10/02/2015 - Jeff Davis Talks Financial Repression & the Effects on the US Banking Sector

10/02/2015 - Jeff Davis Talks Financial Repression & the Effects on the US Banking Sector

Special Guest: Jeff Davis – Managing Director, Financial Institutions Group, Mercer Capital

FRA Co-Founder Gordon T. Long interviews Jeff Davis of Mercer Capital, and discusses financial repression and its effects on the banking sector.

Davis is currently a Managing Director of Financial Institutions Group at Mercer Capital. Davis also provides financial advisory services primarily related to the valuation of privately-held equity and debt issued by financial services companies and advisory related to capital structures and M&A.

FINANCIAL REPRESSION’S EFFECT ON THE US BANKING SECTOR

“Financial repression is a price control that relates to all facets of the economy and has profound impact.”

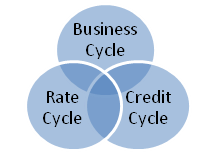

The 3 major cycles: Business Cycle, Credit Cycle and Rate Cycle.

“The banks straddle all 3 to be a key contributor of capital in the US economy. Financial repression impacts at a very base level for all 3 cycles.”

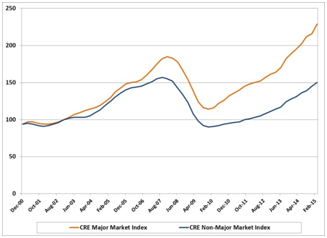

“Financial repression has artificially pumped up asset value.

“Commercial real estate values really pivoted in 2010. There is additional risk in the system now that asset values are pumped up”(See Chart to Left)

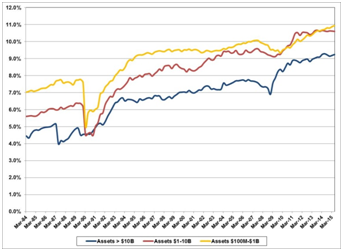

Leverage Ratio

“If you look at the leverage ratio we can see that over the last 20 years the industry has been raising capital. I don’t think that’s a bad thing. We are significantly much better capitalized than Europe which is a good thing, but as it relates to an investor there is a lower return on equity.”(See Chart to Left)

“Regarding financial repression, if you think about interest rates today, it is very painful for an institution to hold cash. There is significant risk taking occurring amongst commercial banks in taking additional credit risk and duration risk. Structurally banks aren’t as spread in terms of their assets relative to their borrowings that fund these assets.”

“Companies don’t go broke because they don’t make money. Companies go broke when they have no liquidity, so what financial repression has done is push liquidity into the system. So now heavily indebted companies are able to borrow money and we will soon see the consequences of that.”

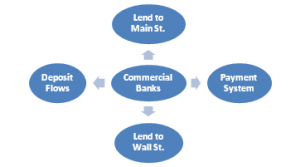

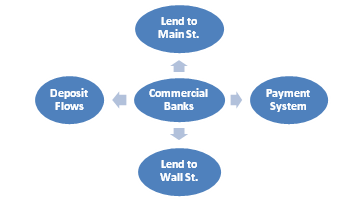

HOW BANKS FUNCTION

“The banks are special for being separated from commerce.”

“The objective for a bank is to earn a spread on assets. Loans being the highest yielding asset, followed by bonds, and finally cash. The banks role is to take the deposits and prudently while still taking risk, lend the money into the economy to help finance the economy.”

SHADOW BANKING

“Over the last several decades the shadow banking system has developed into an alternative lender as well as another place for people to put their money.”

The term “shadow bank” was coined by economist Paul McCulley in a 2007 speech at the annual financial symposium hosted by the Kansas City Federal Reserve Bank in Jackson Hole, Wyoming. In McCulley’s talk, shadow banking referred mainly to nonbank financial institutions that engaged in what economists call maturity transformation.

Commercial banks engage in maturity transformation when they use deposits, which are normally short term, to fund loans that are longer term. Shadow banks do something similar.

“Shadow banking system is separate from commercial banking system, but is a very large piece of the credit allocator. A lot of risk has been pushed out of commercial banks and is now in the shadow banking system, where it is not as opaque as a commercial bank.”

CONCERNS WITH SUSTAINED LOW INTEREST RATES

One day there will be a reckoning. It’s simply a buildup of risk; an attempt by central authorities to guide the economy.

Malinvestment: A mistaken investment in wrong lines of production, which inevitably lead to wasted capital and economic losses, subsequently requiring the reallocation of resources to more productive uses.

“A delay of lost recognition and mass malinvestment which is all a credit risk within the banking systems. However, my biggest concern is a dramatic slowdown in the economy, short rates at zero.”

Abstract written by Karan Singh karan1.singh@ryerson.ca

Commercial Real Estate Values

{kind=link}