03/17/2017 - The Roundtable Insight: Daniel Amerman On How Varying Forms Of Financial Repression Will Need To Be Applied To Address Surging U.S. Social Security And Medicare Benefits

03/17/2017 - The Roundtable Insight: Daniel Amerman On How Varying Forms Of Financial Repression Will Need To Be Applied To Address Surging U.S. Social Security And Medicare BenefitsFRA is joined by Daniel Amerman in a thorough discussion on the future of the US national debt and the impact of the upcoming surge in social security and medicare benefits.

Daniel R. Amerman is a Chartered Financial Analyst, author, and speaker, with BSBA and MBA degrees in Finance, and over 30 years of professional financial experience. As an investment banking vice president in the 1980s he did groundbreaking work in the security originations and asset/liability management areas, including CMO/REMIC originations as part of portfolio restructurings for financial institutions, as well as the creation of synthetic securities for institutional clients. As an independent quantitative analyst in the 1990s and 2000s, he structured mortgage-backed bond financings and provided analytical services for real estate acquisitions by multifamily and commercial real estate owners, investment banks, and tax-exempt issuers.

Mr. Amerman is the creator of a number of DVDs and books on finance, including two books published by McGraw-Hill (and subsidiary): Mortgage Securities, and Collateralized Mortgage Obligations: Unlock The Secrets Of Mortgage Derivatives. He has been a speaker and workshop leader for sponsors including The Institute for International Research, New York University, and many banking groups.

US NATIONAL DEBT AND THE FUTURE OF INTEREST RATES

The easiest way to talk about financial repression is to look back at the classic financial repression period of roughly 1945-1970, when all the developed economies in the west were engaged in financial repression. In this case, financial repression means forcing negative real interest rates, which is how they escaped from very high government debt levels relative to the economy the last time we were in this situation. Many things today are different from that time, and the difference is that when financial repression was occurring the first time, what was happening was that the baby boomers gave us a tremendous number of workers producing real goods and services, which gave the the economy a boost and helped get government debts under control.

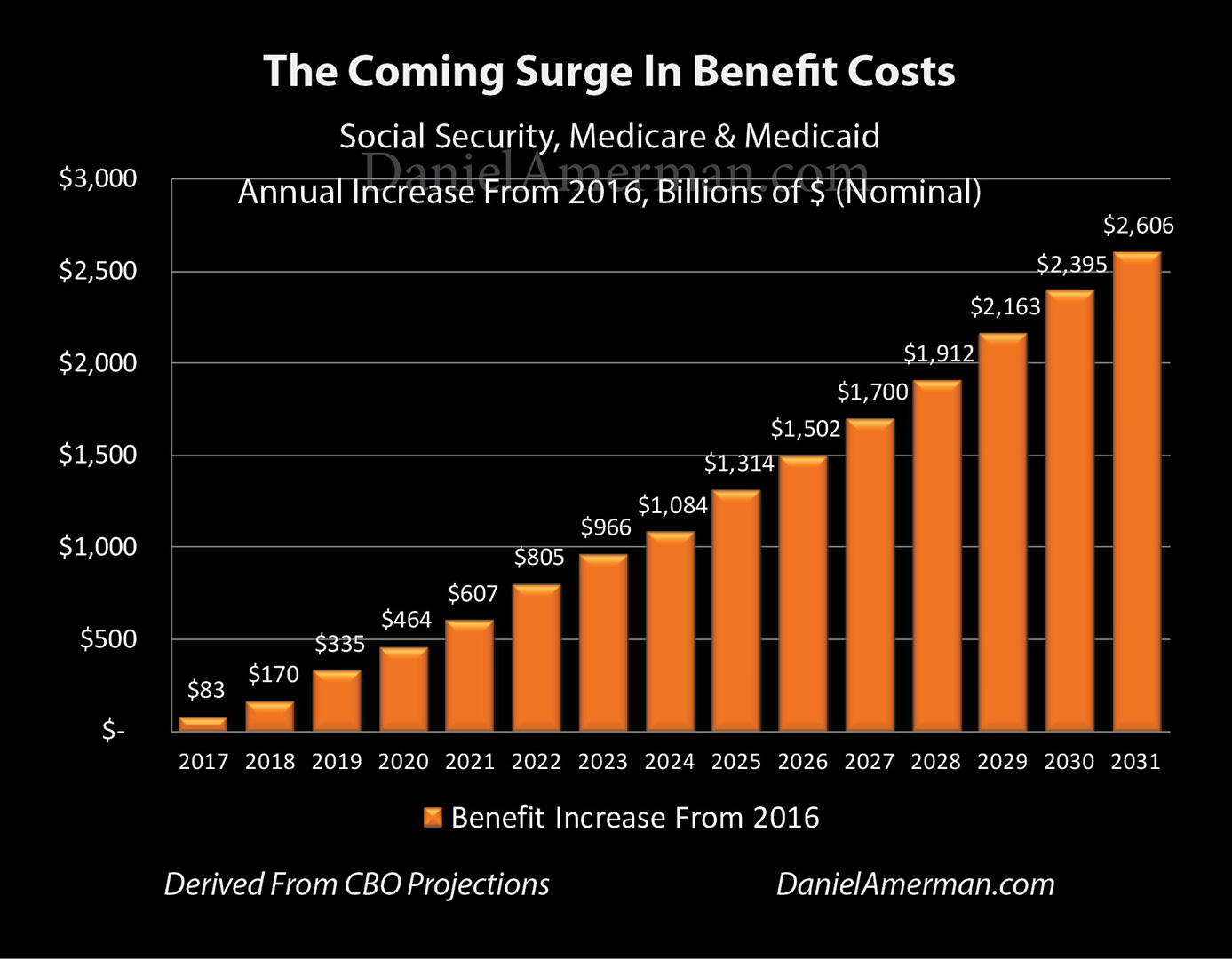

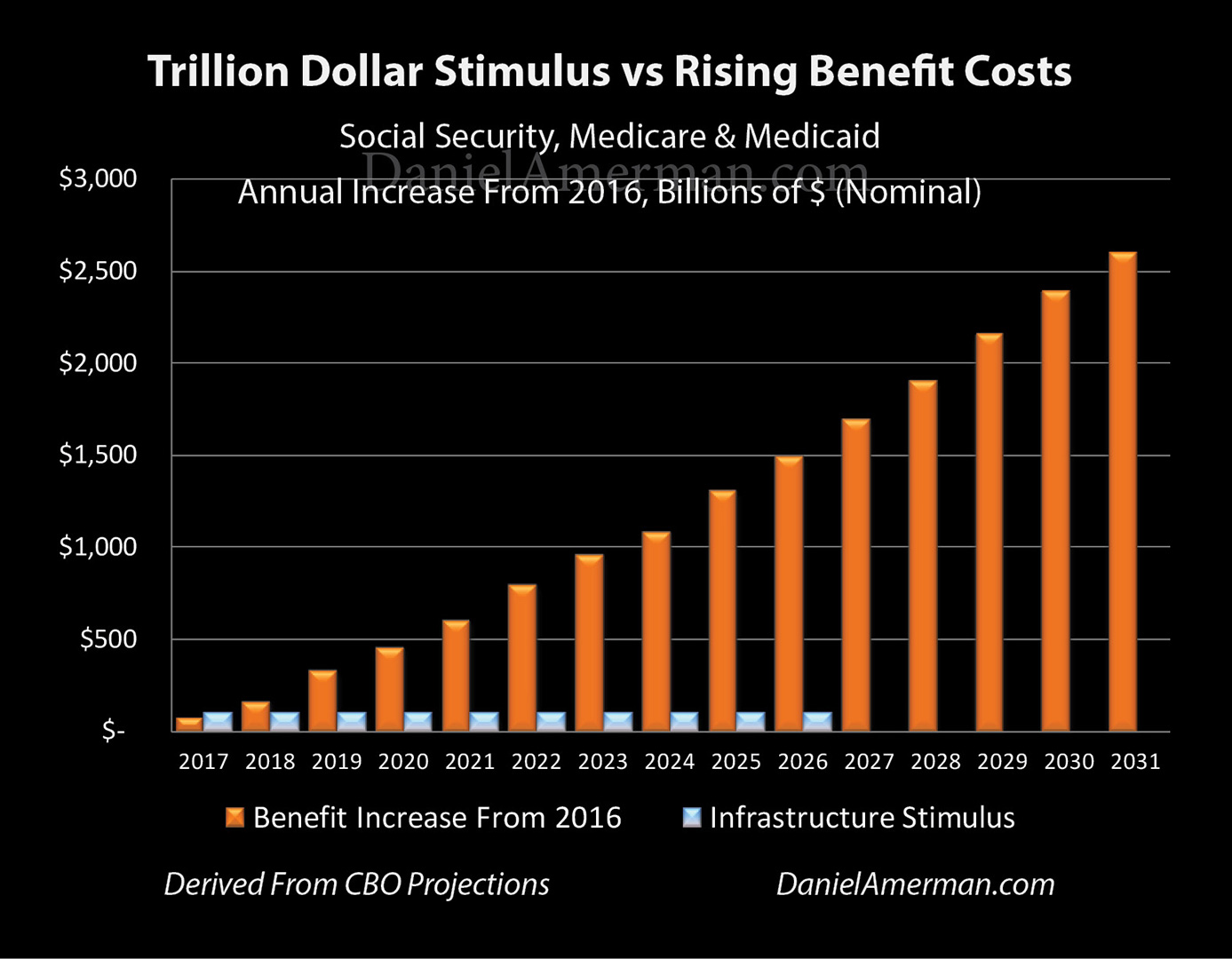

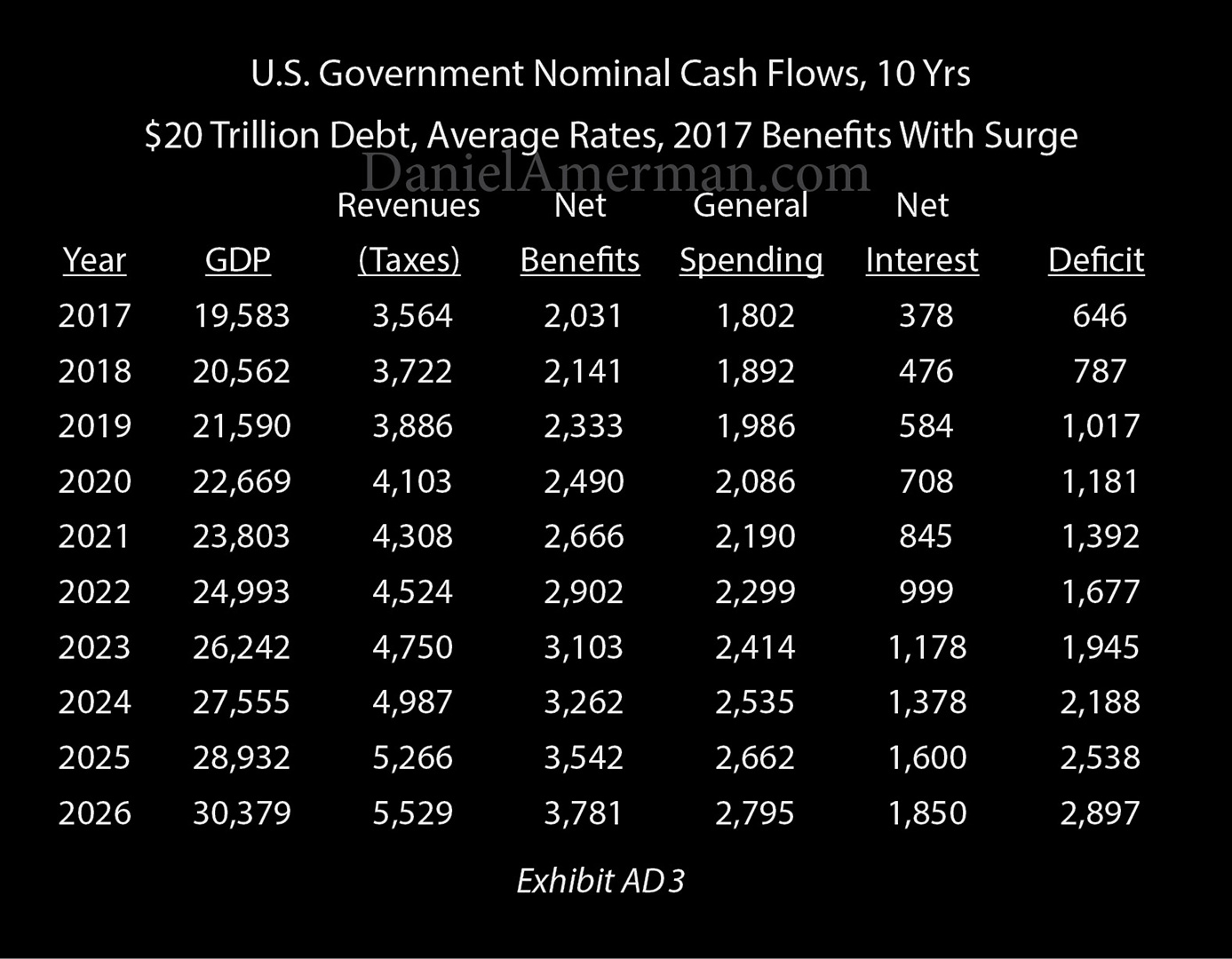

The difference this time is that the boomers are retiring, and the expenses of paying for them are about to get far more expensive. You can see that we have a tremendous increase in projected benefit payouts. You take the entire US government expenditures right now, and just paying out anticipated social security and medicare that so many boomers are going to be collecting, we’re expecting to be adding another trillion dollars per year by 2024. We have this tremendous increase in cost at the same time that we’re starting with a $20T national debt.

There are a number of different ways that social security and medicare costs can be effectively reduced by nicking it in small little ways that reduce overall payments for everybody substantially over the years to come. In the US, social security payments are not tied to the CPI, but a different index that tracks wages that increases at a slower rate than overall consumer prices.

HIGH DEBT, SOCIAL SECURITY & MEDICARE COSTS

The key point is that we can’t really look at financial repression in the post-WW2 example because it’s fundamentally very different. They used financial repression to hold the debt level in inflation-adjusted terms for a 25 year period. We went from the national debt exceeding the total size of the economy to being under 30% of the size of the economy, but they weren’t facing this tremendous challenge we are with benefits costs. Because of that, the impact on investors and anyone who is expecting social security or medicare benefits means things have to work differently this time around.

We know for a fact that in the coming years we’re going to have this force that’s getting more powerful every year that we’re just not used to dealing with. We have twinned unprecedented situations: a $20T debt and much higher social security and medicare costs on the way quickly, and those two are happening at the same time.

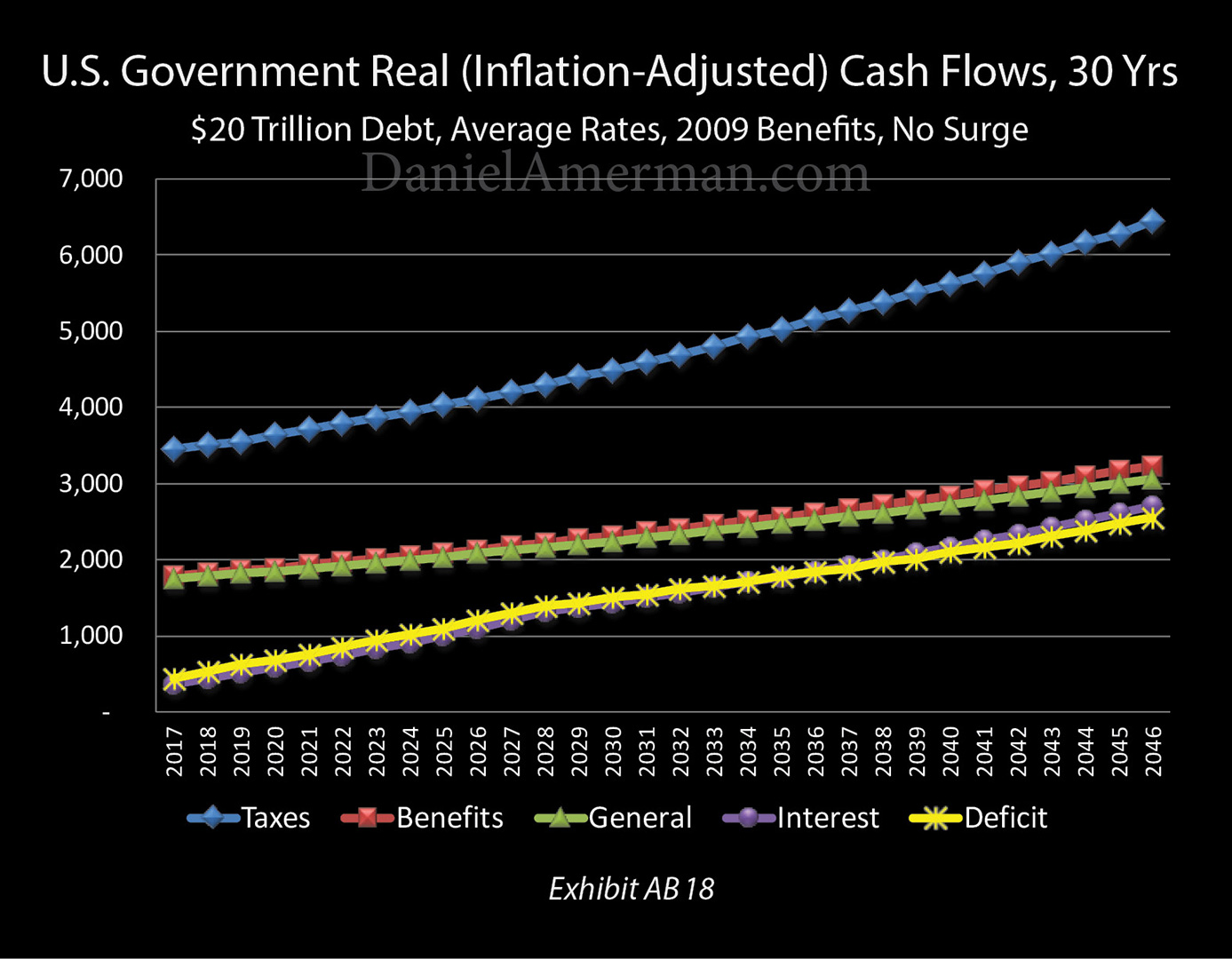

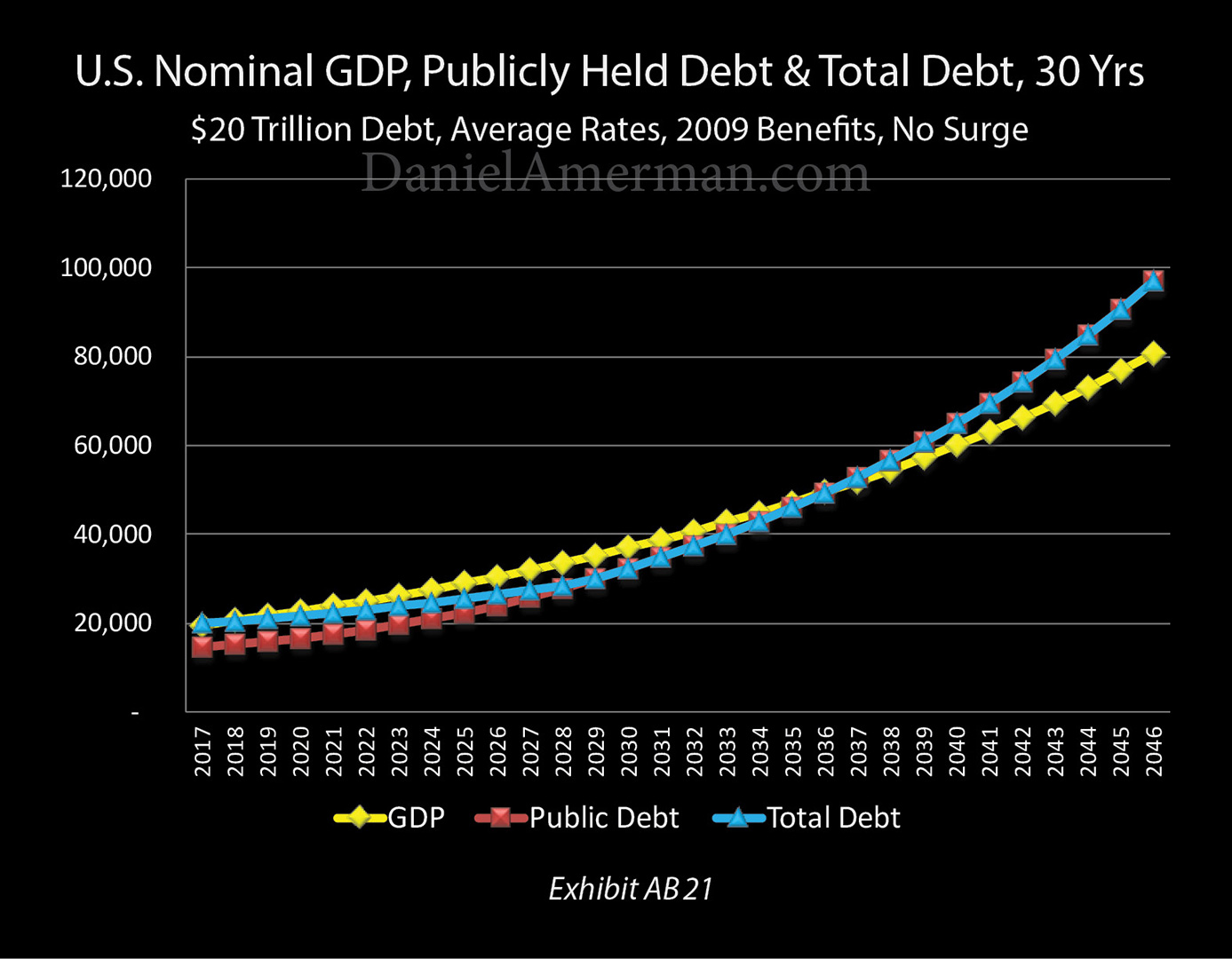

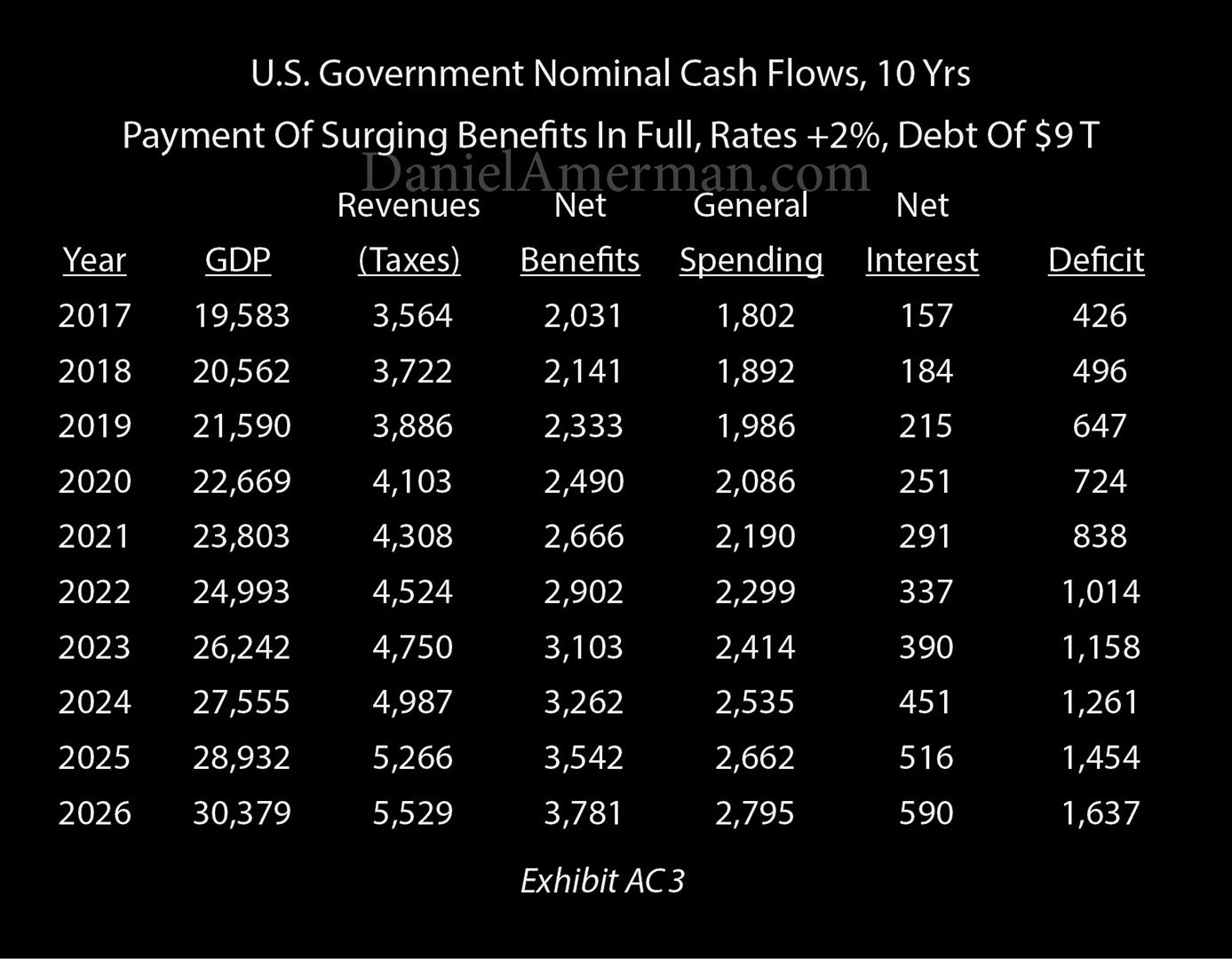

When you look at these, the key column is net interest which is exploding upwards. It doesn’t happen instantly because the weighted average life of the debt outstanding is 5.8 years, so it takes a number of years for it to actually reflect in the interest payments going out. What would happen is that we’d still have this surge in the deficit that’s going up almost dollar for dollar with the net interest payments. If you look at the overall impact on the economy and total governmental debt, what economists usually do is compare the size of the government debt to the economy, and you can see that the debt crosses the size of the economy by the mid 2030s and accelerates from there.

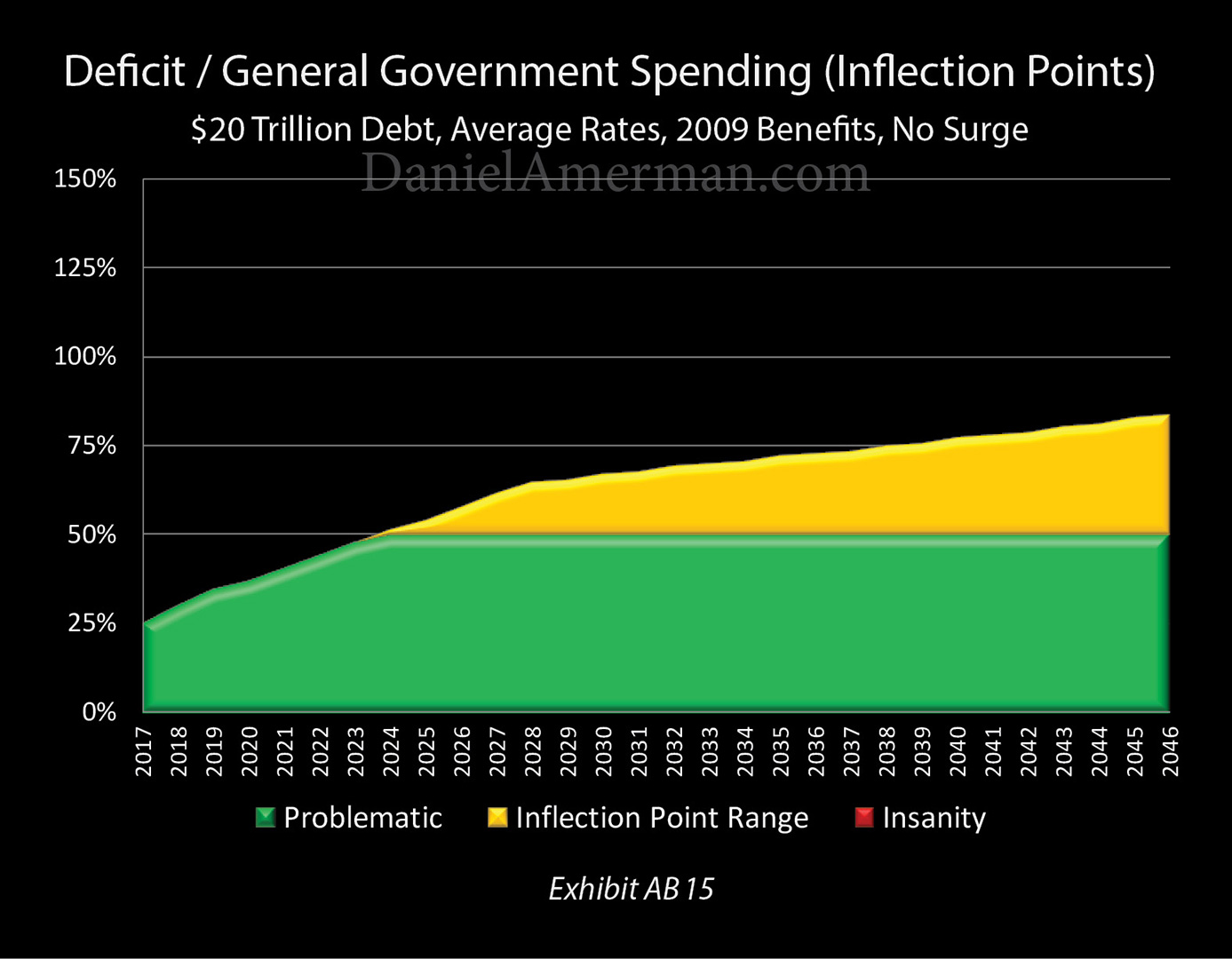

BENCHMARK OF “INSANITY”

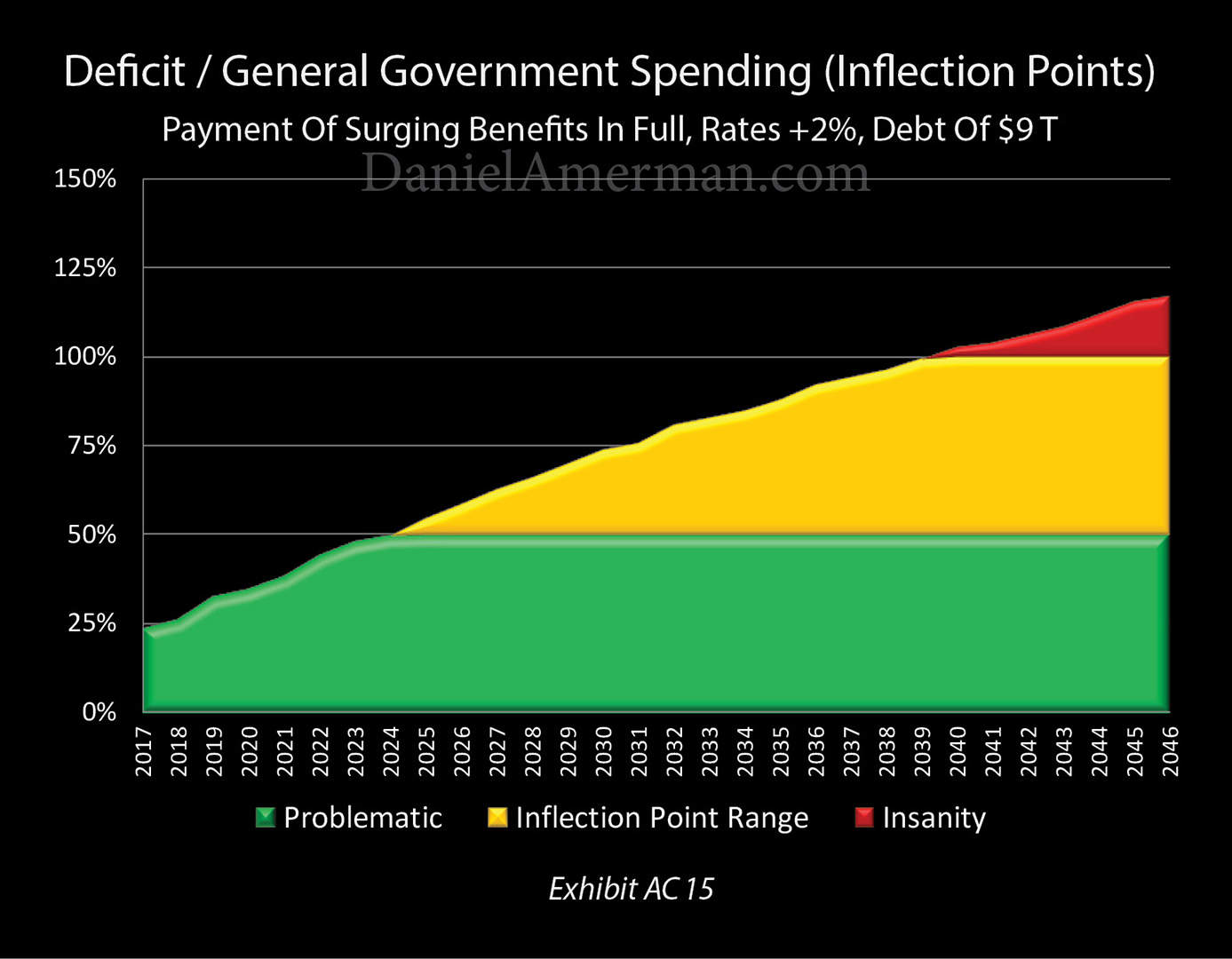

We define insanity as if benefits and interest payments consumes all government taxes and every other dollar of government spending has to be borrowed. By the 2020s, we’re more than halfway there, and in that dangerous yellow zone that could shift at any time.

From AC3, with benefits being paid in full, the net interest column has been negated. But now the problem is in the net benefits column, where the deficit is shooting up out of control again. You can see how the red line is pulling the yellow line up step by step, and by the time it reaches 2039 the annual deficit exceeds all normal governmental spending.

We have two entirely independent compelling major financially problems out there. There’s the $20T debt being held in check by some the lowest interest rates in history, and we also have the tremendous increase in social security and medicare payments that’s going to hit soon. The problem is that in reality, we have both of these hitting us at the same time.

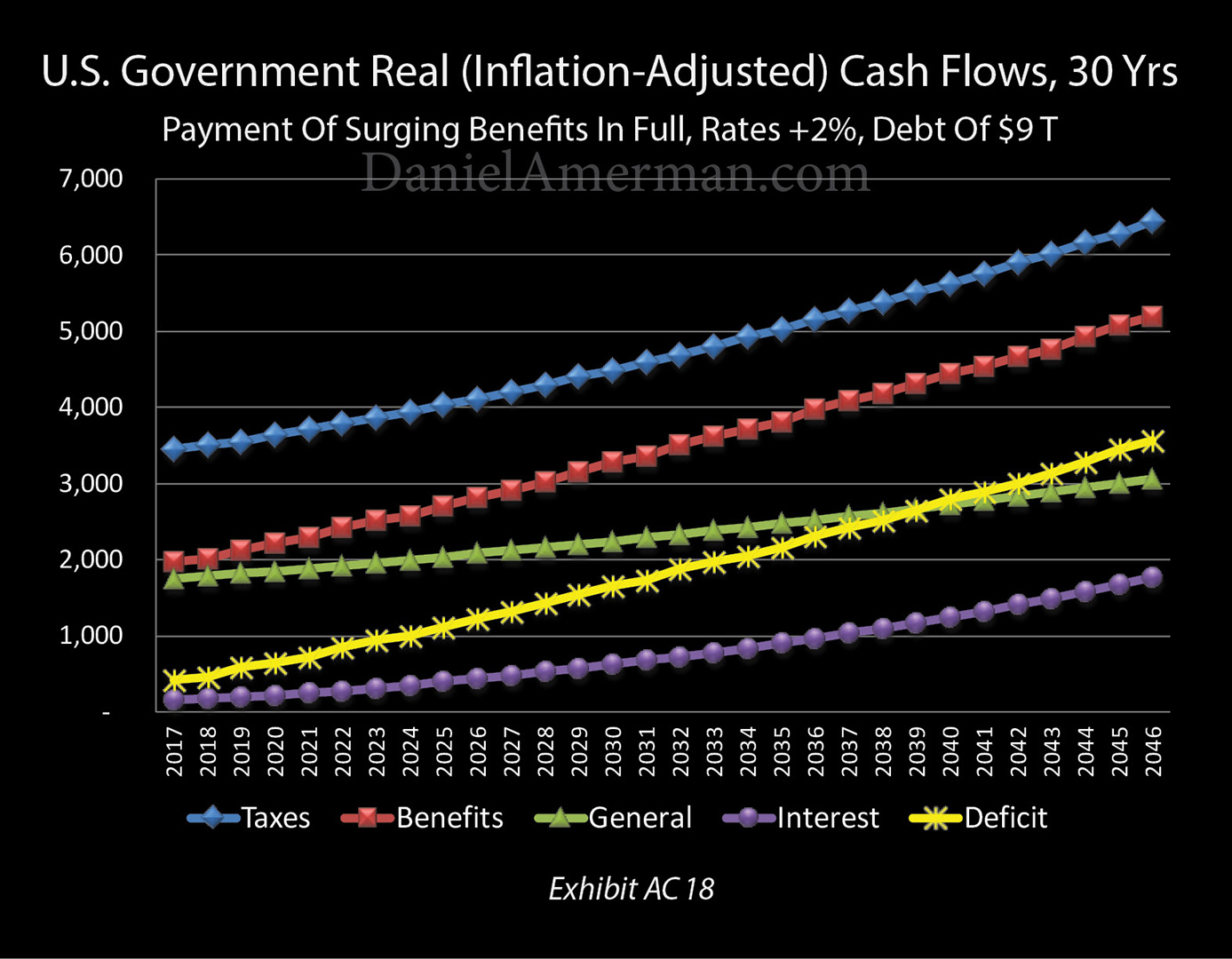

AD3 shows what would happen if we return to historically accurate interest rates. It takes some time for it to be reflected, but we still go from $400B in net interest payments to almost $2T at the same time that we have net benefits almost doubling. When those two hit together, it’s like we have two exponential series hitting each other simultaneously and reinforcing it. If you look at AD15, you see that we’re in the insanity range in under ten years. The future national debt, the future social security and medicare, and the future interest rates are all intertwined.

GOVERNMENT REACTION

The point is not to say these scenarios will happen, the point is that this will happen if we had normality in the same way most people are building their assumptions when it comes to long term retirement planning. People are expecting to get their benefits in full because that’s what the government has assured them. They’re looking for long term historical returns in terms of investment allocations, and the point is that if everyone’s expectations were met simultaneously, then the country’s very quickly in the insanity range.

Even with 2% economic growth rate, you can stay in the green the entire time. You can do that with interest rates, you can do that with benefits, you can do that prioritizing interest rates over benefits, you can do it prioritizing benefit changes over interest rates, you can do it with tax changes, and you can do it with inflation. All of these are valid ways of staying within the range.

If you look at paying everything with taxes, the degree taxes would have to rise is shocking. This would be very difficult politically to do. Part of the appeal of financial repression to the government is that there is virtually no political cost to this. People pay personal cost in their lives, but this is generally not understood by the voters. Some of the methodologies of staying in the green are far more politically palatable than others, so we’re more likely to see those used and those are the ones where individuals need to have their defenses in place for. Every single one of these possibilities for staying in the zone has very broad effects on all investment categories.

Much depends on the specific methods being used and the exact approach the government takes. Bonds in general are not a good idea during financial repression, though there are some time periods where they could be a good investment for a period of time. Real estate, gold, silver, and things like that are good investments.

There is very much a direct personal cost for savers, and working in a different way but related, a direct personal cost for beneficiaries.

CLOSING REMARKS

Social security is not fully inflation indexed. Most people have their medicare premiums deducted from their social security payments, and there is a provision called hold harmless which allows the government to strip away all inflation indexing to the extent that medicare premiums are increasing. Often times when people look at things at this, they take a high drama approach.

All it takes is a tweak of a half percent here and next thing you know these seemingly huge problems have gone away. But when you follow through to the impact on individual savers and individual beneficiaries, they are in fact being paid in full. If you’re going to make a $100T problem go away, $100T in pain has to be shifted somewhere. It happens, but not in a way where people can say, this is happening to me right now because this change was made here.

Abstract by: Annie Zhou <a2zhou@ryerson.ca>

LINK HERE to get the podcast in MP3