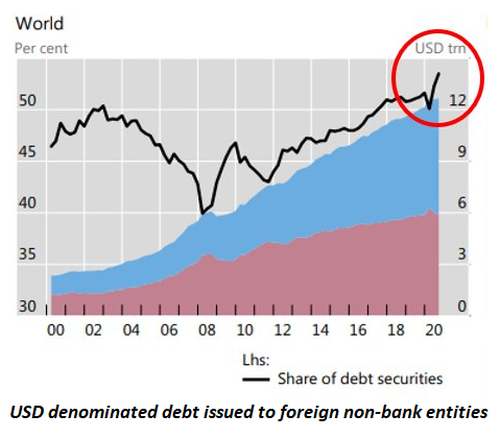

“The strong dollar is not a blessing in these tumultuous financial conditions as it places a great deal of stress on the world’s emerging markets, which are BORROWED in US DOLLARS due to the FOMC’s flooding the global system with very low interest possible loans. Cheap dollar loans become expensive when interest rates rise and the cost of DOLLARS rise along with it. A classic case of this was in January 2015, when Eastern European countries borrowed in Swiss francs because of low Swiss interest rates coupled with a guaranteed level of euro/Swiss franc at 1.20, A NO BRAINER.

But when the Swiss National Bank could no longer hold the PEG the market panicked and the SWISS FRANC rallied in dramatic fashion, leaving borrowers stuck having to repay with expensive Swiss francs. This is the current situation confronting the massive amount of loans held by private and public emerging borrowers with prior cheap dollar loans. This is just the beginning of this important discussion. ”

Link Here to the Blog Post

Disclaimer: The views or opinions expressed in this blog post may or may not be representative of the views or opinions of the Financial Repression Authority.

08/04/2022 - Yra Harris – Dissecting the Fed With Darius Dale

08/04/2022 - Yra Harris – Dissecting the Fed With Darius Dale