08/09/2014 - THE GOVERNMENT’S GAME OF “ENTRAPMENT” via FINANCIAL REPRESSION

08/09/2014 - THE GOVERNMENT’S GAME OF “ENTRAPMENT” via FINANCIAL REPRESSION

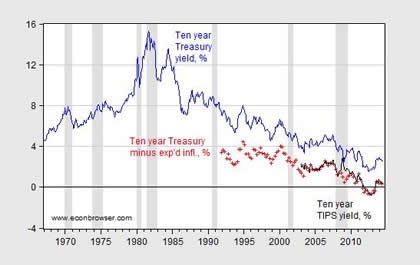

FINANCIAL REPRESSION

Initially Forced Fund Managers Into

Junk Bond Yields

THE SET-UP

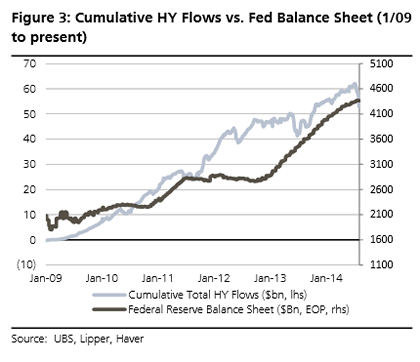

STEP 1: EXCESSIVE LIQUIDITY

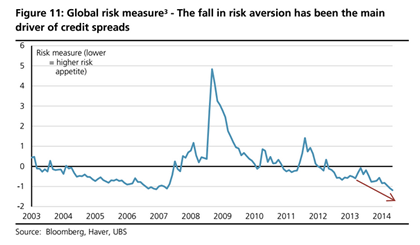

STEP 2: EXCESSIVE RISK TAKING

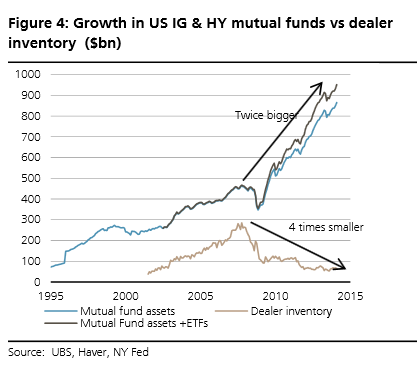

STEP 3: BAD MONEY FORCES OUT GOOD MONEY

NOW THE SQUEEZE

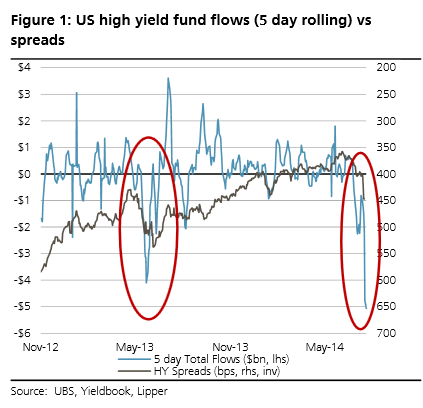

STEP 4: THE PANIC

THE FLIGHT TO PERCEIVED SAFETY

STEP 5: ACHIEVE GOAL -> CHEAPER GOVERNMENT FINANCING COSTS

“Wolf Richter’s essay posted on Stockman’s Contra Corner sees junk bond investors running for the hills, “But there no hills” .. In the latest week, investors yanked $7.1 billion out of junk bond funds, a record amount, according to Lipper – this exodus has been going on since early July, junk bond prices have dropped, yields have jumped from all-time lows, yield spreads have suddenly widened .. “After having been inflated to dizzying proportions, the junk-bond bubble has been pricked. And the hot air is hissing out of it .. Neither glorious economic fundamentals nor corporate financial engineering caused investors to pile helter-skelter, eyes-closed into this high-yield junk. The Fed’s financial repression did .. The Fed has made it impossible for yield investors to earn a noticeable return above the rate of inflation with low-risk paper. So they chased after whatever yield they could get and they held their noses and ventured deeper and deeper into a swamp they normally wouldn’t want to be in. They did that in unison. The demand they created for junk drove up valuations and repressed yields further into low-yield purgatory, where potential losses are huge and potential gains very meager. Exactly as the Fed had wanted them to .. But the Fed has changed its mind”CliffKule.com