11/20/2015 - Robert Wenzel – The Fed Flunks! My Austrian Economic Speech at the NY Federal Reserve

11/20/2015 - Robert Wenzel – The Fed Flunks! My Austrian Economic Speech at the NY Federal Reserve

Special Guest: Robert Wenzel – Editor & Publisher of Economic Policy Journal.com & Target Liberty

Investing based on The Austrian school of Economics

FRA Interview of Robert Wenzel by FRA Co-founder Gordon T Long.

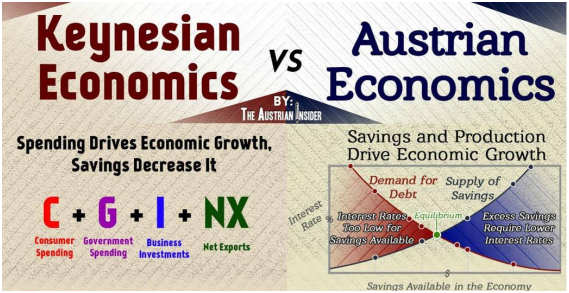

Across well-known literature, the Austrian school of economics has earned and put its indelible mark on the complicated world of economic analysis and theory. The school of thought varies significantly from the mainstream schools of economics like the classical, neoclassical and Keynesian schools of thought. In essence the Austrian school of thought believes in using logical thoughts to explain and solve economic problems rather than getting technical and going into mathematics to explain the same problems.

“The key to understanding is that what you have with mainstream economists is that they look at things from a very mathematical, very empirical approach… unlike in physical sciences you cannot do that for the science of economics because you’re dealing so many variables like changes and desires”

Unlike the mainstream none-Austrian economists, Wenzel believes that there’s a lot to be understood from the economy based on logical build up from solid premises. He goes on to mention that another key aspect to be understood is that Austrian economists believe that when the Fed injects money into certain sectors of the economy, it’s those sectors that turn to boom. According to Wenzel, when the Feds eventually start tightening this money supply it leads to a crash.

On the current economy:

“We’re in a period of accelerated money supply”

Wenzel thinks there could be an increase in price inflation and the possibility of another dip in the price of oil.

Explaining how we have inflation in some areas and deflation in others when we’ve been pumping money into the system, he explains it by outlining how it depends on how quickly people want to spend the money.

“if there’s a great desire to hold money, you’re not going to see the inflation right away”

When people don’t spend money what happens is you have money building up in cash balances which Wenzel terms “the desire to hold cash balances”. With this you see people reluctant to spend money and hence a low velocity of money.

On the confusing environment of economics and how understanding the Austrian school can help to clear things up …. Understanding the business cycle and inflation comes about in terms of the Austrian school of thought. It definitely helps to clear a lot of things up but even more can be taken from this approach. The methodology additionally helps out in terms of having people analyzing the world through logic rather than attacking it solely with empirical data.

On considering Quantitative easing and going into negative nominal rates …. QE is a method where the fed prints a lot of money and buys long durtion debt. The negative nominal rates idea is based on the Keynesian idea that it’s spending that helps the economy to grow, so the idea is to use negative rates to pressure people to spend their money. Wenzel calls this “a tax on holding money”.

Asked if he sees Hyperinflation in the future:

It could happen at some point. The Fed’s target of 2% could easily go up to three 3% with accelerated printing of money. At this point they might raise rates but if the inflation is at 5% and they raise rates from 12bp to 2% that still won’t be able to fight the inflation. However it may be too soon to say hyperinflation.

The business cycle should be understood as a boom and bust cycle.

“Whatever is going up now does not necessarily mean it will go up long term. The bust will occur but they will pump it up with new fed printing, which is eventually where the inflation comes in”

Abstract by Agang Moeng. Can be reached at agang.moeng@ryerson.ca

The infographic above shows some differences in Keynesian and Austrian views. Courtesy of The Austrian Insider.