10/04/2014 - FED POLICY ADOPTION Macro Prudential Policy (Financial Repression) to be Yellen’s PRIMARY TOOL

10/04/2014 - FED POLICY ADOPTION Macro Prudential Policy (Financial Repression) to be Yellen’s PRIMARY TOOL

In July, Janet Yellen remarked about what seems to be her preferred choice, a topic that has been central to her Chair.

.. efforts to promote financial stability through adjustments in interest rates would increase the volatility of inflation and employment. As a result, I believe a macroprudential approach to supervision and regulation needs to play the primary role.

We are, as Yellen proclaims, in the capable hands of regulators and their “macroprudential” systems and arcana:

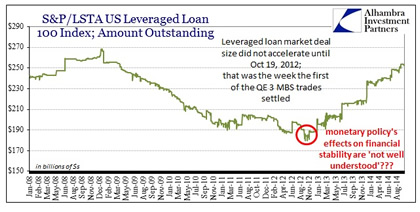

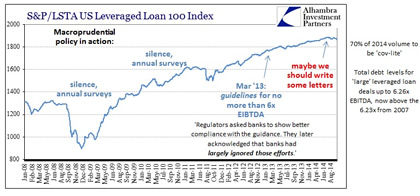

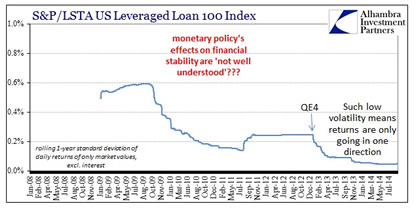

The Federal Reserve is stepping up its oversight of high-risk leveraged loans, shifting to a deal-by-deal review after its previous industry-wide guidelines were largely ignored by banks.

Truer words have never been written, as if you were observing the leveraged loan market from afar with little prior experience you would come to the conclusion that there was no such thing as “guidelines” in leveraged loans.

Until now, supervisors collected loan data in an annual survey, and last year told banks they needed better adherence to standards they put forth in guidelines in March 2013. Over the past several weeks, they have shifted tactics and are examining loans as they are made, showing a new urgency in avoiding the kind of overly risky lending that was blamed for igniting the financial crisis.

To sum up: the leverage lending market had prior guidelines that were supervised (using that term loosely) via an annual loan survey leading to a surge in the kind of “overly risky lending” usually reserved for the bitter ends of cycle peaks; and now, long after all that behavior has been entrenched and hundreds of billions of loans made, macroprudential policy wishes to step up regulatory pressure.