the job situation.

Charles: Right, and you know Richard it’s hard to know where to start, but I think we could profitably start with the basic context of the economy and the millennial generation. And so in terms of financial repression, perhaps the one key sector that we need to look at is student loan debt because so many millennials are carrying student loan debt, and you know a small student loan debt is like $25,000-$30,000 if someone can escape with a bachelor’s diploma and only have $30,000 in debt they’re considered to have done quite well, but when you think about it that’s a pretty large debt for somebody who doesn’t even have a full-time job yet.

Richard: Yeah, mine was $13,000 I think when I came out, $13,500

Charles: Wow that was very low. And nowadays, 10 times that is not uncommon especially if you go to graduate school. And so we all know why this is but it’s worth touching on because the financial repression part is when the central state, you know the central government and its central bank, when the central state guarantees any sort of lending where a lender can’t lose money because the government will step in and cover any losses. Well, then there’s a huge incentive to lend out to marginal borrowers and to really push every loan you can. And that’s exactly what we have with student loans: anybody that is breathing can get a student loan in an immense amount, and these are non-recourse loans right? Talk about financial repression, you can’t take them to bankruptcy court or reduce them in any way short of a few government programs such as if you join the government service and then you get a reduction and so on. So it’s like the financial system on financial repression steroids. And so they’ve really tasted the worst of neoliberal banking, the interest rates on student loans are not that low, sometimes they’re as high as 7.5%-8.5%, and then the higher level education system, which is supposed to be concerned with educating the youth have just gorged on all this free money, built fabulous buildings on campus. And the administration, I just looked at this statistic, the number of administrators in higher administration in America went up 34 fold in like 30 years where the number of students barely rose, or that was much more modest. So anyways this is like the worst possible combination of financial repression and state guarantees, and so the millennials have that burden on them right from the start.

Richard: Yeah, just trying to get out of the gate in terms of leaving the nest or getting a family formation how can they do that? How can they buy a home or a car, just getting out, right? A lot of them have difficulty even getting a job even given the large amount of debt to begin with.

Charles: Right, right. And you sent me several interesting articles talking about the impact of the last decade’s financial stagnation on the millennial frame of mind or their value system. And of course, a lot of them grew up seeing their parents under a lot of financial stress, during the bubble pop global financial meltdown in 2008-2009. And so this has made them wary of debt and again just for context, consumer debt continues to climb, and this of course is mostly people who are older than their early twenties, it’s hard for them to acquire much more debt than their student loans. I have a chart here from the St. Louis Fed, and it’s the total consumer credit owned and securitized. And it shows a minor dip in the 2009 time frame, and then it’s rocketed even higher, it’s rocketed another 1.2 trillion.

So I think that the millennials are well aware that the entire system, not just the student loans that they’re under, but the entire system is incredibly burdened with debt.

Richard: And so how does this resulting in their views, their values, how they’ve grown up, and what they see as prospects for jobs, and just where to live in general, does it make sense to live in the inner city or out in the suburbs exurbs?

Charles: Right, right. Well one of the essays you sent me was an excerpt from Marc Faber’s recent essay kind of exploring the concept that the millennial generation is much more risk adverse and we can see why, because they’ve seen the damage and the stress and the losses that can result from taking on way too much debt and not having enough income or collateral to support that debt. So, they’re obviously wary of taking on these gigantic mortgages that their parents did and buying new cars and adding debt on top of debt on top of debt. And so I think as a generalization, they’re less willing to take the risk of taking on a gigantic mortgage, and I mean by that in the $700,000-$800,000 range, right? You and I were speaking, a one million dollar house in Toronto or Vancouver or Seattle or the San Francisco bay area or Boston; you know you name it, I mean a million bucks you have to put down a quarter million, and so you’re on the hook for $750,000 that’s a lot of money. And so that risk aversion, it carries several potential consequences. One that was being discussed in the essay was that there’s less entrepreneurial activity for the same reason: why risk everything on a business that might fail?

Richard: Yeah, I mean the millennial generation is the least entrepreneurial.

Charles: Right, and that’s at odds with this sort of tech hub environment in which the assumption is here’s a bunch of 23-year-olds or 25-year-olds starting a billion dollar company in the living room. But that’s actually just the bleeding edge of a generation that’s generally risk adverse. So then we go look at housing, and I submitted a couple of charts that showed two of the millennials favourite cities at least judging by surveys of where you’d like to move after college, Seattle and Portland are quite high on that list. And according to the Case-Shiller home price index, those two cities now have exceeded the 2007 bubble in terms of housing valuation.

And I think that many other favoured cities, cities that are attractive to millennials like Austin Texas and San Francisco Bay area, I mean there’s a lot of other places that are exhibiting the same kind of enormous home valuation bubbles or expansions to the point that only the top earners can afford that, and so then that raises the question, what are the millennials going to do?

And so Joel Kotkin who’s a demographer, you know studies demographics and the economy, his view is millennials do want to buy and own homes, but they’re only willing to do so if they can afford them. And so that basically eliminates most of the super desirable core city centers of Seattle, Portland, Austin, San Francisco and so on, and Boston, Brooklyn, Manhattan you know. And so where do they go to buy a home? And his theory, he proposed that they are willing to move to the suburbs if that’s where it’s affordable. But my question on that is, I don’t think that suburban homes in super desirable urban areas like greater Seattle and around Austin, around the San Francisco Bay area, those houses are not much cheaper than the core houses, so I’m sure that that’s really an opportunity. So I kind of think that the opportunities at least in North America are in smaller cities. In the range of 50,000-100,000, maybe a quarter million residents, not these megalopoleis. And the only millennial I know, well I know a few millennials that have purchased homes, one bought a house in Portland for I think it was around $400,000 or $450,000. And they both work and they had a condo that had purchased a while ago so they had some equity. And then another couple bought a house in Columbus Ohio, which is a classic college town in the Midwest, the upper Midwest for less than $50,000. Now this was not a large house, and it was an old house, and you know it needed some work and all that. But I mean we’re talking about a house for less than 50,000 roughly a tenth of the values of these hot desirable core cities. So that raises some interesting investment questions about where the millennials going to go and where is real estate going to be desirable to them.

Richard: Yeah and it also factors into who are the baby boomers going to sell to, because if there’s nobody there or no demand to buy these houses due to lack of income or insufficient income, that could also pose some challenges to baby boomers looking to sell their house nest egg.

Charles: Right, I think that’s a huge demographic question that I haven’t seen any really good statistics on because of course most of the boomers are still in their late 50s or 60s, early 70s and they’re not yet to the point where the older generation like the boomer parents, the so-called silent generation, which has sold their houses or given them to their offspring, their adult children. But we’re talking about such huge numbers, and just for context, in general roughly two-thirds of the baby boom generation owns homes, about 65%, low 60s. So there’s a large percentage of the boomers who own homes, and typically they bought these homes when they were younger and had families and so there’s going to be a huge incentive for them as they age to unload these houses. And in the good old days when there was more family wealth, they might have been able to afford to basically give that house to their children, and then retire somewhere else on their income. But now, with the cost of retirement so high, and I know because I’m 63 and my mom is in a retirement home so I know if you can get into $4,000 or $5,000 a month on assisted living that’s usually quite reasonable and it can go as high as $7,000 $8,000 $9,000 a month. So almost everybody facing that kind of sum of money is going to have to sell their house in order to liquidate their equity in order to retire on that. So they’re not going to be able just to hand the keys over to their adult children. So that’s a question that I don’t think we know the answer to, but if millennials can’t buy the boomers house at the current value than basic supply and demand economics suggests that prices will have to fall to the point at which they’re affordable to millennials. Which in many areas suggests a 50% drop, right.

Richard: Yeah, yeah exactly. I mean they may be initially thinking perhaps I’ll just get the house through inheritance and therefore I can focus my current income on things like coffee at Starbucks and looking for trips to Machu Picchu or something, you know Patagonia. This is where their values and emphasis seem to be. So they might be saying let me just spend that money there and then I’ll eventually get the house. But the house is now likely going to be needed for retirement by the baby boomers, is what you’re saying.

Charles: Right, and so they won’t be able to inherit. The parents are going to be selling that house in order to extract the equity to retire on or downsize. In which case they’ll be competing with their children for affordable housing, small apartments and that kind of thing. So the other key element here is what can we expect in the future for millennial incomes? And every indication that we have currently, statistically, is that millennials are making considerably less money at the same age compared to the gen X and boomers made in their early to mid-20s and early 30s. And what we do see is a great concentration, a skewing of national income to the top 1% and 5%. I mean this is well established that the top 5% what we might call the techno-crack professional entrepreneurial class, is their income is continuing to grow ahead of inflation and expenses, but everybody else below that, their income is stagnating. I don’t think there’s any evidence at this point to presume that the millennials are going to suddenly in some magical point in the future start making a lot more money and be able to afford overvalued housing. There’s no evidence for that, all the trends are the opposite: stagnating incomes and a millennial income trend that will stay sub-par, below that of previous incomes for decades to come. So I don’t think there’s any magic bullet on that, and if we look at what’s the other magic bullet in financial repression armory, well it’s lowering interest rates to zero. Hey, we’ve been there for 8 years, right. Or near zero, and mortgage rates below 4% were basically unprecedented lows and they’re starting to click back up above 4, 4.5. So we’ve already used up all that ammunition about lowering interest rates to near zero, to push mortgages down to make very overvalued homes affordable, that’s done. In fact, the trend suggests we’re at a bottom there and mortgage rates may continue to click higher and put another sort of pressure on the incomes of millennials.

Richard: Yeah, so the repressed interest rates is sort of affecting a large number of age groups because the inability to get sufficient income off of fixed income assets and investments as baby boomers retire, looking maybe more to go into bonds or fixed income type of investments, with the interest rates being so low, that’s very difficult. And therefore maybe you go to the house and reverse mortgage and all that. But at the same time that’s all secondarily affecting the millennial generation as well so there’s not much discussion in that regard, you know how repressed interest rates have negatively affected the millennial generation.

Charles: That’s right, that’s right. If you’re a borrower, if you’re a saver then of course you’re receiving very little income. And that’s hurt the older generations which have been saving money for their retirement.

But the millennials who are the borrowers of student loans and auto loans and so on, other than the teaser rates that have been offered for auto loans, if you’re paying a student loan or a credit card, I mean the interest rates are sky high still, they’re very high. As we know credit cards are often 15%-16%. And so the millennials aren’t really getting an enormous benefit from this so-called zero rates because much of their debt is not at 1%. Yeah, you can get a 1% auto loan if you qualify, but most of the debt out there is at much high rates.

Richard: Yeah, exactly.

Charles: So, Richard maybe one of the key questions here going forward is, what happens to the United States, and perhaps we can include Canada with at least the high value cities of Toronto and Vancouver where young people that just have regular normal income jobs are priced out of buying a single family homes in those areas. What happens to the society and the economy when people can’t afford to buy a home, that they’re just renters? I mean what impact does that have socially, economically, and politically? I don’t think we’ve really explored that too much. And what Joel Kotkin was arguing against was the idea that oh the millennials will be perfectly happy to be renters their whole lives. And he was suggesting that well maybe that’s just a happy story without any actual basis, maybe they’ll be quite angry that they can’t afford to buy a house.

Richard: Yeah and just the sense of ownership that goes along with that, I mean there’s some other points that go to that regard in that Marc Faber article where he references a number of authors, so that we talked before about the risk aversion that’s infecting even now corporate America in terms of in the old days there was budgets for doing research and development. And now it’s being more money is spent on legal compliance and human resources instead and less on training less on research and development. That’s also related to the fall in entrepreneurial activity, innovation. And then Marc quotes Edward Gibbon in terms of how it ended up like in Athens in Greece in the ancient history where in the end more than they wanted freedom, they wanted security when the Athenians finally wanted not to give to society, but for society to give to them, when the freedom they wished for was freedom from responsibility, then Athens ceased to be free. And so that is a big issue in terms of what could happen resulting from the spirit of risk aversion and a sense of greater entitlement from the government.

Charles: Yes, that’s an excellent point, Richard. And kind of following that up, Joel Kotkin also mentioned that there’s a generational conflict brewing in land use and how we provide housing how we build housing. And as we all know that the last I’d say 20 some years has been dominated by nimbyism, like not in my backyard right. Don’t build any new housing, don’t build any high-density housing, don’t build a new complex by my house, right. And so that has really stifled construction in a lot of cities, especially those with very little open land left. And then, of course, the local governments have raised the fees on building, and so it can cost I think the number that he mentioned was $50,000 per unit just for the development costs, you know the permits and sewer connection, and you know there’s a $10,000 fee for everything right. For each item, and so if it costs 50,000 just to get a permit basically before you’ve even spent a dollar on the land, and then the whole process is dragged down so you spend two years basically paying interest and principal on the land you purchase before you actually get permission to build. All these things have made it so the housing that is built is super unaffordable. And so if we’re going to look at the millennial sort of tendency some people say towards socialism, like well the government is the entity that can fix this, if we look at what the government has done with housing, for instance rent control has been a disaster because that immediately kills off any new construction and reduces the incentive for land owners and landlords to maintain their property because their income is fixed. And the other thing that the government has done in response to this affordable housing crisis is it’s built so-called affordable housing, but the vast majority of cases that is merely subsidizing housing. In other words, it still costs $250,000 to build that tiny apartment per unit. And then the taxpayers subsidize $150,000 of it, making it affordable. But that’s only a subsidy, they didn’t do anything to lower the cost of construction or ownership. And so obviously there’s extreme limits on that kind of thing. And so many cities end up patting themselves on the back for building like 400 units because this subsidy cost is so extreme. And so maybe what the millennials could do, and I don’t know if there’s any potential for this, but if they took a political voice, they might do better than instead that government builds subsidize housing that just adds burden to the taxpayers, maybe they can overturn a lot of these super restrictive codes and nimbyism, you know that’s choking the construction of new affordable housing.

Richard: Yeah I think the regulation issue is big, and it’s also affecting if you look at the positive side of some of what’s happening, like this move towards tiny houses where you have maybe 160-1,000 square feet type, very small houses that can be almost like mobile homes. And then maybe the retro-fitting also of dying malls to have them go into housing, to housing developments to be retro-fitted from malls and just other things like containers that are being retro-fitted into houses as well, all of that. But there’s a lot of regulations in many communities that prohibit that type of thing to happen in terms of putting these tiny houses on property.

Charles: That’s right, there has to be a change in as you say the regulatory spirit of the law, and that’s a political process. But you know, Richard, to speak briefly in an investment potential here, where is there an opportunity here for people that want to participate in this huge demographic economic housing shift we’re talking about. Well, just anecdotally, I can’t give you national statistics, but just from people I talk to, it seems like the opportunity is in these small cities that have some assets. In other words, they have a port, you know they’re on the seacoast or they have a riverfront or they have some state universities, these kinds of assets that tend to be institutional or profoundly economic. Those small cities seem to be where the millennials can afford and where they’re interested in revitalizing. I was speaking with another blogger podcaster, and he was saying Buffalo New York, which was for quite a few years considered a poster child for urban decay upstate New York. And he said it’s actually becoming a happening place because young people are moving there and opening brewpubs because it’s cheap. And so I think the key here is to find places where housing and commercial space to open a restaurant of café or some sort of business, if you can find a place with super cheap rent super cheap housing you can buy for like I said in a neighborhood of $40,000 $50,000 $60,000 $70,000 $80,000 than that’s going to be a magnet for young people for the affordability and as we all know the trend for many decades has been the artist and creative types will go to a rundown neighborhood or town and then they will revitalize it because it’s affordable to them. And so that may be the opportunity going forward, is in smaller cities that have some assets, and by that I mean compared to a place that was dependent on one auto assembly plant, and so when the plant closes the whole place is shut down and there’s no other assets to draw on. But if you have institutions then there’s some foundation there that can support a revitalization and so just people have told me Buffalo New York seems to have some magnet potential and Columbus Ohio is two examples and I’m sure there’s many others, dozens. And so if I were a real estate investor I would start looking at places like that.

Richard: Yeah, no I think you’re right. And that’s also consistent with the trend towards a move to the center, the so called fly over America land between the coasts in the interior in the Midwest where there was places that have been very depressed, Buffalo, maybe Detroit. Very very low cost and the cost base is already beginning from a very low point. But at the same time you’ve got resources, you’ve got land, arable land for agriculture potential. And then the potential for fiscal spending on infrastructure, so you’ve got the Midwest that has the potential there, where it’s traditionally played a role. So that sort of whole manufacturing infrastructure agriculture in the interior of the U.S. that trend. And certainly, people moving out of California for various reasons in high-cost areas, highly taxed areas, going more towards the favourable areas in the interior.

Charles: Yes, absolutely, and you mentioned agriculture and arable land, well I also just, I don’t know them personally but through other millennials I know it turns out there’s quite a few millennials who are homesteady. In other words, they’re buying abandoned farms or they’re buying rural land and starting to raise pigs and chickens. And again, the cost is so much lower, and I want to make a last point here which is this could be a global trend. In other words, it may not be isolated to the U.S. or North America. Because I know, again anecdotally, that there’s evidence of this in Japan. Which is highly urbanized, highly expensive, you know basically housing is not affordable in Kanto plain around Tokyo. That there’s millennials there who are just giving up their full-time job, moving to these abandoned villages, or almost abandoned, there’s only a few old people left, and they’re renting these beautiful old farm homes for like 200 bucks a month including the land around it, starting a garden, and then they’re working part time online. Because a lot of them they’re illustrators or they’re graphic designers, or they’re programmers. And so that’s that other aspect of our economy, what I call the emerging economy or what a lot of people call the fourth industrial revolution, the digital economy for a lot of young people with technical skills, they can work anywhere. So they can actually afford to live in a small town that’s super cheap and just work part time online. So there’s a lot of positive things that the government can’t destroy here with over regulation. And there may be ways to get around the damage of the financial repression. And so anyways, those are the potential positives.

Richard: Yep, exactly ending on a positive note that through some type of regulatory reform process as we discussed earlier together with innovative ideas on housing in terms of tiny houses, container housing, retrofitted malls, with the trend of working at home, telecommuting, internet online based businesses, the whole retail sector, malls dying but everybody setting up businesses that are online through Amazon or Shopify. Maybe that’s the positive trend to allow more affordable housing and opportunities.

Charles: That’s right, that’s a good summary Richard because if it’s not affordable it’s not going to work for the millennials. They’re not interested in overextending themselves on debt. And so it has to be affordable and that’s where the opportunity is for everybody who wants to be part of this, I think is to provide affordable retail space and affordable housing and get in on that as you say with things like tiny homes. And maybe my final comment would be, the local governments, the local city governments, and the county governments who get in on this are going to prosper. The ones who allow tiny homes and make it easy for young people to start businesses, low-cost low fees, they’re going to prosper. And everybody who is in this high regulatory barrier, high cost, high expenses, overregulation, they’re going to die. And we already see that, and I’d say Chicago is probably a good prospect for a city on the way down from just too many expenses and overregulation. So, yeah.

Richard: Well, that’s great insight Charles, and how can our listeners learn more about your work?

Richard: Great, and we’ll do another session on another topic in about a month.

Charles: Yes, looking forward to it.

Richard: Great, thank you very much, Charles.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/15/2017 - Martin Armstrong: The Coming Central Bank Crisis

“I have warned that whenever a government creates a solution to any crisis, that solution becomes the next crisis. This is what I have called the Paradox of Solution.The unfolding of the exit of the central banks from the Quantitative Easing monetary policy will become a much more serious threat to the financial markets than anyone suspects .. The real problem lies with the European Central Bank (ECB) and the Japanese central bank and when they exit their Quantitative Easing programs, their economies are not the reserve currency and lack a solid bid from international capital. The end of QE will lead to a sharp increase in yields on the bond markets, and thus the financing costs for the states will explode far more rapidly today than at any time in past history. It is also possible that other sectors of the financial system, such as the stock markets and the foreign exchange markets in peripheral economies to the USA, will be cast into turmoil experiencing great difficulties without the financial support of the central banks .. The crisis emerges when governments, who are the ones who have been subsidized since 2008, find no bid for their paper. This will really send rates upward at a rapid pace .. The balance sheets of both the Japanese central bank and the ECB are unlikely to follow the Fed just yet. A withdrawal of the ECB’s purchases of securities could produced the most widespread damage in Europe since the Dark Ages.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/12/2017 - The Roundtable Insight – Alasdair Macleod On How The International Coordination Of Monetary Policies Has Increased The Potential Scale Of The Next Credit Crisis

FRA is joined by Alasdair Macleod in a discussion of international monetary policies, particularly China and the Eurozone.

Alasdair Macleod writes for Goldmoney. He has been a celebrated stockbroker and Member of the London Stock Exchange for over four decades. His experience encompasses equity and bond markets, fund management, corporate finance and investment strategy.

INTERNATIONAL COORDINATION OF MONETARY POLICIES

The business cycle that the banks are trying to manage isn’t actually a business cycle, but a cycle of credit created by the banks themselves. Assuming you have an economy working with sound money, under those circumstances there can’t be what we call a business cycle because everything is random. You get creative destruction of businesses which are ill-founded. When they go to the wall, they do so on a random basis. There’s no cyclical behavior. Then the central bank comes in and feels that the economy isn’t performing strongly enough so it encourages the banks to create credit. Suddenly you have extra money going into the economy. Instead of people having to make a choice, they can have both. The creative destruction you see in an economy gets postponed, and accumulates the whole time under the hood. Eventually what happens is that the excess credit in the economy has to come to a halt.

The cycle of credit is what creates what we believe to be a business cycle. Central banks coordinate their stimulation of the economy to stop the economy from overheating. The effect of this is that they all do the same thing at the same time.

EFFECT ON CURRENCIES AND GOLD

It depends on the stimulation an individual central bank gives to its economy. On top of that, you’ve got what people actually do with the currency and the cycle is basically the change in purchasing power of the currencies the whole time. Underneath this you get an accumulation of debt that never gets washed out on this credit cycle. When you raise interest rates to the point where the economy suddenly shudders to a halt, you start lowering interest rates to try and expand the quantity of money in the economy to prevent people from going bankrupt. Generally central banks succeed in that, but the effect of this is to defer the destruction of debt which is completely unproductive. This rolls into the next cycle, and every time it just gets bigger and bigger. Then you look at statistics and you see the amount of debt built up has increased immeasurably, so the next financial crisis will be worse than the last one.

The protection the ordinary person has against fiat currency losing its purchasing power is to hold some money in gold. You want to be able to use this money when paper currencies either lose most or all of its value. In that sense, gold gives the most protection. If you want to insulate yourself from the collapse of the paper currency, then gold is the only thing you can use. Maybe silver, but silver has been demonetized. The only sound money in the market at the moment is physical gold.

You ask yourself, to what level would the Fed fund’s rate have to rise to trigger the next credit crisis, and that level is in the region of 2.5%. The credit cycle is really comprised of stimulation, inflation, and having to destimulate. You destimulate to the point where you collapse things, because there’s no fine line between slowing things down and creating the next crisis. You can’t just slow things down because it’s not enough of a response to kill price inflation; if you raise interest rates a bit, the market thinks the central banks are too afraid and then continue to advance purchases and dispose of money in favor of goods. The only way the central banks can stop this is to raise interest rates to the level where we change our behaviour.

The central banks raise interest rates to the point where the collapse occurs, then they crash interest rates and chuck money into the economy to ensure nobody goes bust. The idea that the central banks think they can manage what they think is a business cycle is just completely bizarre. Governments are effectively stuck in a debt trap as well. What we’ve got to look through is next time, is how much money does the Fed have to write an open cheque for this time, and what will be the effect on the Dollar. The Dollar, after all, is the currency to which other currencies tie themselves, and if the Dollar falls we all fall. This time around it will be considerably worse than last time.

TIMING OF NEXT CRISIS

The whole situation has become quite unstable. In Europe, there’s a movement of money away from the banking system and into principally Germany, Luxenberg, and the Netherlands. These banking systems are, as far as large depositors are concerned, safe relative to the banks in the Mediterranean countries. The flight of capital from these weaker countries has hit record levels. The ECB is sitting on the situation and saying it’s not a problem, but the ECB has the eventual liability for the settlement system which is reflecting these imbalances. The total imbalance is in the region of 1.3T Euros. The important part is that the statistics coming out of the Eurozone indicate that there’s economic recovery going on. If there’s economic recovery going on, why do we have the continuing flight of capital?

Lots of people would say that China is a problem. What it’s now trying to do is deflate a bubble in the domestic market while inflating another bubble as it’s indulging in infrastructure spending. The annual spend on infrastructure is now in the order of $750B equivalent. That’s why you’ve got the demand for commodities coming out of China. But China finds that the wealth funds have been frontrunning her by buying commodities. This credit is getting more difficult for central banks to manage, and whole situation is becoming very unstable.

EFFECT OF USD INTERPOLITICALLY

If you pick up on China’s view as to what America is dong, you get a very different view from what’s reported in mainstream media in the West. The Chinese have worked out that America gains a huge amount from exporting the Dollar for value. They take it one step further and say that when Americans to raise funds, they encourage those Dollars back by destabilizing the region those Dollars have gone to. We’re now in a situation where Trump has been elected, but one of the problems he has is that he can’t raise any money because the debt limit has been reached and it’s not being extended. So how would you extend the debt? The Chinese would say that you destabilize a region where the Dollars are, and those Dollars are going to come flooding back. How do you get Congress on your side? You play the patriotic card and threaten to wage war with North America. No American can actually go against the idea of patriotism, so he got the extension up to October. This also explains why Trump moved from peace-making to warmonger in the space of less than 100 days.

Iran is also likely to be targeted later on this year, when Trump wants to increase the budget deficit after October, because the Middle East is one of the areas where there are lots of Dollars owned.

The Shanghai Cooperation Organization is set up by China and Russia, which started as an intention and security agreement and morphed into an economic unit. The idea is that the whole of Asia would become a free trade area. Between them, they are creating an industrial revolution throughout the most populous continent in the world. We’re talking about 40% of the world’s population suddenly having an industrial revolution that will link the whole continent. This is also impinging on Europe. It takes roughly two weeks to get a container from Beijing to Madrid right now, and it will be cut down. Compared to shipping by sea, which takes three weeks, you can see how the investment in these rail communications is massive. All the capital investment that is going to create this industrial revolution in Asia has to be financed, which is why the Asian infrastructure investment bank was set up by China and Russia jointly. All that infrastructure development has to be financed, and London is the center from which it is going to be financed. As far as the Chinese and Russians are concerned, they don’t want America to be involved at all. New York is completely frozen out of this for the reason that everything they do is reflected in bank balances back in the American banking system; they don’t want American interference or Dollars. London, working with Hong Kong, is how this is going to be financed. The big, big game is no longer Europe, it’s the whole of Asia.

EFFECT ON EXCHANGES IN SHANGHAI

China has been trying to promote the Yuan as an international trade settlement currency. It’s got a long way to go; the Dollar dominates this market. But one way they can promote the Yuan is by ensuring there are efficient financial markets that would allow people to do with the Yuan what they do with the Dollar. One of the things they have done at the outset is to set up a Yuan-gold contract in the futures market in Shanghai, settled in physical gold. We now have another thing that has been postponed: an oil contract in Yuan, that could result in oil priced in gold. America’s response to this is to be seen, but it’s clear that the future major economy in the world is going to be the whole of Asia.

In order to promote the Yuan at the expense of the Dollar, there has got to be some form of a gold conversion for trade purposes. Only when that happens can the Dollar be knocked off its pedestal as the major trade settlement currency.

There will be a point where China offers a gold option on trade settlements. If you want to do it at a gold price it has to be a far higher level, so the Chinese would move toward a higher level. But they don’t want to destabilize the world economically, so they’re reluctant to do it. As things evolve, they’re getting closer toward having to take that decision. To an extent it depends on what America does. China owns an awful lot of US Treasuries, which will have to be written off at some stage. Either America stops them selling, in which case China simply waits for them to mature and doesn’t reinvest their proceeds, or China forces the pace. We’re getting closer to the point where some decision has to be taken.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/12/2017 - IMF Proposes Capital Levy On Bank Accounts In Europe; Also, IMF Encourages Germany To Raise Property Taxes

“The International Monetary Fund (IMF) .. has told Germany it should raise its property tax, cut social welfare contributions and invest more to reduce income inequality .. The IMF argues for higher taxes on property are in fact necessary and that the government should demand higher wages .. Years ago, Italy simply imposed a tax on money in one’s account. This was called a ‘capital levy’. This was a one-time charge as an exceptional measure to restore the sustainability of the debt. The IMF is also suggesting that measure be invoked to help the coming Sovereign Debt Crisis. .. The IMF has already calculated how much the measure would cost every Eurozone citizen:

‘The amount of the tax would have to bring the European sovereign debt back to the pre-crisis level. In order to reduce the debt to the level of 2007 (for example in the euro area countries), a tax of about 10 percent is needed for households with a positive asset.’ .. As you can see, there is NEVER any discussion about reducing taxes or the size of government. The solution is always to raise taxes and to not even look at the old Italian trick of a 10% seizure of all cash in your account.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/10/2017 - Yra Harris And Rick Santelli: Lessons From Japan & Implications Of France’s Vote

“The global markets have been lulled into an eerie calm–think Minsky—as the recent Dutch and French elections have driven the anti-euro populists back underground. I caution that the economic situation still remains a very serious concern as President Draghi continues to build the ECB balance sheet in an effort to bail-out the fiscally weak states of Italy, Spain, Portugal, France and others. Italy is still a major concern as the non-performing loans plague its domestic banks. Add in that Italy has a debt-to-GDP ratio of 136% and it will take the entire EU to backstop the Italian financial system. I WARN ALL READERS THAT THE GLOBAL DEBT SITUATION IS FAR MORE PERILOUS THAN GLOBAL EQUITY MARKETS REFLECT .. The world’s central banks have been busy adding liquidity to the financial system, which provides the backdrop for a Minsky Moment for complacency in the realm of ZIRP creates instability below the surface. We do not fight markets and therefore have not been sellers of equity markets by battling the power of central bank liquidity creation. But as geopolitics calm markets will return to focus on the fragile financial situation created by mountains of debt.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/08/2017 - Martin Armstrong: Central Banks Accelerate Buying Of Equities In Efforts To Implement Their Monetary Policies

Martin Armstrong: “I wrote about that explaining that the central banks have been buying equities since 2014. The Swiss National Bank posted its latest 13-F holdings showing it has been buying equities at a stepped up pace during the first quarter 2017. Their total equity holdings have now reached $80.4 billion, up $17 billion from the $63.4 billion at the end of 2016 .. The central banks are trapped. Lowering interest rates to virtually zero reduced their yield on reserves and they cannot sell off government securities. The only viable hedge is US treasuries in the bond world against the chaos of the Eurozone. That offers no diversification just more government debt. The ECB owns 40% of European government debt. The Swiss are buying US equities as a hedge against the Euro and political unrest. This is not manipulation. They lost a fortune trying to maintain the peg the franc with the Euro. They cannot use pegs, so the only alternative to just buying US Treasuries is private equities .. The central bankers understand what our model is warning about. As confidence continues to decline in governments, the central banks can go bankrupt UNLESS they too diversify out of government bonds .. Granted, nobody wants to talk about this yet in public. This is NOT manipulation.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/08/2017 - Dr. Marc Faber: Are High Home Prices [Driven By Repressed Interest Rates] Turning American Millennials Into The New Serfs?

“They are concerned about political correctness, about having the latest-model iPhone and the number of likes their photos receive and how many followers they have on Facebook. But most of all, they are concerned about extracting as much as possible from the government in the form of subsidies and other kinds of benefits. It is a generation that avoids hard work (such as on the factory floor), and is content to work part-time in bars and restaurants, and to live carefree .. It is also the generation whose major contribution to civilization may be the invention of ‘retirement before working’ .. Needless to say, this concept of retirement before working has been fostered and encouraged by governments, which, with their generous transfer payments, make it more economical for some people not to work .. Therefore, compared to the boomers it is only natural and completely understandable that the millennials’ drive for achievement and thriftiness are inferior to the one that their parents had. But can the relative decline of the financial condition of the millennials be satisfactorily explained by their less entrepreneurial spirit? .. ‘The spirit of risk-aversion is also infecting corporate America. The once lavish budgets companies devoted to research and development are now spent on legal compliance and human resources.”

FRA Commentary: The pillars of financial repression like repressed interest rates has resulted in high asset and real estate prices .. this is shaping the views by millennials in many ways – we will explore these ways with Charles Hugh Smith in an interview discussion this week.

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/07/2017 - Alasdair Macleod: International Coordination of Monetary Policies Has Increased The Potential Scale Of The Next Credit Crisis

“This article gets to the heart of why central banks’ monetary policy will never succeed.The fundamental error is to regard economic cycles as originating in the private sector, when they are the consequence of fluctuations in credit .. Monetary inflation transfers wealth from savers and those on fixed incomes to the banking sector’s favored customers. It has become a major cause of increasing disparities between the wealthy and the poor .. The credit cycle is a repetitive boom-and-bust phenomenon. The bust phase is the market’s way of eliminating unsustainable debt, created through credit expansion. If the bust is not allowed to proceed, trouble accumulates for the next credit cycle .. Today, economic distortions from previous credit cycles have accumulated to the point where only a small rise in interest rates will be enough to trigger the next crisis. Consequently, central banks have very little room for manoeuver for dealing with future price inflation .. International coordination of monetary policies has increased the potential scale of the next credit crisis, and not contained it as the central banks believe .. The unwinding of the massive credit expansion in Greece, Portugal, Italy, Spain and France following the creation of the euro is an additional risk to the global economy .. Central banks should desist from using monetary policy as a management tool for the economy .. An economy that works best is one where sound money permits an increase in purchasing power of that money over time, reflecting the full benefits to consumers of improvements in production and technology. In such an economy, Schumpeter’s process of ‘creative destruction’ takes place on a random basis. Instead, consumers and businesses are corralled into acing herd-like, financed by artificial credit. The creation of the credit cycle forces us all into cyclical behavior that otherwise would not occur.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

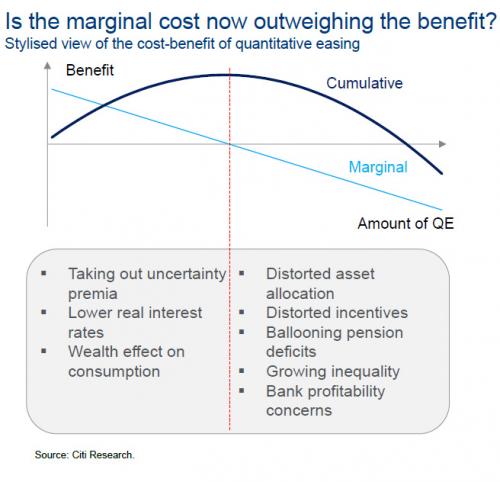

05/07/2017 - Central Banks Injected A Record $1 Trillion In 2017 – “It’s Not Enough”?!

“The latest weekly report by Deutsche’s Credit Strategist Dominic Konstam finds something even more troubling: $1 trillion in central bank liquidity YTD – or roughly $250 billion per month – is not enough .. Konstam’s conclusion is that there are two outcomes: either asset prices drops, or central banks will ultimately be forced to inject even more liquidity .. The bottom line, however, boils down to the following chart first shown by Citi last September, demonstrating that the marginal cost of central bank liquidity injection is now negative…

… and is located in the lower right quadrant, something both markets and policy makers realize.

Which means that when stocks realize just how insufficient the record $1 trillion in central bank liquidity has become, central banks – which have stepped into every single market correction over the past 7 years with some ‘liquidity supernova’ – will, for the first time since the financial crisis – be out of tools… something Janet Yellen appears to have realized some time ago.”

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

05/06/2017 - The Roundtable Insight: Yra Harris On The Bond, Currency, Equity and Commodity Markets

FRA is joined by Yra Harris to discuss the current state of bond, currency, equity, and commodity markets.

Yra Harris is a recognized Trader with over 40 years of experience in all areas of commodity trading, with broad expertise in cash currency markets. He has a proven track record of successful trading through a combination of technical work and fundamental analysis of global trends; historically based analysis on global hot money flows. He is recognized by peers as an authority on foreign currency. In addition to this he has specific measurable achievements as a member of the Board of the Chicago Mercantile Exchange (CME). Yra Harris is a Registered Commodity Trading Advisor, Registered Floor Broker and a Registered Pool Operator. He is a regular guest analysis on Currency & Global Interest Markets on Bloomberg and CNBC.

Yra highly recommends reading The Rotten Heart of Europe – send an email to rottenheartofeurope@gmail.com to order

BOND AND CURRENCY MARKETS